A Half-day Workshop on “Stress Testing” (A Tool of Risk Management) Held at Learning Resource Centre, SBP November 23, 2006 Conducted by: Mr. Muhammad Akhtar Javed, Joint Director-BSD Ms. Rizwana Rifat, Assistant Director-BSD STATE BANK OF PAKISTAN

Transcript

A Half-day Workshop on“Stress Testing”

(A Tool of Risk Management)Held at Learning Resource Centre, SBP

November 23, 2006

Conducted by:

Mr. Muhammad Akhtar Javed, Joint Director-BSDMs. Rizwana Rifat, Assistant Director-BSD

STATE BANK OF PAKISTAN

SBP

Outline

Stress TestingStress Testing Meaning of Stress TestingMeaning of Stress Testing Why need stress TestingWhy need stress Testing Uses of Stress TestingUses of Stress Testing

Main Guidelines Underpinning Sound Main Guidelines Underpinning Sound Stress Testing by InstitutionsStress Testing by Institutions Relevance Depending on Size and Sophistication of Relevance Depending on Size and Sophistication of

InstitutionsInstitutions Stress Testing CoverageStress Testing Coverage Stress Testing CalibrationStress Testing Calibration Frequency and Time Horizon of Stress TestingFrequency and Time Horizon of Stress Testing Data Quality and IT SystemsData Quality and IT Systems

SBP

Outline – Continued...

Main Guidelines …..Main Guidelines ….. Role of Management Body and Senior ManagementRole of Management Body and Senior Management Review and Update of Stress Testing MethodologyReview and Update of Stress Testing Methodology

Stress Testing Guidelines Issued by Stress Testing Guidelines Issued by SBP….SBP…. Reporting FormatReporting Format What is required from BanksWhat is required from Banks Road to futureRoad to future Stress Test ResultsStress Test Results International ExperiencesInternational Experiences

SBP

Stress Testing- Meaning

As defined by the BIS, stress testing is a risk management technique used to evaluate the potential effects on an institution’s financial condition of a specific event and/or movement in a set of financial variables. The traditional focus of stress testing relates to exceptional but plausible events.

SBP

Why Need Stress Tests

Stress testing is : Risk management tool

Helps in assessment of the risks Quantifies the resilience towards shock events Helps manage the shock results

Required by the Capital Directive…Basel II rigorous program of stress testing periodic stress tests of the credit risk

concentrations the realization of collateral in stressed situations stress testing processes for use in the assessment

of its capital adequacy…. etc.

SBP

Uses of Stress Testing

As a diagnostic tool to improve the institution’s understanding of its risk profile.Earnings are a part of an institution’s overall capital planning and are the first line of defense to absorb losses. Therefore, institutions should, in the context of their internal capital adequacy assessment process (ICAAP), assess how their earnings are affected by stress situations.

As a forward looking toolsStress testing may be used to assess the adequacy of

internal capital.

SBP

Types of Stress Testing

Stress testing could generally fall within the following two categories and concepts: scenario tests and sensitivity analyses.

Sensitivity analyses are generally less complex to carry out since they assess the impact on an institution's financial condition of a move in one particular risk factor, the source of the shock not being identified.

Whereas scenario tests tend to consider the impact of simultaneous moves in a number of risk factors, the stress event being well defined.

SBP

Main Guidelines Underpinning Sound Stress Testing by InstitutionsRelevance depending on the size and sophistication of institutions•As a general rule, sophisticated institutions should use a combination of both scenario tests and sensitivity analysis whereas less complex institutions may develop a less technically demanding approach. •Scenarios with greater coverage across product lines or geographical regions, and considering secondary effects, may be rather employed by large and complex institutions.

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…Stress testing coverage

Institutions should identify their material risks.

The main areas which institutions have considerable exposure to (e.g. where they are an active market maker) should be the ones most thoroughly captured under a stress testing framework. Institutions should thus determine all material risks that can be subject to stress testing.

The identification of material risks could stem from:

•a comprehensive review by institutions of the nature and composition of their portfolios.•a review of the external environment in which institutions are operating with a view to assessing the extent that this could affect their financial condition.

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…Stress testing calibration

Based upon the identification of material risks, institutions should derive material risk factors that should be subject to stress testing.Institutions should first identify their points of vulnerability in order to stress the relevant risk factors that may affect their earnings/profitability or solvency. With this in mind, an analysis of past losses can provide valuable information.The number of risk factors to be stressed should depend on the complexity of the portfolio and the risks the institution is exposed to.

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…Frequency and time horizon of stress

testing•the nature of the risk factors captured under the stress testing framework, and in particular their volatility.•the techniques used by institutions while performing stress tests.•significant changes in the external environment or in the risk profile of institutions.•the availability of the external data required to conduct the stress tests (for instance, data necessary to perform macroeconomic stress tests).

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…Frequency and time horizon of stress

testing

•Institutions should determine the time horizon of stress testing in accordance with the maturity and liquidity of the positions stressed.

•Under specific circumstances, supervisors may require institutions to perform ad hoc stress tests at a specific point in time.

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…Data quality and IT systems

Institutions should use accurate, complete, appropriate andrepresentative data when performing stress tests and the ITresources should be commensurate with the complexity of thetechniques and the coverage of stress tests performed byinstitutions

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…

Role of the management body and senior management; reporting and interpretation of stress testing results

•The management body has the ultimate responsibility for the overall stress testing framework. Where appropriate the management body can delegate certain aspects of this framework to specific risk committees or senior management, keeping the effective oversight.

•The stress testing process should be an integral part of an institution’s risk management framework, with clear reporting lines and communication in an understandable format.

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…

Review and update of stress testing methodology

Institutions should consider periodically whether stress tests are still adequate. In particular, institutions should ensure that assumptions regarding the risk profile and the external environment are still valid over time .

This assessment should cover in particular:the scope of exposures captured under the stress testing process,•· the validity of the assumptions,•· the adequacy of the management information system,

SBP

Main Guidelines Underpinning Sound Stress Testing by Institutions…

Review and update of stress testing methodology

•· the integration into the institution’s management processes, including the clarity of reporting lines,•· the approval policy of the stress testing process (including in case of changes),•· the reliability, accuracy and completeness of data incorporated into the stress testing process, and•· the quality of the documentation of the stress testing process.

SBP

Stress testing guidelines by risk categories

Macroeconomic stress testsIn doing so, an institution should consider the effects of macroeconomic factors on its capital and whether it could affect its strategic plans.

If the level of risk of a specific category is material enough to make the institution vulnerable with respect to this risk, the institution has to take the risk into account when assessing the adequacy of its internal capital. However, some risks are more qualitative in nature and therefore cannot be measured exactly.

•some kinds of operational risk (e.g. legislative risk), •reputational risk or strategic risk.

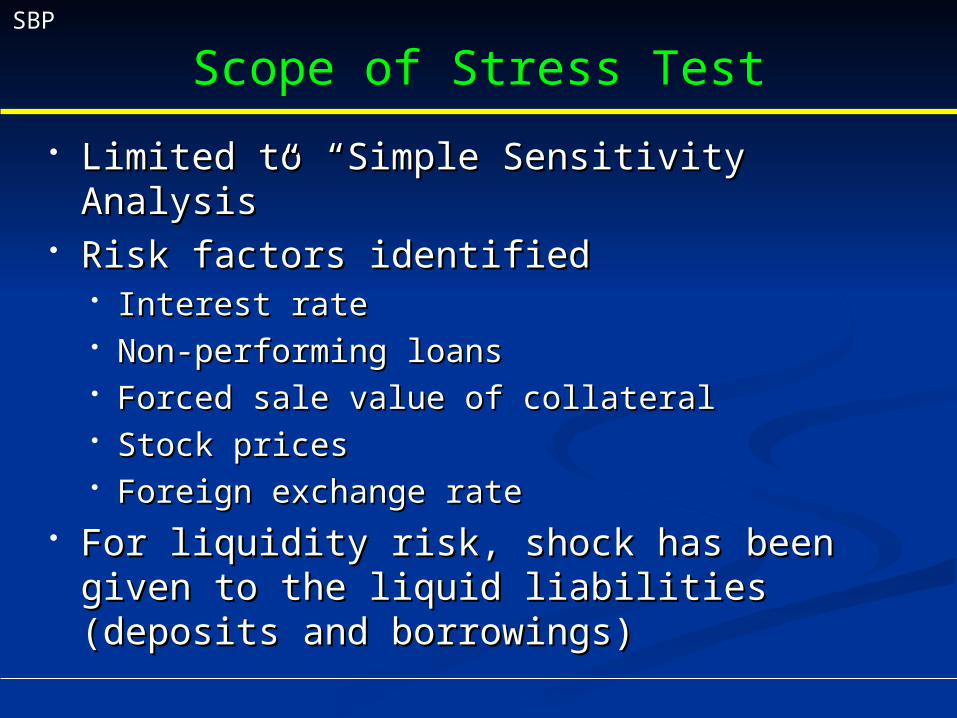

Limited to “Simple Sensitivity Analysis”Limited to “Simple Sensitivity Analysis” Risk factors identifiedRisk factors identified

Interest rateInterest rate Non-performing loansNon-performing loans Forced sale value of collateralForced sale value of collateral Stock prices Stock prices Foreign exchange rateForeign exchange rate

For liquidity risk, shock has been given For liquidity risk, shock has been given to the liquid liabilities (deposits and to the liquid liabilities (deposits and borrowings)borrowings)

SBP

Level of Shocks

Risk FactorsRisk Factors MinoMinorr

ModeraModeratete

MajoMajorr

Increase in Interest Rate Increase in Interest Rate 1%1% 2%2% 5%5%

Adverse movement in Adverse movement in Exchange RateExchange Rate

5%5% 10%10% 15%15%

Increase in NPLs Increase in NPLs 5%5% 10%10% 20%20%

Downward Shift in NPLs Downward Shift in NPLs categoriescategories

50%50% 80%80% 100100%%

Fall in the FSV of Fall in the FSV of CollateralCollateral

10%10% 20%20% 40%40%

Fall in the value of Equity Fall in the value of Equity ExposureExposure

10%10% 20%20% 40%40%

Fall in Liquid LiabilitiesFall in Liquid Liabilities 10%10% 20%20% 30%30%

SBP

Methodology

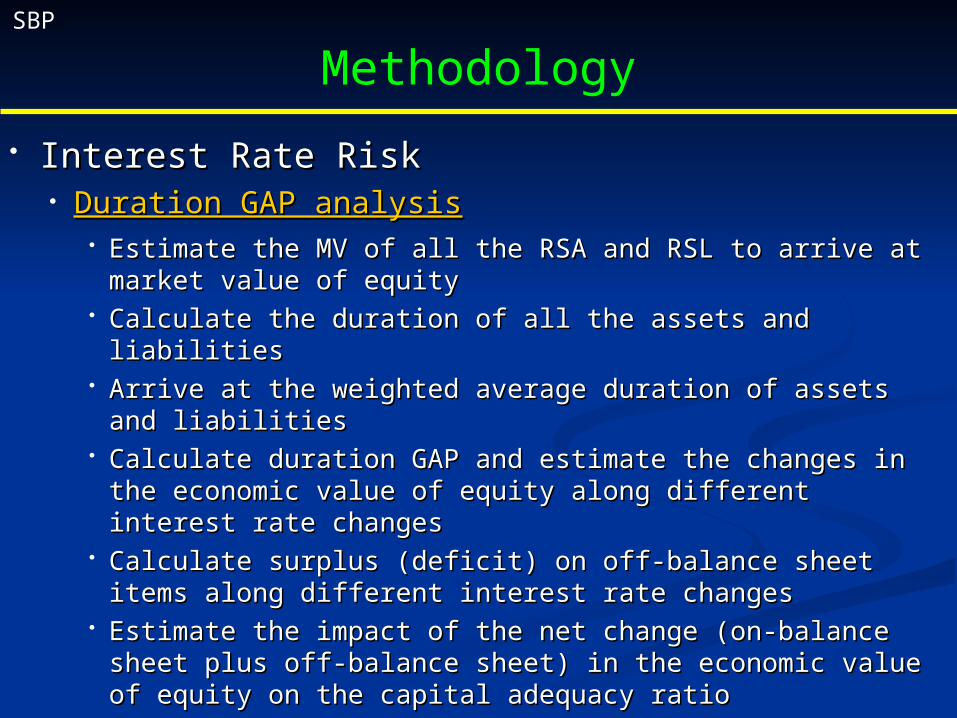

Interest Rate RiskInterest Rate Risk Duration GAP analysisDuration GAP analysis

Estimate the MV of all the RSA and RSL to arrive at Estimate the MV of all the RSA and RSL to arrive at market value of equitymarket value of equity

Calculate the duration of all the assets and liabilitiesCalculate the duration of all the assets and liabilities Arrive at the weighted average duration of assets and Arrive at the weighted average duration of assets and

liabilitiesliabilities Calculate duration GAP and estimate the changes in the Calculate duration GAP and estimate the changes in the

economic value of equity along different interest rate economic value of equity along different interest rate changeschanges

Calculate surplus (deficit) on off-balance sheet items Calculate surplus (deficit) on off-balance sheet items along different interest rate changesalong different interest rate changes

Estimate the impact of the net change (on-balance sheet Estimate the impact of the net change (on-balance sheet plus off-balance sheet) in the economic value of equity plus off-balance sheet) in the economic value of equity on the capital adequacy ratioon the capital adequacy ratio

SBP

Methodology

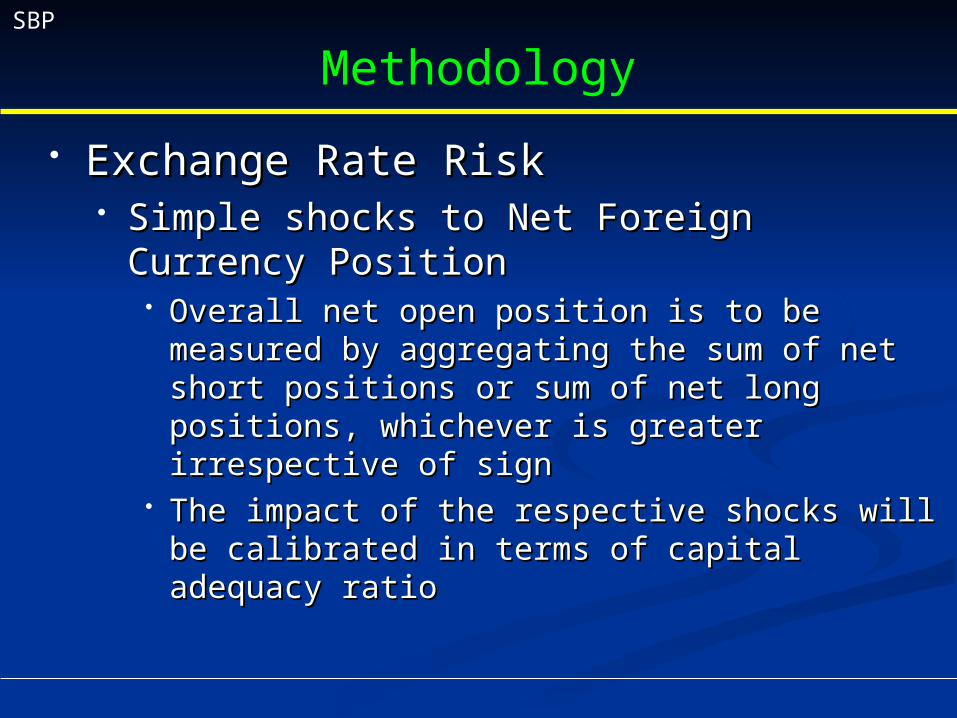

Exchange Rate RiskExchange Rate Risk Simple shocks to Net Foreign Currency Simple shocks to Net Foreign Currency

PositionPosition Overall net open position is to be measured by Overall net open position is to be measured by

aggregating the sum of net short positions or aggregating the sum of net short positions or sum of net long positions, whichever is greater sum of net long positions, whichever is greater irrespective of signirrespective of sign

The impact of the respective shocks will be The impact of the respective shocks will be calibrated in terms of capital adequacy ratiocalibrated in terms of capital adequacy ratio

SBP

Methodology

Credit RiskCredit Risk Involves three types of shocksInvolves three types of shocks

Increase in NPLs by 5%, 10% and 20% and Increase in NPLs by 5%, 10% and 20% and directly downgraded to loss category directly downgraded to loss category

Shift in NPLs categories by 50%, 80% and Shift in NPLs categories by 50%, 80% and 10%10%

Fall in the forced sale value of mortgaged Fall in the forced sale value of mortgaged collateral by 10%, 20% and 40%collateral by 10%, 20% and 40%

Tax-adjusted impact of each scenario will Tax-adjusted impact of each scenario will be calibrated in capital adequacy ratiobe calibrated in capital adequacy ratio

SBP

Methodology

Equity Price RiskEquity Price Risk Simple shocks to the market value of Simple shocks to the market value of

listed shares, NIT units and mutual funds listed shares, NIT units and mutual funds etc. by 10%, 20% and 40%etc. by 10%, 20% and 40%

The impact of resultant loss will be The impact of resultant loss will be calibrated in the CARcalibrated in the CAR

SBP

Methodology

Liquidity RiskLiquidity Risk Simple shocks to the liquid liabilities Simple shocks to the liquid liabilities

(deposits and borrowings)(deposits and borrowings) Impact is calibrated in liquid assets to Impact is calibrated in liquid assets to

liquid liabilities ratioliquid liabilities ratio Comfortable level of ratio after shock is Comfortable level of ratio after shock is

considered at 30%considered at 30%

SBP

Reporting Format

Please see the Reporting Format on the Please see the Reporting Format on the Following Link:Following Link:

Stress Testing Reporting FormatStress Testing Reporting Format

SBP

What’s Required from Banks and DFIs

Establishing an organizational set-up Establishing an organizational set-up for regular stress testingfor regular stress testing

Carrying out and submit to SBP stress Carrying out and submit to SBP stress test on half-yearly basis in line with test on half-yearly basis in line with these guidelinesthese guidelines

SBP

Road to Future

With the increasing know how and With the increasing know how and availability of more data the model will availability of more data the model will over time undergo further refinementover time undergo further refinement

SBP BOX - 6.1Reference Scenarios

Credit ShocksScenario C-1 assumes a 10 percent increase in NPLs (with a provisioning rate of 100 percent).Scenario C-2 assumes a withdrawal of benefit of FSV against NPLs.Scenario C-3 assumes a cumulative impact of the two shocks under Scenarios C-1 and C-2.

Scenario C-4 assumes an increase in NPLs equivalent to 5 percent of gross advances (with aprovisioning rate of 50 percent for additional NPLs).Scenario C-5 refers to the NPLs to total loans ratio, which would wipe out capital (with a 50 percentprovisioning rate for additional NPLs).

Market Risk: Interest Rate ShocksScenario IR-1 assumes an increase in interest rates by 200 basis points.Scenario IR-2 assumes an increase in interest rates of outlying maturities (by 0, 100, and 150 basispoints)Scenario IR-3 assumes a shift coupled with flattening of the yield curve by increasing 150,100 and 50basis points in the three maturities respectively.

Market Risk: Exchange Rate ShocksScenario ER-1 assumes a depreciation of ER by 25 percent (around double of the change in themonthly average PKR/US$ exchange rate (12.83) over the period from Jan 1994 to Dec 2005, inSeptember 2000).

Scenario ER-2 is based on the hypothetical assumption of appreciation of rupee by 10 percent.

Scenario ER-3 assumes a 10 percent depreciation of the rupee and deterioration in the quality of 10percent of unhedged foreign currency loans with 50 percent provisioning requirement.

Market Risk: Equity Price Risk ShocksScenario E-1 assumes the impact of a 20 percent decline in the Stock Market Index.Scenario E-2 assumes the impact of a 40 percent decline in the Stock Market Index.

Liquidity ShocksScenario L-1 assumes a 5 percent decline in the liquid liabilities and its impact on liquidity coverageratio calculated after excluding Govt. securities under Held to Maturity category from liquid assets.

Scenario L-2 assumes a 10 percent decline in the liquid liabilities and its impact on liquidity coverageratio calculated after excluding Govt. securities under Held to Maturity category from liquid assets.

Scenario L-3 assumes a 5 percent decline in the liquid liabilities and its impact on liquidity coverageratio calculated after including Govt. securities under Held to Maturity category in liquid assets.

Scenario L-4 assumes a 10 percent decline in the liquid liabilities and its impact on liquidity coverageratio calculated after including Govt. securities under Held to Maturity category in liquid assets.

SBP

%age Point Change in

CAR

Revised CAR- After Shock

%age Point Change in

CAR

Revised CAR- After Shock

Credit ShocksScenario C-1 Deterioration in the quality of loan -0.52 11.83 -0.49 12.08Scenario C-2 Withdrawal of Benefit of FSV -0.98 11.37 -0.98 11.59Scenario C-3 Combined impact of Scenario C1 & C2 -1.50 10.85 -1.47 11.10Scenario C-4 Deterioration in the quality of loan by 5% -1.97 10.38 -1.96 10.61Scenario C-5 Level of NPLs to loans ratio where capital wipes out (i.e.

34.74% in Mar-06 and 35.09% in Jun-06) -12.35 0.00 -12.57 0.00Market Shocks; Interest Rate ShocksScenario IR-1 Shift in the yield curve -0.94 11.41 -0.88 11.69Scenario IR-2 Steepening of the yield curve (large shock) -0.84 11.51 -0.62 11.95Scenario IR-3 Shift & flattenining of the yield curve -0.28 12.07 -0.27 12.30Market Shocks; Exchange Rate ShocksScenario ER-1 Depreciation of Rs/US$ exchnage rate (double of the

historical high) 1.42 13.77 0.03 12.60Scenario ER-2 Appreciation of Rs/US$ exchnage rate (hypothetical) -0.58 11.77 -0.01 12.56Scenario ER-3 Depreciation in ER along with deterioration of quality of FX

Loans (50 % Provisioning) 0.00 12.35 -0.21 12.36Market Shocks; Equity Price ShocksScenario E-1 Fall in the KSE index (historical high) 0.00 12.35 -0.14 12.43Scenario E-2 Fall in the KSE index (hypothetical scenario) -0.31 12.04 -0.42 12.15

Actual Stressed Actual Stressed

Scenario L-1 5 Percent Fall in the Liquid Liabilities 32.9 29.4 36 32.6Scenario L-2 10 Percent Fall in the Liquid Liabilities 32.9 25.5 36 28.9Scenario L-3 5 Percent Fall in the Liquid Liabilities 39.4 36.2 40 36.9Scenario L-4 10 Percent Fall in the Liquid Liabilities 39.4 32.6 40 33.4Note: The results have not been adjusted for deferred tax benefits accruing on these losses.

Liquidity Coverage Ratio

Mar-06

Single and multifactor sensitivity tests

Jun-06

BOX 6.2

Results of “Stress Tests” of Pakistan's Banking System

Liquidity Shocks

International International ExperiencesExperiences

Adopted by Europe, America and Many Emerging EconomiesA survey conducted on some of these countries

reveals that these countries believe stress testing as a tool

Interest rates are the most common theme among the sensitivity stress tests reported on the census.

Nearly all banks responded that stress tests are used as a tool for risk managers to understand the firm’s risk profile and communicate that information to senior management.

International International Experiences…Experiences…

Banks use stress test limits in combination with other limits, on notional position size, position sensitivity (ie delta), or VaR.

a majority of the reporting banks have acted on the results of stress tests.

Three-quarters of global dealer banks and just over half of internationally active banks answered that stress tests have led to the unwinding or hedging of a position.

All banks reported that stress tests covered the trading book, while two-thirds reported that stress tests also covered the banking book.

The design of stress tests draws heavily on historical events, even for hypothetical scenarios.