A PRACTICAL GUIDE TO TRADE POLICY ANALYSIS A Case Study on Pakistan Institute of Business Administration, Karachi University Road, Karach-75270 Pakistan Email address: [email protected]Aadil Nakhoda November 2016

Trade over GDP measure ...................................................................................................................................... 4

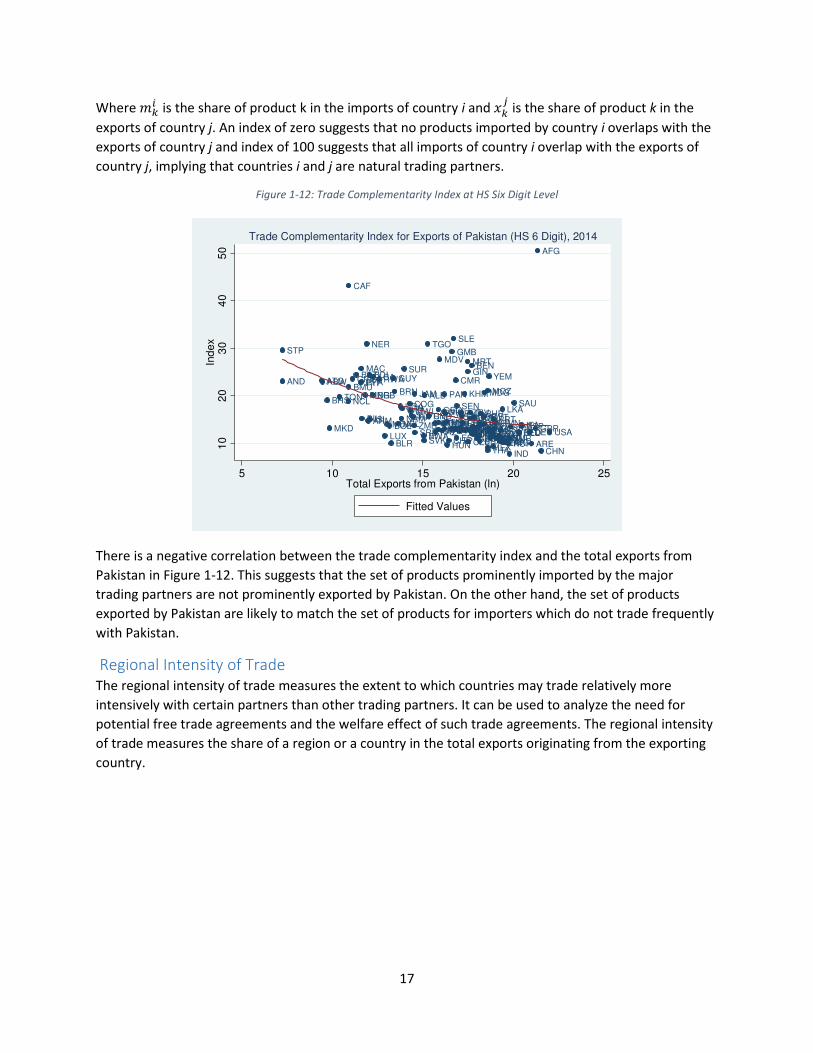

Trade Complementarity Index ............................................................................................................................. 16

Regional Intensity of Trade ...................................................................................................................................... 17

Other Important Concepts....................................................................................................................................... 19

Theoretical Model ............................................................................................................................................... 31

Downloading the Data ........................................................................................................................................ 34

Table B-2: Six Digit HS Product Codes Corresponding to Details of Household Expenditure to Determine

Income Effect .............................................................................................................................................. 51

Figures:

Figure 1-1: Exports, Imports and Trade Openness of Pakistan ..................................................................... 4

Figure 1-2: Percentage Change in Openness and GDP per Capita, 2004-2014 ............................................. 5

Figure 1-3: Exports, Imports and Trade Openness of Pakistan, South Asian Countries and World as a

Percentage of GDP ........................................................................................................................................ 6

Figure 1-4: Percentage of Total Exports from Pakistan to its Top Ten Export Destinations in 2014 ............ 7

Figure 1-5: Percentage of Total Exports from Pakistan in Top Ten HS Sections in 2014 .............................. 8

Figure 1-6: Total Exports from Pakistan and Global Imports (By Destination) ............................................. 9

Figure 1-7: Geographical Orientation of Exports from Pakistan in 2014 ...................................................... 9

Figure 1-8: Product Orientation of Exports from Pakistan in 2014 at HS Six Digit-Level (Textile Products vs

Product Orientation of Exports from Pakistan at HS Six Digit-Level

1

23

4

5

67

8

9 1011

12

13

14

1516

17

18

19 20

21

22

05

10

15

CA

GR

in Im

port

s 2

004

-20

14

(%

)

-10 -5 0 5% Share in Total Exports (ln), 2014

Fitted Values

By HS Section

Product Orientation of Exports from Pakistan

11

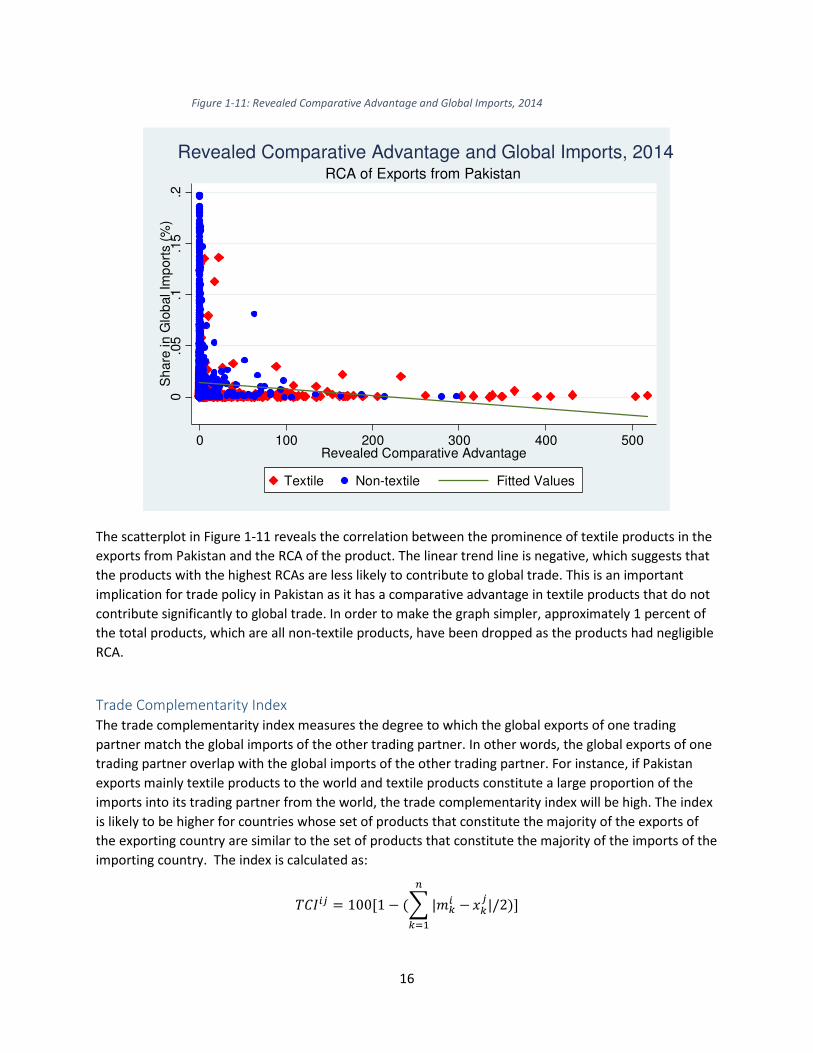

The product orientation of exports from Pakistan is plotted in Figure 1-8, comparing textile to non-

textile products5. The regression line is flat, which suggests that there is no relationship between import

growth between 2004 and 2014 and the share of products in the total exports from Pakistan in 2014.

The growth rates are calculated for products that report positive exports in 2004 and 2014, while the

percentage share of exports is calculated for products that report positive exports in 2014. As expected,

majority of the products with larger share of total exports are textile products. However, when the

relationship is studied at the sectoral-level, the results in Figure 1-9 suggest a positive relationship

between the share of sectors in total exports from Pakistan and the growth in total imports between

2004 and 2014. Mineral products, vegetable products and precious metals reported the highest growth

rates in their trading values. These growth rates were likely driven by their price-levels as several

commodities reached their historical peak between 2004 and 2014.

Intra-industry Trade

The United States not only exports cars to Germany but also imports car parts from Germany. This is an

example of intra-industry trade. A large proportion of global trade takes place within the same industry,

when two countries may trade in the same product in both directions. Intra-industry trade is more likely

between countries that produce as well as consume a greater number of varieties, such as countries

with higher levels of GDP and GDP per capita. In addition, intra-industry trade is more likely between

trading partners that trade more frequently.

In order to determine the degree of intra-industry trade, the total value of products traded in both

directions (the sum of imports and exports of products that are both exported as well imported by the

two trading partners) is divided by the sum of total exports and imports between the two countries. This

formula indicates the trade overlap between two countries as it determines the ratio of bilateral trade

that flows in both directions to total bilateral trade. For instance, if Pakistan exports $100 million of

cotton yarn and imports $ 100 million of cotton yarn from China as well as imports $ 200 million of

mobile phones from China but does not export any mobile phones to China, the trade overlap will be (�������)����������� = 0.5. The numerator is the sum of products that are exported to China as well as imported

into Pakistan (two-way trade) and the denominator is the sum of total exports and imports between

Pakistan and China. The products are considered at HS six digit-level.

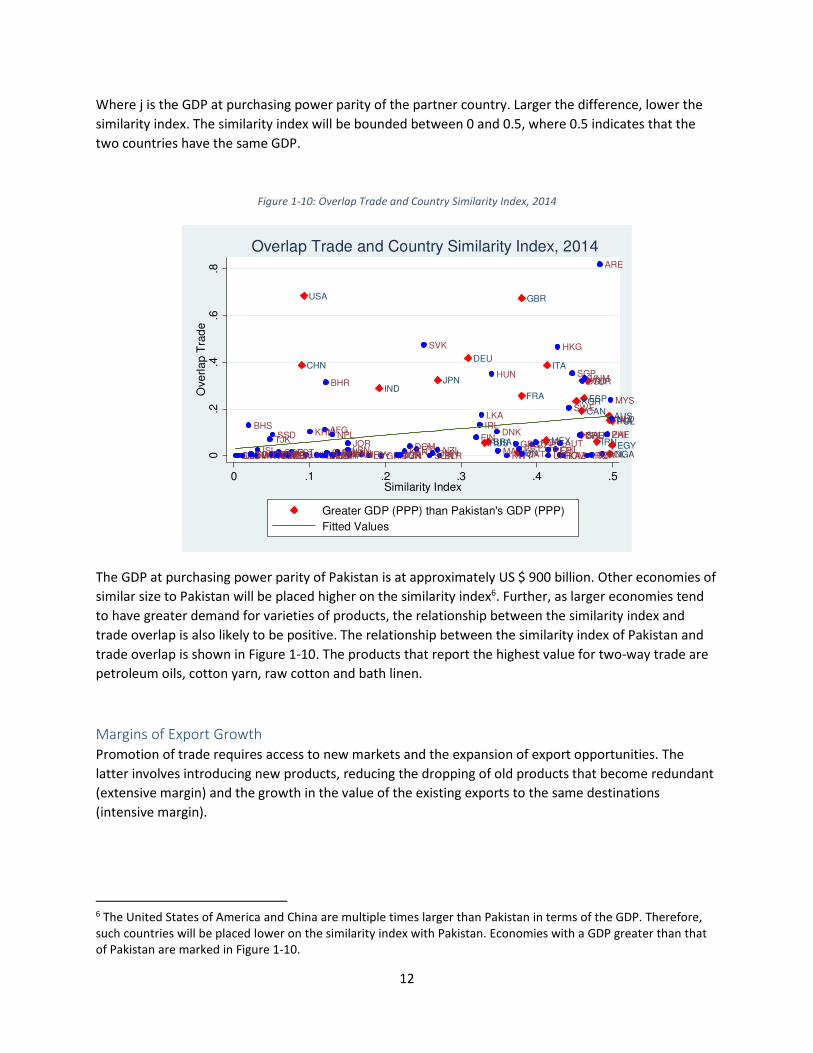

The similarity index, which is calculated as the lack of difference in the GDP between the reporting

country and the partner country, is likely to play an important role in influencing the overlapping trade

between two countries. The similarity index can be written as:

� = 1 − ������������ + �����

�− ���������� + �����

�

5 Section numbers and short title in brackets: 1 (Live Animals), 2 (Vegetable Products), 3 (Animal Fats), 4 (Prepared

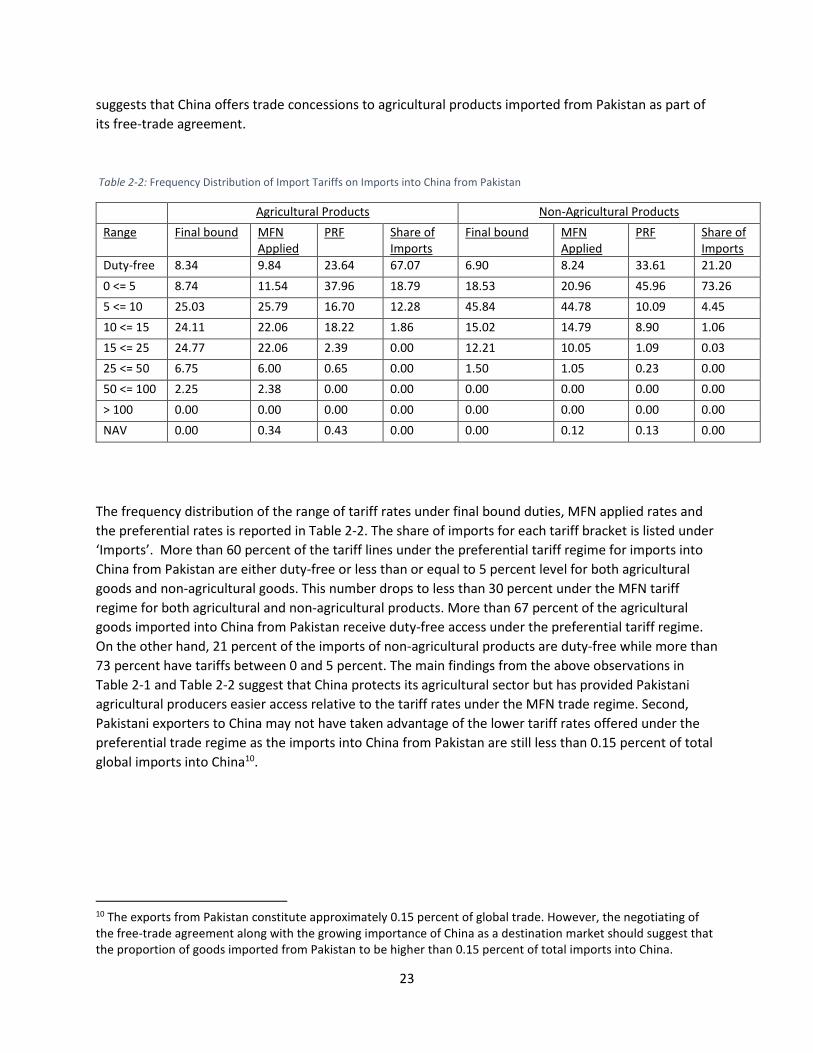

The section-wise breakup of final bound duties, MFN applied rates and preferential rates on imports

into China from Pakistan are reported in Table 2-3. The ‘duty-free share’ is the percentage of tariff lines

25

that are provided duty-free access under the respective trade regime11. The share of imports is

calculated as the percentage share of total imports into China from Pakistan in each section. The duty-

free share of imports indicates the percentage of imports that are imported into China from Pakistan

duty-free under the preferential trade regime12. China provides significant benefits to Pakistani

exporters as the share of duty-free tariffs under the preferential tariff regime is higher than the share of

duty-free tariffs under the MFN regime for majority of the HS sections.

11 The number of products reported under MFN tariffs differ from the number of products reported under PRF.

Therefore, this may give rise to the discrepancy between the percentages of tariff lines that are duty-free under

the respective trade regime. 12 More than 90 percent of the imports into China from Pakistan in mineral products, wood, and base metals is

already duty-free under the MFN applied tariff regime.

26

Chapter 3 : Analyzing Bilateral Trade Using the Gravity Equation

Gravity Equation:

The size of the bilateral flow between two countries can be estimated by the “gravity equation”.

Analogous to the Newtonian law of gravity, countries are likely to trade in proportion to their sizes and

proximity to each other. The simple gravity equation can be formulized in the following terms13:

�(� ��(4�∅(�

Where �(� is the total exports from i to j, �( comprises of exporter characteristics, 4� comprises of

importer characteristics and ∅(� represents the degree of access of exporter i into the market of

importer j.

Source:

The bilateral export flow from Pakistan to the respective trading partners is borrowed from UN

COMTRADE. The total number of export destinations with positive flows ranged from 183 in 2009 to 190

in 2014. The time period considered is from 2004 to 2014. Pakistan signed free trade agreements with

multiple trading partners as well as witnessed a doubling of its total exports during this time period. The

GDP per capita at PPP (current international dollars) and GDP at PPP (current international dollars) for

the importers are borrowed from World Development Indicators. Distance between Pakistan and the

trading partner, the dummy variables on border with Pakistan, common official language, colonizer,

common colonizer and whether the importing country is landlocked is borrowed from CEPII. Pakistan

has signed trade agreements with Sri Lanka (2005), other SAFTA countries (2006), China (2007) and

Malaysia (2008)14.

Empirical Equation:

The gravity equation can be represented by taking the natural logarithms of the variables. The exports

can be estimated using the following logarithmic equation:

67�(� 67� � 67�( � 674� � 67∅(�

The monetary value of exports, GDP of the respective countries and distance can be converted to

natural logarithmic values. However, some of the variables included are taken as dummy variables, such

as border, common official language, colonizer, common colonizer, and regional trade agreements.

These variables are included in the binary form (0 or 1). The aforementioned dummy variables tend to

lower the search costs between businesses across countries as presence in countries sharing borders,

having historical linkages and engaging in trade agreements are likely to lower their costs of business.

The regression analysis below estimates the exports from Pakistan to its trading partners based on

independent variables such as GDP of the importing country, GDP per capita of the importing country,

whether the importing county is land locked (dummy variable) and bilateral variables, such as distance,

13 Several additions to the simple gravity model have been introduced. One such addition adjusts the trade costs

between two countries using land and border characteristics such as whether countries are either landlocked or an

island or whether the two countries share a contiguous border, a common language or colonial linkages. 14 SAFTA countries include Afghanistan (acceded in 2011), Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan

and Sri Lanka. The information on RTAs is available at World Trade Organization’s http://rtais.wto.org/

27

common border, common official language, trading partner as colonizer, common colonizer and the

enforcing of a regional trade agreement. Except for distance, all bilateral variables are binary dummy

variables with a value of either 1 if true or 0 if false. The analysis is conducted using simple ordinary least

squares estimation as well as Tobit and Poisson estimations.

There are several countries that do not trade with each other in a given year. The bilateral exports from

Pakistan to the trading partner will not be reported for such instances. The natural logarithmic value for

such either missing values or zeros is undefined. The values can be dropped if zeros are randomly

distributed and that the presence of zero trade flow is not informative. However, trade theory suggests

that there is substantial costs involved to participate in international trading activities and that zero

trade can indicate either or all of the following: prohibitive transportation costs, low returns to

investments in costs related to trade or relatively small size of the trading partner. Therefore, the

observation of zero trade flow is informative and the value should be included in the estimations. The

Tobit and Poisson estimations are introduced in order to account for the zero values.

The Tobit estimation is a standard method to estimate equations in which the dependent variable is

likely to consist of a larger number of zeros. As Tobit model requires some observations to be censored,

it is a plausible assumption for measuring trade flow for countries in which data may not be accurate. If

the data is accurate, the Tobit estimation may however eliminate crucial information necessary to

determine the trading patterns. The Poisson estimation avoids dropping zeros and is used to model

count data. The Poisson distribution involves a skewed, discrete distribution that includes non-negative

numbers only. The Poisson estimator determines the probability that trade occurs between the trading

partners.

The OLS is estimated using export values where zero trade values are treated as missing values after log

transformation15. However, all trade values (including zeros) are scaled by adding one before the log

transformation for the Tobit estimations. The log of trade values between countries that do not report

any trade are treated as zero in the Tobit estimations and the estimation is left-censored. As the Poisson

estimation is a count model for the number of times an event occurs, the zero trade values are included

in the estimations.

15 Approximately 6.5 percent of the observations reported for the export value are zero trade values.

28

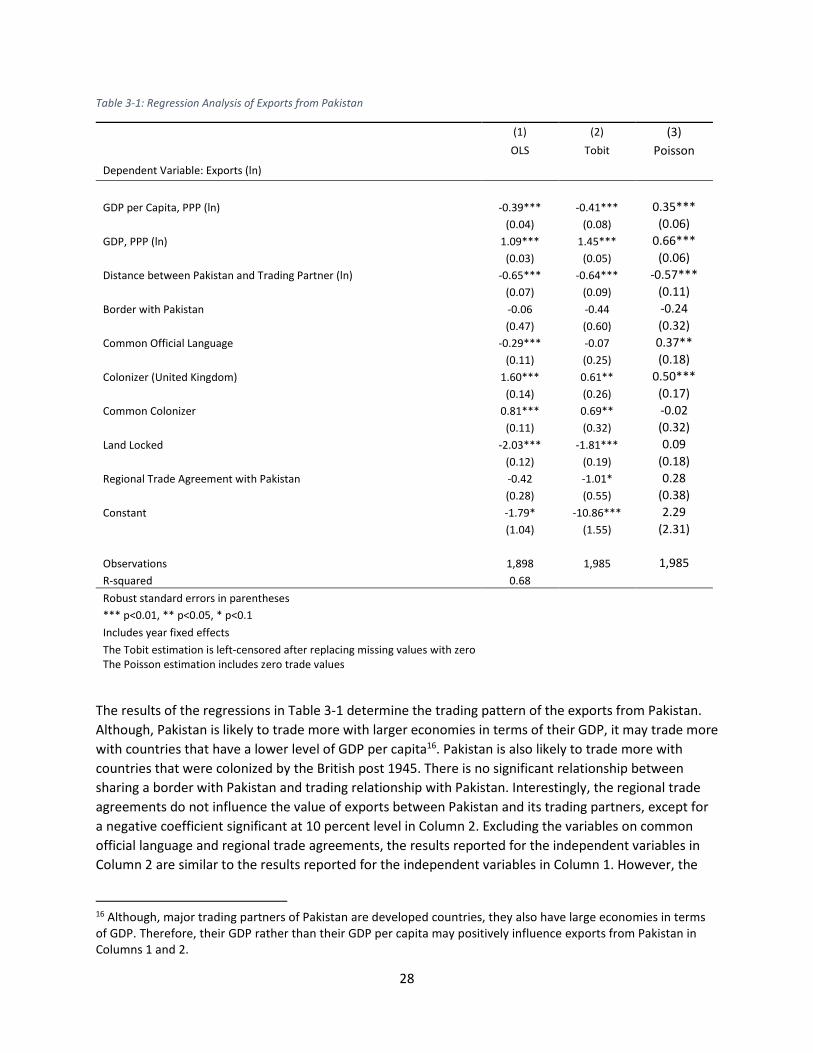

Table 3-1: Regression Analysis of Exports from Pakistan

(1) (2) (3)

OLS Tobit Poisson

Dependent Variable: Exports (ln)

GDP per Capita, PPP (ln) -0.39*** -0.41*** 0.35***

(0.04) (0.08) (0.06)

GDP, PPP (ln) 1.09*** 1.45*** 0.66***

(0.03) (0.05) (0.06)

Distance between Pakistan and Trading Partner (ln) -0.65*** -0.64*** -0.57***

(0.07) (0.09) (0.11)

Border with Pakistan -0.06 -0.44 -0.24

(0.47) (0.60) (0.32)

Common Official Language -0.29*** -0.07 0.37**

(0.11) (0.25) (0.18)

Colonizer (United Kingdom) 1.60*** 0.61** 0.50***

(0.14) (0.26) (0.17)

Common Colonizer 0.81*** 0.69** -0.02

(0.11) (0.32) (0.32)

Land Locked -2.03*** -1.81*** 0.09

(0.12) (0.19) (0.18)

Regional Trade Agreement with Pakistan -0.42 -1.01* 0.28

(0.28) (0.55) (0.38)

Constant -1.79* -10.86*** 2.29

(1.04) (1.55) (2.31)

Observations 1,898 1,985 1,985

R-squared 0.68

Robust standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1 Includes year fixed effects

The Tobit estimation is left-censored after replacing missing values with zero

The Poisson estimation includes zero trade values

The results of the regressions in Table 3-1 determine the trading pattern of the exports from Pakistan.

Although, Pakistan is likely to trade more with larger economies in terms of their GDP, it may trade more

with countries that have a lower level of GDP per capita16. Pakistan is also likely to trade more with

countries that were colonized by the British post 1945. There is no significant relationship between

sharing a border with Pakistan and trading relationship with Pakistan. Interestingly, the regional trade

agreements do not influence the value of exports between Pakistan and its trading partners, except for

a negative coefficient significant at 10 percent level in Column 2. Excluding the variables on common

official language and regional trade agreements, the results reported for the independent variables in

Column 2 are similar to the results reported for the independent variables in Column 1. However, the

16 Although, major trading partners of Pakistan are developed countries, they also have large economies in terms

of GDP. Therefore, their GDP rather than their GDP per capita may positively influence exports from Pakistan in

Columns 1 and 2.

29

Poisson estimations in Column 3 reveal certain differences. As the Poisson estimation is a count model it

estimates the impact on the count of the dependent variable due to changes in the independent

variable. The expected increase in log count of trading relationships between Pakistan and its trading

partner with an increase in one-unit of the independent variable is determined by the coefficient. As

reported in Column 3, Pakistan is more likely to report trading relationships with larger economies and

countries with higher GDP per capita as well countries with common official language and with United

Kingdom, its colonizer. It is less likely to report trading relationships with countries located at a further

distance. The Poisson distribution may seem more realistic as the effect of GDP per capita and the

common official language are positive. This is more consistent to the theoretical aspects of the gravity

Where ki is the labor income generated by the household, \i�̂ is the share of income generated by

selling tradable goods, \iJ� is the share of income generated by selling non-tradable goods, \i^l is the

share of expenditure in consumption of tradable goods and \iJl is the share of expenditure in

consumption of non-tradable goods. <\i�̂ � \i^l @ and <\iJ� � \iJl @ are the exposure of households to

changes in prices of tradable goods and non-tradable goods respectively. Larger the difference, greater

the impact of changes in prices of the respective goods and consequently, the total effect. An increase in

the tariff rates will result in ∆]^j > 0 and a decrease in the tariff rates will result in ∆]^j < 0. For

simplicity, it is assumed that the change in tariff rates has no impact on ∆]Jj and ∆[j.

Source

The data is borrowed from the Household Integrated Economic Survey (HIES) 2010-11. The HIES is a

component of the Pakistan Social and Living Standard Measurement (PSLM) Project by the Pakistan

Bureau of Statistics. The HIES collects information on several social and economic indicators of

households across provinces in Pakistan. The primary purpose of the HIES is to collect information on

39

the income and consumption patterns of households. Household characteristics such as size of family

and the employment status of household member amongst others are also collected.

Although, the data collected from the surveys is extensive and across both urban and rural areas, this

study is limited to households in the rural areas as the purpose of this study focuses on the income and

consumption effects of a change in tariff on food products. Rural households are more likely than urban

households to be consumers as well as producers of food products. The households are surveyed on

their bi-weekly expenditure on food items and the income generated from the cultivation of crops. The

per capita expenditure is calculated to measure the purchasing power of the households.

The tariff data is borrowed from World Integrated Trade Solution (WITS) available at

http://wits.worldbank.org. World average tariff rates on the imports of goods into Pakistan for 2004 and

2011 is downloaded from WITS18. The data is downloaded at six digit HS code. The HS codes are

matched to the list of products specified in HIES, provided in Appendix B, in order to determine the tariff

rates necessary to calculate the consumption effect and the income effect. The products listed in

household expenditures sheet is matched with the tariff data available from WITS at four digit HS codes

and the products listed in the household income sheet is matched with the tariff data available from

WITS at six digit HS codes.

Background on Trade Liberalization in Pakistan between 2004 and 2011

Pakistan adopted trade liberalization policies in early 2000s. The policies to lower import tariffs increase

the import of food items such as sugar, livestock and vegetables along with other commodities.

According to COMTRADE, the imports increased from US $18 billion in 2004 to US $25 billion in 2005, an

increase of almost 50 percent in one year. The imports reached US $43.5 billion in 2011. The imports of

food items included in the household expenditure survey increased from US $453 million in 2004 to US

$1.47 billion in 2011. The simple average tariff rate for all imports in 2004 was 16.64 percent and the

weighted average tariff rate was 13.01 percent. The simple average tariff rate for all imports in 2011 was

12.34 percent and the weighted average tariff rate was 9.02 percent. This suggests a drop in the tariff

rates between 2004 and 2011. Pakistan undertook policies to lower import tariffs on several goods

including food items. The income effect and the consumption effect of rural households will reflect the

results of such policies. During this period, Pakistan also negotiated and signed free trade agreements

with China, Sri Lanka and Malaysia signifying the adoption of trade liberalization in Pakistan.

Empirics

Downloading the Tariff Data and Matching with the HIES Survey Data

First, the tariff data is downloaded from WITS to calculate the changes in the import tariffs between

2004 and 2011. The tariff data is downloaded at six digit HS codes, converted to four digits HS code to

match the product codes of food items in the expenditure survey. As the import tariffs are listed at six

18 Although, it is possible that the majority of the change in the price levels between 2004 and 2011 may have

occurred in the earlier years rather than the latter years. This exercise does not discount for such a scenario. The

purpose of the exercise is to determine the simple percentage price change between 2004 and 2011. Please refer

to the section on the background for a summary analysis of import flow into Pakistan between 2004 and 2011 and

the change in tariff rates.

40

digit HS code, the tariffs are weighted at the six-digit level using import data and then summed up to the

respective product-level category in the HIES.

The HS codes are maintained at six digit-level to match the products listed in the income survey and

subsequently calculate the income effect. The trade-weighted import tariffs for each product code

reported in HIES are calculated using the collapse function in STATA by assigning import values as

weights for the respective tariffs.

Calculating the Change in Weighted Tariff Rates

Next, the weighted tariffs for 2004 and 2011 are used to calculate the change in price levels19. The

following formula is used to calculate the change in tariff rates, ∆`(,����p����, ∆ �̀,����p����:20

∆`(,����p���� = 100 + `(,����100 + `(,���� − 1

∆ �̀,����p���� = 100 + �̀,����100 + �̀,���� − 1

where each product group in the household bi-weekly expenditure survey is denoted by i, and each

product group in the household income survey is denoted by j21. `(,���� is the weighted average tariff

rates for the products listed in the household surveys in 2004 and `(,���� is the weighted average tariff

rates for the products listed in the household surveys in 2011.

The level of expenditure incurred and the level of income earned in 2004 for the consumption and the

production respectively of the same bundle of goods as in 2011 will be higher if the prices of the

tradable goods decrease between 2004 and 2011. The consumption effect is the impact of trade policies

on household expenditures through the prices of goods consumed by the household. The income effect

is the impact of trade policies on household income through the prices of goods produced by the

household. Theoretically, a reduction in the prices of goods will lead to a positive consumption effect

and a negative income effect.

The change in weighted average tariff is multiplied by the share in expenditure of each product group in

total expenditure on food products22. The resultant value is the change in the share in expenditure of

each product group. Therefore, an increase in the total share implies that the households are incurring

greater expenditure on food products in order to remain at the same utility level in the base year, 2011.

This is the case if the prices of a product are higher in 2004 than in 2011, our base year for the survey

19 The household surveys were conducted in 2011. Therefore, all percentage changes have been calculated taking

2011 as the base year. A lower tariff rate in 2011 than 2004 will imply a fall in prices between 2004 and 2011.

Therefore, the consumption effect will be positive and the income effect will be negative for a tariff rate that is

lower in 2011 than in 2004. 20 As the product groups are classified differently in the household expenditure sheet and the household income

sheet, different notations have been adopted to denote the product groups across the two sheets. 21 Bi-weekly expenditures can be scaled up to annual expenditures. The shares in bi-weekly expenditures will be

the same as in annual expenditures. 22 For simplicity, only the food products are classified as tradable goods. All the remaining products are classified as

non-tradable goods.

41

data. The summation of this across all product groups will provide the value of the consumption effect.

Tariff liberalization will have a positive impact on the consumption effect. A similar inference can be

made for the income effect.

Calculating the Consumption Effect

The change in share of expenditure on food products at the household-level between 2004 and 2011, \i(,����lq/r , is calculated by multiplying the change in weighted tariff between 2004 and 2011, as

formulated above, with the share of expenditure on food items incurred for each of the nine product

groups of tradable goods listed in the bi-weekly household expenditure sheet in 2011:

\i(,����lq/r = ∆`(,����p���� ∗ (\i(,����l ) The consumption effect at the household level is then calculated as the summation of the change in share

of all food products purchased between 2004 and 2011, where i=1,2,……,T:

\i^,����lq/r = ∑ \i(,����lq/r(̂0�

The total consumption effect in the economy across all households in the rural areas is the summation

of all the values calculated at the household level.

Calculating the Income Effect

After calculating the consumption effect, the next step is to determine the income effect. The change in

share of income generated by cultivating and selling tradable products between 2004 and 2011, \i�,�����jqR

, is the income share of that product sold in 2011 multiplied by the change in weighted tariff for the

respective product between 2004 and 2011.

\i�,�����jqR = ∆ �̀,����p���� ∗ (\i�,����

� )

The income effect at the household level is calculated as the summation of the change in share of all

tradable products sold between 2004 and 2011, where where j=1,2,……,T: :

\i^,�����jqR = ∑ \i�,�����jqR�̂0�

The total effect for a household from a reduction in price of tradable goods between 2004 and 2011 is:

\i^,����^qT \i^,����lq/r � \i^,�����jqR

where the consumption effect and the income effect have opposite signs.

The per capita annual expenditure is calculated as the total annual expenditure incurred by a household

divided by the total number of individuals in the households. The consumption effect and the income

effect are plotted against per capita annual expenditure incurred by a household in order to capture the

42

purchasing power of a household with respect to the number of individuals belonging to a household. A

richer household will have a greater purchasing power. If government policies favorably redistribute

income, the consumption effect of a decrease in price should be higher for the poorer households and

the income effect of a decrease in price should be smaller for poorer households.

As the number of households surveyed is substantially lower than the number of households actually

present within each primary sampling unit, a sampling weight is assigned to each primary sampling unit

in order to determine the actual size of the primary sampling unit with respect to the number of

households surveyed. The weight determines the probability that the household will be selected. If the

household has a high probability of being selected, then the household will be over-represented in the

survey, and a lower weight will be assigned to a household. The weights used in the study are provided

in the HIES data.

43

Results

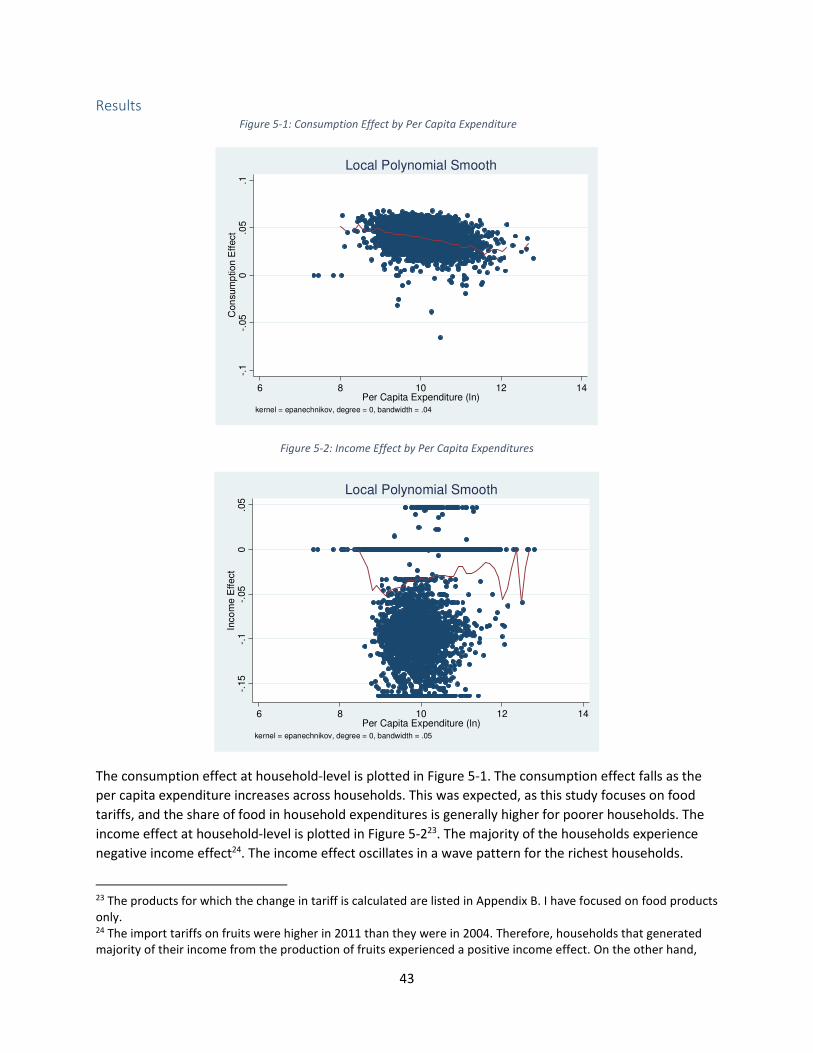

Figure 5-1: Consumption Effect by Per Capita Expenditure

Figure 5-2: Income Effect by Per Capita Expenditures

The consumption effect at household-level is plotted in Figure 5-1. The consumption effect falls as the

per capita expenditure increases across households. This was expected, as this study focuses on food

tariffs, and the share of food in household expenditures is generally higher for poorer households. The

income effect at household-level is plotted in Figure 5-223. The majority of the households experience

negative income effect24. The income effect oscillates in a wave pattern for the richest households.

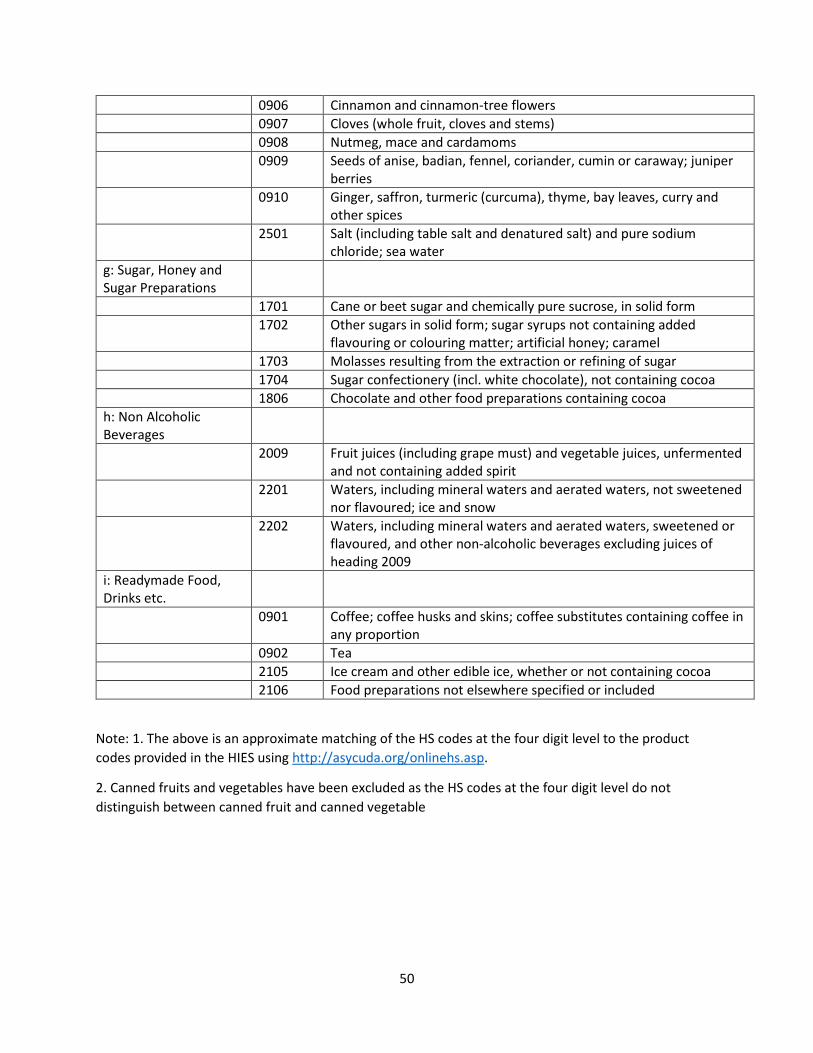

23 The products for which the change in tariff is calculated are listed in Appendix B. I have focused on food products

only. 24 The import tariffs on fruits were higher in 2011 than they were in 2004. Therefore, households that generated

majority of their income from the production of fruits experienced a positive income effect. On the other hand,

The weighted average tariff rates on the product group defined as fruits is greater in 2011 than in 2004.

Therefore, the prices of fruits has increased during the time period. This suggests a positive income

effect for households that earn a larger proportion of their income by cultivating fruits.

Table 5-1: Income, Consumption and Overall Effects by Deciles

Decile Income Effect Consumption

Effect

Total Effect

1 -0.044 0.045 0.001

2 -0.043 0.043 0.000

3 -0.033 0.042 0.009

4 -0.036 0.041 0.005

5 -0.034 0.041 0.007

6 -0.031 0.040 0.009

7 -0.035 0.039 0.004

8 -0.032 0.038 0.006

9 -0.028 0.036 0.007

10 -0.026 0.032 0.006

The total effect by decile of per capita expenditure is listed in Table 5-1. The poorest households in the

rural areas experience the smallest total effect as the larger positive consumption effect is canceled by

the negative income effect, which is similar in magnitude. The consumption effect falls as the level of

per capita expenditure by households increase. However, the income effect is oscillatory across the per

capita expenditure incurred by households. Although, the poorest households face lower total effect

than the richest households in the rural areas, the households belonging to the middle deciles of per

capita expenditure levels benefit the most in terms of total effect than the households in the two

extremes of per capita expenditure levels.

wheat reported the highest change in tariff rates between 2004 and 2011. Households concentrated towards the

bottom of the graph, below -0.15, are likely to generate income predominantly from wheat.

45

Figure 5-3: Total Effect by Provinces

The box plot for the total effects by provinces is shown in Figure 5-3. The lower and the upper edges of

the boxes display the 25th and the 75th percentile of the rural households respectively, the horizontal line

within the box displays the 50th percentile and the upper horizontal line above the boxes display the 95th

and below the boxes display the 5th percentile of the rural households in the respective provinces. The

outliers are represented by dots. The box plot shows that more than 50 percent of the rural households

will gain from trade liberalization across all provinces. Only the outliers will lose in Balochistan due to

trade liberalization, suggesting that only an insignificant proportion of households in the province lose

from trade liberalization. It is also interesting to note that the gap between the respective percentile

identifiers is spread out for the lower percentiles than for the upper percentiles. This suggests that there

is lower dispersion in the total effect amongst households that report higher levels of gain in total

effect25.

In order to determine whether the removal of a tariff has a progressive or a ‘pro-poor’ bias, that is it

benefits the poor households more than the richer households, it is important to quantify the impact of

tariffs and tariff changes on different income levels based on either the quantiles, deciles or centiles of

income. This can be achieved by performing the Locally Weighted Scatterplot Smoothing (LOWESS

estimation in STATA).

25 A deeper analysis, for instance using population weights and GDP weights for provinces, is necessary to obtain a

better understanding of the distribution of the total effect across provinces. Such an exercise is beyond the scope

of this project.

-.15

-.1

-.05

0.0

5.1

Tota

l E

ffe

ct

Balochistan KP (NWFP) Punjab Sindh

46

Figure 5-4: Tariff and Change in Tariff Sorted on Income Distribution

The consumption-weighted average tariffs and average change in tariffs are calculated on the basis of

the weight of the products (food items) consumed by the households. The total income earned by the

households is distributed based on centiles. Sampling weights provided in the survey data are used. The

lowess smoother curves are plotted in Figure 5-4. The richer households faced higher tariff rates than

the poorer households. Further, the reduction in the tariff rates between 2004 and 2011 was ‘pro-poor’

as the change had a greater impact on the consumption bundle of the poorer households than the

richer households.

78

910

11

12

(Mean)

Tariff, 2011

0 20 40 60 80 100100 quantiles of income

bandwidth = .8

Lowess smoother

3.5

44.5

55.5

(Mean)

Perc

enta

ge C

hange in T

ari

ff, 2004-2

011

0 20 40 60 80 100100 quantiles of income

bandwidth = .8

Lowess smoother

47

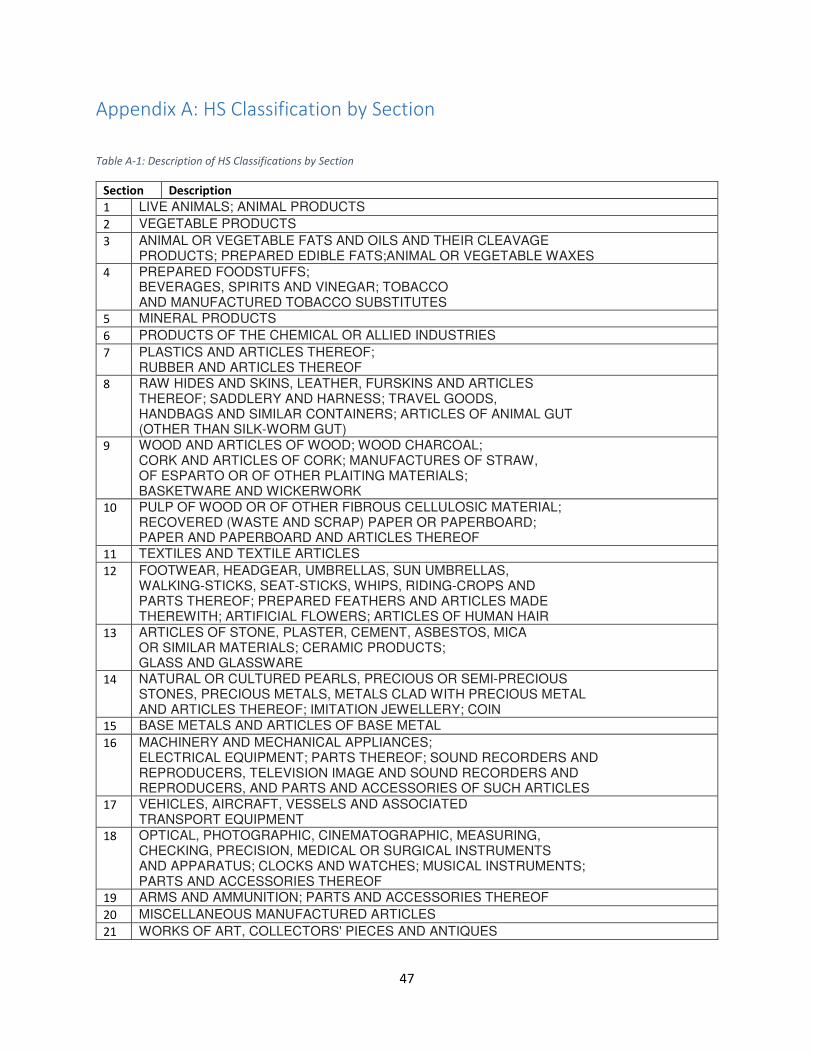

Appendix A: HS Classification by Section

Table A-1: Description of HS Classifications by Section

Section Description

1 LIVE ANIMALS; ANIMAL PRODUCTS

2 VEGETABLE PRODUCTS

3 ANIMAL OR VEGETABLE FATS AND OILS AND THEIR CLEAVAGE PRODUCTS; PREPARED EDIBLE FATS;ANIMAL OR VEGETABLE WAXES

4 PREPARED FOODSTUFFS; BEVERAGES, SPIRITS AND VINEGAR; TOBACCO AND MANUFACTURED TOBACCO SUBSTITUTES

5 MINERAL PRODUCTS

6 PRODUCTS OF THE CHEMICAL OR ALLIED INDUSTRIES

7 PLASTICS AND ARTICLES THEREOF; RUBBER AND ARTICLES THEREOF

8 RAW HIDES AND SKINS, LEATHER, FURSKINS AND ARTICLES THEREOF; SADDLERY AND HARNESS; TRAVEL GOODS, HANDBAGS AND SIMILAR CONTAINERS; ARTICLES OF ANIMAL GUT (OTHER THAN SILK-WORM GUT)

9 WOOD AND ARTICLES OF WOOD; WOOD CHARCOAL; CORK AND ARTICLES OF CORK; MANUFACTURES OF STRAW, OF ESPARTO OR OF OTHER PLAITING MATERIALS; BASKETWARE AND WICKERWORK

10 PULP OF WOOD OR OF OTHER FIBROUS CELLULOSIC MATERIAL; RECOVERED (WASTE AND SCRAP) PAPER OR PAPERBOARD; PAPER AND PAPERBOARD AND ARTICLES THEREOF

11 TEXTILES AND TEXTILE ARTICLES

12 FOOTWEAR, HEADGEAR, UMBRELLAS, SUN UMBRELLAS, WALKING-STICKS, SEAT-STICKS, WHIPS, RIDING-CROPS AND PARTS THEREOF; PREPARED FEATHERS AND ARTICLES MADE THEREWITH; ARTIFICIAL FLOWERS; ARTICLES OF HUMAN HAIR

13 ARTICLES OF STONE, PLASTER, CEMENT, ASBESTOS, MICA OR SIMILAR MATERIALS; CERAMIC PRODUCTS; GLASS AND GLASSWARE

14 NATURAL OR CULTURED PEARLS, PRECIOUS OR SEMI-PRECIOUS STONES, PRECIOUS METALS, METALS CLAD WITH PRECIOUS METAL AND ARTICLES THEREOF; IMITATION JEWELLERY; COIN

15 BASE METALS AND ARTICLES OF BASE METAL

16 MACHINERY AND MECHANICAL APPLIANCES; ELECTRICAL EQUIPMENT; PARTS THEREOF; SOUND RECORDERS AND REPRODUCERS, TELEVISION IMAGE AND SOUND RECORDERS AND REPRODUCERS, AND PARTS AND ACCESSORIES OF SUCH ARTICLES

17 VEHICLES, AIRCRAFT, VESSELS AND ASSOCIATED TRANSPORT EQUIPMENT

18 OPTICAL, PHOTOGRAPHIC, CINEMATOGRAPHIC, MEASURING, CHECKING, PRECISION, MEDICAL OR SURGICAL INSTRUMENTS AND APPARATUS; CLOCKS AND WATCHES; MUSICAL INSTRUMENTS; PARTS AND ACCESSORIES THEREOF

19 ARMS AND AMMUNITION; PARTS AND ACCESSORIES THEREOF

20 MISCELLANEOUS MANUFACTURED ARTICLES

21 WORKS OF ART, COLLECTORS' PIECES AND ANTIQUES

48

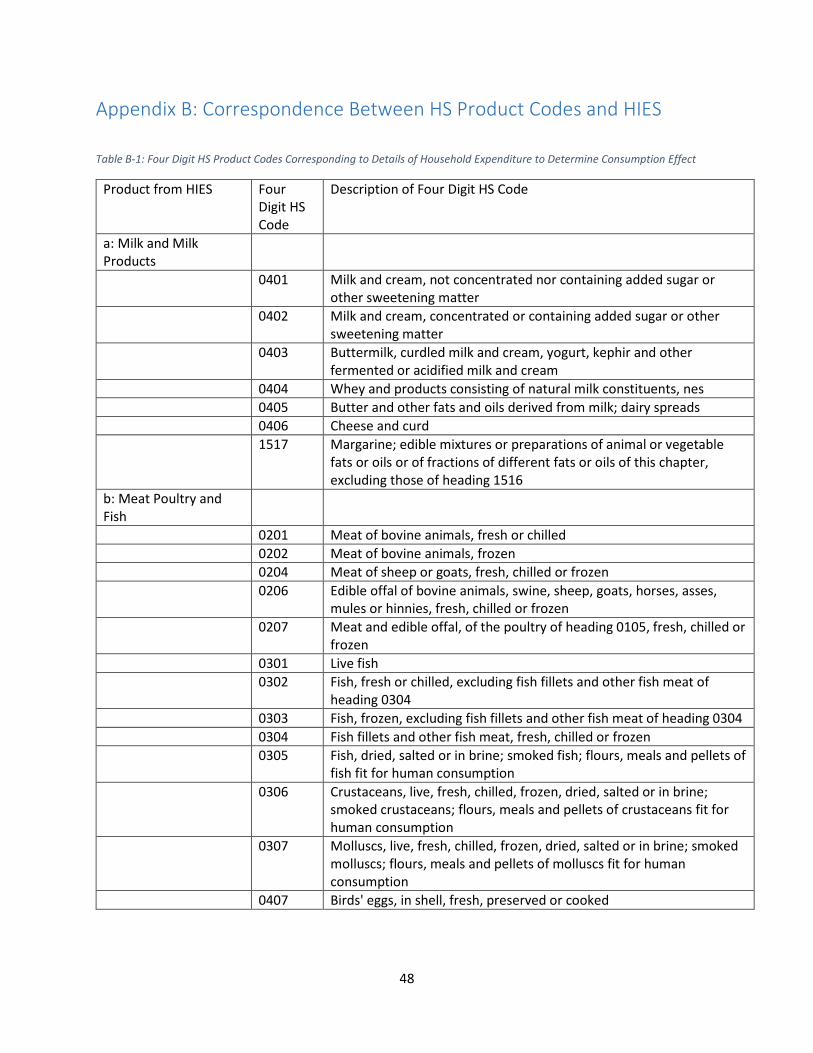

Appendix B: Correspondence Between HS Product Codes and HIES

Table B-1: Four Digit HS Product Codes Corresponding to Details of Household Expenditure to Determine Consumption Effect

Product from HIES Four

Digit HS

Code

Description of Four Digit HS Code

a: Milk and Milk

Products

0401 Milk and cream, not concentrated nor containing added sugar or

other sweetening matter

0402 Milk and cream, concentrated or containing added sugar or other

sweetening matter

0403 Buttermilk, curdled milk and cream, yogurt, kephir and other

fermented or acidified milk and cream

0404 Whey and products consisting of natural milk constituents, nes

0405 Butter and other fats and oils derived from milk; dairy spreads

0406 Cheese and curd

1517 Margarine; edible mixtures or preparations of animal or vegetable

fats or oils or of fractions of different fats or oils of this chapter,

excluding those of heading 1516

b: Meat Poultry and

Fish

0201 Meat of bovine animals, fresh or chilled

0202 Meat of bovine animals, frozen

0204 Meat of sheep or goats, fresh, chilled or frozen

![JD Edwards EnterpriseOne Applications Localizations for … · 2020-06-11 · [1]JD Edwards EnterpriseOne Applications Localizations for Australia and Singapore Implementation Guide](https://static.documents.pub/doc/80x56/5f3196ce7cc95632a0421491/jd-edwards-enterpriseone-applications-localizations-for-2020-06-11-1jd-edwards.jpg)

![JD Edwards EnterpriseOne Applications Localizations for ... · [1]JD Edwards EnterpriseOne Applications Localizations for Portugal Implementation Guide Release 9.1 E23360-09 February](https://static.documents.pub/doc/80x56/5e5ae6c17374176a324da0df/jd-edwards-enterpriseone-applications-localizations-for-1jd-edwards-enterpriseone.jpg)