25

1 Analyzing the Internet of Things Investment Landscape A data-driven look at financing trends, investors, acquirers and hot markets within the IoT ecosystem

1

Analyzing the Internet of Things Investment Landscape A data-driven look at financing trends, investors, acquirers and hot markets within the IoT ecosystem

2

Table of Contents Research Brief Page

Flying High – VC Funding to Drones Tops $100 Million in 2014

3

The 10 Largest Wearable Tech Funding Deals of 2014

5

The Most Active Internet of Things Investors of 2014

6

The Periodic Table of IoT 7

Wearables Are Hot: More than $1.4B Invested Since 2009

11

Connected Car Space Sees Investment Deals Climb 4x Since 2009

17

How Much Venture Capital are Kickstarter and Indiegogo

Hardware Projects Raising?

19

3

February 14, 2015

Flying High – VC Funding to Drones Tops $100 Million in 2014 Funding to drone startups increased 104% as venture firms including

Lightspeed Venture Partners, GGV Capital and Kleiner Perkins

among others jumped into the space with sizable bets.

According to CB Insights data, investment in 2014 to the nascent drone

industry topped $108M across 29 deals. Year-over-year funding increased 104% as venture firms including Lightspeed Venture Partners, GGV Capital

and Kleiner Perkins Caufield & Byers among others jumped into the drone

space with sizable bets.

(Note: The charts below are screenshots directly taken from CB Insights

Industry Analytics. No Excel required.)

Follow-on investments bulk up for drone startups

Between 2010 and 2012, there were fewer than five VC deals to drone companies. But as hype and interest catalyzed for the space (Amazon

famously revealed plans for drone delivery in December 2013), investment

has grown. There are now at least 10 drone companies with Series A

funding or later including Ehang, Skycatch and Kespry. A handful of companies have raised Series B financing including 3D Robotics and Airware.

4

The chart below highlights deal activity in the drone space by stage over the

last five years. To date, venture investment has not touched the late-stage (Series D+) in the drone space yet which is primarily a function of the

industry’s relative immaturity.

The most well-funded drone companies

Of the current crop of drone startups, Airware is the most well-funded having raised $40M from firms including First Round Capital, Andreessen

Horowitz and Felicis Ventures in addition to a strategic investment from GE Ventures. 3D Robotics is a close second, having raised $35M from investors

including True Ventures, O’Reilly AlphaTech Ventures and Mayfield Fund. A

compilation of the top 5 most well-funded private drone startups is below:

Update: Bilal Zuberi at Lux Capital published this nice Investor’s Perspective on the Proposed Drone Regulations over the weekend, after the FAA

published its regulatory framework.

5

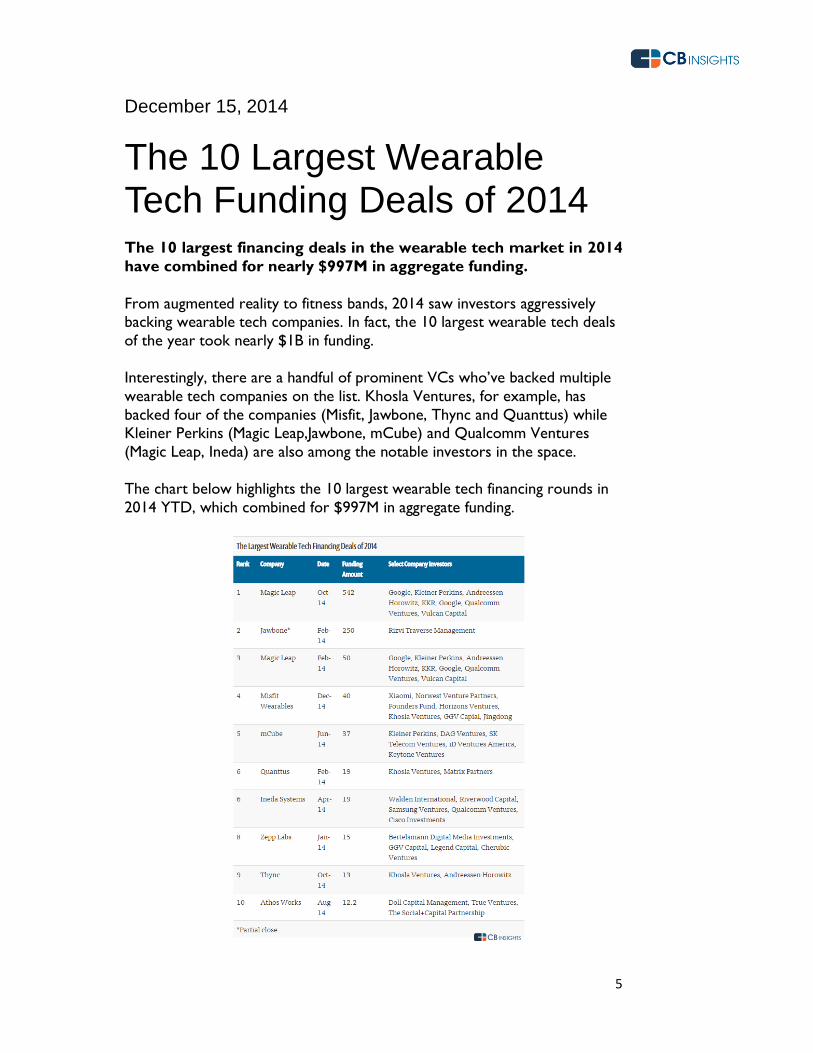

December 15, 2014

The 10 Largest Wearable Tech Funding Deals of 2014 The 10 largest financing deals in the wearable tech market in 2014

have combined for nearly $997M in aggregate funding.

From augmented reality to fitness bands, 2014 saw investors aggressively backing wearable tech companies. In fact, the 10 largest wearable tech deals

of the year took nearly $1B in funding.

Interestingly, there are a handful of prominent VCs who’ve backed multiple

wearable tech companies on the list. Khosla Ventures, for example, has

backed four of the companies (Misfit, Jawbone, Thync and Quanttus) while Kleiner Perkins (Magic Leap,Jawbone, mCube) and Qualcomm Ventures

(Magic Leap, Ineda) are also among the notable investors in the space.

The chart below highlights the 10 largest wearable tech financing rounds in

2014 YTD, which combined for $997M in aggregate funding.

6

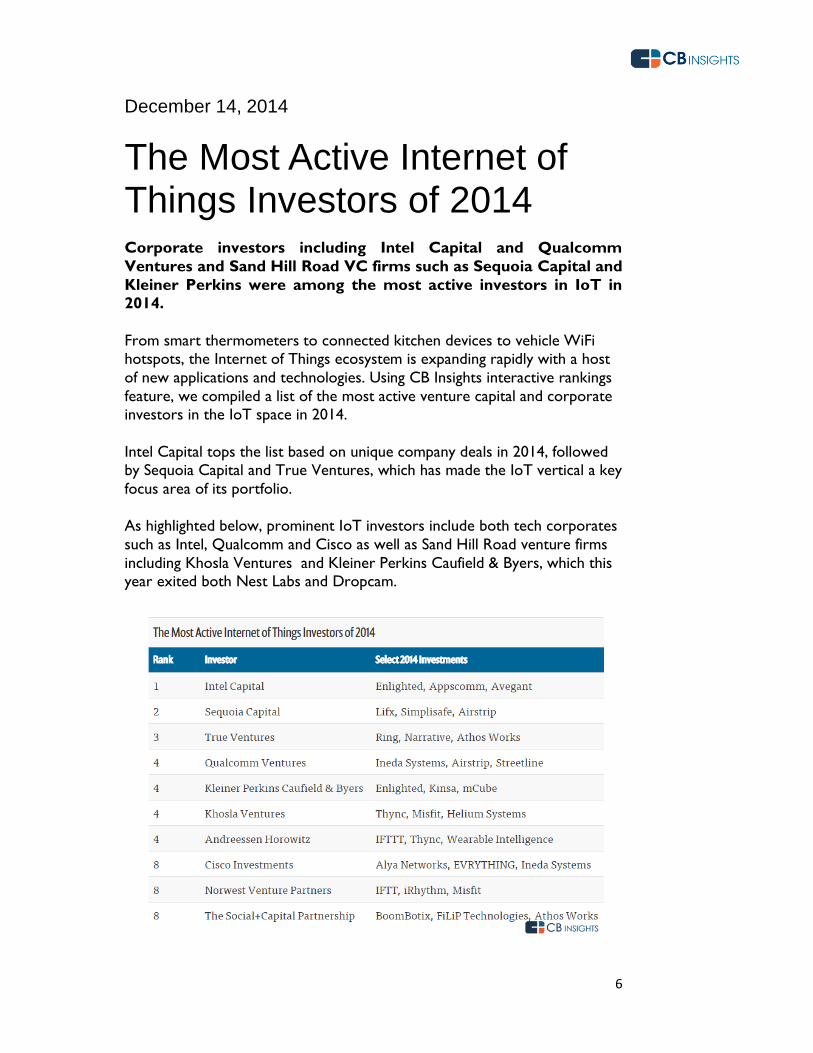

December 14, 2014

The Most Active Internet of Things Investors of 2014 Corporate investors including Intel Capital and Qualcomm

Ventures and Sand Hill Road VC firms such as Sequoia Capital and

Kleiner Perkins were among the most active investors in IoT in 2014.

From smart thermometers to connected kitchen devices to vehicle WiFi

hotspots, the Internet of Things ecosystem is expanding rapidly with a host

of new applications and technologies. Using CB Insights interactive rankings

feature, we compiled a list of the most active venture capital and corporate investors in the IoT space in 2014.

Intel Capital tops the list based on unique company deals in 2014, followed by Sequoia Capital and True Ventures, which has made the IoT vertical a key

focus area of its portfolio.

As highlighted below, prominent IoT investors include both tech corporates

such as Intel, Qualcomm and Cisco as well as Sand Hill Road venture firms

including Khosla Ventures and Kleiner Perkins Caufield & Byers, which this year exited both Nest Labs and Dropcam.

7

October 24, 2014

The Periodic Table of IoT The 141 companies, VCs, corporate investors, angels, accelerators,

and acquirers engaged in the Internet of Things space that you

should know.

The promise of connecting devices across homes, retail stores, automobiles,

and physical machinery, otherwise referred to as the Internet of Things, has emerged into what is now a substantial ecosystem of private companies,

corporations, venture investors and acquirers.

So after putting out The Periodic Table of Tech and The Periodic Table of Healthcare, today we’re excited to introduce the Periodic Table of IoT

(Internet of Things) – a guide to help make sense of the key players in the growing Internet of Things universe. The 141 companies, investors and

acquirers on the list were drawn from analysis using CB Insights data around financial health, company momentum, investor quality and M&A activity.

We expect that this list of 141 will change over time as new entrants emerge and gain prominence and others falter, exit and/or get removed. If

you believe someone should be added, please leave a comment with your rationale.

8

Navigating the Periodic Table of IoT

The table focuses on seven different types of organizations as follows (from left to right).

The left side of the Periodic Table of IoT includes companies across

several sub-verticals that comprise IoT. More details on these sub-areas of IoT are below.

On the far right, the table shifts to venture capital firms (both multi-stage and micro VCs), corporate investors, angels,

accelerators/incubators and crowdfunding platforms selected based primarily on total portfolio investments into IoT and recency of

investment in the Internet of Things.

The bottom section below is acquirers and notable IoT exits.

Because the Internet of Things is more of a theme than a single industry, it spans a wide variety of areas and companies who are attacking very different

problems. As a result, we broke the IoT companies down into several sub-areas as you’ll see on the Periodic Table.

Wearable Tech

Private wearable tech firms on the list include clothing or accessory companies that fuse sensor and other connected technologies in order to

help track primarily health-related matters such calories burned, heart rate, steps taken, sleep and hearing but also more general use cases such as

photos, email and GPS location.

Connected Home

Private connected home companies on the list offer connected software

platforms and hardware for your home in functional areas ranging from security, temperature management and lighting.

Building Blocks & Platforms

Companies that help power, facilitate and/or create the IoT universe. This

ranges from open-source IoT toolkits to embedded chip makers to DIY

electronics.

Industrial Internet

A term credited to GE, this includes a subset of companies working to

extend the capabilities of connected devices to physical machinery, industrial

processes and workplaces. Many of the firms listed primarily operate in the drone and/or robotics spaces.

9

Healthcare

Healthcare companies on the table span key remote patient monitoring or machine-to-machine products for the healthcare industry, specifically for use

by physicians or home healthcare providers.

In-store Retail

Companies using sensor, beacon and WiFi technologies within the physical retail store in order to help better track and understand in-store customers.

Connected Car

Connected car companies on the table provide wireless technology and/or hardware to help drivers be alerted of details including traffic, accidents,

alerts and speeding.

Venture Capital Firms

Venture capital firms included make venture equity investments across the

stage spectrum and geographies focusing on IoT opportunities. The VC firm

category spans both micro VCs and large multi-stage firms with LP

commitments ranging from $25M to well over $1B+.

Corporate Investors

Corporate investors in the Internet of Things include both corporations making direct investments and separately identifiable corporate venture

units such as Intel Capital and Qualcomm Ventures.

Angel Investors

IoT angel investors span both angel groups that bridge the gap between

angel investment and institutional VC, providing either a managed fund or direct investment from angel group members as well as individual angel

investors who offer early-stage capital, advice and networks to startups in

exchange for equity or convertible debt.

Crowdfunding

Internet platforms for financing ventures or projects through contributions from the ‘crowd’, a larger group of people whose collective contributions

help fund the project. See our prior report on Kickstarter-funded hardware projects.

10

Accelerators/Incubators

Accelerators and startup incubators typically offer some combination of equity investment, mentorship and resources around company development.

Those on the Internet of Things periodic table have either funded a number of IoT portfolio companies or have a specific focus on hardware i.e. R/GA

TechStars and Lemnos Labs.

IoT Acquirers

Key public corporations that have acquired private IoT companies in the last

two years.

Notable acquisitions

Key IoT companies that have been acquired already ranging from smart home companies (Nest, Dropcam, SmartThings) to wearable computing

firms (Basis) to M2M application platforms (ThingWorx).

11

September 6, 2014

Wearables Are Hot: More than $1.4B Invested Since 2009 Deals in the space increased by 135% in 2013 and funding has already

hit an annual record in 2014 (in only 8 months). Will Apple's moves

in the space and some already big exits spur more investment into

the space?

With rumors swirling that Apple will be making a big wearables-related announcement (the “iWatch”) at its upcoming September 9th event, we

used CB Insights data to see just how hot the wearables market is. Over

the last 5 years, the wearables space has seen more than $1.4B of investment into emerging, private wearable startups. With the tailwind

Apple’s wearables entry & announcement might offer and the already

notable exits this year of wearables companies ($3.1B IPO from GoPro and

$2B acquisition of Oculus VR by Facebook), it is conceivable that 2014 might be the first year to see more than $1 billion of investment flowing into

wearables.

This wearables research brief will cover:

Wearable financing trends

Wearable investment trends by stage

Wearables most active investors

The most well-funded wearables companies and notable exits

First, how do we define wearables? The different sub-categories within wearable computing as well as some of the companies within each are

provided below:

Augmented Reality & Personal Display - Companies that, like Google

Glass, offer wearable hardware augmented by computer-generated features such as text messages or GPS data. This includes companies

such as Lumus Ltd. and Pebble Technology.

Body Monitoring (Health & Fitness) – Companies that offer tools for

knowing your own mind and body, which include Fitbit and Jawbone.

12

Brain Monitoring – Companies that deliver biosensors that can monitor and learn from the human brain, which can assist with

capacities such as stress reduction and mental performance.

Controlled Computing - Companies offering wearable devices that allow users to control their computers via the body and bypassing

conventional controls such as keyboards.

POV (Point of View) - Companies specializing in wearable cameras and audio recorders such as GoPro and nugg-it.

Financing Trends by Year

When we look at the 5-year trend of investor-backed wearable companies,

the upward trend is clear and rapid. Between 2012 and 2013 we saw a 135%

jump in deals, and funding has already reached an all time high of $502M in

investments so far, which is a 38% year over year increase from 2013 (and four months remain in 2014).

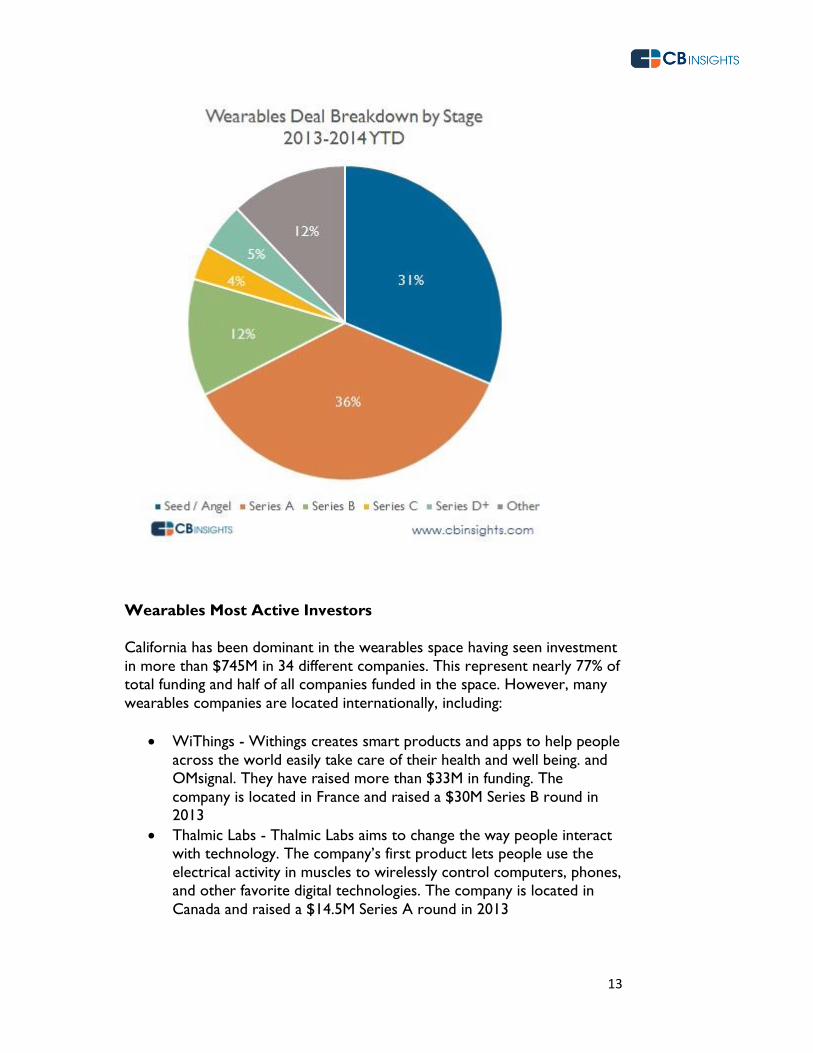

Financing Trends by Stage

Looking at a stage breakdown, the majority of deals in the past two years

have occurred in the early stages as more companies enter the market. This

is expected given wearables is essentially a new category. More than two-

thirds of all recent deals have occurred in the Seed/Angel and Series A

stages with a total of 56 deals in the last two years. Funding has been concentrated in Series A and B rounds, with $249M and $193M being

invested respectively in the past two years.

13

Wearables Most Active Investors

California has been dominant in the wearables space having seen investment

in more than $745M in 34 different companies. This represent nearly 77% of total funding and half of all companies funded in the space. However, many

wearables companies are located internationally, including:

WiThings - Withings creates smart products and apps to help people

across the world easily take care of their health and well being. and

OMsignal. They have raised more than $33M in funding. The

company is located in France and raised a $30M Series B round in 2013

Thalmic Labs - Thalmic Labs aims to change the way people interact with technology. The company’s first product lets people use the

electrical activity in muscles to wirelessly control computers, phones, and other favorite digital technologies. The company is located in

Canada and raised a $14.5M Series A round in 2013

14

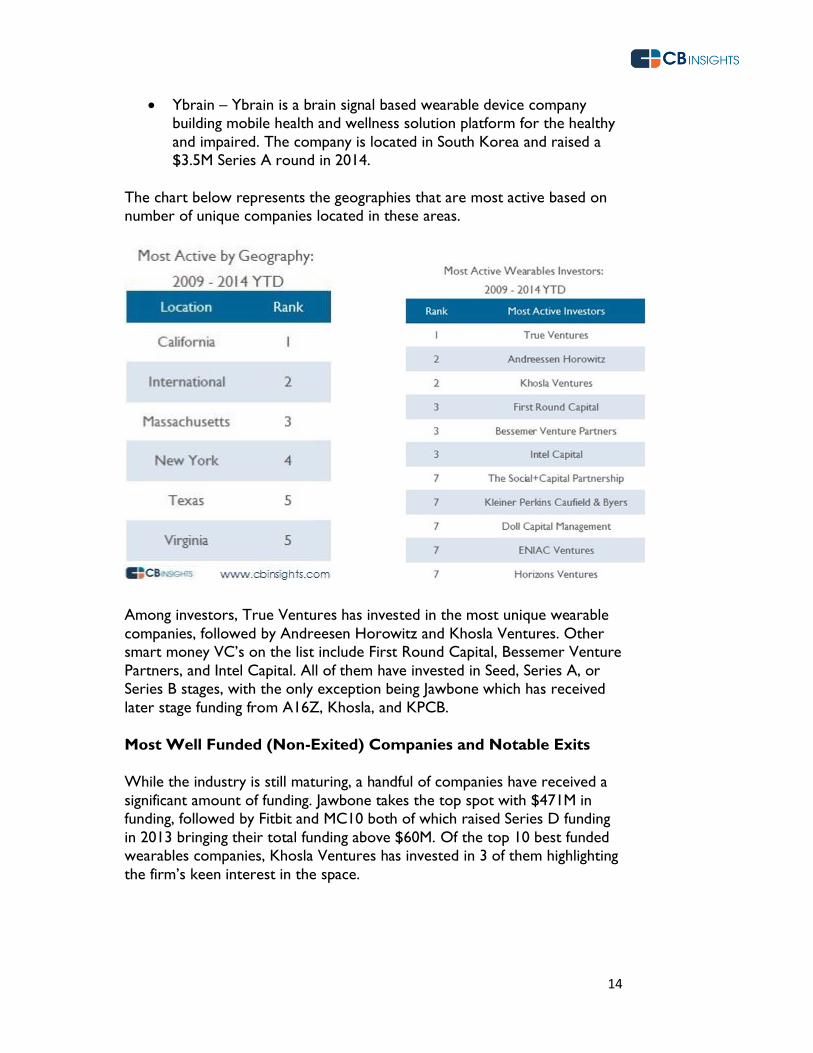

Ybrain – Ybrain is a brain signal based wearable device company building mobile health and wellness solution platform for the healthy

and impaired. The company is located in South Korea and raised a $3.5M Series A round in 2014.

The chart below represents the geographies that are most active based on

number of unique companies located in these areas.

Among investors, True Ventures has invested in the most unique wearable

companies, followed by Andreesen Horowitz and Khosla Ventures. Other smart money VC’s on the list include First Round Capital, Bessemer Venture

Partners, and Intel Capital. All of them have invested in Seed, Series A, or Series B stages, with the only exception being Jawbone which has received

later stage funding from A16Z, Khosla, and KPCB.

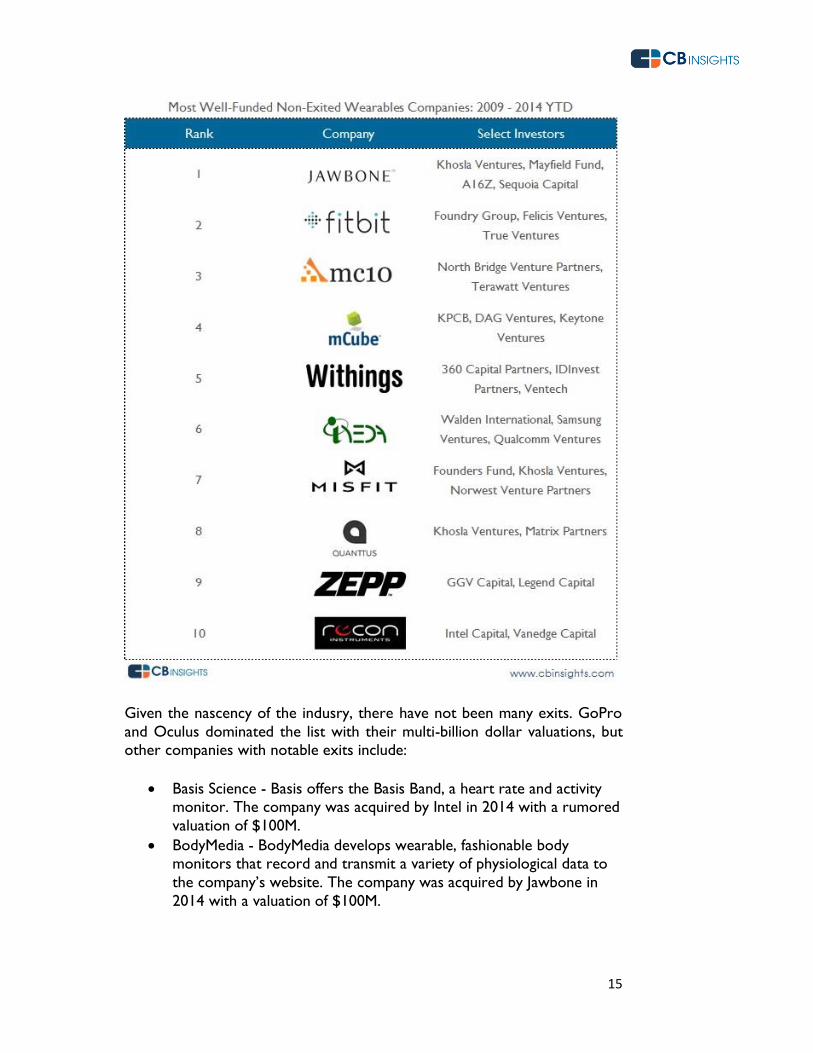

Most Well Funded (Non-Exited) Companies and Notable Exits

While the industry is still maturing, a handful of companies have received a

significant amount of funding. Jawbone takes the top spot with $471M in funding, followed by Fitbit and MC10 both of which raised Series D funding

in 2013 bringing their total funding above $60M. Of the top 10 best funded wearables companies, Khosla Ventures has invested in 3 of them highlighting

the firm’s keen interest in the space.

15

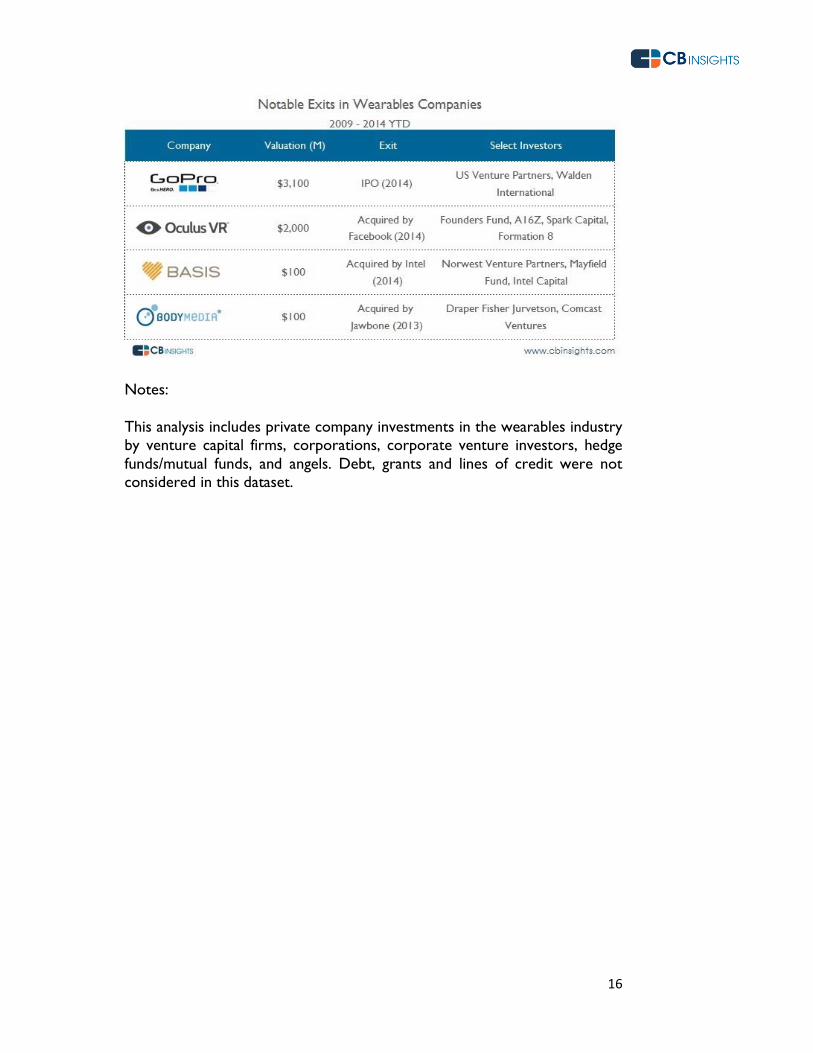

Given the nascency of the indusry, there have not been many exits. GoPro

and Oculus dominated the list with their multi-billion dollar valuations, but other companies with notable exits include:

Basis Science - Basis offers the Basis Band, a heart rate and activity monitor. The company was acquired by Intel in 2014 with a rumored

valuation of $100M.

BodyMedia - BodyMedia develops wearable, fashionable body monitors that record and transmit a variety of physiological data to

the company’s website. The company was acquired by Jawbone in

2014 with a valuation of $100M.

16

Notes:

This analysis includes private company investments in the wearables industry by venture capital firms, corporations, corporate venture investors, hedge

funds/mutual funds, and angels. Debt, grants and lines of credit were not considered in this dataset.

17

August 13, 2014

Connected Car Space Sees Investment Deals Climb 4x Since 2009 Investments to companies in and around the connected car space

are indeed gaining traction from both venture and corporate

investors.

Over the past couple years, both Nokia Growth Partners and Intel Capital

announced separate $100M Connected Car Funds. Is the promise of universally connected and intelligent vehicles closer to becoming a reality?

According to the data, investments to companies in and around the

connected car space are indeed gaining traction among both venture capital and corporate investors. Firms tracked in the connected car market within

the CB Insights database include a range of technologies, covering:

Automotive and fleet telematics – Companies providing software and

sensors to monitor the location, movements, behavior and habits of consumer and/or enterprise vehicles or fleets of vehicles. Examples include

Telogis and Airbiquity.

Smart parking solutions and apps – Companies helping drivers detect, track and facilitate the parking process including when vehicles occupy or

leave a parking space. Examples include Streetline and Parko.

Ease-of-use navigation – Companies offering in-car technologies to

navigate and track road travel and conditions. This includes Inrix and Loc&All.

Driver assistance/driverless technology - Companies proving

technologies for driver safety, accident avoidance as well as autonomous driving. Examples include Mobileye and Cruise Automation.

Not including a $400M round to now public Mobileye in 2013, startups in the connected car space have raised $625M across 90 deals since 2009. On

a year-over-year basis, deal activity to the connected car ecosystem grew

42% between 2013 and 2012 and over 4x on a five-year basis. Among the notable deals in 2014 so far are Zubie‘s $8M round led by Nokia Growth

Partners and Magna International and Inrix’s $10M Series E.

18

The chart below highlights the growth in deals to the connected car market

since 2009. The 2014 figure is a YTD number so we can expect more deals in the remainder of the year.

Corporates get busy in connected car space

When we visualize the universe of connected car companies using the CB

Insights’ Business Social Graph, it’s clear that the connected car space is one

corporate investors are keen on staying on top of. As the social graph below

shows, corporates ranging from BMW and Castrol to Intel and Qualcomm have been busy in the connected car space.

Among the corporate-backed firms in the space are CloudMade (Intel Capital), Streetline (Qualcomm Ventures, Citi Ventures), Dash Labs

(CyberAgent Ventures) and Glympse (Verizon Ventures).

19

August 11, 2014

How Much Venture Capital are Kickstarter and Indiegogo Hardware Projects Raising? A data-driven look at venture capital financing trends of crowd-

funded hardware projects on Kickstarter and Indiegogo.

When crowdfunding first emerged as a popular model to raise money from groups of individuals, many pundits felt that crowdfunding would create a

competitive threat to the venture capital model of financing startups.

Today, it’s apparent the crowdfunding phenomenon has indeed affected the

VC ecosystem – as a complementary force. With thousands of consumer-

oriented hardware campaigns looking for financing for everything from smart watches to beacon technologies, crowdfunding platforms such as

Indiegogo and Kickstarter have provided VC investors with a valuable source for dealflow.

This report – the first of its kind – analyzes CB Insights financing and crowdfunding data to identify trends among crowdfunded hardware

companies that began on Kickstarter or Indiegogo.

The Data

This report analyzes 443 hardware projects that have raised over $100K on

Kickstarter or Indiegogo. Using this data, we examined how many of these 443 companies have raised outside venture capital equity financing and other

associated trends.

A summary of the data & trends follows.

Summary Findings

$321 million – Total VC financing to-date to crowdfunded hardware projects

9.5% – The percentage of crowdfunded hardware campaigns that

have gone onto raise VC

2013 – The momentum has been building as might be expected and 2013 was a big year for funding. 2014, if the current run-rate

20

continues, we will see a new deal high for crowdfunded hardware

campaigns.

5x – The amount of investor-backed companies and outside funding to Kickstarter hardware campaigns vs. Indiegogo

Misfit, Formlabs and SmartThings – The top 3 most well-funded crowdfunded hardware startups (un-exited)

Unrelated – Surprisingly, there doesn’t appear to be a relationship between the amount a campaign raises on a crowdfunding platform and the amount it raises from VCs.

Funding to crowdfunded hardware companies booms in 2013

Venture funding to crowdfunded hardware startups went mainstream in

2013, reaching over $200M across 23 deals. The bulk of activity came in Q4

2013 when 10 startups including Scanadu, Formlabs and Misfit Wearables raised over $150M in aggregate funding. The largest round of 2013 went to

virtual reality company Oculus VR, which raised a $75M Series B in December from investors including Andreessen Horowitz, Formation 8,

Spark Capital and Matrix Partners. Only a couple months later in March

2014, Facebook announced the acquisition of Oculus for $2 billion marking the largest windfall to-date for a crowdfunded project.

In 2014, investor deal activity to crowdfunded hardware companies is on pace to break 2013’s record with 19 deals already in the first seven months

of the year. If the current run-rate continues through the end of the year, 2014 will see over 30 deals.

Among the largest 2014 VC deals to crowdfunded hardware projects are

smart bulb startup Lifx, which raised a $12M Series A led by Sequoia Capital after previously raising $1.3M on Kickstarter and a $10M Series A led by

Khosla Ventures to home security product Canary. Canary previously raised just under $2M in one of the most successful hardware campaigns on

Indiegogo to date.

21

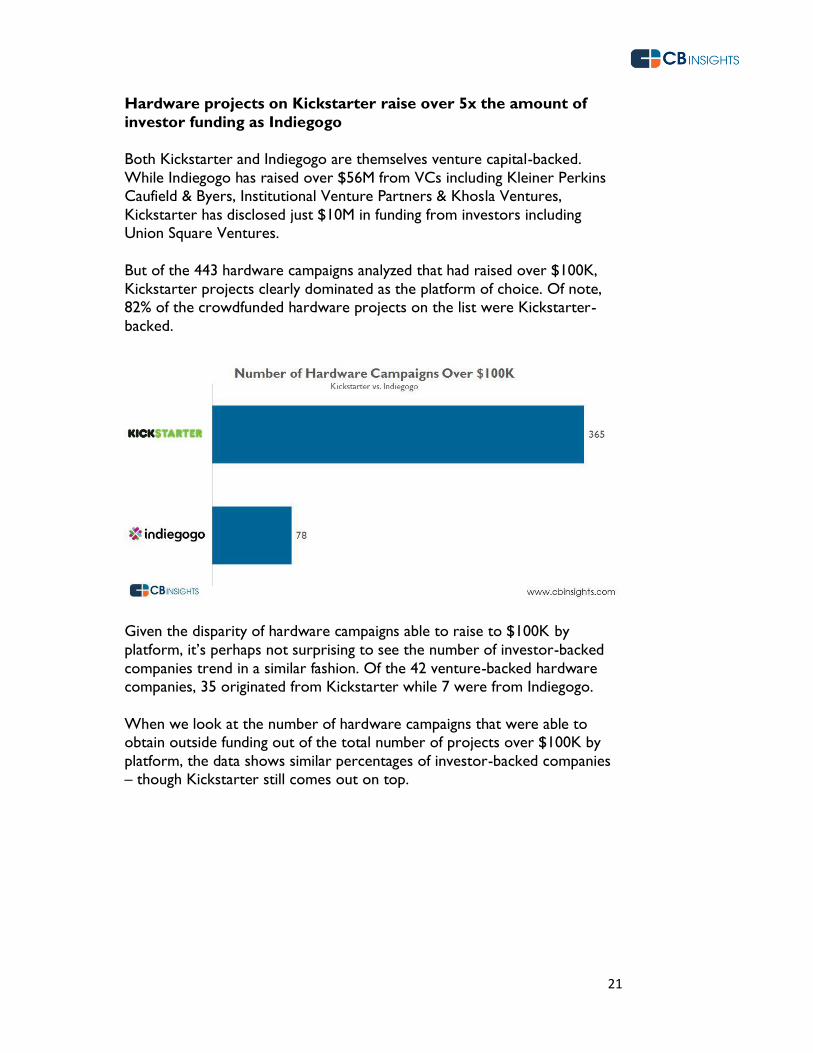

Hardware projects on Kickstarter raise over 5x the amount of

investor funding as Indiegogo

Both Kickstarter and Indiegogo are themselves venture capital-backed.

While Indiegogo has raised over $56M from VCs including Kleiner Perkins Caufield & Byers, Institutional Venture Partners & Khosla Ventures,

Kickstarter has disclosed just $10M in funding from investors including Union Square Ventures.

But of the 443 hardware campaigns analyzed that had raised over $100K,

Kickstarter projects clearly dominated as the platform of choice. Of note, 82% of the crowdfunded hardware projects on the list were Kickstarter-

backed.

Given the disparity of hardware campaigns able to raise to $100K by

platform, it’s perhaps not surprising to see the number of investor-backed

companies trend in a similar fashion. Of the 42 venture-backed hardware companies, 35 originated from Kickstarter while 7 were from Indiegogo.

When we look at the number of hardware campaigns that were able to obtain outside funding out of the total number of projects over $100K by

platform, the data shows similar percentages of investor-backed companies

– though Kickstarter still comes out on top.

22

The chart below highlights overall funding raised by hardware companies on

the respective platforms. Of note, Kickstarter-backed hardware projects have raised over $268M to date, besting the $52M invested in Indiegogo projects

by 416%. On average, both Kickstarter and Indiegogo-backed companies with VC funding have both raised nearly $9M.

23

The most well-funded crowdfunded hardware startups

The disparity in outside funding to Kickstarter vs. Indiegogo hardware

campaigns is largely due to a small number of companies that have raised sizable financing rounds to date. In fact, of the top 10 hardware startups that

have raised the highest amount of outside capital – 7 were Kickstarter projects (Misfit, Scanadu and Canary were Indiegogo projects). Given it has

already exited, Oculus VR, which raised $91M prior to its acquisition, was not included on the list.

24

California dominates among crowdfunded hardware startups that

raise VC funding

Just under 79% of the investor-backed crowdfunded hardware startups are based in the U.S. Among the U.S.-based companies, 52% are headquartered

in California including Romotive, Pebble and LUMO BodyTech to name a few.

Massachusetts and New York each saw three companies. Internationally,

crowdfunded startups that have raised outside capital span a diverse range of

markets including Australia (Ninja Blocks), Singapore (Pirate 3DP) and Sweden (Narrative).

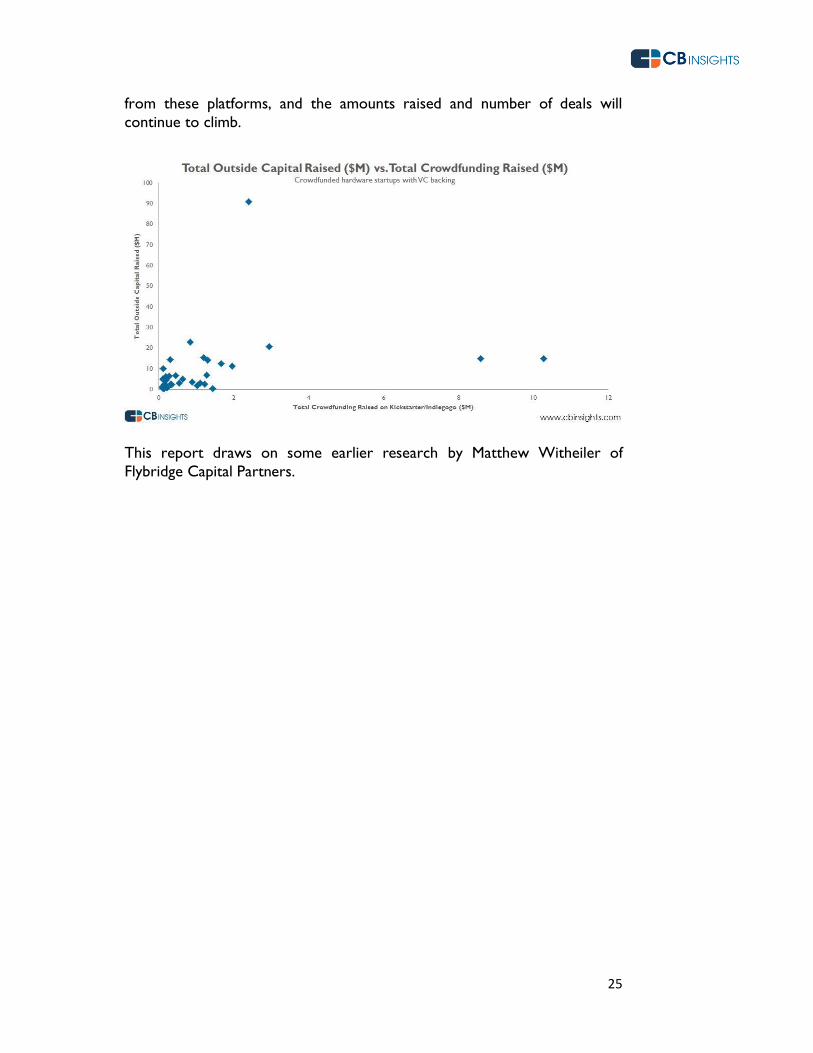

Do projects that raise more during their campaigns also raise more

outside capital?

Lastly, we took a look at whether the hardware companies that were able to

raise more funding via their Indiegogo or Kickstarter campaigns went on to

raise larger sums of equity capital from venture capital investors.

And based on the data, there is no clear trend. While Oculus went on to raise

$91M from VC investors after a $2.4M Kickstarter campaign, there have been

others like smartwatch startup Pebble and video game console Ouya that

raised over $8M from crowdfunding but have raised at or around the same amount of venture capital as some hardware firms that raised less than $2M

during their campaigns.

Of course, given the nascency of the market, many of the hardware startups that fall into the lower left corner of the below chart may still go on to raise

additional funding sums in the future. As crowdfunding only proliferates, we

can expect that venture capital investors will expand their sourcing of deals

25

from these platforms, and the amounts raised and number of deals will

continue to climb.

This report draws on some earlier research by Matthew Witheiler of

Flybridge Capital Partners.