36

A Discussion of the Affordable Care Act

| Date post: | 02-Jan-2016 |

| Category: |

Documents |

| Upload: | corey-arnold |

| View: | 213 times |

| Download: | 0 times |

A Discussion of the Affordable Care Act

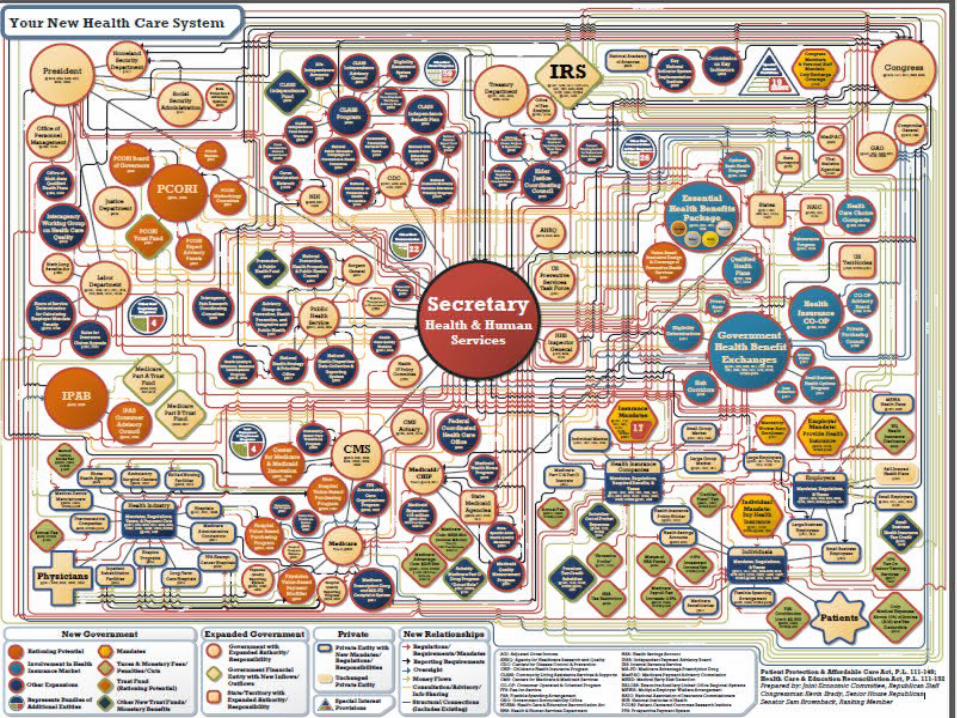

Overview of the Affordable Care Act

►Effective March 23, 2010►Purpose was to decrease the number of uninsured Americans and to

reduce the overall costs of health care. Its provisions are intended to: Expand access to insurance Increase consumer protections, and Improve outcomes

►First insurance reforms became effective 6 months after passage (September 23, 2010).

►Most significant insurance reforms became effective January 1, 2014

Insurance Coverage Reforms

Scope of Health Insurance Reforms

► The ACA reforms apply to health insurance issuers offering group or individual health insurance coverage.

► "Health insurance issuer► "Health insurance coverage"

► The ACA categorizes "health insurance coverage" into three markets: ► the individual market► the small group market ► the large group market.

► Exceptions to ACA► Excepted Benefits

Guaranteed Availability and Renewability

►Guaranteed Availability► Requires issuers offering non-grandfathered health insurance coverage to accept every individual

or employer who applies for coverage in the individual or small group market (Subject to certain exceptions such as limits on network capacity)

May restrict enrollment to open or special enrollment periods

►Guaranteed Renewability Requires any health insurance issuer offering coverage in the individual or group market to renew

coverage at the option of the plan sponsor or individual. Exceptions:

nonpayment of premium, fraud, violation of participation/contribution rules, movement outside the service area, membership in association ceases, discontinuing a particular product, or exiting the market

Uniform modification of coverage is permitted

Insurance Coverage Reforms

► Coverage of adult children to age 26► Internal and External appeal procedures► Prohibition on lifetime and annual limits on essential health benefits► Limits on ability to rescind coverage► Prohibition on preexisting conditions exclusions► Coverage for Clinical trials► Access to Providers:

Direct access to OB/GYN Permit pediatrician to be selected as a PCP

► No prior authorization or increased cost sharing for out of network emergency services► Coverage for Preventive Services without cost sharing► Limits on Cost Sharing► Actuarial Level of Coverage – Bronze, Silver, Gold or Platinum► Coverage for Essential Health Benefits

Essential Health Benefits

►Ambulatory Patient Services►Emergency Services►Hospitalization►Maternity and Newborn Care►Mental Health and Substance Use ►Prescription Drugs►Rehabilitation and Habilitative services►Laboratory Services►Preventive Service►Pediatric Services (dental and vision)

1

2

3

4

5

6

7

8

9

10

Grandfathered and Transitional Plans

► Many of the mandates of the ACA do not apply to grandfathered or transitional plans. ► Grandfathered Plans

► Group or individual health insurance coverage that was in place prior to March 23, 2010, and continues to maintain its grandfathered status

► A plan may lose grandfathered status ► Transitional Plans

► Non-grandfathered group or individual plans that were in existence on October 1, 2013 and may be renewed through October 1, 2016

► Notice must be provided to the affected individuals► Annual increases in premium rates are permissible

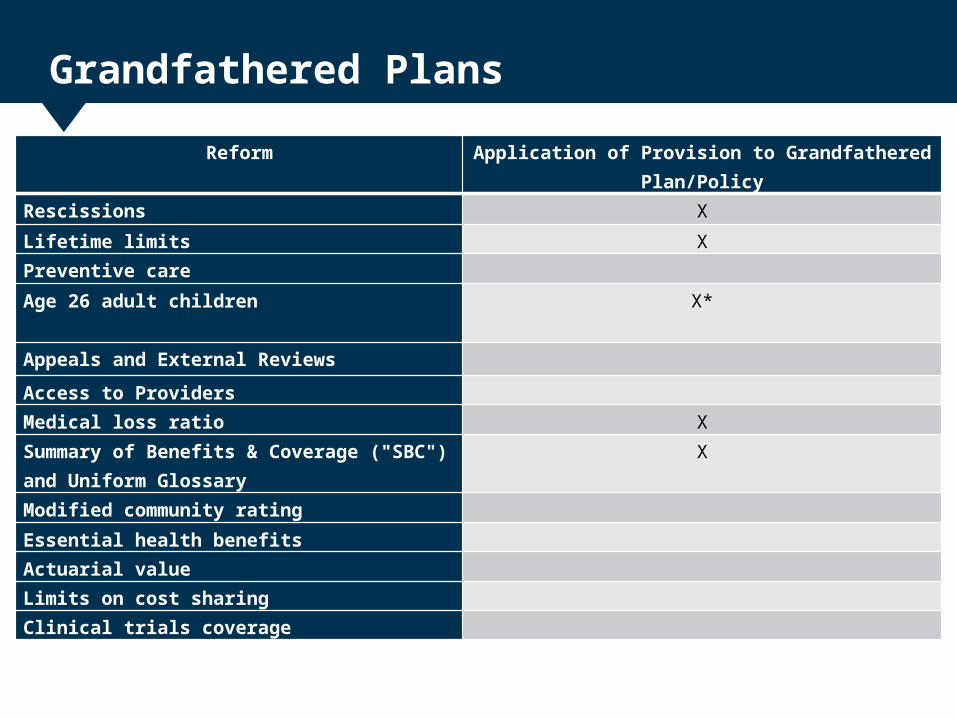

Grandfathered Plans

Reform Application of Provision to Grandfathered Plan/Policy

Rescissions X

Lifetime limits XPreventive care

Age 26 adult children

X*

Appeals and External Reviews

Access to Providers

Medical loss ratio X

Summary of Benefits & Coverage ("SBC") and Uniform Glossary

X

Modified community rating

Essential health benefits

Actuarial value

Limits on cost sharing

Clinical trials coverage

Mandates to Purchase

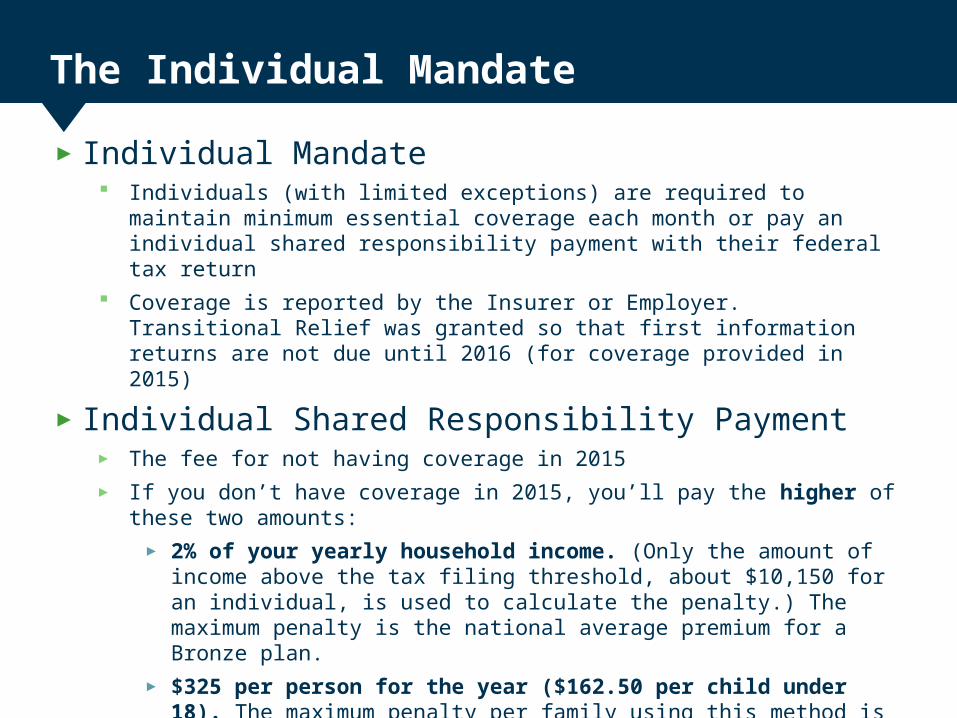

The Individual Mandate

► Individual Mandate Individuals (with limited exceptions) are required to maintain minimum essential coverage each

month or pay an individual shared responsibility payment with their federal tax return Coverage is reported by the Insurer or Employer. Transitional Relief was granted so that first

information returns are not due until 2016 (for coverage provided in 2015)

► Individual Shared Responsibility Payment► The fee for not having coverage in 2015► If you don’t have coverage in 2015, you’ll pay the higher of these two amounts:

► 2% of your yearly household income. (Only the amount of income above the tax filing threshold, about $10,150 for an individual, is used to calculate the penalty.) The maximum penalty is the national average premium for a Bronze plan.

► $325 per person for the year ($162.50 per child under 18). The maximum penalty per family using this method is $975.

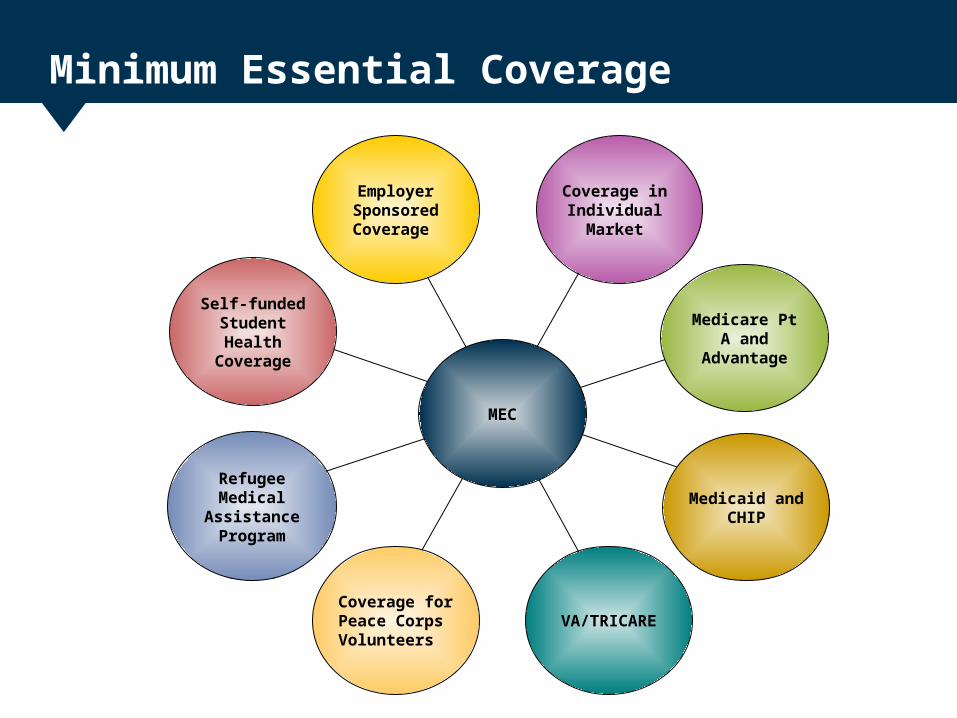

Minimum Essential Coverage

EmployerSponsoredCoverage

Coverage in Individual

Market

Coverage for Peace Corps Volunteers

VA/TRICARE

Medicaid and CHIP

Medicare Pt A and

Advantage

Self-funded Student Health

Coverage

Refugee Medical

Assistance Program

MEC

The Employer Mandate

►Employer Mandate The ACA does not specifically require employers (large or small) to

provide coverage to employees. The ACA does require a large employer to pay a shared responsibility

fee if one or more of its full-time employee(s) enroll in subsidized coverage in an Exchange

Employer Shared Responsibility Payment Applies to large employers that do not offer coverage or offer coverage

to fewer than 95% of its full-time employees (and their dependents) Payment is the number of full-time employees the employer employed

for the year (minus up to 30) multiplied by $2,000, as long as at least one full-time employee receives the premium tax credit.

Indiana Federally Facilitated Marketplace

► Indiana has a Federally Facilitated Marketplace (“FFM”)► Indiana is an Effective Rate Review State

► The IDOI maintains jurisdiction over all QHPs and non-QHPs sold in Indiana in the following areas:

► Licensing► Rate and form review► Financial solvency ► EHB benchmark review

►A QHP issuer must offer at least one QHP at the silver level and at least one QHP at the gold level

Affordability Programs

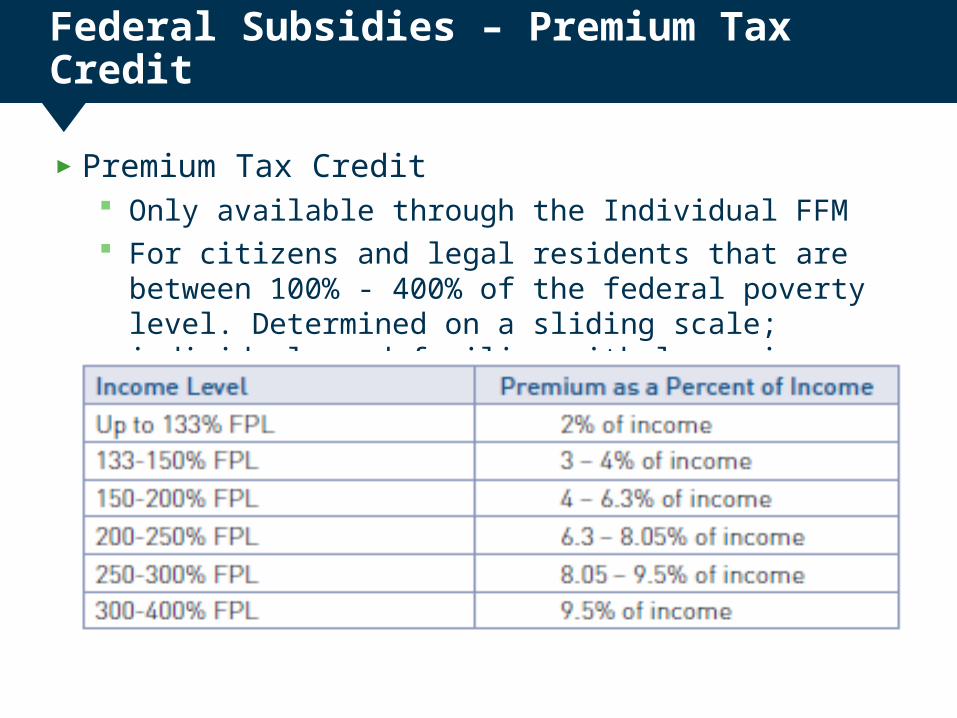

Federal Subsidies – Premium Tax Credit

►Premium Tax Credit Only available through the Individual FFM For citizens and legal residents that are between 100% - 400% of the

federal poverty level. Determined on a sliding scale; individuals and families with lower incomes receive more assistance.

Federal Subsidies – Cost Sharing

►Cost Sharing Subsidy Only available if purchased an individual silver plan through the FFM and

are below 250% of FPL* Subsidy will reduce all of the person’s cost-sharing, including

deductibles, coinsurance, copayments and out of pocket maximums Amount of subsidy is based upon the person’s income.

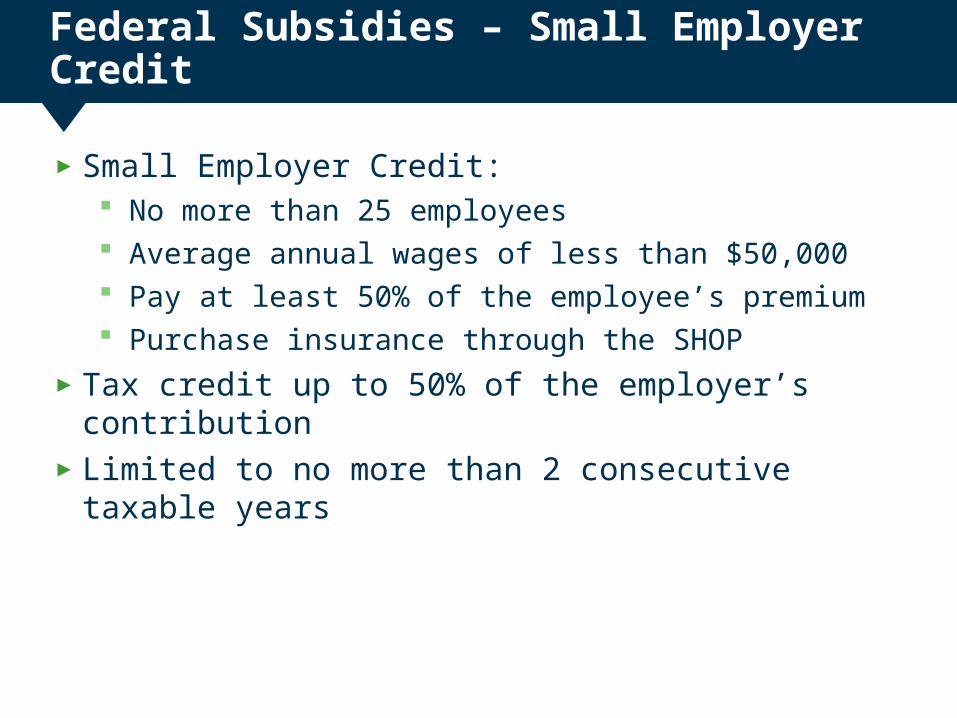

Federal Subsidies – Small Employer Credit

►Small Employer Credit: No more than 25 employees Average annual wages of less than $50,000 Pay at least 50% of the employee’s premium Purchase insurance through the SHOP

►Tax credit up to 50% of the employer’s contribution►Limited to no more than 2 consecutive taxable years

Premium Stabilization Programs

Risk Adjustment, Reinsurance and Risk Corridors

► Risk Adjustment Program Permanent program intended to normalize the individual risks of health insurance issuers

to ensure premiums remain stable Payments transfer from issuers with low risk persons to issuers with high risk persons. All non-grandfathered plans in the individual and small group markets are subject to the

risk adjustment program Indiana carriers received approximately $122 million for 2014

► Transitional Reinsurance Program 3 year program ending in 2017 Intended to stabilize premium for coverage in the individual market due to higher cost

individuals gaining insurance during the first 3 years of guaranteed availability of coverage

► Transitional Risk Corridor Program 3 year program ending in 2017 that provides additional protection for health insurance

issuers on the FFM.

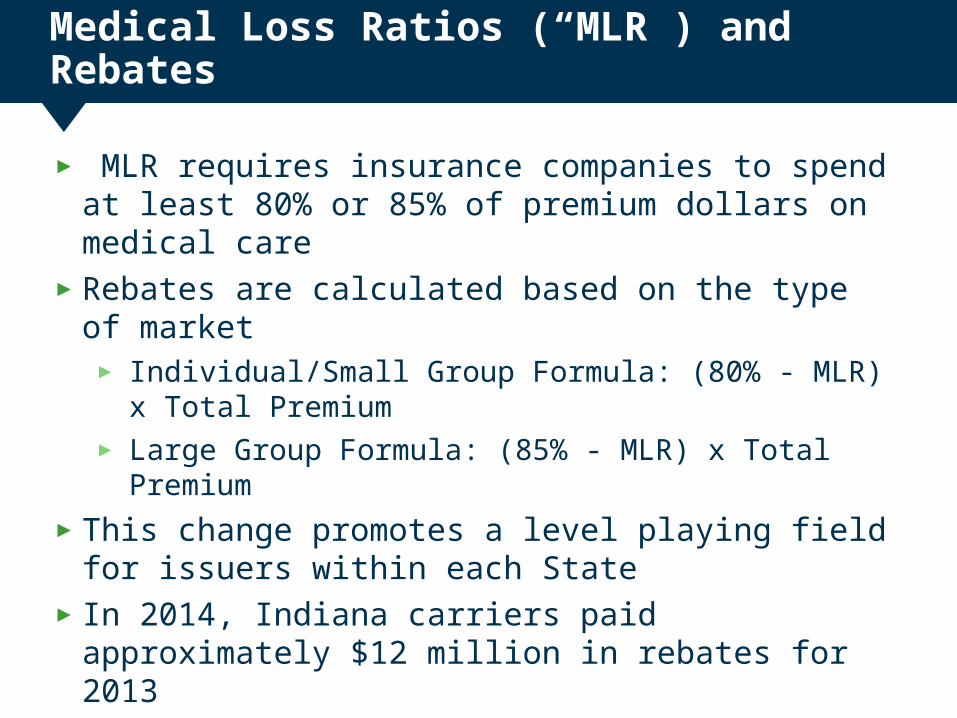

Medical Loss Ratios (“MLR”) and Rebates

► MLR requires insurance companies to spend at least 80% or 85% of premium dollars on medical care

►Rebates are calculated based on the type of market► Individual/Small Group Formula: (80% - MLR) x Total Premium► Large Group Formula: (85% - MLR) x Total Premium

►This change promotes a level playing field for issuers within each State

► In 2014, Indiana carriers paid approximately $12 million in rebates for 2013

►The rebate amounts for 2014 will be available September 30, 2015

Taxes/Fees on Health Insurance Issuers and Group Health Plans

Tax/Fee Paid By Purpose

Health Insurer Provider Fee Health insurance issuers and certain self-insured plansNon-profit issuers that receive more than 80% of their net premium from government programs are exempt – approximately $8 billion for 2014 and $11 billion for 2015

To help cover the premium subsidies

Marketplace User Fees Health insurance issuers offering coverage on the Marketplace – currently 3.5% of premium

To cover administrative costs of the Exchange

Transitional Reinsurance Fee Health insurance issuers and self-insured plans - $63 for 2014 and $44 for 2015 and $27 for 2016

To fund the Transitional Reinsurance Program

Risk Adjustment User Fee Health insurance issuers that participate in the individual or small group market – approximately $0.15 per member per month

To fund the Risk Adjustment Program

Patient-Centered Outcomes Research Institute (“PCORI”) Fee

Health insurance issuers and self-insured plans – approximately $0.17 per policy per year

To fund research to assess health outcomes

High Value Plan Tax (“Cadillac Fee”)

Health insurance issuers and self-insured plans – approximately 40% on the premium in excess of thresholds

To offset costs of the ACA

Risk Pools

►Generally require health insurance issuers to treat all of their non-grandfathered business in the individual and small group market, inside and outside the exchange, as a single risk pool

►A state would have the authority to choose to direct issuers to merge their non-grandfathered individual and small group pools into a combined pool

► Indiana did not merge its individual and small group pools

Rating Factors

►Age Rating► 3:1 ratio

►Age Curve► Uniform age curve

►Family Tiers► Premiums are limited to 3 for those dependents under age 21

►Tobacco Rating► Limitation goes away in 2015

►Geographic Rating Areas► IDOI Bulletin 197

Impact on State Law

Preemption of State Law

►The Affordable Care Act does not preempt all state laws that regulate health insurance

►State laws that interfere with the ACA provisions are preempted

►State are permitted to adopt and enforce laws and regulations that afford greater consumer protections

Case law and Regulations

Recent Case law – King v. Burwell

King v. Burwell, 135 S.Ct. 2480 (June 24, 2015)► Facts: HHS provides subsidies on state and federally-facilitated Exchanges;

Plaintiffs claim it can’t do this for federally-facilitated Exchanges. If subsidies are not available in a State, the individual coverage mandate would not apply to many people and the employer mandate would not apply at all.

► Issue: May a federal agency promulgate regulations to extend tax-credit subsidies to coverage purchases through federally-facilitated Exchanges?

► Lower Courts: District Court: Granted defendants’ motion to dismiss; held subsidies available

everywhere 4th Circuit: Affirmed; found ACA ambiguous on this point and deferred to the

agency’s interpretation► Holding: Tax credits authorized under the ACA are available to individuals who

purchase insurance through a federal exchange in their state

Case law - King v Burwell

► No Chevron deference ► Principles of statutory interpretation:

The meaning of “established by a State” was ambiguous when read in context of the “overall statutory scheme”

Giving the phrase “established by the State” its most natural meaning would render other parts of the ACA meaningless or nonsensical

Other parts of the ACA assumed tax credits would be made available on both State and Federal exchanges:

► Broader structure of the ACA Structure of the ACA was designed to expand individual health insurance

coverage while controlling costs The Virginia residents’ reading “would destabilize the individual insurance

market in any State with a Federal Exchange, and likely create the very ‘death spirals’ that Congress designed the Act to avoid”

87% of people bought insurance on a Federal Exchange with tax credits

Case law - National Federation of Independent Business v. Sebelius:

National Federation of Independent Business v. Sebelius, 132 S.Ct. 2566 (June 28, 2012)► Issues: Constitutionality of:

Individual Mandate Medicaid Expansion

►Holding: The individual mandate is a constitutional exercise of Congress’ power to

levy taxes. The Medicaid expansion provision of the ACA violates the Constitution

by threatening states with the loss of their existing Medicaid funding if they decline to comply with the expansion.

2015 Developments - Administrative Rulemaking

► Agency Information Collection Activities: Proposed Collection; Comment [Transparency reporting by QHP Issuers], 80 FR 48320-01 (August 12, 2015)

► IRS Notice 2015-52: Excise Tax on High Cost Employer-Sponsored Health Coverage, www.irs.gov/pub/irs-drop/n-15-52.pdf (July 30, 2015)

► Final Rule: Coverage of Certain Preventive Services Under the Affordable Care Act. Coverage of Certain Preventive Services Under the Affordable Care Act, 80 FR 41318-01 (July 14, 2015)

► Final Rule: Summary of Benefits and Coverage and Uniform Glossary, 80 FR 34292-01 (June 16, 2015)

2015 Developments Continued

► Temporary Final Rule: Health Insurance Providers Fee, 80 FR 10333-01 (February 26, 2015)

► Final Rule: Application for Recognition as a 501(c)(29) Organization [Consumer Operated and Oriented Plan (COOP)], 80 FR 4791-01 (January 25, 2015)

► Proposed Rule: To amend the regulations and interpretive guidance implementing Title I of the Americans with Disabilities Act as they relate to employer wellness programs; 80 FR 21659-01 (April 20, 2015)

► Small Group Definition► Beginning January 1, 2016, the definition of small group will change from 1-50

employees to 1-100 employees► H.R. 1624 was proposed to keep the current definition of 1-50 employees

ACA Impact on Indiana

Impact on Market Size by 2019

Source of Health Insurance 2010 Estimate 2/15/2015 estimate 2019 ProjectionUninsured 875,000 525,000 300,000 – 525,000Public Programs 950,000 1,200,000 1,450,000 – 1,625,000Individual Insurance 200,000 220,000 450,000 - 875,000

Employer-Sponsored Insurance

Insured Small Group (2-50 employees) 300,000 275,000 225,000 – 300,000 Insured Large Group(51+ employees) 475,000 450,000 350,000 - 475,000 Self-Funded (All employer sizes) 2,825,000 2,830,000 2,850,000 – 3,125,000Total Indiana Residents Ages 0 to 64 5,625,000 5,500,000 6,200,000 – 6,500,000

References

►Annual Letter to Issuers in the Federally Facilitated Marketplace►Annual HHS Notice of Benefit and Payment Parameters►Annual Instructions Medical Loss Ratio Reporting► IDOI Company Compliance Rate/Forms including reference

documents available at www.in.gov/idoi/2588.htm ►CMS regulations and guidance available at

www.cms.gov/cciio/resources/regulations-and-guidance/ and www.regtap.info

►QHP Application, Instructions, Templates and Materials available at www.cms.gov/cciio/programs-and-initiatives/health-insurance-marketplaces/qhp.html