A Computable General Equilibrium Model of Energy Taxation André J. Barbé Department of Economics Rice University International Association for Energy Economics June 16, 2014 Barbé A New Model of Energy Taxation 1 / 29

Transcript

A Computable General Equilibrium Modelof Energy Taxation

André J. Barbé

Department of EconomicsRice University

International Association for Energy EconomicsJune 16, 2014

Barbé A New Model of Energy Taxation 1 / 29

Motivation

Background:Corporate income tax reform is always a hot topicObama’s 2014 budget eliminates deductions for fossil fuelsAdministration says these deductions favor fossil fuels

Complication:Current energy tax models are missing key issues

Barbé A New Model of Energy Taxation 2 / 29

My contribution

Key problems:Does the budget improve tax neutrality or social efficiency?How important are the issues previous models are missing?

SolutionCreate new energy tax modelInclude all key issues of energy taxation in my modelUse model to determine the social efficiency of the budgetproposal

Barbé A New Model of Energy Taxation 3 / 29

Outline

1 IntroductionWhat are the proposed changes?Why is a computable general equilibrium (CGE) modelthe best way to examine this tax reform?

2 ModelHow does my model improve on previous literature?

3 ResultsTax reform increases social welfare if carbonexternalities are at least $14 per tonMy model’s innovations are important

Barbé A New Model of Energy Taxation 4 / 29

Budget increases taxes on fossil fuel

Budget proposal changes a number of provisions inthe corporate income tax

Supporters say budget eliminates tax preferences forfossil fuels

Tax neutralityA tax system is neutral if it does not favor any type ofeconomic activity over anotherRelated to social efficiency

Budget identifies areas that need reform but does notaccomplish reform

Barbé A New Model of Energy Taxation 6 / 29

LIFO inventory accounting changes

Table 1 : Taxation of Inventory Appreciation

Inflationary RealAppreciation Appreciation

Current Law No Tax No TaxBudget Proposal Tax TaxNeutral Tax System No Tax Tax

Current law taxes too little, budget proposal too much

Barbé A New Model of Energy Taxation 7 / 29

Are taxes higher or lower on fossil fuels thanother sectors?

Marginal Effective Tax Rate (METR) on investment is the metricused by the literature to measure tax rates

CBO (2005): 9% to 25% for fossil fuel assets and 24% forall business assetsMackie (2002): 25% to 36% for fossil fuel industries and20% for entire economy

Barbé A New Model of Energy Taxation 8 / 29

Modeling energy taxes

Barbé A New Model of Energy Taxation 9 / 29

3 main issues determine the social efficiencyof energy taxes

1 Substitution between different goods

Taxing fossil fuels at different rates than other goods leads toproductive inefficiency due to substitution away from themore taxed goods

2 Energy resource supply

If energy resources are inelastically supplied, there is littleinefficiency to taxing them

3 ExternalitiesTaxes internalize costs from climate change

Barbé A New Model of Energy Taxation 10 / 29

3 main issues determine the social efficiencyof energy taxes

1 Substitution between different goods

Taxing fossil fuels at different rates than other goods leads toproductive inefficiency due to substitution away from themore taxed goods

2 Energy resource supply

If energy resources are inelastically supplied, there is littleinefficiency to taxing them

3 ExternalitiesTaxes internalize costs from climate change

Barbé A New Model of Energy Taxation 10 / 29

3 main issues determine the social efficiencyof energy taxes

1 Substitution between different goods

Taxing fossil fuels at different rates than other goods leads toproductive inefficiency due to substitution away from themore taxed goods

2 Energy resource supply

If energy resources are inelastically supplied, there is littleinefficiency to taxing them

3 ExternalitiesTaxes internalize costs from climate change

Barbé A New Model of Energy Taxation 10 / 29

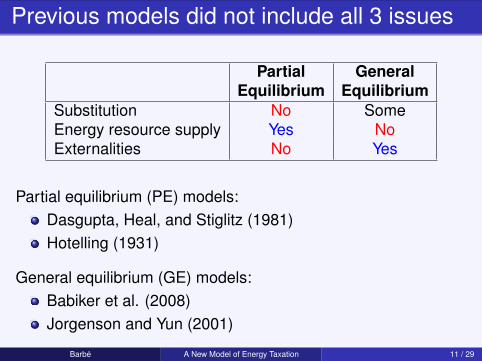

Previous models did not include all 3 issues

Partial GeneralEquilibrium Equilibrium

Substitution No SomeEnergy resource supply Yes NoExternalities No Yes

Partial equilibrium (PE) models:Dasgupta, Heal, and Stiglitz (1981)Hotelling (1931)

General equilibrium (GE) models:Babiker et al. (2008)Jorgenson and Yun (2001)

Barbé A New Model of Energy Taxation 11 / 29

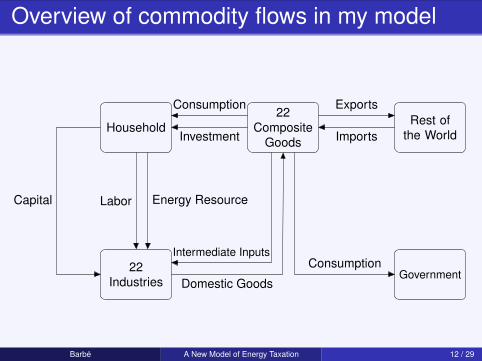

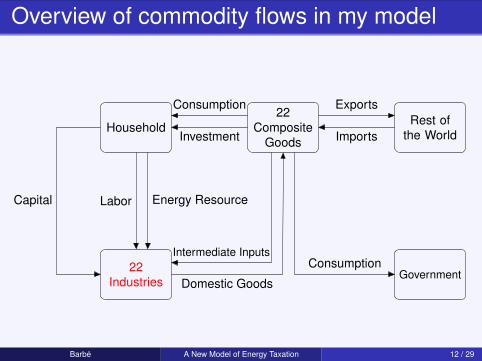

Overview of commodity flows in my model

22Composite

GoodsHousehold

22Industries

Rest ofthe World

Government

Labor Energy ResourceCapital

Domestic Goods

Imports

Intermediate Inputs

Exports

Investment

Consumption

Consumption

Barbé A New Model of Energy Taxation 12 / 29

Overview of commodity flows in my model

22Composite

GoodsHousehold

22Industries

Rest ofthe World

Government

Labor Energy ResourceCapital

Domestic Goods

Imports

Intermediate Inputs

Exports

Investment

Consumption

Consumption

Barbé A New Model of Energy Taxation 12 / 29

Overview of commodity flows in my model

22Composite

GoodsHousehold

22Industries

Rest ofthe World

Government

Labor Energy ResourceCapital

Domestic Goods

Imports

Intermediate Inputs

Exports

Investment

Consumption

Consumption

Barbé A New Model of Energy Taxation 12 / 29

Overview of commodity flows in my model

22Composite

GoodsHousehold

22Industries

Rest ofthe World

Government

Labor Energy ResourceCapital

Domestic Goods

Imports

Intermediate Inputs

Exports

Investment

Consumption

Consumption

Barbé A New Model of Energy Taxation 12 / 29

Substitution

Barbé A New Model of Energy Taxation 13 / 29

Cost and expenditure functional forms

Fixed coefficient (Leontief)No substitutionCannot capture productive inefficiency at all

Constant elasticity of substitution (CES)Restricts all inputs to have the same elasticity of substitution

TranslogAllows for different elasticities of substitution for each pair ofinputsCan accurately model productive inefficiency

Barbé A New Model of Energy Taxation 14 / 29

Regression

Use regression to find credible parameter values for the costfunction

Cost share of input i for industry x at time t :

sharexit =∑N

j=1 βsubstitutionxij ln (pricexit) + βtrend

xi year + βconstantxi

Problems with estimating this equation:Cost shares are endogenous to input pricesCost share error terms are correlated

Iterated 3-stage least-squares solves both of these problems

Barbé A New Model of Energy Taxation 15 / 29

Data sources for regression

Regression needs data on prices and cost shares foreach industry and input

Data sources for regression describe the USeconomy from 1960-2010

Jorgenson (2007)BEA

NIPA (National Income and Product Accounts)Gross output price index

Barbé A New Model of Energy Taxation 16 / 29

Energy Resource

Barbé A New Model of Energy Taxation 17 / 29

Energy resource supply

An energy resource is required to produce fossil fuels

This resource has isoelastic supply

Determine impact of resource supply by runningsimulation multiple times with different elasticities

Barbé A New Model of Energy Taxation 18 / 29

Externalities

Barbé A New Model of Energy Taxation 19 / 29

Externalities

There is disagreement about carbon externalities so Iavoid the debate entirely

Calculate social cost of carbon for which budget hasno net effect on welfare

Social cost of carbon =Equivalent variation

Reduction in emissions

Barbé A New Model of Energy Taxation 20 / 29

Results

Barbé A New Model of Energy Taxation 21 / 29

Budget is inefficient without externalities

Table 2 : The Effects of the Budget Proposal

Percent Change inSpecification Welfare Capital Stock EmploymentBaseline -0.50 -0.04 -0.01

The budget proposal decreases household welfare, capitalstock, and employment, but also emissions

Social cost of carbon must be at least $14 for the budgetproposal to be welfare neutral

Barbé A New Model of Energy Taxation 22 / 29

What is the intuition behindthese results?

Barbé A New Model of Energy Taxation 23 / 29

Budget decreases productivity

Table 3 : The Effects of the Budget Proposal on Productivity

Percent Change in Productivity ofSpecification Capital LaborBaseline -0.09 -0.06

Costs of the budget proposal come from decreased productivity

Worse allocation of capital, labor, and consumption across uses

Lower productivity means lower income, output, and welfare

Barbé A New Model of Energy Taxation 24 / 29

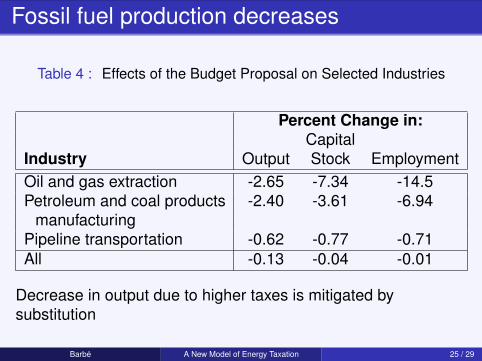

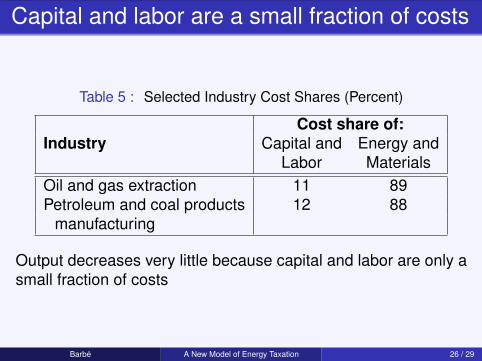

Fossil fuel production decreases

Table 4 : Effects of the Budget Proposal on Selected Industries

Percent Change in:Capital

Industry Output Stock EmploymentOil and gas extraction -2.65 -7.34 -14.5Petroleum and coal products -2.40 -3.61 -6.94

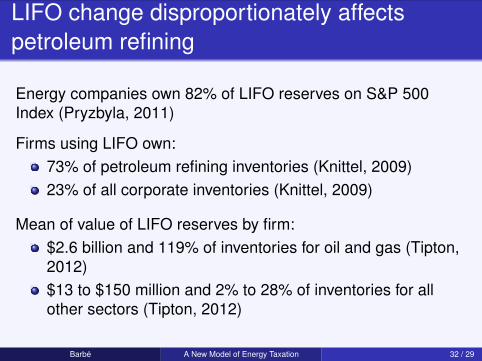

Energy companies own 82% of LIFO reserves on S&P 500Index (Pryzbyla, 2011)

Firms using LIFO own:73% of petroleum refining inventories (Knittel, 2009)23% of all corporate inventories (Knittel, 2009)

Mean of value of LIFO reserves by firm:$2.6 billion and 119% of inventories for oil and gas (Tipton,2012)$13 to $150 million and 2% to 28% of inventories for allother sectors (Tipton, 2012)

Barbé A New Model of Energy Taxation 32 / 29

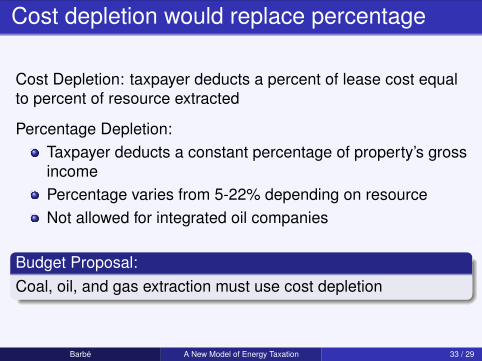

Cost depletion would replace percentage

Cost Depletion: taxpayer deducts a percent of lease cost equalto percent of resource extracted

Percentage Depletion:Taxpayer deducts a constant percentage of property’s grossincomePercentage varies from 5-22% depending on resourceNot allowed for integrated oil companies

Budget Proposal:Coal, oil, and gas extraction must use cost depletion

Barbé A New Model of Energy Taxation 33 / 29

Percentage depletion is not first-best but maybe second

Non-neutral in a first best world:Percentages based on resource extractedEligibility based on organizational formDeduction not based on actual cost of capital invested

Offset other distortionary features:Severance taxesExcise taxes

Barbé A New Model of Energy Taxation 34 / 29

US taxes foreign source income but creditstaxes paid

Territorial tax system:Does not tax foreign source income

Worldwide tax system:Does tax foreign source incomeCredit for certain foreign taxes

Dual capacity:A foreign tax is creditable if it is not payment for a specificeconomic benefitA dual-capacity taxpayer has some non-creditable taxes

Barbé A New Model of Energy Taxation 35 / 29

Firms could only credit income tax

What foreign taxes are creditable?Facts and circumstances method: tax creditable if not forspecific economic benefitSafe harbor method: credit an amount equal to hostcountry’s generally imposed income tax rate

Budget Proposal:Firms must credit an amount equal to host country’s income taxrate for other industries

Barbé A New Model of Energy Taxation 36 / 29

No consensus on taxation of foreign sourceincome

Is budget method more accurate than facts andcircumstances method?

Should foreign source income be taxed at all?Kleinbard (2007) and Gravelle (2012) say yesDesai and Hines (2004) says no

Barbé A New Model of Energy Taxation 37 / 29

Taxes excluded from METR are significant

Figure 1 : Taxes paid by Fossil Fuel Producers in 1998-2009

Source: Author’s calculation from Bureau of Economic Analysis (BEA)US Input-Output Accounts and NIPA Table 6.18D.

Barbé A New Model of Energy Taxation 38 / 29

Corporate prevalence by industry

Table 6 : Business Receipts in 2007 by Industry and Type of Entity(Percent)

Source: Table 3 of the Internal Revenue Service’sIntegrated Business Dataset

Barbé A New Model of Energy Taxation 39 / 29

Calculating average effective tax rates

Average effective tax rate =tax payments

tax baseWhat payments?

All corporate income and firm production taxesIncludes federal, state, and local taxes

What base?Total value of output base

Forward shifting (tax borne by consumers)Factor income base

Backward shifting (tax borne by capital or labor)

Barbé A New Model of Energy Taxation 40 / 29

Average of all taxes are higher on fossil fuels

Table 7 : Average Effective Tax Rates of All Firm Taxes by Sector,1998-2009

AETR (%)Sector Factor Income Value of OutputOil and gas extraction 19.3 12.0Petroleum and coalproducts manufacturing 20.4 5.1Pipeline transportation 16.5 7.2All fossil fuel 19.6 7.3

All sectors 10.8 5.9

Barbé A New Model of Energy Taxation 41 / 29

Average of all taxes are higher on fossil fuels

Table 7 : Average Effective Tax Rates of All Firm Taxes by Sector,1998-2009

AETR (%)Sector Factor Income Value of OutputOil and gas extraction 19.3 12.0Petroleum and coalproducts manufacturing 20.4 5.1Pipeline transportation 16.5 7.2All fossil fuel 19.6 7.3

All sectors 10.8 5.9

Barbé A New Model of Energy Taxation 41 / 29

But the AETR is incomplete too

Limitations:Firm taxes excludes those paid under the personal incometaxMarginal rates can differ greatly from average rates

Non-uniform rates may be efficiency enhancing:Externalities

Barbé A New Model of Energy Taxation 42 / 29

Most of my model is conventional

1 representative household and 22 firms

Industries are perfectly competitive with constantreturns to scale

Capital, labor, and energy resource are perfectlymobile between sectors

Consumer expenditure function and producer costfunction determine their purchases

Barbé A New Model of Energy Taxation 43 / 29

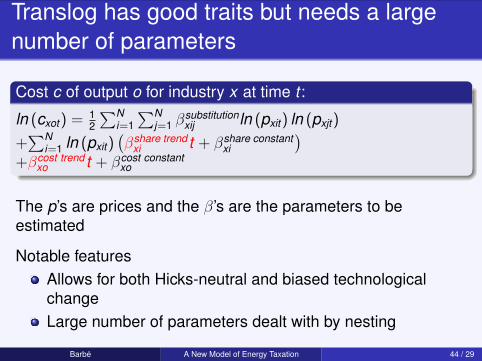

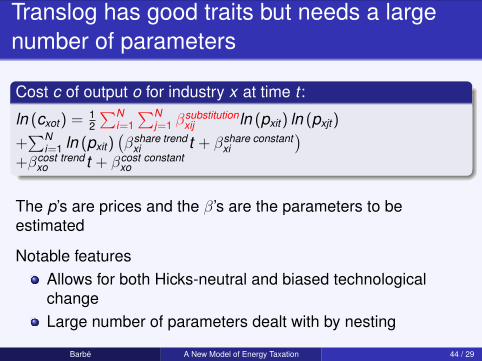

Translog has good traits but needs a largenumber of parameters

Cost c of output o for industry x at time t :

ln (cxot) =12

∑Ni=1

∑Nj=1 β

substitutionxij ln (pxit) ln (pxjt)

+∑N

i=1 ln (pxit)(βshare trend

xi t + βshare constantxi

)+βcost trend

xo t + βcost constantxo

The p’s are prices and the β’s are the parameters to beestimated

Notable featuresAllows for both Hicks-neutral and biased technologicalchangeLarge number of parameters dealt with by nesting

Barbé A New Model of Energy Taxation 44 / 29

Translog has good traits but needs a largenumber of parameters

Cost c of output o for industry x at time t :

ln (cxot) =12

∑Ni=1

∑Nj=1 β

substitutionxij ln (pxit) ln (pxjt)

+∑N

i=1 ln (pxit)(βshare trend

xi t + βshare constantxi

)+βcost trend

xo t + βcost constantxo

The p’s are prices and the β’s are the parameters to beestimated

Notable featuresAllows for both Hicks-neutral and biased technologicalchangeLarge number of parameters dealt with by nesting

Barbé A New Model of Energy Taxation 44 / 29

Translog has good traits but needs a largenumber of parameters

Cost c of output o for industry x at time t :

ln (cxot) =12

∑Ni=1

∑Nj=1 β

substitutionxij ln (pxit) ln (pxjt)

+∑N

i=1 ln (pxit)(βshare trend

xi t + βshare constantxi

)+βcost trend

xo t + βcost constantxo

The p’s are prices and the β’s are the parameters to beestimated

Notable featuresAllows for both Hicks-neutral and biased technologicalchangeLarge number of parameters dealt with by nesting

Barbé A New Model of Energy Taxation 44 / 29

Nesting

Nesting functions means putting cost functions inside other costfunctions in order to group the most similar products together

Nesting increases the number of equations but reduces thenumber of parameters in each equation

I follow the nesting structure of Jorgenson and Yun and have 9nests

The model has 23 sets (22 industries and 1 household) ofregressions for each nest

Barbé A New Model of Energy Taxation 45 / 29

CES Nesting

Oi

MiEi

Li

Ki

Barbé A New Model of Energy Taxation 46 / 29

Cost functions nesting in my model

Final domestic output of industry x

Mx

MOx

MOTx

484442

5323

MSx

MSSx

815452

565551

MPx

72716261

MMx

N312111

Ex

48632422211

LxKx

Barbé A New Model of Energy Taxation 47 / 29

Cost functions nesting in my model

Final domestic output of industry x

Mx

MOx

MOTx

484442

5323

MSx

MSSx

815452

565551

MPx

72716261

MMx

N312111

Ex

48632422211

LxKx

Barbé A New Model of Energy Taxation 47 / 29

Cost functions nesting in my model

Final domestic output of industry x

Mx

MOx

MOTx

484442

5323

MSx

MSSx

815452

565551

MPx

72716261

MMx

N312111

Ex

48632422211

LxKx

Barbé A New Model of Energy Taxation 47 / 29

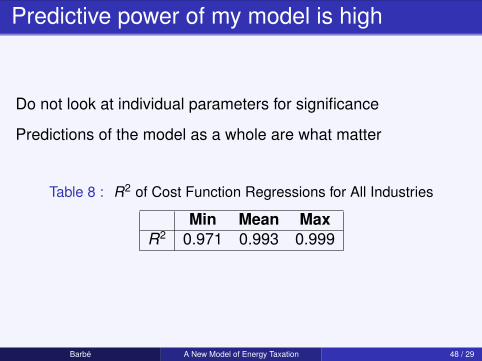

Predictive power of my model is high

Do not look at individual parameters for significance

Predictions of the model as a whole are what matter

Table 8 : R2 of Cost Function Regressions for All Industries

Min Mean MaxR2 0.971 0.993 0.999

Barbé A New Model of Energy Taxation 48 / 29

Remove tax preferences in abase-broadening reform

Compare long-run equilibrium of US economy under current lawand budget proposal

Tax reformIncrease tax rates on fossil fuel producing sectors as givenin budget proposalSimultaneously lower overall capital tax rate on all sectorsRevenue neutral

Results express the effects of the budget proposal

Externalities are included by calculating the social cost ofcarbon for which the proposal has no net effect on welfare

Barbé A New Model of Energy Taxation 49 / 29

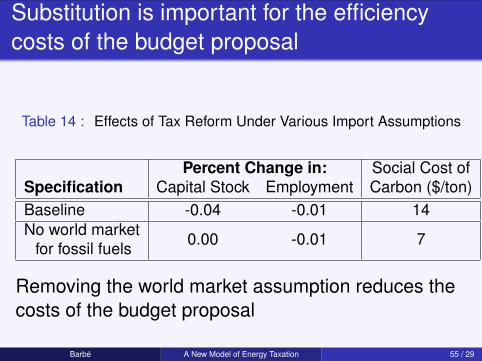

Including the energy resource matters butexactly how does not

Table 9 : The Effects of Budget Proposal Under Various ResourceSupply Assumptions

Percent Change in: Social Cost ofSpecification Capital Stock Employment Carbon ($/ton)Baseline -0.04 -0.01 14Elastic resource -0.05 -0.01 15Inelastic resource -0.04 -0.01 13No energy resource -0.09 -0.02 21

Including an energy resource changes results but exactly how itis modeled matters little

Barbé A New Model of Energy Taxation 50 / 29

Including the energy resource matters butexactly how does not

Table 9 : The Effects of Budget Proposal Under Various ResourceSupply Assumptions

Percent Change in: Social Cost ofSpecification Capital Stock Employment Carbon ($/ton)Baseline -0.04 -0.01 14Elastic resource -0.05 -0.01 15Inelastic resource -0.04 -0.01 13No energy resource -0.09 -0.02 21

Including an energy resource changes results but exactly how itis modeled matters little

Barbé A New Model of Energy Taxation 50 / 29

Including the energy resource matters butexactly how does not

Table 9 : The Effects of Budget Proposal Under Various ResourceSupply Assumptions

Percent Change in: Social Cost ofSpecification Capital Stock Employment Carbon ($/ton)Baseline -0.04 -0.01 14Elastic resource -0.05 -0.01 15Inelastic resource -0.04 -0.01 13No energy resource -0.09 -0.02 21

Including an energy resource changes results but exactly how itis modeled matters little

Barbé A New Model of Energy Taxation 50 / 29

Instruments are weak

Weak instruments can harm inference

Test instruments by testing for for underidentification (Anderson,1951) and weak instruments (Stock and Yogo, 2002)

Table 11 : Effects of Budget Proposal under Different InstrumentalVariables

Percent Change in: Social Cost ofSpecification Capital Stock Employment Carbon ($/ton)Baseline -0.04 -0.01 142 period lags for IV -0.03 -0.01 19No instruments -0.05 -0.01 13

Barbé A New Model of Energy Taxation 52 / 29

Results are not sensitive to cost functionvalues

Table 12 : Effects of Reform in Monte Carlo Simulations