Corso di Laurea In Economics and Management Tesi di Laurea Italian IT startup migration from Italian ecosystem to the new Berlin startup hub Relatore Prof. Paolo Pellizzari Laureando Matteo Luca Baiamonte Matricola 832318 Anno Accademico 2013/2014

Transcript

Corso di Laurea In Economics and Management

Tesi di Laurea

Italian IT startup migration from Italian ecosystem to the new Berlin startup hub

“It's not about ideas. It's about making ideas happens”Scott Belsky, Behance Co-founder

The aim of this paper is to analyse the phenomena of migration of start-ups in the Information

technology sector and of entrepreneurs from Italy to Berlin start-up hub.

Startups have been a subject of many researches and papers, due to their importance in job creation

and innovation progress; this importance is also enhanced by the overall Worldwide economy, in

which jobs creation process is fundamental.

However, the high mortality of startup businesses in IT sectors, mainly for the uncertain and

unverified business model and for the turbulent situation of the economy Worldwide, forces

entrepreneurs to move towards better environments, in which key factors of growth are more

developed.

Keeping in mind that Europe overall is struggling to reach the level of competitiveness of U.S start-

up hubs, leaded by Silicon Valley, I will focus on this paper on startups and startuppers migrating

from Italy to Berlin start-up hub, that in the recent years gained more importance and international

interest, becoming one of the most important startup centres In Europe, with London and Paris.

Using Berlin as benchmark for evaluating the Italian landscape for startups, it will be possible to

answerer questions such as “In which way Italy can improve in order to match Berlin landscape?”

and “In which way Italy and Public Authorities can create clusters of innovation renoned at an

international level?”.

The methodology I used for this paper starts with the comparison of Italian and Berlin landscapes

trough the analysis of some key factors determinant for the growth of the startup in order to get the

first quantitative and qualitative results. The next step of the method is carried out by a survey on

the Italian community of digital entrepreneurs in Berlin “DigItaly”; through the questionnaire, it has

been possible to collect direct feedbacks not only about the key factors of both environments but

also on the main reasons why of their migration.

IV

CHAPTER ONE

The startup phenomena

1.1 Definition of startup

The main purpose of this research is to analyse the issues at the basis of the migration of IT

start-ups from Italy to Germany; in particular, Berlin, location of a high growing startup

environment

The word “startup” has become mainstream and very famous since the dot.com boom in the

end of the 90’s and the beginning of the 2000s with the dot.com bubble1

It is important, first, to give a definition of a start-up since the common knowledge considers a

startup only a business merely related to the high technology sector and at its initial phase only

(examples can be: web platforms or e-commerce businesses or mobile applications). According to

the definition of Eric Ries, a startup is a “a human institution designed to create a new product or

service under conditions of extreme uncertainty”2. This is a very broad definition, in which no

business model is specified, so that even a new way of serving ice cream, a no-profit organizations

or a project inside well-established companies may fall within the realm of this definition. The

definition of startups of Eric Ries also highlights the fundamental features of a product such as the

values offered to the customers, the novelty and innovation related to the product. Few examples of

successful startups can be:

Airbnb, a website for people seeking a temporary accommodation all over the world.

Founded by Brian Chesky, Joe Gebbia and Nathan Blecharczyk in 2008, the website

“pioneered the market of community consumption and peer-to-peer accommodation

1 The “dot com bubble” was a phenomenon – occurring at the beginning of the year 2000 – when, due to the increasing enthusiasm surrounding the web revolution, the stock prices of internet companies publicly traded reached remarkable peaks also encouraged by the those banks encouraging such investments. Given the fact that many of those companies did not have any sustainable business model, they ended up in bankruptcy and the burst bubble led the stock prices at an incredbly lower value. (Zhu Wang, “Technological Innovation and Market Turbulence: The Dot-com Experience”, 2006, pp1-5)2 Eric Ries, “The lean Startup”, Crown Pub, 2011

5

rentals”3. Even though the fierce competition that is facing day after day, Airbnb raised a

considerable financial capital of $119.8m, and it has a wide range of active users, more than

10 million people, over 26,000 cities in 192 countries4.

Tetrasun, is a startup that promoted a new technology for photovoltaic systems able to save

up until 21% energy at a low cost rate thanks to an innovative silicon architecture. The

startup ended its life in 2013, when it was acquired by First Solar, one of the main

worldwide photovoltaic company.

The leitmotif of a startup is “innovation”; namely, the fact of having a new idea and being able

to develop it. However, innovation also embodies a large set of improvements based on added

values to the final users, while giving the developers an advantage necessary to emerge between

other start-ups and compete within an evolving market. The survival of a startup, is therefore based

on its ability to be flexible and able to adapt to the changing environment of the markets and the

taste of customers.

The pathway of entrepreneurs that want to create a start-up has been described as “the hero’s

journey”5, an expression that emphasizes the fact that nothing is sure during the initial phase: not

just in terms of surviving, but also in terms of growth. Due to the uncertainty related to the success

of a startup, it is necessary to identify a rational approach towards two main topics:

entrepreneurship and durable growth. With regard to durable growth, in particular, it is necessary to

highlight that, together with variables that are within the startup itself and related to management

techniques, the context where the startup develops plays a fundamental role.

1.2 The life-cycle and growth milestones of the start-up

Increasing opportunities and reduction of costs, mainly due to the possibility to outsource

some key activities, lead the IT sector to be characterized by a huge competition between startups,

Competition is even worse especially for the web and mobile based platforms, in which start-ups

have to compete globally with each other. For this reason, it is important to emerge as a leader in

3 http://www.econ.ucla.edu/sboard/teaching/tech/Airbnb.pdf4 "Airbnb Fact Sheet, http://assets.airbnb.com/press/press-releases/Airbnb%20Fact%20Sheet_en.pdf5 Steve G.Blank, “The four steps to epiphany”, K&S Ranch, 2007, iiii

6

the market segment in which the start-up operates.

Due to competition in contending scarce resources, both financial and human capital, start-ups are

forced to use different management techniques than the usually employed by traditional enterprises;

in addition, startups need at each phase of their life-cycle a startup-frendly environment, that gives

the possibility to startups pursue a sustainable growth. For this reason, the entrepreneurs are forced

to reach as soon as possible better environments in order to differentiate their startup business from

the competitors.

The main growth milestones, needed in order to create an innovative product/service able

tosatisfycustomers,are:

Figure 1: Growth phases of a start-up, Source: “The four steps to epiphay”, Steve G. Blank

Problem solution fit is the “first step to understand if the product is something worth

doing”6, understanding if the needs that the start-up wants to satisfy are really crucial to

customers.

Product/market fit means “being in a good market with a product that can satisfy that

market”7; it is the most important milestone of the growth process, in which the final

product developed by the start-up has found a good position in the market niche with a great

reaction by customers

Scale phase, In which the start-up is seeking expansion, both in customer pool both trying to

serve new customer segments

In the next paragraphs, I will analyse more precisely each growth phase, highlighting the new

management techniques used as well as the needs of start-ups from the external environment, that

are critical for the overall growth process.

6 “Running lean”, Ash Maruya, pag 21, 20107 Marc Andreessen’s blog, Pmarca Guide to Startups

7

1.2.1 The Concept Phase

To reach the first milestone, the Problem/solution fit, it is useful for a start-up to follow a process

called Customer Discovery 8, aimed at confirm the initial vision about the possible market and

customers for the product; it consists of Interviews and contacts with possible early customers,

focusing only on a small market segment, in order to understand if:

They are aware of the problem that we want to solve

The problem is enough important for them in order to set up a business and if they are aware

of the problem

They would pay for that problem to be solved

They are looking a solution in the market for that problem

If the result, after those interviews, is that there are enough people with those characteristics, the

start-up has just found the most important source of learning: early visionary or enthusiastic

customers, also called by Steve G. Blank “earlyvangelists” to emphasize their role in developing the

product and in spreading the start-up vision.

However, even in this initial phase, the start-up benefits from a start-up friendly environment; in

fact, it is fundamental, at this phase, to belong to an inclusive start-up community, with a start-up

culture inclusive oriented rather than exclusive, in which:

Experienced entrepreneurs, also called serial entrepreneurs, share their experience with

others to collaborate through an informal mentoring process, a birth of a new start-up9

Regardless any background of the entrepreneur, the community of entrepreneurs accepts

incumbents in their networks.10

A necessary condition, not just for achieving the Problem/solution fit, for the creation of a vibrant

start-up community is to operate in a technological lively environment, in which the

implementation of new ideas, successful or not, is incentivized rather than looked with suspect.

This kind of environment, often, can be found near Universities or Research centres; In fact,

universities has always played a key role in fostering start-up communities to take root, and they are

“Feeders that, at minimum, generate a steady steam of new young community into the start-up

8 Steve G. Blank, “the four steps to epiphany”, K&S Ranch, pp 27-339 See supra, pag 14710 Brad Feld, “Startup Communities”.Brad Feld,

8

community” 11.

Famous examples are Stanford university, which in the end of the 50's, namely, “created” the

Silicon Valley, fostering innovative projects; In fact, two Stanford students, Bill Hewlett and David

Packard, founded Hewlett-Packard company, an important company for the development of the IT

sector. Another example of how universities can contribute in the creation of a fervent startup scene

is New York, where thanks to the building, during these years, of a campus, that is technology and

entrepreneurship oriented called ConellNYC Tech, thanks to a joint venture between the Cornell

University and the Technion-Israel Institute of Technology, has made possible for New York to

become the third startup centre in US and the fifth globally in few years.12

However, at this early phase, called concept phase, no funding are required, being the interview

carried out personally by the entrepreneurs.

1.2.2 The early/seed phase

After the Problem/solution fit has been achieved, the continuous learning principle is now

applied to learn what people wants, that is exactly the aim of the most important growth milestone:

the product/Market fit. This can be achieved by using a tool, called the Build-Measure-Learn loop,

in which a minimum valuable product (MVP)13, that can be a working prototype with the main basic

feature or just an image of it, is offered, sometimes it can be sold, to the earlyvangelists, getting

feedbacks directly from them.

Figure 2: The “Build-Measure-Learn loop”; source: Eric Ries, “The lean model”

Every time the loop is completed, through the collection and the measurement of feedbacks, we can

learn useful informations about possible features to include that our target customers perceive as

11 “Startup Communities”.Brad Feld, 12 Maria Teresa Cometto, Alessandro Piol, “Tech and the City”, Angelo Guerini e Associati, 2013, pp-6613 Eric Ries, “The lean Startup”, Crown Pub, 2011, pp 82

9

fundamental.

The aim of this loop process is to understand if our strategy, e.g. our market segment or our

customers profile, is correct, meaning that the entrepreneurs have taken the right path and they can

persevere; if it results to be incorrect, the strategy must be changed or, more precisely, there is the

need of a pivoting.

In this phase of life-cycle, including the seed stage and the startup phase, the presence of a startup-

friendly environment is a greater concern than the previous phase.

In fact, besides the needs of mentoring from other entrepreneur and of a vibrant technological

community, the seed and the startup phases are characterized also by a strong need of fund raising,

especially in computer hardware and computer gaming.

Differently from traditional enterprises, startups, can not depend upon traditional financing, for

example on bank loans, in which the principle called “ belt and suspenders”14 still dominates the

investment decisions. For this reason ,in the seed phase, new informal types of investors play a key

role in the growth process:

Friends and relatives of the entrepreneurs15

Business angels investors

The latter type of investor is a peculiar figure of the startup environment, because they are a high

net worth individual, acting alone or in a formal or informal syndicate, “who invests his or her own

money directly in an unquoted business in which there is no family connection and who, after

making the investment, generally takes an active involvement in the business”16. Very important is

the fact that their time schedule about their exit strategy is very flexible, leaving the pressure of fast

returns on the entrepreneurs.17

They choose in which project to invest following some criteria:

It must be near their residence, in order to increase the direct contact of the angel with

14 The “belt and suspenders” principle is the necessary condition of repaying the debt trough their operative cash flowor tangible assets. (Hardymon, F. and A. Leamon, "Silicon Valley Bank.",Boston: Harvard Business School Publishing,2001)

15 Wilson, K. and F. Silva (2013), “Policies for Seed and Early Stage Finance: Findings from the 2012 OECD Financing Questionnaire”, OECD Science, Technology and Industry Policy Papers, No. 9, OECD Publishing. (http://dx.doi.org/10.1787/5k3xqsf00j33-en)

16 Mason and Harrison, “Business angel investment activity in the financial crisis: UK evidence and policy implications”, Environment and Planning C: Government and Policy, 2008, pag 309

17 Jon Hoyos Iruarrizaga , María Saiz Santos, “The informal investment context: specific issues concerned with business angels”, 2013,, pp 180-183

10

entrepreneurs

It belongs to a sector In which the angel investor is experienced, reducing the information

asymmetry between entrepreneurs and angels

Angels investors are crucial not just for the cash that they supply to startups but also for :

providing knowledge to entrepreneurs, about the know how and the best practices

creating a network between the startup and possible suppliers or possible strategic partners

filling the investments gap between the early stage and the later stage in which more formal

investor invest only at a less risk level.18

Signal the quality of the projects to the market, increasing the probability of getting funding

at later stages.

Even if the number of Business angels (Bas), working independently or in networks (BAN) is

increasing annually at a fast rate, especially in Europe where the BANs increase by 14% in number

annually, and even if the trend of total amount invested shows an increase in volume of investments,

according to the results from the European Business Angels Network (EBAN) survey in 201219,

only 16 startups out of 100 business angels gets financed.20

For this reason, startups can increase the probability of getting financed by Bas in a context in

which business angels are very active, forcing them to migrate towards more developed seed

financing system environment.

Due to the low probability of getting backed by business angels, a startup can not only depend

upon them as the major funding channel; for this reason, new kinds of investment and institutions

emerged, especially in flourishing technological areas:

Type of investment Features Amount invested and phase of

investmentCrowdfunding

platforms21

Through web platform, crowdfunding

platforms employs users as investor for:

Investments mostly in the early

stage of financing cycles

18 See supra, pp 18319 European Business Angels Network (EBAN) 2013 survey (http://www.eban.org/e5-1-billion-market-shows-

european-angels-on-the-rise/#.U-aSXPl_vzt)20 European Busines Angels Network (EBAN) survey, 201321 Oliver Gadja and James Walton, “Review of Crowdfunding for Development Initiatives”, Department for

International Development, 2013 (http://www.europecrowdfunding.org/wpcontent/blogs.dir/12/files/2013/10/EoD_HD061_Jul2013_Review_Crowd

11

Financing the project, using

equity based, loans, reward,

donation or a combination of

them22

Developing the product, making

them choose between different

products or even allowing them

to develop it by themselves

Creating open discussion between

investors for what concerns

possible improvements about the

product

Averages for:

Equity based: 150,000 US $

Loans based: 5,000 US $

Reward based: 5,000 US$,

wth great variation between

some small projects and some

huge financed projects

Combination: it depeds on

the startup project that has to

be financed

Incubators23 Institutions, that can be private or public

owned, aimed at offering to the new

born startup services in exchange of

equity stakes. The services that they

offer are:

Working spaces in their location

Seed Funding from the incubator

itself or through their network of

investors

Mentoring and coaching the

founders

Human resource and legal

Seed stage and startup stage

Funding.pdf)22 Equity based crowdfunding is a model of crowdfunding in which the investors receive equity stakes for their

contributions. Loan based crowdfunding is based upon private loans, where interests will be paid by the startup. Reward based crowdfunding consists in giving incentives and rewards to the investors ; those rewards can be of different types, depending also on the amount invested. The donation crowdfunding model, instead, is used typically by non-profit organizations and social causes, does not bring any financial reward to the investors

23 Centre for Strategy & Evaluation Services (CSES) for the European Commission’s Enterprise DG, “Benchmarkingof the Business Incubators”, 2002,

12

support

Contact with other startups,

creating a flow of knowledge and

networks between entrepreneurs

(network incubators)Accelerators24 Institutions, that can be private or

public, offering a “intensive acceleration

programs” to startup at the seed stage, in

exchange of an equity stake, averaging

between 6% -10%. The accelerator

programs are characterized by:

A high selections of projects and

teams (max. 3 persons per team)

A Defined time period in which

the firm can be part of the

program, between 3 and 6 months

More intense coaching and

mentoring than incubators

A Final presentation to possible

investors

Usually the possibility to working space

Seed stage

Average investmets: 50,000US $

Table 1: Crowdfunding, Incubators and accelerators characteristics

The importance of those new kinds of financial resources, in order to substitute the lack of

business angel backing, for a startup is clear; in fact, those financial channels showed worldwide a

constant growth, both in numbers of , both in the total amount invested.

In fact, for what concerns crowdfunding platforms, it is observable a sustained growth in the

amount of total investment trough such platforms, reaching 2.7 billion dollars in 2012 globally25

and in the overall number of crowdfunding platforms worldwide:

24 http://www.dutchincubator.nl/uploads/Documents/49.pdf25 “Crowdfunding industry report”, Massolution,2013

13

Figure 3: Total amount invested through crowdfunding platforms; Source: Crowdfunding industry report”,

Massolution,2013

Figure 4: Percentage growth of crowdfunding platforms worldwide from 2008 to 2012; Source:

For what concerns the incubators and accelerators, there have been seen a boom in their

numbers, with 29% annual increase since 2008 as we can see from the data relative to 10 European

countries26, highlighting their importance for startups:

26 The research was focused on Czech Republic, France, Germany, Ireland, Italy, the Netherlands, Slovakia, Spain, Sweden and the United Kingdom. (Eduardo Salido, Marc Sabás and Pedro Freixas,“The Accelerator and Incubator ecosystem in Europe”, Telefonica, 2013)

The flexibility of the tax system not only encourages entrepreneurs to set the operation in that

location, but also helps it growing during the first difficult periods by allowing the startup to retain

more liquidity;a flexible tax system also on investments in risky startups helps to increase the flow

of capital towards start-ups.

However, if the startups must fill the bankruptcy pathway,as it occurs often in those early phases, it

needs to take little time in order for the entrepreneur to be able to create another startup in less time,

instead of carrying the burden of failure for years, undermining the creativity and passions of the

entrepreneurs, reducing dramatically the probability of creating another startup, keeping in mind

that a heavy burden is also carried by investors who invested or lended money into a failed

business.

1.2.3 The expansion/scale phase

After the startup has been able to achieve the most important growth milestone, the

product/market fit, in which the business model has been validated ad the product is able to satisfy

the first customers, the focus can shifts from persevere/pivot to scale, increasing the number of

customers, with the goal to create fans loyal to the startup brand and product, trying to serve also

the largest part of customers, the mainstream customers, rather than only enthusiastic ones.

The startup main objective now is the creation of a strategic selling strategy by building a

sustainable revenue stream rather than depend on sporadic and casual transactions, called “ heroic

selling”.29

The process of creating and acquiring loyal customers and of developing a continuous revenue

stream is well described by the AARR metrics, developed by Dave McClure, and is composed by

five different building blocks30:

Acquisition phase, in which people that does not know our product is becoming an interest

possible customer, also called prospect,; the focus in this phase is the way in which

customers can find the startup and to attract initially its interest.

Activation phase, during which customer makes the fundamental step: use and get a first

approach with the product; in this phase it is important is to offer him an amazing

29 Lorenzo Paoli,“Il coaching per la tua startup”, Antonio Vallardi Editore, 2014, pp 113-11530 AARR metrics framework was first presented by Dave McClure in his blog

Retention phase, the most important step at this phase of growth, in which data are collected

about how many times a customer uses or buys our product. It is the main indicator of the

success of our business model, highlighting the overall level of satisfaction with the product

of the start-up.

Revenue phase, measures the time at which the activity of customers are monetized. It is still

another important indicator of success of the product.

Referral phase, the last phase, in which the satisfaction of the customers becomes the best

marketing tool for the startup, spreading the name of the startup across their networks,

exploiting the increasing curiosity of interested prospects about the product in order to

transform them into loyal customers through the AARR cycle.

Figure 6: AARR metrics; Source: Dave McClure Blog

Startup have to complete as fast as possible this process of “fans” creation, increasing its pools of

customers, building a strong brand awareness among different kind of consumers. One example of

the power of referral is Facebook, a social network started from a small niche market of Harvard

students in 2004, spread to other college students in US just few months after the first launch. Now

it has become is the most visited page in the web, overtaking also Google.31

Once the success has been obtained by the startup, its successful journey ends with one of those

destinations32:

31 Facebook timeline, may 3 2006 (https://newsroom.fb.com/news/2006/05/facebook-expands-to-include-work-networks-2/)

32 David Smith, “Zero-to-IPO & Other fun destinations”, Cambridge Manhattan Group, 2013, pp 19-21

17

Destination ResultsAsset Sale The company is sold, even if it is not profitable: the

acquirer buys the intellectual property of the startup33

Cash-flow sale The company is sold as a self-sustaining company

IPO Shares of the company are traded In the public

market: the startup is no more a private independent

entityTable 2: Possible successful destinations of startups

The best possible destinations for the startup are IPO and Cash flow sale, in which both

entrepreneurs and investors are fully rewarded for their efforts in building and supporting the

business, respectively.

However, the road to one of those final milestones requires some key factors in the external

environment in which startup resides.

In fact, at this later stage, also called expansion phase, the startup needs a more intensive capital

support from more formal investors through the venture capital funding channel.

This kind of funding is characterized by the figure of venture capitalists that, differently from

business angels, are intermediaries between an investment fund, such as pension fund, public fund

or a fund of high net worth individuals,and the growing startup in which they invest.

Given the fact that the fund they manage is much higher than the typical budget of a business

angel, the investment of venture capitalist are much more intense, raging from 2 millions dollar to 5

million dollars or more.34

The importance of venture capital is not limited only to the substantial financial support, but they

are also crucial in:

Creating a very good reputation for the startup, attracting more skilled employees,

increasing their market power in transactions with suppliers/buyers by signalling the clear

growth opportunities of the startup

Reducing the risk of moral hazard or opportunistic behaviours from employees and

founders, by providing incentives, specially with larger equity stakes than traditional equity

33 If the intellectual property is valuable only if it is related to the core product team that developed it, the supporting team is also brought into the acquiring company (David Smith, “Zero-to-IPO & Other fun destinations”, CambridgeManhattan Group, 2013, pp 233-235)

34 Jon Hoyos Iruarrizaga , María Saiz Santos, “The informal investment context: specific issues concerned with business angels”, 2013, pag 183

18

funding35

Supporting the management of the startup, by participating in the board of directors

membership and by supporting the human resource management.

Recent studies also showed that venture capital increases the innovation activities, also by looking

at the number of patents36 and in the potential of scale activity37.

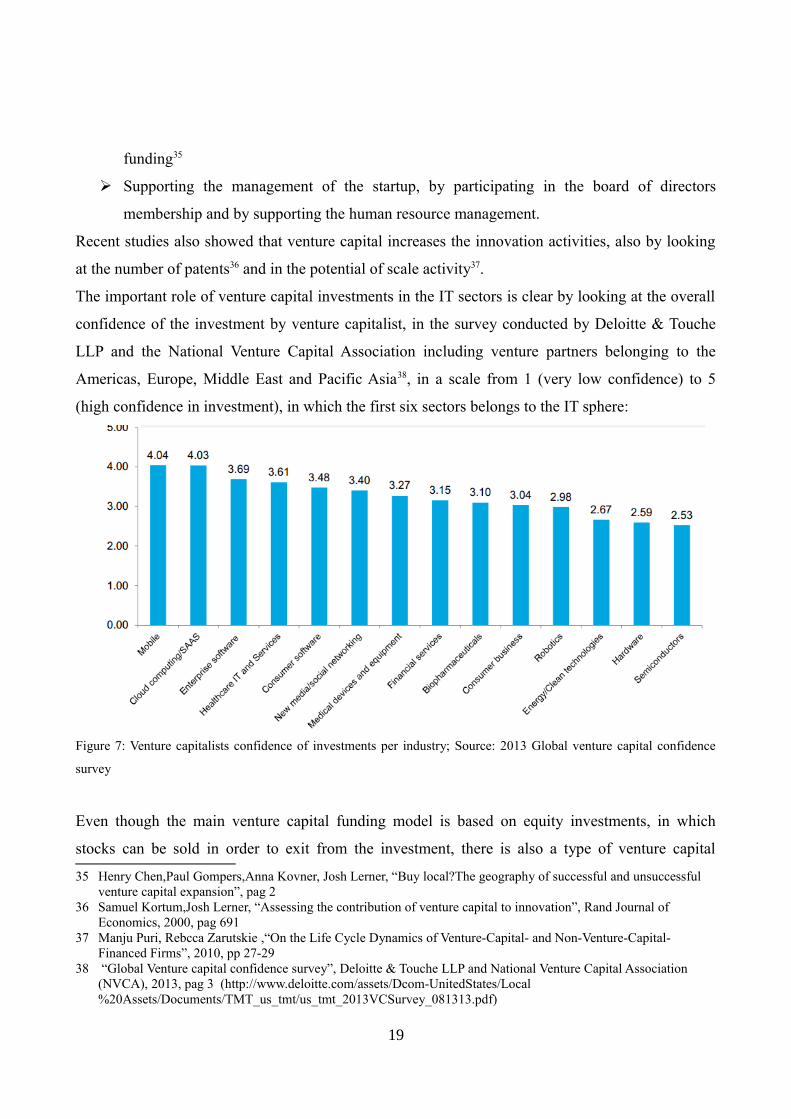

The important role of venture capital investments in the IT sectors is clear by looking at the overall

confidence of the investment by venture capitalist, in the survey conducted by Deloitte & Touche

LLP and the National Venture Capital Association including venture partners belonging to the

Americas, Europe, Middle East and Pacific Asia38, in a scale from 1 (very low confidence) to 5

(high confidence in investment), in which the first six sectors belongs to the IT sphere:

Figure 7: Venture capitalists confidence of investments per industry; Source: 2013 Global venture capital confidence

survey

Even though the main venture capital funding model is based on equity investments, in which

stocks can be sold in order to exit from the investment, there is also a type of venture capital

35 Henry Chen,Paul Gompers,Anna Kovner, Josh Lerner, “Buy local?The geography of successful and unsuccessful venture capital expansion”, pag 2

36 Samuel Kortum,Josh Lerner, “Assessing the contribution of venture capital to innovation”, Rand Journal of Economics, 2000, pag 691

37 Manju Puri, Rebcca Zarutskie ,“On the Life Cycle Dynamics of Venture-Capital- and Non-Venture-Capital-Financed Firms”, 2010, pp 27-29

38 “Global Venture capital confidence survey”, Deloitte & Touche LLP and National Venture Capital Association (NVCA), 2013, pag 3 (http://www.deloitte.com/assets/Dcom-UnitedStates/Local%20Assets/Documents/TMT_us_tmt/us_tmt_2013VCSurvey_081313.pdf)

19

funding based on loans.

This kind of venture funding is called venture lending and is aimed at substitute the typical bank

loans by providing loans at growing startups, usually operating with a negative cash flow and with

few physical assets, causing the traditional loans to avoid those kind of investments.

Instead of physical assets, venture loans use intellectual properties as warranty and take as a signal

of quality of the project an already funding backed startup, which increases the probability for the

startup to receive the venture loans. However, venture capital firms distribution shows how they

tend to concentrate into few and vibrant technological environment; in fact, according to the U.S

venture capital firms market, more than one half of the 1000 venture capital firms registered in

“Pratt’s Guide to Private Equity and Venture Capital Sources” set their operations in only three

main areas: San Francisco, Boston, New York.39

Given the fact that the monitoring cost in controlling and coaching the startup increases as the

distance between them increases, implying also a decrease supporting to the management by

venture capitalists, startup are better off moving towards environment in which there is an active

network of venture capital, in order to increase the probability of getting financed and supported.

There is a trend in which, globally, the amount of venture capital invested is increasing year after

year, especially in U.S, a well developed venture capital market, in which a remarkable amount of

29.7 billion dollars have been achieved in 201340.

Figure 8: Total venture capital invested in U.S between 2010 and the second quarter of 2014; source: MoneyTree

Report by PricewaterhouseCoopers LLP and the National Venture Capital Association

39 Henry Chen , Paul Gompers, Anna Kovner , Josh Lerner,“Buy Local? The Geography of Successful and Unsuccessful Venture Capital Expansion”, Boston: Harvard Business School Publishing, 2009, pag 2

40 MoneyTree Report by PricewaterhouseCoopers LLP and the National Venture Capital Association (NVCA)

20

Due to the low probability of getting backed by a venture capitalist, where only 1 out of 100

business plans received by a venture capital firm is accepted and eligible for the funding, startup

increases their probability of getting financed in a context in which there are venture capitalists and

in which the international attention, through research and articles by scientific and business

international newspapers, is interested in.

Another needed factor, for a start-up at this phase, is to operate in an environment in which

operating costs, such as the rent for the office and the cost of living, does not hurdle the growth

pathway of the start-up, putting in danger its liquidity by costs that are not finalized to create value

to the final consumer.

It is equally fundamental to offer the start-ups infrastructures that help the growth phase, such as a

fast and reliable internet connection, especially for web based startups; the importance of the

internet connection network is also proved by the fact that offering a broadband as large as possible

is one of the main goal of the European Digital Agenda.41

1.3 Mortality rate of startups

The new management techniques that we have explained previously are aimed to reduce

drastically the major causes of death of startups due to bad practices, such as premature scaling

caused by too low direct contact with final customers or a lack of a strategic selling cycle.42

In fact, the large number of internet companies failed after the bust of the internet bubble in 2001

was due to an attempt to apply the traditional management techniques, based on the creation of a

product without any ex ante feedback from customers, inducing companies to scale a wrong

business model.

The environment, instead, is fundamental to increase the probability to survive for a startup and to

make startups able to grow and compete globally, especially in the fast changing and challenging IT

sector. However, due to the intrinsic characteristics of startups, the mortality rate remains

considerable; in fact, it is remarkable the death rate in 2014, even in a well developed startup

41 Digital Agenda for Europe, by improving the broadband connection, has the goal to exploit the digitalization of theeconomy. The program was first launched in 2010, and the progression towards the achievement of these goals are reported annually in the Digital Agenda Scoreboard. (Digital Agenda for Europe Mainpage: http://ec.europa.eu/digital-agenda/digital-agenda-europe)

42 “Five Reasons 8 Out Of 10 Businesses Fail”, Forbes, http://www.forbes.com/sites/ericwagner/2013/09/12/five- reasons-8-out-of-10-businesses-fail/

21

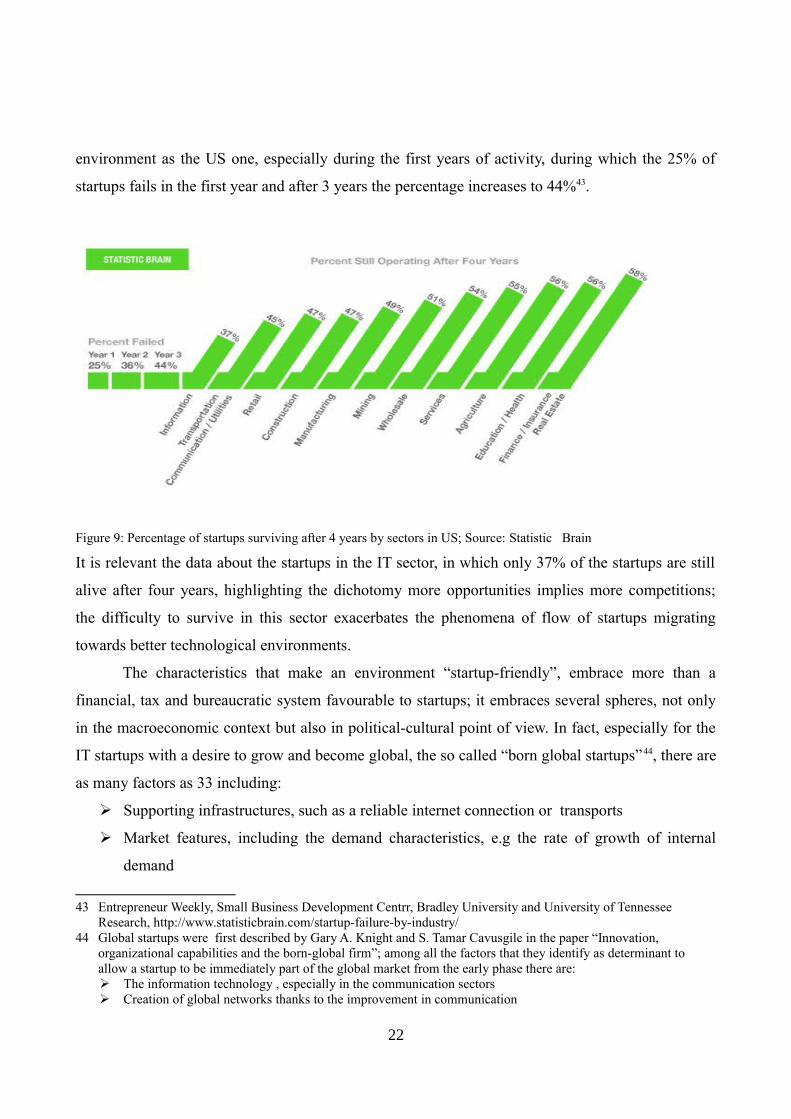

environment as the US one, especially during the first years of activity, during which the 25% of

startups fails in the first year and after 3 years the percentage increases to 44%43.

Figure 9: Percentage of startups surviving after 4 years by sectors in US; Source: Statistic Brain

It is relevant the data about the startups in the IT sector, in which only 37% of the startups are still

alive after four years, highlighting the dichotomy more opportunities implies more competitions;

the difficulty to survive in this sector exacerbates the phenomena of flow of startups migrating

towards better technological environments.

The characteristics that make an environment “startup-friendly”, embrace more than a

financial, tax and bureaucratic system favourable to startups; it embraces several spheres, not only

in the macroeconomic context but also in political-cultural point of view. In fact, especially for the

IT startups with a desire to grow and become global, the so called “born global startups”44, there are

as many factors as 33 including:

Supporting infrastructures, such as a reliable internet connection or transports

Market features, including the demand characteristics, e.g the rate of growth of internal

demand

43 Entrepreneur Weekly, Small Business Development Centrr, Bradley University and University of Tennessee Research, http://www.statisticbrain.com/startup-failure-by-industry/

44 Global startups were first described by Gary A. Knight and S. Tamar Cavusgile in the paper “Innovation, organizational capabilities and the born-global firm”; among all the factors that they identify as determinant to allow a startup to be immediately part of the global market from the early phase there are: The information technology , especially in the communication sectors Creation of global networks thanks to the improvement in communication

22

International reputation of the environment

However in the next chapter, in which I describe the Italian environment for IT startups, for the

purpose of my research I will focus only on few factors that, in my point of view, are critical for the

recent phenomena of migration of entrepreneurs from Italy to Berlin:

Financial system

Labour cost and human resource

Bureaucracy concerning the creation and the cessation of a startup

23

CHAPTER TWO

Italian IT startup landscape

2.1 Italian Startup ecosystem in the Information technology sector

Startups in Italy has become a subject of social interest, both for economic and social point

of view, only in recent times.

The recent economic crises it Italy have moved the attention to innovative startups, as a way to

overcome the innovation gap that was becoming remarkable with respect other nations and as a tool

to promote self-employment, in a period in which unemployment rate is eroding the trust of the

current economic system.

The corporate drain phenomena, namely the migration of one startup to another foreign country,

showed a 20% increase in 201245, according to the Mind in the Bridge46 2012 survey; in order to

stop this trend, the government was forced to develop a plan with the goal to not only protect them

and retain them from leaving Italy, but also to be more able to compete in a global environment.

In fact, right in the middle of a fierce recession in Italy in 2012, innovative startups for the first time

were “legally” described , in the “Decreto legge crescita 2.0”, as powerful human institutions able

to 47:

Decrease unemployment, especially between young people, that in Italy reached nowadays

the peak of 43.7 % with respect to the 20% European average48

Fostering a sustainable growth of Italian economy, especially after the global financial crisis

of 2008

Fostering a technological progress exploiting the creativity of entrepreneurs

Creating an innovative culture in Italy

Creating an Innovative environment, start-up friendly, encouraging social mobility and the

45 “Startup in Italy: facts and trend”, mind the bridge survey 2012, pag 12. 46 Mind in the bridge foundation, founded by Marco Marinucci, is a San Francisco based incubator that, on an annual

basis, carries out research on italian entrepreneurship with the ultimAte goal to create a “Bridge” betweeen U.S entrepreneurial ecosystem and the Italian one.

47 Gazzetta Ufficiale, legislation decree n° 179 of 18/10/2012 http://www.gazzettaufficiale.it/atto/serie_generale/caricaDettaglioAtto/originario?atto.dataPubblicazioneGazzetta=2012-12-18&atto.codiceRedazionale=12A13277

48 European Commission Eurostat website, http://epp.eurostat.ec.europa.eu/statistics_explained/index.php/Unemployment_statistics

24

make more attractive the Italian ecosystem in order to attract foreign investments and

talented people

However, in order to be considered “innovative startups” , following the definition of Decreto legge

crescita 2.0, they have to be in possess those requirements49:

The majority of shares and of votes must be held by physical person, not by institutions for

example banks

Less then 48 months of past activities

Legal and operational office in Italy

The value of their production, since the second year of activity, must be lower than 5

millions

No profits are yielded

Main social objective is the “development, the production and the commercialization of

innovative products or services with high degree of technology”

An investment of At least 30% of the value added50 in R&D activities or having at least one

third of the total workforce with a master or PhD; as an alternative, the startup must possess

a patent

Even though the goal of the Decreto legge crescita 2.0 was to foster entrepreneurship by reshaping

the financial system, the bureaucracy and employment procedures , this legislation decree still

needs, after 2 years, more laws in order to become effective. This can be explained by the large

amount of important matters embraced by this legislation decree.

The lack of a well-working and effective legislation of startups in Italy obstacles the creation of a

trustfully ecosystem, needed to attract more entrepreneurs and capital from foreign countries. This

is even worse for the IT sector.

The larger proportion of startups in Italy, in fact, operates in the Information communication

technology (21.8%) and in the web platforms (49.1%)51..

49 Legislation decree n° 179 of 18/10/2012 art 25 comma 1-450 Value added is given by revenues of a firm less cost of purchases of material and services, such as labour wages51 Mind in the bridge survey 2012, “Startup in Italy: facts and trend”, mind the bridge, pag 12

25

Figure 10: Distribution of Italian startups by industry; Source: Mind in the bridge report 2012

For what concerns the geographical distribution across Italy of these startups, there is an

evidence of the poor exploitation of entrepreneurship in the south are clear by looking at the

location of startups in Italy.

Figure 11: Geographical distribution of startups per macro-areas; Source: Mind in the Bridge report 2012

The bad situation concerning the entrepreneurship in the southern regions, mostly due to bad politic

management and waste of public resources, makes it far less attractive for entrepreneurs to set their

businesses in those regions.

Another information we can extrapolate from the geolocation distribution of startups in Italy is that

the main regions are Lombardia, with 25% of startups and Lazio, with 17% of total startups, with

26

their main centres in Milan and Rome, respectively, according to Mind in the Bridge survey 2012.

Those results are also confirmed by looking at the distribution per region of innovative startups

registered in the Chamber of Commerce register, 2508 in August 201452:

Area Region Number of Innovativestartups

Relative distribution ofstartups

North east Trentino Alto Adige 112 4,5%

Friuli-Venezia Giulia 75 3%

Veneto 198 7,9%

Emilia Romagna 274 10,9%

North west Valle d'Aosta 9 0,4%

Piemonte 190 7,6%

Lombardia 553 22%

Liguria 36 1,4%

Center Toscana 173 6,9%

Lazio 227 9%

Umbria 30 1,2%

Marche 100 3,9%

South and Islands Abruzzo 38 1,5%

Basilicata 12 0,5%

Calabria 44 1,7%

Campania 136 5,4%

Molise 11 0,4%

Puglia 105 4,2%

Sardegna 76 3%

Sicilia 99 3,9%

Italy 2508

Table 3: Distribution of innovative startups per region; Source: Chamber of commerce register of innovative startups,25 august 2014

It is clear how the majority of startups (1447 of 2508, approximately 58%) belongs to the north area

of Italy, with peaks in Lombardia (553), Emilia Romagna (274), Veneto (198) and Piemonte (190).

For what concerns the central Italy, the results are coherent with Mind in the Bridge survey 2012

results, with a total of 530 out of 2508, or approximately 21%, of total startups with Lazio as a

52 Chamber of Commerce, “Registro imprese” http://startup.registroimprese.it/report/startup.pdf, retrieved on 25 August 2014

The unexploited entrepreneurial potential of the southern regions and the islands is confirmed by

looking at the total amount of startups in the eight regions composing this area, with 531 total

startups, or 21% of the total, with only two regions exceeding the threshold of 100 startups:

Campania (136) and Puglia (105).53

After this brief introduction to the startup environment in Italy, especially for what concerns the IT

sectors, in which we described the main legislation and some key data about startup, the next

paragraph will be devoted to the analysis of the financing system, from public institutions and

private institutions

2.2 Financing channels in Italy

Italian startups in high technology sectors,like any startup, needs to raise funds in every

stage of its life cycle, in order to foster the growth process.

In the next paragraphs I will focus on the main funding channels for start-ups:

Public financing

Private equity investments

Incubators/accelerator

Crowdfunding platforms

The focus will be on quantitative data for each funding channel as well as the recent legal regulation

concerning the equity crodwfunding platforms.

2.2.1 The public financing channels

Public financing plays a key role in helping startups at the very early stage and in fostering

innovation as we said in the first chapter.

In Italy, even though historically has been a country in which the public participation in the

economy was very intense, the direct public financing in startups turns out to be not as effective as

it has been for traditional enterprises.

In fact, public funding is considered by startups very difficult to get and not enough effective to rely

53 Data are elaborated from “Registro imprese” http://startup.registroimprese.it/report/startup.pdf

28

entirely on it, and is considered by enterpreneurs only a secondary tool of funding.54

Two of these projects of public funding for startups are:

SIMEST “start-up fund”, which supply investment in minority stakes, up to 49% of shares,

for new born startups that are going to undertake international projects outside EU. This

investment can be complementary to other financing sources, but not greater than €200.000

for each project, for a duration of 2-4 years, up to a maximum of 6 years. The exit strategy

for the investment is the repurchase by the startup of the equity stakes.55

“Fondo Italiano d'Investimento”56 is an investment company, specialized in investing in

already established companies, with revenues between 25 millions and 250 millions, with

good assets balances. Only recently it opened a program, “program 101” in cooperation with

another investment company, Azimut; the the “Program 101” makes available a venture

capital fund of €35m dedicated to startups. It will be carried on also in collaboration with H-

farm, the biggest accelerator in Europe in Sile area, in Veneto, in order to enlarge the

discovery process of new innovative startups.

It is clear, however, that public institutions understood the importance of startups, during those

years, as key players in jobs creation and that's why Public entities have set up several projects,

aimed at creating a bridge between startups and traditional businesses. One of the most peculiar

project of this kind is called “AdottUp”, carried out by the employer federation Confindustria with

the support of Intesa San Paolo; it consists in fostering the “adoption” of high technology startups

by SME's traditional businesses, , through the share of services or trough partnership. Thanks to this

project, startups can exploit new financial, technological, distribution and networks channels

opportunities in a consolidated environment and, at the same time, they can use better

infrastructures. The advantages for the SME enterprises, instead, are to enrich the innovation

opportunities of their business as well as a tool to diversify from their core businesses.

It is clear how the startup public funding system, especially at the seed stage, is still growing

in Italy and has not reached yet a maturity necessary to satisfy fully the needs of Italian

entrepreneurs. In the next paragraph I will analyze another important component of the financing

channels used by startups: the private equity.

54 Rocco Frodinzi, Maria Matilde, Elona Guga, “Start-ups in the Cultural and Creative Industries: Main Criticisms in Italy”, Euro-Mediterranean Dialogue on Public Management (MED), 2013

As the public financing, also the private equity is facing diffculties in reaching a level of

investments able to satisfy completely the needs of IT startups, especially in the early phases of

growth; in fact, by looking at the sources of financial resources that Italian startups use at the seed

stage, according to the mind in the bridge results of the survey in 2012, we get that only 16 % of

startups were able to raise private equity capital; analysing more in deep the private equity

investments, 8% of the startups raised funds from business angels, 6% from seed capital, including

incubators and accelerators programs, and only 1.2% were able to raise venture capital funds.

Another important data that we can get from this research is that Bootstrapping, with 58% of the

startups, is the biggest source of financing at the early stage of startups, especially in the technology

sectors.

In the 6% of the financial institutions investments, for example banks loans, are included also loans

warranted by personal assets belonging to the founders rather than firm assets, and it is considered

an external source of financing, rather than a bootstrapping strategy. For this reason, the data about

financial institutions may be inflated and must be taken carefully.

At the same time, 8% of the startup were able to get a grant, and mostly they belongs to university

grants of research; in fact, 30% of the entrepreneurs obtaining a grant were researchers in

universities.

The results are summarized in the following table:

Financing source Number of startups able to receive the fund (in%)

Bootstrapping 58%

Private Equity 16%

Grants 8%

Financial institutions 6%

Non-financial institutions 6%Table 4: Distribution of starups by funding channels used; Source: Mind in the bridge report 2012

The venture capital investments are still at a primordial phase in Italy by looking at the

proportion of investment in business not yet appealing for the revenues.

In fact, by looking at the distribution of private equity investments for different dimensions of the

businesses (using revenues as main indicator) in the second semester in Italy, it turns out that the

30

large majority of venture capital investments belongs to the range of 15-50 million Euros of

revenues, with 50% of the total investments; the recent trend shows how especially venture capital

investors in Italy are switching their investments into larger and more consolidated companies, with

22,5 % of investments in companies with more than €100m of revenues.57.

Figure 12: Venture capital distribution for revenuees; Source: Deloitte report 2013

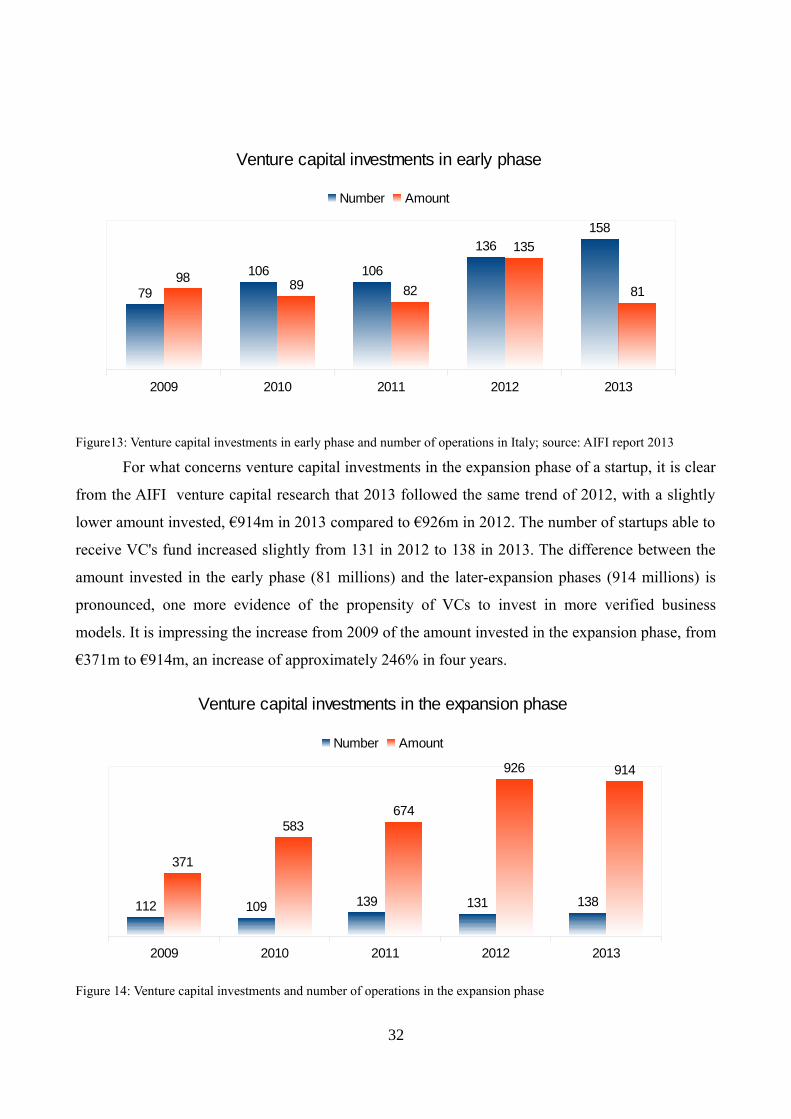

Analysing more in deep the seed/startup phase ad expansion phase of venture capital

structure, thanks to the research of the Association of private equity and venture capital (AIFI)58 in

2013, it is possible to look at the trend in the amount of capital invested and in the number of

companies that was able to receive it.

Focusing on the early phase, we can see that in the year 2013, the amount invested has fallen, from

the €135m euro reached in 2012, to €81m in 2013,approximately the amount that was invested in

2011 (81). At the same time, the number of startups that was able to being financed by Vcs

increased to 158, while in 2012 the number of companies was 136.

We can see that the general trend, since 2009, is an increase in the number of startups in which Vcs

invests at the early phase; in fact, the number of startups that received Vcs fund in the early stage

doubled, from 9 in 2009 to 158.

57 Deloitte, “Italy private equity confidence survey: outlook per il secondo semestre 2013”, 2013 (http://www.deloitte.com/assets/Dcom-Italy/Local%20Assets/Documents/Pubblicazioni/PrivateEquity_2semestre2013.pdf)

58 Italian Association of private equity and venture capital (AIFI),“Il mercato italiano del private equity e venture capital nel 2013”, AIFI report, 2013

31

Figure13: Venture capital investments in early phase and number of operations in Italy; source: AIFI report 2013

For what concerns venture capital investments in the expansion phase of a startup, it is clear

from the AIFI venture capital research that 2013 followed the same trend of 2012, with a slightly

lower amount invested, €914m in 2013 compared to €926m in 2012. The number of startups able to

receive VC's fund increased slightly from 131 in 2012 to 138 in 2013. The difference between the

amount invested in the early phase (81 millions) and the later-expansion phases (914 millions) is

pronounced, one more evidence of the propensity of VCs to invest in more verified business

models. It is impressing the increase from 2009 of the amount invested in the expansion phase, from

€371m to €914m, an increase of approximately 246% in four years.

Figure 14: Venture capital investments and number of operations in the expansion phase

32

2009 2010 2011 2012 2013

112 109 139 131 138

371

583674

926 914

Venture capital investments in the expansion phase

Number Amount

2009 2010 2011 2012 2013

79

106 106

136158

9889 82

135

81

Venture capital investments in early phase

Number Amount

Following the AIFI analysis, the main operators of VCs funds are:

Management Investment Company (SGR companies)

Regional/Public operators

Investment companies

Early stage operators

Italian banks

International operators

Their distribution of investments are different between the early phase and expansion phase; the dta

are summarized in the following table:

VC operators Early Phase Expansion Phase

SGR companies 36% 41%

Regional/Public operators 23% 22%

Investment companies 7% 18%

Ealy stage operators 34% 10%

Italian banks / 5%

International operators / 4%Table 5: Source: AIFI, the Italian market of venture capital and private equity in 2013

Another important data that AIFI research produces concerns the geographical distribution of

investments; the data highlights the gap between northern and southern regions. In fact, by looking

at the origin of the venture capital, 89% of the total invested comes from North Italy, while only 7%

from the centre and 3% from the South; 1 %, instead, comes from foreign investments.

Figure 15: Geographical distribution of venture capital investments; Source: AIFI report 2013

It is remarkable also the gap within northern region for what concerns the geographical distribution

33

89%

7%

3%1%

North Italy

Centre Italy

South Italy

Abroad

of the investments; in fact, Lombardia leads with 106 investments, followed by Emilia Romagna

with only 41, Campania (46), Sardegna (30), Lazio (24) and Veneto (18).

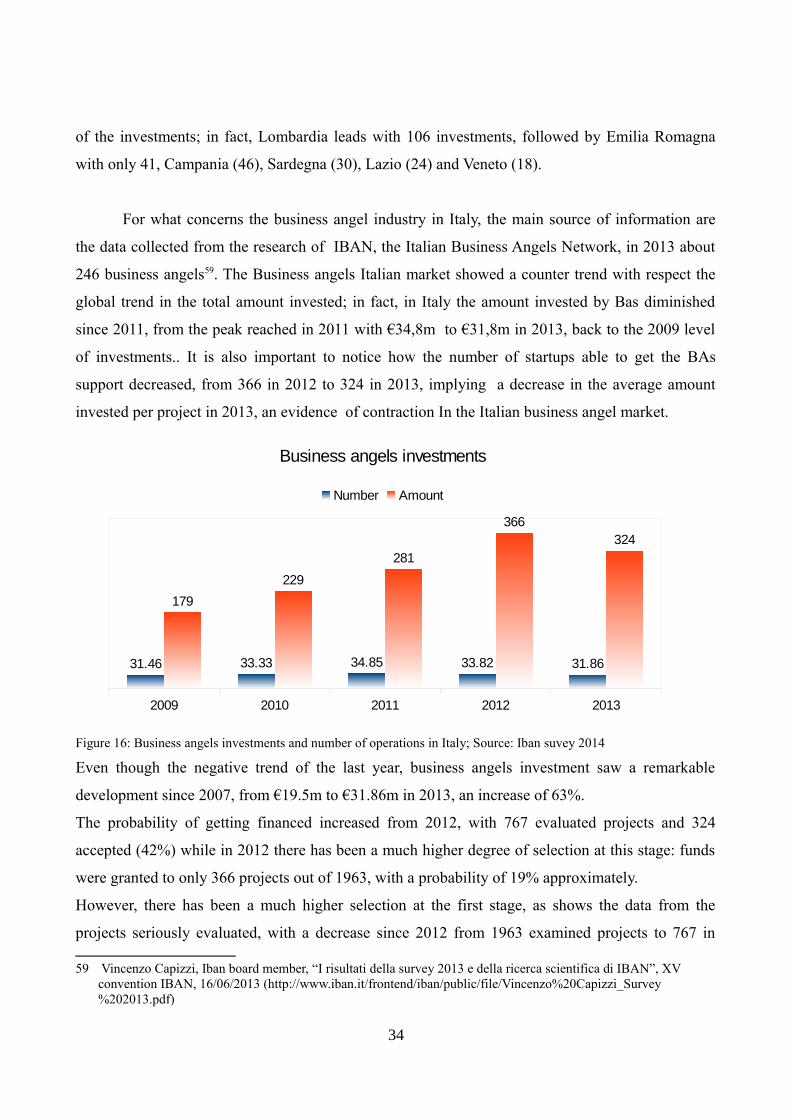

For what concerns the business angel industry in Italy, the main source of information are

the data collected from the research of IBAN, the Italian Business Angels Network, in 2013 about

246 business angels59. The Business angels Italian market showed a counter trend with respect the

global trend in the total amount invested; in fact, in Italy the amount invested by Bas diminished

since 2011, from the peak reached in 2011 with €34,8m to €31,8m in 2013, back to the 2009 level

of investments.. It is also important to notice how the number of startups able to get the BAs

support decreased, from 366 in 2012 to 324 in 2013, implying a decrease in the average amount

invested per project in 2013, an evidence of contraction In the Italian business angel market.

Figure 16: Business angels investments and number of operations in Italy; Source: Iban suvey 2014

Even though the negative trend of the last year, business angels investment saw a remarkable

development since 2007, from €19.5m to €31.86m in 2013, an increase of 63%.

The probability of getting financed increased from 2012, with 767 evaluated projects and 324

accepted (42%) while in 2012 there has been a much higher degree of selection at this stage: funds

were granted to only 366 projects out of 1963, with a probability of 19% approximately.

However, there has been a much higher selection at the first stage, as shows the data from the

projects seriously evaluated, with a decrease since 2012 from 1963 examined projects to 767 in

59 Vincenzo Capizzi, Iban board member, “I risultati della survey 2013 e della ricerca scientifica di IBAN”, XV convention IBAN, 16/06/2013 (http://www.iban.it/frontend/iban/public/file/Vincenzo%20Capizzi_Survey%202013.pdf)

34

2009 2010 2011 2012 2013

31.46 33.33 34.85 33.82 31.86

179

229

281

366324

Business angels investments

Number Amount

2013. For what concerns the average amount invested, the data shows that 68% of the investments

were below €100,000, while 24% of investments were under €15,000

Figure 17: Distribution of Business angel investments amounts in 2013; Source: Iban survey 2013

It is Interesting also how the number of investments by Business angels are distributed among

different sectors; from the IBAN survey 2013, the sector that has received most of the investments,

in terms of number, is the ICT sector, with 30% of investments in this particular segment, followed

by Media and entertainment (14%) and medical technology (11%). This confirms the global trend

of BAs investing, mostly, in the IT sector.

Figure 18: Business angel investments per industry in 2013,Source:IBAN survey 2014

35

<15,000

15,000-30,000

30,000-50,000

50,000-75,000

75,000-100,000

100,000-200,000

200,000-300,000

300,000-500,000

>500,000

0 0.05 0.1 0.15 0.2 0.25

Distribution of Business Angel investments amounts

According to IBAN survey 2014 results, the typical Italian Business angel:

Is a man of 40-50 years old

Has a disposable income of less than €2m, 10% of that finalized for angel investments;

46% of them invested alone, while 31% has invested with more than 8 Business angels

35% of the Business angels has invested in a startup with no revenues.

Both the VC and BA investments are in a clear growth trend in Italy, both in the number of

investments and in the total amount invested; it is also true that there still exists an investment gap

with other European countries, like UK, but this can be filled, in my opinion, exploiting more the

southern regions and increasing the awareness of entrepreneurs about possible private equity

funding channels.

The next funding channel analysed will be the Incubator/accelerator networks.

2.2.3 Incubators/Accelerators networks

For what concerns incubators/accelerators and technological-scientific parks, that carry out

incubators activities, there are 61 institutes60 in Italy.

It is interesting to look at the data about their distribution across Italy and the proportion of them

that are public owned by the government or local entities to have a snapshot of the current Italian

situation. From the survey on Incubators and on businesses being incubated carried out by Banca

d'Italia in 2012, the results shows that the number of incubators, as we mentioned before, is higher

in the north, especially at the north-east where Emilia Romagna region shows the maximum amount

of incubators (9).

It is also important to notice the high percentage of public owned incubators/accelerators,

averaging overall 63.6%; in my own opinion, this participation of the State in the

incubators/accelerators programs may compensate the lack of an efficient and effective direct

public financing system. Moreover, the high number of public owned incubators/accelerators in the

Southern regions is a proof of the efforts by the public institutions to foster entrepreneurial activities

In the South Italy.

60 Marta Auricchio, Marco Cantamessa, Alessandra Colombelli, Roberto Cullino, Andrea Orame, Emilio Paolucci, “Gli Incubatori d'Impresa d'Italia”, Banca d'Italia, 2012, pag 10

36

Geographical area Number of operatingincubators/accelerators

Public owned(percentage)

Private owned(Percentage)

North-east 18 58,8% 41,2%

North-west 10 50% 50%

Center 17 58.8% 41.2%

South Italy and Islands 13 90.9% 9.1%

Italy 58 63.6% 36.4%

Table 6: Distribution and Ownership of incubators and accelerators in Italy; Source: IndagineBanca d’Italia sugli incubatori e sulle imprese incubate 2012

Another important data collected by the survey on incubators in 2012 carried out by Banca

d'Italia is the level of relationship with university or research institutes; according to the research,

74% of incubators of the survey have some relationship with universities and research centres but

only 48% of them has a tight relation with them with them.61

Figure 19: Level of relationship beetween incubators/acceleators and unviersities-research centres; Source: Indagine

Banca d’Italia sugli incubatori e sulle imprese incubate 2012

One of the main incubator/accelerator operating in Italy is H-farm, in the province of Treviso,

specialized in digital startup with the goal to foster the process of technological and digitalization of

Italian companies62. It's importance is due both for its huge dimension, with offices also in Seattle

(US), London (UK) and in Mumbai (India) and for the relevance it has on the entrepreneurship on

the region area in which it started their operations, the North- east.

61 See supra, pag 1262 H-farm homepage, http://www.h-farmventures.com/en/who-we-are-2/

37

In fact, H-farm organizes many events in collaborations with universities, aimed at fostering an

entrepreneurial culture in the young people; they are called Hackatons, in which in only one day,

teams, composed by developers, marketers and designers, have to find solutions to problems of the

enterprises participating in the event.

Successful teams are given the possibility to:

Being incubated in the H-camp, in its incubator program of a duration of 2 months

Being incubated or getting a mentoring from other partner Incubator and Accelerators, as

happened to me and my team (EXITE) during the H-wine hackathon, where we were hosted

by “33entrepreneurs” in Bordeaux.

In this way not only the young people can be attracted by the world of entrepreneurship, especially

in internet oriented sectors, but also, at the same time, H-farm is able to get the attention of foreign

investors or “startup hunters”, namely business angels. The need to develop a tight relation with

schools, public institutions, research centres or financial institutions, that carry on projects related to

innovative startups, is one of the requirement for incubators, included in “Decreto crescita 2.0”, in

order to be certificated.63 Other requirements are:

Infrastructures sufficient to host in an efficient way the startup

The incubator have to posses facilities, such as broadband internet connection, meeting

rooms

The incubator has to be managed by people with a high degree of knowledge about the

startup ecosystem and about innovation matters; at the same time, they have to be supported

by a permanent managerial advisory entity

The incubator has a proven experience in supporting startups, attested by a legal document,

taking into account indicators such as:

number of applications received and evaluated by the incubator in an annual time frame

number of startup and annual percentage change of startups hosted and came out in a

year

average rate of growth of the production value of incubated startups

number of patents submitted by startups

total amount of risk capital obtained by the incubators from

Even if Italy has a famous incubator/accelerator like H-farm, in general their number is smaller than

63 Gazzetta Ufficiale, legislation decree n° 179 of 18/10/2012, art 25 comma 5 http://www.gazzettaufficiale.it/atto/serie_generale/caricaDettaglioAtto/originario?

38

in the European counterparts, for example France and Germany, with 130 and 150 incubators

respectively.64

Due to the low probability of getting incubated from Italian incubators, averaging to 11,3% with

3820 business ideas and 430 accepted65

2.2.4 Crowdfunding platforms

Italian government understood the growing importance of getting financed trough crowdfunding

web platforms, regulating the equity based model, in the article 30 of “Decreto Legge Crescita 2.0”,

then implemented by the Consob, the Controller of the Public market exchanges, in 2013, with its

regulation n°1853266; the regulation is limited to the equity crowdfunding model platforms.

This regulation put rules and limitations to a world, the web 2.0, that “usually auto-regulates,

auto-validate and with unlimited possibilities”67.

Italy has been the fist country in Europe to regulate the equity based crowdfunding internet

platform68, trying to overcome the intrinsic difference between formal financing, characterized by

bureaucracy and a top-down selection of projects, and the freedom and dynamism of

crownfudning. The main goal of the Consob Regulation n° 18592 in 2013 was to control and

guarantee the reliability of the equity internet platforms and to check the quality of the projects.

The new regulations developed by Consob in 2013 starts with the distinction of two categories of

equity based platforms trough the creation of two distinct registers:

“Registro ordinario”, in which subjects and entities, authorized by Consob, register

themselves after the necessary requirements have been checked69

64 Marta Auricchio, Marco Cantamessa, Alessandra Colombelli, Roberto Cullino, Andrea Orame, Emilio Paolucci, “Gli incubatori d'impresa in Italia”, Banca d'Italia, 2014, pag 12 (http://www.bancaditalia.it/pubblicazioni/econo/quest_ecofin_2/qef216/QEF_216.pdf pag 12

65 See supra, pag 1266 Consob regulation n°18592/2013 (http://www.consob.it/main/documenti/bollettino2013/d18592.htm?

symblink=/main/trasversale/risparmiatori/investor/crowdfunding/link_reg18592.html)67 Umberto Piattelli,“Il crowdfunding in Italia: una regolamentazione all'avanguardia o un'occasione mancata”, Linea

content/uploads/2013/08/equity_crowdfunding_1.pdf)69 The necessary conditions in order to be accepted in the registro ordinario are:

The company juridical form Shareholdersr and management people have to be persons of good standing For the management team, every member has to be of proved competence A relation has to be presented to Consob about the organizational structure and the activities carried out by the

platform

39

“Registro speciale”70, in which “gestori di diritto”, such as banks and investment

companies, are authorized to operate in investment activities and have to signal their

intention to carry on equity crowdfunding activities

Trough the control and vigilance activities of Consob, only the most reliable equity crowdfunding

portal may operate.

Thanks to the requirements of complete disclosure of information about the web platform, about the

high risks of the investments and about every single project , the “Decreto legge Crescita 2.0” was

able to foster not only the transparency in the equity based crowdfunding model, but also the public

awareness to the overall crowdfunding industry.

In fact, the recent trend, by looking at the results of the analysis carried by the Italian Crowdfunding

Network on of the italian crowdfunding platforms in 201471 , showed a boom in the number of

crowdfunding platforms in Italy of all types, with an increase of 42 platforms since 2011;

furthermore, the total amount invested through crowdfunding platforms increased by,

approximately, 33% from 2012 to 2013.

Figure 20: Number of all crowdfunding platforms since 2011; Source: “Analisi delle piattaforme di crowdfunding in

Italia”, Italian crowdfunding network, 2014

70 Consob regulation n°18592/2013, art 4 comma 2 (http://www.consob.it/main/documenti/bollettino2013/d18592.htm?symblink=/main/trasversale/risparmiatori/investor/crowdfunding/link_reg18592.html)

71 Daniela Castrataro, Ivana Pais, “analisi delle piattaforme italiane di crowdfunding”, Italian Crowdfunding network, 2014

40

2011 2012 2013 2014

12

21

41

54

Number of crowdfunding platforms

Figure 21: Total value of the investments trought crowdfudning platforms since 2012; Source: “Analisi delle

piattaforme di crowdfunding in Italia”, Italian crowdfunding network, 2014

Even thought the trend shows an increase both in the number and in the total amount invested

trough crowdfunding platforms, the equity based crowdfunding showed difficulties and a slower

growth with respect to other crowdfudning models in 2014, with only the 0.52% of the total

investments, compared with the 76.6% of lending based crowdfunding and the 13.3% of the reward

plus donation based crowdfunding.72

Another data, still obtained from the “Analysis of italian crowdfunding platforms”, that remarks

how the goal to foster startups funding raising trough equity crowdfunding has not been reached

yet, is the low percentage of total investments in entrepreneurial projects, with only 14%, compared

with the 63% of social projects and 23% of the creative projects.

Among the possible explanations of the failure in improving the flow of equity crowdfunding to

startups are73:

Lack of detailed regulations for the reward/donation based crowdfunding

Lack of a culture of crowdfunding, which requires a higher promotion of its characteristics,

especially to new born startups in order to increase its usage.

Immaturity of equity crowdfunding, where the pursue of the reduction of possible frauds

trough legislation brought to a bureaucratization of the process

72 Daniela Castrataro and Ivana Pais, “Analisi delle piattaforme italiane di crowdfunding”, Italian Crowdfunding network, 2014 73 See supra, pag 20

41

2012 2013 2014

13,274,205.00

22,947,578.00

30,621,050.00

Total amount invested

Strong opposition carried on by traditional institution, such as banks, in collaborating and in

assisting web platforms

International competitions from foreign crodwfunding internet platforms

It is clear how the Italian financing system for startups, especially in the IT sector, is still

developing nowadays and have not yet reached the level of other European countries, such as U.K

and France. However, the first necessary milestones, such as the attention by the government and

public institutions on the financing system of startups trough legislation and regulations and a

developed network of infrastructures, have been reached and a better situation, from my point of

view, can be achieved in the next years.

In the next chapter I will analyse two crucial factors for the entrepreneurship activity,

especially in specialized sectors of IT, that is the human resource availability and the labour costs in

Italy.

2.3 Human resources and Labour cost

One of the biggest problem for startups, from the early phase towards the different growth

milestones, is to be able to employ and find the right people with the right skill.

In my paper I will describe labour costs faced by Italian IT startups by focusing on three important

components:

Searching cost for the right employee with the right skills

Motivating employee to undertake the dangerous journey of the startup

Flexibility in hiring/firing employee

Before analysing in detail each of the components of labor costs, it is useful to give an

insight about the team composition of the startups in specialized IT sector.

The team composition of “digital” startups in Italy, basing on both on data available from the “Mind

on the bridge survey 2013”74 on 108 startups and 254 entrepreneurs and on the research of Niccolò

Meroni, starting from the data available from “Startupbusiness”, on 185 “digital” entrepreneurs, is:

74 Mind in the Bridge, “Sorry, not everyone is born to be a startupper “, Mind in the Bridge Foundation, 2013 (http://mindthebridge.org/wp-content/uploads/2013/12/MIND-THE-BRIDGE-REPORT-2013_ENG.pdf)

42

Raging from 2-4 members, averaging 30 years old

composed by entrepreneurs having established friendship networks in the work environment

(39%), during university studies (26.1%) or other channels (31.5%); less probable is family

entrepreneurship (9.67%)

30% of entrepreneurs are identified by Mind in the bridge as “Proven Entrepreneur”, with

past experience in the entrepreneurial activity, with 38% of co-founders belonging to this

type

The data about the proven entrepreneurs is particularly relevant for the ability of startup to attract

better human resource; in fact, proven entrepreneurs, due to their management skills and previous

entrepreneurship activities, are able to obtain considerable amount of funding (30% of them succeed

in raising more than €200,000, 50% of them more than €100000) and are more able to attract a

higher degree of human capital skills (22% of the startups of proven entrepreneurs have more than 4

founders).

2.3.1 Human resource availability

A recent trend in Italy is the boom in the technological parks and incubators in Italy, as we

have explained in the previous paragraph. The proliferation of an active and vibrant ecosystems of

infrastructures, especially in collaboration with universities, provides an useful human capital pool

from which choose the employee with the right skills needed for the startups and a tool for making

the young to come into know about the startups.

Although the recent trend of reduction of public financing to the Italian university system,

universities managed to develop a network of different infrastructures, such as:

Offering co-working spaces for startuppers-students

Incubators financed by the universities itself.

Peculiar examples can be found in different geographical areas of Italy, highlighting the fact that

this trend is spread at a national level, rather than constrained to already well-developed regions:

43

Geographicalarea

University Project name Description Sectors

North-east University ofPadova

“Start Cube”75 Incubator program inpartnership with“Fondazione Cassa diRisparmio di Padova eRovigo”

Hightechnology

North-west Politecnico diTorino

“I3P”76 Incubator program; since2011 I3P launched theprogram“Tetrabit”, focusingon projects related toconsumer services in the ITsector, such as e-commerce,web and mobile app

IT sector, especially: Gaming Social Mobile apps Consumer

services, e.gdaily life

web platforms

South andregions

University ofCalabria

Technest78 Incubator, financed also bythe Minister of economic ofgrowth as part of theC.R.E.S.C.I.T.A project(development project topromote the creation ofhightech startups inCalabria)

Hightech, for whatconcerns the IT sectorit is specialized onopen source software

Table 7: Examples of University incubators and accelerators

Incubators and accelerators, in light of what we have analysed before, help in creating clusters of

innovation which are beneficial to IT startups in two different ways: