20

| Date post: | 17-Jul-2015 |

| Category: |

Economy & Finance |

| Upload: | grape |

| View: | 41 times |

| Download: | 0 times |

Up or down the value chain?A comparative analysis of the GVC position of the economies of the

NMS

Jan Hagemejer1 & Mahdi Ghodsi2

1NBP & University of Warsaw 2WIIW & UoWFunded by NSC grant no 2013/09/D/HS4/01519

February 27, 2015

Motivation: NMS production shares

Source: WIOD

I NMS maintain a high share of manufacturing in total output...

I ...despite ongoing growth in the service sector

I �The NMS are the backbone of the German manufacturing�

Motivation (2): NMS trade partners shares

Figure: Trade structure

Source: WIOD

I European integration has brought a relative increase of intra-NMStrade...

I ... but the fragmentation and globalization processes have boostedimports and exports from/to China and RoW

I International trade in substitutes or complements (competition vscooperation)?

Motivation (3): NMS production and trade structure

Figure: Imports, exports and output

Figure: Share of intermediates in exports and imports

Questions

I Q: What is the overall position of the NMS in the global value chain(GVC)?

I Q: Do NMS compete with China and other emerging markets or theEU15?

I Q: What is the sectoral composition of output that determines theposition of countries in the GVC?

I A: (Relatively) new data sources

I A: The upstreamness measure - the distance from �nal demand.

I This work is an INPUT to a larger project.

Upstreamness measure (1)

I Antras, Chor, Fally, and Hillberry [2012]: Output of sector is a sumof the �nal and intermediate demand

Yi = Xi+N∑j=1

zijYj

I Substituting recursively:

Yi = Xi+N∑j=1

zijXj+N∑j=1

N∑k=1

zijzjkXj+N∑j=1

N∑k=1

N∑l=1

zijzjkzklXj + · · ·

I Each element corresponds to one production stage. The distancefrom �nal demand is de�ned as a weighted average:

ui = 1· Xi

Yi+2·

N∑j=1

zijXj

Yi+3·

N∑j=1

N∑k=1

zijzjkXj

Yi+4·

N∑j=1

N∑k=1

N∑l=1

zijzjkzklXj

Yi+· · ·

(if only �nal demandui = 1)

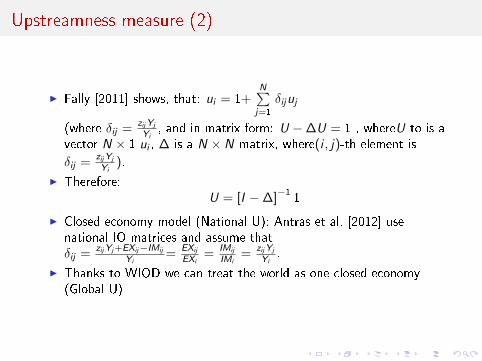

Upstreamness measure (2)

I Fally [2011] shows, that: ui = 1+N∑j=1

δijuj

(where δij =zijYj

Yi, and in matrix form: U − ∆U = 1 , whereU to is a

vector N × 1 ui , ∆ is a N × N matrix, where(i , j)-th element is

δij =zijYj

Yi).

I Therefore:U = [I − ∆]−1

1

I Closed economy model (National U): Antras et al. [2012] usenational IO matrices and assume thatδij =

zijYj+EXij−IMij

Yi=

EXij

EXi=

IMij

IMi=

zijYj

Yi.

I Thanks to WIOD we can treat the world as one closed economy(Global U)

World input-output database

I 1435x1435 input-output matrix:

I �nal demand and its sources in each countryI intermediate demand across sectors AND countries for each sector

AND country

I 35 sectors (NACE/CPA)

I 40 countries and RoW (UE, OECD)

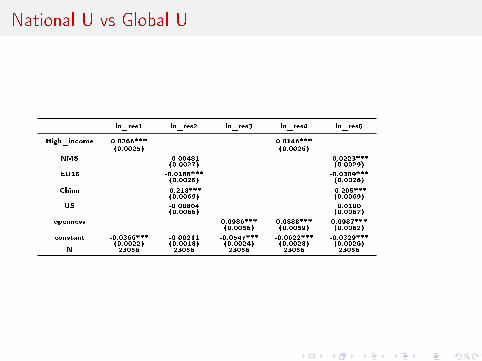

National U vs Global U

Figure: Global vs country-level upstreamness

Source: own calculations using WIOD data.

National U vs Global U

ln_res1 ln_res2 ln_res3 ln_res4 ln_res5

High_income 0.0266*** 0.0146***(0.0025) (0.0026)

NMS -0.00481 -0.0223***(0.0027) (0.0029)

EU15 -0.0188*** -0.0309***(0.0025) (0.0026)

China -0.218*** -0.205***(0.0069) (0.0069)

US -0.00804 0.0100(0.0066) (0.0067)

openness 0.0986*** 0.0888*** 0.0987***(0.0056) (0.0059) (0.0062)

constant -0.0366*** -0.00211 -0.0547*** -0.0622*** -0.0329***(0.0022) (0.0018) (0.0024) (0.0028) (0.0026)

N 23056 23056 23056 23056 23056

Global U: ongoing fragmentation and growth ofmanufacturing

Figure: Global and sectoral U. Shares in global output

Source: own calculations using WIOD data.

Manufacturing vs Overall Economies

Figure: Overall U (L) vs U for manufacturing (R)

Source: own calculations using WIOD data.

Imports vs exports

Figure: U weighted by exports and imports

Source: own calculations using WIOD data.

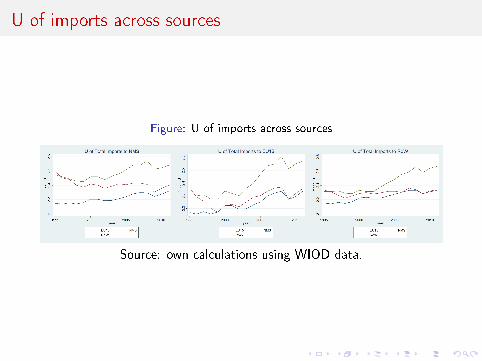

U of imports across sources

Figure: U of imports across sources

Source: own calculations using WIOD data.

Evolution of manufacturing structures

Figure: Evolution of industry shares for NMS

Source: own calculations using WIOD data.

Structure of manufacturing

Table: Structure of NMS manufacturing in 2011

Sector Share in output Share in exports

Leather, Leather and Footwear 0,6% 1,0%

Wood and Products of Wood and Cork 3,0% 2,0%

Textiles and Textile Products 3,0% 4,0%

Manufacturing, Nec; Recycling 3,7% 4,3%

Other Non-Metallic Mineral 4,1% 2,0%

Pulp, Paper, Paper , Printing and Publishing 4,7% 2,6%

Rubber and Plastics 5,5% 5,5%

Chemicals and Chemical Products 6,4% 8,1%

Coke, Re�ned Petroleum and Nuclear Fuel 6,9% 4,4%

Machinery, Nec 7,6% 9,7%

Electrical and Optical Equipment 11,8% 19,0%

Basic Metals and Fabricated Metal 13,2% 11,9%

Transport Equipment 14,0% 18,8%

Food, Beverages and Tobacco 15,4% 6,7%

Source: own calculations using WIOD

Selected sectors (with high output shares)

Across NMS...

Figure: U of the NMS (export-weighted)

Source: own calculations using WIOD data.

The pipeline

I Local vs global U:

I distill EU integration e�ects from world trendsI sectoral composition vs within sector changesI geographical composition vs sectoral compostition.

I U as a determinant of bilateral value added trade �ows

I Upstreamness vs domestic VA in exports - how does the relativeposition in the GVC translate to domestic VA creation?

I Upstreamness vs knowledge spillovers from FDI - do technologyspillovers depend on the distance from �nal demand?

Bibliography

Pol Antras, Davin Chor, Thibault Fally, and Russell Hillberry. Measuringthe Upstreamness of Production and Trade Flows. American Economic

Review, 102(3):412�16, May 2012.

Thibault Fally. On the fragmentation of production in the us. Universityof Colorado mimeo, 2011.