9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE DIARY OF THE NIGERIA – SÃO TOMÉ E PRÍNCIPE JOINT DEVELOPMENT ZONE Carlos B. Gomes ED Commercial & Investment and Chairman of the Board and Authority NIGERIA – SÃO TOMÉ E PRÍNCIPE JOINT DEVELOPMENT AUTHORITY NOT AN OFFICIAL UNCTAD RECORD

Transcript

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

DIARY OF THE

NIGERIA – SÃO TOMÉ E PRÍNCIPE

JOINT DEVELOPMENT ZONE

Carlos B. GomesED Commercial & Investment and Chairman of the Board and Authority

NIGERIA – SÃO TOMÉ E PRÍNCIPE

JOINT DEVELOPMENT AUTHORITY

NOT AN OFFICIAL UNCTAD RECORD

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

CONTENTS OF PRESENTATION

Joint Development Zone (JDZ) Key Dates

Joint Development Authority (JDA) Objectives

Summary of PSC Terms

1st JDZ Licensing Round 2003

2nd JDZ Licensing Round 2004

Future Opportunities

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

JDZ KEY DATES

December 1999: Official talks begin between Nigeria and São Tomé

e Príncipe on competing territorial claims in the Gulf of Guinea

December 2000: Heads of State agree on the joint development of

resources in the disputed area

February 2001: Joint Development Zone (JDZ) and Authority (JDA)

created in a formal Treaty between the two States

January 2002: JDA inaugurated

April 2003 - October 2003: 1st JDZ Licensing Round

October 2004 - November 2004: 2nd JDZ Licensing Round

1 Feb 2005: Block 1 PSC signed

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

JDA OBJECTIVES

Realise the potential of the JDZ in a timely manner

Conduct licensing activity in a transparent, co-operative spirit

Understand the risk and reward balance required for investors

Design a fiscal regime that would: generate early revenue for the JDA;

generate early payback for investors;

be flexible and fairly respond to changes in the economic environment such as high (or low) discovery sizes, prices or costs; and

be competitive with global fiscal regimes designed for deepwater operations, especially those in neighbouring areas

Listen to the opinions and concerns of potential investors

Be flexible throughout and amenable to reasonable requests

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

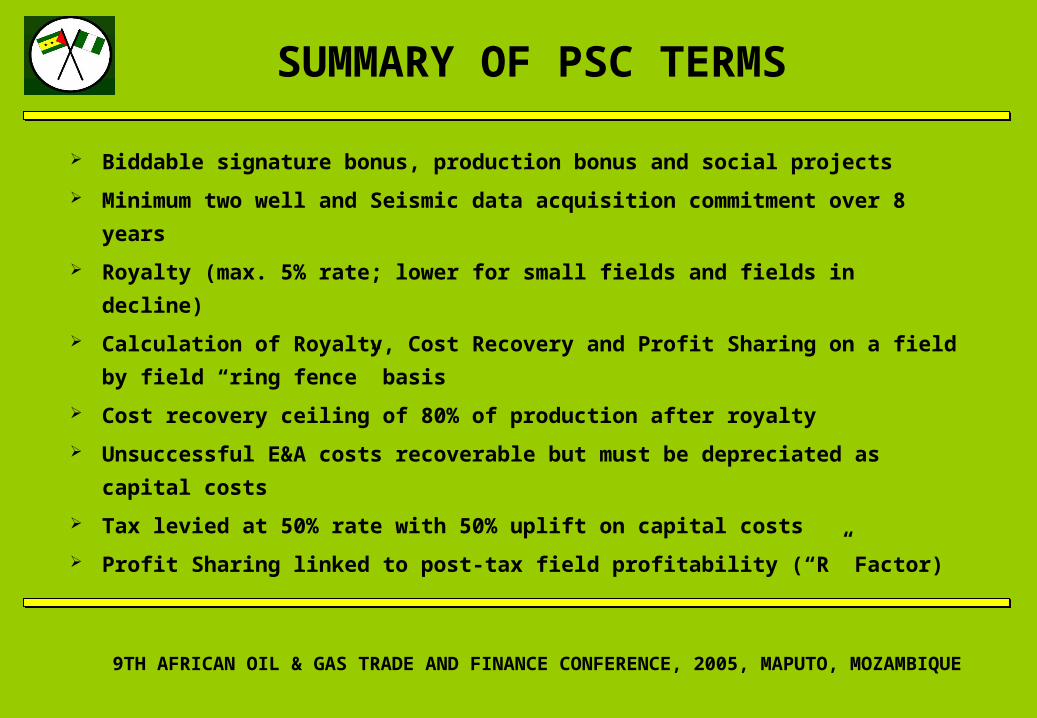

Biddable signature bonus, production bonus and social projects

Minimum two well and Seismic data acquisition commitment over 8 years

Royalty (max. 5% rate; lower for small fields and fields in decline)

Calculation of Royalty, Cost Recovery and Profit Sharing on a field by field

“ring fence” basis

Cost recovery ceiling of 80% of production after royalty

Unsuccessful E&A costs recoverable but must be depreciated as capital

costs

Tax levied at 50% rate with 50% uplift on capital costs

Profit Sharing linked to post-tax field profitability (“R” Factor)

SUMMARY OF PSC TERMS

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

JDZ PSC TERMS: FLOWCHART

- Costs - Costs

+ Revenue + Royalty Oil

- Fees & Bonuses + Fees & Bonuses

+ Cost Oil

+ Tax Oil

+ Profit Share+ Profit Share

Contractor JDAPSC

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

0%10%20%30%40%50%60%70%80%90%

100%

Irelan

d

Canad

a (E

.Coa

st)

UKIn

dia

US (GoM

)

New Z

ealan

d

Gabon

Angola

Nigeria

Brazil

Nigeria

-Sao

Tom

e JD

Z

Congo

(Br.)

Equat

orial

Guin

ea

Mau

ritan

ia

Indo

nesia

Philipp

ines

Cote

d'Ivo

ire

Mala

ysia

Norway

Egypt

Brune

i

Trini

dad

& Toba

go

Vietna

m

Go

vt

Ta

ke

(%

Pre

-Ta

ke

PV

10

)

JDZ GOVERNMENT TAKE

JDZ Government Take in middle of range of global deepwater terms Note: Government Take based on hypothetical 500 mmbbl field and excludes

signature bonuses, if applicable

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

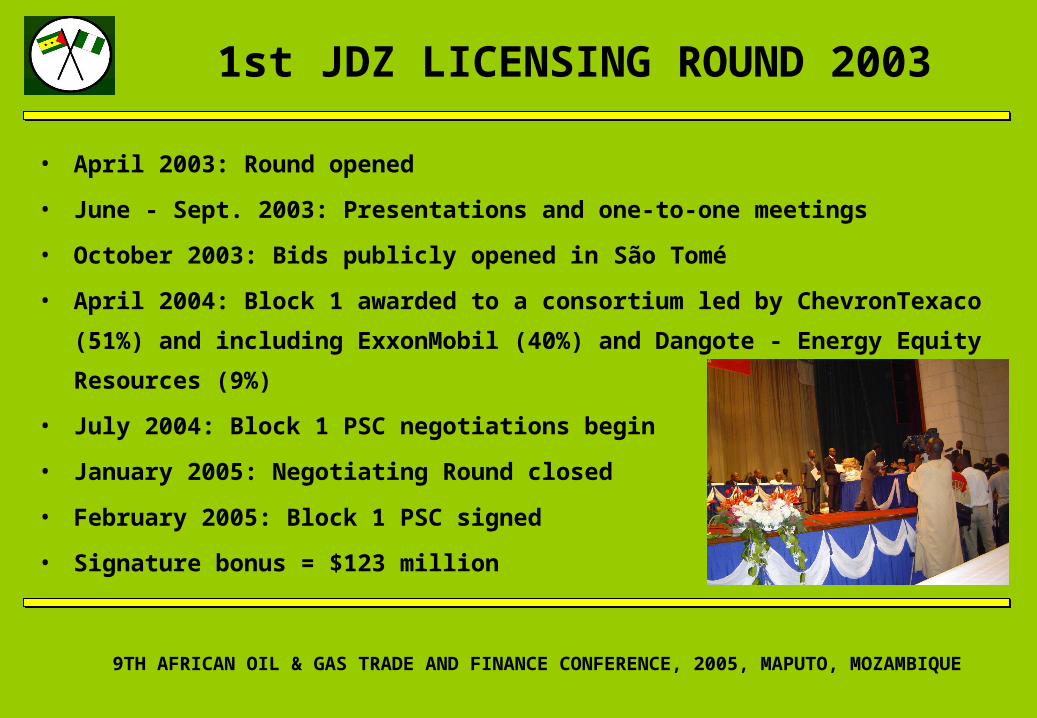

• April 2003: Round opened

• June - Sept. 2003: Presentations and one-to-one meetings

• October 2003: Bids publicly opened in São Tomé

• April 2004: Block 1 awarded to a consortium led by ChevronTexaco (51%) and

including ExxonMobil (40%) and Dangote - Energy Equity Resources (9%)

• July 2004: Block 1 PSC negotiations begin

• January 2005: Negotiating Round closed

• February 2005: Block 1 PSC signed

• Signature bonus = $123 million

1st JDZ LICENSING ROUND 2003

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

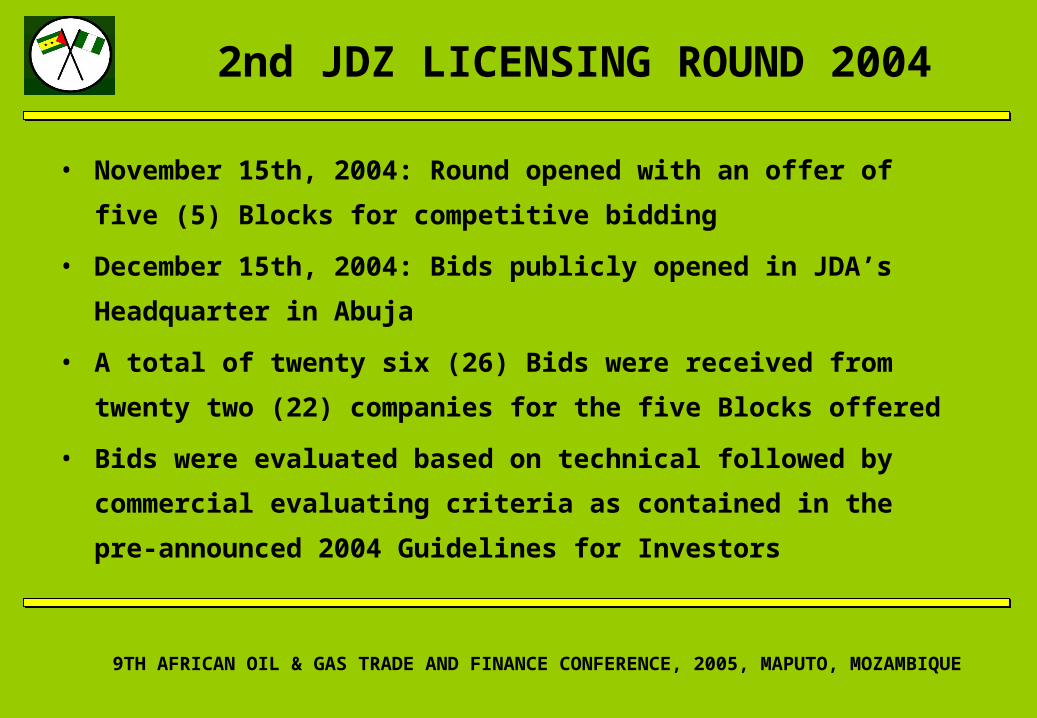

• November 15th, 2004: Round opened with an offer of five (5)

Blocks for competitive bidding

• December 15th, 2004: Bids publicly opened in JDA’s Headquarter

in Abuja

• A total of twenty six (26) Bids were received from twenty two (22)

companies for the five Blocks offered

• Bids were evaluated based on technical followed by commercial

evaluating criteria as contained in the pre-announced 2004

Guidelines for Investors

2nd JDZ LICENSING ROUND 2004

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

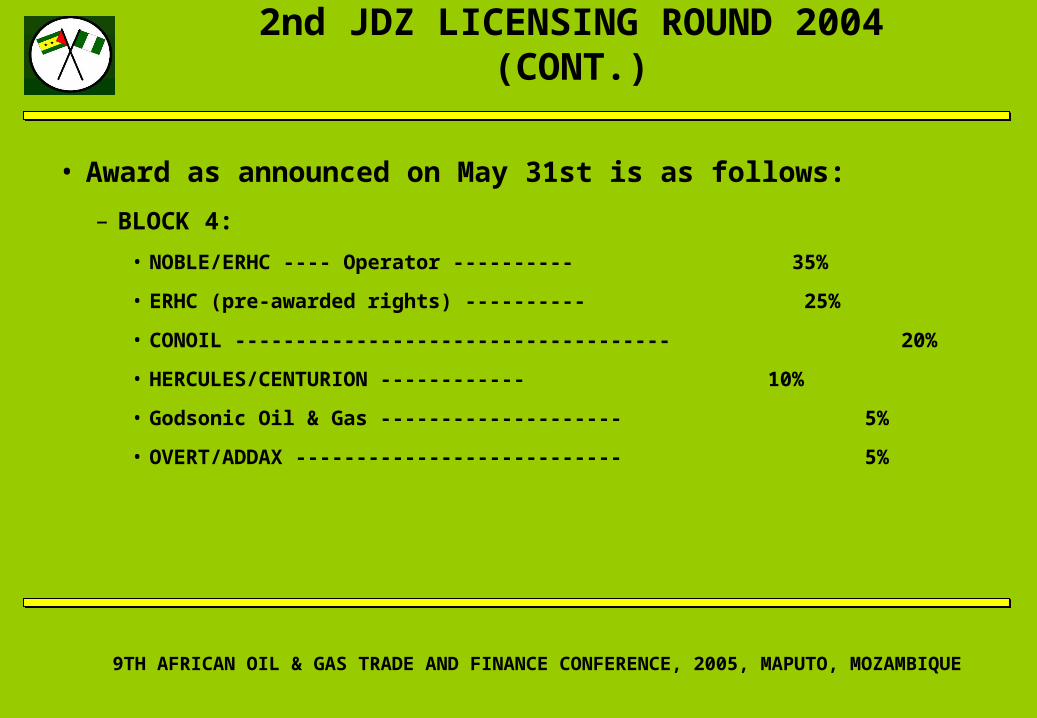

• Highest Bona Fide Bids were retained as follows:

– BLOCK 2 ------------------------------------------- $71 million

– BLOCK 3 ------------------------------------------- $40 million

– BLOCK 4 ------------------------------------------- $90 million

– BLOCK 5 ------------------------------------------- $37 million

– BLOCK 6 ------------------------------------------- $45 million

– TOTAL FOR 2004 LIC. ROUND ------------ $283 million

– TOTAL for 2003 & 2004 LR ----------------- $406 million

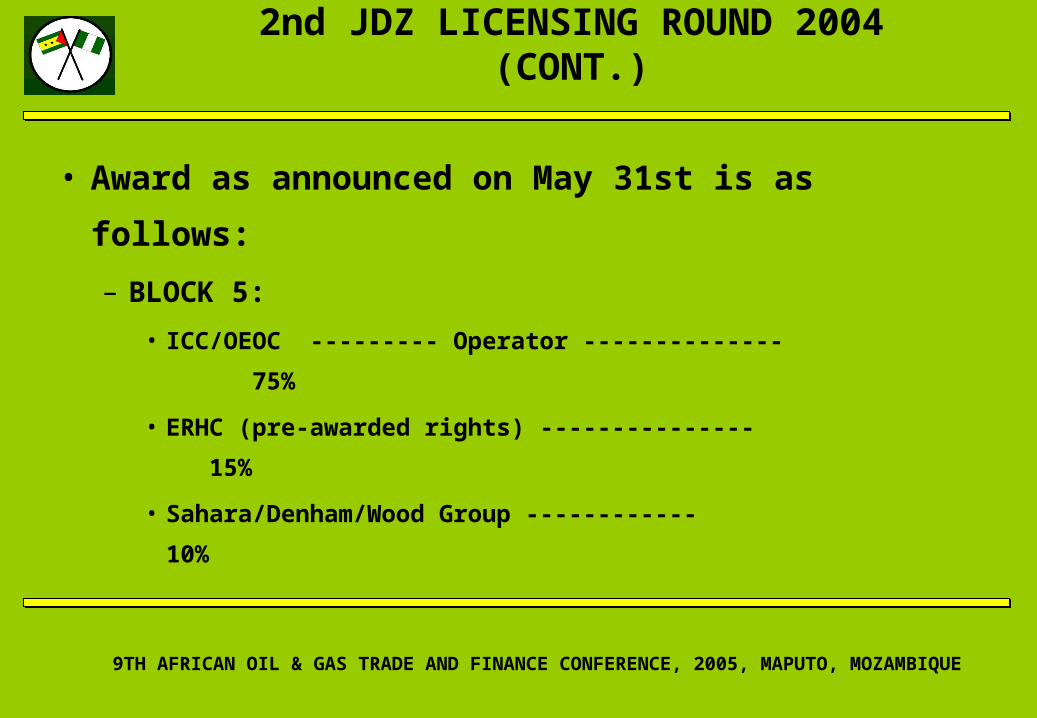

2nd JDZ LICENSING ROUND 2004 (CONT.)

9TH AFRICAN OIL & GAS TRADE AND FINANCE CONFERENCE, 2005, MAPUTO, MOZAMBIQUE

• Based on a previous agreement with the Democratic Republic of Sao

Tome and Principe, certain Pre-Emption rights were accorded to

ExxonMobil and ERHC.

• ExxonMobil decided not to exercise their 25% optional rights (in any two

blocks) under the current Licensing Round. ERHC rights are as folows: