Chapter 08 Inventories: Measurement True / False Questions 1. Physical counts of inventory are never done with perpetual inventory systems. True False 2. The main difference between perpetual and periodic inventory systems is the timing of the allocation of costs between inventory and cost of goods sold. True False 3. LIFO periodic and LIFO perpetual always produce the same amounts for ending inventory. True False 4. FIFO periodic and FIFO perpetual always produce the same amounts for cost of goods sold. True False 5. Cost of goods on consignment is included in the consignee's inventory until sold. True False 6. Shipping charges on outgoing goods are included in either cost of goods sold or selling expenses. True False

Transcript

Chapter 08

Inventories: Measurement

True / False Questions

1. Physical counts of inventory are never done with perpetual inventory systems. True False

2. The main difference between perpetual and periodic inventory systems is the timing

of the allocation of costs between inventory and cost of goods sold. True False

3. LIFO periodic and LIFO perpetual always produce the same amounts for ending

inventory. True False

4. FIFO periodic and FIFO perpetual always produce the same amounts for cost of goods

sold. True False

5. Cost of goods on consignment is included in the consignee's inventory until sold.

True False

6. Shipping charges on outgoing goods are included in either cost of goods sold or

selling expenses. True False

7. Net purchases are reduced for discounts taken whether the net method is used or the

gross method is used. True False

8. The choice of cost flow assumption (FIFO, LIFO, or average) does not depend on the actual physical flow of the product. True False

9. Inventory costing methods are merely means by which costs are allocated between

ending inventory and cost of goods sold. True False

10. During periods of falling prices, LIFO ending inventory will be less than FIFO ending

inventory. True False

11. LIFO always provides a better match of revenue and expense than does FIFO.

True False

12. Unit LIFO is more costly to implement than dollar-value LIFO.

True False

13. LIFO liquidation profits occur when inventory quantity declines and costs are rising.

True False

14. The gross profit ratio is calculated by dividing gross profit by average inventory.

True False

15. Dollar-value LIFO eliminates the risk of LIFO liquidations.

True False

16. A company that prepares its financial statements according to International Financial

Reporting Standards can use all of the same inventory valuation methods as a company that prepares its statements under U.S. GAAP. True False

Multiple Choice Questions

17. In a perpetual inventory system, the cost of purchases is debited to:

A. Purchases.

B. Cost of goods sold.

C. Inventory.

D. Accounts payable.

18. In a periodic inventory system, the cost of purchases is debited to:

A. Purchases.

B. Cost of goods sold.

C. Inventory.

D. Accounts payable.

19. In a perpetual inventory system, the cost of inventory sold is:

A. Debited to accounts receivable.

B. Credited to cost of goods sold.

C. Debited to cost of goods sold.

D. Not recorded at the time goods are sold.

20. In a periodic inventory system, the cost of inventories sold is:

A. Debited to accounts receivable.

B. Credited to cost of goods sold.

C. Debited to cost of goods sold.

D. Not recorded at the time goods are sold.

21. The inventory method that will always produce the same amount for cost of goods

sold in a periodic inventory system as in a perpetual inventory system would be:

A. FIFO.

B. LIFO.

C. Weighted average.

D. None of the above.

22. The Mateo Corporation's inventory at December 31, 2013, was $325,000 based on a physical count priced at cost, and before any necessary adjustment for the following:

▪ Merchandise costing $30,000, shipped f.o.b. shipping point from a vendor on December 30, 2013, was received on January 5, 2014.▪ Merchandise costing $22,000, shipped f.o.b. destination from a vendor on December 28, 2013, was received on January 3, 2014.▪ Merchandise costing $38,000 was shipped to a customer f.o.b. destination on December 28, arrived at the customer's location on January 6, 2014.▪ Merchandise costing $12,000 was being held on consignment by Traynor Company.

What amount should Mateo Corporation report as inventory in its December 31, 2013, balance sheet?

A. $367,000.

B. $427,000.

C. $405,000.

D. $325,000.

23. Ending inventory is equal to the cost of items on hand plus:

A. Items in transit sold f.o.b. shipping point.

B. Purchases in transit f.o.b. destination.

C. Items in transit sold f.o.b. destination.

D. None of the above.

24. Purchases equal the invoice amount:

A. Plus freight-in, plus discounts lost.

B. Less purchase returns, plus purchase allowances.

C. Plus freight-in, less purchase discounts.

D. Plus discounts, less purchase returns.

25. Using the gross method, purchase discounts lost are:

A. Included in purchases.

B. Added to accounts payable.

C. Included in interest expense.

D. Deducted from discount income.

26. Under the net method, purchase discounts lost are:

A. Included in purchases.

B. Added to accounts payable.

C. Included in interest expense.

D. Deducted from discount income.

27. Inventory does not include:

A. Materials used in the production of goods to be sold.

B. Assets intended to be sold in the normal course of business.

C. The cost of office equipment.

D. Assets currently in production for normal sales.

28. Under the gross method, purchase discounts taken are:

dresses from McGuire on July 17 and received an invoice with a list price amount of $6,000 and payment terms of 2/10, n/30. Alison uses the net method to record purchases. Alison should record the purchase at:

A. $5,940.

B. $5,880.

C. $6,000.

D. $6,120.

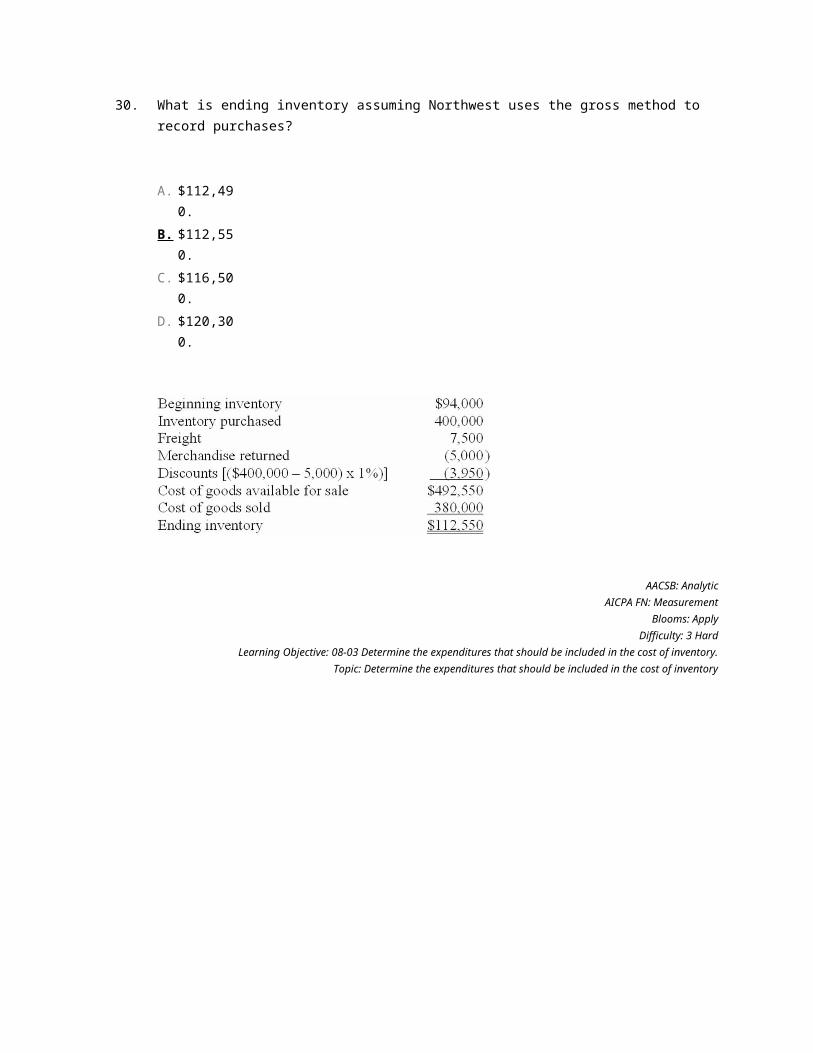

Northwest Fur Co. started 2013 with $94,000 of merchandise inventory on hand. During 2013, $400,000 in merchandise was purchased on account with credit terms of 1/15, n/45. All discounts were taken. Purchases were all made f.o.b. shipping point. Northwest paid freight charges of $7,500. Merchandise with an invoice amount of $5,000 was returned for credit. Cost of goods sold for the year was $380,000. Northwest uses a perpetual inventory system.

30. What is ending inventory assuming Northwest uses the gross method to record purchases?

A. $112,490.

B. $112,550.

C. $116,500.

D. $120,300.

31. Assuming Northwest uses the gross method to record purchases, what is the cost of

goods available for sale?

A. $492,500.

B. $496,500.

C. $490,500.

D. $492,550.

Cinnamon Buns Co. (CBC) started 2013 with $52,000 of merchandise on hand. During 2013, $280,000 in merchandise was purchased on account with credit terms of 2/10, n/30. All discounts were taken. Purchases were all made f.o.b. shipping point. CBC paid freight charges of $9,000. Merchandise with an invoice amount of $4,000 was returned for credit. Cost of goods sold for the year was $316,000. CBC uses a perpetual inventory system.

32. Assuming CBC uses the gross method to record purchases, ending inventory would

be:

A. $6,480.

B. $15,400.

C. $15,480.

D. $21,000.

33. What is cost of goods available for sale, assuming CBC uses the gross method?

A. $312,480.

B. $326,000.

C. $331,480.

D. $337,000.

34. Cost of goods sold is given by:

A. Beginning inventory - net purchases + ending inventory.

B. Beginning inventory + accounts payable - net purchases.

C. Net purchases + ending inventory - beginning inventory.

D. Net Purchases + beginning inventory - ending inventory.

35. The LIFO Conformity Rule states that if LIFO is used for:

A. One class of inventory, it must be used for all classes of inventory.

B. Tax purposes, it must be used for financial reporting.

C. One company in an affiliated group, it must be used by all companies in an affiliated group.

D. Domestic companies, it must be used by foreign partners.

36. The largest expense on a retailer's income statement is typically:

A. Salaries and wages.

B. Cost of goods sold.

C. Income tax expense.

D. Depreciation expense.

37. In a perpetual average cost system:

A. A new weighted-average unit cost is calculated each time additional units are purchased.

B. The cost allocated to ending inventory is generally the same as it would be in a periodic inventory system.

C. The moving-average unit cost is determined following each sale.

D. The average is determined by dividing the total number of units sold by the cost of units purchased during the period.

38. In a period when costs are rising and inventory quantities are stable, the inventory

method that would result in the highest ending inventory is:

A. Weighted average.

B. Moving average.

C. FIFO.

D. LIFO.

39. During periods when costs are rising and inventory quantities are stable, cost of goods sold will be:

A. Higher under FIFO than LIFO.

B. Higher under FIFO than average cost.

C. Lower under average cost than LIFO.

D. Lower under LIFO than FIFO.

40. During periods when costs are rising and inventory quantities are stable, ending

inventory will be:

A. Higher under LIFO than FIFO.

B. Lower under average cost than LIFO.

C. Higher under average cost than FIFO.

D. Higher under FIFO than LIFO.

41. In periods when costs are rising, LIFO liquidations:

A. Can't occur.

B. Are used to reduce tax liabilities.

C. Are a source of off-balance-sheet financing.

D. Distort the net income.

42. The use of LIFO during a long inflationary period can result in:

A. A net increase in income tax expense.

B. An inflated balance sheet.

C. Significant cash flow advantages over FIFO.

D. A reduction in inventory turnover over FIFO.

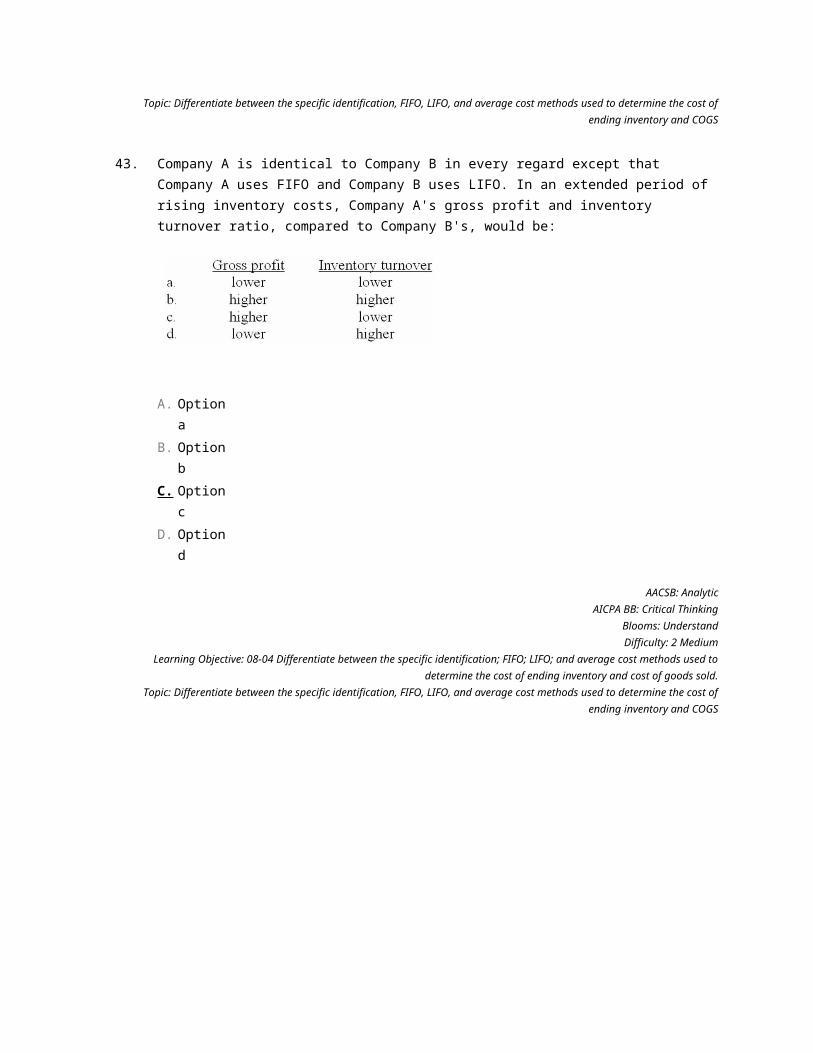

43. Company A is identical to Company B in every regard except that Company A uses

FIFO and Company B uses LIFO. In an extended period of rising inventory costs, Company A's gross profit and inventory turnover ratio, compared to Company B's, would be:

A. Option a

B. Option b

C. Option c

D. Option d

44. Company C is identical to Company D in every respect except that Company C uses LIFO and Company D uses average costs. In an extended period of rising inventory costs, Company C's gross profit and inventory turnover ratio, compared to Company D's, would be:

A. Option a

B. Option b

C. Option c

D. Option d

Fulbright Corp. uses the periodic inventory system. During its first year of operations, Fulbright made the following purchases (listed in chronological order of acquisition):

• 40 units at $100• 70 units at $80• 170 units at $60

Sales for the year totaled 270 units, leaving 10 units on hand at the end of the year. 45. Ending inventory using the average cost method (rounded) is:

A. $650.

B. $1,000.

C. $707.

D. $600.

46. Ending inventory using the FIFO method is:

A. $650.

B. $1,000.

C. $707.

D. $600.

47. Ending inventory using the LIFO method is:

A. $650.

B. $1,000.

C. $707.

D. $600.

Nu Company reported the following pretax data for its first year of operations.

48. What is Nu's net income if it elects FIFO?

A. $480.

B. $288.

C. $1,360.

D. $144.

49. What is Nu's net income if it elects LIFO?

A. $288.

B. $144.

C. $240.

D. $480.

50. What is Nu's gross profit ratio if it elects LIFO?

A. 80%.

B. 49%.

C. 40%.

D. 5%.

Nueva Company reported the following pretax data for its first year of operations.

51. What is Nueva's gross profit ratio (rounded) if it elects FIFO?

A. 30%.

B. 32%.

C. 10.7%.

D. 60%.

52. What is Nueva's net income if it elects FIFO?

A. $440.

B. $264.

C. $620.

D. $372.

53. What is Nueva's net income if it elects LIFO?

A. $440.

B. $264.

C. $620.

D. $372.

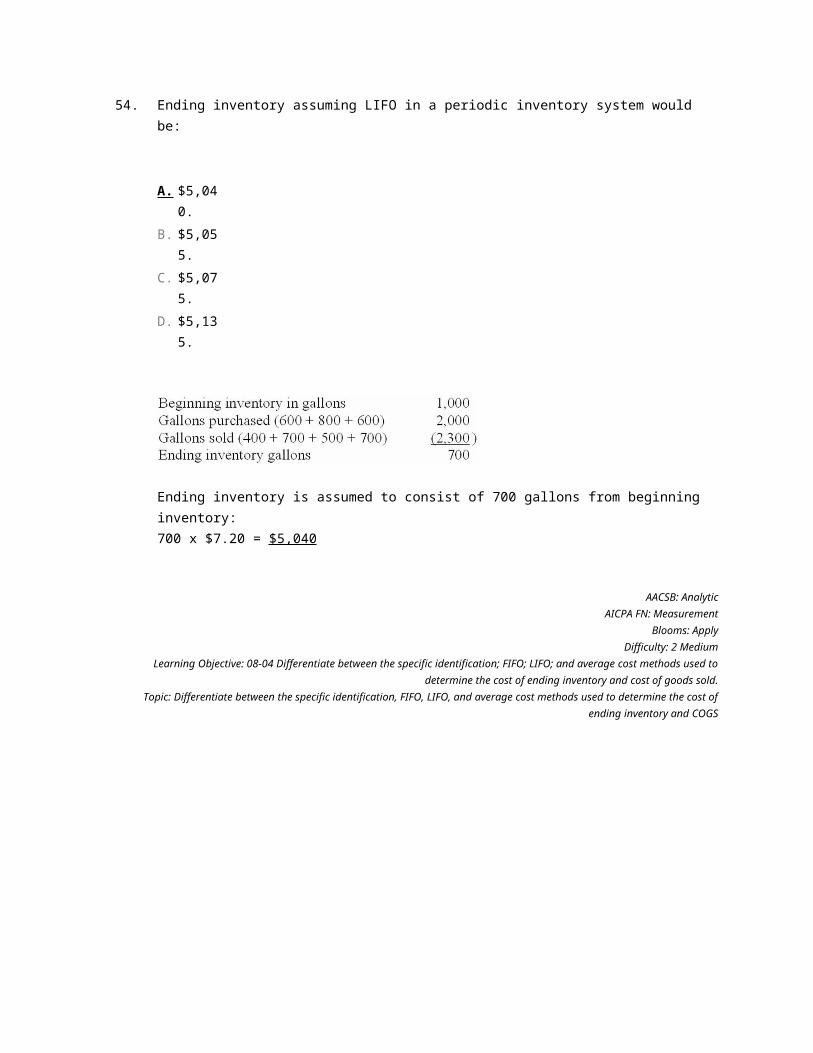

Inventory records for Herb's Chemicals revealed the following:

March 1, 2013, inventory: 1,000 gallons @ $7.20 = $7,200

54. Ending inventory assuming LIFO in a periodic inventory system would be:

A. $5,040.

B. $5,055.

C. $5,075.

D. $5,135.

55. Ending inventory assuming LIFO in a perpetual inventory system would be:

A. $4,960.

B. $5,060.

C. $5,080.

D. $5,140.

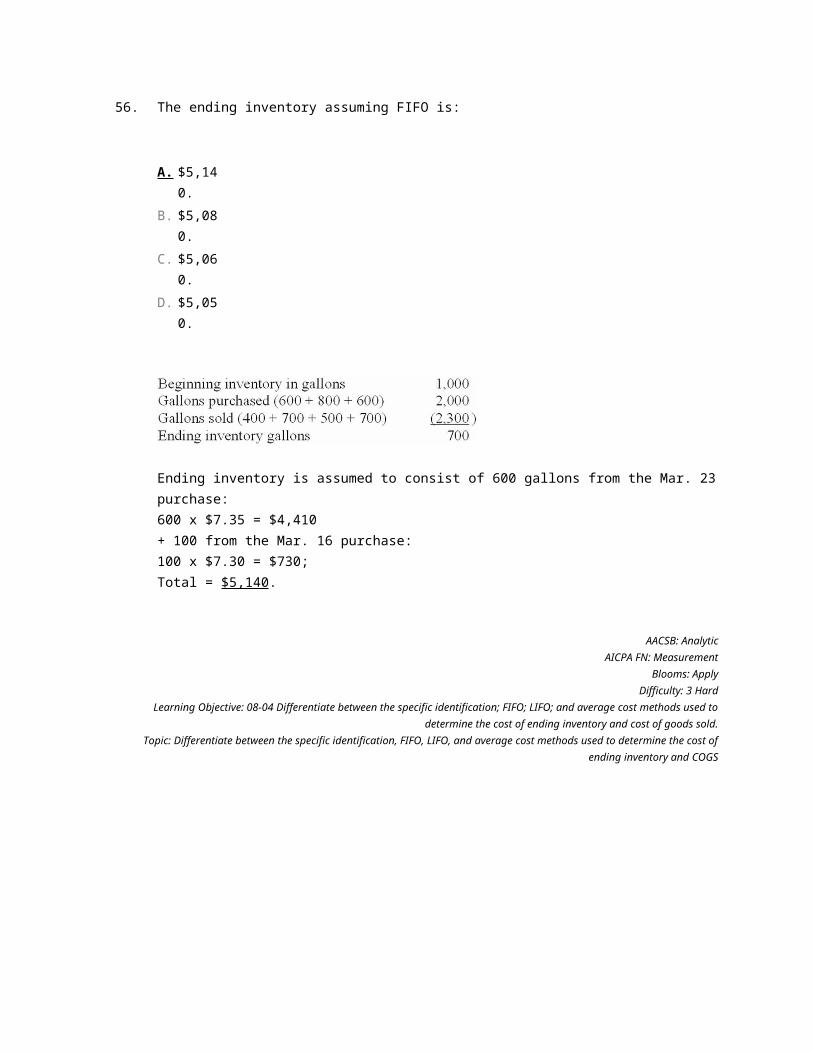

56. The ending inventory assuming FIFO is:

A. $5,140.

B. $5,080.

C. $5,060.

D. $5,050.

57. The ending inventory under a periodic inventory system assuming average cost

(rounding unit cost to three decimal places) is:

A. $5,087.

B. $5,107.

C. $5,077.

D. $5,005.

Texas Petrochemical reported the following April activity for its VC-30 lubricant, which had a balance of 300 qts. @ $2.40 on April 1.

58. The ending inventory assuming LIFO and a periodic inventory system is:

A. $1,580.

B. $1,510.

C. $1,575.

D. $1,470.

59. The ending inventory assuming LIFO and a perpetual inventory system is:

A. $1,545.

B. $1,470.

C. $1,580.

D. $1,510.

60. The use of LIFO in accounting for a firm's inventory:

A. Usually matches the physical flow of goods through the business.

B. Is usually used for internal management purposes.

C. Usually provides a better match of expenses with revenues.

D. None of the above is correct.

61. In a period when costs are falling and inventory quantities are stable, the lowest taxable income would be reported by using the inventory method of:

A. Weighted average.

B. LIFO.

C. Moving average.

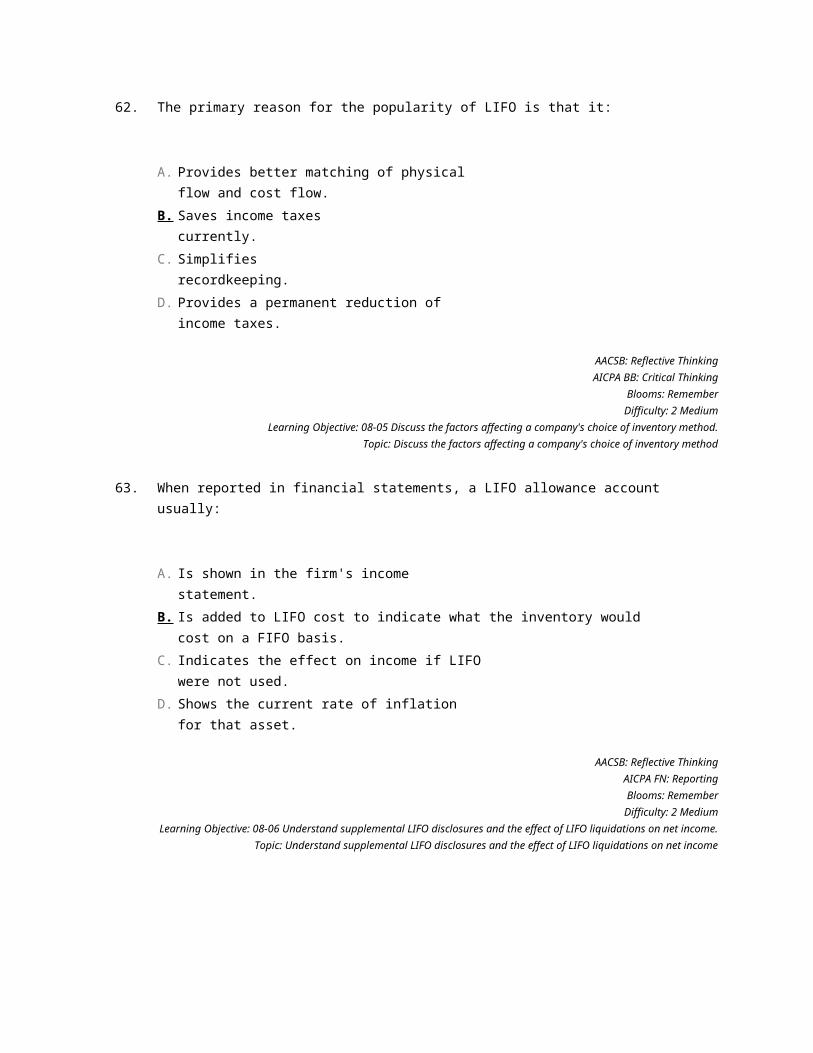

D. FIFO. 62. The primary reason for the popularity of LIFO is that it:

A. Provides better matching of physical flow and cost flow.

B. Saves income taxes currently.

C. Simplifies recordkeeping.

D. Provides a permanent reduction of income taxes.

63. When reported in financial statements, a LIFO allowance account usually:

A. Is shown in the firm's income statement.

B. Is added to LIFO cost to indicate what the inventory would cost on a FIFO basis.

C. Indicates the effect on income if LIFO were not used.

D. Shows the current rate of inflation for that asset.

64. If a company uses LIFO, a LIFO liquidation is problematic for a company's income taxes:

A. When inventory purchase costs are rising.

B. When inventory purchase costs are declining.

C. Whether inventory purchase costs are declining or rising.

D. LIFO liquidations are not problematic for a company's income taxes.

65. GG Inc. uses LIFO. GG disclosed that if FIFO had been used, inventory at the end of

2013 would have been $15 million higher than the difference between LIFO and FIFO at the end of 2012. Assuming GG has a 40% income tax rate:

A. Its reported cost of goods sold for 2013 would have been $9 million higher if it had used FIFO rather than LIFO for its financial statements.

B. Its reported cost of goods sold for 2013 would have been $15 million higher if it had used FIFO rather than LIFO for its financial statements.

C. Its reported net income for 2013 would have been $9 million higher if it had used FIFO rather than LIFO for its financial statements.

D. Its reported net income for 2013 would have been $15 million higher if it had used FIFO rather than LIFO for its financial statements.

66. HH Company uses LIFO. HH disclosed that if FIFO had been used, inventory at the end

of 2013 would have been $20 million lower than the difference between LIFO and FIFO at the end of 2012. Assuming HH has a 30% income tax rate:

A. Its reported cost of goods for 2013 would have been $14 million less if it had used FIFO rather than LIFO for its financial statements.

B. Its reported cost of goods for 2013 would have been $20 million less if it had used FIFO rather than LIFO for its financial statements.

C. Its reported cost of goods sold for 2013 would have been $14 million higher if it had used FIFO rather than LIFO for its financial statements.

D. Its reported cost of goods sold for 2013 would have been $20 million higher if it had used FIFO rather than LIFO for its financial statements.

67. During 2013, WW Inc. reduced its LIFO eligible inventory quantities due to a problem with its major supplier. The effect of this liquidation was to increase its cost of goods sold by approximately $50 million. WW has a 40% income tax rate. If WW had not experienced these supplier problems and the resulting liquidation:

A. Its 2013 net income would have been $30 million lower because inventory purchase prices were rising.

B. Its 2013 net income would have been $30 million lower because inventory purchase prices were declining.

C. Its 2013 net income would have been $30 million higher because inventory purchase prices were rising.

D. Its 2013 net income would have been $30 million higher because inventory purchase prices were declining.

Thompson TV and Appliance reported the following in its 2013 financial statements:

68. Thompson's 2013 gross profit ratio is:

A. 25%.

B. 19%.

C. 20%.

D. None of the above is correct.

69. Thompson's 2013 inventory turnover ratio is:

A. 3.91.

B. 4.00.

C. 4.88.

D. 5.00.

70. Robertson Corporation's inventory balance was $22,000 at the beginning of the year

and $20,000 at the end. The inventory turnover ratio for the year was 6.0 and the gross profit ratio 40%. What were net sales for the year?

A. $126,000.

B. $200,000.

C. $120,000.

D. $210,000.

Anthony Thomas Candies (ATC) reported the following financial data for 2013 and 2012:

71. ATC's gross profit ratio (rounded) in 2013 is:

A. 53.4%.

B. 51.9%.

C. 50.3%.

D. None of the above is correct.

72. ATC's inventory turnover ratio for 2013 is:

A. 2.42.

B. 2.76.

C. 3.21.

D. None of the above is correct.

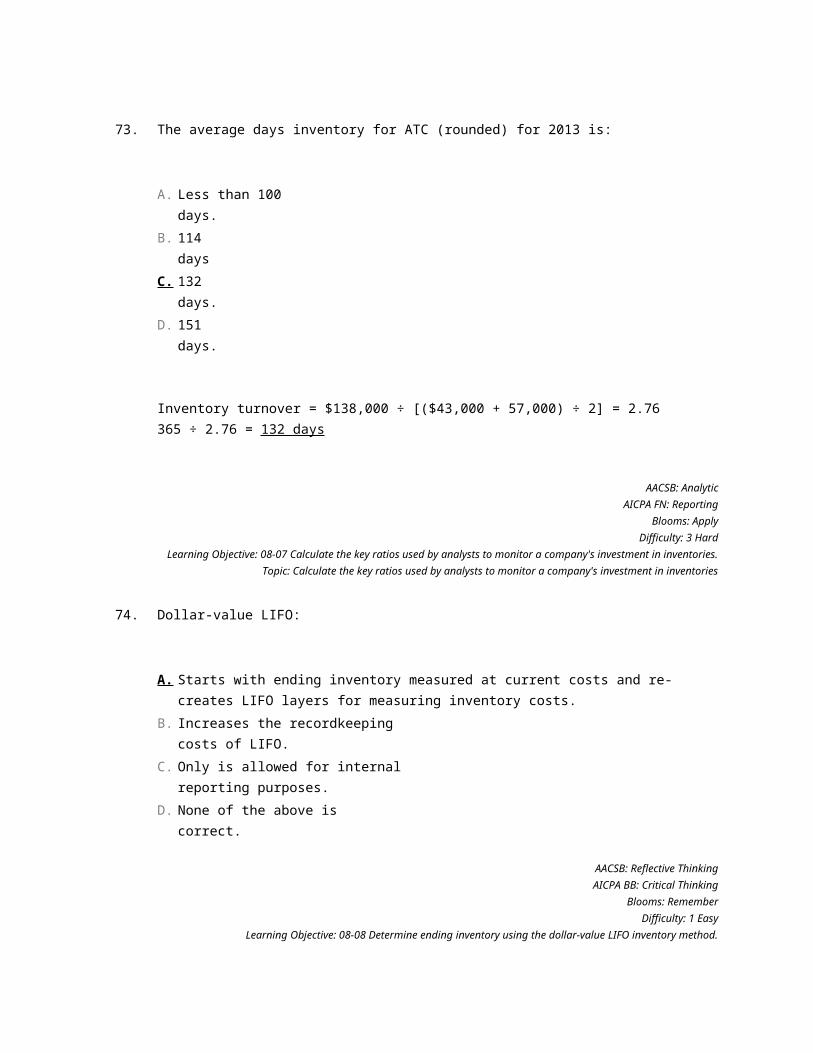

73. The average days inventory for ATC (rounded) for 2013 is:

A. Less than 100 days.

B. 114 days

C. 132 days.

D. 151 days.

74. Dollar-value LIFO:

A. Starts with ending inventory measured at current costs and re-creates LIFO layers for measuring inventory costs.

B. Increases the recordkeeping costs of LIFO.

C. Only is allowed for internal reporting purposes.

D. None of the above is correct.

75. Compared to dollar-value LIFO, unit LIFO is:

A. Less costly to implement.

B. Less susceptible to LIFO liquidation.

C. More costly to implement.

D. More concerned with cost indexes.

76. Bond Company adopted the dollar-value LIFO inventory method on January 1, 2013. In applying the LIFO method, Bond uses internal cost indexes and the multiple-pools approach. The following data were available for Inventory Pool No. 3 for the two years following the adoption of LIFO:

Under the dollar-value LIFO method, the inventory at December 31, 2014, should be

A. $357,600.

B. $350,000.

C. $351,600.

D. None of the above.

On January 1, 2013, Badger Inc. adopted the dollar-value LIFO method. The inventory cost on this date was $100,000. The 2013 ending inventory, valued at year-end costs, was $126,000. The relative cost index for this inventory in 2013 was 1.05.

77. What inventory balance should Badger report on its 12/31/13 balance sheet?

A. $126,000

B. $121,000

C. $120,000

D. $100,000

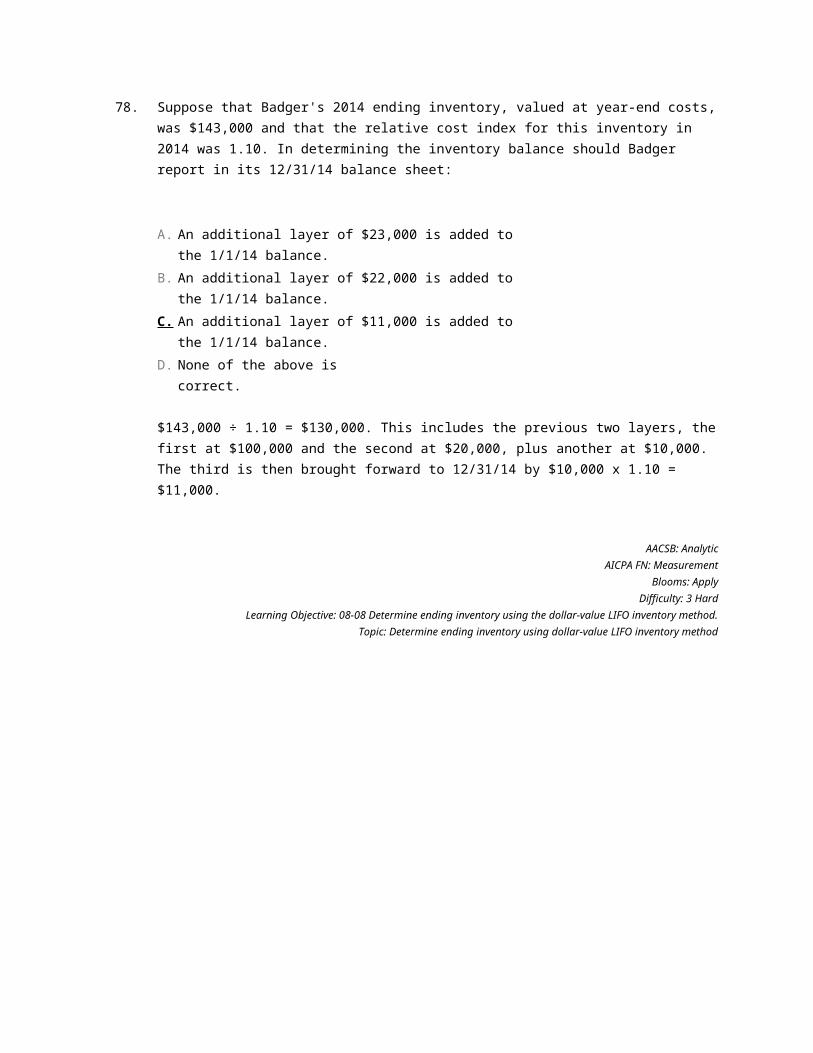

78. Suppose that Badger's 2014 ending inventory, valued at year-end costs, was $143,000 and that the relative cost index for this inventory in 2014 was 1.10. In determining the inventory balance should Badger report in its 12/31/14 balance sheet:

A. An additional layer of $23,000 is added to the 1/1/14 balance.

B. An additional layer of $22,000 is added to the 1/1/14 balance.

C. An additional layer of $11,000 is added to the 1/1/14 balance.

D. None of the above is correct.

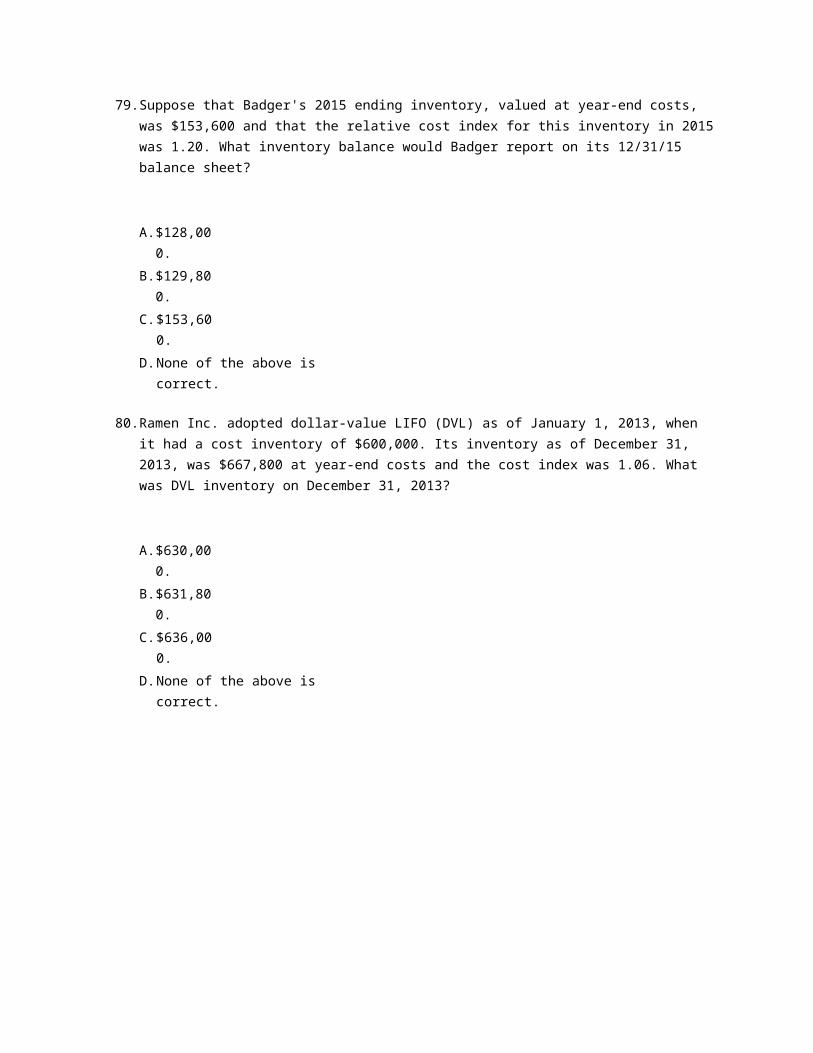

79. Suppose that Badger's 2015 ending inventory, valued at year-end costs, was

$153,600 and that the relative cost index for this inventory in 2015 was 1.20. What inventory balance would Badger report on its 12/31/15 balance sheet?

A. $128,000.

B. $129,800.

C. $153,600.

D. None of the above is correct.

80. Ramen Inc. adopted dollar-value LIFO (DVL) as of January 1, 2013, when it had a cost

inventory of $600,000. Its inventory as of December 31, 2013, was $667,800 at year-end costs and the cost index was 1.06. What was DVL inventory on December 31, 2013?

A. $630,000.

B. $631,800.

C. $636,000.

D. None of the above is correct.

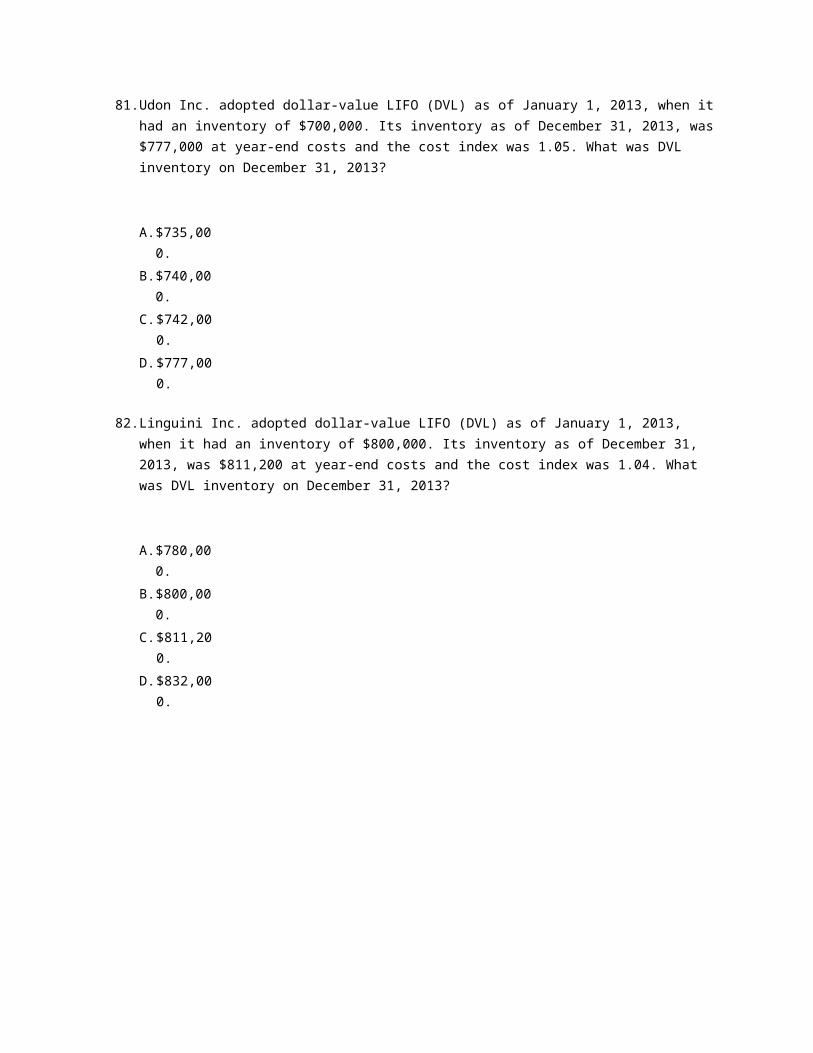

81. Udon Inc. adopted dollar-value LIFO (DVL) as of January 1, 2013, when it had an inventory of $700,000. Its inventory as of December 31, 2013, was $777,000 at year-end costs and the cost index was 1.05. What was DVL inventory on December 31, 2013?

A. $735,000.

B. $740,000.

C. $742,000.

D. $777,000.

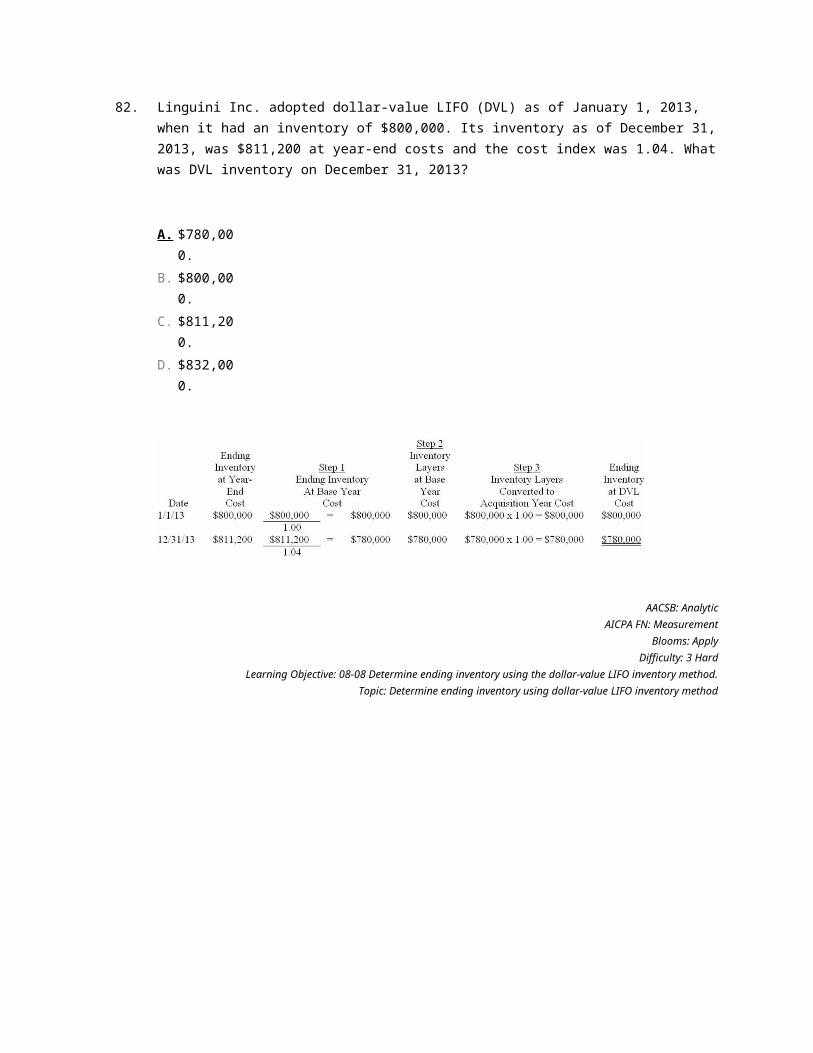

82. Linguini Inc. adopted dollar-value LIFO (DVL) as of January 1, 2013, when it had an

inventory of $800,000. Its inventory as of December 31, 2013, was $811,200 at year-end costs and the cost index was 1.04. What was DVL inventory on December 31, 2013?

A. $780,000.

B. $800,000.

C. $811,200.

D. $832,000.

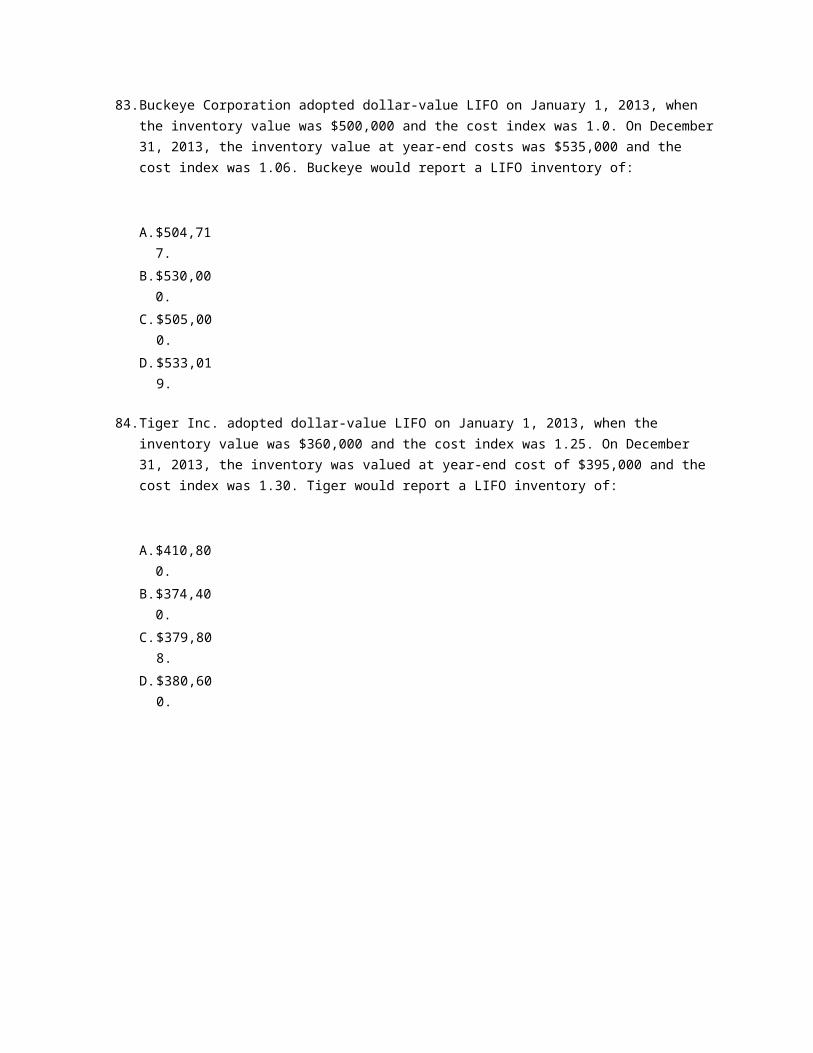

83. Buckeye Corporation adopted dollar-value LIFO on January 1, 2013, when the

inventory value was $500,000 and the cost index was 1.0. On December 31, 2013, the inventory value at year-end costs was $535,000 and the cost index was 1.06. Buckeye would report a LIFO inventory of:

A. $504,717.

B. $530,000.

C. $505,000.

D. $533,019.

84. Tiger Inc. adopted dollar-value LIFO on January 1, 2013, when the inventory value was $360,000 and the cost index was 1.25. On December 31, 2013, the inventory was valued at year-end cost of $395,000 and the cost index was 1.30. Tiger would report a LIFO inventory of:

A. $410,800.

B. $374,400.

C. $379,808.

D. $380,600.

85. A company that prepares its financial statements according to International Financial

Reporting Standards can use each of the following inventory valuation methods except:

A. Average cost.

B. FIFO.

C. LIFO.

D. All of the above methods can be used.

Matching Questions

86. Listed below are 5 terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

1. Net purchases Adjusts inventory at the end of

the period. ____2. LIFO conformity rule

LIFO must be used for financial reporting if elected for taxes. ____

3. Periodic inventory system

Reduced by discounts taken under both gross and net methods. ____

4. Finished goods Inventory ready for sale. ____5. Cost of Goods available for sale

Allocated between ending inventory and cost of goods sold. ____

87. Listed below are 5 terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. LIFO liquidation Reduces the quality of current

period earnings information. ____2. Perpetual inventory system

Units grouped according to similarities. ____

3. Freight-in Continuously records changes in

inventory. ____4. LIFO pools Considered a product cost. ____

5. Physical flow Captured by FIFO for perishable

products. ____ 88. Listed below are 5 terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. FIFO Goods are transferred to another

party but title remains with transferor. ____

2. LIFO Items sold are assumed to be those

acquired first. ____3. Cost of goods sold

Items sold are assumed to be those acquired last. ____

4. Average cost

Items sold are assumed to come from a mixture of goods acquired during the

period. ____

5. Consignment Cost of goods available for sale less

ending inventory. ____

89. Listed below are 5 terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

1. Specific identification method

Legal title passes when goods are delivered to common carrier. ____

2. F.o.b. shipping point

Not required to correspond to actual product flow. ____

3. F.o.b. destination Making sure goods in transit are

Legal title passes when goods arrive at customer location. ____

5. Inventory cut-off Not feasible for many types of

products. ____ 90. Listed below are 5 terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. Specific identification

Purchase discounts not taken are considered interest expense. ____

2. Net method Products that are not yet complete. ____3. Gross profit ratio

Purchase discounts not taken are included in inventory. ____

4. Gross method Most recent purchases will be

included in ending inventory. ____5. FIFO 1 - (Cost of goods sold ÷ Net sales). ____

91. Listed below are 5 terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. Raw materials

Used to convert ending inventory at year-end cost to base year cost. ____

2. Cost index

Could be used instead of an internally generated index in dollar-value LIFO

computations. ____3. Specific identification

Method not feasible for most inventories. ____

4. LIFO The cost of components purchased

from other manufacturers. ____5. Consumer Price Index

Most recent purchases will be included in cost of goods sold. ____

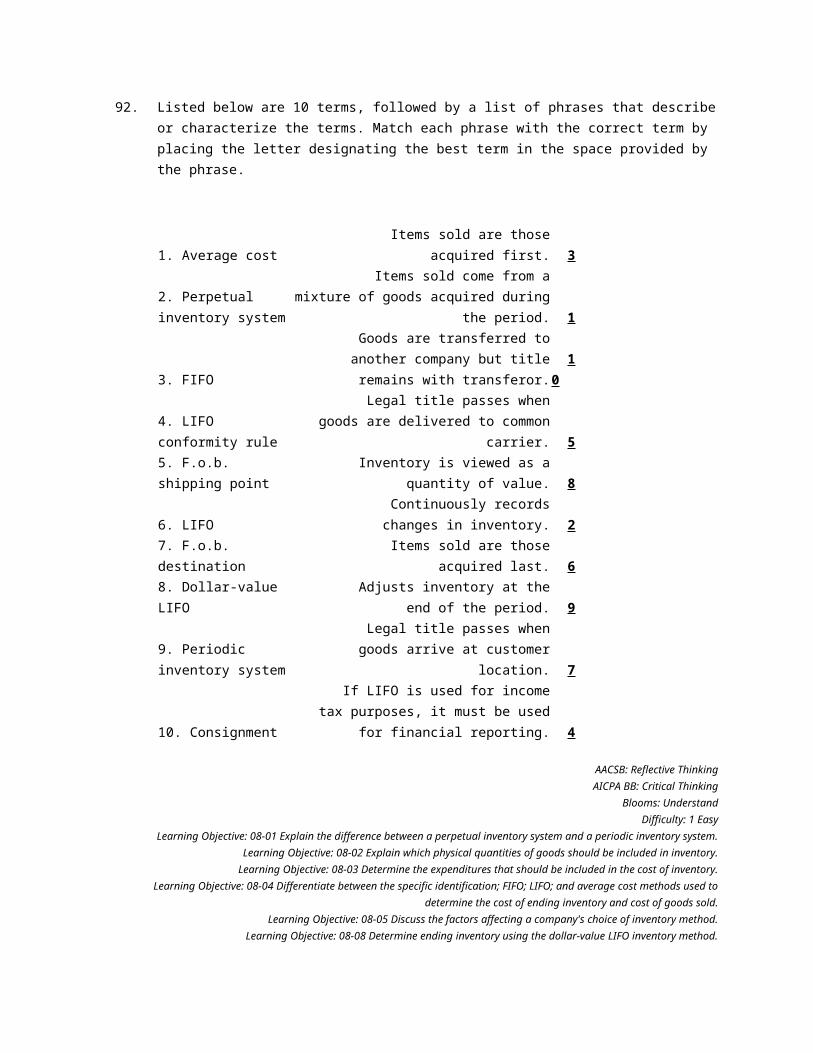

92. Listed below are 10 terms, followed by a list of phrases that describe or characterize the terms. Match each phrase with the correct term by placing the letter designating the best term in the space provided by the phrase.

1. Average cost Items sold are those acquired first. ____2. Perpetual inventory system

Items sold come from a mixture of goods acquired during the period. ____

3. FIFO

Goods are transferred to another company but title remains with

transferor. ____4. LIFO conformity rule

Legal title passes when goods are delivered to common carrier. ____

5. F.o.b. shipping point

Inventory is viewed as a quantity of value. ____

6. LIFO Continuously records changes in

inventory. ____7. F.o.b. destination Items sold are those acquired last. ____

8. Dollar-value LIFO Adjusts inventory at the end of the

period. ____9. Periodic inventory system

Legal title passes when goods arrive at customer location. ____

10. Consignment

If LIFO is used for income tax purposes, it must be used for financial

reporting. ____

Short Answer Questions

93. Bascomb Company purchased $420,000 in merchandise on account during the month of April, and merchandise costing $350,000 was sold on account for $425,000.

Required:

1. Prepare journal entries to record the purchases and sales assuming Bascomb uses a perpetual inventory system.2. Prepare journal entries to record the purchases and sales assuming Bascomb uses a periodic inventory system.

94. Meteor Co. purchased merchandise on March 4, 2013, at a price of $30,000, subject

to credit terms of 2/10, n/30. Meteor uses the net method for recording purchases and uses a periodic inventory system.

Required:

1. Prepare the journal entry to record the purchase.2. Prepare the journal entry to record the appropriate payment if the entire invoice is paid on March 11, 2013.3. Prepare the journal entry to record the appropriate payment if the entire invoice is paid on April 2, 2013.

95. Slinky Company purchased merchandise on June 10, 2013, at a price of $20,000, subject to credit terms of 2/10, n/30. Slinky uses the net method for recording purchases and uses a perpetual inventory system.

Required:

1. Prepare the journal entry to record the purchase.2. Prepare the journal entry to record the appropriate payment if the entire invoice is paid on June 18, 2013.3. Prepare the journal entry to record the appropriate payment if the entire invoice is paid on July 8, 2013.

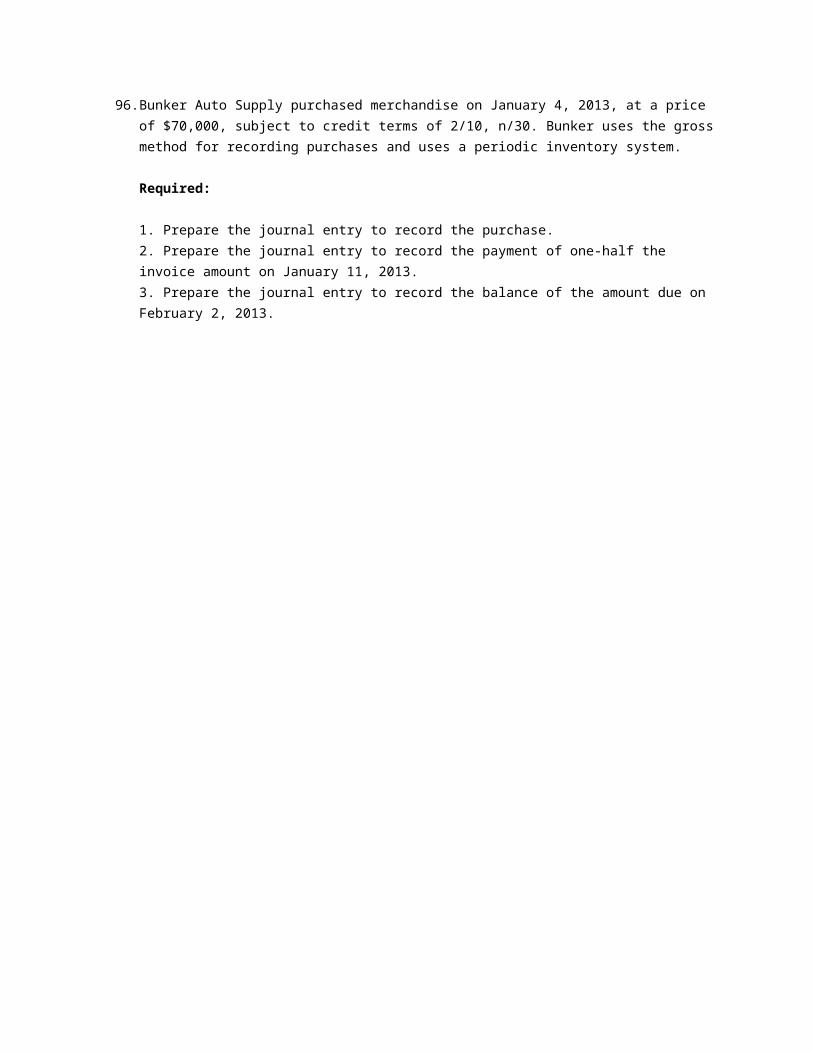

96. Bunker Auto Supply purchased merchandise on January 4, 2013, at a price of $70,000,

subject to credit terms of 2/10, n/30. Bunker uses the gross method for recording purchases and uses a periodic inventory system.

Required:

1. Prepare the journal entry to record the purchase.2. Prepare the journal entry to record the payment of one-half the invoice amount on January 11, 2013.3. Prepare the journal entry to record the balance of the amount due on February 2, 2013.

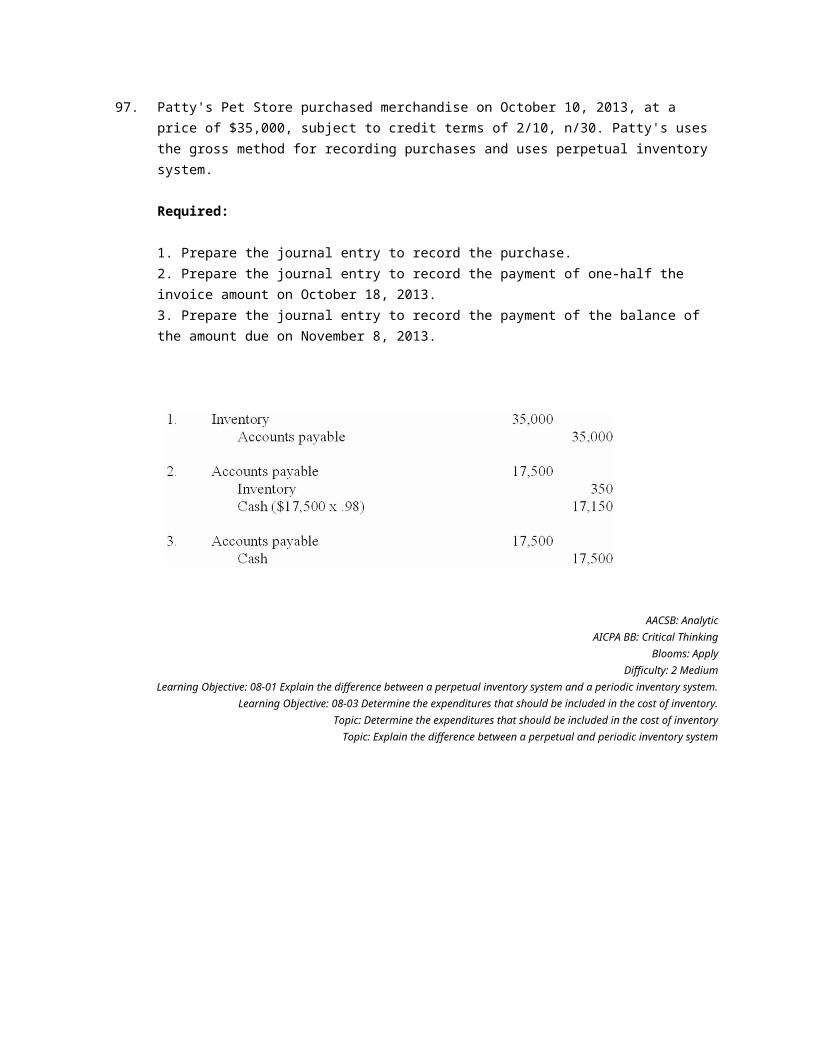

97. Patty's Pet Store purchased merchandise on October 10, 2013, at a price of $35,000, subject to credit terms of 2/10, n/30. Patty's uses the gross method for recording purchases and uses perpetual inventory system.

Required:

1. Prepare the journal entry to record the purchase.2. Prepare the journal entry to record the payment of one-half the invoice amount on October 18, 2013.3. Prepare the journal entry to record the payment of the balance of the amount due on November 8, 2013.

98. Boston Dollar Store uses the gross method to record purchase discounts and uses a

perpetual inventory system. Boston engaged in the following transactions during April:

Required:

Prepare journal entries to record the above transactions.

99. Hazelton Corporation uses a periodic inventory system and the LIFO method to value its inventory. The company began 2013 with $59,000 in inventory of its only product. The beginning inventory consisted of the following layers:

During 2013, 6,000 units were purchased at $8 per unit and during 2014, 7,000 units were purchased at $9 per unit. Sales, in units, were 7,000 and 12,000 during 2013 and 2014, respectively.

Required:

1. Calculate cost of goods sold for 2013 and 2014.2. Disregarding income tax, determine the LIFO liquidation profit or loss, if any, for 2013 and 2014.

100.

The Tucson Corporation's fiscal year ends on December 31. Tucson determines inventory quantity by a physical count of inventory on hand at the close of business on December 31. The company's controller has asked for your help in deciding if the following items should be included in the year-end inventory count.

1. Goods purchased from a vendor shipped f.o.b. shipping point on December 24 that arrived on January 4.2. Goods shipped f.o.b. shipping point on December 27 arrived at the customer's location on January 4.3. Goods purchased from a vendor shipped f.o.b. destination on December 27 that arrived on January 5.4. Freight charges on goods purchased in 1.5. Merchandise held on consignment for Masterwear, Inc.6. Goods shipped f.o.b. destination on December 29 that arrived at the customer's location on January 2.

Required:

Determine if each of the six items above should be included or excluded from the company's year-end inventory.

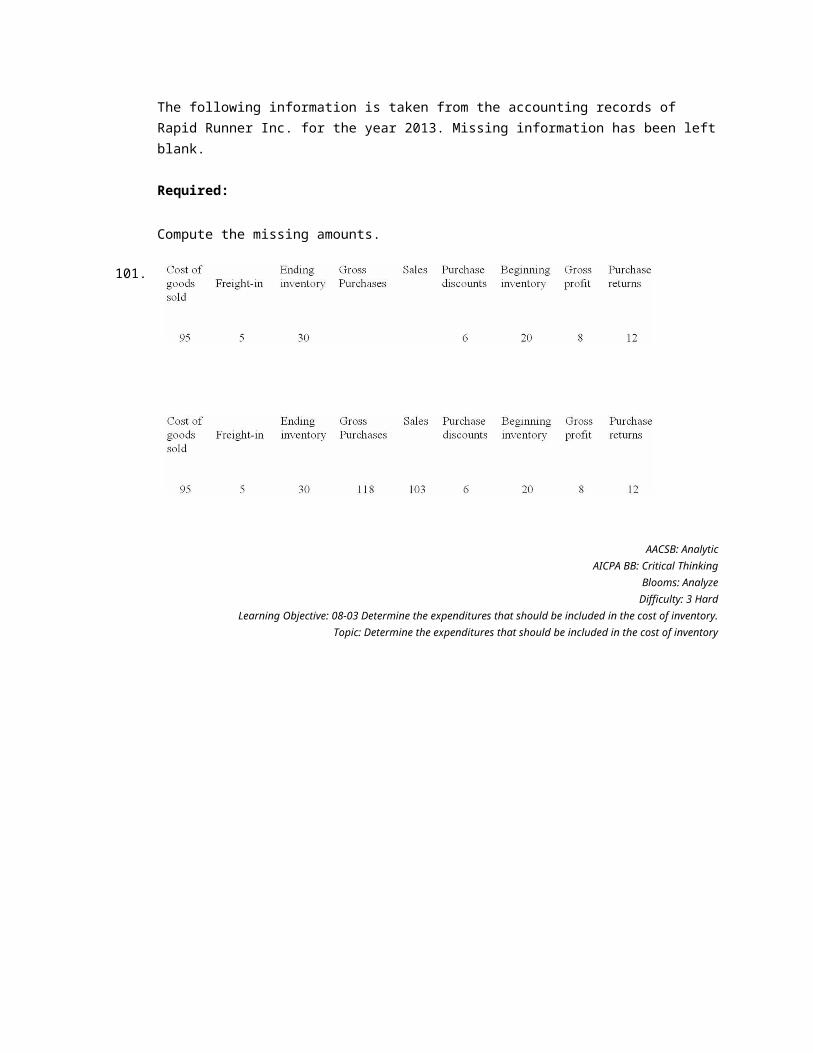

The following information is taken from the accounting records of Rapid Runner Inc. for the year 2013. Missing information has been left blank.

Required:

Compute the missing amounts.

101.

102.

103.

104.

105.

The following information is taken from the accounting records of Madeline Inc. for the year 2013. Missing information has been left blank. Inventory is the only supply that Madeline purchases on credit.

Required:

Compute the missing amounts. 106.

107.

108.

109.

110.

Shown below is activity for one of the products of Denver Office Equipment:

January 1 balance, 500 units @ $55 $27,500Purchases:

Sales:

111.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Denver uses FIFO.

112.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Denver uses LIFO and a perpetual inventory system.

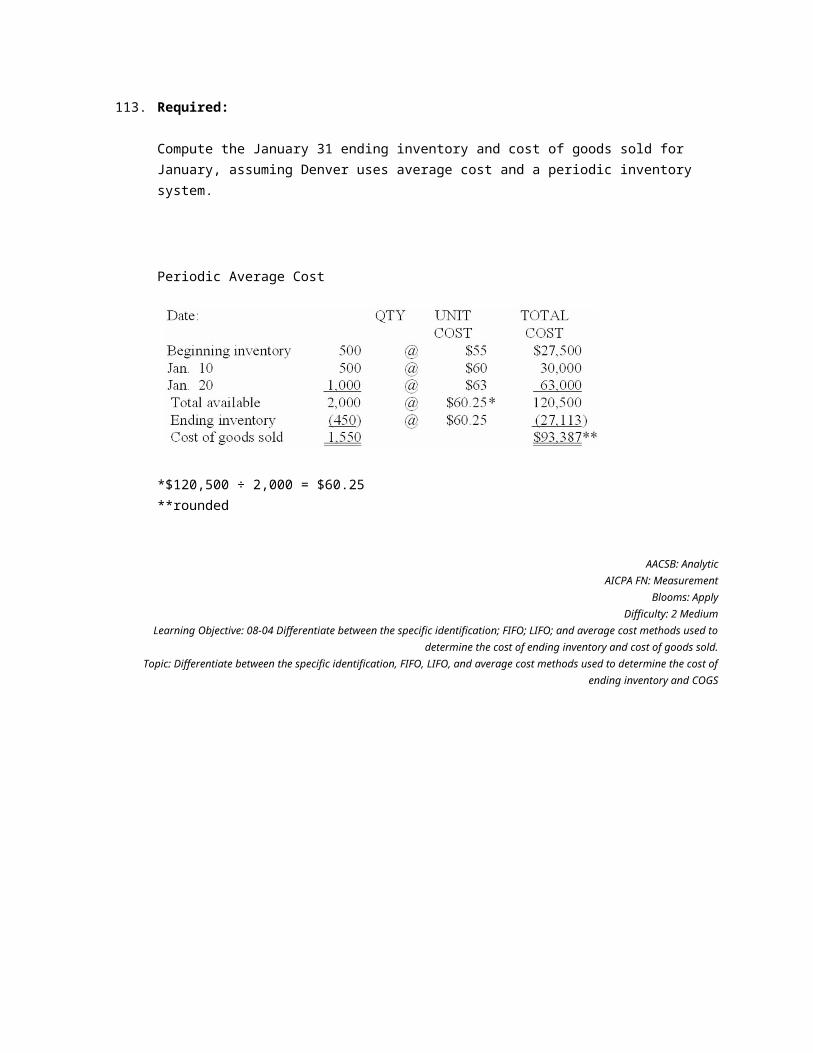

113.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Denver uses average cost and a periodic inventory system.

114.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Denver uses average cost and a perpetual inventory system.

115.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Denver uses LIFO and a periodic inventory system.

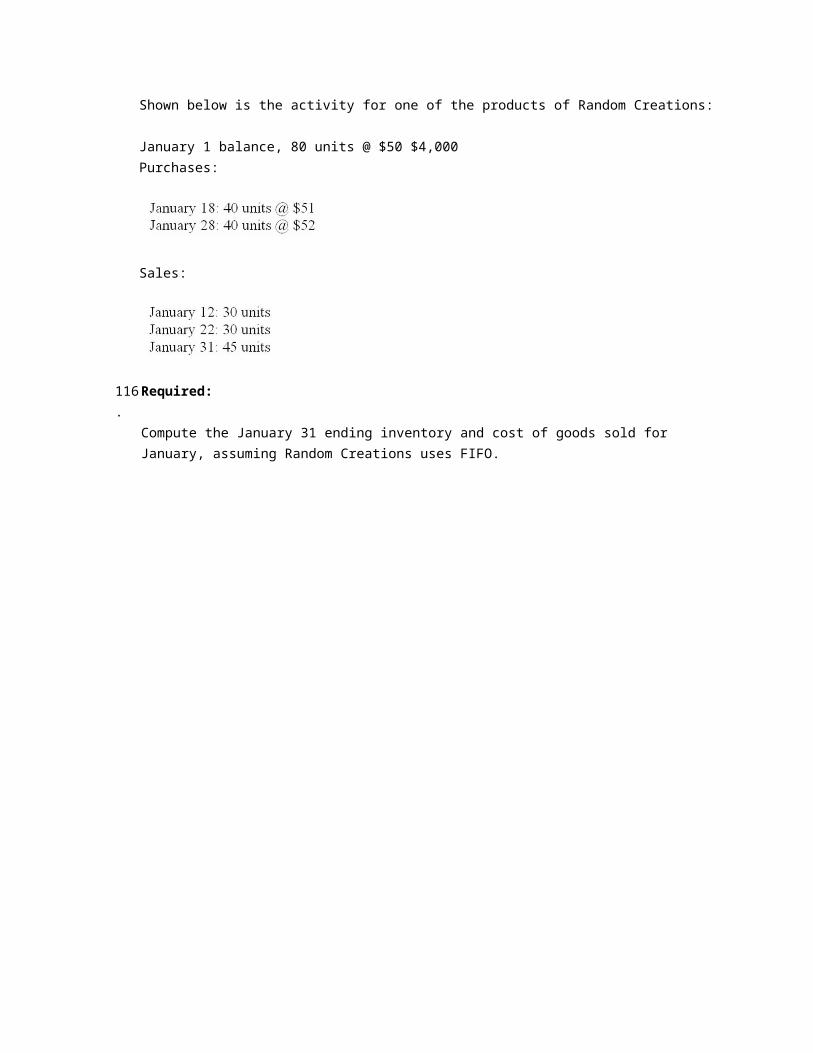

Shown below is the activity for one of the products of Random Creations:

January 1 balance, 80 units @ $50 $4,000Purchases:

Sales:

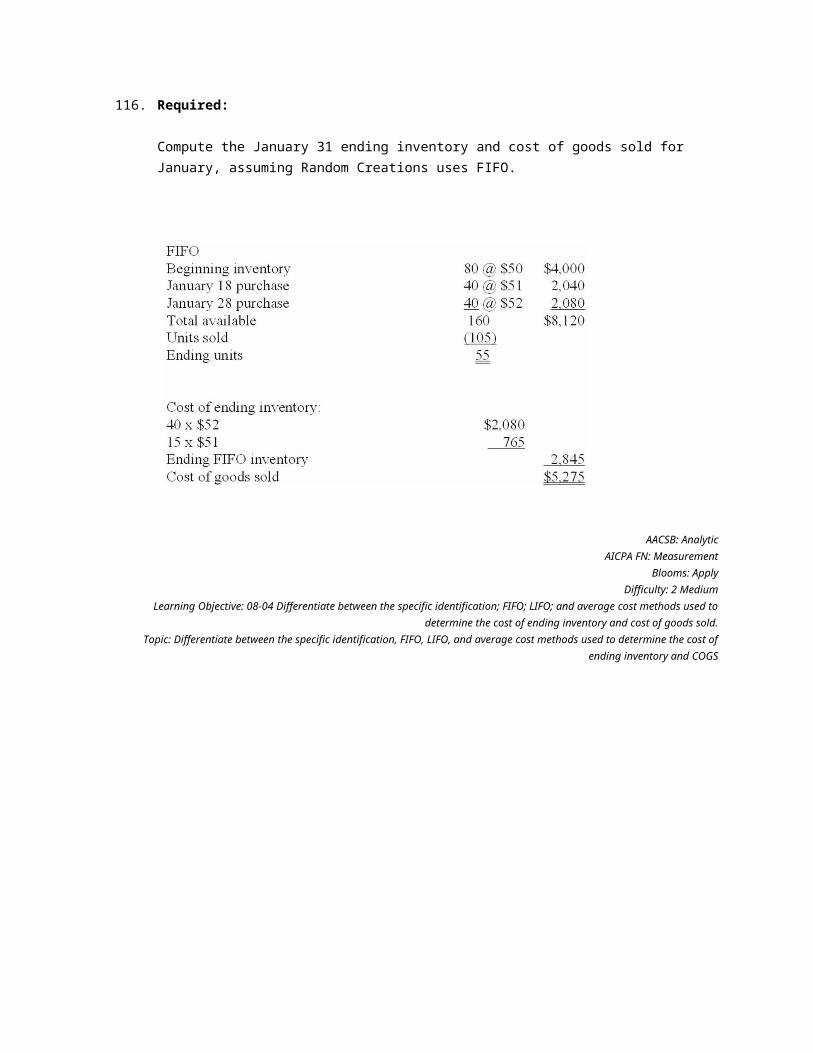

116.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Random Creations uses FIFO.

117.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Random Creations uses LIFO and perpetual inventory system.

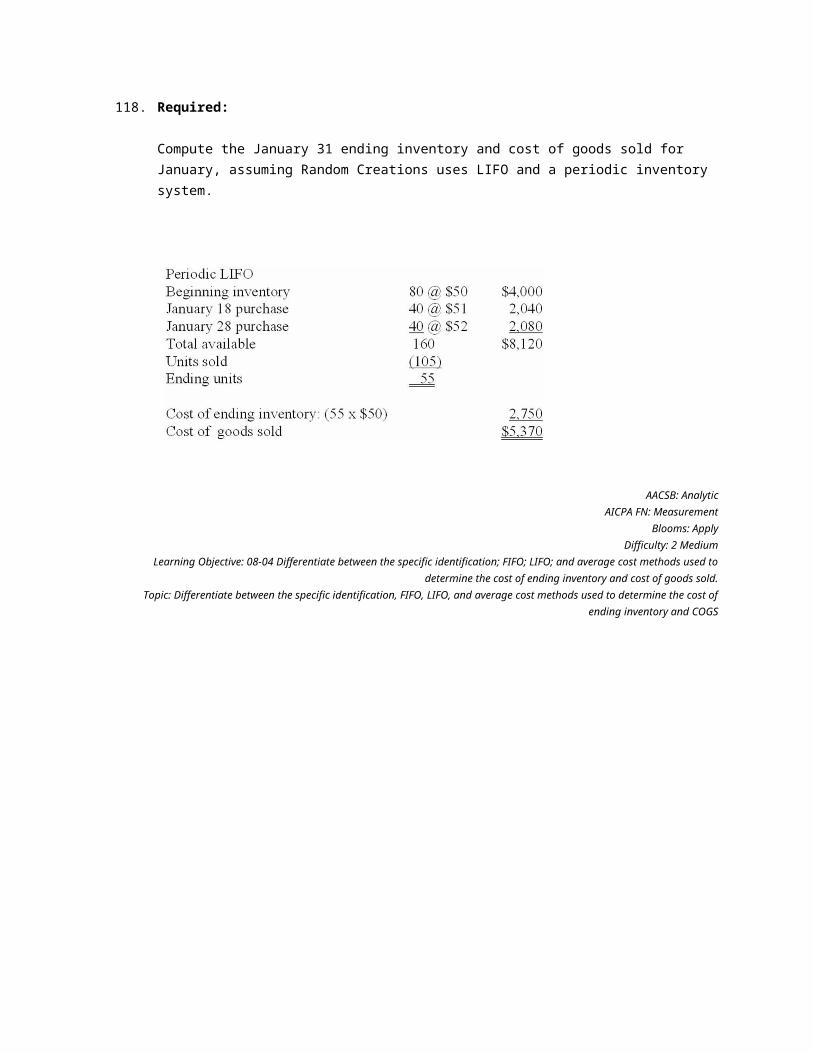

118.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Random Creations uses LIFO and a periodic inventory system.

119.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Random Creations uses average cost and a periodic inventory system.

120.

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming Random Creations uses average cost and a perpetual inventory system.

121.

Bettencourt Clothing Corporation uses a periodic inventory system and the LIFO cost method. The company began 2013 with the following inventory layers (listed in chronological order of acquisition):

During 2013, 20,000 units were purchased for $15 per unit. Sales for the year totaled 30,000 units at various prices, leaving 3,000 units in ending inventory.

Required:

1. Calculate cost of goods sold for 2013.2. Determine the amount of LIFO liquidation profit that the company must report in a disclosure note to its 2013 financial statements, assuming the amount is material. Assume an income tax rate of 40%.

122.

Modern Day Appliances, Inc. is a wholesaler of kitchen appliances. The company uses a periodic inventory system and the LIFO cost method. Modern Day's December 31, 2013, fiscal year-end inventory of its main product, double-door stainless steel refrigerators, consisted of the following (listed in chronological order of acquisition):

The replacement cost of the refrigerators throughout 2014 was $900. Modern Day sold 5,000 of these refrigerators during 2014. The company's selling price throughout 2014 was $1,200.

Required:

1. Compute the gross profit (sales minus cost of goods sold) and the gross profit ratio for 2014 assuming that Modern Day purchased 5,200 units during the year.2. Repeat requirement 1 assuming that Modern Day purchased only 4,500 units.3. For requirements 1 and 2, what amount of before-tax LIFO liquidation profit or loss would Modern Day report in its 2014 disclosure notes, if any, assuming any calculated amount is material?

123.

Selected financial statement data from Western Colorado Stores is shown below.

Required:

1. Compute the gross profit ratio for 2013.2. Compute the inventory turnover ratio for 2013.

124.

The following information comes from the 2011 American Greetings Corporation (AG) Corporation annual report to shareholders:

Inventories included the following ($ in thousands):

Inventories are valued at the lower of cost or market, with cost being determined by the LIFO method for 80% of inventories. The cost of all other inventories is determined primarily by the FIFO method. AG's cost of goods sold for 2011 was $682,368 thousand.

Required:

If AG used only FIFO for all of its inventories instead of its current policy, what would its cost of goods sold have been for 2011?

125.

The following information comes from the 2010 Occidental Petroleum Corporation annual report to shareholders:

NOTE 4 INVENTORIESNet carrying values of inventories valued under the LIFO method were approximately $177 million and $175 million at December 31, 2010 and 2009, respectively. Inventories in continuing operations consisted of the following: ($ in millions)

The LIFO reserve indicates that inventories would have been $72 million and $81 million higher at the end of 2010 and 2009, respectively, if Occidental Petroleum had used FIFO to value its entire inventory.

Required:

If Occidental Petroleum had used FIFO to value its entire inventory how would its 2010 pre-tax income be affected?

A note to the 2011 financial statements for Precision Castparts Corporation (PCC), worldwide manufacturer of complex metal components and products reveals the following:

"All inventories are stated at the lower of cost or current market values. Cost for inventories at the majority of our operations is determined on a last-in, first-out ("LIFO") basis."

Inventories consisted of the following ($ in millions):

"During fiscal 2011 and 2010, certain LIFO inventory quantities were reduced. The reductions resulted in a liquidation of LIFO inventory quantities carried at costs paid in prior years, which had the effect of increasing cost of goods sold by approximately $0.1 million in fiscal 2011 and decreasing cost of goods sold by $4.7 million in fiscal 2010 as compared with the cost of purchases in fiscal 2011 and 2010, respectively."

126.

Required:

The disclosure note indicates an inventory liquidation during 2010 and 2011. By how much did net income in 2010 increase due to the liquidation? Assume an income tax of 40%.

127.

What additional income tax payments did the 2010 liquidation cost PCC?

128.

Spando Apparel uses the LIFO inventory method for external reporting and for income tax purposes but maintains its internal records using FIFO. The following disclosure note was included in a recent annual report:

Inventories ($ in millions):

The company's income statement reported cost of goods sold of $3,120 million for the fiscal year ended December 31, 2013.

Required:

1. Spando adjusts the LIFO reserve at the end of its fiscal year. Prepare the December 31, 2013, adjusting entry to record the cost of goods sold adjustment.2. If Spando had used FIFO to value its inventories, what would cost of goods sold have been for the 2013 fiscal year?

129.

The table below contains selected financial information from recent financial statements of KBI Toys and Little Tikes Adventure Toys, Inc., two toy manufacturing companies ($ in thousands):

Required:

Calculate the 2013 gross profit ratio, inventory turnover ratio, and the average days in inventory for the two companies (rounded).

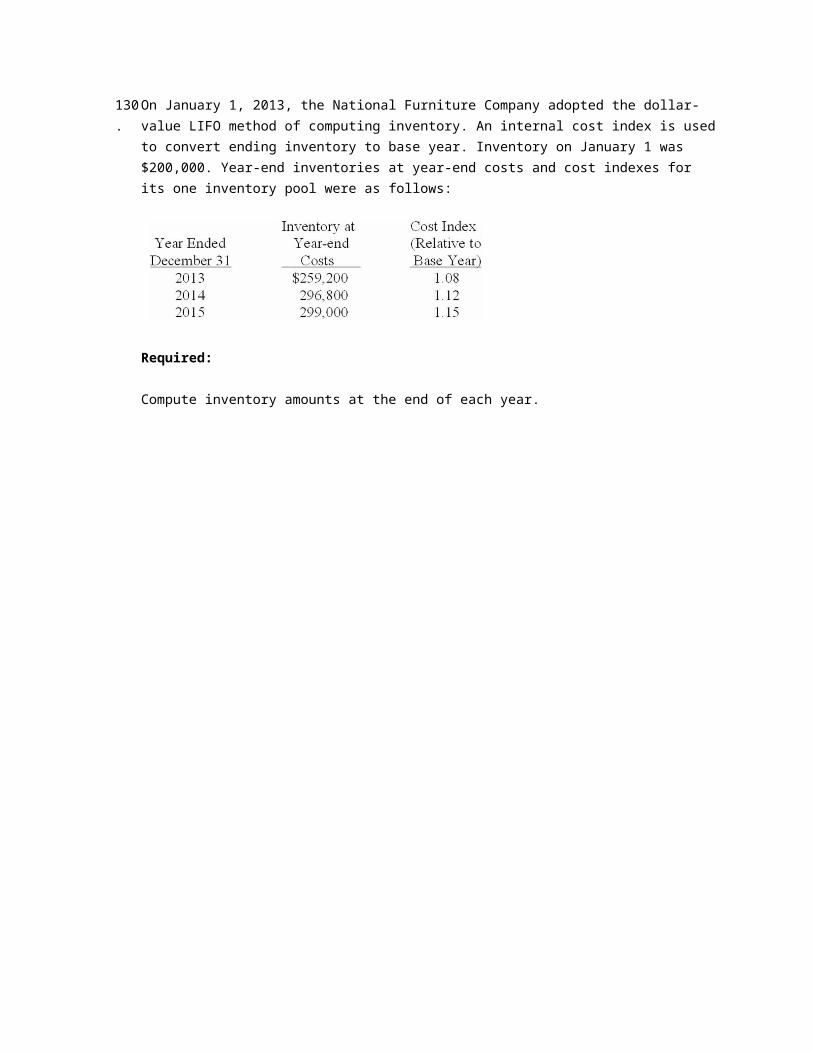

130.

On January 1, 2013, the National Furniture Company adopted the dollar-value LIFO method of computing inventory. An internal cost index is used to convert ending inventory to base year. Inventory on January 1 was $200,000. Year-end inventories at year-end costs and cost indexes for its one inventory pool were as follows:

Required:

Compute inventory amounts at the end of each year.

131.

Appleton Inc. adopted dollar-value LIFO on January 1, 2013, when the inventory value was $1,200,000. The December 31, 2013, ending inventory at year-end costs was $1,430,000 and the cost index for the year is 1.1.

Required:

Compute the dollar-value LIFO inventory valuation for the December 31, 2013, inventory.

132.

Chavez Inc adopted dollar-value LIFO on January 1, 2013, when the inventory value was $850,000. The December 31, 2013, ending inventory at year-end cost was $950,000 and the cost index for the year is 1.08.

Required:

Compute the dollar-value LIFO inventory valuation (rounded) for the December 31, 2013, inventory.

133.

Liquidated Corporation had a DVL inventory of $800,000 at the beginning of the current year when it adopted DVL. Its year-end inventory at year-end prices was $850,000. The index for the current year was 1.08.

Required:

Compute the DVL inventory (rounded) to be reported at the end of the year.

134.

On January 1, 2012, ECT Co. adopted the dollar-value LIFO method for its one inventory pool. The pool's value on this date was $600 million. The 2012 and 2013 ending inventory valued at year-end costs were $702 million and $840 million, respectively. The appropriate cost indexes are 1.08 for 2012 and 1.20 for 2013.

Required:

Calculate the inventory balance that ECT Co. would report on its year-end balance sheets for 2012 and 2013, using the dollar-value LIFO method.

135.

On January 1, 2012, RAY Co. adopted the dollar-value LIFO method for its one inventory pool. The pool's value on this date was $300 million. The 12/31/12 inventory valued at year-end costs was $385 million. The 12/31/12 inventory, using dollar-value LIFO was $355 million.

Required:

Calculate 2012 cost index for RAY's inventory.

Essay Questions

136.

Briefly describe why companies that use perpetual inventory systems must still perform physical inventories.

137.

It is the end of the accounting period, and your boss asks you to help determine the inventory balance to place in the company's balance sheet. Explain which physical quantities of inventory that you will include and which you will exclude.

138.

Briefly explain when there would be a tax benefit from electing LIFO rather than FIFO.

139.

Briefly explain how companies that use LIFO can both increase and decrease reported earnings by "managing" ending inventories.

140.

Costs and prices regularly fall every year in the microcomputer industry. Briefly indicate your recommendation and rationale for an inventory method for a firm about to enter this industry.

141.

Carmen Inc., producer of high-tech boating equipment, disclosed the following information in its 2013 annual report to shareholders:

Inventories are valued at the lower of cost or net realizable value with cost determined by the last-in, first-out (LIFO) method for inventories.

Inventories at May 31 were as follows:

If the inventory had been valued using the first-in, first-out (FIFO) method, inventories would have been higher by $22,200 and $24,400 ($ in thousands) at the end of 2013 and 2012, respectively.

How does the supplemental LIFO information indicating what the value of ending inventory would have been if measured using FIFO improve the quality of financial reporting by Carmen?

142.

Briefly explain the advantages of dollar-value LIFO (DVL).

Chapter 08 Inventories: Measurement Answer Key

True / False Questions

1. Physical counts of inventory are never done with perpetual inventory systems. FALSE

Learning Objective: 08-01 Explain the difference between a perpetual inventory system and a periodic inventory system.

Topic: Explain the difference between a perpetual and periodic inventory system

2. The main difference between perpetual and periodic inventory systems is the timing of the allocation of costs between inventory and cost of goods sold. TRUE

Learning Objective: 08-02 Explain which physical quantities of goods should be included in inventory.Topic: Explain which physical quantities of goods should be included in inventory

6. Shipping charges on outgoing goods are included in either cost of goods sold or selling expenses. TRUE

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Explain which physical quantities of goods should be included in inventory

7. Net purchases are reduced for discounts taken whether the net method is used or the gross method is used. TRUE

AACSB: Reflective Thinking

AICPA FN: MeasurementBlooms: Remember

Difficulty: 1 EasyLearning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.

Topic: Determine the expenditures that should be included in the cost of inventory

8. The choice of cost flow assumption (FIFO, LIFO, or average) does not depend on the actual physical flow of the product. TRUE

Learning Objective: 08-05 Discuss the factors affecting a company's choice of inventory method.Topic: Discuss the factors affecting a company's choice of inventory method

9. Inventory costing methods are merely means by which costs are allocated between ending inventory and cost of goods sold. TRUE

AACSB: Reflective Thinking

AICPA FN: MeasurementBlooms: Remember

Difficulty: 1 EasyLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

10. During periods of falling prices, LIFO ending inventory will be less than FIFO ending inventory. FALSE

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

11. LIFO always provides a better match of revenue and expense than does FIFO. TRUE

Learning Objective: 08-05 Discuss the factors affecting a company's choice of inventory method.Topic: Discuss the factors affecting a company's choice of inventory method

12. Unit LIFO is more costly to implement than dollar-value LIFO. TRUE

Learning Objective: 08-08 Determine ending inventory using the dollar-value LIFO inventory method.Topic: Determine ending inventory using dollar-value LIFO inventory method

16. A company that prepares its financial statements according to International Financial Reporting Standards can use all of the same inventory valuation methods as a company that prepares its statements under U.S. GAAP. FALSE

AACSB: Diversity

AACSB: Reflective ThinkingAICPA BB: Global

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 08-09 Discuss the primary difference between U.S. GAAP and IFRS with respect to determining the cost of inventory.

Topic: Discuss the primary difference between U.S. GAAP and IFRS with respect to determining the cost of inventory

Multiple Choice Questions

17. In a perpetual inventory system, the cost of purchases is debited to:

Learning Objective: 08-01 Explain the difference between a perpetual inventory system and a periodic inventory system.

Topic: Explain the difference between a perpetual and periodic inventory system

21. The inventory method that will always produce the same amount for cost of goods sold in a periodic inventory system as in a perpetual inventory system would be:

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

22. The Mateo Corporation's inventory at December 31, 2013, was $325,000 based on a physical count priced at cost, and before any necessary adjustment for the following:

▪ Merchandise costing $30,000, shipped f.o.b. shipping point from a vendor on December 30, 2013, was received on January 5, 2014.▪ Merchandise costing $22,000, shipped f.o.b. destination from a vendor on December 28, 2013, was received on January 3, 2014.▪ Merchandise costing $38,000 was shipped to a customer f.o.b. destination on December 28, arrived at the customer's location on January 6, 2014.▪ Merchandise costing $12,000 was being held on consignment by Traynor Company.

What amount should Mateo Corporation report as inventory in its December 31, 2013, balance sheet?

A. $367,000.

B. $427,000.

C. $405,000.

D. $325,000.

$325,000 + 30,000 + 38,000 + 12,000 = 405,000

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-02 Explain which physical quantities of goods should be included in inventory.

Topic: Explain which physical quantities of goods should be included in inventory

23. Ending inventory is equal to the cost of items on hand plus:

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Determine the expenditures that should be included in the cost of inventory

24. Purchases equal the invoice amount:

A. Plus freight-in, plus discounts lost.

B. Less purchase returns, plus purchase allowances.

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Determine the expenditures that should be included in the cost of inventory

25. Using the gross method, purchase discounts lost are:

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Determine the expenditures that should be included in the cost of inventory

26. Under the net method, purchase discounts lost are:

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Determine the expenditures that should be included in the cost of inventory

27. Inventory does not include:

A. Materials used in the production of goods to be sold.

B. Assets intended to be sold in the normal course of business.

C. The cost of office equipment.

D. Assets currently in production for normal sales.

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Determine the expenditures that should be included in the cost of inventory

28. Under the gross method, purchase discounts taken are:

Learning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.Topic: Determine the expenditures that should be included in the cost of inventory

29. Alison's dress shop buys dresses from McGuire Manufacturing. Alison purchased dresses from McGuire on July 17 and received an invoice with a list price amount of $6,000 and payment terms of 2/10, n/30. Alison uses the net method to record purchases. Alison should record the purchase at:

A. $5,940.

B. $5,880.

C. $6,000.

D. $6,120.

$6,000 x 98% = $5,880.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.

Topic: Determine the expenditures that should be included in the cost of inventory

Northwest Fur Co. started 2013 with $94,000 of merchandise inventory on hand. During 2013, $400,000 in merchandise was purchased on account with credit terms of 1/15, n/45. All discounts were taken. Purchases were all made f.o.b. shipping point. Northwest paid freight charges of $7,500. Merchandise with an invoice amount of $5,000 was returned for credit. Cost of goods sold for the year was $380,000. Northwest uses a perpetual inventory system.

30. What is ending inventory assuming Northwest uses the gross method to record purchases?

A. $112,490.

B. $112,550.

C. $116,500.

D. $120,300.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.

Topic: Determine the expenditures that should be included in the cost of inventory

31. Assuming Northwest uses the gross method to record purchases, what is the cost of goods available for sale?

A. $492,500.

B. $496,500.

C. $490,500.

D. $492,550.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.

Topic: Determine the expenditures that should be included in the cost of inventory

Cinnamon Buns Co. (CBC) started 2013 with $52,000 of merchandise on hand. During 2013, $280,000 in merchandise was purchased on account with credit terms of 2/10, n/30. All discounts were taken. Purchases were all made f.o.b. shipping point. CBC paid freight charges of $9,000. Merchandise with an invoice amount of $4,000 was returned for credit. Cost of goods sold for the year was $316,000. CBC uses a perpetual inventory system.

32. Assuming CBC uses the gross method to record purchases, ending inventory would be:

A. $6,480.

B. $15,400.

C. $15,480.

D. $21,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.

Topic: Determine the expenditures that should be included in the cost of inventory

33. What is cost of goods available for sale, assuming CBC uses the gross method?

A. $312,480.

B. $326,000.

C. $331,480.

D. $337,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-03 Determine the expenditures that should be included in the cost of inventory.

Topic: Determine the expenditures that should be included in the cost of inventory

34. Cost of goods sold is given by:

A. Beginning inventory - net purchases + ending inventory.

B. Beginning inventory + accounts payable - net purchases.

C. Net purchases + ending inventory - beginning inventory.

D. Net Purchases + beginning inventory - ending inventory.

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

35. The LIFO Conformity Rule states that if LIFO is used for:

A. One class of inventory, it must be used for all classes of inventory.

B. Tax purposes, it must be used for financial reporting.

C. One company in an affiliated group, it must be used by all companies in an affiliated group.

D. Domestic companies, it must be used by foreign partners.

AACSB: Reflective Thinking

AICPA FN: ReportingBlooms: Remember

Difficulty: 1 EasyLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

36. The largest expense on a retailer's income statement is typically:

A. Salaries and wages.

B. Cost of goods sold.

C. Income tax expense.

D. Depreciation expense.

AACSB: Reflective Thinking

AICPA FN: ReportingBlooms: Understand

Difficulty: 1 EasyLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

37. In a perpetual average cost system:

A. A new weighted-average unit cost is calculated each time additional units are purchased.

B. The cost allocated to ending inventory is generally the same as it would be in a periodic inventory system.

C. The moving-average unit cost is determined following each sale.

D. The average is determined by dividing the total number of units sold by the cost of units purchased during the period.

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

38. In a period when costs are rising and inventory quantities are stable, the inventory method that would result in the highest ending inventory is:

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

39. During periods when costs are rising and inventory quantities are stable, cost of goods sold will be:

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

40. During periods when costs are rising and inventory quantities are stable, ending inventory will be:

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

41. In periods when costs are rising, LIFO liquidations:

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

43. Company A is identical to Company B in every regard except that Company A uses FIFO and Company B uses LIFO. In an extended period of rising inventory costs, Company A's gross profit and inventory turnover ratio, compared to Company B's, would be:

A. Option a

B. Option b

C. Option c

D. Option d

AACSB: Analytic

AICPA BB: Critical ThinkingBlooms: UnderstandDifficulty: 2 Medium

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

44. Company C is identical to Company D in every respect except that Company C uses LIFO and Company D uses average costs. In an extended period of rising inventory costs, Company C's gross profit and inventory turnover ratio, compared to Company D's, would be:

A. Option a

B. Option b

C. Option c

D. Option d

AACSB: Analytic

AICPA BB: Critical ThinkingBlooms: UnderstandDifficulty: 2 Medium

Learning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost methods used to determine the cost of ending inventory and cost of goods sold.

Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and COGS

Fulbright Corp. uses the periodic inventory system. During its first year of operations, Fulbright made the following purchases (listed in chronological order of acquisition):

• 40 units at $100• 70 units at $80• 170 units at $60

Sales for the year totaled 270 units, leaving 10 units on hand at the end of the year.

45. Ending inventory using the average cost method (rounded) is:

A. $650.

B. $1,000.

C. $707.

D. $600.

[(40 x $100) + (70 x $80) + (170 x $60)] = $19,800 ÷ 280 units = $70.71 per unit 10 units x $70.71 = $707 (rounded)

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

46. Ending inventory using the FIFO method is:

A. $650.

B. $1,000.

C. $707.

D. $600.

10 units x $60 = $600.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

47. Ending inventory using the LIFO method is:

A. $650.

B. $1,000.

C. $707.

D. $600.

10 units x $100 = $1,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

Nu Company reported the following pretax data for its first year of operations.

48. What is Nu's net income if it elects FIFO?

A. $480.

B. $288.

C. $1,360.

D. $144.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

49. What is Nu's net income if it elects LIFO?

A. $288.

B. $144.

C. $240.

D. $480.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

50. What is Nu's gross profit ratio if it elects LIFO?

A. 80%.

B. 49%.

C. 40%.

D. 5%.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-07 Calculate the key ratios used by analysts to monitor a company's investment in

inventories.Topic: Inventory Management

Nueva Company reported the following pretax data for its first year of operations.

51. What is Nueva's gross profit ratio (rounded) if it elects FIFO?

A. 30%.

B. 32%.

C. 10.7%.

D. 60%.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-07 Calculate the key ratios used by analysts to monitor a company's investment in

inventories.Topic: Calculate the key ratios used by analysts to monitor a company's investment in inventories

52. What is Nueva's net income if it elects FIFO?

A. $440.

B. $264.

C. $620.

D. $372.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

53. What is Nueva's net income if it elects LIFO?

A. $440.

B. $264.

C. $620.

D. $372.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

Inventory records for Herb's Chemicals revealed the following:

March 1, 2013, inventory: 1,000 gallons @ $7.20 = $7,200

54. Ending inventory assuming LIFO in a periodic inventory system would be:

A. $5,040.

B. $5,055.

C. $5,075.

D. $5,135.

Ending inventory is assumed to consist of 700 gallons from beginning inventory:700 x $7.20 = $5,040

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

55. Ending inventory assuming LIFO in a perpetual inventory system would be:

A. $4,960.

B. $5,060.

C. $5,080.

D. $5,140.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

56. The ending inventory assuming FIFO is:

A. $5,140.

B. $5,080.

C. $5,060.

D. $5,050.

Ending inventory is assumed to consist of 600 gallons from the Mar. 23 purchase:600 x $7.35 = $4,410+ 100 from the Mar. 16 purchase:100 x $7.30 = $730;Total = $5,140.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

57. The ending inventory under a periodic inventory system assuming average cost (rounding unit cost to three decimal places) is:

A. $5,087.

B. $5,107.

C. $5,077.

D. $5,005.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

Texas Petrochemical reported the following April activity for its VC-30 lubricant, which had a balance of 300 qts. @ $2.40 on April 1.

58. The ending inventory assuming LIFO and a periodic inventory system is:

A. $1,580.

B. $1,510.

C. $1,575.

D. $1,470.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

59. The ending inventory assuming LIFO and a perpetual inventory system is:

A. $1,545.

B. $1,470.

C. $1,580.

D. $1,510.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-04 Differentiate between the specific identification; FIFO; LIFO; and average cost

methods used to determine the cost of ending inventory and cost of goods sold.Topic: Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine

the cost of ending inventory and COGS

60. The use of LIFO in accounting for a firm's inventory:

A. Usually matches the physical flow of goods through the business.

B. Is usually used for internal management purposes.

C. Usually provides a better match of expenses with revenues.

Learning Objective: 08-05 Discuss the factors affecting a company's choice of inventory method.Topic: Discuss the factors affecting a company's choice of inventory method

61. In a period when costs are falling and inventory quantities are stable, the lowest taxable income would be reported by using the inventory method of:

Learning Objective: 08-05 Discuss the factors affecting a company's choice of inventory method.Topic: Discuss the factors affecting a company's choice of inventory method

62. The primary reason for the popularity of LIFO is that it:

A. Provides better matching of physical flow and cost flow.

B. Saves income taxes currently.

C. Simplifies recordkeeping.

D. Provides a permanent reduction of income taxes.

Learning Objective: 08-05 Discuss the factors affecting a company's choice of inventory method.Topic: Discuss the factors affecting a company's choice of inventory method

63. When reported in financial statements, a LIFO allowance account usually:

A. Is shown in the firm's income statement.

B. Is added to LIFO cost to indicate what the inventory would cost on a FIFO basis.

C. Indicates the effect on income if LIFO were not used.

D. Shows the current rate of inflation for that asset.

AACSB: Reflective Thinking

AICPA FN: ReportingBlooms: RememberDifficulty: 2 Medium

Learning Objective: 08-06 Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income.

Topic: Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income

64. If a company uses LIFO, a LIFO liquidation is problematic for a company's income taxes:

A. When inventory purchase costs are rising.

B. When inventory purchase costs are declining.

C. Whether inventory purchase costs are declining or rising.

D. LIFO liquidations are not problematic for a company's income taxes.

When costs are rising, a liquidation causes pre-tax income and income taxes to rise.

Learning Objective: 08-06 Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income.

Topic: Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income

65. GG Inc. uses LIFO. GG disclosed that if FIFO had been used, inventory at the end of 2013 would have been $15 million higher than the difference between LIFO and FIFO at the end of 2012. Assuming GG has a 40% income tax rate:

A. Its reported cost of goods sold for 2013 would have been $9 million higher if it had used FIFO rather than LIFO for its financial statements.

B. Its reported cost of goods sold for 2013 would have been $15 million higher if it had used FIFO rather than LIFO for its financial statements.

C. Its reported net income for 2013 would have been $9 million higher if it had used FIFO rather than LIFO for its financial statements.

D. Its reported net income for 2013 would have been $15 million higher if it had used FIFO rather than LIFO for its financial statements.

This is (1 - tax rate) x the pre-tax effect of $15 million.

AACSB: Analytic

AICPA FN: ReportingBlooms: Create

Difficulty: 3 HardLearning Objective: 08-06 Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net

income.Topic: Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income

66. HH Company uses LIFO. HH disclosed that if FIFO had been used, inventory at the end of 2013 would have been $20 million lower than the difference between LIFO and FIFO at the end of 2012. Assuming HH has a 30% income tax rate:

A. Its reported cost of goods for 2013 would have been $14 million less if it had used FIFO rather than LIFO for its financial statements.

B. Its reported cost of goods for 2013 would have been $20 million less if it had used FIFO rather than LIFO for its financial statements.

C. Its reported cost of goods sold for 2013 would have been $14 million higher if it had used FIFO rather than LIFO for its financial statements.

D. Its reported cost of goods sold for 2013 would have been $20 million higher if it had used FIFO rather than LIFO for its financial statements.

AACSB: Analytic

AICPA FN: ReportingBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-06 Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net

income.Topic: Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income

67. During 2013, WW Inc. reduced its LIFO eligible inventory quantities due to a problem with its major supplier. The effect of this liquidation was to increase its cost of goods sold by approximately $50 million. WW has a 40% income tax rate. If WW had not experienced these supplier problems and the resulting liquidation:

A. Its 2013 net income would have been $30 million lower because inventory purchase prices were rising.

B. Its 2013 net income would have been $30 million lower because inventory purchase prices were declining.

C. Its 2013 net income would have been $30 million higher because inventory purchase prices were rising.

D. Its 2013 net income would have been $30 million higher because inventory purchase prices were declining.

The effect of WW's LIFO liquidation was a reduction in pre-tax income by $50 million and a reduction in net income by $30 million. This would have been avoided if the supplier problems had been avoided. The inventory prices were declining because the effect of using older inventory prices was to increase cost of goods sold.

AACSB: Analytic

AICPA FN: ReportingBlooms: Create

Difficulty: 3 Hard

Learning Objective: 08-06 Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income.

Topic: Understand supplemental LIFO disclosures and the effect of LIFO liquidations on net income

Thompson TV and Appliance reported the following in its 2013 financial statements:

68. Thompson's 2013 gross profit ratio is:

A. 25%.

B. 19%.

C. 20%.

D. None of the above is correct.

$84,000 ÷ $420,000 = 20%

AACSB: Analytic

AICPA FN: ReportingBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-07 Calculate the key ratios used by analysts to monitor a company's investment in

inventories.Topic: Calculate the key ratios used by analysts to monitor a company's investment in inventories

69. Thompson's 2013 inventory turnover ratio is:

A. 3.91.

B. 4.00.

C. 4.88.

D. 5.00.

$336,000 ÷ [($82,000 + 86,000) ÷ 2] = 4.00

AACSB: Analytic

AICPA FN: ReportingBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-07 Calculate the key ratios used by analysts to monitor a company's investment in

inventories.Topic: Calculate the key ratios used by analysts to monitor a company's investment in inventories

70. Robertson Corporation's inventory balance was $22,000 at the beginning of the year and $20,000 at the end. The inventory turnover ratio for the year was 6.0 and the gross profit ratio 40%. What were net sales for the year?

A. $126,000.

B. $200,000.

C. $120,000.

D. $210,000.

Average inventory = $21,000 x 6.0 = $126,000 = cost of goods sold$126,000 ÷ (1 - .40) = $210,000

AACSB: Analytic

AICPA FN: ReportingBlooms: Apply

Difficulty: 3 HardLearning Objective: 08-07 Calculate the key ratios used by analysts to monitor a company's investment in

inventories.Topic: Calculate the key ratios used by analysts to monitor a company's investment in inventories

Anthony Thomas Candies (ATC) reported the following financial data for 2013 and 2012:

71. ATC's gross profit ratio (rounded) in 2013 is:

A. 53.4%.

B. 51.9%.

C. 50.3%.

D. None of the above is correct.

$158,000 ÷ $296,000 = 53.4%

AACSB: Analytic

AICPA FN: ReportingBlooms: Apply

Difficulty: 2 MediumLearning Objective: 08-07 Calculate the key ratios used by analysts to monitor a company's investment in

inventories.Topic: Calculate the key ratios used by analysts to monitor a company's investment in inventories

72. ATC's inventory turnover ratio for 2013 is: