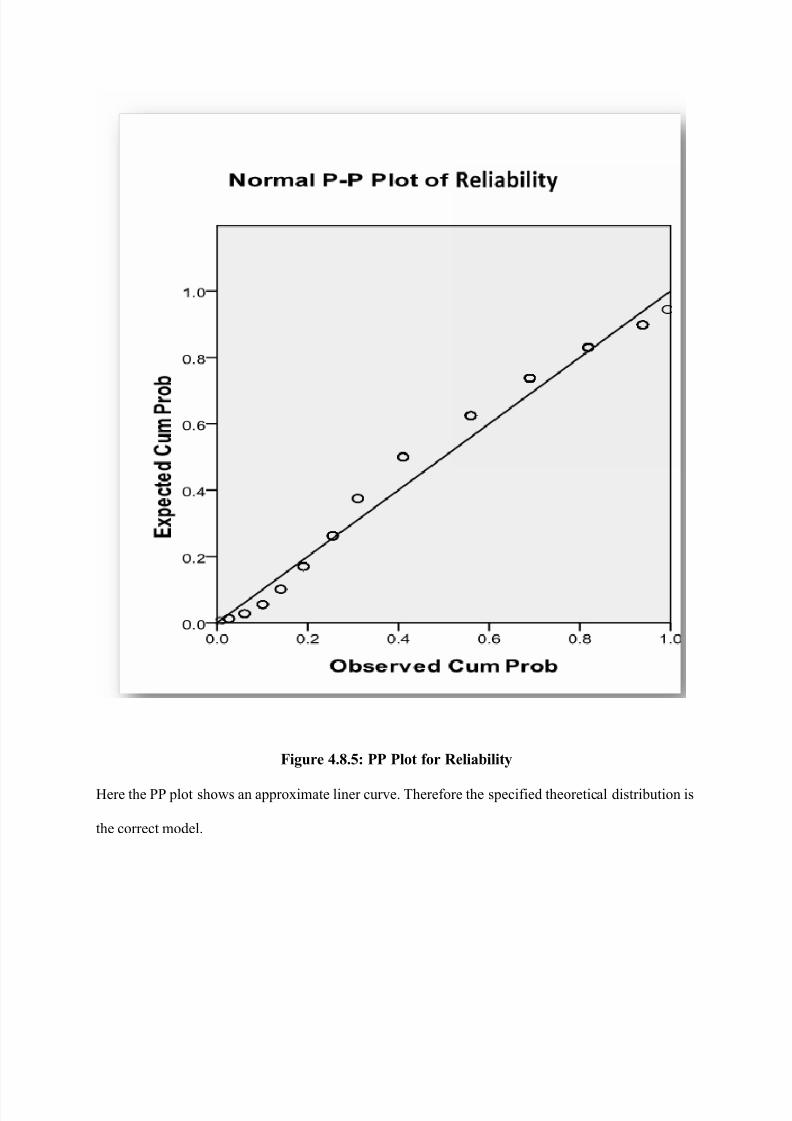

4.1. DESCRIPTIVE STATISTICSFor the research, descriptive statistics include the numbers, charts and graphs used to describe, organize and present data on each variable. For the research eight variables were determined: Lenders trustworthy, Assurance of Credit Risk, Requirement, types of loan, New Loans, Loans against documentary bills payment, factor for providing a customer loan, significant is dependent variables. Values of the variables were derived after averaging three questions under each variable. Mean, standard deviation, variance, minimum & maximum value for each value is shown in the following table. TABLE 1: Descriptive Statistics of all variables Descriptive Statistics N Minimum Maximum Mean Std. Devia tion Variance MEAN of Lenders Trustworthy 100 2.29 4.43 3.6714 .44323 .196 MEAN of Assurance ofCredit Risk100 2.00 4.83 3.5183 .53070 .282 MEAN of Credit Analysis 100 1.60 4.80 3.6480 .65697 .432 MEAN of Consideration Factor100 1.60 4.60 3.4440 .59396 .353 MEAN of Significance 100 2.50 4.67 3.8333 .52384 .274 Valid N (list wise) 100 This table provides the basic statistical information about the data set, such as showing the mean response for average of five questions for each variable individual questions and its deviation from the mean. For this information, for instance we find that the among the 100 participants 72were male and 28 were female which is 72% male & 28% female. Participants of the research came from various age groups. Age range of the participants is 20 to above 40. But most of the participants belongs to the age group 25 -34 & 31 -35. These descriptive statistics of the entire data set has been represented in Table 1 (given in Appendix). 4.2. Frequency distribution and charts Graphical representation of data and frequency distribution :

Transcript

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 1/56

4.1. DESCRIPTIVE STATISTICS

For the research, descriptive statistics include the numbers, charts and graphs used to describe,

organize and present data on each variable. For the research eight variables were determined:

Lenders trustworthy, Assurance of Credit Risk, Requirement, types of loan, New Loans, Loans

against documentary bills payment, factor for providing a customer loan, significant is dependent

variables. Values of the variables were derived after averaging three questions under each

variable. Mean, standard deviation, variance, minimum & maximum value for each value is

shown in the following table.

TABLE 1: Descriptive Statistics of all variables

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation Variance

MEAN of Lenders

Trustworthy

100 2.29 4.43 3.6714 .44323 .196

MEAN of Assurance of

Credit Risk

100 2.00 4.83 3.5183 .53070 .282

MEAN of Credit Analysis 100 1.60 4.80 3.6480 .65697 .432

MEAN of Consideration

Factor

100 1.60 4.60 3.4440 .59396 .353

MEAN of Significance 100 2.50 4.67 3.8333 .52384 .274

Valid N (list wise) 100

This table provides the basic statistical information about the data set, such as showing the mean

response for average of five questions for each variable individual questions and its deviation

from the mean. For this information, for instance we find that the among the 100 participants

72were male and 28 were female which is 72% male & 28% female. Participants of the research

came from various age groups. Age range of the participants is 20 to above 40. But most of the

participants belongs to the age group 25 -34 & 31 -35. These descriptive statistics of the entire

data set has been represented in Table 1 (given in Appendix).

4.2. Frequency distribution and charts

Graphical representation of data and frequency distribution:

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 2/56

Table4.2.1: Gender of the respondents

Frequency Percent Valid Percent Cumulative Percent

Valid Male 72 72.0 72.0 72.0

Female 28 28.0 28.0 100.0

Total 100 100.0 100.0

Figure 4.2.1: Diagram showing the frequency distribution of gender

There were 100 respondents of which 72 were male and 28 were female. These respondents are

all employees and customers in BASIC Bank Limited from various departments in various

branches.

From the various branches we found that the numbers of male employees are more than the

female employees.

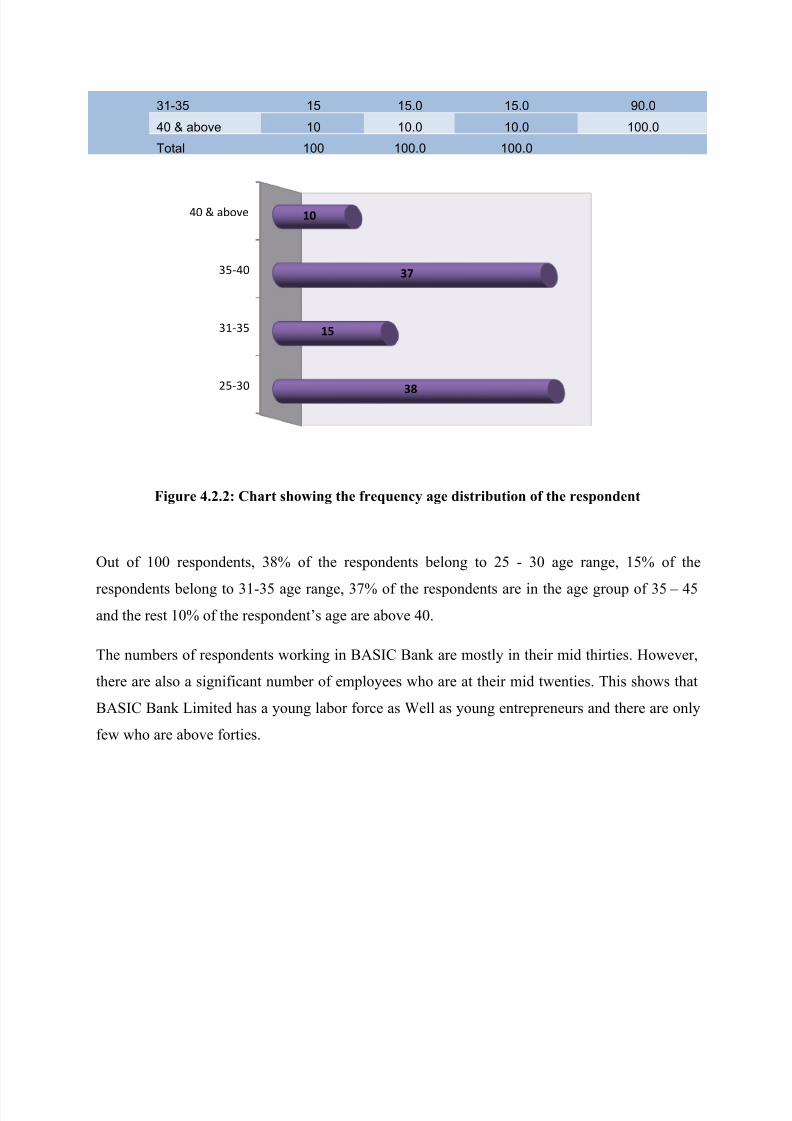

Table 4.2.2: Respondents Age Distribution

Frequency Percent Valid Percent Cumulative Percent

Valid

25-30 38 38.0 38.0 38.0

35-40 37 37.0 37.0 75.0

72

28

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 3/56

31-35 15 15.0 15.0 90.0

40 & above 10 10.0 10.0 100.0

Total 100 100.0 100.0

Figure 4.2.2: Chart showing the frequency age distribution of the respondent

Out of 100 respondents, 38% of the respondents belong to 25 - 30 age range, 15% of the

respondents belong to 31-35 age range, 37% of the respondents are in the age group of 35 – 45

and the rest 10% of the respondent’s age are above 40.

The numbers of respondents working in BASIC Bank are mostly in their mid thirties. However,

there are also a significant number of employees who are at their mid twenties. This shows that

BASIC Bank Limited has a young labor force as Well as young entrepreneurs and there are only

few who are above forties.

38

15

37

10

25-30

31-35

35-40

40 & above

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 4/56

Figure 4.2.3: Chart showing the frequency Educational background distribution of the

respondents

Of the respondents 29% of above respondents education background are science, 27% are from

commerce education background, 31% respondents are from Arts, and 10% are vocational and

others 3%.

Employees of BASIC bank Limited are from various educational backgrounds. From the 50

sample size, 16 employees are from Arts, Science and Commerce are almost same 14 and 13

each. Only a few employees are from vocational and others types of educational background.

29

27

31

10

3

0

5

10

15

20

25

30

35

0 1 2 3 4 5 6

Table 4.2.3: Respondents Educational background

Frequency Percent Valid Percent Cumulative Percent

Valid

science 29 29.0 29.0 29.0

commerce 27 27.0 27.0 56.0 Arts 31 31.0 31.0 87.0

vocational 10 10.0 10.0 97.0

others 3 3.0 3.0 100.0

Total 50 100.0 100.0

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 5/56

Table 4.2.5: Lenders Potential

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 5 10.0 10.0 10.0

Disagree 19 38.0 38.0 48.0

Neutral 14 28.0 28.0 76.0

agree 7 14.0 14.0 90.0

strongly agree 5 10.0 10.0 100.0

Total 50 100.0 100.0

Figure 4.2.5: Showing the frequency distribution of Lenders Potential

Of the 50 respondents 10% strongly agreed to the satisfaction in the current IT system used in the

current process, 14% agreed, 28% are neutral about the satisfaction with the IT system, 38%

disagreed that there is no satisfaction and 10% strongly disagreed.

0

5

10

15

20

25

30

35

40

strongly

Disagree

Disagree Neutral agree strongly

agree

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 6/56

Most of the employees are unconcerned about the Lenders potential. Although a significant

number of employees are satisfied with their current process they use. It is because, employees

aren’t aware of the different method or software used in the job.

Figure 4.2.6: Showing the frequency distribution of Lenders Honesty

Of the 100 respondents 20% strongly agreed to the current process, 56% agreed, 12% are neutral

about the satisfaction with the existing method system while 10% disagreed and thought they

shouldn’t take it as a and 2% strongly disagreed.

0

10

20

30

40

50

60

strongly

DisagreeDisagree

Neutralagree

strongly

agree

Table4.2.6: Lenders Honesty

Frequency Percent Valid Percent Cumulative

Percent

Valid strongly Disagree 1 2.0 2.0 2.0

Disagree 5 10.0 10.0 12.0

Neutral 6 12.0 12.0 24.0

agree 28 56.0 56.0 80.0

strongly agree 10 20.0 20.0 100.0

Total 50 100.0 100.0

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 7/56

Maximum no. of employees is not satisfied with the existing system. There is a significant no. of

employees think the Existing system could hinder employees’ productivity.

Figure 4.2.7: Showing the frequency distribution of Asset and Liability

Of the 100 respondents 22% strongly agreed that the current method by the management used decrease

overall efficiency, 52% agreed, 12% are neutral with the current process, 8% disagreed that Existing

system does not decrease overall efficiency and 5% strongly disagreed.

6

812

52

22

0

10

20

30

40

50

60

strongly

Disagree

Disagree Neutral agree strongly agree

Table 4.2.7: Asset and Liability

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 3 6.0 6.0 6.0

Disagree 4 8.0 8.0 14.0

Neutral 6 12.0 12.0 26.0

agree 26 52.0 52.0 78.0

strongly agree 11 22.0 22.0 100.0

Total 50 100.0 100.0

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 8/56

According to a large number of respondents, they are not happy with the liability. They think that existing

liability decrease overall efficiency.

Figure 4.2.8: Showing the frequency distribution of Profitability

Of the respondents 34% strongly agreed to the improvement of profitability is needed when

examining a new client, 42% agreed, 10% are neutral, 12% disagreed that there is no need to

change that formula and 2% strongly disagreed.

strongly Disagree,

1

Disagree, 6

Neutral, 5

agree, 21

strongly agree, 17

Table 4.2.8: Profitability

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 1 2.0 2.0 2.0

Disagree 6 12.0 12.0 14.0

Neutral 5 10.0 10.0 24.0

agree 21 42.0 42.0 66.0

strongly agree 17 34.0 34.0 100.0

Total 50 100.0 100.0

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 9/56

Majority of the employees said that the practice used in their current system doesn’t need to be

improved. However, a significant number of employees feel the need of improvement in their

current structure.

Figure 4.2.9: Showing the frequency distribution of Timely Repayment

Of the respondents 26% strongly agreed to the timely repayment is needed to ensure granting

further sanction, 44% agreed, 18% are neutral about the improvement, 8% disagreed that there is

no need for enhancement and 4% strongly disagreed.

4

8

18

44

26

0

5

10

15

20

25

30

35

40

45

50

strongly

Disagree

Disagree Neutral agree strongly agree

Table4.2.9: Timely Repayment

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 2 4.0 4.0 4.0

Disagree 4 8.0 8.0 12.0

Neutral 9 18.0 18.0 30.0

agree 22 44.0 44.0 74.0

strongly agree 13 26.0 26.0 100.0

Total 50 100.0 100.0

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 10/56

Most of the employees said that timely repayment method can be improved if there is an

improvement loan processing. It is because the current system used by the employees of BASIC

Bank Limited isn’t satisfactory for which their skills aren’t able to enhance.

Figure 4.2.10: Showing the frequency distribution of Supervision

Of the respondents 32% strongly agreed to perform effectively by saving time, 36% agreed, 14%

are neutral about the performance, 10% disagreed that the current system helps to perform

effectively and 7% strongly disagreed.

8

10

14

3632

0

5

10

15

20

25

30

35

40

strongly

Disagree

Disagree Neutral agree strongly agree

Table 4.2.10: Supervision

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 4 8.0 8.0 8.0

Disagree 5 10.0 10.0 18.0

Neutral 7 14.0 14.0 32.0

agree 18 36.0 36.0 68.0

strongly agree 16 32.0 32.0 100.0

Total 50 100.0 100.0

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 11/56

From the graph, it can be seen that most of the employees believe that improvement in

supervision doesn’t help them to perform effectively by saving time. It is because they are not

aware of other method of doing the work. Hence, the employees don’t know the effect of

business process reengineering on the performance of their work.

Table 4.2.11: Monitoring

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 4 4.0 4.0 4.0

Disagree 4 8.0 8.0 12.0

Neutral 9 18.0 18.0 30.0

agree 24 48.0 48.0 78.0

strongly agree 11 22.0 22.0 100.0

Total 50 100.0 100.0

Figure 4.2.11: Showing the frequency distribution of Monitoring

Of the respondents 22% strongly agreed to perform efficiently by minimizing errors monitoring

frequently, 48% agreed, 18% are neutral about the performance, 7% disagreed that monitoring

frequently helps to perform efficiently and 4% strongly disagreed.

48

18

48

22

0

5

10

15

20

25

30

35

40

45

50

0 1 2 3 4 5 6

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 12/56

From the graph, it can be seen that most of the employees believe that improvement in

monitoring process doesn’t help them to perform efficiently by minimizing errors. It is because

they are not aware of other method of doing the work. Hence, the employees don’t know the

effect of business process reengineering on the performance of their work.

Table 4.2.12: Credit Policy

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 7 14.0 14.0 14.0

Disagree 20 40.0 40.0 54.0

Neutral 10 20.0 20.0 74.0

agree 10 20.0 20.0 94.0

strongly agree 3 6.0 6.0 100.0

Total 50 100.0 100.0

Figure 4.2.12: Showing the frequency distribution of Credit Policy

Of the respondents 6% strongly agreed of their satisfaction with the credit policy they maintain

in the current process, 20% agreed, 20% are neutral about the satisfaction, 40% disagreed with it

and 14% strongly disagreed.

14

20

20

20

6

0 10 20 30 40 50

strongly Disagree

Disagree

Neutral

agree

strongly agree

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 13/56

It can be seen from the graph that the employees aren’t satisfied with credit policy and it needs

reengineering in the current process. The employees believe that there is a need of more strict

policy in their current process in order to enhance their work performance.

Table 4.2.13: Credit Procedure

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 2 4.0 4.0 4.0

Disagree 8 16.0 16.0 20.0

Neutral 7 14.0 14.0 34.0

agree 22 44.0 44.0 78.0

strongly agree 11 22.0 22.0 100.0

Total 50 100.0 100.0

Figure 4.2.13: Showing the frequency distribution of Credit Procedure

Of the respondents 22% strongly agreed to the need of Credit Procedure in the unit, 44% agreed,

14% are neutral about the satisfaction, 16% disagreed with more number of skilled employees

and 4% strongly disagreed.

0

10

20

30

40

50

strongly

DisagreeDisagree

Neutralagree

strongly

agree

416

14

44

22

7/29/2019 8.Stat

http://slidepdf.com/reader/full/8stat 14/56

Majority of the employees agreed and disagreed to the need of more of Credit procedure in the

unit. It maybe because the current employees find addition of new employees to the work as a

threat to their job and other welcomes the help of more techniques as they believe it can enhance

the efficient level of the working environment.

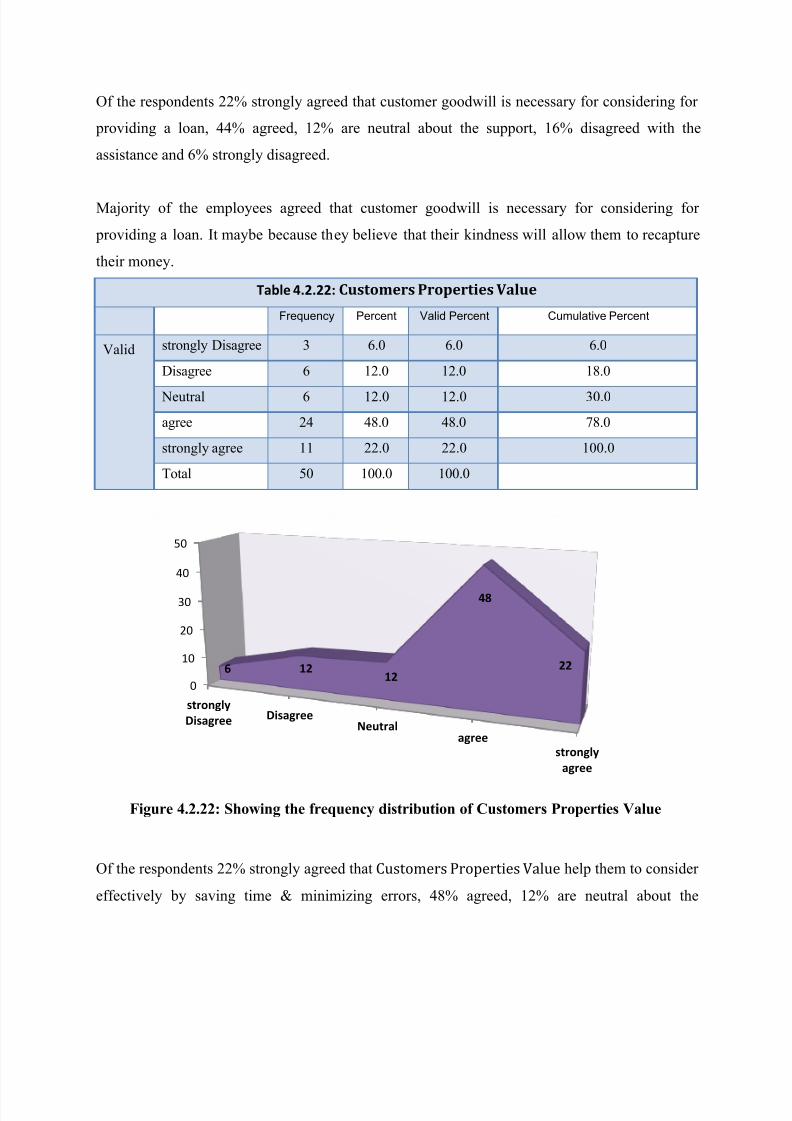

Table 4.2.14: Quality of Credit Portfolio

Frequency Percent Valid Percent Cumulative Percent

Valid strongly Disagree 3 6.0 6.0 6.0

Disagree 7 14.0 14.0 20.0

Neutral 11 22.0 22.0 42.0

agree 20 40.0 40.0 82.0

strongly agree 9 18.0 18.0 100.0

Total 50 100.0 100.0

Figure 4.2.14: Showing the frequency distribution of Quality of Credit Portfolio

Of the respondents 6% strongly agreed that Quality of Credit Portfolio are necessary while 40%

agreed, 22% are neutral about the necessity, 14% disagreed with the necessity and 6% strongly

![8[1].Basic Stat Inference](https://static.documents.pub/doc/80x56/577cc7291a28aba711a02b49/81basic-stat-inference.jpg)