30

A Fresh Look at A Fresh Look at Your Retirement Your Retirement Plan Plan by Your Name, CFP

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | stephanie-golden |

| View: | 217 times |

| Download: | 0 times |

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

by

Your Name, CFP

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

Recent market events compel us to review your retirement plan in a more realistic way

After every market correction, we see that plans that were prepared using conventional retirement calculators, become irrelevant

Retirement dreams seem to be pushed further and further away, especially after each market correction

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

Before your retirement dreams turn into retirement nightmares, let’s review your retirement plan

This time, I propose using a new tool that is significantly more innovative than other retirement calculators that we have been using

This new retirement calculator uses an entirely different philosophy. It may change the way we look at retirement planning

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

All conventional retirement calculators make a FORECAST using certain assumptions:

average assumed portfolio growth rateaverage assumed inflation

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

The following example shows the reality for three generation of retirees:

The grandfather retires at the beginning of 1929

His son retires at the beginning of 1966His grandson retires at the beginning of

2000

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

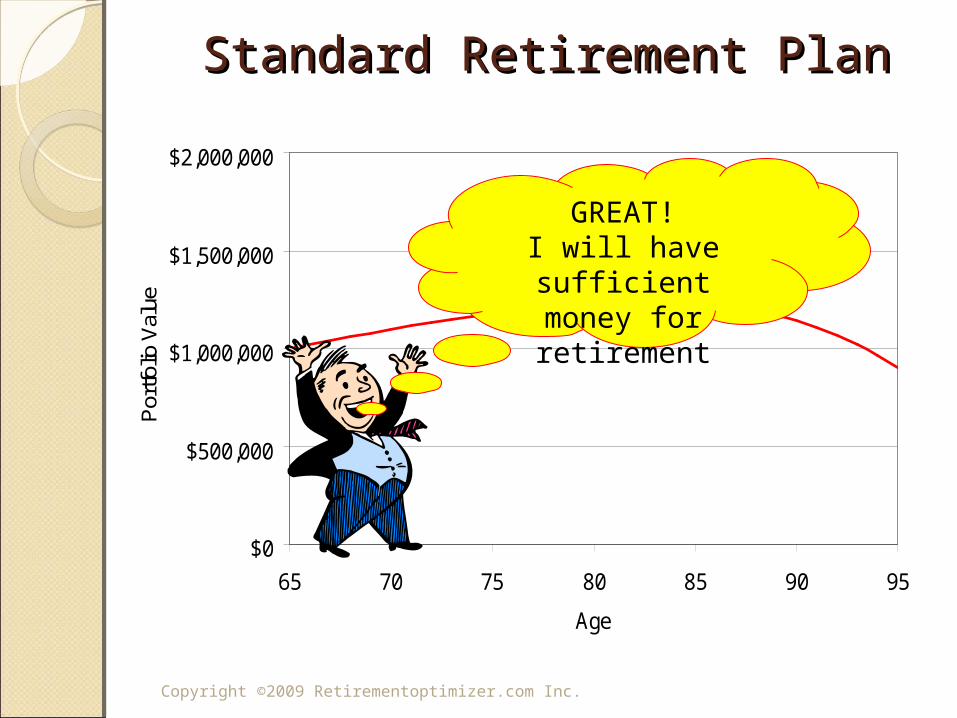

Each one starts with $1 million of retirement savings

Each one needs $60,000 to take out annuallyEach one start his retirement at age 65We assume an annual portfolio growth rate

of 8%We assume an inflation rate of 3% per year

Let’s see what happens to their retirement dreams:

Copyright ©2009 Retirementoptimizer.com Inc.

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

65 70 75 80 85 90 95

Age

Por

tfolio

Val

ue

Standard Retirement PlanStandard Retirement Plan

GREAT!I will have sufficient

money for retirement

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

The forecast looks fantastic!Let’s do a Reality Check

Copyright ©2009 Retirementoptimizer.com Inc.

Data Source: Dow Jones & Company

10

100

1,000

10,000

100,000

1900 1920 1940 1960 1980 2000 2020

DJIA

1929

Wow!Nice Bull Market!Time to Retire!

Grandfather retires in 1929

Copyright ©2009 Retirementoptimizer.com Inc.

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

65 70 75 80 85 90 95

Age

Por

tfolio

Val

ue

1/1/1938

1/1/1929

Grandfather is broke 9 years later!

Copyright ©2009 Retirementoptimizer.com Inc.

Data Source: Dow Jones & Company

10

100

1,000

10,000

100,000

1900 1920 1940 1960 1980 2000 2020

DJIA

Wow!Nice Bull Market!Time to Retire!

1966

His son retires in 1966

Copyright ©2009 Retirementoptimizer.com Inc.

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

65 70 75 80 85 90 95

Age

Por

tfolio

Val

ue

1/1/1966

1/1/1979

The son is broke 13 years later!

Copyright ©2009 Retirementoptimizer.com Inc.

Data Source: Dow Jones & Company

10

100

1,000

10,000

100,000

1900 1920 1940 1960 1980 2000 2020

DJIA

Wow!Nice Bull Market!Time to Retire?

1/1/2000

The grandson retires in year 2000

Copyright ©2009 Retirementoptimizer.com Inc.

The grandson will be likely broke

only 12 years later!

Age: 65

Age: 77

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

In the real world, it does not matter how accurate your assumptions are for your forecast.

What matters is the SEQUENCE OF RETURNS that you experience during the early years of your retirement.

Copyright ©2009 Retirementoptimizer.com Inc.

Portfolio Life Depends on Portfolio Life Depends on How Lucky How Lucky YouYou Are Are

10

100

1,000

10,000

100,000

19

00

19

10

19

20

19

30

19

40

19

50

19

60

19

70

19

80

19

90

20

00

DJIA

10.0

20.0

30.0

40.0

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000P

ort

folio

Life,

yrs

Sometimes, you might catch a bullish

trend:You can have

income for 40+ years

More often than not, you don’t catch a

bullish trend:Portfolio lasts about

15 years

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

The retirement planning tool that I use, does not forecast anything.

It does not require any assumptions or averages

This new tool only uses the actual market history.

This method of planning is called AFTCASTING

Aftcasting shows you all possible outcomes based on actual market history since 1900

Copyright ©2009 Retirementoptimizer.com Inc.

Your Retirement Plan based on Your Retirement Plan based on Actual Market HistoryActual Market History

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

Now, you can decide in a much more informed way:

When can you retire? How much do you need to save until

retirement?How much you can spend after retirement?What strategies can you to use for lifelong

income?How can you export the longevity, market and

inflation risks to others? Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

OUR GOAL:To determine your essential and discretionary

expenses during your retirementTo figure out when you can retire To create a personal pension for your essential

expensesTo minimize the luck factor for your retirement

ageTo optimize your current portfolio to maximize

return and minimize risk

Copyright ©2009 Retirementoptimizer.com Inc.

A Fresh Look at A Fresh Look at Your Retirement PlanYour Retirement Plan

Let’s try this new tool and see how we can plan your retirement more realistically.

Do you want to go ahead?

Copyright ©2009 Retirementoptimizer.com Inc.

DisclaimerDisclaimer

Otar Retirement Calculator (ORC), illustrates how a mix of asset classes (stocks, bonds, cash or inflation indexed bonds), or income classes (investment portfolio, immediate life annuity, variable annuity with or without guaranteed income), would have fared under historical market conditions, given your stated financial goals and your cash flow. It does not provide a prediction of your ability to meet your goals; rather, it merely reports the hypothetical outcomes that would have occurred in the past.

ORC should not be used as the primary basis for any investment or tax-planning decisions. Results will vary in the future. ORC is not intended to predict the future value of actual investments or actual holdings in your portfolio. It is also not intended to predict the current and future value of actual lifetime income.

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORC ORC

1. Determine retirement income and expenses

Use the “Retirement Income Cash Flow Worksheet and Budget” or your own worksheet.Spend as much time as needed to figure out these numbers as accurately as possible.

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORC ORC

2. Enter current information into ORC: Main Page: Current age, desired retirement age, current asset mix, the value of total assets earmarked for retirement, current level of savings (% of income or $/year), how much income required after retirement (% of preretirement income or $/year).Cash Flow Page: Any other income and expense information from Step #1.Observe the outcome, probability of depletion, etc.-If this is second opinion, enter the assumed growth rate and inflation in the existing plan into the comparative boxes on the main page. See if it is realistic.

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORC ORC

3. Asset Allocation - Optimize Asset Mix:Optimization of the asset mix is the easiest way of potentially improving the outcome.After optimization, observe the outcome, did it improve?- Is the optimum asset mix within your tolerable range?- Would you feel comfortable with this optimum asset mix ? If the answer is “yes” to both questions, change the asset mix to the optimum.

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORC ORC

4. Check the outcome: - Excellent: good news, skip to Step # 6

- Good, Adequate: must review annually or after major family or market events. But for the time being, skip to Step # 6

- Inadequate: needs work, go to Step # 5

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORC ORC

5. Ask, input and analyze one question at a time:- Can you delay retirement?- Can you work part-time after retirement? - Can you live on less money? (Distinguish between ”Essential” versus “Required” expenses) - Can you save more money until retirement?- Do you expect an inheritance?- How does a guaranteed income product (SPIA or VA-GMWB or VA-GMIB) improve the outcome?- Would you consider selling your home at age __ and

then renting?

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORCORC

6. Income Allocation: Optimum pension creationJust like optimizing the asset allocation is important when creating wealth during the accumulation stage, optimizing the income allocation is important during distribution stage to minimize the luck factor.To reduce the effect of the luck factor, a “pension” needs to be created. - If the outcome is “Excellent” your investment portfolio already acts as your pension. Review annually. - Otherwise, you can crate that pension either through

life annuities or variable annuities with GMWB or GMIB with lifelong income guarantees.

Copyright ©2009 Retirementoptimizer.com Inc.

Seven Steps for Using Seven Steps for Using ORCORC

7. Summarize and Present your Plan:- Print only what is necessary. I print usually only the the “Main” and “Cash Flow” pages for the base case, “Optimization” page if you are suggesting a change in the asset mix, and the “Main” page for all other scenarios. - Write your walk-through of questions, answers, scenarios- Ensure that there are no unanswered questions left - If you are handing over the plan to a client, follow your compliance rules.

Copyright ©2009 Retirementoptimizer.com Inc.

DisclaimerDisclaimer

Otar Retirement Calculator (ORC), illustrates how a mix of asset classes (stocks, bonds, cash or inflation indexed bonds), or income classes (investment portfolio, immediate life annuity, variable annuity with or without guaranteed income), would have fared under historical market conditions, given your stated financial goals and your cash flow. It does not provide a prediction of your ability to meet your goals; rather, it merely reports the hypothetical outcomes that would have occurred in the past.

ORC should not be used as the primary basis for any investment or tax-planning decisions. Results will vary in the future. ORC is not intended to predict the future value of actual investments or actual holdings in your portfolio. It is also not intended to predict the current and future value of actual lifetime income.

Copyright ©2009 Retirementoptimizer.com Inc.