• The following disclosures are included, as a minimum, within the notes to the financial statements: (P.104)

• a statement of compliance with FRS 102;

• significant accounting policies;

Notes to the FS – S.8

• information about judgements that management has made in applying the accounting policies and that have the most significant effect on the amounts disclosed in the financial statements; (P.62 & P.90)

• key sources of estimation uncertainty;

• explanatory notes for items presented in the financial statements; and

• information not presented in the primary statements.

Consolidated and Separate FS S.9

• 9.3 Small Group Exemption (P.115)

– CA 2014 T/o €20m, BS €10m, 250 Ee 2 out of 3

– Intermediate parent exemption

• Subsidiary defined based on control

• Control is the power to govern the financial and operating policies of an entity to obtain benefits from its activities

• S10.5 When adopting policies if FRS does not not fully cover a transaction or condition

– Apply the FRS (or FRC Guidance documents)

– SORP

– The basic concepts and pervasive principles

• S10.6 Management may also consider the requirements of EU Adopted IFRS

Accounting Policies – S.10

• Changes in policies

– Full and specific disclosure

– Prior period adjustment – retrospective application

– Transitional Provisions

• Changes in estimates

– Prospective treatment

– Disclosure

Accounting Policies – S.10

• FRS 18 V FRS 102• FRS 18 ‐ In exceptional circumstances if the financial statements

in prior periods have been issued with errors that are of such significance as to destroy the “true and fair” view and hence the validity of the financial statements (fundamental errors) prior periods should be accounted for retrospectively (prior period adjustment adjust opening reserves and comparative figure) with all other errors being accounted for prospectively (adjusted in the current period)

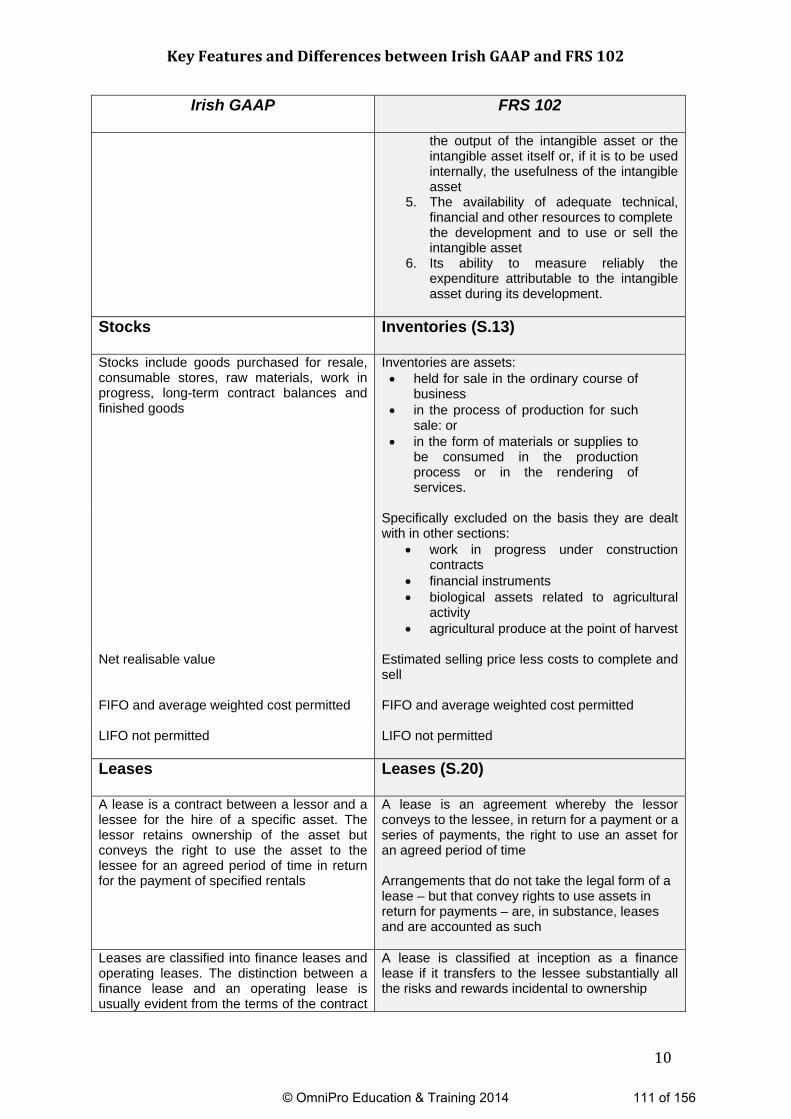

• Development – may be capitalised if it meets the criteria

– The technical feasibility of completing the intangible asset so that it will be available for use or sale.

– Its intention to complete the intangible asset and use or sell it.

– Its ability to use or sell the intangible asset.

Intangible Assets other than Goodwill S.18

How the intangible asset will generate probable future economic benefits. Among other things, the entity can demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, theusefulness of the intangible asset.

The availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset.

Its ability to measure reliably the expenditure attributable to the intangible asset during its development.

• Comparative periods ending 31st of December 2014

• Transition Date 1st of January 2014

• Comparatives to be reported

The Transition Process – S35

• The entity’s first financial statements that conform to FRS102 make an explicit and unreserved statement.

• “This is the first set of financial statements prepared in accordance with FRS 102

The Transition Process – S35

• At the date of transition entities are required to prepare anopening balance sheet (opening statement of financial position)

• Four Steps– Recognise all assets and liabilities in accordance with FRS 102– Derecognise items previously recognised as assets/liabilitiesnot permitted under FRS 102

– Reclassify items that it recognised under Irish GAAP that aretreated differently under FRS 102

– Apply FRS 102 in measuring all recognised assets andliabilities

– A description of the nature of each change in accountingpolicy

– Reconciliation of equity as determined under previous IrishGAAP and its equity determined under FRS 102

• At the date of transition to FRS 102• At the end of the latest reporting period presented in the financial

statements

– A reconciliation of the profit/(loss) determined inaccordance with Irish GAAP for its latest reporting periodand its profit/(loss) for the same period as determinedunder FRS 102

The Transition Process – S35

Mandatory Exceptions for RetrospectiveApplication of FRS 102

– Derecognition of financial assets and liabilities– Hedge Accounting– Accounting Estimates– Discontinued Operations– Measuring Non-Controlling Interests

• Group Accounts Consolidation and the Adoption of Accounting Policies

Current Financial Reporting Issues

• Treatment of Preference Shares under FRS 25 –Equity V Liabilities

• Goodwill Amortisation Rates under FRS 10

• FRS 15 – Non Depreciation of Assets & Disclosure of valuations

• Related Party Transactions and Group Relief from Disclosure

OmniPro Why– Assist Accountants– Sustain profitability– Deal with on-going changes– Improve quality of customer service– Be compliant – Institute, audit company & law– Achieve success– Gain peace of mind– So Accountants can do the same for their clients

– OmniPro Practice Support • Pre-Monitoring Visits• Hot File Reviews• Cold File Reviews• Practice Development• Practice Sale, Purchase & Merger• In House Training• File Review Services• Practice Incorporation

– OmniPro Education & Training & cpdstore.com

– Professional CPD Seminars – Public & Online

• Technical CPD

• Personal Development Training for Accountants

– Time management, business communication skills, Presentation skills, team leadership, management development

Year Ended 31 December 2015 ______________________________________________________________ Disclaimer These financial statements are solely illustrative and intended to be used exclusively for educational and training purposes. They provide guidance in relation to the format and contents of FRS 102 company financial statements under the relevant company legislation and financial reporting standards. They do not purport to give definitive advice in any form. Despite taking every care in the preparation of this document OmniPro does not take any legal responsibility for the contents of these financial statements and the consequences that may arise due to any errors or omissions. OmniPro shall therefore not be liable for any damage or economic loss occasioned to any person acting on, or refraining from any action, as a result of or based on the material contained in this publication. The size criteria used to assess small and medium companies is outlined below. For those Companies which exceed two or more of the following in the current and preceding year. Large Co Medium Co Turnover €15,236,856 €8,800,000Balance Sheet Total €7,618,428 €4,400,000Employees 250 50

ES PASE (Ethical Standard Provisions Available for Small Entities) may be availed of for those Companies which meet two or more of the following:

not more than €7.3million in turnover; not more than €3.65million balance sheet total; and not more than 50 employees.

Disclosures in this regard have been included in this Pro-Forma set of Financial Statements. Each set of Financial Statements should be specifically tailored for each client.

Page Directors and other information 3 Directors report 4 - 7 Directors responsibilities 8 Independent Auditors Report to the Members 9 - 10 Profit and loss account 11 Balance sheet 12 Statement of Changes in Equity 13 Cashflow Statement 14 Statement of accounting policies 15 - 21 Notes to the financial statements 22 - 34

Directors1 Mr A Director Ms B Director Mr C Director Secretary Mr A Director Auditors Compliant Accountant & Co,

Registered Auditors, Accountants Row, Any County Bankers Any Big Bank PLC, Money Street, Moneysville, Any County Deep Pockets Bank, Financial Services Sector, Ballycash, Any County Solicitors Legal Eagles & Co., Court Place, Judgestown Any County Registered Office Construction Place, Builders Lane, Dunblock Any County

This information is disclosed as best practice, there are no legislative requirements attaching to directors and other information disclosures 1 State nationality of directors if not Irish

The directors present their annual report and audited financial statements for the year ended 31 December 2015. Principal Activities and Business Review23 The principal activity of the company is the provision of construction services to both the private and commercial sectors. From their operations base and depot in Construction Place, Builders Lane, Dunblock, Any County they also sell pre-cast concrete products to private individuals and the construction industry. The company is supplied with the pre-cast concrete products by a wholly owned subsidiary company, which operates independently from a separate location. The company has continued to improve performance in recent years. Turnover has increased by xx% on prior year allowing the firm to maintain excellent profitability levels in a challenging and rapidly changing industry. Future Developments4 The directors are not expecting to make any significant changes in the nature of the business in the near future. Or The directors have indicated their intention to capitalise on industry shifts by continuing to review and focus their operations accordingly in the future. Results and Dividends5 The retained profit for the financial year amounted to €244,883 (2013: €276,132) and this was transferred to reserves at the year end. The directors have not declared a dividend for the year. Or The retained profit for the financial year amounted to €244,883 (2013: €276,132). An interim dividend of €xx.xx (2013: €xx.xx) per ordinary share, amounting to €xx,xxx (2013: €xx,xxx) was paid on 1 December 2013. A final dividend of €xx.xx (2013: €xx.xx) per ordinary share, amounting to €xx,xxx (2013: €xx,xxx) was declared and authorised on 30 May 20146 and will be paid on 30 September 2014.7 €xx,xxx was transferred to reserves at the year end. Principal Risks and Uncertainties8 In common with all companies operating in Ireland in this sector, the company faces increasing energy and material costs. The directors are of the opinion that the company is well positioned to manage these costs. 2 Section 13(a), Companies (Amendment) Act 1986 – Include information relevant to subsidiary undertakings if necessary 3 Section 158(3), Companies Act 1963 – Document any significant changes during the year in the nature of the business of the company or of its subsidiary undertakings 4 Section 13(c), Companies (Amendment) Act 1986 5 Section 158(1), Companies Act 1963 6 Dividends must be declared and authorised in advance of the year end 7 Amend as appropriate depending on the payment of dividend or not 8 Section 13(a), Companies (Amendment) Act 1986 – Include information relevant to subsidiary undertakings if necessary

OmniPro Sample Medium/Large Company operates in a cyclical industry and is affected by factors beyond the control of the company for example level of construction activity. OmniPro Sample Medium/Large Company faces strong competition in the market and if the company fails to compete successfully market share may decline. Financial Risk Management9 The company’s operations expose it to a variety of financial risks that include price risk, credit risk, liquidity risk and interest rate risk. To maintain stable cash out flows the company maintains 100% (2013: 100%) of its debt at fixed rate and to maintain 50% of its debt payable within one year. The company does not use derivative financial instruments to manage financial risk and no hedge accounting is applied. Price Risk The company is exposed to the price risk of commodities through its operations. The directors believe that the cost of managing this risk is in excess of the potential benefits given the size of the company. The directors, however, review the appropriateness of this policy on an annual basis. Credit Risk The company requires that appropriate credit checks are carried out on new customers before sales are made. All customers have individual credit limits that are reviewed on an on-going basis by the board. Provisions for bad debts are made based on historical evidence and any new events which might indicate a reduction in the recoverability of cash flows. Liquidity Risk The company maintains a mix of long and short term finance to ensure the company has sufficient funds available to meet obligations as they fall due. Interest Rate Risk The company holds both interest bearing assets and liabilities. Assets include cash balances which earn a fixed rate of interest. The company policy is to maintain debt at a fixed rate to ensure future interest cash flows. Impact of FRS 102 The financial statements for the year ended 31 December 2015 have been prepared in accordance with FRS 102 and the comparative figures for the year ended 31 December 2014 were restated where necessary under FRS 102. Directors The directors who held office during the year are listed on page 3. Mr. A Director and Ms. B Director retire from the board by rotation in accordance with the Articles of Association and, being eligible, offer themselves for re-election10.

9 Section 13(f), Companies (Amendment) Act 1986 – Required for large companies where material financial instruments are used by the company 10 Deemed best practice under Memo & Arts

Director’s & Secretary’s interests11 The director’s and secretary’s interests in the company at the beginning and end of the year were as follows; Mr A Director Ms B Director €1 ordinary shares €1 ordinary shares Total At the beginning of the year 550 250 800 At the end of the year 550 250 800

Or Details of directors’ shareholdings, transactions and related interests are set out in Note XX to the financial statements. Events after the Balance Sheet date12 There have been no significant events affecting the company since the year-end. Or Post year end the company into a contract to purchase the trade of a related business, this will increase turnover and profits going forward. Research and Development13 The company did not engage in any research and development activity during the year. Or The company was engaged in research and development activities in the development of patents, the cost incurred in the year was €xx,xxxx. Political donations14 The company made the following political donations in the current year:

Party A - €xx,xxx Party B - €xx,xxx Party C - €xx,xxx

Payment of Creditors15

11 Section 63, Companies Act 1990 – Director’s interests can also be disclosed by way of note to the accounts (Shadow directors interests must also be disclosed) 12 Section 13(b), Companies (Amendment) Act 1986 13 Section 13(d), Companies (Amendment) Act 1986 14 Section 17, Electoral (Amendment) (Political Funding) Act 2012 – Disclosure is required if political donations are in excess of €200 in the year. 15 Disclose if suppliers purport to trade under the terms of the EC (Late Payment in Commercial Transactions) Regulations 2012

The directors acknowledge their responsibility for ensuring compliance with the provisions of the EC (Late Payment in Commercial Transactions) Regulations 2012. It is the company’s policy to agree payment terms with all suppliers and to adhere to those payment terms. Accounting Records16 The Directors acknowledge their responsibilities under Section 202 of the Companies Act 1990 to keep proper books and records for the company. In order to comply with the requirements of the act, a full time management accountant is employed. The books and records of the company are kept at the registered office and principal place of business at Construction Place, Builders Lane, Dunblock, Any County. Auditors In accordance with Section 160 (2) of the Companies Act, 1963, the auditors, Compliant Accountant & Co., Registered Auditors / Statutory Auditors / Statutory Audit Firm, Accountants Row, Any County will continue in office. On behalf of the board17 Mr A Director Ms B Director Director Director DATE: Additional disclosures not covered above:

An analysis of financial and non-financial key performance indicators used by the company - Section 13(a), Companies (Amendment) Act 1986

An indication of the existence of overseas branches and the countries in which they operate - Section 13(c), Companies (Amendment) Act 1986

16 Section 90, Company Law Enforcement Act 2001 17 Section 158(2), Companies Act 1963

The directors are responsible for preparing the Directors' Report and the financial statements in accordance with Irish law and regulations. Irish company law requires the directors to prepare financial statements giving a true and fair view of the state of affairs of the company and the profit or loss of the company for each financial year. Under that law the directors have elected to prepare the financial statements in accordance with Irish Generally Accepted Accounting Practice (accounting standards issued by the Financial Reporting Council and promulgated by the Chartered Accountants Ireland / Institute of Certified Public Accountants / Association of Chartered Certified Accountants/Institute of Incorporated Public Accountants18 and Irish law). In preparing these financial statements, the directors are required to:

select suitable accounting policies and then apply them consistently; make judgments and accounting estimates that are reasonable and prudent; prepare the financial statements on the going concern basis unless it is inappropriate to

presume that the company will continue in business19.

The directors are responsible for keeping proper books of account that disclose with reasonable accuracy at any time the financial position of the company and enable them to ensure that the financial statements comply with the Companies Acts 1963 to 2013. They are also responsible for safeguarding the assets of the company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities. The directors are responsible for the maintenance and integrity of the corporate and financial information included on the company's website. Legislation in Ireland governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions20. On behalf of the board Mr A Director Ms B Director Director Director DATE:

18 Amend as required depending on regulating Institute 19 Include where no separate statement on going concern is made by the directors 20 Include only if accounts are available on the company website

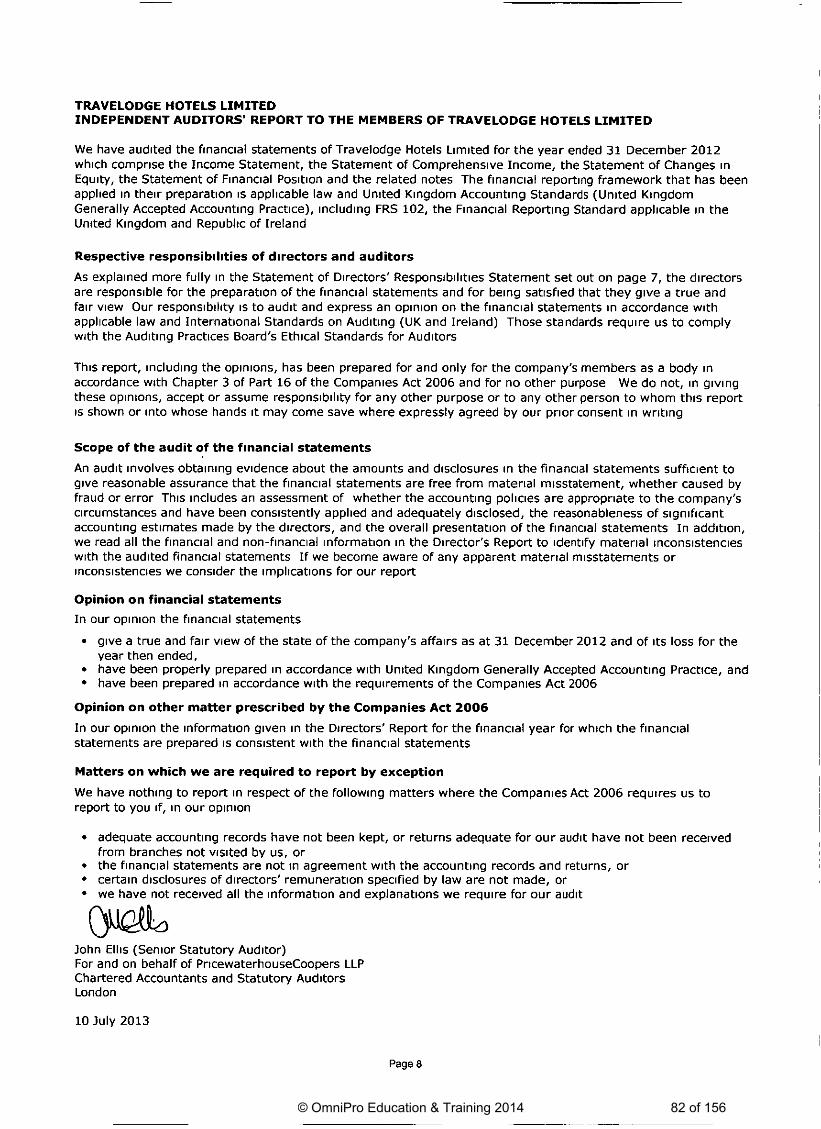

Independent Auditors Report to the Members of OmniPro FRS 102 Sample Co. Limited for the year ended 31 December 2015

We have audited the financial statements of OmniPro FRS 102 Sample Co Limited for the year ended 31 December 2015, which comprises of Profit and Loss Account, the Balance Sheet, Statement of Changes in Equity and a Statement of Cash Flows and the related notes. The financial reporting framework that has been applied in their preparation is Irish law and accounting standards issued by the Financial Reporting Council and promulgated by Chartered Accountants Ireland / Institute of Certified Public Accountants / Association of Chartered Certified Accountants / Institute of Incorporated Public Accountants21, including FRS 102 “The Financial Reporting Standard applicable in the UK and Republic of Ireland (Generally Accepted Accounting Practice in Ireland). This report is made solely to the company's members as a body in accordance with Section 193 of the Companies Acts, 1990. Our audit work has been undertaken so that we might state to the company's members those matters that we are required to state to them in the audit report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company or the company’s members as a body for our audit work, for this report, or for the opinions we have formed. Respective responsibilities of directors and auditors As explained more fully in the Directors’ Responsibilities Statement the directors are responsible for the preparation of the financial statements giving a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with Irish law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board's [APB's] Ethical Standards for Auditors, including "APB Ethical Standard – Provisions Available for Small Entities (Revised)", in the circumstances set out in note [x] to the financial statements22. Scope of the audit of the financial statements An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the company’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the annual report to identify material inconsistencies with the audited financial statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report. Opinion on financial statements In our opinion the financial statements:

give a true and fair view in accordance with Generally Accepted Accounting Practice in Ireland of the state of the company’s affairs as at 31 December 2015 and of its profit for the year then ended; and

have been properly prepared in accordance with the requirements of the Companies Acts 1963 to 2013

Matters on which we are required to report by the Companies Acts 1963 to 2013

21 Amend as required depending on regulating Institute 22 Insert if ES PASE is being applied by the firm

We have obtained all the information and explanations which we consider necessary for the purposes of our audit.

In our opinion proper books of account have been kept by the company. The financial statements are in agreement with the books of account. In our opinion the information given in the director’s report is consistent with the financial

statements. The net assets of the company as stated in the balance sheet are more than half the amount of

its called-up share capital and, in our opinion, on that basis there did not exist at 30th of June 2014 a financial situation which under Section 40 (1) of the Companies (Amendment) Act 1983 would require the convening of an extraordinary general meeting of the company.

Matters on which we are required to report by exception We have nothing to report in respect of the provisions in the Companies Acts 1963 to 2013, which require us to report to you if, in our opinion the disclosures of directors’ remuneration and transactions specified by law are not made23. Signed by: Personal name of auditor Date: For and on behalf of: Compliant Accountant & Co24

Chartered Chartered Accountants & Registered Auditors/Statutory Audit Firm, Accountants Row, Any County

ACCA

Chartered Certified Accounts & Statutory Auditors/Statutory Auditor, Accountants Row, Any County

CPA

Certified Public Accountants & Statutory Audit Firm, Accountants Row, Any County

IIPA

Incorporated Public Accountant Firm, Accountants Row, Any County

23 Section 191(8), Companies Act 1963 – Particulars of Directors salaries not disclosed

24 The firm name must reflect the name of the firm as it appears on the public register of the Registrar of Companies

Distribution expenses (345,987) (326,531)Administration expenses 5 (2,837,435) (2,945,133)

Operating profit 1,799,085 281,207

Interest payable and similar costs 6 (246,586) (199,721)

Profit on ordinary activities before taxation 1,552,499 81,486

Taxation 7 (297,505) (92,626)

Profit/(Loss) on ordinary activities after taxation 1,254,994 (11,140) 31-Dec 31-Dec 2015 2014 Statement of Comprehensive Income € € Profit/(Loss) for the financial year 1,254,994 (11,140) Deferred tax relating to revaluation of tangible assets - 25,000 Total Comprehensive Income for the year 1,254,994 13,860

The accompanying notes form an integral part of the financial statements.

The revenue and operating profit relate to continuing operations as no businesses were acquired or disposed of in 2015 or 2014.

On behalf of the board Mr A Director Ms B Director Director Director

Fixed assets Property, plant and equipment 9 1,470,024 84,886Investment properties 10 850,725 3,390,021Investment in subsidiaries 11 35,640 209,200

2,356,389 3,684,107

Current assets Inventories 12 396,209 472,166Trade and other receivables 13 3,187,177 1,464,187Cash and cash equivalents 126,772 17,721

3,710,158 1,954,074

Creditors due within one year Trade and other payables 14 (726,539) (541,830)Borrowings 15 (1,066,950) (2,078,458)Current tax liability (280,351) (64,812)Provisions for other liabilities and charges (188,907) (178,139)

(2,262,747) (2,863,239)

Net current assets 1,447,411 (909,165)

Total assets less current liabilities 3,803,800 2,774,942

Creditors due after one year Borrowings 15 (1,903,810) (2,130,125)

The significant accounting policies adopted by the Company and applied consistently are as follows: (a) General information OmniPro Sample FRS 102 Company Limited is primarily engaged in the provision of construction services to both the private and commercial sectors. From their operations base and depot in Construction Place, Builders Lane, Dunblock, Any County they also sell pre-cast concrete products to private individuals and the construction industry. The company is supplied with the pre-cast concrete products by a wholly owned subsidiary company, which operates independently from a separate location. The company is a limited liability company incorporated and domiciled in Ireland. The company is tax resident in Ireland. This is the first set of financial statements prepared by OmniPro Sample FRS 102 Company Limited in accordance with accounting standards issued by the Financial Reporting Council, including the FRS 102 “The Financial Reporting Standard applicable in the UK and Republic of Ireland” (“FRS 102”). The company transitioned from previously extant Irish and UK GAAP to FRS 102 as at 1 January 2014. An explanation of how transition to FRS 102 has affected the reported financial position and financial performance is given in note 2. The significant accounting policies adopted by the Company and applied consistently in the preparation of these financial statements are set out below. (b) Basis of preparation The Financial Statements are prepared on the going concern basis, under the historical cost convention, as modified by the revaluation of certain tangible fixed assets measured at fair value through profit or loss. The financial statements are prepared in Euro which is the functional currency of the company. (c) Consolidation25 The company and its subsidiaries combined meet the size exemption criteria for a group and the company is therefore exempt from the requirement to prepare consolidated financial statements by virtue of Regulation 7 of the European Communities (Companies: Group Accounts) Regulations, 1992. Consequently, these financial statements deal with the results of the company as a single entity. (d) Currency (i) Functional and presentation currency

Items included in the financial statements of the company are measured using the currency of the primary economic environment in which the company operates ("the functional currency"). The financial statements are presented in euro, which is the company's functional and presentation currency and is denoted by the symbol "€".

(ii) Transactions and balances

Foreign currency transactions are translated into the functional currency using the spot exchange rates at the dates of the transactions. At each period end foreign currency monetary items are translated using the closing rate. Non-monetary items measured at historical cost are translated using the exchange rate at the date of the

25 Applicable to Group companies who do not meet the size criteria to prepare consolidated financial statements

transaction and non-monetary items measured at fair value are measured using the exchange rate when fair value was determined. Foreign exchange gains and losses that relate to borrowings and cash and cash equivalents are presented in the profit and loss account within ‘finance (expense)/income’. All other foreign exchange gains and losses are presented in the profit and loss account within ‘Other operating (losses)/gains’.

(e) Revenue Revenue is recognised to the extent that the company obtains the right to consideration in exchange for its performance. Revenue comprises the fair value of consideration received and receivable exclusive of value added tax and after discounts and rebates. Where the consideration receivable in cash or cash equivalents is deferred, and the arrangement constitutes a financing transaction, the fair value of the consideration is measured as the present value of all future receipts using the imputed rate of interest. Revenue from the sale of goods is recognised when the significant risks and rewards of ownership of the goods have passed to the buyer, usually on dispatch of the goods, the amount of revenue can be measured reliably, it is probable that the economic benefits associated with the transaction will flow to the entity and the costs incurred or to be incurred in respect of the transaction can be measured reliably. Revenue from the provision of services is recognised in the accounting period in which the services are rendered and the outcome of the contract can be estimated reliably. The company uses the percentage of completion method based on the actual service performed as a percentage of the total services to be provided. (f) Interest income Interest income is recognised using the effective interest method. (g) Dividend income Dividend income from subsidiaries is recognised when the Company’s right to receive payment has been established. (h) Dividend distribution Dividend distribution to the company’s shareholders is recognised as a liability in the Company’s financial statements in the period in which the dividends are approved by the company’s shareholders. (i) Government grants Government grants are recognised at their fair value in profit or loss where there is a reasonable assurance that the grant will be received and the Company has complied with all attached conditions. Capital Grants received where the Company has yet to comply with all attached conditions are recognised as a liability (and included in deferred income within trade and other payables) and released to income when all attached conditions have been complied with. Revenue Grants are credited to income so as to match them with the expenditure to which they relate. Government grants received are included in ‘other income’ in profit or loss.

(j) Taxation The company is managed and controlled in the Republic of Ireland and, consequently, is tax resident in Ireland. Tax is recognised in the profit and loss account, except to the extent that it relates to items recognised in other comprehensive income or directly in equity. In this case tax is also recognised in other comprehensive income or directly in equity respectively. (i) Current tax

Current tax is calculated on the profits of the period. Current tax is determined using tax rates (and laws) that have been enacted or substantively enacted by the balance sheet date.

(ii) Deferred tax

Deferred tax arises from timing differences that are differences between taxable profits and total comprehensive income as stated in the financial statements. These timing differences arise from the inclusion of income and expenses in tax assessments in periods different from those in which they are recognised in financial statements. Deferred tax is provided in full on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements. Deferred tax is determined using tax rates (and laws) that have been enacted or substantively enacted by the balance sheet date and are expected to apply when the related deferred income tax asset is realised or the deferred tax liability is settled. Deferred tax assets are recognised to the extent that it is probable that future taxable profits will be available against which the temporary differences can be utilised.

Current or deferred taxation assets and liabilities are not discounted. (k) Property plant and equipment (i) Cost

Property, plant and equipment are recorded at historical cost or deemed cost, less accumulated depreciation and impairment losses. Cost includes prime cost, overheads and interest incurred in financing the construction of tangible fixed assets. Capitalisation of interest ceases when the asset is brought into use. Freehold premises are stated at cost (or deemed cost for freehold premises held at valuation at the date of transition to FRS 102) less accumulated depreciation and accumulated impairment losses The company previously adopted a policy of revaluing freehold premises and they were stated at their revalued amount less any subsequent depreciation and accumulated impairment losses. The company has adopted the transition exemption under FRS 102 paragraph 35.10(d) and has elected to use the previous revaluation as deemed cost. The difference between depreciation based on the deemed cost charged in the profit and loss account and the asset’s original cost is transferred from revaluation reserve to retained earnings. Equipment and fixtures and fittings are stated at cost less accumulated depreciation and accumulated impairment losses.

(ii) Depreciation Depreciation is provided on property, plant and equipment, on a straight-line basis, so as to write off their cost less residual amounts over their estimated economic lives. The estimated economic lives assigned to property, plant and equipment are as follows:

Freehold Premises 2% straight line on cost Motor vehicles 25% straight line on cost Office Equipment, fixtures & fittings 12½% straight line on cost Computer equipment 25%/33⅓% straight line on cost

The company’s policy is to review the remaining economic lives and residual values of property, plant and equipment on an on-going basis and to adjust the depreciation charge to reflect the remaining estimated life and residual value. Fully depreciated property, plant & equipment are retained in the cost of property, plant & equipment and related accumulated depreciation until they are removed from service. In the case of disposals, assets and related depreciation are removed from the financial statements and the net amount, less proceeds from disposal, is charged or credited to the income statement.

(iii) Impairment Assets not carried at fair value are also reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. Value in use is defined as the present value of the future pre-tax and interest cash flows obtainable as a result of the asset’s continued use. The pre-tax and interest cash flows are discounted using a pre-tax discount rate that represents the current market risk free rate and the risks inherent in the asset. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units). If the recoverable amount of the asset (or asset’s cash generating unit) is estimated to be lower than the carrying amount, the carrying amount is reduced to its recoverable amount. An impairment loss is recognised in the profit and loss account, unless the asset has been revalued when the amount is recognised in other comprehensive income to the extent of any previously recognised revaluation. Thereafter any excess is recognised in profit or loss. If an impairment loss is subsequently reverses, the carrying amount of the asset (or asset’s cash generating unit) is increased to the revised estimate of its recoverable amount, but only to the extent that the revised carrying amount does not exceed the carrying amount that would have been determined (net of depreciation) had no impairment loss been recognised in prior periods. A reversal of an impairment loss is recognised in the profit and loss account.

(l) Investment properties The group owns a number of freehold office buildings that are held to earn long term rental income and for capital appreciation. The property is not occupied by any group companies. Investment properties are initially recognised at cost. Investment properties whose fair value can be measured reliably are measured at fair value. Changes in fair value are recognised in the profit and loss account.

(m) Investments in subsidiary undertakings Investments in subsidiary undertakings are shown at historical cost less provision for impairments in value. (n) Leases (i) Finance leases

Leases in which substantially all the risks and rewards of ownership are transferred by the lessor are classified as finance leases. Tangible fixed assets acquired under finance leases are capitalised at the lease’s commencement at the lower of the fair value of the leased property and the present value of the minimum lease payments and are depreciated over the shorter of the lease term and their useful lives. The capital element of the lease obligation is recorded as a liability and the interest element of the finance lease rentals is charged to the profit and loss account on an annuity basis. Each lease payment is apportioned between the liability and finance charges using the effective interest method.

(ii) Operating leases

Leases in which substantially all the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are charged to profit or loss on a straight-line basis over the period of the lease.

(iii) Lease incentives Incentives received to enter into a finance lease reduce the fair value of the asset and are included in the calculation of present value of future minimum lease payments. Incentives received to enter into an operating lease are credited to the profit and loss account, to reduce the lease expense, on a straight-line basis over the period of the lease.

(o) Inventories Inventories comprise consumable items and goods held for resale. Inventories are stated at the lower of cost and net realisable value. Cost is calculated on a first in, first out basis and includes invoice price, import duties and transportation costs. Net realisable value comprises the actual or estimated selling price less all further costs to completion or to be incurred in marketing, selling and distribution. At the end of each reporting period inventories are assessed for impairment. If an item of inventory is impaired, the identified inventory is reduced to its selling price less costs to complete and sell and an impairment charge is recognised in the profit and loss account. Where a reversal of the impairment is recognised the impairment charge is reversed, up to the original impairment loss, and is recognised as a credit in the profit and loss account. (p) Trade receivables Trade receivables are recognised initially at fair value and subsequently less any provision for impairment. A provision for impairment of trade receivables is established when there is objective evidence that the company will not be able to collect all amounts due according to the original terms of receivables. The amount of the provision is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the effective interest rate. All movements in the level of the provision required are recognised in the profit and loss.

(q) Cash and cash equivalents Cash and cash equivalents include cash on hand, demand deposits and other short- term highly liquid investments with original maturities of three months or less. Bank overdrafts are shown within borrowings in current liabilities on the statement of financial position. (r) Trade payables Accounts payable are classified as current liabilities if payment is due within one year or less. If not, they are presented as non-current liabilities. Trade payables are recognised initially at the transaction price and subsequently measured at amortised cost using the effective interest method. (s) Borrowings Borrowings are recognised initially at the transaction price (present value of cash payable to the bank, including transaction costs). Borrowings are subsequently stated at amortised cost. Interest expense is recognised on the basis of the effective interest method and is included in finance costs. Borrowings are classified as current liabilities unless the Company has a right to defer settlement of the liability for at least 12 months after the reporting date. (t) Provisions Provisions are recognised when the company has a present legal or constructive obligation as a result of past events; it is probable that an outflow of resources will be required to settle the obligation; and the amount of the obligation can be estimated reliably. Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small. Provisions are measured at the present value of the expenditures expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the obligation. The increase in the provision due to passage of time is recognised as a finance cost. (u) Contingencies Contingent liabilities, arising as a result of past events, are not recognised when (i) it is not probable that there will be an outflow of resources or that the amount cannot be reliably measured at the reporting date or (ii) when the existence will be confirmed by the occurrence or non-occurrence of uncertain future events not wholly within the company’s control. Contingent liabilities are disclosed in the financial statements unless the probability of an outflow of resources is remote. Contingent assets are not recognised. Contingent assets are disclosed in the financial statements when an inflow of economic benefits is probable. (v) Employee Benefits The company provides a range of benefits to employees, including annual bonus arrangements, paid holiday arrangements and defined contribution pension plans.

(i) Short term benefits Short term benefits, including holiday pay and other similar non-monetary benefits, are recognised as an expense in the period in which the service is received.

(ii) Annual bonus plans

The company recognises a provision and an expense for bonuses where the company has a legal or constructive obligation as a result of past events and a reliable estimate can be made.

(iii) Defined contribution pension plans The Company operates a defined contribution plan. A defined contribution plan is a pension plan under which the company pays fixed contributions into a separate fund. Under defined contribution plans, the company has no legal or constructive obligations to pay further contributions if the fund does not hold sufficient assets to pay all employees the benefits relating to employee service in the current and prior periods. For defined contribution plans, the company pays contributions to privately administered pension plans on a contractual or voluntary basis. The company has no further payment obligations once the contributions have been paid. The contributions are recognised as employee benefit expense when they are due. Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in the future payments is available.

(w) Dividend distribution Dividend distribution to equity shareholders are recognised as a liability in the company's financial statements in the period in which the dividends are approved by the equity shareholders. These amounts are recognised in the statement of changes in equity. (x) Share capital Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new ordinary shares or options are shown in equity as a deduction, net of tax, from the proceeds. (y) Related party transactions The company discloses transactions with related parties which are not wholly owned with the same group. It does not disclose transactions with members of the same group that are wholly owned.

Prior to 1 January 2014 the company prepared its financial statements under previously extant Irish GAAP. From 1 January 2013, the company has elected to present its annual financial statements in accordance with FRS 102 and the Companies Act 1963 to 2013. The comparative figures in respect of the 2014 financial statements have been restated to reflect the company’s adoption of FRS 102 from the date of transition at 1 January 2014. Set out below are the changes in accounting policies which reconcile profit for the financial year ended 31 December 2014 and the total equity as at 1 January 2014 and 31 December 2014 between Irish GAAP as previously reported and FRS 102. In preparing this financial information, the company has applied certain exceptions and exemptions from full retrospective application of FRS 102 as noted below. Exceptions Derecognition of financial assets and liabilities In accordance with FRS 102, as a first-time adopter, the company did not retrospectively recognise financial assets and liabilities previously derecognised under Irish GAAP before the date of transition. Accounting estimates In accordance with FRS 102, as a first-time adopter, the company did not revise estimates on transition to reflect new information subsequent to the original estimates. Exemptions Business combinations The company has elected not to apply Section 19 of FRS 102 retrospectively to business combinations effected before 1 January 2014. Rent free period for operating leases Under previous Irish GAAP operating lease incentives such as rent free periods, were spread over the shorter of the lease period or the period to when the rental was set to a fair market rent. FRS 102 requires that such incentives to be spread over the lease period. The company has taken advantage of the exemption for existing leases at the transition date to continue to recognise these lease incentives on the same basis as previous Irish GAAP. Accordingly the FRS 102 accounting policy has been applied to new operating leases entered into since 1 January 2014. Investments in subsidiaries The company has adopted the carrying value of subsidiary investments under Irish GAAP on the date of transition as their deemed cost rather than carrying out a valuation at the date of transition as permitted by FRS 102.

2. FRS 102 PRINCIPLE ADJUSTMENTS

The reconciliation of the profit and loss prepared in accordance with Irish GAAP and in accordance with FRS 102 for the year ended 31 December 2014 and the reconciliation of the amount of total equity at 31 December 2014, before and after the application FRS 102, is as follows:

- Rent free period for operating leases (b) (32,000) (32,000)

Deferred tax impact of:

- Holiday pay accrual 1,000 7,000 8,000

- Rent free period for operating leases 4,000 0 4,000

- Revaluation of freehold premises (25,000) (25,000)

As reported under FRS 102 13,860 631,136 644,996

(a) Holiday pay accrual Irish GAAP Under Irish GAAP provisions for holiday pay accruals were not recognised and holiday pay was charged to the Profit and Loss account as they were paid. FRS 102 FRS 102 requires short-term employee benefits to be charged to the profit and loss account as the employee service is received. Impact This has resulted in the company recognising a liability for holiday pay of €62,000 on transition to FRS 102. In the year to 31 December 2014 an additional charge of €12,000 was recognised in the profit and loss account and the liability at 31 December 2014 was €74,000. (b) Rent free period for operating leases Irish GAAP Under Irish GAAP operating lease incentives, such as rent free periods were spread over the shorter of the lease period or the period to when the rental was set to a fair market rent. FRS 102 FRS 102 requires that such incentives to be spread over the lease period. The company has taken advantage of the exemption for existing leases at the transition date to continue to recognise these lease incentives on the same basis as previous Irish GAAP. Accordingly the FRS 102 accounting policy has been applied to new operating leases entered into since 1 January 2014. Impact This has resulted in an increased operating lease charge of €32,000 for the year 31 December 2014 with a corresponding increase in the accrued lease liability at 31 December 2014.

(c) Revaluation of tangible assets Under previous Irish GAAP the company had a policy of revaluing freehold premises. On transition to FRS 102 the company has elected to use the previous revaluation of certain premises at 31 December 2013 as the deemed cost for that asset. There is no effect on the balance sheet on transition. In the year ended 31 December 2014 the revaluation for the year ended 31 December 2014 is no longer recognised in Other Comprehensive income. As the revaluation was effected at the end of the financial year there was no change to the depreciation charge for the year ended 31 December 2014. (d) Deferred taxation The company has accounted for deferred taxation on transition as follows: (i) Holiday pay accrual - Deferred tax of €7,000 has been recognised at 12.5% on the liability

recognised on transition at 1 January 2014. In the year ended 31 December 2014 the company has recognised a charge of €1,000 in the profit and loss account in respect of the reduction of the holiday pay accrual.

(ii) Rent free period for operating leases – In the year ended 31 December 2014 the company has

recognised a charge of €4,000 in the profit and loss account in respect of the increased operating lease charge.

(iii) Revaluation of freehold premises – Under previous Irish GAAP the company was not required to

provide for taxation on revaluations. Under FRS 102 deferred taxation is provided on the temporary difference arising from the revaluation. A deferred tax charge of €25,000 arose on transition to FRS 102.

(e) Statement of cash flows Irish GAAP Under Irish GAAP, cash flows were presented separately for operating activities, returns on investment and servicing of finance, taxation, capital expenditure and financial investment, acquisitions and disposals, equity dividends paid and financing. FRS 102 Under FRS 102, cash flows are required to be shown separately for three categories only, namely, operating, investing and financing. Additionally the cash flow statement reconciles to cash and cash equivalents whereas under previous Irish GAAP the cash flow statement reconciled to cash. Cash and cash equivalents are defined in FRS 102 as “cash on hand and demand deposits and short term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value” whereas cash is defined in FRS 1 as “cash in hand and deposits repayable on demand with any qualifying institution, less overdrafts from any qualifying institution repayable on demand”. Impact Cash flows from taxation and returns on investments and servicing of finance shown under Irish GAAP are included as operating activities under FRS 102.

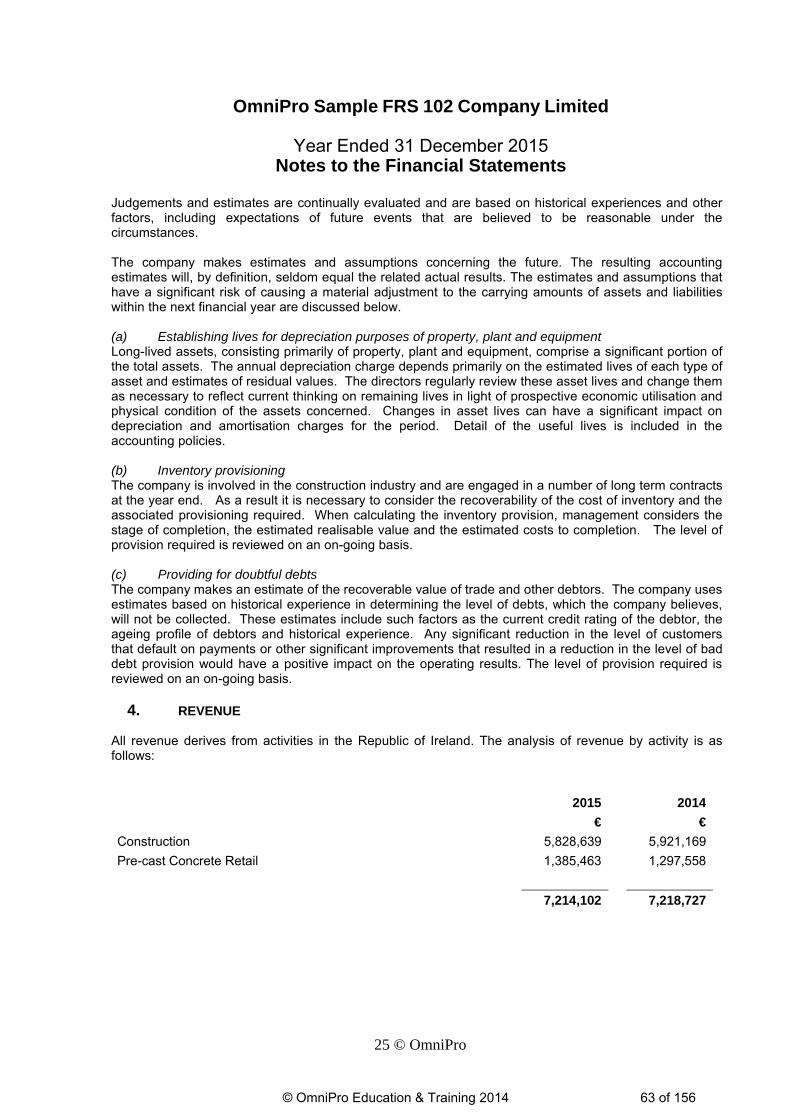

3. CRITICAL ACCOUNTING JUDGEMENTS AND ESTIMATES The preparation of these financial statements requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses.

Judgements and estimates are continually evaluated and are based on historical experiences and other factors, including expectations of future events that are believed to be reasonable under the circumstances. The company makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below. (a) Establishing lives for depreciation purposes of property, plant and equipment Long-lived assets, consisting primarily of property, plant and equipment, comprise a significant portion of the total assets. The annual depreciation charge depends primarily on the estimated lives of each type of asset and estimates of residual values. The directors regularly review these asset lives and change them as necessary to reflect current thinking on remaining lives in light of prospective economic utilisation and physical condition of the assets concerned. Changes in asset lives can have a significant impact on depreciation and amortisation charges for the period. Detail of the useful lives is included in the accounting policies. (b) Inventory provisioning The company is involved in the construction industry and are engaged in a number of long term contracts at the year end. As a result it is necessary to consider the recoverability of the cost of inventory and the associated provisioning required. When calculating the inventory provision, management considers the stage of completion, the estimated realisable value and the estimated costs to completion. The level of provision required is reviewed on an on-going basis. (c) Providing for doubtful debts The company makes an estimate of the recoverable value of trade and other debtors. The company uses estimates based on historical experience in determining the level of debts, which the company believes, will not be collected. These estimates include such factors as the current credit rating of the debtor, the ageing profile of debtors and historical experience. Any significant reduction in the level of customers that default on payments or other significant improvements that resulted in a reduction in the level of bad debt provision would have a positive impact on the operating results. The level of provision required is reviewed on an on-going basis.

4. REVENUE All revenue derives from activities in the Republic of Ireland. The analysis of revenue by activity is as follows:

5. OPERATING COSTS Operating costs are stated after charging:

2015 2014

€ €

Depreciation 149,999 170,037

Directors' remuneration: 212,000 225,600

Auditors' remuneration 13,000 12,500

6. FINANCE INCOME AND COSTS 2015 2014

€ €

On bank loans, overdrafts and other loans wholly repayable within five years

(246,586)

(199,721)

7. INCOME TAX 2015 2014

€ €

(a) Tax expense in the profit and loss:

Current tax expense 294,652 99,722

Deferred tax expense:

Origination and reversal of temporary difference 2,853 (7,096)

Total income tax expense in income statement 297,505 92,626

(b) Reconciliation of tax charge The tax assessed for the period is higher than the standard rate of corporation tax in Ireland for the year end 31 December 2015 of 12.5% (2014: 12.5%). The differences are explained below.

2015 2014

€ €

Profit before tax 1,552,449 106,486

Tax calculated at Irish tax rates of 12.5% (2014: 12.5%) 194,062 13,311

Effects of:

Non deductible expenses 22,088 3,137

Capital allowances less than depreciation 87,914 7,046

Utilisation of losses forward (626,128)

Corporation tax surcharge 30,948 28,881

Capital gain 545,408 27,181

Adjustment in respect of prior periods 40,360 20,166

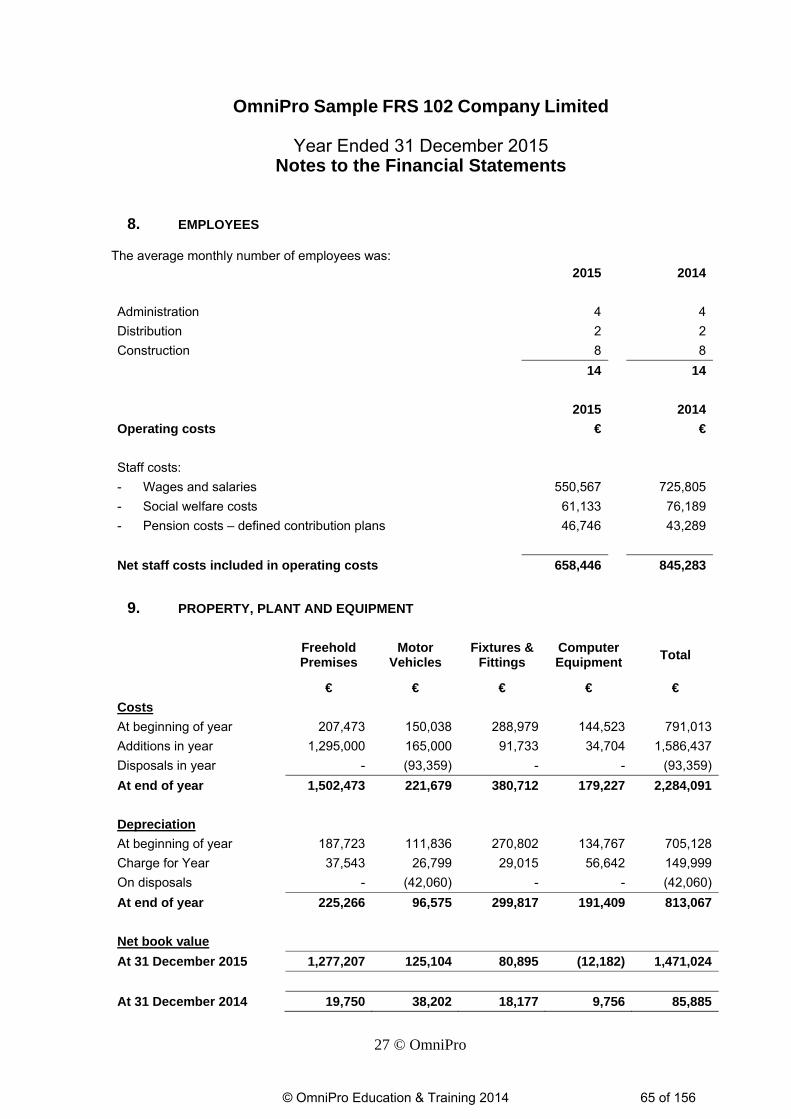

The company's policy is to review the remaining economic lives and residual values of property, plant and equipment on an on-going basis and to adjust the depreciation charge to reflect the remaining estimated lives and residual value. Included above are the following amounts in respect of Motor Vehicles held under finance leases:

The capital and reserves and profit of the subsidiary was as follows:

2015 2014

€ €

Profit 212,387 172,834

Capital and reserves 854,346 641,959

12. INVENTORIES

2015 2014

€ €

Stock of raw material 33,724 42,108

Stock of precast concrete products 71,769 84,968

Work in progress 290,716 345,090

396,209 472,166

The net replacement cost of stocks is not expected to be materially different from that shown above. Inventories are stated after provisions for impairment of €32,000 (2014: €28,000).

The fair values of trade and other receivables approximate to their carrying amounts. Trade debtors are stated after provisions for impairments of €105,000 (2014: €113,000).

Amounts owed by group companies are unsecured, interest free, have no fixed date of repayment and are repayable on demand.

14. TRADE AND OTHER PAYABLES 2015 2014

€ €

Trade creditors 669,675 475,652

Other creditors and accruals 56,864 66,178

726,539 541,830

15. BORROWINGS 2015 2014

€ €

Current

Bank borrowings 1,066,950 2,078,458

Non-current

Bank borrowings 1,903,810 2,130,125

The bank facilities are secured by a debenture incorporating fixed and floating charges over the assets of the company and personal guarantees from the Directors

The facilities expiring within one year are annual facilities subject to review at various dates during 2015/2016.

1,000,000 ordinary shares of 1.27 each 1,269,738 1,269,738

Alloted, called up and fully paid equity

145,000 ordinary shares of 1.27 each 184,112 184,112 All issued shares are fully paid and have equal rights to vote at general meetings and receive dividends.

17. RESERVES Equity Share

Revaluation Retained Total

Capital Reserve Earnings Equity

€ € € €

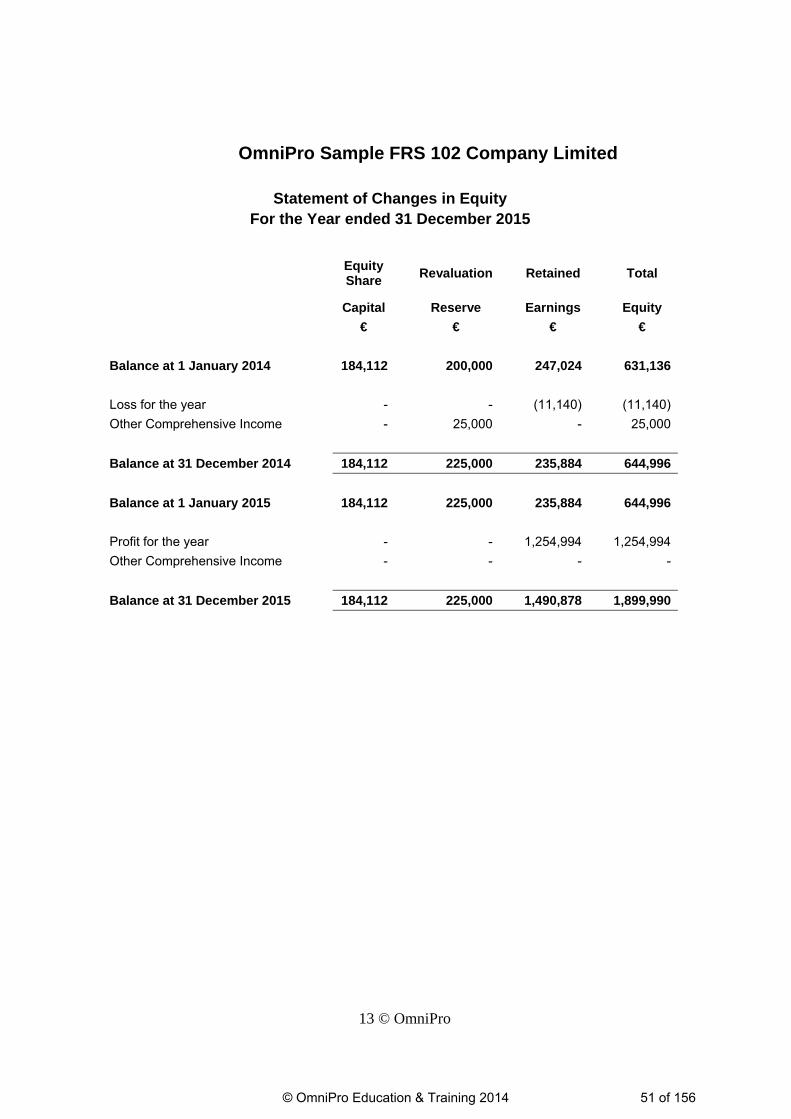

Balance at 1 January 2014 184,112 200,000 247,024 631,136

Loss for the year (11,140) (11,140)

Other Comprehensive Income 25,000 25,000

Balance at 31 December 2014 184,112 225,000 235,884 644,996

Balance at 1 January 2015 184,112 225,000 235,884 644,996

Profit for the year 1,254,994 1,254,994

Other Comprehensive Income

Balance at 31 December 2015 184,112 225,000 1,490,878 1,899,990

18. CONTINGENCIES A legal action is pending against the company for alleged unfair dismissal. The directors under advisement from their legal team expect that the claim will be successfully defended. Should the company be unsuccessful in the action the maximum estimated settlement is not expected to exceed €10,000. It is not anticipated that any material liabilities will arise from the contingent liabilities other than those provided for.

19. CAPITAL COMMITMENTS There were no capital commitments at the year ended 31 December 2015.

20. DIRECTORS INTERESTS The director’s interests in the company at the beginning and end of the year were as follows;

Mr A Director Ms B Director€1 ordinary

shares €1 ordinary

shares Total

At the beginning of the year 72,500 72,500 145,000

At the end of the year 72,500 72,500 145,000

21. PENSIONS

2015 2014

€ €

Pension costs 46,746 43,289 The company operates an externally funded defined contribution scheme that covers substantially all the employees of the company. The assets of the scheme are vested in independent trustees for the sole benefit of these employees.

22. RELATED PARTY TRANSACTIONS The company regards OmniPro plc, a company incorporated in Ireland, as the ultimate parent company. The following transactions were carried out with related parties:

2015 2014

€ €

Sales of goods and services

OmniPro plc 119,632

Purchase of goods and services

OmniPro plc 15,987

Year end balances arising from sale/purchase of goods/services

Receivable from related parties

OmniPro plc 1,721,862 191,852

Key management includes the Board of Directors (executive and non-executive), all members of the Company Management and the Company Secretary. The compensation paid or payable to key management for employee services is shown below: 2015

€ 2014

€Key management compensation Salaries and other short-term employee benefits 268,000 257,000Post-employment benefits 19,000 12,000 287,000 269,000 Loans to directors Mr A

Director Ms B

Director Opening balance 14,332 18,320Repayment to directors 5,395 14,605Advances from directors 10,000 10,000 18,937 13,715 Maximum amount outstanding to directors during the year26 No provision has been required in 2015 and 2014 for the loans made to key management personnel and associates.

26 Disclosure of maximum amount only required if debit balance at the year end

23. APB ETHICAL STANDARDS – PROVISIONS AVAILABLE TO SMALL ENTITIES As a small entity under the provisions of the APB in relation to Ethical Standards we engage our auditor to provide basic tax compliance and bookkeeping and accounts preparation.

24. APPROVAL OF THE FINANCIAL STATEMENTS The directors approved the financial statements on .

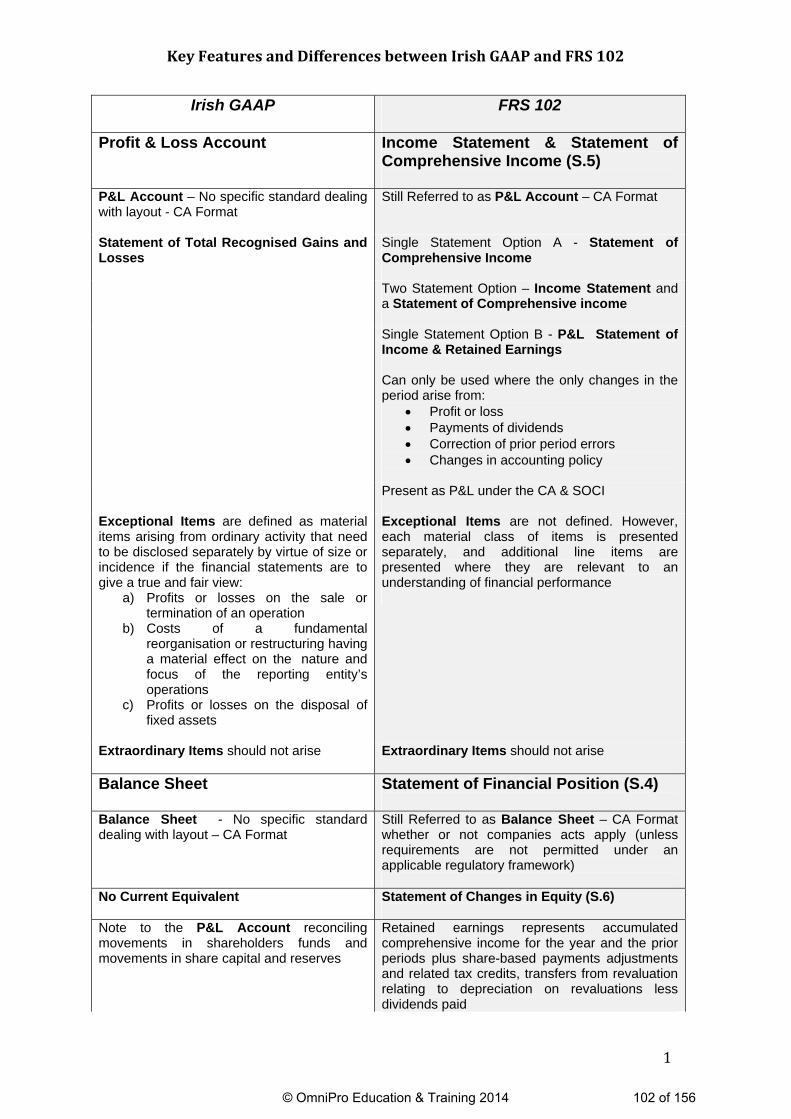

Profit & Loss Account Income Statement & Statement of Comprehensive Income (S.5)

P&L Account – No specific standard dealing with layout - CA Format

Still Referred to as P&L Account – CA Format

Statement of Total Recognised Gains and Losses

Single Statement Option A - Statement of Comprehensive Income

Two Statement Option – Income Statement and a Statement of Comprehensive income

Single Statement Option B - P&L Statement of Income & Retained Earnings Can only be used where the only changes in the period arise from:

Profit or loss Payments of dividends Correction of prior period errors Changes in accounting policy

Present as P&L under the CA & SOCI

Exceptional Items are defined as material items arising from ordinary activity that need to be disclosed separately by virtue of size or incidence if the financial statements are to give a true and fair view:

a) Profits or losses on the sale or termination of an operation

b) Costs of a fundamental reorganisation or restructuring having a material effect on the nature and focus of the reporting entity’s operations

c) Profits or losses on the disposal of fixed assets

Exceptional Items are not defined. However, each material class of items is presented separately, and additional line items are presented where they are relevant to an understanding of financial performance

Extraordinary Items should not arise

Extraordinary Items should not arise

Balance Sheet Statement of Financial Position (S.4)

Balance Sheet - No specific standard dealing with layout – CA Format

Still Referred to as Balance Sheet – CA Format whether or not companies acts apply (unless requirements are not permitted under an applicable regulatory framework)

No Current Equivalent Statement of Changes in Equity (S.6)

Note to the P&L Account reconciling movements in shareholders funds and movements in share capital and reserves

Retained earnings represents accumulated comprehensive income for the year and the prior periods plus share-based payments adjustments and related tax credits, transfers from revaluation relating to depreciation on revaluations less dividends paid

Option to use Statement of Income & Retained Earnings if the only changes are a result of profit or loss, payment of dividends, correction of material prior period errors or changes in accounting policy

Cashflow Statement Statement of Cashflows (S.7)

Exemptions – small entities and subsidiary undertakings where 90% or more of voting rights are controlled within the group and consolidated financial statements publically available

Exemption - Entity included in publically available consolidated financial statements that give a true and fair view. No small entity exemption

9 Headings – Operating Activities, Dividends from Joint Ventures and Associates, Returns on investment and servicing of finance, Taxation, Capital Expenditure and financial investments, Acquisitions and disposals, equity dividends paid, management of liquid resources, financing

3 Headings – Net Cash from Operating Activities, Cashflow from Investing Activities, Cashflow from Financing Activities

Operating Activities – cash receipts from sale of goods and rendering of services, royalties, fees, commissions and other revenue, cash payments to suppliers for goods and services, cash payments to and on behalf of employees, refunds of income tax

Investing activities – Cash payments to acquire and cash receipts in relation to the sale of PPE, intangible assets and other long term assets, cash payments or receipts in relation to acquisition or disposal of equity or debt instruments, cash advances and loans to and from other parties

Financing Activities – cash proceeds from issuing shares or other equity instruments, cash payments to redeem the entity’s shares, cash repayments of amounts borrowed, cash payments for the reduction of outstanding liabilities relating to a finance lease, cash proceeds from issuing debentures, loans, notes, bonds, mortgages or other short term or long term borrowings

Note reconciling the movement of cash in the period with the movement in net debt required

Accounting policies adopted should result in information that is: (a) relevant to the economic decision-making needs of users (b) reliable, in that the financial statements:

i. represent faithfully the financial position, financial performance and cash

ii. flows of the entity iii. reflect the economic substance of

transactions, other events and conditions iv. and not merely the legal form v. are neutral, i.e. free from bias vi. are prudent vii. are complete in all material respects

Changes in accounting estimates are not treated as prior period adjustments

Changes in accounting estimates are not treated as prior period adjustments

In exceptional circumstances if the financial statements in prior periods have been issued with errors that are of such significance as to destroy the “true and fair” view and hence the validity of the financial statements (fundamental errors) prior periods should be accounted for retrospectively (prior period adjustment adjust opening reserves and comparative figure) with all other errors being accounted for prospectively (adjusted in the current period)

All material prior period errors are adjusted retrospectively (prior period adjustment) unless it is not possible to quantify the effect of the error

Notes to the Financial Statements

Notes to the Financial Statements (S.8)

The following disclosures are included, as a minimum, within the notes to the financial statements: whether the financial statements

have been prepared in accordance with applicable accounting standards

a description of each material accounting policy

a description of each material accounting estimate, including the estimation techniques

additional information that is necessary for financial statements to give a true and fair view

The following disclosures are included, as a minimum, within the notes to the financial statements: a statement of compliance with FRS

102 Reconciliation of equity reported

under previous Irish GAAP to equity under FRS 102

Reconciliation of the profit/loss reported under previous Irish GAAP for the latest period to the profit/loss under FRS 102

First-time adoption requires full retrospective application of FRS 102 effective at the reporting date for an entity’s first new FRS 102 financial statements. There are five mandatory exceptions, 17 optional exemptions in section 35 of FRS 102, and one general exemption on the grounds of impracticability regarding retrospective application

information about judgements that management has made in applying the accounting policies and that have the most significant effect on the amounts disclosed in the financial statements

key sources of estimation uncertainty; explanatory notes for items presented

in the financial statement information not presented in the

primary statements

Turnover

Revenue (S.23)

Turnover is the revenue resulting from exchange transactions under which a seller supplies to customers the goods or services that it is in the business to provide – that is, as part of its operating activities

‘Turnover’ is defined as the amounts derived from the provision of goods and services falling within the entity’s ordinary activities, after deduction of:

i. trade discounts ii. value added tax iii. any other taxes based on the amounts so

derived

‘Revenue’ is the gross inflow of economic benefits during the period arising in the course of the ordinary activities of an entity where those inflows result in increases in equity, other than increases relating to contributions from equity participants. It is referred to by a variety of names, including sales, fees, interest, dividends, royalties and rent

Turnover is recognised when an entity obtains the right to consideration in exchange for its performance

Revenue recognition criteria include the probability that the economic benefits associated with the transaction will flow to the entity and that the revenue and costs can be measured reliably

Government Grants

Governments Grants (S.24)

Government grants are assistance by government in the form of cash or transfers of assets to an enterprise in return for past or future compliance with certain conditions relating to the operating activities of the entity

Similar to old Irish GAAP, except that grants exclude forms of assistance that cannot reasonably be valued or distinguished from normal trading of the entity

Grant income is not recognised unless there is reasonable assurance that the entity will comply with the conditions of the grant and the grant will be received

FRS 102 prohibits recognition of grant income unless there is reasonable assurance that the entity will comply with the conditions of the grant and the grant will be received

Government grants are recognised as income over the periods necessary to match them with the related costs that they are intended to compensate, on a systematic basis

Where recognition criteria are met, entities have a choice between the performance and the accruals model for recognition

Functional currency is defined as the currency of the primary economic environment in which the entity operates

Same as Irish GAAP

Presentation currency is defined as the currency in which the financial statements are presented

Retirement Benefits

Employee Benefits (S.28)

Irish GAAP is limited to retirement benefits only

FRS 102 is wider in scope than Irish GAAP. Employee benefits are all forms of consideration given by an entity in exchange for services rendered by its employees. These benefits include:

short-term employee benefits (such as wages, salaries, profit sharing and bonuses)

termination benefits (such as severance and redundancy pay)

post-employment benefits (such as retirement benefit plans)

other long-term employee benefits (such as long-term service leave and jubilee benefits)

The principles of FRS 12, ‘Provisions, contingent liabilities and contingent assets’, have been relevant to the accounting for short-term employee benefits

Where an employee has rendered services, an expense is recognised for the cost of the undiscounted amount of the short-term employee benefits expected to be paid

Retirement benefits are provided to employees either through defined contribution schemes or defined benefit schemes

Same as Irish GAAP

Corporation Tax

Income Tax (S.29)

Current tax is the amount of tax estimated to be payable or recoverable in respect of the taxable profit or loss for the period, along with adjustments to estimates in respect of previous periods

Same as Irish GAAP

Current tax is measured at the amounts expected to be paid (or recovered) using the tax rates and laws that have been enacted or substantively enacted by the balance sheet date

Recognised on a timing differences basis – differences between an entity’s taxable profits and its results as stated in the financial statements

Recognised on asset revaluations and on assets and liabilities in a business combination with the exception of goodwill

Deferred tax assets are recognised to the extent that they are recoverable – Is it more likely than not that there will be taxable profits from which future reversal of timing differences can be deducted:

Entered into a binding agreement to sell the revalued assets

Recognised the gains and losses expected to arise on sales

Deferred tax is recognised on timing differences arising on the revaluation of an asset including non-monetary asset revaluations through other comprehensive income

Can be discounted

Cannot be discounted

Deferred tax is measured using tax rates that have been enacted or substantively enacted at the balance sheet date and that are expected to apply in the periods in which the timing differences are expected to reverse

Deferred tax is measured using tax rates that have been enacted or substantively enacted at the balance sheet date and that are expected to apply in the periods in which the timing differences are expected to reverse

Deferred tax on a revalued non-depreciable asset (for instance, land) is measured using the tax rates and allowances that apply on sale of the asset

Deferred tax on an investment property held at fair value is measured using the tax rates and allowances that apply on sale of the asset, unless the property is held in a business model where substantially all of the property’s economic benefits will be consumed over time

Tangible Fixed Assets

Property Plant & Equipment (S.17)

Cost or valuation model may be adopted

Cost or valuation model may be adopted

More detailed guidance on valuation basis and methods – every 5 years with interim revaluation in year 3 as required

Revaluations with sufficient regularity to ensure that the carrying amount does not differ materially from the fair value

Residual value based solely on initial residual value at the date of acquisition or the date of revaluation and do not take into account expected future price changes

Residual value allows account to be taken of inflation arising after the acquisition of the asset and up to the current reporting date or balance sheet date. (Potential impact on Depreciation)

Depreciable amount - the difference between the cost and the initial residual value

Depreciable amount - the difference between the cost and the residual value

Depreciation – allocation of depreciable amount on a systematic basis over it’s remaining useful life reflecting the consumption of economic benefit

Properties surplus to an entities requirements – Open Market Value less selling costs

Tangible fixed assets other than properties – Open Market Value (or Depreciated Replacement Cost where market value not obtainable)

Plant & Equipment – market value determined by appraisal

If no market-based evidence of fair value because of specialised nature of the item, which is rarely sold, except as part of a continuing business Depreciated Replacement Cost may be estimated

More detail in relation to subsequent expenditure – enhancement of economic benefit, related to a component that was separately depreciated, related to a major inspection or overhaul

Day-to-day servicing recognised in the profit and loss in the period incurred

Revaluation gains recognised in STRGL unless reversing previous revaluation losses.

Revaluation gains recognised in other comprehensive income and accumulated in equity. Recognised in P&L to extent that it is reversing decrease of assets previously recognised in P&L

A review for impairment of a fixed asset or goodwill is carried out if events or changes in circumstances indicate that the carrying amount of the fixed asset or goodwill may not be recoverable. There is no requirement for an impairment review if there are no indicators

Entities assess if there are any impairment indicators at each reporting date. If there is an indicator, an impairment test is required.

Investment Property

Investment Property (S.16)

Included in balance sheet at open market value

Carried at fair value

Cost model not permitted If carried at cost on the basis that it cannot be measured without undue cost or effort, carried at cost within PPE

Gains and losses are recognised in STRGL Gains and losses are recognised in the P&L

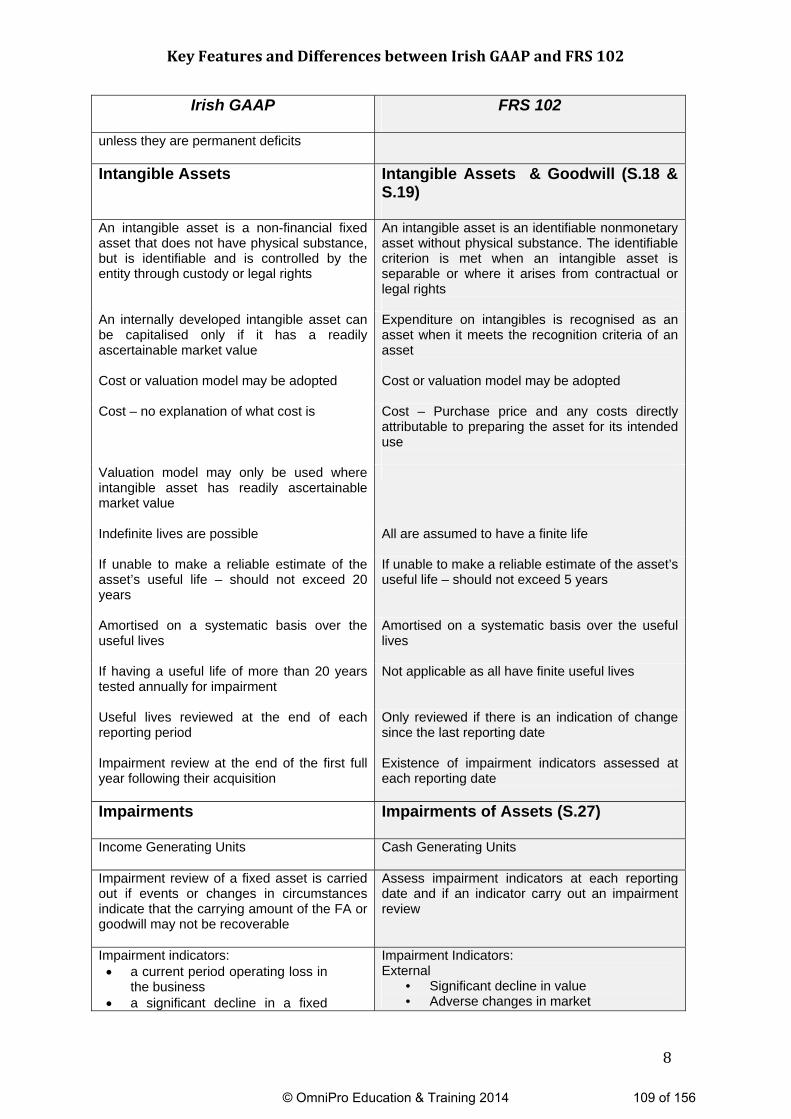

unless they are permanent deficits Intangible Assets

Intangible Assets & Goodwill (S.18 & S.19)

An intangible asset is a non-financial fixed asset that does not have physical substance, but is identifiable and is controlled by the entity through custody or legal rights

An intangible asset is an identifiable nonmonetary asset without physical substance. The identifiable criterion is met when an intangible asset is separable or where it arises from contractual or legal rights

An internally developed intangible asset can be capitalised only if it has a readily ascertainable market value

Expenditure on intangibles is recognised as an asset when it meets the recognition criteria of an asset

Cost or valuation model may be adopted

Cost or valuation model may be adopted

Cost – no explanation of what cost is Cost – Purchase price and any costs directly attributable to preparing the asset for its intended use

Valuation model may only be used where intangible asset has readily ascertainable market value