31

9,24% REPSOL YPF PURCHASE OPERATION

9,24% REPSOL YPF PURCHASE OPERATION

2

Index

Main points of the transaction

Foundations of the transaction

Financial Analysis

SyV: a story of value generation

Main points of the transaction

4

Main Points of the transaction

Acquisition of a 5.00465% of Repsol YPF through Sacyr Vallehermoso Participaciones Mobiliarias, S.L. (100% Sacyr’s ownership). Besides, there are equity derivatives agreed with financial entities per 4.23158%. The total participation ( the direct one together with equity derivatives) is 9.23624% at an average price of €25.32 per share, which represents a total investment of €2,855.6 million.

Description

Structureof the

operation

The total amount of the direct investment, €1,504.7million, hasbeen financed through a bridging loan (due date: 15/1/2007) which will be refinanced through a non-recourse debt.

Non-Recourse debt: 85%Equity: 15%

Non –Recourse debt: Euribor + 0.9% (4.85%)

Term: 5-6 years

Basis of the transaction

6

Basis of the transaction

The operation is based on a diversification strategy of the Group SyV.

In this sense, the operation confirms that:

it is a complement of the economic cycles of the rest of divisions through long-term business with supported profitability.

It is a complement of the traditional business of the Group SyV by adding higher margins and results.

Growth directed towards its presence in the main companies of every sector

1.- Strategic reserve

Construction Promotion AssetsConcessionsServices Energy

9,24%

7

Basis of the transaction

Due to its size, position in the market and healthy financial situation Repsol YPF is an unique opportunity to go into the energy market

The moment when the transaction is performed reinforces even more the perspectives of value generation for the Group SyV;

Reduced debt level

Benefits coming from the improvements predicted in the strategic plan 2005-2009 of Repsol YPF

Future Sustained Growth of the shareholder’s earnings

Recovery of the economic situation of Latin-America

New projects in upstream/downstream

Increase of the profitability and margins.

The current value of Repsol YPF is highly priced-attractive with respect to the rest of Spanish companies

2.- Unique opportunity in the energy market

8

Basis of the transactions

Growing demand: According to the Energy Information Administration (EIA) the worldwide oil demand will increase in a 48% between 2003 and 2030.

Long term Prices relatively steady. It is predicted that the oil prices will not suffer important drops until 2030.

3.- Attractive views of the market

Evolution of prices at a worldwide level

Sources: Historical: EIA Projections: EIA, System for the Analysis of Global Energy Markets (2006)

Sources: Historical EIA Projections: EIA, Annual Energy Outlook (2006)

Worldwide consume of primary energy

9

173,549

126,943

98,072 95,608

31,93316,536 12,878 12,046 6,328

BP TOTAL ROYALDUTCHSHELL

ENI REPSOLYPF

CEPSA NORSKHYDRO

STATOIL OMV

Basis of the transaction4.- Description of Repsol YPF: among the main European leaders

Market capitalization of the main European companies (€million)

Fifth integrated oil company in Europe

Average market capitalization of the last month as of 13/10/2006Source: Factset

10

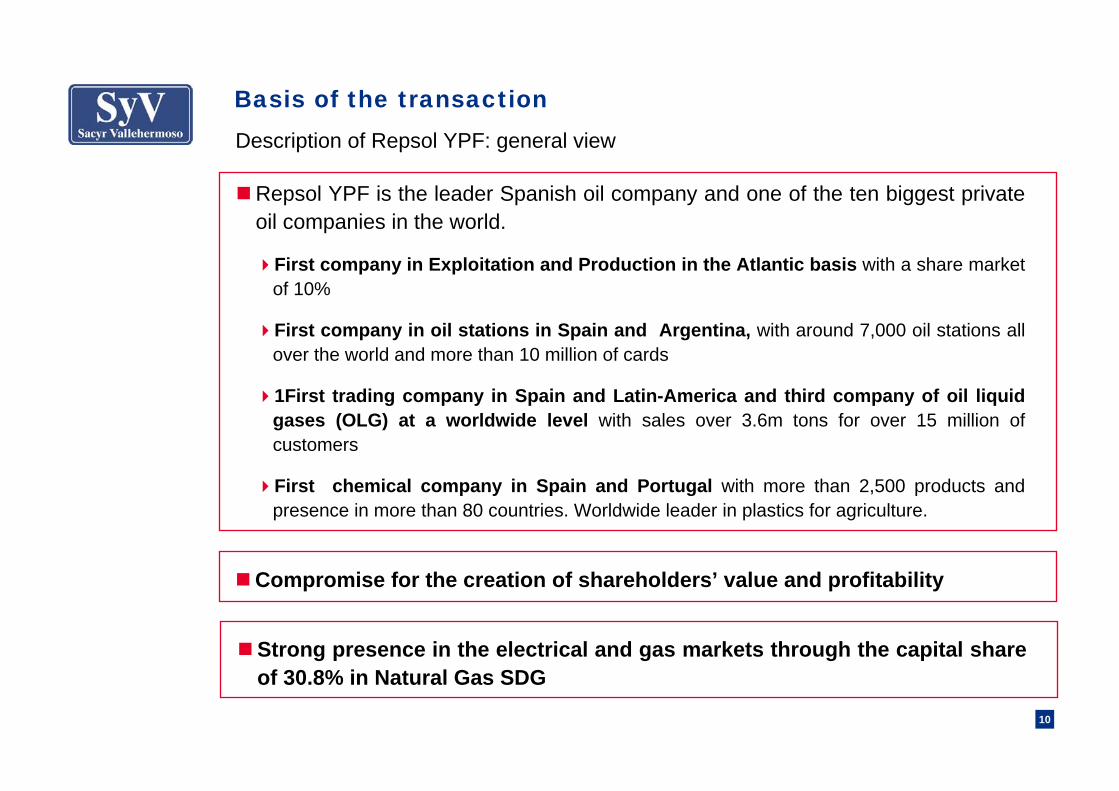

Basis of the transactionDescription of Repsol YPF: general view

Repsol YPF is the leader Spanish oil company and one of the ten biggest private oil companies in the world.

First company in Exploitation and Production in the Atlantic basis with a share market of 10%

First company in oil stations in Spain and Argentina, with around 7,000 oil stations all over the world and more than 10 million of cards

1First trading company in Spain and Latin-America and third company of oil liquid gases (OLG) at a worldwide level with sales over 3.6m tons for over 15 million of customers

First chemical company in Spain and Portugal with more than 2,500 products and presence in more than 80 countries. Worldwide leader in plastics for agriculture.

Compromise for the creation of shareholders’ value and profitability

Strong presence in the electrical and gas markets through the capital share of 30.8% in Natural Gas SDG

11

Basis of the transaction

Working Incomes

EBITDA

Working results

Results after taxes

Investments

55.719

9.684

6.414

3.281

4.076

Financial Key Figures (€million) 30/06/2006 (LTM)(1)

Hydrocarbon Production (K Bep/ day)(2)

Oil (K Bep/day)(2)

Gas (K Bep/ day)(2)

Oil products Sales (kt)

Liquid oil gases sale (LOG) (kt)

Chemical products Sales (kt)

1.100504

597

58.696

3.605

4.802

Working Key Figures 30/06/2006 (LTM)(1)

(1) Last 12 months as for 30/06/2006.(2) Data in 30/06/2006. Source: Repsol YPF

12

Description of Repsol YPF: geographic presence

EBIT 30/06/2006 (LTM)(1)

Total: 6.414 m€

Repsol is present in more than 30 countries

Basis of the transaction

(1) Last 12 months as of: 30/06/2006

Source : Repsol YPF * ABB: Argentina, Brazil and Bolivia

Resto del mundo

34%

España33%

ABB*33%

Rest of the World

Spain

13

Description of Repsol YPF: business areas

European company integrated in the whole value chain of production and trading of oil products

Source: Own data

Basis of the transaction

Exploration(oil and gas)

Production

Oil and gas)Pure y Marketing oil(inc.

LNG)

Petrochemistry

LNG

14

Description of Repsol YPF: exploration and production

Basis of the transaction

Business development based on the relations with National Oil Companies (NOCs)

Production of 1.060 K Bep /day1)

First steps in Russia and Central Asia

Gulf of Mexico Northern Africa Caribbean Sea

Solid presence in strategic areas

(1) Last 12 months as of: 30/06/2006

Source : Repsol YPF

15

Description of Repsol YPF: transport, trading and wholesale marketing

CanaportCanada

Camisea

Trinidad andTobago

Nigeria

Gassi TouilAlgeria

Persian

Leader in Liquid Natural Gas (LNG) in the Atlantic Bais, with a 10% of the market

Electric Third power of the worldwide market per volume of LNG managed through the joint venture with Gas Natural SDG, only back from the companies KOGAS and Tokio Electric

Attractive customers portfolio (Trinidad, Argelia, Iran)

Source: Repsol YPF

Basis of the transaction

16

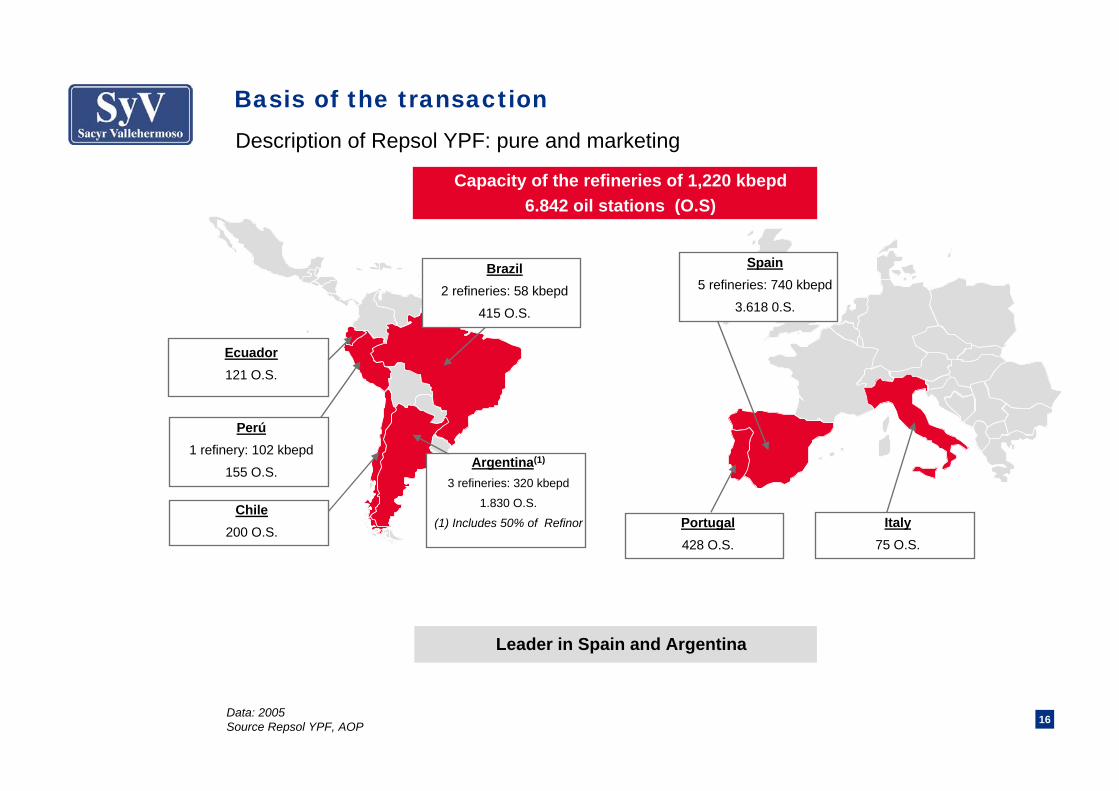

Basis of the transactionDescription of Repsol YPF: pure and marketing

Ecuador121 O.S.

Perú1 refinery: 102 kbepd

155 O.S.

Chile200 O.S.

Argentina(1)

3 refineries: 320 kbepd

1.830 O.S.

(1) Includes 50% of Refinor

Brazil2 refineries: 58 kbepd

415 O.S.

Spain5 refineries: 740 kbepd

3.618 0.S.

Portugal428 O.S.

Italy75 O.S.

Capacity of the refineries of 1,220 kbepd6.842 oil stations (O.S)

Leader in Spain and Argentina

Data: 2005Source Repsol YPF, AOP

17

Basis of the transactionDescription of Repsol YPF: leadership in the business of LNG

3,3

0 2 4 6

Ferrel

Total Gaz

ENI

Mitsubishi LPG

Zeta Group

Indian Oil

Amerigas

Repsol YPF

Shell

SHV Holding

SHVHolding

m t

Compañías no petroleras

Third worldwide company in LNG and second oil company Market share of 81% in Spain

Ecuador: 38%Peru 30%

Bolivia: 37%

Chile: 37%Argentina: 34%

Brazil

India

MoroccoPortugal: 21%Spain: 81%

France

Data 2005source: Repsol YPF

Million tons

non oil companies

18

Basis of the transactionDescription of Repsol YPF: Petrochemical

CorunnaBasis: 60 kt

SinesBasis: 580 ktDerived: 275 kt

Santader Derived 54 kt

Dynasol (50%) BilbaoBasis: 80 kt

TarragonaBasis: 1.285 kt

Derived: 1.557 kt

PuertollanoBase: 537 ktDerived: 704 kt

AltamiraDerived 45 ktDynasol (50%)

EnsenadaBasis: 175 kt Derived 592 kt

Plaza HuinculDerived: 411 kt

Bahía Blanca(1)

Derived. 933 kt

(1) 50% of Profertil

Capacity of production in 20057.402 kt

First petrochemical company in Spain and Portugal

Data 2005Source: Repsol YPF

19

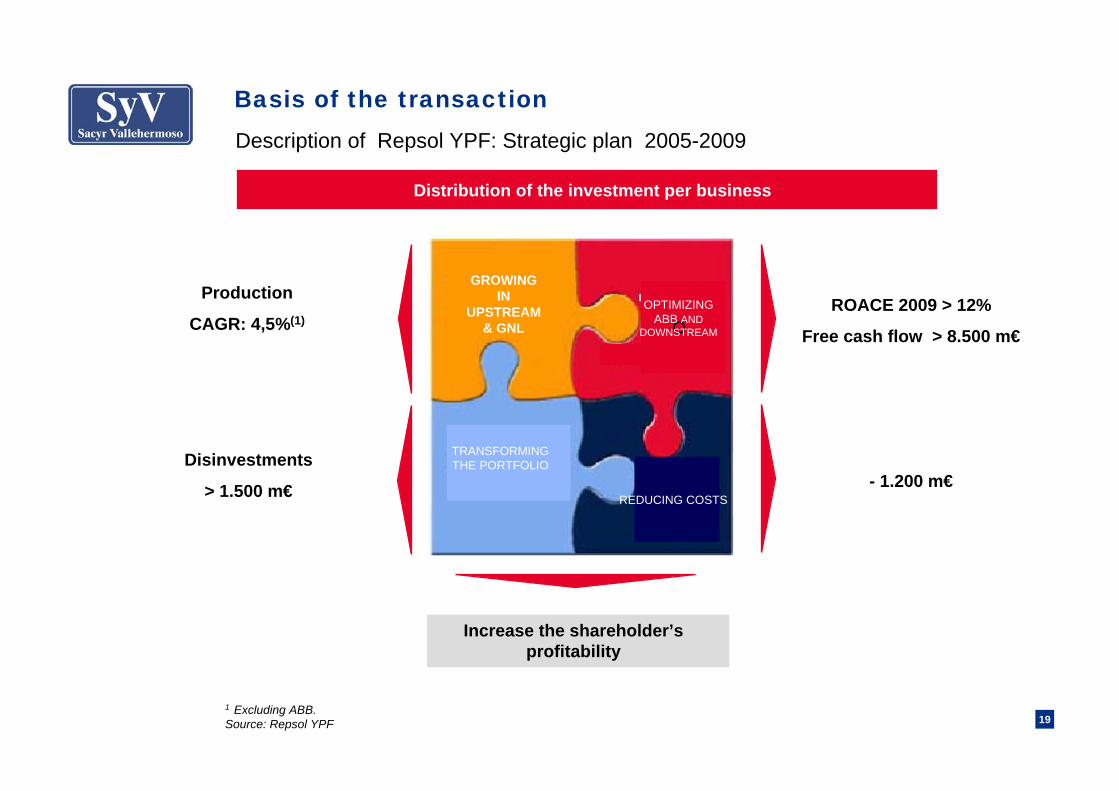

Basis of the transactionDescription of Repsol YPF: Strategic plan 2005-2009

Distribution of the investment per business

ROACE 2009 > 12%

Free cash flow > 8.500 m€

- 1.200 m€Disinvestments

> 1.500 m€

Production

CAGR: 4,5%(1)

1 Excluding ABB.Source: Repsol YPF

Increase the shareholder’s profitability

GROWING IN

UPSTREAM & GNL O

OPTIMIZING ABB AND

DOWNSTREAM

TRANSFORMINGTHE PORTFOLIO

REDUCING COSTS

Financial analysis

21

5.7x

4.5x

5.5x5.8x 5.7x5.6x

4.2x

5.6x 5.7x 5.9x5.5x

7.1x

5.7x

4.2x

5.7x 5.8x 5.8x

7.1x

5.3x 5.3x

8.5x

5.3x5.2x 5.2x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

Repsol Norsk Hydro OMV Total ENI Royal Dutch Shell Statoil BP2006e 2007e 2008e

Financial Analysis

The implicit multiples of the acquisition of 9.24% of Repsol YPF are highly in line with the multiples EV/DACF and P/E at which the rest of comparable European companies are quoting

Implicit multiples of acquisition vs. multiples of comparable European companies

EV/DACF

Source: Analyst reports

22

9.2x

7.7x 7.8x

8.9x

7.8x8.2x

9.1x9.9x10.0x

7.8x8.5x

9.3x8.7x

9.4x8.6x

9.9x10.6x

8.7x 8.7x9.5x

9.1x 9.4x 9.6x10.0x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

Repsol Norsk Hydro OMV Total ENI Royal Dutch Shell Statoil BP2006e 2007e 2008e

Financial AnalysisImplicit multiples of acquisition vs. Multiples of European Comparable companies

P/E

Source: Analysts Reports

23

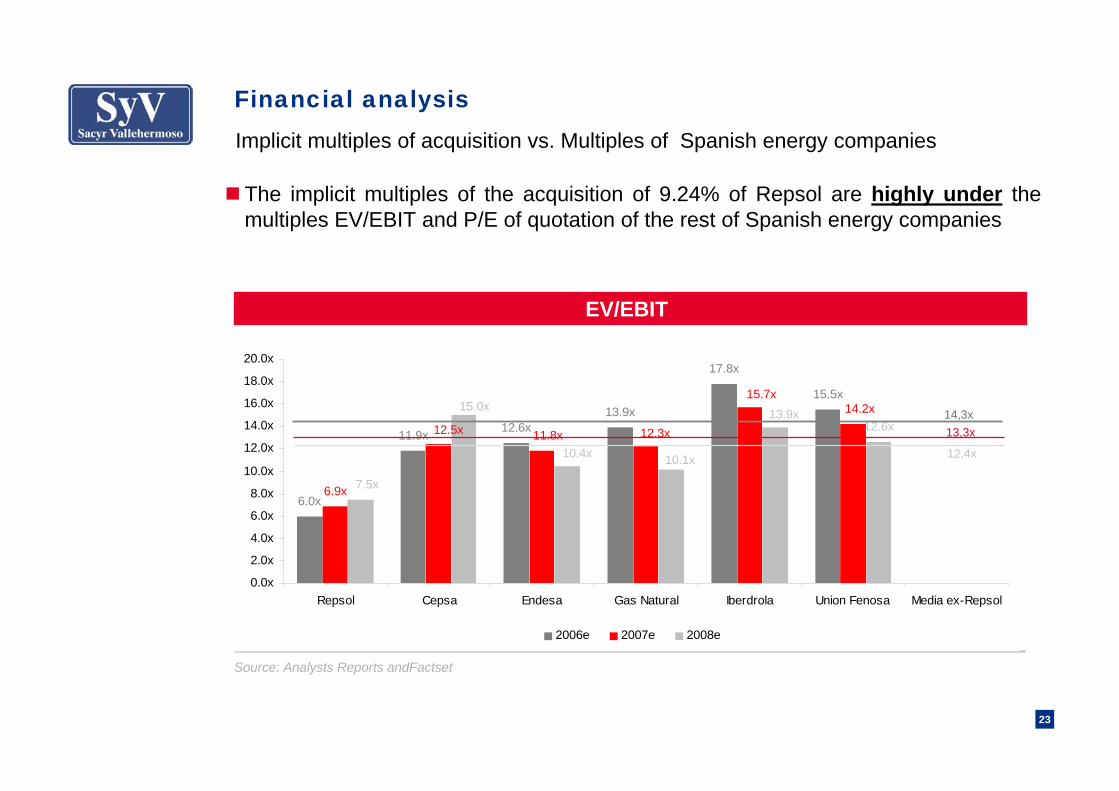

Financial analysis

The implicit multiples of the acquisition of 9.24% of Repsol are highly under the multiples EV/EBIT and P/E of quotation of the rest of Spanish energy companies

Implicit multiples of acquisition vs. Multiples of Spanish energy companies

EV/EBIT

Source: Analysts Reports andFactset

6.0x

11.9x 12.6x13.9x

17.8x

15.5x

6.9x

12.6x14.2x

11.8x12.5x 12.3x

15.7x

10.4x

7.5x

15.0x

10.1x

13.9x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x

Repsol Cepsa Endesa Gas Natural Iberdrola Union Fenosa Media ex-Repsol

2006e 2007e 2008e

14,3x13,3x

12,4x

24

9.0x

16.4x

26.9x 26.0x

29.9x31.3x

9.7x

26.3x

22.1x

17.8x

25.8x 25.7x

22.8x23.5x

20.0x22.3x

10.3x

24.6x

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

Repsol Cepsa Endesa Gas Natural Iberdrola Union Fenosa Media ex-Repsol

2006e 2007e 2008e

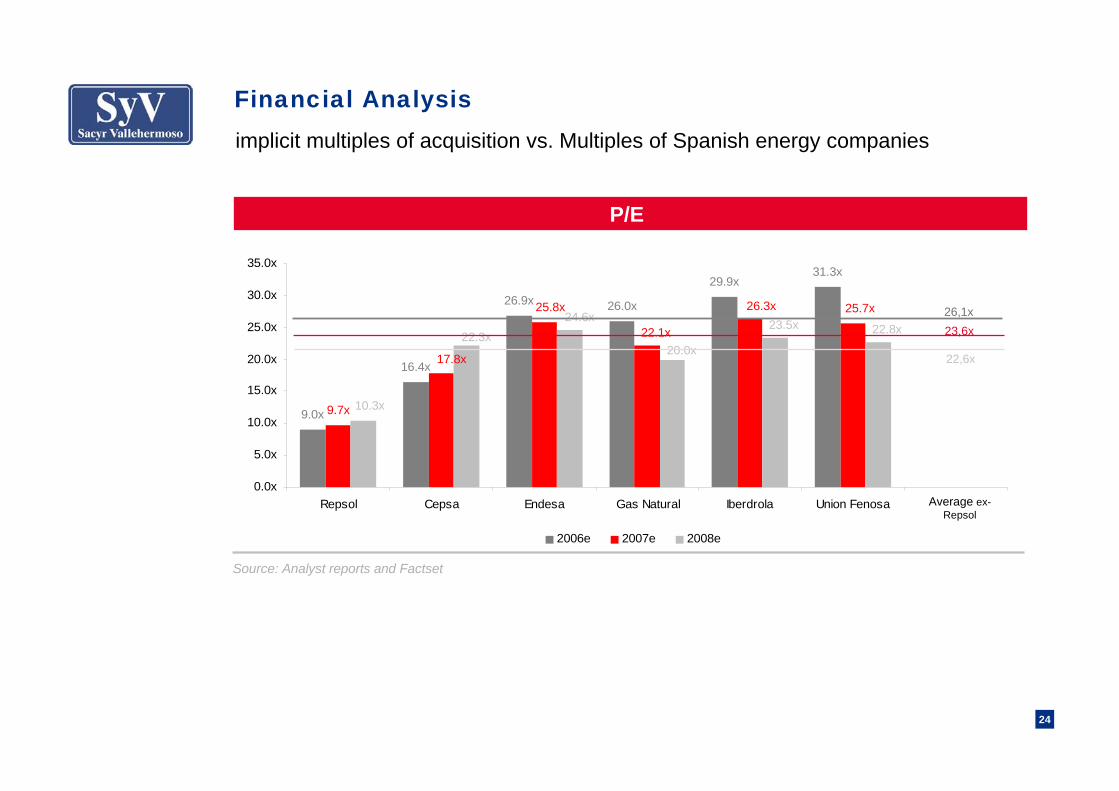

Financial Analysisimplicit multiples of acquisition vs. Multiples of Spanish energy companies

P/E

Source: Analyst reports and Factset

26,1x

22,6x

23,6x

Average ex-Repsol

25

Financial AnalysisImpact on the Group SyV: net benefit per share

Impact on the NBPS of SyV

Note: It has not been considered any type of synergy or goodwill.

Consolidation by the equity method of 3 months for an estimated result of Repsol YPF according to the consensus of Factset of €3,377 million and of SyV of €356 million together with 9 months of Eiffage (400*33%)

Consolidation by the equity method for an estimated result of Repsol YPF according to the consensus of Factset of €3,377 million and of SyV of €403million, together with Eiffage (434*33%)

*

*

**

**

1,06

1,601,79

2,63

1,50

1,001,201,401,601,80

2,002,202,402,602,80

2004 2005 2006 2006 Post 2007 E

BPAEPS

26

Financial AnalysisImpact on the Group SyV: balance

30/06/0630/06/2006

Post(€ million)

1.21.0Total net debt/ Market capitalization

7.35.8Total net Debt/ Net worth

11,2798,423Non-recourse debt

5,5902,734Corporative debt net

14,01311,157Net debt

19,99717,141Total assets

1,9081,908Net worth

SyV: a story of value creation

28

Market Capitalization as of 02/06/2003 (€ million)(1)

SyV: a story of value creationRanking per market capitalization 2003

+303%

Source: Factset(1) Merger date between Sacyr and Vallehermoso

397

2,7183,029

3,296

2,532

4,187

ACS SYV FER FCC ANA OHL

29

1,488

7,7058,768

9,482

11,551

13,504

ACS SYV FER FCC ANA OHL

In the last 3 years SyV has been the company of services and construction with the highest growth, multiplying its market capitalization per 4.6x

SyV: a story of value creation

(x3.2)

(x4.6)

(x2.9)(x2.9)

(x2.8)

(x3.7)

Market capitalization as of 13/10/2006 (€million)

Ranking per market capitalization 2006

Source Factset

30

SyV: a story of value creation

(euros per share)

Note: the price of the shares and index have as a base the price of the share of Sacyr-Vallehermoso in September 2004

stock market evolution in the last 2 years

SyV share has been the one with the highest revaluation in the sector, also highly above the reference index of the Spanish and European markets.

In 2 years the share price of SyV has been multiplied 3.6 times

31

Conclusion

The operation is framed in the strategy of diversification and growth of SyV. It

comes to reinforce the long term business and sustained profitability and confirms the idea of being present in the main companies of every sector where

the Group is acting.