19

A Guide to Startup Resources for Agriculture and Food Technology Innovation Bridging the gaps between innovation, investment, and business

A Guide to Startup Resources for Agriculture and Food Technology Innovation Bridging the gaps between innovation, investment, and business

Contents

149

111415

| WhyDoestheFoodandAgricultureTechnology/Innova?onLandscapeNeedSupport?

| ProposedCategoriesandDefini?ons

| LandscapeOverview

| InsightsandGaps

| Conclusion

| Appendix

1

WhyDoestheFoodandAgricultureTechnology/InnovationLandscapeNeedSupport?Thefoodandagricultureindustryisundergoingunprecedentedchanges.Astheleastdigitizedindustryintheworld,accordingtoMcKinsey,theindustryislongdueanotherrevolution,andthereisapressingneedtoevolvethefoodsystemsoitcansupportfuturegenerations.Wearenowonthecuspofthatrevolution.Entrepreneurs,investors,policy-makers,andcorporationsfromallcornersoftheglobearegettinginvolved,culminatingin$4.6billionofventureinvestmentintothesectorin2015.Whilethefundingoptionsforstartupsareskyrocketing,therearestillchallenges.Inparticular,startupsmustovercometwokeychallenges,orsupportgaps,onthepathfromfoundationalresearchtoindustry-widediffusion.

Thefirstgapexistsbetweenthescienceandbasicresearchthatoccurswithinuniversitylabsandcommercial,sellableproductsandservicesthatfarmerscanutilize.Billionsofresearchdollarsarespenteachyeartodeveloptransformativetechnologiesandscientificbreakthroughs;yetsupport,includingbutdefinitelynotlimitedtocapital,isnecessarytotranslatethisresearchintoviablestartupbusinesses.Thesecondgapexistsbetweenagriculturestartupsandestablished,sustainablebusinesses.Since2013,$9.65billionhasbeeninvestedinagtechstartups,withfundinglevelsgrowingexponentiallyeachyear.Whileit’sstillearlydaysforagtechinvestments,therehavebeenafewsuccessfulventureexitsinthesector.TheClimateCorporation,adigitalagriculturecompany,andBeckerUnderwood,aseedtechnologycompany,werethesector’sfirstunicornsaftertheywereacquiredbyMonsantoandBASFin2013and2012respectively.It’suncertainwhatrolethepublicmarketswillplay,butmostventurecapitalfirmsarebettingthatstrategicacquisitionswillbetheirmainexitroute,whilesomeagtechcompaniesplantobecomestandalonebusinesses.Eitherway,theindustryneedstoseemoreexitstoensureagtechstartupsremainasustainableinvestmentdestinationforventurecapitalfirms.Thechallengeofbridgingthesegapsiscomplexandwillrequiremorethanfundingandtechnicalexpertise.Trustandcredibilityremainbarriers.Participantsinallroles,fromresearchersanduniversities,tocorporationslookingforthenextdisruptiveinnovation,togovernmentstryingtosecurethefuture,tofarmersandindustrygroups,needclarityonhowtobestgetinvolvedandeffectivelycollaborate.

Science/R&D Startups Companies

Gap Gap

2

Inotherindustries,likesoftwareandevenhardware,ecosystemslikeSiliconValleyhaveenabledresearcherstoconnectwith,orevenbecome,theentrepreneursandinvestorsthatcanthen

turnbasicscientificinsightsintotransformativebusinesses.Incontrast,researchandindustryexpertiseinfoodandagriculturehasremainedinsideofuniversityandcorporatelabs.Theindustryisstrugglingtobringagreaternumberoftheseinnovationstomarketandtoscale.Resourcestosupportfoodandagricultureventuresinbridgingthesegapsareemerging.Atthetimeofthisreport,wehaveidentified77resourcesdedicatedspecificallytofoodandagriculture.Theseresourcesrangefromacceleratorstoincubatorstoventuredevelopmentorganizations(VDOs).

Throughdifferentapproaches,theseresourcefocusoncreatingandsupportingsuccessfulfoodandagriculturetechnologycompanies.Somefocusonprovidingfunding,whereasothersfocusonfosteringcollaborationbetweenscientists,engineers,famers,entrepreneurs,andinvestors.Whileresourceswillundoubtedlyhelptofillcriticalgapsinthecontinuumfromideatoimpact,thereisstillsignificantconfusionaroundwhatexactlytheyallofferandtheterminologyusedtodescribethem.Theindustrylacksacommonlanguagetodescribeanddifferentiatetheseresources.

0%5%10%15%20%25%30%35%40%45%

Accelerator CorporateIncubator

Incubator Network/Ecosystem

PitchEvent Prize VDO

ResourceCategoriesbyNumberandPercentofTotal

32 4 6 6 7 11 11

Agriculturalresearchinvestmenthasalwaysbeenacornerstoneofgovernmentinvestmentandyethasbeenanunderexploredareafordeal9low.Thislackofinvestmentdepthisdrivenpartiallybythefactthat

researchinagricultureisoftendisconnectedandwithoutthevisibilityofcomplementarytechnologysuitesandexpertise,developmentisoftenundertakeninavacuumwithonlyonepieceofthepuzzle.Ithasalsobeenlimitedbythefactthatthetalentpoolofag-entrepreneursandsophisticatedinvestorswithdomainexpertisehasbeenlimited.

–Kapyon(VDO)

3

Thisreportlaysoutaproposalforhowtodefinethedifferenttypesofresourcesastheyemergeinthesector.Wedescribethecurrentlandscapeasitis,includingworkingdefinitionsforcategoriesofresources,andacomprehensivelistofresourceswithineachcategory.Ouraimistostarttoresolvesomeoftheconfusionandtostartthediscussiononthisgrowingecosystem.Weinvitecomments,suggestions,etc.aswehopethisworkcanleadtomoreclarity,efficiency,collaboration,andimpactfulinnovationacrossthefoodandagriculturelandscape.

TerminologyUsed• Resource:program,organization,oreventintendedtosupportearly-stage

ventures(e.g.,Food-X,FoodSystem6,AgTechAccelerator)• Category:genericclassificationforaresource(e.g.,Accelerator,Incubator)• Subsector:specificareaoffocuswithinthefoodandagriculturesystem(e.g.,

FoodTech,CPG,rowcropproductionagriculture,etc.).• FoodandAgricultureSystem:broadlydefinedvaluechain,frominputsand

productiontoprocessing,manufacturing,anddistribution.

4

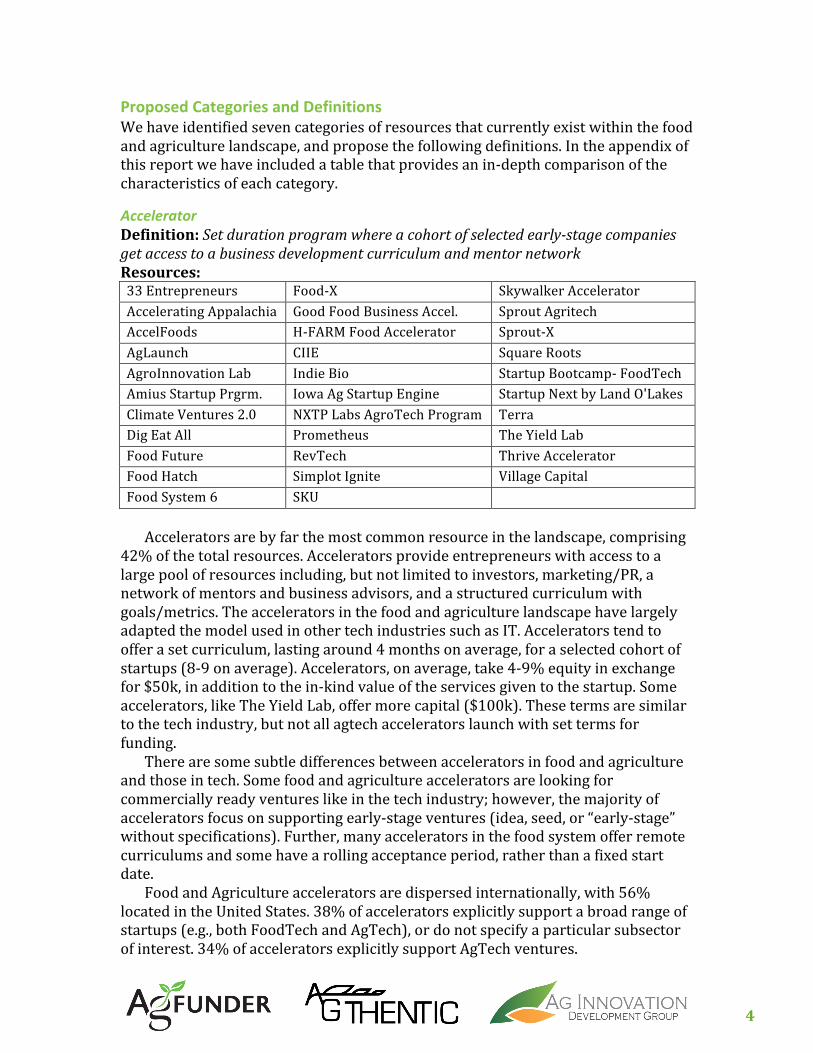

ProposedCategoriesandDefinitionsWehaveidentifiedsevencategoriesofresourcesthatcurrentlyexistwithinthefoodandagriculturelandscape,andproposethefollowingdefinitions.Intheappendixofthisreportwehaveincludedatablethatprovidesanin-depthcomparisonofthecharacteristicsofeachcategory.

AcceleratorDefinition:Setdurationprogramwhereacohortofselectedearly-stagecompaniesgetaccesstoabusinessdevelopmentcurriculumandmentornetworkResources:33Entrepreneurs Food-X SkywalkerAcceleratorAcceleratingAppalachia GoodFoodBusinessAccel. SproutAgritechAccelFoods H-FARMFoodAccelerator Sprout-XAgLaunch CIIE SquareRootsAgroInnovationLab IndieBio StartupBootcamp-FoodTechAmiusStartupPrgrm. IowaAgStartupEngine StartupNextbyLandO'LakesClimateVentures2.0 NXTPLabsAgroTechProgram TerraDigEatAll Prometheus TheYieldLabFoodFuture RevTech ThriveAcceleratorFoodHatch SimplotIgnite VillageCapitalFoodSystem6 SKU Acceleratorsarebyfarthemostcommonresourceinthelandscape,comprising

42%ofthetotalresources.Acceleratorsprovideentrepreneurswithaccesstoalargepoolofresourcesincluding,butnotlimitedtoinvestors,marketing/PR,anetworkofmentorsandbusinessadvisors,andastructuredcurriculumwithgoals/metrics.TheacceleratorsinthefoodandagriculturelandscapehavelargelyadaptedthemodelusedinothertechindustriessuchasIT.Acceleratorstendtoofferasetcurriculum,lastingaround4monthsonaverage,foraselectedcohortofstartups(8-9onaverage).Accelerators,onaverage,take4-9%equityinexchangefor$50k,inadditiontothein-kindvalueoftheservicesgiventothestartup.Someaccelerators,likeTheYieldLab,offermorecapital($100k).Thesetermsaresimilartothetechindustry,butnotallagtechacceleratorslaunchwithsettermsforfunding.

Therearesomesubtledifferencesbetweenacceleratorsinfoodandagricultureandthoseintech.Somefoodandagricultureacceleratorsarelookingforcommerciallyreadyventureslikeinthetechindustry;however,themajorityofacceleratorsfocusonsupportingearly-stageventures(idea,seed,or“early-stage”withoutspecifications).Further,manyacceleratorsinthefoodsystemofferremotecurriculumsandsomehavearollingacceptanceperiod,ratherthanafixedstartdate.

FoodandAgricultureacceleratorsaredispersedinternationally,with56%locatedintheUnitedStates.38%ofacceleratorsexplicitlysupportabroadrangeofstartups(e.g.,bothFoodTechandAgTech),ordonotspecifyaparticularsubsectorofinterest.34%ofacceleratorsexplicitlysupportAgTechventures.

5

CorporateIncubatorDefinition:Accesstocapitalandresourcesofacorporation,usuallywithintentionofbeingacquiredResources:ChobaniFoodIncubator MarriottCANVASCoca-ColaVEB TheKitchenCorporateincubatorsareinnovationprogramsthatbringstartupsintoa

particularcompanywiththeexplicitpurposeofaddressinganeedofthecompanyoritscustomers.Essentially,corporateincubatorshelpcompaniesoutsourcetheirR&Dinhopesofmakingtheinnovationprocesscheaperandfaster.Theestablishedcompanycanscoutpotentiallydisruptivetechnologies,andthenbringthesestartupsin,therebygainingcontrolandensuringtheestablishedcompanywillbenefitdirectly.Startupsbenefittoo:thecorporationprovidesresourcessuchasphysicalspace(e.g.,lab),mentorship,accesstotheirindustryexpertiseandnetworks,andpossiblycapital(inexchangeforequity).Corporateincubatorsprovidesignificantlymorefundingthanaccelerators,oftencloserto$500k.Butstartupsenteringacorporateincubatormayriskappealingtoonlyonecompanyandlimitingtheirexitpotentialorcustomerbase.Corporateincubatorsinthefoodandagriculturelandscapearespreadinternationally,andmosthaveaCPGfocus.

Wehaveidentifiedfourcorporateincubatorprogramsexplicitlydedicatedtosupportingventureswithinthefoodandagriculturesystem.TwoareintheU.S.oneinIsrael,andonewithmultipleinternationallocations.Allfourcorporateincubatorsarefood(ratherthanagriculture)focused.Corporateincubators,liketheUnileverFoundry,thatmaysupportventuresinthisspacebutarenotentirelyfocusedonthisindustry,werenotincluded.

IncubatorDefinition:Physicalworkspaceorlabthatprovidessupportsuchastechnologicalexpertiseandmentorship;nofixedduration;rollingacceptanceResources:Ag-celeratorProgram UCDavis-HM.CLAUSELifeScienceInnovationCenter

Farm491 WesternGrowersInnovationCenter

RoCRE AgricenterInternational

Wehaveidentifiedsixincubatorprograms.FourareintheU.S.andtwoareintheUK.AllsixoftheincubatorsarefocusedontheAgTechsubsector,accordingtoourclassifications,thoughonlytwoofthefiveexplicitlymentiontechnologyasakeycomponent(i.e.,othersmentiononly“agriculture”).Incubatorsoftenhaveexplicitconnectionstogrowersorgrowerorganizations,thereforeofferingservicessuchaspilotsorfieldtrials.Manyoftheincubatorsalsohaveconnectionstouniversitiesandseektoprovideapathwaytocommercializationforemergingresearch.Incubatorssupportearlystageventures,potentiallyevenworkingattheideaorbenchstageofthedevelopmentprocess.

6

Network/EcosystemDefinition:Platform,oftenvirtual,thatprovidesaccesstoresourcessuchasmentorsandinvestorsResources:AgFunder Coca-ColaFoundersAgri-TechEast Farm2050Branchfood RoyseLawAgTechInnovationNetwork

Virtualnetworksthatservetoconnectentrepreneurstoeachotherandtoresourcessuchasmentorsandinvestorsareemergingasalow-commitmentsupportresourceforfoodandagricultureventures.Someofthesenetworksareglobalandentirelyvirtual,whileothersfocusoncreatinganinnovationhubinaparticularregion.Thesixthatwehaveidentifiedsupportearly-stageFoodTechandAgTechstartups.Intermsofsupport,theseresourcesofferevents,hackathons,orworkshopsinadditiontovirtualservices(e.g.,newsletter,networkofmentors).OtherthanAgFunder,whichisacrowdfundingplatform,thesenetwork/ecosystemsdonotprovidefunding.

PitchCompetitionDefinition:One-timeevent,usuallyfocusedonconnectingstartupstoinvestorsResources:AgInnovationShowcasebyLarta InvestMidwestVentureCapitalForumFoodBytesbyRabobank MixingBowlGoldenBlenderAwardFoodFunded WorldAgri-TechInvestmentSummitGAIAgTechWeek

Wehaveidentifiedsevenpitchevents,sixofwhichhappenintheU.S.andonethatoccursinvariouslocationsinternationally.Thepitcheventsarebroadintermsofthesubsectorstheysupport.

Pitchcompetitionsgivestartupsanopportunitytopresenttheirvisionandbusinessplantoanaudience,usuallyfilledwithinvestorsandotherentrepreneurs.Pitchcompetitionstypicallydonotoffermonetaryprizes;thebenefitfortheentrepreneurisrecognitionandthechancetovalidatetheirideawiththejudgesandaudience.Pitchcompetitionsareone-timeevents,often,butnotalways,occurringaspartofaconference.Sometimes,finalistsmustpassthroughmultipleselectionroundsbeforebeingacceptedtothefinalpitchevent.Startupsaregenerallyjudgedonsomecombinationoftechnologicalviability,marketopportunity,originalityoftheidea,team,andqualityofthepresentation.Frequentlyinvestorsarethejudges.

7

PrizeDefinition:Competition,usuallyculminatinginapitchevent,withmonetaryrewardResources:AgBiotechShowcase NetImpactFoodForward

AccentureFairFoodInnovationAward

SecuringWaterforFood

Fish2.0 SyngentaCropChallengeFoodEcosystemaccelerator ThoughtforFood(TFF)GROWBusinessPlanCompetitionbyAgri-techEast

VerticalFarmingInnovationAward

MITFoodandAgribusinessInnovationPrize

Unlikepitchevents,prizesrewardwinnerswithcash.Theamountofprize

moneyvariesbetween$5kand$50k,thoughmostprizesoffer$5k-$10kawards.Prizeshaveamulti-stageselectionprocess,oftenincludingamentorshipperiodwhereselectedstartupsworkwithmentorstorefinetheirideasandpresentationskills.Prizesculminateinapitcheventwherethewinnersareselectedbyapanelofinvestorjudgesoraliveaudience.Likewithpitchcompetitions,startupsaregenerallyjudgedonsomecombinationoftechnologicalviability,marketopportunity,originalityoftheidea,team,andqualityofthepresentation.Prizesoftenreceivesponsorshipfromoneormorecorporations.

Wehaveidentifiedelevenprizeeventsinternationally.FiveareintheU.S.,andthreeareintheNetherlands.Someprizestargetveryspecificareas,suchasseafoodorverticalfarming,whileothersarebroadandopentoventuresinmanysubsectors.

VentureDevelopmentOrganizationDefinition:PerformscommercializationfunctionseitherasaserviceorbylicensingIP;oftentheyareregionallyfocused,andhavetiestocorporations,universities,and/orgovernment.Resources:AgInnovationDevelopmentGroup KapyonAgri-FoodVentureAccelerationProgram(AVAP)

RutgersFoodInnovationCenter

AgTechAccelerator SteinbeckInnovationCenterBioEnterprise TrendlinesAgTechFlagshipVentureLabs WaikatoLinkVentureIncubator

GreatLakesAgTechBusinessIncubator

VDOsareuniquewithinthelandscapeinthattheysupportventuresatallstages,

frombenchtomarket.Forexample,aVDOmightworkwithemergingIP,licensingitandbuildingacompany.ThatIPmightbedevelopedin-house,orsourcedfrom

8

externalorganizationssuchascorporateoruniversitylabs.SomeVDOsalsoworkwithestablishedstartups,providingsupportintheformofconsultingservicesoraccesstogrowersforpilots.Regardlessoftheoriginofthetechnology,VDOslooktobringaportfolioofinnovationstomarketthroughmultiplechannels.Technologiesmaybelicensed,soldentirely,orspunoutintoastartup.

VDOsarealsouniqueinthattheyseektoleveragepublicfunding,forexamplebyprovidinganacceleratedpathwaytomarketfortechnologiesemergingfromagriculturalresearchinstitutions.TheVDOmodelhasbeensuccessfulinotherindustries,suchashealthcare,butthemodelisnewandthereforeunprovenwithinAgTech.

VDOsmainlyrelyonthereturnsfromtheirportfolioofcompanies,aswellasfeesfromconsultingservices.Adiversifiedportfolioisthereforecriticaltosuccess;however,itisalsoachallengetofindthetalentrequiredtocommercializeabroadportfolio.SomeVDOshirethisexpertise,whileothersincentivizenetworksofconsultants.Further,bringingaproducttomarketistoughinallcases,yetVDOsmustattractorcreatesufficientdealflowwhilesimultaneouslycontrollingcosts.Despitethesechallenges,VDOsinfoodandagriculturehaveattractedinvestmentfromleadingagribusinesses.

WehaveidentifiedelevenVDOs,sevenofwhichareintheU.S.TenoftheVDOssupporttheAgTechsubsector;onesupportsCPG.

9

LandscapeOverview

SummaryofResources:• Thereare77resourcesgloballythatarespecificallyintendedtosupportfood

andagricultureventures

• Over80%wereestablishedwithinthelastfouryears

• 58%arelocatedinU.S.

• Mostresourcessupportagricultureventures.Many(27%)supportmultiple

subsectorsand/ordonotspecifywhichparticularsubsectorsareofinterest.

• Mostresourcestargetearlystage-ventures(e.g.,idea/seed)

SubsectorsInthechartbelow,wehaveclassifiedthe77resourcesaccordingtothe

subsectorstheyclaimtosupport.Themajorityoftheresourcesincludedinthis

reportdonottargetaspecificsubsector(e.g.,CPG)ormarketvertical(e.g.,precision

agriculture);instead,theresourcesbrandthemselvesasprovidingsupportfor

“FoodTech”and/or“AgTech”startups.

WehaveclassifiedthosethatsupportbothFoodTechandAgTech,ormake

evenbroaderclaims,withinthe“Multiple/All”category.Thiscategorylargely

comprisesaccelerators.Acceleratorsoftenhavemultiplestakeholders,from

corporatesponsors,tomentors,toinvestors,totheirfund’sLPs,tothestartups

themselves,sohavingabroadareaofinterestmaybepartoftheirstrategytocater

tothesediverseinterests.Forstartups,thismayormaynotbeanadvantage.Onone

hand,adiversecohorthasabreadthofexperiencesandcanoffermultiple

10

perspectives;however,theacceleratormaynotbeabletoproviderelevantresourcesforparticularareas.

CPGresourceswarranttheirowncategory,astheventurestheysupportaregenerallynottechnology-based,andthereforerequirementorswithdifferentexpertise.ResourcesdedicatedtoCPGventuresincludeaccelerators,corporateincubators,andoneVDOandonePrize.

Theresourceswithinthe“other”categorysupportanumberofmorespecificverticals,includingrestauranttech,gastronomy,alcohol,andcannabis.

Thoughsomeconsensusisemergingaroundthedefinitionofeachsubsector,forexamplefromthecategorizationprovidedintheoft-citedAgFunderbi-annualfundingreports,thesetermsarelargelyundefinedandremainextremelybroad.Thisisachallenge,asupstreamventures(e.g.,sensorsuitesthatenhanceon-farmdecisionmaking)facefundamentallydifferentobstaclesthandownstreamventures(e.g.,mealkits;seaweedchips).

11

InsightsandGapsDespitetheremarkablenumberofresourcesacrossthefoodandagriculture

landscapethatarededicatedtosupportingearly-stageinnovation,challengesremainforallstakeholders.Herearethefivekeyinsightsgainedfromthisreport,includingoutstandinggapsandpromisingopportunities.

1. ResourcesneedtoclearlycommunicatetheirvaluepropositionThefoodandagricultureindustrylacksacommonlanguagetodescribeboththe

categoriesofsupportresourcesaswellasthevarioussubsectorsthatexistfromproductiontoconsumption.Understandingthedifferencebetween,forexample,anincubatorandVDO,orFoodTechandAgTech,isimportantasitenableseachresourcetodifferentiateitself.Currently,websites,andevenpressreleasesandmediacoverage,arelargelyinsufficientintermsofexplainingaresource’suniquevalueproposition,acceptancecriteria,andsubsectorsofinterest.Everyoneisusingthesamelanguage;or,evenworse,providingverylittleexternalinformationatall.Potentialinvestorsorcollaboratorsthereforestruggletonavigatethelandscape.

Further,eachsubsectorhasauniquesetofchallenges,andentrepreneursmustbeabletofinddedicatedsupportfortheirventures.Forexample,ventureswithinupstreamsubsectorsmayneedaccesstogrowersoron-farmpilots,whiledownstreamventuresmayneedtoworkcloselywithretailers.Go-to-marketstrategies,pricingmodels,andmarketingpersonaswillbedrasticallydifferentacrosssubsectors.Successfulresourcesmustappreciatethesedifferencesandprovideappropriateexpertisetotheventurestheysupport.

Further,asothertypesofsupportresourcescontinuetoemerge,it'snecessarytounderstandwheretheyfitintothelandscape.Aretheyaddressingaspecificgap,andifso,whichgap,andhowwilltheyattempttofillit?Acommonunderstandingofthecurrentlandscapewillhelpnewresources,andthosethinkingaboutcreatingnewresources,totargetagapinthelandscapeandpositionthemselvestouniquelyaddvalue.

Clarityonuniquevaluepropositions,acceptancecriteria,andareasofexpertisewillmakethematchmakingprocessbetweenstartupsandsupportresourcesmuchmoreefficient.

2. Whatisasustainablebusinessmodel?Iftheresourcesinthefoodandagriculturelandscapearegoingtohelpcreate

impactful,commercialcompaniesoutoffoundationaltechnologies,theythemselvesmustbesustainablebusinesses.Currently,thebusinessmodelformostoftheresourcesdependsonacombinationofsponsorshipsandgrants,consultingrevenues,andreturnsonequityinvestments.Therearechallengeswitheachoftheserevenuestreams.Forexample,sponsorshipsandgrantsaretemporaryandnotreliable,andstartupsmaynotbeabletoaffordconsultingfees.

Further,itisnotclearifraisingafundandrelyingonequityinvestmentswillwork.Aventurefundcanbehelpful:theresourcecanhirededicatedoperatorsandpaythemwiththefund’smanagementfees;theresourceitselfservesasapipelineofdealsforthefund;andventuresthatparticipateintheresourceknowthatthe

12

resourcehasavestedinterestinsupportingthem.However,ifthefundisnotsuccessful,theresourcemayhavetroubleraisingsubsequentones.Also,thefinancialmodelfortheresourceisthendependentonVC-typereturnsandtimeframes.Itisnotclearifthiswillworkforallsubsectorswithinthefoodandagriculturelandscape.

3. Competitionwithtraditional(tech)resources Thoughonlypreliminaryresearchaboutacceleratorsuccessratesexists,data

indicatethattopprogramsareindeedvaluabletostartups(e.g.,Cohen&Hochberg,2014;Fehder,2015).However,notopprogramshaveemergedwithinthefoodandagriculturelandscape.Entrepreneursmaythereforebemorelikelytoapplytoestablishedresourcesinotherindustriessuchastech.Forexample,in2016theYCombinatordemodayfeaturedfiveAgTechstartups.

Competitionisoverallagoodthing,asitforcestheresourcestoadduniquevalue.But,atthisstageforfoodandagriculture,toomuchcompetitionmaycreateaviciouscyclewherebydedicatedfoodsystemresourcesstruggletogaintraction.

4. Wheredoinvestorsfit?AsleadingtechVCsturntheirattentiontowardtheopportunitiesinfoodand

agriculture,morefundsdedicatedtofoodandagriculturearelaunched,andnewformsofcapitalsuchasimpactinvestors,familyoffices,andcorporateventurecapitalfundsemerge,investorsofalltypesneedtodifferentiatethemselvestomaintainhighqualityandhighvolumedealflow.

Onestrategyisforinvestorstogetinvolvedwiththetypesofsupportresourcesoutlinedinthisreport.Forexample,investorsoftenserveasmentorsandadvisorstothestartupsinacceleratorsorVDOs.Investorsarewellpositionedtohelpstartupsrefinetheirpitchandde-riskthemselvestoattractcapital:theyknowwhattheyandtheirpeersarelookingforinaportfoliocompany.Investorscanalsoprovidefinancialsupportfortheresources,liketheVCfirmSOSVwhichbacksIndieBioandFood-X,orCultivationCapitalwhichbacksTheYieldLab.Investorsarealsoservingontheboardoroperatingteamofaresource,suchasstrategicinvestorsSyngentaandBayerservingontheAgTechAcceleratorboardofdirectors.Finally,investors,especiallystrategicinvestors,canofferconnectionstotheirparentcompaniesandaccesstoinfrastructure,distribution,orcustomers.

Investors,especiallyVCs,arealsoincreasingthespectrumofservicestheyprovidetotheirportfoliocompanies.Inaway,thismakestheinvestorverysimilartoothersupportresources,suchasanacceleratororincubator.Forexample,SonomaBrandsreferstoitselfasa“ventureincubator”forCPGfoodstartups,andRadicleCapitalreferstoitselfasan“acceleratorfund.”Neitherofthesetworesourcesisincludedinourcategorizationabove.Thoughadditionalsupportfrom

Wechose[aleadingtechaccelerator]becauseconnectionstothefoodindustryareabsolutelycriticalforus,butourbiggerprioritywaslearninghowtobuild

andscaleaB2B/enterprisetechcompany.Joiningamoretraditionalbusinessacceleratorhasallowedustodevelopthemoreprofessionalbrandasatechnologycompanytoappealtobothlarge-scalefood

businessesandVCs.Ialsothink[beingafoodcompany]differentiatedusintheapplicationprocessforsomeofthemoretraditionalaccelerators.

-FoodTechStartupFounder

13

investorsisawelcomeadditiontothelandscape,thesenameshighlightthelackofconsensusaroundterminology,creatingconfusionforallparticipants.

5. Istheresufficientdomain-specificsupport?Tobridgethegapsbetweenresearchandcommercialcompaniesinfoodand

agriculture,significantdomainexpertisemaybenecessary.Inparticular,thisisachallengeforupstreamsubsectors(i.e.agriculture)giventhecomplexityofthenatural,technical,andsocialsystemsinvolved.Thoughmanyresourcescurrentlyseektosupportventuresinthisspace,therearestillafewcriticalgaps.Forexample:

• Lackoffocusonsmall,butimportant,nicheareassuchasrowcropcommodityproduction,specialtycropirrigation,andsoilhealth

• Lackofgrowerengagementacrossmostoftheresourcesinthelandscape• Lackofphysicalinfrastructure,suchaslabspaceandin-fieldpilotsUnfortunately,evenmanyofthemost“successful”agricultureventureshave

thusfarfailedtoachievedeepmarketpenetration.GrowersmaybeusingAgTechproducts,butunfortunatelytheseproductshavefailedtodemonstratesufficientvaluetoattractpayingcustomersonalargescale.Focusingonhigh-valueniches,engagingwithgrowers,andaccessinginfrastructurearenecessary.Ingeneral,thereisalackofsupport-andcapitalinparticular-forin-fieldagriculture,asmuchofthefundingiscurrentlyallocatedtodownstreamsubsectors(i.e.,FoodTech,andespeciallyecommerce).Thoughthisischangingastheindustryisbeginningtoacknowledgethisgap,providingmoredomain-specificsupportforAgTechventuresisahugeopportunityfortheresourcesinthelandscape.

Finally,itisalsoworthraisingthequestionofwhetheritismosteffectivetoprovidedomain-specificexpertiseattheresourcelevel.IfAgTechstartupscan,forexample,succeedbyworkingwithYCombinator,thenmaybededicatedfoodandagricultureresourcesarenotnecessary.Perhapsfoodandagricultureventuresshouldbeworkingwithleadingtechnologyandbusinessresources,butbuildingtheirteamswithin-housedomainexpertiseorlookingforinvestorswithdomainexpertise.

14

ConclusionEffectivesupportforearly-stageinnovationwithinthefoodandagriculture

systemiscritical.Theresourcesidentifiedinthisreporthavethepotentialtohelpcrossthegapsbetweenfoundationalresearchandindustry-widediffusionandimpact.Butwestillhavealongwaytogoandmanyquestionsremainedunanswered.

Ratherthanattempttoanswertheoutstandingquestions,thisreportisintendedtostimulatediscussionandcollaborationwithinthefoodandagricultureinnovationecosystem.Inotherwords,wewantyourfeedback.Didweplacearesourceinthewrongcategory?Doyouhavesuggestionsforhowtorefinetheproposeddefinitions?Didwemissaresource?

We’dlovetohearfromyou.PleasecontactauthorSarahNoletatsvnolet@agthentic.com.

15

Appendix:MethodologyandSummaryofCategoryDefinitionsThisreportisintendedtoprovideanoverviewoftheavailablesupport

resourcesforstartupsinthefoodsystem.Thedatawerecollectedviacompanywebsites,pressreleases,andnewsarticlesfromsourcessuchasAgFunderNewsandTechCrunch.Foreachresource,thefollowingdatawerecollected:name,location,yearestablished,subsectorsofinterest,targetcompanystage,fundingreceived/costtoparticipate,cohortsize,timeline,andwhethercompaniesmustparticipateinperson.Thoughwebelievethisreporttobecomprehensive,itispossiblethatsomeresourceswereunintentionallyexcluded.

Simultaneously,weconductedareviewoftheliteratureonearly-stageventuresupportresourcesfromotherindustries,suchashealthcare,software,andbiotech.Wespecificallyfocusedoncategorydefinitions(e.g.,incubatorvs.accelerator).Theseindustrydatawerecomparedwithourfindingsonfoodsystemresources,andultimatelytheexistingcategorydefinitionswereamendedasappropriatetoderivethedefinitionsproposedinthisreport.Thefollowingtypesofresourceswereintentionallyexcludedfromthisreport:coworkingspaces,crowdfundingplatforms,hackathonsandotherevents,commissarykitchensandkitchenincubators,andanyresourcesthatdonothavethefoodindustryasastatedfocus(e.g.,TechStars).

WhilethemajorityoftheresourcesincludedinthisreportarefocusedonprovidingsupportforFoodTechandAgTechventures,wehaveincludedresourcesforstartupsacrossthefoodsystem,fromupstreamagriculture,includinginputsandsyntheticbiology,toconsumer-facingproducts,suchasCPGfoodandbeverageandrestauranttech.Thoughitisclearlyusefultoentrepreneurstounderstandthefocusareandexpertiseofaparticularresource,ourfindingsindicatethatmanyoftheresourcesthemselvesdonotprovidespecificguidanceontheirparticularsubsectorsofinterest.

Thetablebelowprovidesasummaryofthecategoriesanddefinitionsproposedinthisreport.

16

Learn more at www.AgThentic.com | Contact us at [email protected]

AgThentic is a sustainability and innovation

consulting firm for the food system. We sit at the intersection of big companies, entrepreneurs, and investors, helping change agents create the food

system of the future.

This report was produced by AgThentic, in collaboration with AgFunder and Ag Innovation Development Group