Option Pricing in a Black-Scholes Model with Markov Switching Fuh, Cheng-Der 1 and Wang, Ren-Her Institute of Statistical Science, Academia Sinica, Taipei, Taiwan, R.O.C. Cheng, Jui-Chi Graduate Institute of Finance, National Taiwan University, Taipei, Taiwan, R.O.C. ABSTRACT The theory of option pricing in Markov volatility models has been developed in recent years. However, an efficient method to compute option price in this setting remains lacking. In this article, we present a way of modeling time-varying volatility; to generalize the classical Black-Scholes model to encompass regime-switching properties. Specifically, the unobserved state variables for stock fluctuations are governed by a first-order Markov process, and the drift and volatility parameters take different values depending on the state of this hidden Markov model. Standard option pricing procedure under this model becomes problematic. We first provide a closed-form formula for the arbitrage-free price of the European call option. In the case of the underlying Markov process has two states, we have an explicit analytic formula for option price. When the number of states for the underlying Markov process is bigger than two, we propose an approximation formula for option price. The idea of the approximation formula is that we replace the distribution of occupation time for a given state by its corresponding stationary distribution multiplies the whole time period. Numerical methods, such as Monte-Carlo simulation and Markovian tree, to compute European call option price are presented for comparison. Our numerical results show that the approximation formula provide an efficient and reliable implementation tool for option pricing. Implied volatility and implied volatility surface are also given. Keywords: Arbitrage, Black-Scholes model, European call option, hidden Markov model, implied volatility, Laplace transform, Monte Carlo, tree. 1. Research partially supported by NSC 91-2118-M-001-016. 1

Transcript

Option Pricing in a Black-Scholes Model with Markov Switching

Fuh, Cheng-Der1 and Wang, Ren-Her

Institute of Statistical Science, Academia Sinica, Taipei, Taiwan, R.O.C.

Cheng, Jui-Chi

Graduate Institute of Finance, National Taiwan University, Taipei, Taiwan, R.O.C.

ABSTRACT

The theory of option pricing in Markov volatility models has been developed in recent

years. However, an efficient method to compute option price in this setting remains

lacking. In this article, we present a way of modeling time-varying volatility; to generalize

the classical Black-Scholes model to encompass regime-switching properties. Specifically,

the unobserved state variables for stock fluctuations are governed by a first-order Markov

process, and the drift and volatility parameters take different values depending on the

state of this hidden Markov model. Standard option pricing procedure under this model

becomes problematic. We first provide a closed-form formula for the arbitrage-free price

of the European call option. In the case of the underlying Markov process has two

states, we have an explicit analytic formula for option price. When the number of states

for the underlying Markov process is bigger than two, we propose an approximation

formula for option price. The idea of the approximation formula is that we replace

the distribution of occupation time for a given state by its corresponding stationary

distribution multiplies the whole time period. Numerical methods, such as Monte-Carlo

simulation and Markovian tree, to compute European call option price are presented

for comparison. Our numerical results show that the approximation formula provide

an efficient and reliable implementation tool for option pricing. Implied volatility and

implied volatility surface are also given.

Keywords: Arbitrage, Black-Scholes model, European call option, hidden Markov model,

implied volatility, Laplace transform, Monte Carlo, tree.

1. Research partially supported by NSC 91-2118-M-001-016.

1

1. Introduction

It is well-known that the volatility of financial data series tends to change over time,

and changes in return volatility of stock returns tend to be persistent. The statistical

properties of return volatility have been deeply studied and uncovered in the financial

economic literatures, for instance, the extensive work on modeling stock fluctuations

with stochastic volatility (cf. Anderson, 1996; Hull and White, 1987; Stein, 1991; Wig-

gins, 1987; Heston, 1993), and uncertain volatility (Avellaneda, Levy, and Paras, 1995).

Many efforts have been made to study financial markets with different information levels

among investors (cf. Duffie and Huang, 1986; Ross, 1989; Anderson, 1996; Karatzas and

Pikovsky, 1996; Guilaume et. al., 1997; Grorud and Pontier, 1998; Imkeller and Weisz,

1999). Like the Markov switching model of Hamilton (1988, 1989) may provide more

appropriate modeling of volatility. In this regard, Hamilton and Susmel (1994) proposed

the Markov switching ARCH model. In a partial equilibrium model, Turner, Startz and

Nelson (1989) formulate a switching model of excess returns in which returns switch ex-

ogenously between a Gaussian low variance regime and a Gaussian high variance regime.

So, Lam and Li (1998) generalizes the stochastic volatility model to incorporate Markov

regime switching properties. Diebold and Inoue (2001) considers the properties of long

memory and regime switching.

In deed, recent research (cf. Bittlingmayer, 1998) has shown that investors’ un-

certainty over some important factors affecting the economy may greatly impact the

volatility of stock returns. More generally, there is evidence that investors tend to be

more uncertain about the future growth rate of the economy during recessions, thereby

partly justifying a higher volatility of stock returns. In this paper, to encompass the

empirical phenomena of the stock fluctuations relate to business cycle, we introduce a

model of an incomplete market by adjoining the Black-Scholes exponential Brownian

motion model for stock fluctuations with a hidden Markov process. Specifically, we

assume that stock of asset pricing are generated by realization of a Gaussian diffusion

process, and the drift and volatility parameters take different values depending on the

state of a hidden Markov process. That is, we assume that identical investors cannot

observe the drift rate, as well as the volatility of course, of the dividend process, but

they have to infer it from the observation of past dividends. We call this model a Black-

Scholes model with Markov switching, or a hidden Markov model in brief. Related works

in this type have been studied and documented in the literatures, for instance, Detemple

(1991) and David (1997) encompass the regime switching properties of the drift to the

classical Cox-Ingersoll-Ross model, while Veronesi (1999) studies the Gaussian diffusion

model. These papers focus on the issue of modeling stock returns and their empirical

phenomena. They also study investors’ optimal portfolio allocation and show that equi-

librium marketwise excess returns display changing volatility, negative skewness, and

negative correlation with future volatility.

2

For the concern of option pricing in Markov volatility models. Di Masi, Kabanov

and Runggaldier (1994) considers the problem of hedging an European call option for

a diffusion model where drift and volatility are function of a two state Markov jump

process. Guo (2001) also considers the same model and gives a closed-form formula for

the European call option. However, her formula is not appropriate stated and has a

mistake. The contribution of this paper is to give a closed-form formula in the case of

a two state hidden Markov model, and to propose an approximation formula for the

arbitrage-free price of the European call option in general case. The idea of the approxi-

mation formula is that we replace the distribution of occupation time for a given state by

its corresponding stationary distribution multiplies the whole time period. Numerical

methods, such as Monte-Carlo simulation and Markovian tree, to compute European

call option price are presented for comparison. Our numerical results show that the

approximation formula provide an efficient and reliable implementation tool for option

pricing.

This article is organized as follows. In Section 2, we first define the Black-Scholes

model with Markov switching that capture the phenomenon of business cycle in stock

fluctuations. Then, we provide a closed-form formula for the price of the European call

option, and in particular, we give an explicit analytic formula for option price when the

underlying Markov process has two states. In Section 3, we propose an approximation

formula for option price in a finite state hidden Markov model. To illustrate the perfor-

mance of the approximation formula, in Section 4, we presents numerical and simulation

results for comparison. These outcomes are reported in terms of Monte-Carlo simulation

and Markovian tree, respectively. Implied volatility and implied volatility surface are

also given to support our results. Section 5 is conclusions. The derivation of the option

price formula is in the Appendix.

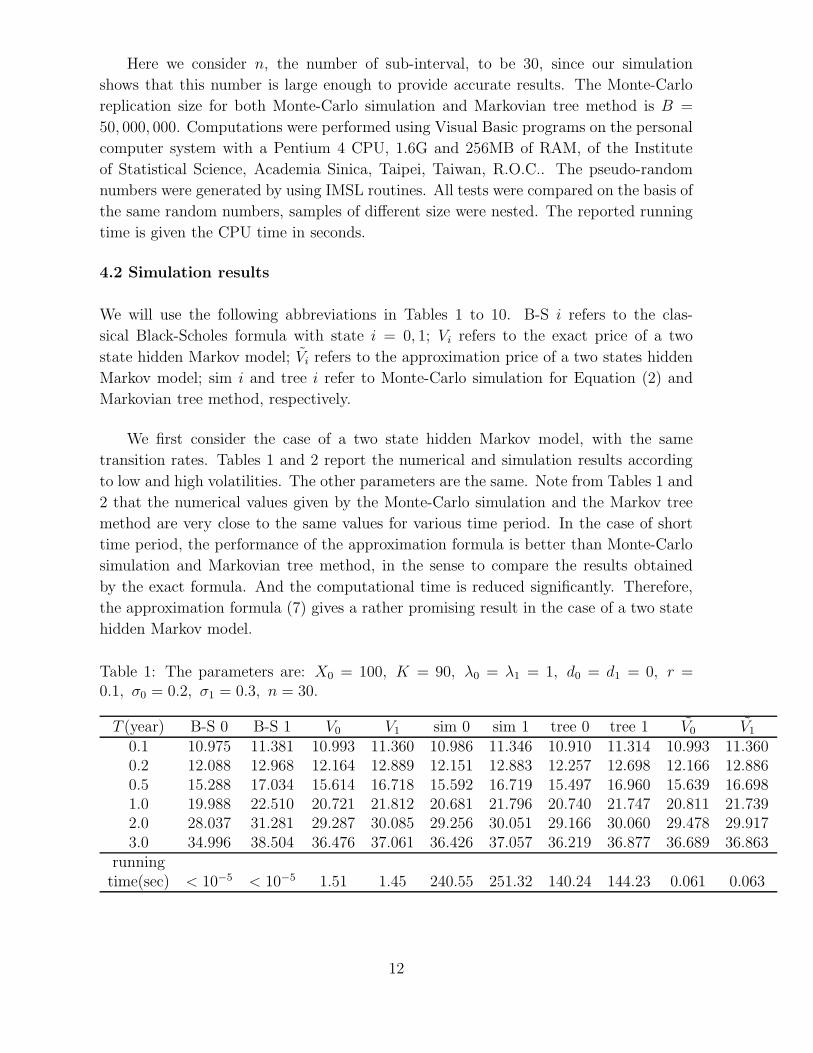

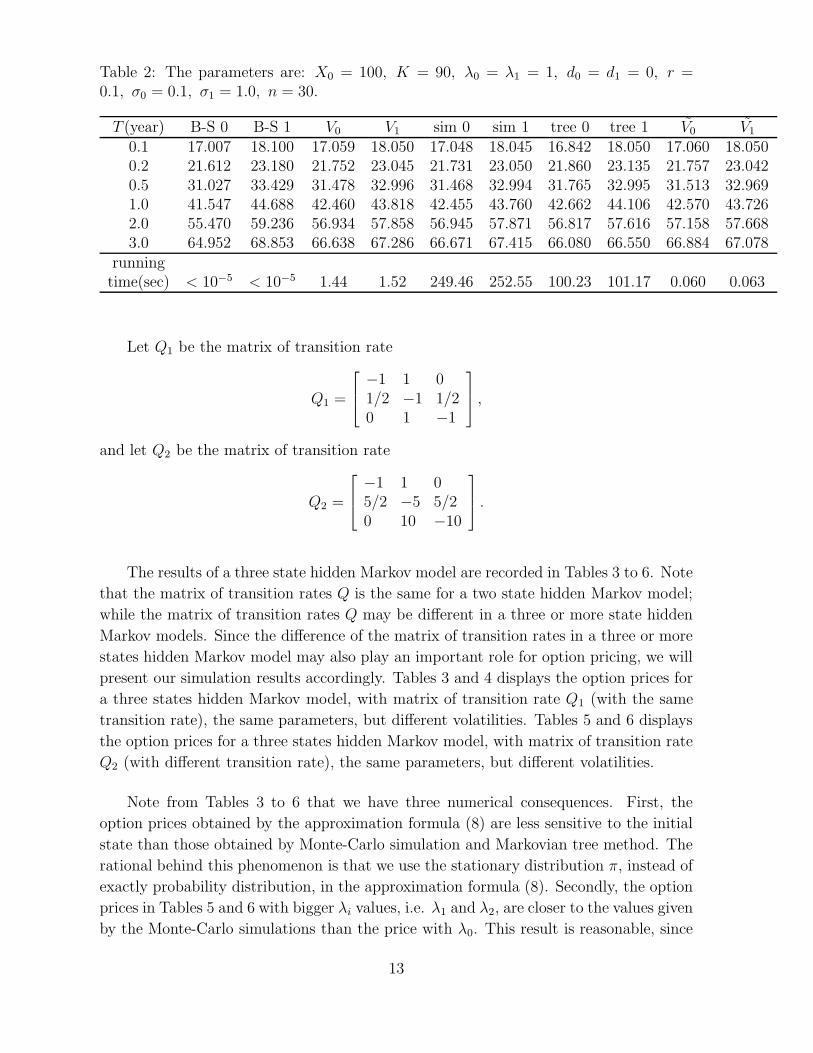

2. The hidden Markov model and option price

We incorporate the existence of business cycle by modeling the fluctuations of a single

stock price Xt, using an equation of the form

dXt = Xtµε(t)dt+Xtσε(t)dWt, (1)

where ε(t) is a stochastic process representing the state of business cycle, Wt is the

standard Wiener process which is independent of ε(t). For each state of ε(t), the drift

parameter µε(t) and volatility parameter σε(t) are known, and take different values when

ε(t) is in different state.

We also assume that the supply of the risky asset is fixed and normalized to 1. The

risky free asset is supplied and has an instantaneous rate of return equal to r. Note that

3

this assumption not only simplify the analysis, in particular for option pricing, but also

matches the empirical finding that the volatility of the risk-free rate is much lower than

the volatility of market returns.

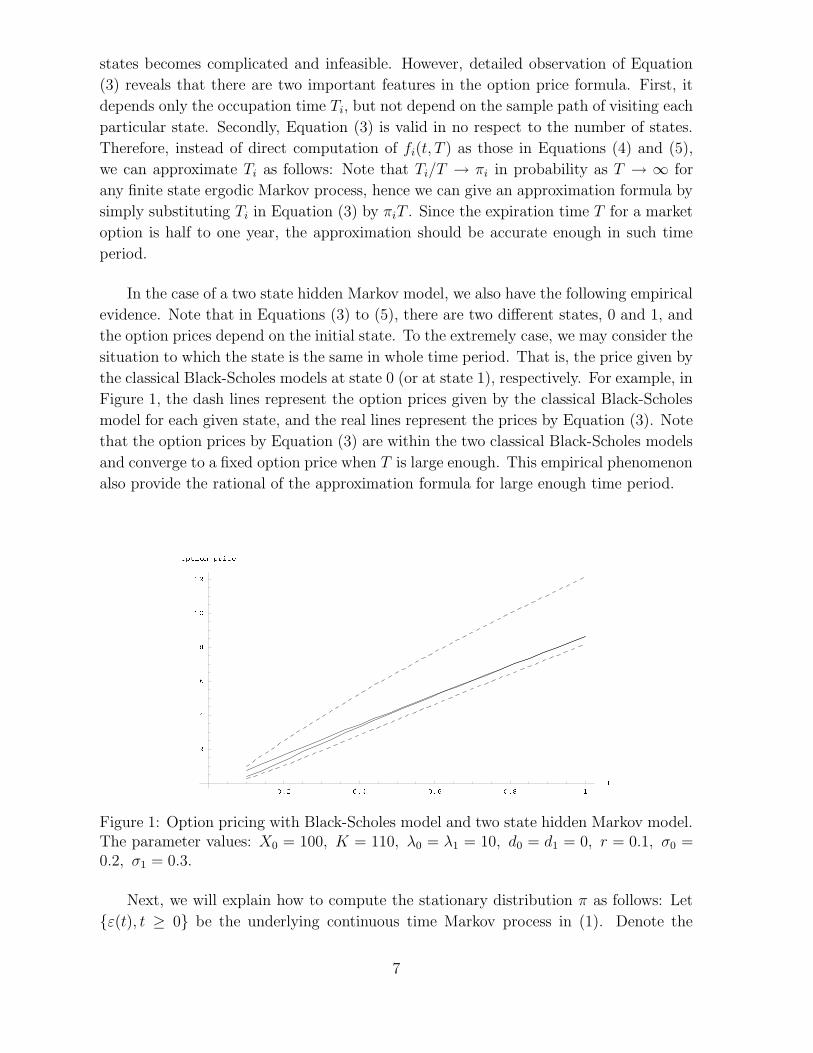

Assume that ε(t) is a Markov process with a few states (maybe two or three states).

In financial economic, we know that business cycle can divide into two different states

called expansion and contraction. A growing economy is described as being in expansion.

In this state, let ε(t) = 0, µε(t) = µ0 and σε(t) = σ0. On the other hand, we can take

the value ε(t) = 1, µε(t) = µ1 and σε(t) = σ1 to represent the state in contraction. More

generally, one can use the state space Ω = 0, 1, · · · , N for ε(t) to model more complex

business cycle structures. In this section, for simplicity, we consider a two state hidden

Markov model for a single stock price Xt by using an equation of (1), where ε(t) is a

Markov process representing the state. Let

ε(t) =

0, when the business cycle in expansion,1, when the business cycle in contraction.

Assume σ0 6= σ1.

For the concern of the transition rate, let λi be the rate of leaving state i, and τi the

time of leaving state i. We assume that

P (τi > t) = e−λit, i = 0, 1.

Then the memoryless property of this process is plausible in that, from a practical

standpoint, the information flow be identified more easily otherwise.

It is conceivable that sometimes investors will try to manipulate their buying and

selling in such a way that the existence of such information is not detectable from the

change of volatilities, namely σ are identical, see Detemple (1991), David (1997), and

Veronesi (1999). The problem of detecting the state change of ε(t) when σ remain

unchanged appears to be hard to solve mathematically. It is plausible that change in

business cycle distribution, hence predictability, manifests itself in the diffusion coeffi-

cient in the form of both stochastic volatility and drift. If we assume that the σ are

distinct then it is no loss of generality to assume that ε(t) is actually observable, since

the local quadratic variation of Xt in any small interval to the left of t will yield σε(t)

exactly. (For details, see McKean, 1969.) Hence, even if Xt is not Markovian, the joint

distribution (Xt, ε(t)) is so.

Despite the success of the classical Black-Scholes model, some empirical phenom-

ena have received much attention recently. An important assumption in the Black-

Scholes model is that the underlying asset distribution is assumed to be Normal, and

the volatility is a fixed constant. However, empirical evidences suggest that it has clus-

ter phenomenon, leptokurtic and unsymmetrical feature. Due to the adjoin of the stock

4

fluctuations with a hidden Markov process (the drift and volatility parameters take dif-

ferent values depending on the state of this hidden Markov process) in the Black-Scholes

exponential Brownian motion model, David (1997) shows that model (1) displays the

asymmetric leptokurtic features, negative skewness, and negative correlation with future

volatility. Veronesi (1999) shows that model (1) is better than the Black-Scholes model

to explain features of stock returns, including volatility clustering, leverage effects, ex-

cess volatility and time-varying expected returns. They both show that model (1) can

be embedded into a rational expectation equilibrium framework. For the concern of the

empirical phenomenon on volatility smile, we will present implied volatility and implied

volatility surface in the end of Section 4.

To get the option price formula, we know model (1) is arbitrage-free but incomplete

(cf. Harrison and Pliska (1981), Harrison and Kreps (1979)). One way to treat this

situation can be found in Follmer and Sondermann (1986), and Schweizer (1991), based

on the idea of hedging under a mean-variance criterion. Here, we follow the method by

D. Duffie to complete the market: at each time t, there is a market for a security that

pays one unit of account (say, a dollar) at the next time τ(t) = infu > t|ε(u) 6= ε(t)that the Markov chain ε(t) changes state. One can think of this as an insurance contract

that compensates its holder for any losses that occur when the next state change occurs.

Of course, if one wants to hedge a given deterministic loss C at the next state change,

one holds C of the current change-of-state (COS) contracts. For the detail, see Guo

(2001). It can be shown that the absence of arbitrage is effectively the same as the

existence of a probability Q, equivalent to P , under which the price of any derivative is

the expected discounted value of its future cash flow.

The same exercise applied to the underlying risky-asset implies that its price process

X must have the formdXt

Xt= (r − dε(t))dt+ σε(t)dW

Qt , (2)

where WQt is the standard Brownian motion under the risk-neutral probability Q, and

dε(t) = r − µε(t). Note that dε(t) is the cost of change of state at the time t. When the

state change at time t, the drift is different from the riskless interest rate r by d0 − d1,

and the arbitrage opportunity emerges at this moment.

Denote Ti as the total time between 0 and T during which ε(t) = 0, starting from

state i for i = 0, 1. Let fi(t, T ) be the probability distribution function of Ti.

Theorem 1 Under hidden Markov model (1). Given Equation (2), COS, and riskless

interest rate r, the arbitrage free price of a European call option with expiration date T

and strike price K is

Vi(T,K, r) = E[e−rT (XT −K)+|ε(0) = i]

5

= e−rT∫ ∞

0

∫ T

0

y

y +Kρ(ln(y +K), m(t), v(t))fi(t, T )dtdy, (3)

where ρ(x,m(t), v(t)) is the normal density function with expectation m(t) and variance

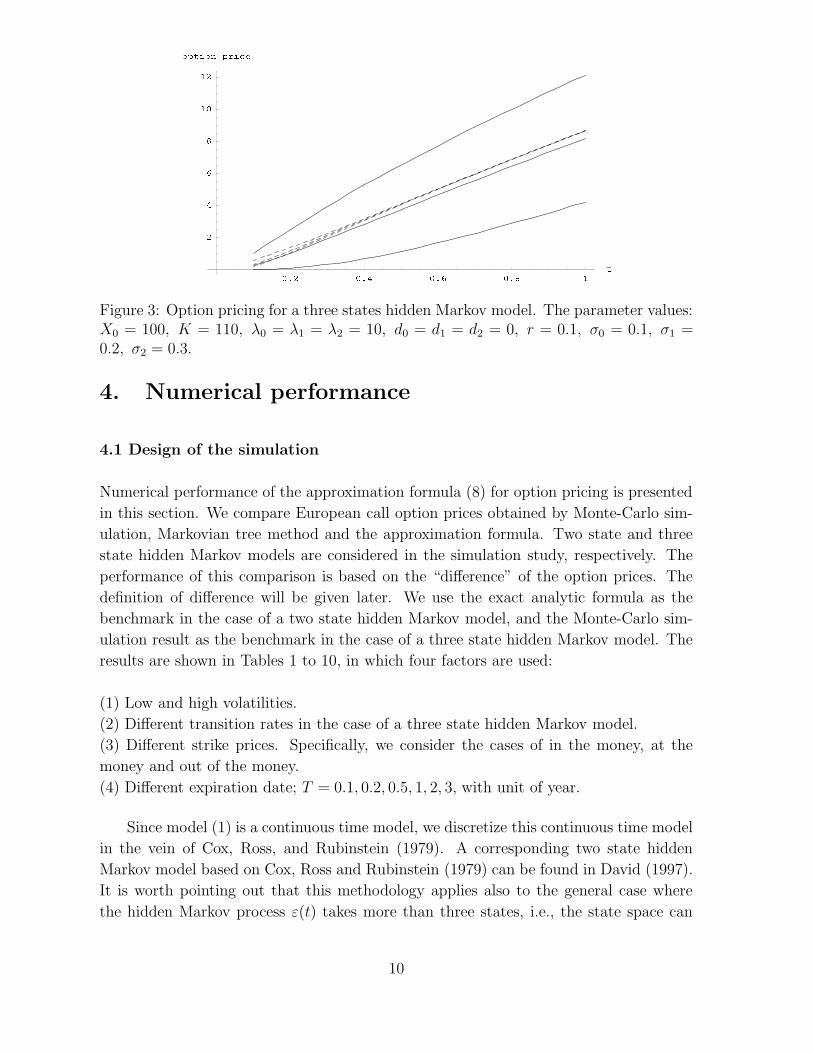

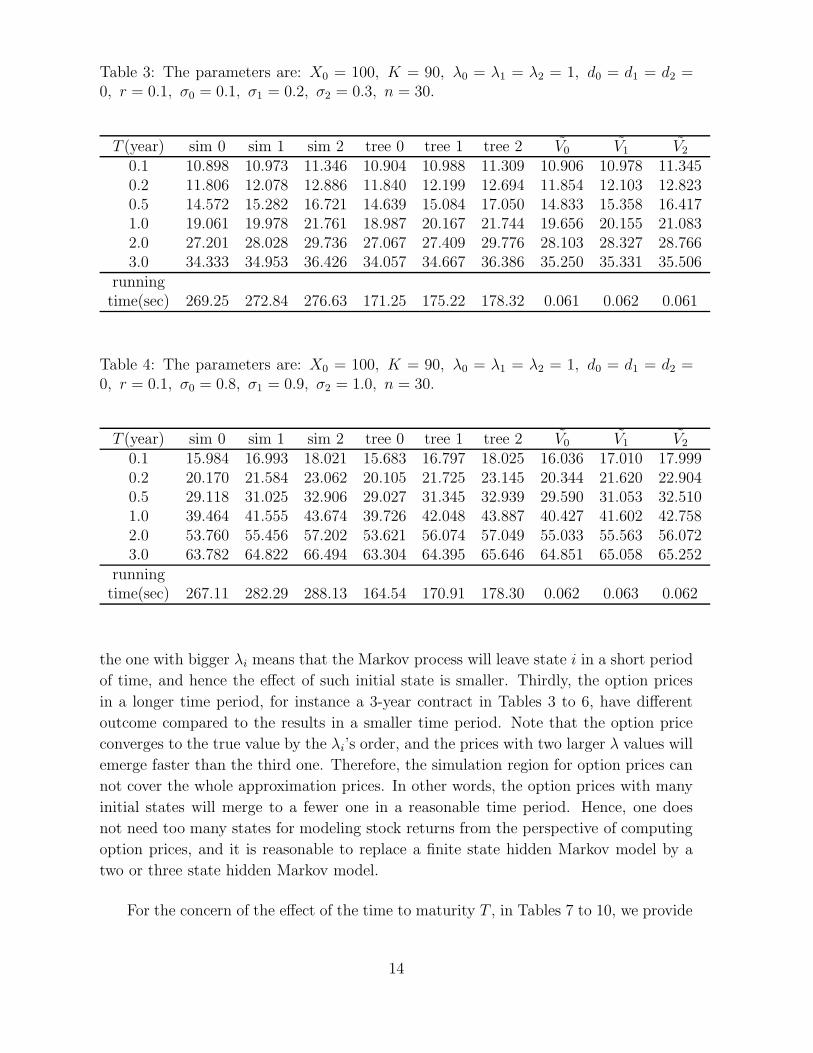

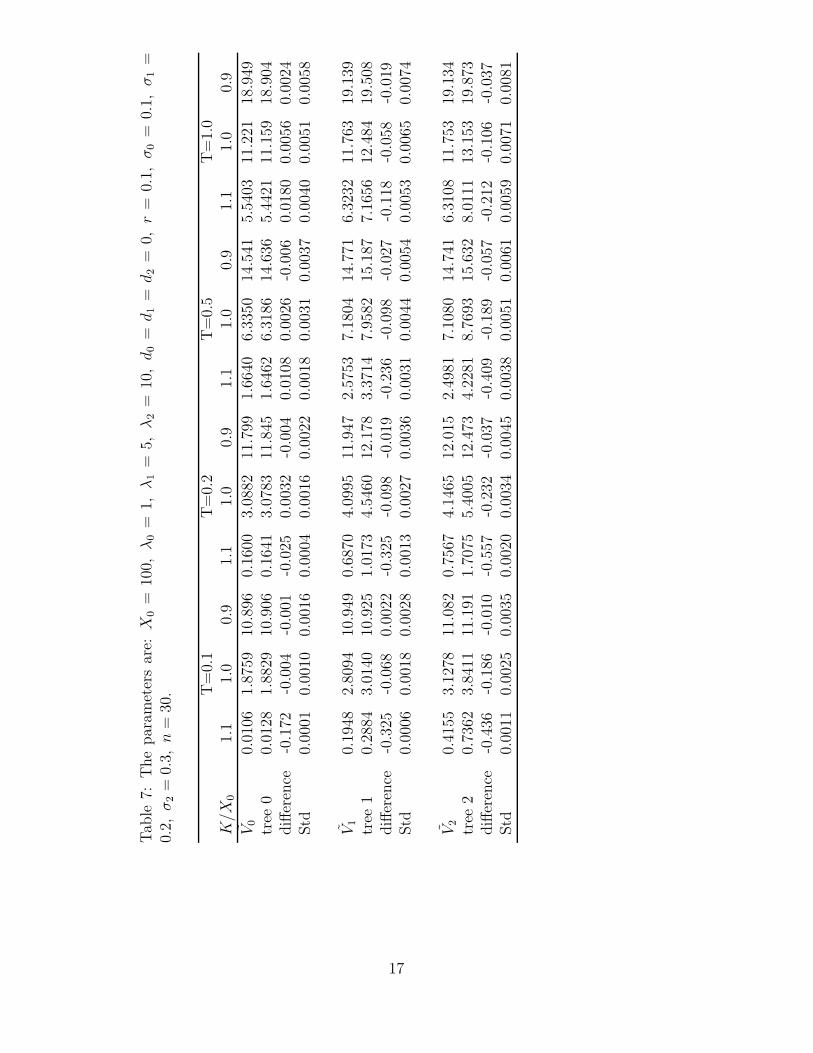

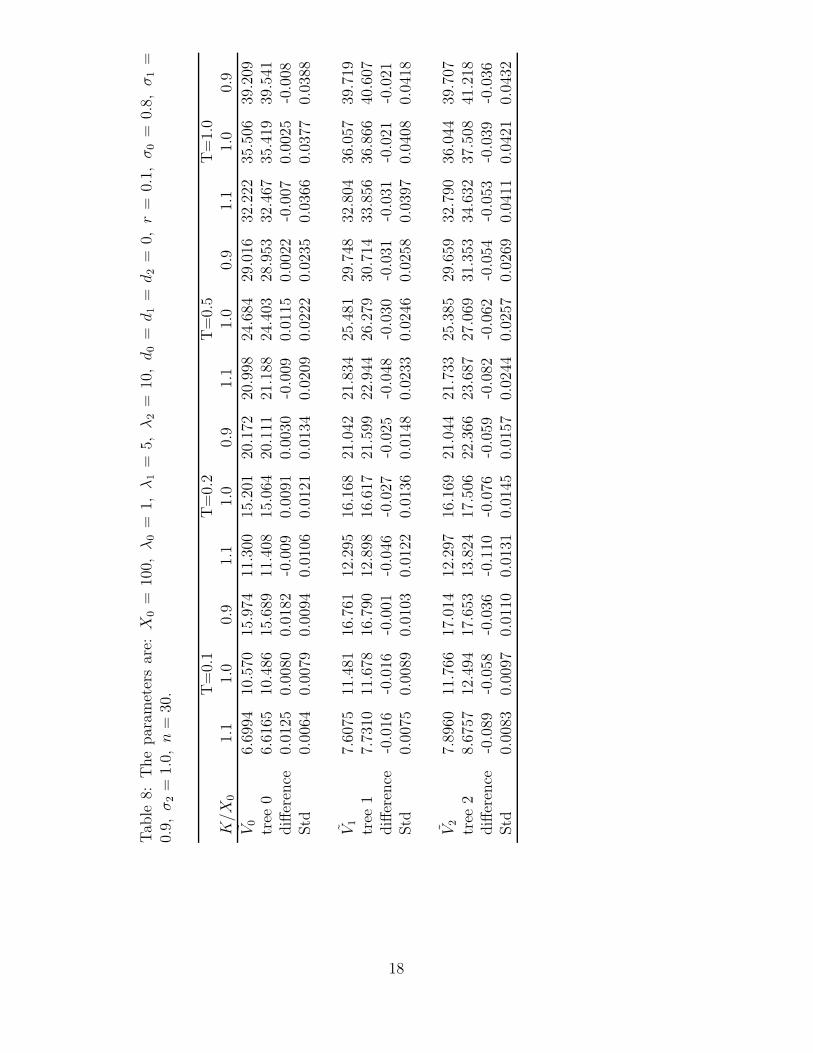

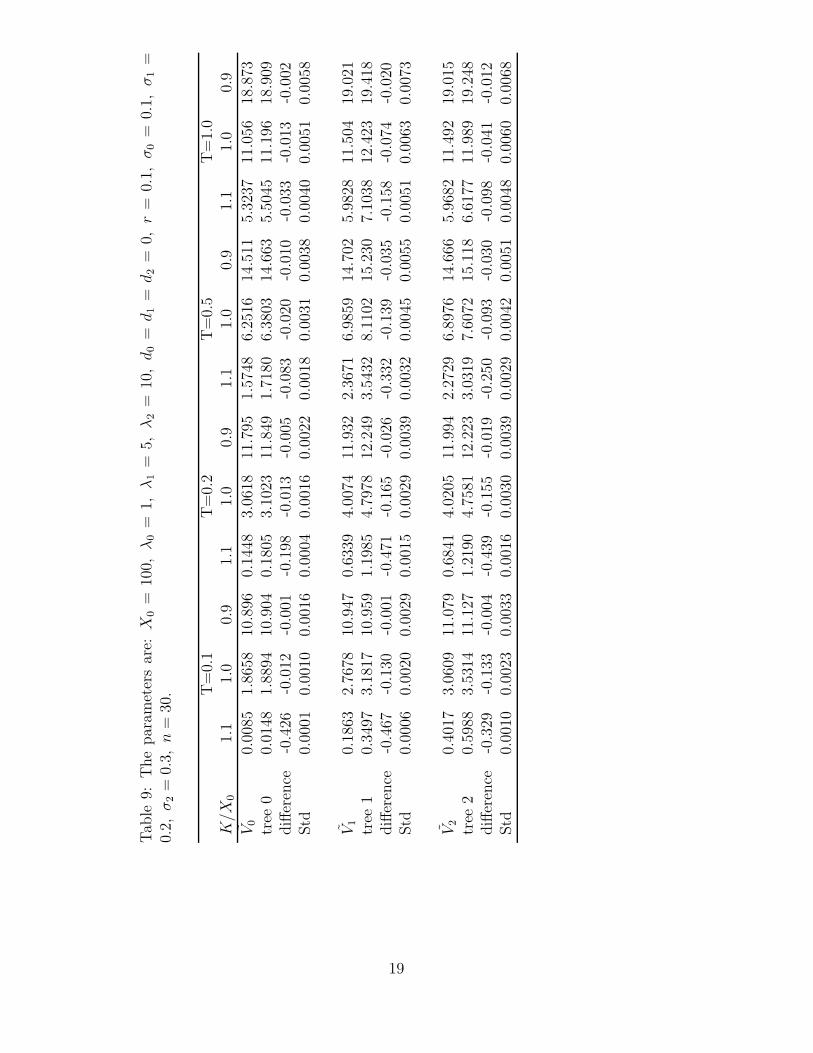

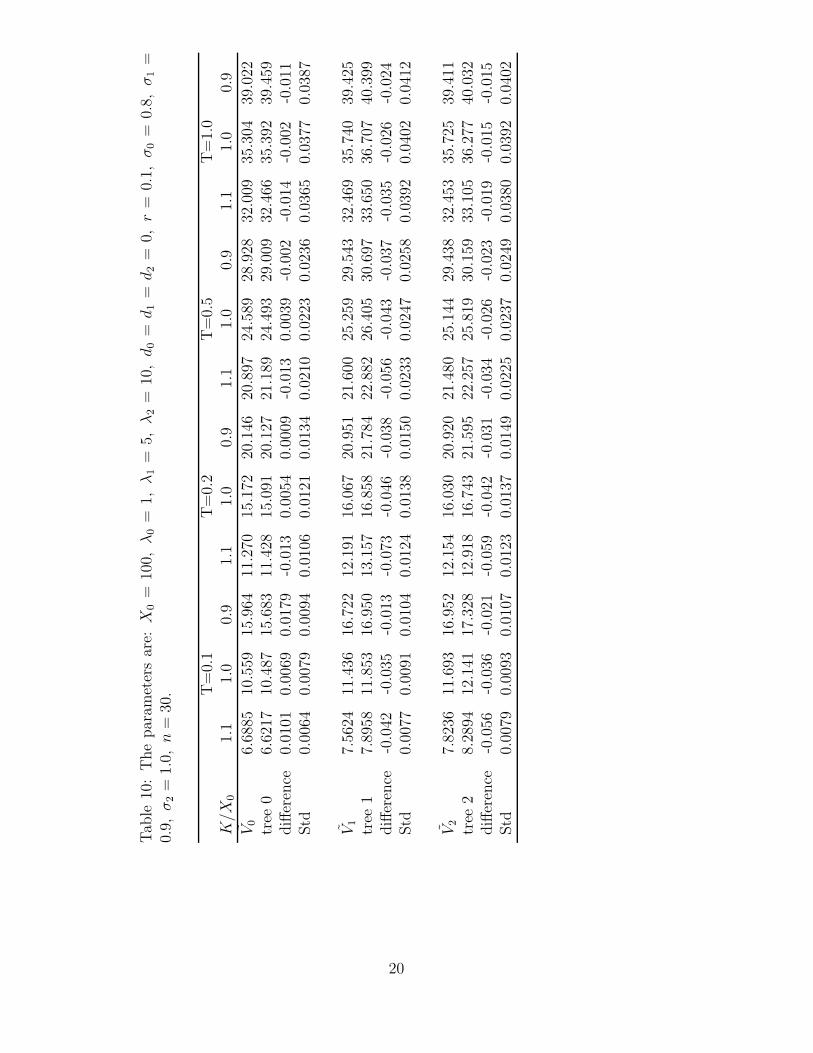

approximate European call option prices for various T in a hidden Markov model with

three states. Tables 7 and 9 reports the case of low volatilities, and Tables 8 and 10

reports the case of high volatilities. The matrix of transition rates in Tables 7 and 8 is

Q2, and the matrix of transition rate in Tables 9 and 10 is Q3, which is defined as

Q3 =

−1 1 00 −5 510 0 −10

.

For each strike price K, we consider three different strike-to-stock price ratios K/X0.

They are 1.1, 1.0 and 0.9. Note that in Tables 7 to 10, the first row in each panel is

the approximate analytical prices with different initial state, whereas the second and

forth rows report Monte-Carlo tree prices and their standard deviation, respectively.

The number in the third row is error estimate between the approximation value and

15

Monte-Carlo simulation. Specifically, in Tables 7 to 10, Vi refers the approximate price

for a three state hidden Markov model with state i = 0, 1, 2.; tree i refers to Monte-Carlo

method for tree with Q2; difference is the ratio between approximate price and tree price,

i.e. difference:= (Vi − tree i)/tree i; and Std is the standard deviation of Monte-Carlo

tree prices.

Note that the option prices Vi for i = 0, 1, 2 in Table 7 is higher than the corre-

sponding option prices in Table 9. The reason can be described as follows: Although

the parameters in both tables are the same, the matrix of transition rates are different.

We use Q2 in Table 7; while Q3 in Table 9. By the definition of Q2 and Q3, it is easy to

see that the occupation time of state 0 in Q3 is longer than that of Q2, and state 0 is

the worst state. By using the same argument, we have the option prices Vi for i = 0, 1, 2

in Table 8 is higher than the corresponding option prices in Table 10. Note from Tables

1 to 10, the convergence rate of option price in approximation formula depends on the

value of λ and difference of prices from initial state.

Furthermore, we observe that the option price obtained by the approximation for-

mula (8) depends on the strike price K. It is more accurate in the cases of in the money

and at the money; while it is less accurate in the case of out of the money for each time

period. A heuristic argument based on Equation (3) can be described as follows:

We consider the case of a two state hidden Markov model for simplicity. Let K(1)

and K(2) be two given strike prices with K(1) < K(2). Without loss of generality, we

may assume σ1 > σ0; that is the volatility at state 1 is bigger than the volatility at state

0. Then from Equation (3), we have V1(T,K, r) > V0(T,K, r). It is also known from

Equation (3) again that Vi(T,K(1), r) > Vi(T,K(2), r), for i = 0, 1. Under the condition

V1(T,K(1), r)− V0(T,K(1), r)

V1(T,K(1), r)<V1(T,K(2), r)− V0(T,K(2), r)

V1(T,K(2), r), (11)

which is correct for T is not too large. Note also that |Vi(T,K(1), r)− Vi(T,K(1), r)| ≈V1(T,K(1), r) − V0(T,K(1), r), and |Vi(T,K(2), r) − Vi(T,K(2), r)| ≈ V1(T,K(2), r)−V0(T,K(2), r) for i = 0, 1. Therefore,

|V1(T,K(1), r)− V1(T,K(1), r)|V1(T,K(1), r)

<|V1(T,K(2), r)− V1(T,K(2), r)|

V1(T,K(2), r). (12)

Note that (12) is the definition of “difference” in Tables 7 to 10, and it is an increasing

function of K.

It is easy to see that under the condition (11), we also have

|V0(T,K(1), r)− V0(T,K(1), r)|V0(T,K(1), r)

<|V0(T,K(2), r)− V0(T,K(2), r)|

V0(T,K(2), r). (13)

16

Tab

le7:

The

par

amet

ers

are:

X0

=10

0,λ

0=

1,λ

1=

5,λ

2=

10,d

0=d

1=d

2=

0,r

=0.

1,σ

0=

0.1,

σ1

=0.

2,σ

2=

0.3,n

=30

. T=

0.1

T=

0.2

T=

0.5

T=

1.0

K/X

01.

11.

00.

91.

11.

00.

91.

11.

00.

91.

11.

00.

9

V0

0.01

061.

8759

10.8

960.

1600

3.08

8211

.799

1.66

406.

3350

14.5

415.

5403

11.2

2118

.949

tree

00.

0128

1.88

2910

.906

0.16

413.

0783

11.8

451.

6462

6.31

8614

.636

5.44

2111

.159

18.9

04diff

eren

ce-0

.172

-0.0

04-0

.001

-0.0

250.

0032

-0.0

040.

0108

0.00

26-0

.006

0.01

800.

0056

0.00

24Std

0.00

010.

0010

0.00

160.

0004

0.00

160.

0022

0.00

180.

0031

0.00

370.

0040

0.00

510.

0058

V1

0.19

482.

8094

10.9

490.

6870

4.09

9511

.947

2.57

537.

1804

14.7

716.

3232

11.7

6319

.139

tree

10.

2884

3.01

4010

.925

1.01

734.

5460

12.1

783.

3714

7.95

8215

.187

7.16

5612

.484

19.5

08diff

eren

ce-0

.325

-0.0

680.

0022

-0.3

25-0

.098

-0.0

19-0

.236

-0.0

98-0

.027

-0.1

18-0

.058

-0.0

19Std

0.00

060.

0018

0.00

280.

0013

0.00

270.

0036

0.00

310.

0044

0.00

540.

0053

0.00

650.

0074

V2

0.41

553.

1278

11.0

820.

7567

4.14

6512

.015

2.49

817.

1080

14.7

416.

3108

11.7

5319

.134

tree

20.

7362

3.84

1111

.191

1.70

755.

4005

12.4

734.

2281

8.76

9315

.632

8.01

1113

.153

19.8

73diff

eren

ce-0

.436

-0.1

86-0

.010

-0.5

57-0

.232

-0.0

37-0

.409

-0.1

89-0

.057

-0.2

12-0

.106

-0.0

37Std

0.00

110.

0025

0.00

350.

0020

0.00

340.

0045

0.00

380.

0051

0.00

610.

0059

0.00

710.

0081

17

Tab

le8:

The

par

amet

ers

are:

X0

=10

0,λ

0=

1,λ

1=

5,λ

2=

10,d

0=d

1=d

2=

0,r

=0.

1,σ

0=

0.8,

σ1

=0.

9,σ

2=

1.0,n

=30

. T=

0.1

T=

0.2

T=

0.5

T=

1.0

K/X

01.

11.

00.

91.

11.

00.

91.

11.

00.

91.

11.

00.

9

V0

6.69

9410

.570

15.9

7411

.300

15.2

0120

.172

20.9

9824

.684

29.0

1632

.222

35.5

0639

.209

tree

06.

6165

10.4

8615

.689

11.4

0815

.064

20.1

1121

.188

24.4

0328

.953

32.4

6735

.419

39.5

41diff

eren

ce0.

0125

0.00

800.

0182

-0.0

090.

0091

0.00

30-0

.009

0.01

150.

0022

-0.0

070.

0025

-0.0

08Std

0.00

640.

0079

0.00

940.

0106

0.01

210.

0134

0.02

090.

0222

0.02

350.

0366

0.03

770.

0388

V1

7.60

7511

.481

16.7

6112

.295

16.1

6821

.042

21.8

3425

.481

29.7

4832

.804

36.0

5739

.719

tree

17.

7310

11.6

7816

.790

12.8

9816

.617

21.5

9922

.944

26.2

7930

.714

33.8

5636

.866

40.6

07diff

eren

ce-0

.016

-0.0

16-0

.001

-0.0

46-0

.027

-0.0

25-0

.048

-0.0

30-0

.031

-0.0

31-0

.021

-0.0

21Std

0.00

750.

0089

0.01

030.

0122

0.01

360.

0148

0.02

330.

0246

0.02

580.

0397

0.04

080.

0418

V2

7.89

6011

.766

17.0

1412

.297

16.1

6921

.044

21.7

3325

.385

29.6

5932

.790

36.0

4439

.707

tree

28.

6757

12.4

9417

.653

13.8

2417

.506

22.3

6623

.687

27.0

6931

.353

34.6

3237

.508

41.2

18diff

eren

ce-0

.089

-0.0

58-0

.036

-0.1

10-0

.076

-0.0

59-0

.082

-0.0

62-0

.054

-0.0

53-0

.039

-0.0

36Std

0.00

830.

0097

0.01

100.

0131

0.01

450.

0157

0.02

440.

0257

0.02

690.

0411

0.04

210.

0432

18

Tab

le9:

The

par

amet

ers

are:

X0

=10

0,λ

0=

1,λ

1=

5,λ

2=

10,d

0=d

1=d

2=

0,r

=0.

1,σ

0=

0.1,

σ1

=0.

2,σ

2=

0.3,n

=30

. T=

0.1

T=

0.2

T=

0.5

T=

1.0

K/X

01.

11.

00.

91.

11.

00.

91.

11.

00.

91.

11.

00.

9

V0

0.00

851.

8658

10.8

960.

1448

3.06

1811

.795

1.57

486.

2516

14.5

115.

3237

11.0

5618

.873

tree

00.

0148

1.88

9410

.904

0.18

053.

1023

11.8

491.

7180

6.38

0314

.663

5.50

4511

.196

18.9

09diff

eren

ce-0

.426

-0.0

12-0

.001

-0.1

98-0

.013

-0.0

05-0

.083

-0.0

20-0

.010

-0.0

33-0

.013

-0.0

02Std

0.00

010.

0010

0.00

160.

0004

0.00

160.

0022

0.00

180.

0031

0.00

380.

0040

0.00

510.

0058

V1

0.18

632.

7678

10.9

470.

6339

4.00

7411

.932

2.36

716.

9859

14.7

025.

9828

11.5

0419

.021

tree

10.

3497

3.18

1710

.959

1.19

854.

7978

12.2

493.

5432

8.11

0215

.230

7.10

3812

.423

19.4

18diff

eren

ce-0

.467

-0.1

30-0

.001

-0.4

71-0

.165

-0.0

26-0

.332

-0.1

39-0

.035

-0.1

58-0

.074

-0.0

20Std

0.00

060.

0020

0.00

290.

0015

0.00

290.

0039

0.00

320.

0045

0.00

550.

0051

0.00

630.

0073

V2

0.40

173.

0609

11.0

790.

6841

4.02

0511

.994

2.27

296.

8976

14.6

665.

9682

11.4

9219

.015

tree

20.

5988

3.53

1411

.127

1.21

904.

7581

12.2

233.

0319

7.60

7215

.118

6.61

7711

.989

19.2

48diff

eren

ce-0

.329

-0.1

33-0

.004

-0.4

39-0

.155

-0.0

19-0

.250

-0.0

93-0

.030

-0.0

98-0

.041

-0.0

12Std

0.00

100.

0023

0.00

330.

0016

0.00

300.

0039

0.00

290.

0042

0.00

510.

0048

0.00

600.

0068

19

Tab

le10

:T

he

par

amet

ers

are:X

0=

100,

λ0

=1,

λ1

=5,

λ2

=10,d

0=d

1=d

2=

0,r

=0.

1,σ

0=

0.8,

σ1

=0.

9,σ

2=

1.0,n

=30

. T=

0.1

T=

0.2

T=

0.5

T=

1.0

K/X

01.

11.

00.

91.

11.

00.

91.

11.

00.

91.

11.

00.

9

V0

6.68

8510

.559

15.9

6411

.270

15.1

7220

.146

20.8

9724

.589

28.9

2832

.009

35.3

0439

.022

tree

06.

6217

10.4

8715

.683

11.4

2815

.091

20.1

2721

.189

24.4

9329

.009

32.4

6635

.392

39.4

59diff

eren

ce0.

0101

0.00

690.

0179

-0.0

130.

0054

0.00

09-0

.013

0.00

39-0

.002

-0.0

14-0

.002

-0.0

11Std

0.00

640.

0079

0.00

940.

0106

0.01

210.

0134

0.02

100.

0223

0.02

360.

0365

0.03

770.

0387

V1

7.56

2411

.436

16.7

2212

.191

16.0

6720

.951

21.6

0025

.259

29.5

4332

.469

35.7

4039

.425

tree

17.

8958

11.8

5316

.950

13.1

5716

.858

21.7

8422

.882

26.4

0530

.697

33.6

5036

.707

40.3

99diff

eren

ce-0

.042

-0.0

35-0

.013

-0.0

73-0

.046

-0.0

38-0

.056

-0.0

43-0

.037

-0.0

35-0

.026

-0.0

24Std

0.00

770.

0091

0.01

040.

0124

0.01

380.

0150

0.02

330.

0247

0.02

580.

0392

0.04

020.

0412

V2

7.82

3611

.693

16.9

5212

.154

16.0

3020

.920

21.4

8025

.144

29.4

3832

.453

35.7

2539

.411

tree

28.

2894

12.1

4117

.328

12.9

1816

.743

21.5

9522

.257

25.8

1930

.159

33.1

0536

.277

40.0

32diff

eren

ce-0

.056

-0.0

36-0

.021

-0.0

59-0

.042

-0.0

31-0

.034

-0.0

26-0

.023

-0.0

19-0

.015

-0.0

15Std

0.00

790.

0093

0.01

070.

0123

0.01

370.

0149

0.02

250.

0237

0.02

490.

0380

0.03

920.

0402

20

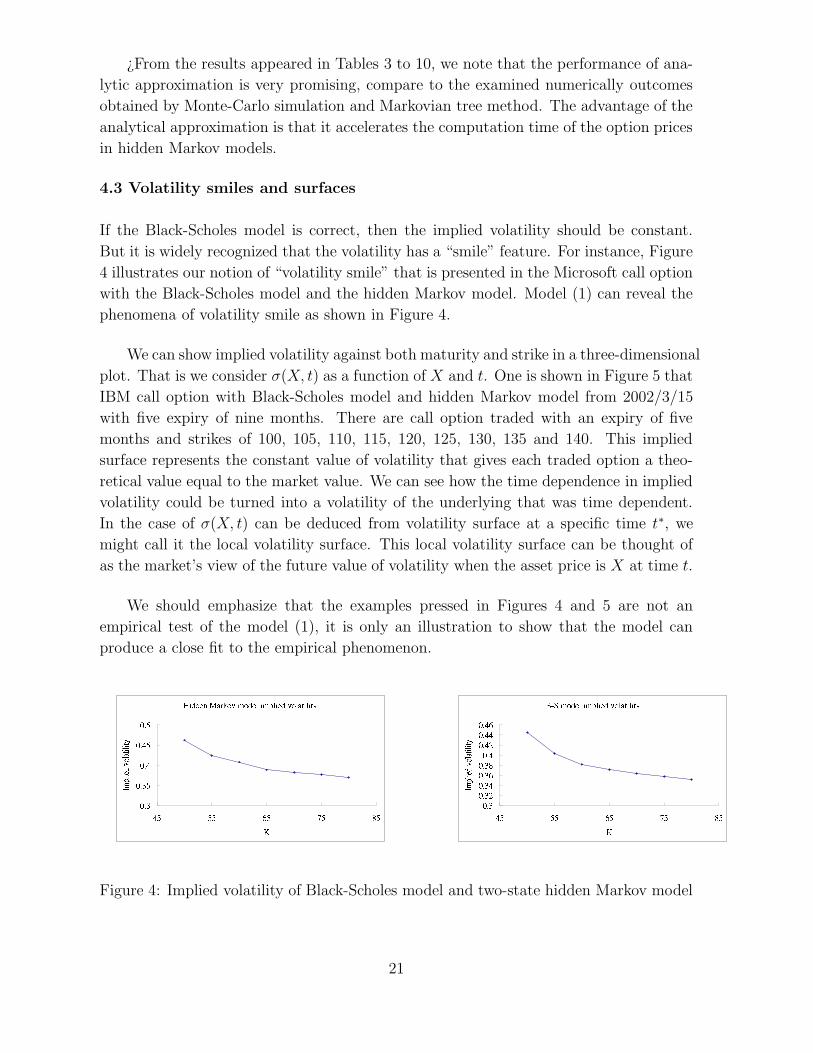

¿From the results appeared in Tables 3 to 10, we note that the performance of ana-

lytic approximation is very promising, compare to the examined numerically outcomes

obtained by Monte-Carlo simulation and Markovian tree method. The advantage of the

analytical approximation is that it accelerates the computation time of the option prices

in hidden Markov models.

4.3 Volatility smiles and surfaces

If the Black-Scholes model is correct, then the implied volatility should be constant.

But it is widely recognized that the volatility has a “smile” feature. For instance, Figure

4 illustrates our notion of “volatility smile” that is presented in the Microsoft call option

with the Black-Scholes model and the hidden Markov model. Model (1) can reveal the

phenomena of volatility smile as shown in Figure 4.

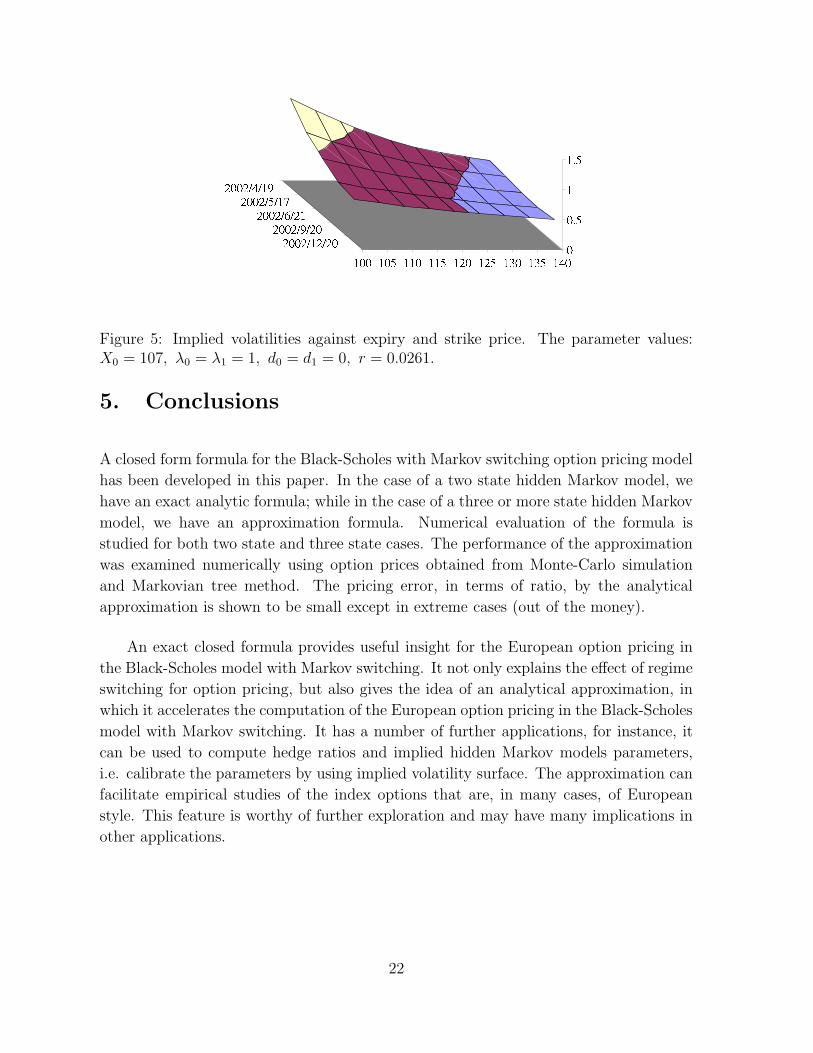

We can show implied volatility against both maturity and strike in a three-dimensional

plot. That is we consider σ(X, t) as a function of X and t. One is shown in Figure 5 that

IBM call option with Black-Scholes model and hidden Markov model from 2002/3/15

with five expiry of nine months. There are call option traded with an expiry of five

months and strikes of 100, 105, 110, 115, 120, 125, 130, 135 and 140. This implied

surface represents the constant value of volatility that gives each traded option a theo-

retical value equal to the market value. We can see how the time dependence in implied

volatility could be turned into a volatility of the underlying that was time dependent.

In the case of σ(X, t) can be deduced from volatility surface at a specific time t∗, we

might call it the local volatility surface. This local volatility surface can be thought of

as the market’s view of the future value of volatility when the asset price is X at time t.

We should emphasize that the examples pressed in Figures 4 and 5 are not an

empirical test of the model (1), it is only an illustration to show that the model can

produce a close fit to the empirical phenomenon.

D=E FGFHI@JLKNM OGPGQ@RSPFGHTE RVUT E HFVQPGT KNW E T E W X

YZ [YZ [G\YZ ]YZ ]\YZ \

]\ \G\ ^G\ _\ `\a

b cdef gh ije klfef l m

no pSqSrsGtuv qVwu v tsVxrGu yNz v u v z

| ~| ~| ~| ~G| ~| | | G|

G

Figure 4: Implied volatility of Black-Scholes model and two-state hidden Markov model

21

-C+ " =

=- == " ==

Figure 5: Implied volatilities against expiry and strike price. The parameter values:X0 = 107, λ0 = λ1 = 1, d0 = d1 = 0, r = 0.0261.

5. Conclusions

A closed form formula for the Black-Scholes with Markov switching option pricing model

has been developed in this paper. In the case of a two state hidden Markov model, we

have an exact analytic formula; while in the case of a three or more state hidden Markov

model, we have an approximation formula. Numerical evaluation of the formula is

studied for both two state and three state cases. The performance of the approximation

was examined numerically using option prices obtained from Monte-Carlo simulation

and Markovian tree method. The pricing error, in terms of ratio, by the analytical

approximation is shown to be small except in extreme cases (out of the money).

An exact closed formula provides useful insight for the European option pricing in

the Black-Scholes model with Markov switching. It not only explains the effect of regime

switching for option pricing, but also gives the idea of an analytical approximation, in

which it accelerates the computation of the European option pricing in the Black-Scholes

model with Markov switching. It has a number of further applications, for instance, it

can be used to compute hedge ratios and implied hidden Markov models parameters,

i.e. calibrate the parameters by using implied volatility surface. The approximation can

facilitate empirical studies of the index options that are, in many cases, of European

style. This feature is worthy of further exploration and may have many implications in

other applications.

22

References

Anderson, T. G. (1996). Return volatility and trading volume: an information

flow interpretation of stochastic volatility. Journal of Finance, 51, 169-204.

Avellaneda, M., Levy, P., and Paras, A. (1995). Pricing and hedging derivative

securities in markets with uncertain volatilities. Applied Mathematical Finance, 2,

73-88.

Bittlingmayer, G. (1998). Output, stock volatility and political uncertainty in a

natural experiment: Germany, 1880-1940. Journal of Finance, 53, 2243-2257.

Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities.

Journal of Political Economy, 81, 637-654.

Cox, J., Ross, S., and Rubinstein, M. (1979). Option pricing, a simplified approach.

Journal of Financial Economics, 7, 229-263.

David, A. (1997). Fluctuating confidence in stock markets: Implications for re-

turns and volatility. Journal of Financial and Quantitative Analysis, 32, 427-462.

Detemple, J. B. (1991). Further results on asset pricing with incomplete informa-

tion. Journal of Economic Dynamics and Control, 15, 425-453.

Di Masi, G. B., Kabanov, Yu, M., and Runggaldier, W. J. (1994). Mean-variance

hedging of options on stocks with Markov volatility. Theory of Probability and Its

Applications, 39, 173-181.

Diebold, F. X., and Inoue, A. (2001). Long memory and regime switching. Journal

of Econometrics, 105, 131-159.

Duffie, D., and Huang, C. F. (1986). Multiperiod security markets with differential

information. Journal of Mathematical Economics, 15, 283-303.

Follmer, H. and Sondermann, D. (1986). Hedging of nonredundant contingent

claims. In: Hildenbrand and Mas-Colell, eds., Contributions to Mathematical

Economics, 205-223.

Grorud, A., and Pontier, M., (1998). Insider trading in a continuous time market

model. International Journal of Theoretical and Applied Finance, 1, 331-347.

Guilaume, D. M., Dacorogna, M., Dave, R., Muller, U., Olsen, R., and Pictet, P.

(1997). ¿From the bird’s eye to the microscope, a survey of stylized facts of the

intra-daily foreign exchange market. Finance and Stochastics, 1, 95-129.

Guo, X. (2001). Information and option pricing. Journal of Quantitative Finance,

1, 38-44.

23

Hamilton, J. D. (1988). Rational-Expectations econometric analysis of changes in

regime: an investigation of term structure of interest rates. Journal of Economic

Dynamics and Control, 12, 385-423.

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary

time series and the business cycle. Econometrica, 57, 357-384.

Hamilton, J. D., and Susmel, R. (1994). Autoregressive conditional heteroscedas-

ticity and changes in regime. Journal of Econometrics, 64, 307-333.

Heston, S. L. (1993). A closed-form solution for options with stochastic volatility

with applications to bond and currency options. Review of Financial Studies, 6,

327-343.

Hull, J. and White, A. (1987). The pricing of options on assets with stochastic

volatility. Journal of Finance, 2, 281-300.

Karatzas, I., and Pikovsky, I. (1996). Anticipative portfolio optimization. Ad-

vances in Applied Probability, 28, 1095-1122.

McKean, H. P. (1969). Stochastic Integrals. Academic Press, New York.

Ross, S. A. (1989). Information and volatility, the no-arbitrage martingale ap-

proach to timing and resolution irrelevancy. Journal of Finance, 44, 1-8.

Schweizer, M. (1991). Option hedging for semimartingales. Stochastic Processes

and their Applications, 37, 339-363.

So, M. K. P., Lam, K., and Li, W. K. (1998). A stochastic volatility model with

Markov switching. Journal of Business & Economic Statistics, 16, 244-253.

Stein, E. M., and Stein, C. J. (1991). Stock prices distribution with stochastic

volatility, an analytic approach. Review of Financial Studies, 4, 727-752.

Turner, C., Startz, R., and Nelson, C. (1989). A Markov model of heteroscendas-

ticity, risk, and learning in the stock market. Journal of Financial Economics, 25,

3-22.

Veronesi, P. (1999). Stock market overreaction to bad news in good times: a