Relevant • Independent • Objecve Currently, most natural gas trade in Asia is via liquefied natural gas (LNG) due to limited pipeline infrastructure, but China and India, the emerging natural gas giants, also have access to inland gas resources, primarily from Russia and the various Central Asian Republics (CAR). The rapid increase in Asian demand, combined with slow economic recovery in Europe, has led gas rich Russia, and the CARs to look at exporng their gas to the Asia Pacific. Subsequently, there have been several interregional pipeline projects that have been proposed. Table 1 summarizes some of these projects. If all of these pipeline projects went forward, the potenal for LNG imports into China and India would be severely diminished. However, a majority of pipeline projects have become stalled due to disagreements on gas price negoaons, or from various geopolical tensions. This is parcularly true between China and Russia where China has refused to sign a long-term oil- linked contract for the Altai pipeline that would put pipeline prices close to LNG prices. Regardless of its disputes with Russia, China has been able to secure over 6 BCFPD of gas from various CARs. For example, it has been willing to pay the tariff charges between $10-$13/ MMBTU for Turkmenistan gas because they allowed China equity in upstream gas producon. 4 Lastly, it is important to remember that China has onshore shale gas reserves of 134.4 tcm (4.7 x 10 3 TCF), of which it hopes to produce approximately 0.6 BCFPD from these shale gas reserves by 2015. 5 It has been quesoned whether Russia has missed the opportunity to enter the Asia Pacific market. Most of Russia’s proposed interregional pipeline projects to Asia have not gone forward. China is explained in the preceding paragraph, but Japan and Russia have failed to come to an agreement due to an unresolved territorial dispute over the Kuril Islands. 6 South Korea has also had difficules accessing Russian natural gas as an offshore pipeline is uneconomic, and an onshore pipeline will need to go through North Korea, which would create either the risk of a substanal tariff to North Korea, or the risk of North Korea cung off gas supplies to South Korea. Despite the difficules of seng up onshore pipelines, Russia has commied itself to building LNG December 2013 CERI Commodity Report — Natural Gas Interregional Natural Gas Pipelines in Asia: An Alternave to LNG Zoey Walden Asia-Pacific is expected to become a rapidly growing hub for natural gas consumpon. China is ancipated to be the largest consumer with the Naonal Development and Reform Commiee (NDRC) projecng in their 12 th Five Year Plan a substanal increase in natural gas consumpon at a rate of ~1.9 billion cubic feet per day (BCFPD) to reach 22 BCFPD by 2015, and increasing even further to 36 BCFPD by 2020. 1 The NDRC foresees that between 7-9 BCFPD would need to be imported by 2015 with domesc producon supplying the remainder. 2 Yet, China is only a fracon of the upcoming Asian market with total Asian demand potenally reaching 89 BCFPD for the year 2020. 3 Figure 1 depicts the projected Asian demand as determined by the IEA World Energy Outlook for 2011. Figure 1: Forecasted Asian Demand Source: IEA, CERI 0 20 40 60 80 100 120 140 160 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 BCFPD Rest of Non-OECD Asia India China Rest of Asia Oceania South Korea Japan CERI Commodity Report – Natural Gas Editor-in-Chief: Dinara Millington ([email protected]) Contents Featured Arcle ................................................................................. 1 Natural Gas Prices.............................................................................. 4 Weather ............................................................................................ 6 Consumpon and Producon............................................................. 8 Transportaon................................................................................... 10 Storage .............................................................................................. 12 Liquefied Natural Gas ........................................................................ 15 Drilling Acvity .................................................................................. 17

Transcript

Relevant • Independent • Objective

Currently, most natural gas trade in Asia is via liquefied natural gas (LNG) due to limited pipeline infrastructure, but China and India, the emerging natural gas giants, also have access to inland gas resources, primarily from Russia and the various Central Asian Republics (CAR). The rapid increase in Asian demand, combined with slow economic recovery in Europe, has led gas rich Russia, and the CARs to look at exporting their gas to the Asia Pacific. Subsequently, there have been several interregional pipeline projects that have been proposed. Table 1 summarizes some of these projects. If all of these pipeline projects went forward, the potential for LNG imports into China and India would be severely diminished. However, a majority of pipeline projects have become stalled due to disagreements on gas price negotiations, or from various geopolitical tensions. This is particularly true between China and Russia where China has refused to sign a long-term oil-linked contract for the Altai pipeline that would put pipeline prices close to LNG prices. Regardless of its disputes with Russia, China has been able to secure over 6 BCFPD of gas from various CARs. For example, it has been willing to pay the tariff charges between $10-$13/MMBTU for Turkmenistan gas because they allowed China equity in upstream gas production.4 Lastly, it is important to remember that China has onshore shale gas reserves of 134.4 tcm (4.7 x 103 TCF), of which it hopes to produce approximately 0.6 BCFPD from these shale gas reserves by 2015.5 It has been questioned whether Russia has missed the opportunity to enter the Asia Pacific market. Most of Russia’s proposed interregional pipeline projects to Asia have not gone forward. China is explained in the preceding paragraph, but Japan and Russia have failed to come to an agreement due to an unresolved territorial dispute over the Kuril Islands.6 South Korea has also had difficulties accessing Russian natural gas as an offshore pipeline is uneconomic, and an onshore pipeline will need to go through North Korea, which would create either the risk of a substantial tariff to North Korea, or the risk of North Korea cutting off gas supplies to South Korea. Despite the difficulties of setting up onshore pipelines, Russia has committed itself to building LNG

December 2013

CERI Commodity Report — Natural Gas

Interregional Natural Gas Pipelines in Asia: An Alternative to LNG Zoey Walden Asia-Pacific is expected to become a rapidly growing hub for natural gas consumption. China is anticipated to be the largest consumer with the National Development and Reform Committee (NDRC) projecting in their 12th Five Year Plan a substantial increase in natural gas consumption at a rate of ~1.9 billion cubic feet per day (BCFPD) to reach 22 BCFPD by 2015, and increasing even further to 36 BCFPD by 2020.1 The NDRC foresees that between 7-9 BCFPD would need to be imported by 2015 with domestic production supplying the remainder.2 Yet, China is only a fraction of the upcoming Asian market with total Asian demand potentially reaching 89 BCFPD for the year 2020.3 Figure 1 depicts the projected Asian demand as determined by the IEA World Energy Outlook for 2011. Figure 1: Forecasted Asian Demand

Source: IEA, CERI

0

20

40

60

80

100

120

140

160

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29

20

31

20

33

20

35

BC

FPD

Rest of Non-OECD Asia

India

China

Rest of Asia Oceania

South Korea

Japan

CERI Commodity Report – Natural Gas Editor-in-Chief: Dinara Millington ([email protected]) Contents Featured Article ................................................................................. 1 Natural Gas Prices.............................................................................. 4 Weather ............................................................................................ 6 Consumption and Production............................................................. 8 Transportation................................................................................... 10 Storage .............................................................................................. 12 Liquefied Natural Gas ........................................................................ 15 Drilling Activity .................................................................................. 17

CERI Commodity Report - Natural Gas

Page 2

Project Capacity (BCFPD) Start Date

Myanmar

Myanmar-China Pipeline ~1 2013 (Operational)

Russia

Altai Pipeline ~2.9 2015+

Sakhalin-Khabarovsk-Vladivostok (SKV)Pipeline

~0.6 2011 (Operational)

SKV Expansion ~2.9 (combined cap.) 2020

Power of Siberia Gas Transmission Project (PSGTP)

~5.9 with ~3.7 to China 2017

Russia-Japan Pipeline ~1.5-1.9 Unknown

South Korea Natural Gas Project ~1 2017+

Central Asian Republics (CAR)

Central-Asia China Gas Pipeline (CACGP) Lines A & B

~2.9 2011 (Operational)

CACGP Line C ~2.4 2014 reach full cap Dec. 2015

CACGP “Line D” ~0.5 2016

CACGP “Line D” ~1.9 (total Line D) 2020

Turkmenistan-Afghanistan-Pakistan-India (TAPI)

~2.6 2017+

Iran

Iran-Pakistan-India Pipeline ~3 Unknown

Source: Various sources

Table 1: Interregional Pipeline Projects to Asia

Figure 2: Russia’s Transmission Network

Source: Gazprom7

Relevant • Independent • Objective

Page 3

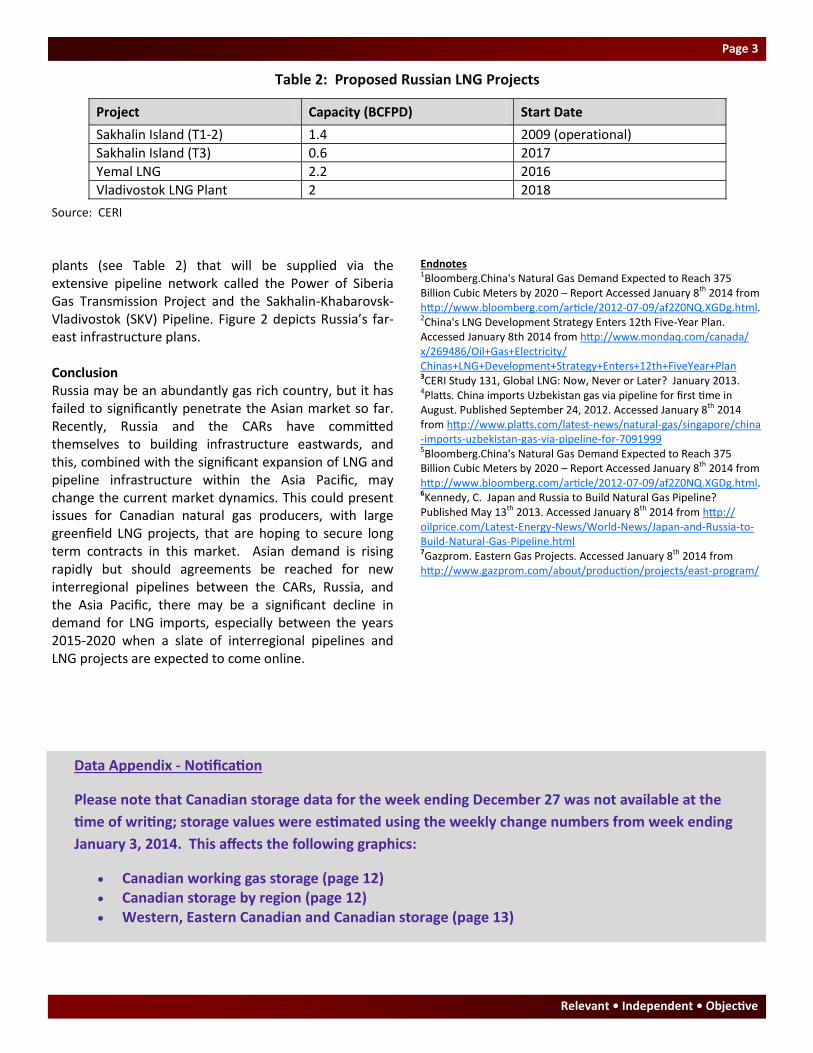

plants (see Table 2) that will be supplied via the extensive pipeline network called the Power of Siberia Gas Transmission Project and the Sakhalin-Khabarovsk-Vladivostok (SKV) Pipeline. Figure 2 depicts Russia’s far-east infrastructure plans. Conclusion Russia may be an abundantly gas rich country, but it has failed to significantly penetrate the Asian market so far. Recently, Russia and the CARs have committed themselves to building infrastructure eastwards, and this, combined with the significant expansion of LNG and pipeline infrastructure within the Asia Pacific, may change the current market dynamics. This could present issues for Canadian natural gas producers, with large greenfield LNG projects, that are hoping to secure long term contracts in this market. Asian demand is rising rapidly but should agreements be reached for new interregional pipelines between the CARs, Russia, and the Asia Pacific, there may be a significant decline in demand for LNG imports, especially between the years 2015-2020 when a slate of interregional pipelines and LNG projects are expected to come online.

Endnotes 1Bloomberg.China's Natural Gas Demand Expected to Reach 375 Billion Cubic Meters by 2020 – Report Accessed January 8th 2014 from http://www.bloomberg.com/article/2012-07-09/af2Z0NQ.XGDg.html. 2China's LNG Development Strategy Enters 12th Five-Year Plan. Accessed January 8th 2014 from http://www.mondaq.com/canada/x/269486/Oil+Gas+Electricity/Chinas+LNG+Development+Strategy+Enters+12th+FiveYear+Plan 3CERI Study 131, Global LNG: Now, Never or Later? January 2013. 4Platts. China imports Uzbekistan gas via pipeline for first time in August. Published September 24, 2012. Accessed January 8th 2014 from http://www.platts.com/latest-news/natural-gas/singapore/china-imports-uzbekistan-gas-via-pipeline-for-7091999 5Bloomberg.China's Natural Gas Demand Expected to Reach 375 Billion Cubic Meters by 2020 – Report Accessed January 8th 2014 from http://www.bloomberg.com/article/2012-07-09/af2Z0NQ.XGDg.html. 6Kennedy, C. Japan and Russia to Build Natural Gas Pipeline? Published May 13th 2013. Accessed January 8th 2014 from http://oilprice.com/Latest-Energy-News/World-News/Japan-and-Russia-to-Build-Natural-Gas-Pipeline.html 7Gazprom. Eastern Gas Projects. Accessed January 8th 2014 from http://www.gazprom.com/about/production/projects/east-program/

Project Capacity (BCFPD) Start Date

Sakhalin Island (T1-2) 1.4 2009 (operational)

Sakhalin Island (T3) 0.6 2017

Yemal LNG 2.2 2016

Vladivostok LNG Plant 2 2018

Table 2: Proposed Russian LNG Projects

Source: CERI

Data Appendix - Notification

Please note that Canadian storage data for the week ending December 27 was not available at the

time of writing; storage values were estimated using the weekly change numbers from week ending

January 3, 2014. This affects the following graphics:

Canadian working gas storage (page 12) Canadian storage by region (page 12) Western, Eastern Canadian and Canadian storage (page 13)