A preliminary assessment of the financial feasibility of basic income in Belgium Emily Van de Walle Academic year 2015-2016 University of Antwerp Faculty of Applied Economics Promoter: Prof. dr. Erreygers G. Master’s thesis submitted to obtain the degree of: Master of Applied Economic Sciences: Economic Policy

Transcript

A preliminary assessment of the

financial feasibility of basic income in Belgium

Emily Van de Walle

Academic year 2015-2016

University of Antwerp

Faculty of Applied Economics

Promoter:

Prof. dr. Erreygers G.

Master’s thesis submitted to obtain the

degree of:

Master of Applied Economic Sciences:

Economic Policy

1 | P a g e

Preface

Basic income has received much attention in the media in recent years and it was also in

this manner that I was first brought into contact with basic income. Admittedly, at first I

was dubious yet interested in the possible advantages of unconditionally granting all

citizens an income. During my bachelor’s year, I was thrilled to find basic income as one of

the topics for the final task of the bachelor’s project and thus wrote a paper on the

futurology and feasibility of basic income. By reading up on the literature about basic

income, my interest for the proposal had grown but at the same time I found myself

bothered by the lack of transparency in the methodology applied by basic income

proponents to assess how basic income may be possibly financed in Belgium. For this

reason, I decided to take up the challenge to personally assess the financial feasibility of

basic income in Belgium and this master’s dissertation is the final product towards that

end.

I could not have made it through this challenging journey without the support of a number

of people. First, I would like to express my deepest gratitude to my promoter prof. dr.

Erreygers Guido. I am not only grateful for his advice, comments, corrections, and his

guidance, but also for giving me the opportunity to write on a subject that I am passionate

about. Second, I am also thankful to my partner for his unconditional support,

encouragement, and for reading my master’s thesis. Third, I would like to thank my parents

and friends for their support from start to finish.

Emily Van de Walle

2 | P a g e

Abstract

The costs of unconditionally granting every citizen an equal fixed monthly income, known

as basic income, are substantial. In Belgium, advocates have attempted to ascertain the

financial feasibility of the proposal; however, the contributions are not only limited in

number but the applied methodology is also lacking in transparency. This dissertation

provides a preliminary assessment of whether basic income is financially feasible in

Belgium for the year 2010. The yearly costs of five basic income proposals including the

costs of the remaining social protection system are estimated. The cost of unconditional

basic income is estimated by multiplying the level of basic income with the number of

beneficiaries and the cost of the social protection system is estimated as prescribed in the

proposal. The basic income proposals covered a range between two extremes, basic income

as a substitute and basic income as a complement to the social protection system. The costs

vary greatly in magnitude depending on the characteristics of each proposal. Proposals

leaning towards the first extreme are naturally more financially feasible due to lower costs

and the opposite is applicable to the second extreme. I suggest a proposal that is financially

feasible as well as socially desirable with respect to beneficiaries of social benefits. The

financing of this proposal was assessed by determining the costs of social benefits that

would be made redundant by implementing basic income. I applied a criterion in which

basic income entirely replaces social benefits that are on average lower than basic income

and partially when higher than the level of basic income. The cost savings on the

replacement of social benefits are determined to be considerable in size and largely

contribute to financing basic income. The financing of the remaining cost of basic income

after accounting for the cost savings is beyond this paper. According to proponents, it is

technically feasible to finance the remaining cost gap with tax reforms. However, besides

improving the techniques to assess the financial feasibility of basic income there are other

concerns that have to be addressed in the context of Belgium, such as political feasibility,

sustainability, distributional effects and behavioral effects which follow from basic income

and the suggested tax reforms. These are the next steps that have to be taken before we can

contemplate implementing basic income in Belgium.

3 | P a g e

Executive summary

The proposal that unconditionally grants every citizen an equal fixed monthly income,

known as basic income, has recently received much attention in the media. In Europe, a

growing number of individuals, academics, policymakers, and interest groups have shown

interest in the proposal thanks to the solutions it has to offer in order to overcome a

number of obstacles. With respect to the high unemployment rates, basic income provides

the unemployed a wider scope of opportunities by granting them income security, enabling

individuals to look for a job they desire. Basic income is said to also stimulate

entrepreneurship. Furthermore, the disincentives to work implied by the conditionality of

unemployment benefits are eliminated as basic income is granted regardless of income.

Last but not least, basic income is said to also emancipate the poor and ensures “real

freedom for all” (Van Parijs, 1995). (Groot, 2004, p. 17-21; Soininvaara, 200, p. 7-8)

The contributions to the literature have been steadily increasing, covering a wide range of

topics varying from, but not limited to the social desirability, the political feasibility, and

the financial feasibility of basic income. In Belgium, there has also been a growing interest

in the radical proposal by academics and politicians alike. The contributions, however, are

limited to only a small number of topics and the financial feasibility of basic income is

unfortunately not one of them. Proponents of basic income have only provided rough

calculations of how to finance basic income with a lack of transparency on the

methodologies of how the calculations were obtained. I, therefore, took up the challenge to

provide a preliminary assessment of the financial feasibility of basic income by providing

an answer to the following two research questions in the context of Belgium, given a

dataset of the year 2010: ‘How much would a scheme of basic income cost?’ and ‘How much

are the cost savings that are realized by basic income replacing social benefits?’

4 | P a g e

Cost of basic income

Aside from the three main features of every basic income, unconditionality, individuality,

and without means test or work requirement, basic income schemes come in all shapes and

sizes, and as a consequence, so do their costs (Peña-Miguel, De la Peña Esteban, &

Fernandez-Sainz, 2014, p. 96). To acknowledge the variety of basic income proposals, five

basic income proposals are discussed that can be placed between two extremes, the ‘basic-

income-to-substitute-everything’ scheme, a low-cost benchmark, and the ‘basic-income-

purely-as-a-complement’ scheme, a high-cost benchmark (Melzochová & Špecián, 2015 p.

555-556).

The first basic income proposal to be considered is of the extreme ‘basic-income-to-

substitute-everything’ and is determined to be the most financially feasible due to the

substantial cost savings implied by the complete abolishment of the social protection

system. Given a breakeven of the costs of basic income and the current expenditures of the

social protection system of €95 billion in 2010, Belgium can afford to grant every adult

citizen a basic income of €911 per month. However, while the extreme proposal is

financially feasible, a number of vulnerable social groups would be worse off under the

scheme of basic income as the level of certain social benefits are higher than the basic

income level, making the proposal socially undesirable. Accounting for social desirability,

the following three discussed basic income proposals partially maintained the social

protection system and the last proposal, which is by the authors Raventos et al., can be

considered to lean closely to the second extreme, ‘basic-income-purely-as-a-complement’.

Raventos et al. namely set the level of basic income so that it is “topped up to an equal

quantity when the public cash benefit is of a greater amount” (Arcarons, Raventos Pañella

& Torrens Mèlich, 2014, p. 82) for current beneficiaries of social benefits. However, given

the great complement to the social protection system, the scheme has considerable costs

and is considered to be less financially feasible. A trade-off is thus identified between

financial feasibility and social desirability: basic income schemes that incorporate the

ethical principles of the social protection system by granting the socially vulnerable groups

a higher level of basic income, is socially desirable, but leads to higher costs. To enhance

the financial feasibility of the proposal by Raventos et al., I modified the proposal and

5 | P a g e

adjusted the level of basic income downwards. This modified proposal grants every adult

€600 per month and every minor €150 per month while ensuring that recipients of social

benefits are at least as well off under the scheme of basic income compared to the current

social protection system. This modified proposal is estimated to cost Belgium €114 billion,

including the cost of health care and the retained social benefits, with a ceteris paribus

assumption for the year 2010. Placing this number in perspective, the total cost is 120% of

what we spent on the social protections system in 2010. The next research question to be

addressed is how to finance this enormous cost. (B.U.B., 2016; FOD Sociale Zekerheid,

2011; Melzochová & Špecián, 2015 p. 555-556)

Financing basic income

There are two main methods through which basic income may be financed, cost savings

and extra government revenues generated through tax reforms. This paper focuses on the

former method, assessing the cost savings that are realized by the replacement of social

benefits by basic income for the modified basic income proposal by Raventos et al. In order

to determine which social benefits are entirely or partially replaced by basic income, I

made a comparison between the average level of social benefits to the level of basic income

while applying the criterion by Raventos et al. that prescribes to entirely replace social

benefits of a lower level by basic income and to partially replace social benefits of a higher

level, up to the level of basic income. So that beneficiaries of social benefits do not receive

the level of basic income on top of what they currently receive. The cost savings that are

realized are concluded to be significant in size. Concerning the modified basic income

proposal by Raventos et al., the cost savings of the proposal is €79 billion, the summation

of the initial total expenditures of all social benefits and health care. The remaining cost gap

of €36 billion can technically be financed through tax reforms suggested by Belgian basic

income proponents. However, the calculations of these tax reforms have to be improved in

quality, applying a transparent and reliable methodology by using micro-simulation models

that allow integrating the behavioral effects as well as the distributional effects of basic

income and the implemented tax reforms. Only then will the picture on the financial

feasibility of basic income truly be complete. (Arcarons et al., 2014)

2.Basic income ...................................................................................................................................... 16

2.1 Defining basic income .......................................................................................................................... 16

2.2 Basic income in Europe ....................................................................................................................... 19

2.2.1 The two obstacles .......................................................................................................................... 19

2.2.2 Overcoming the obstacles .......................................................................................................... 22

2.2.3 The administrative efficiency argument............................................................................... 23

2.3 Basic income in Belgium ..................................................................................................................... 24

3.Financial feasibility of basic income ......................................................................................... 27

3.1 An introductory assessment of the costs of basic income ..................................................... 27

3.2 Review of the literature ....................................................................................................................... 31

3.3 Preliminary themes to consider ....................................................................................................... 33

3.3.1 Social protection in Belgium ..................................................................................................... 33

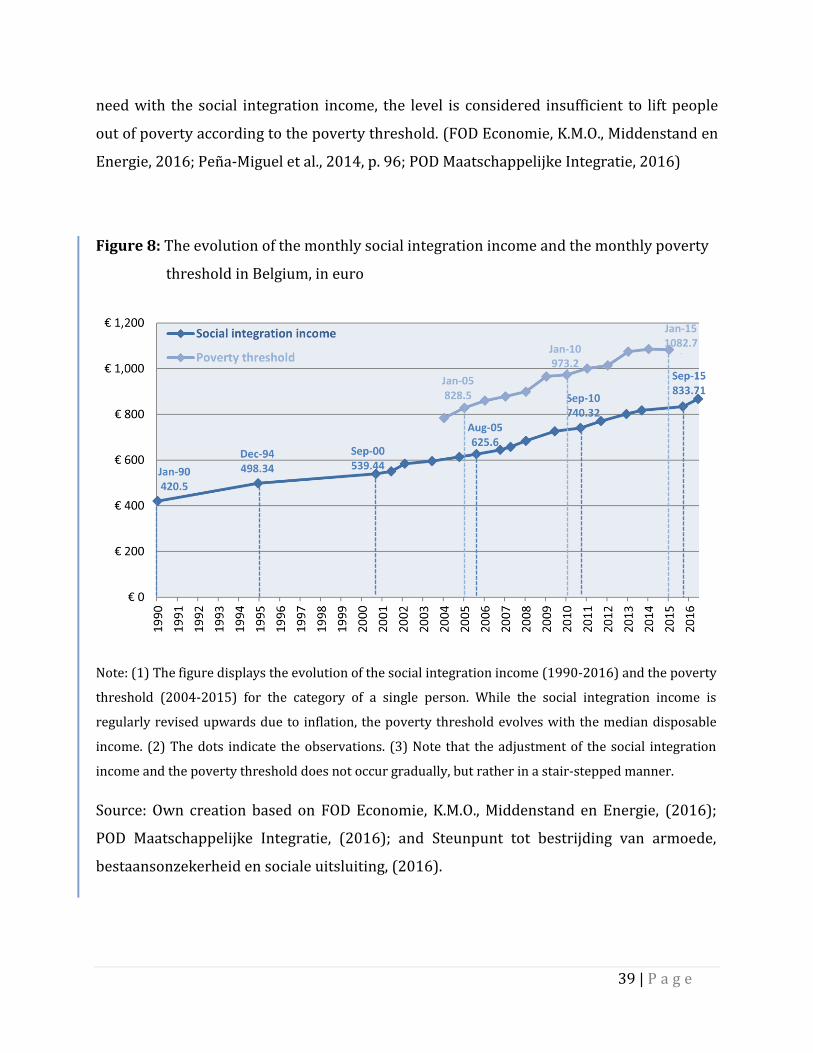

3.3.2 The social integration income and the poverty threshold ............................................ 39

3.3.3 The demographics of Belgium .................................................................................................. 41

3.4 Basic income proposals ....................................................................................................................... 42

3.4.1 The B.U.B. proposal ....................................................................................................................... 44

3.4.2 The Vivant proposal ..................................................................................................................... 48

3.4.3 The proposal by Defeyt ............................................................................................................... 52

3.4.4 The proposal by Raventos et al. ............................................................................................... 55

3.4.5 A modification of the proposal by Raventos et al. ............................................................ 59

3.4.6 An overview of the considered basic income proposals ................................................ 61

Part A - Figures ............................................................................................................................................... 91

Part B – Tables ................................................................................................................................................ 92

Part C - The key figures on social protection expenditures .......................................................... 95

Part D – Statistical figures of social benefits ..................................................................................... 106

Part E – Cost estimations of the basic income proposals............................................................. 126

Figure 5: A Belgian subdivision of the Belgian social protection system ......................................

Figure 6: A European subdivision (ESSPROS) of the social protection expenditures ..............

Figure 7: Social protection expenditures, in percentages (%), Belgium, 2010 ...........................

Figure 8: The evolution of the monthly social integration income and the monthly

poverty threshold in Belgium, in euro ......................................................................................................

Figure 9: Basic income proposals placed between two extremes ....................................................

Figure 10: Total yearly cost of the considered basic income proposals, including social

benefits and health care if applicable, in million euro, Belgium, 2010 ..........................................

Figure 11: Total yearly cost of the modified basic income proposal by Raventos et al., in

million euro, Belgium, 2010 ............................................................................................................................

Figure 12: Comparison of the cost savings and the grand total cost of the basic income

proposal by Raventos et al., in million euro, Belgium, 2010 ..............................................................

Figure 13: The Laffer curve .............................................................................................................................

Appendix: Part A - Figures………………………………………………………………………………………….

Figure A1: Slope of the linear functions: total expenditures on social protection and the

cost of the basic income based on the social integration income, in million euro, Belgium,

Table E2: Regular recurring social benefits, taking time off work, comparison on a yearly

basis, in euro, Belgium, 2010 ..........................................................................................................................

Table E3: Exceptional one-time and yearly recurring social benefits, comparison on a

yearly basis, in euro, Belgium, 2010 ............................................................................................................

Table E4: Basic income proposal by Raventos et al. – Social integration income – Total

costs of basic income and retained social benefits.................................................................................

Table E5: Basic income proposal by Raventos et al. – Poverty threshold – Total costs of

basic income and retained social benefits .................................................................................................

Table E6: A modification of the proposal by Raventos et al. - Total costs of basic income

and retained social benefits ............................................................................................................................

Table E7: List of references, categorized by the type of data .............................................................

13 | P a g e

1. Introduction

The idea of unconditionally granting a benefit to every citizen (or resident) at a regular

interval, a basic income, can be traced back as early as 1797 to the plan of the agrarian

radical, Thomas Spence, in The Rights of Infants. Spence propagated “the ownership of

natural resources, such as land, by local parish communities, who would then proceed to

lease these resources to the highest bidder. [The obtained revenues would contribute to

the financing of] public goods, the national government, and the residual income would be

distributed equally between all members of the parish at quarterly intervals” (Cunliffe &

Erreygers, 2004, p.81), clearly indicating a scheme of basic income. (Cunliffe & Erreygers,

2004, p. 81; Melzochová & Špecián, 2015, p. 550)

The concept of basic income is thus far from being a novel idea in contemporary society. As

a matter of fact, proposals of basic income have kept reappearing throughout the past two

centuries and notably; according to Cunliffe & Erreygers (2004, p. xiii) this has occurred

independently. The appealing characteristics of basic income have again led basic income

to resurface as strong as ever in the twenty-first century. This can be witnessed from the

promising upcoming experiments concerning basic income, such as in Finland, the recently

rejected but meaningful referendum of Switzerland, and the numerous discussions

surrounding basic income by academics, policymakers, and interest groups all over the

world (Agence France-Presse, 2016; Cunliffe & Erreygers, 2004, p. xiii; Soininvaara, 2000;

Laterza, 2015, p. 7).

However, the appealing concept of basic income nevertheless warrants a comprehensive

analysis: basic income remains as radical as it was back in 1797. Namely, the

unconditionality aspect of basic income is grandly opposed to conventional minimum

income schemes which are conditional of nature. This causes basic income to be considered

as “a threat to the primacy of paid work, as the central source of legitimate security”

(Soininvaara, 2000, p. 7). (Cunliffe & Erreygers, 2004, p. 81; Solow, 2000, p. ix)

14 | P a g e

A first traditional approach towards analyzing basic income, according to Solow (2000, p.

ix-x), would be to address the question of the feasibility of basic income on the one hand,

and that of the desirability of basic income and its consequences on the other. Although

both questions are vital in assessing the potential of basic income as a reformation of the

existing social protection system, the focus of this paper will lie on the former aspect: the

financial feasibility of basic income.

Specifically, this paper wishes to contribute to the debate of financial feasibility, by

providing answers to the following two research questions in the context of Belgium: ‘How

much would a scheme of basic income cost?’ and ‘How much are the cost savings that are

realized by basic income replacing social benefits?’

The first research question is a natural starting point when assessing the financial

feasibility of basic income. Basic income proposals come in all shapes and sizes, and

consequently so do the costs of basic income. For this reason, static cost estimations will

be provided for a range of basic income proposals for Belgium. Additionally, the current

social protection system will be analyzed and its costs will be compared to those of the

various basic income schemes in order to have a better perspective of the magnitude of the

costs. (Melzochová & Špecián, 2015, p.554-556)

The second research question contributes directly to the financial feasibility of basic

income. Basic income is namely financed by two methods. On the one hand, the cost savings

realized by basic income replacing social benefits reduces the total costs of basic income.

On the other hand, the remaining costs of basic income are principally financed by a tax

reform. (Monnier & Vercellone, 2014, p. 71-73)

The cost savings are dependent on the specific basic income scheme, but generally,

proponents at least advocate for a partial replacement of social benefits due to the

implausibility of simultaneously sustaining the costs of the social protection system and a

scheme of basic income. In order to concretely assess the cost savings, a criterion is

required to distinguish social benefits that are retained and social benefits that are

15 | P a g e

dissolved with the introduction of basic income. The criterion prescribed by Raventos et al.,

which instructs to completely replace social benefits of a lower level than basic income and

to partially replace social benefits of a higher level than basic income, will be applied for a

specific basic income scheme (Arcarons, Raventos Pañella & Torrens Mèlich, 2014, p. 82).

After accounting for cost savings, the next step is to finance the remaining cost gap. The

most conventional method is to generate extra revenue by tax reforms. A number of tax

reforms suggested by Belgian proponents of basic income will be presented. A formal

analysis of these tax reforms is beyond the scope of this paper; however, this is a step that

needs to be taken in order to complete the picture on financing basic income.

In order to provide an answer to these research questions, the paper is largely composed of

two chapters.

The first chapter allows an understanding of basic income by providing a definition of basic

income as well as by emphasizing its particularities by comparing basic income to

conventional minimum income schemes. Furthermore, the most relevant arguments for

basic income in Europe are discussed before situating the basic income debate in the

context of the political and academic sphere of Belgium.

The second chapter focuses on the financial feasibility of basic income. First, a literature

review will be presented and a number of preliminary themes will be covered, building

towards the cost estimations for a range of basic income proposals for Belgium.

Subsequently, the financing of the cost of basic income will be analyzed. The two research

questions will be addressed and an answer will be formulated in this chapter.

16 | P a g e

2. Basic income

2.1 Defining basic income

Hereby, I introduce two accessible definitions of basic income which jointly reflect the

cornerstone of every basic income proposal.

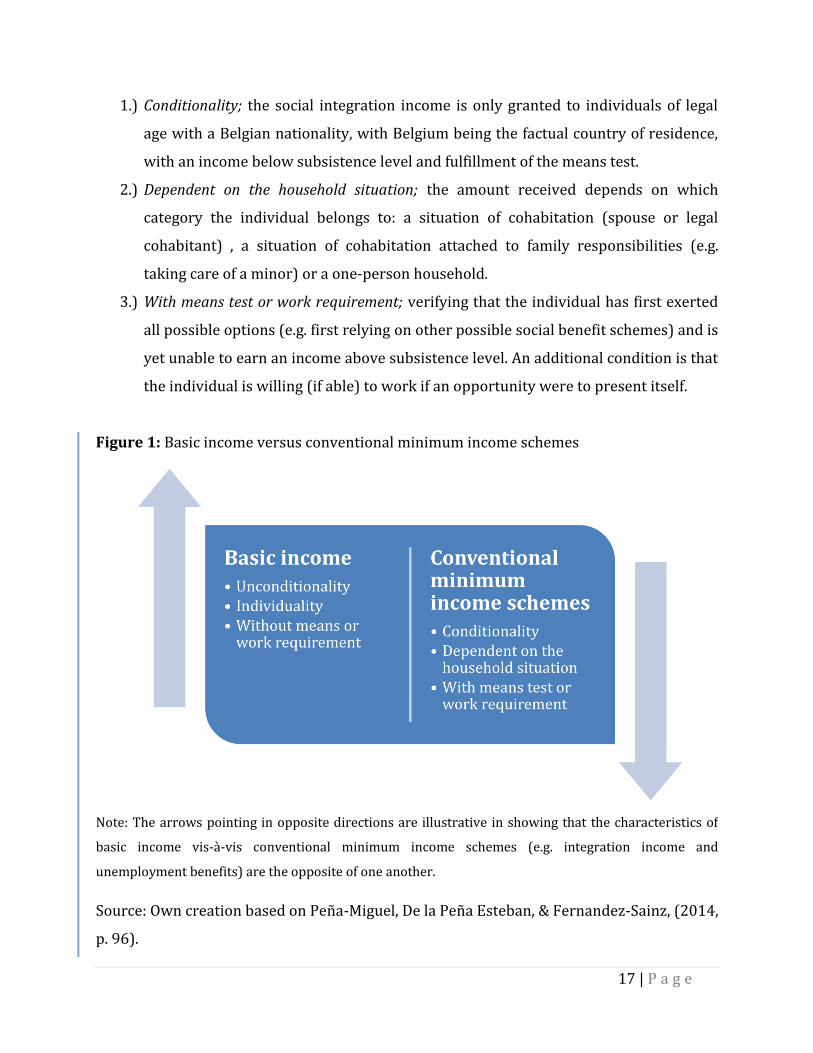

The first definition of basic income put forward by the Basic Income Earth Network (n.d. a)

draws special attention to three features which distinguish basic income from conventional

minimum income guarantees (Peña-Miguel, De la Peña Esteban, & Fernandez-Sainz, 2014,

p.96):

1.) Unconditionality; “basic income is to be considered a fundamental right”

(Melzochová & Špecián, 2015, p.551) regardless of a person’s background.

2.) Individuality; basic income is granted to every individual citizen (or resident)

irrespective of their household situation. (Melzochová & Špecián, 2015, p.551)

3.) Without means test or work requirement; further emphasizes that unconditionality

also implies that basic income is unconditional on any (work) requirement or

income level.

In comparison to conventional minimum income schemes which are conditional of nature,

these three features are exactly the opposite (Frazer & Marlier, 2009, p. 8; Peña-Miguel et

al., 2014, p. 96). A schematic overview is given in Figure 1. To illustrate; the requirements

of receiving a social integration income, a benefit received by individuals enabling them to

meet an income of subsistence level, clearly adheres to the following three opposite

characteristics in Belgium (Vlaanderen, n.d. a):

“A basic income is an income unconditionally granted to all on an individual basis, without

means test or work requirement” (BIEN, n.d. a).

“A universal basic income [is] an income paid by a government, at a uniform level and at

regular intervals, to each adult member of society” (Van Parijs, 2001, p.5).

17 | P a g e

1.) Conditionality; the social integration income is only granted to individuals of legal

age with a Belgian nationality, with Belgium being the factual country of residence,

with an income below subsistence level and fulfillment of the means test.

2.) Dependent on the household situation; the amount received depends on which

category the individual belongs to: a situation of cohabitation (spouse or legal

cohabitant) , a situation of cohabitation attached to family responsibilities (e.g.

taking care of a minor) or a one-person household.

3.) With means test or work requirement; verifying that the individual has first exerted

all possible options (e.g. first relying on other possible social benefit schemes) and is

yet unable to earn an income above subsistence level. An additional condition is that

the individual is willing (if able) to work if an opportunity were to present itself.

Figure 1: Basic income versus conventional minimum income schemes

Note: The arrows pointing in opposite directions are illustrative in showing that the characteristics of

basic income vis-à-vis conventional minimum income schemes (e.g. integration income and

unemployment benefits) are the opposite of one another.

Source: Own creation based on Peña-Miguel, De la Peña Esteban, & Fernandez-Sainz, (2014,

p. 96).

18 | P a g e

The specifications of each basic income proposal, however, (e.g. the exact level of the basic

income, the precise target audience of basic income, whether basic income is

supplementary to the social protection system…) may differ across diverse basic income

proposals. The diversity of these particularities will be illustrated by a range of basic

income proposals, which are discussed in chapter 3 of the paper. (Melzochová & Špecián,

2015, p. 554-555)

The following section first elaborates on the arguments for basic income on European soil

and proceeds by zooming in on the basic income debate in Belgium.

2.2 Basic income in Europe

The current topical reappearance of basic income in Europe, according to Soininvaara

(2000, p. 7-8), is thanks to the solutions offered by basic income in order to overcome two

obstacles faced by the present European welfare systems.

2.2.1 The two obstacles

The first obstacle is the trend of growing structural unemployment with the unskilled

struggling to obtain a job due to a mismatch between labor demand and supply

(Soininvaara, 2000, p.8) (C.W., 2014). This trend has already been occurring in advanced

economies for a number of decades and is expected to continue growing in the future due

to the threat that evolving technology poses for low-skilled jobs (C.W., 2014; Rotman,

2013). The long-term unemployment rates in Figure 2 suggest that especially Europe (EU-

28) seems to be greatly affected, with the EU-28 average being consistently higher than the

OECD average, which in turn is consistently higher than the rates of the United States for

the time span of 2000 to 2015 (OECD, 2016a). Belgium is no exception and seems to suffer

from long-term unemployment rates even higher than the EU-28 average (OECD, 2016a).

High long-term unemployment rates are problematic for various reasons. Besides being an

indicator of inefficient operating labor markets, long-term unemployed individuals are

19 | P a g e

shown “to have poorer health than average [due to mental and material stress] and [these

high rates] squeeze the social security budgets” (C.W., 2014). (OECD, 2016a)

Additional to having a greater percentage of long-term unemployed, Europe bears high

unemployment rates relative to the rest of the OECD and the United States. This is shown in

Figure 3. Note that although the current trend of the European Union is strongly influenced

by the extremely high unemployment rates of Greece and Spain, with respective

unemployment rates being 24.9% and 22.06% in 2015, all countries belonging to the

European Union are in all cases, except for two member states being Germany and the

Figure 2: Long-term unemployment rate, total % of unemployed, 2000 – 2015

Note: “The long-term unemployment rate refers to the proportion of people who have been

unemployed for 12 months or more among all unemployed” (OECD, 2016a).While the indicator itself

is relevant, it may also be considered as a proxy for structural unemployment as there is a tendency

of long-term unemployment turning into structural unemployment (C.W., 2014).

Source: OECD, (2016a).

20 | P a g e

Czech Republic, higher than those of the United States in 2015 (figure not shown). For the

specific case of Belgium, the unemployment rates have been fluctuating around 8% for the

past decade, with a percentage of 8.48 in 2015. (OECD, 2016b)

High levels of unemployment translate to low incomes on the unemployed which in turn

leads to an increased level of government spending on social benefits and decreased tax

revenues (Eurostat, 2016a). The unemployment rates and its effect on the government

revenues, the main source of funding basic income, through personal income taxes form an

important aspect of financing basic income. Although this aspect is beyond the paper, an

assessment thereof is recommended for further research.

Figure 3: Unemployment rate, total % of labor force, 2000 - 2015

Note: “The unemployment rate is the number of unemployed people as a percentage of the labor

force. The labor force consists of the unemployed plus those in paid or self-employment” (OECD,

2016b).

Source: OECD, (2016b).

21 | P a g e

The second obstacle lies in the incompatibility between incentives to enter the labor

market and conditions attached to unemployment benefits (Soininvaara, 2000, p. 8). “The

social income transfers in the European systems [are namely] diminishing as earned

income rises” (Soininvaara, 2000, p.8) with the typical dis-incentivizing outcome of

individuals losing these benefits completely when joining the workforce. In the Belgian

labor market, individuals who are unwillingly unemployed and fulfill the minimum amount

of days of paid employment have the right to request an unemployment benefit (RVA,

2015; Vlaanderen, n.d. b). The level of the unemployment benefit received is again of

conditional nature as it depends on the individual’s household situation, the individual’s

most recent paycheck, their employment history and the duration of unemployment due to

the benefits being of digressive nature (RVA, 2016). In this case, the mismatch is reflected

by receiving a lower level of unemployment benefits if the individual belongs to a

household in which their partner has income and the complete loss of unemployment

benefits when obtaining a job (RVA, 2016).

2.2.2 Overcoming the obstacles

Basic income provides a solution in order to overcome both these obstacles and is the

reason why basic income has received much attention in Europe (Soininvaara, 2000, p. 7-

9).

First, basic income alleviates the problem of high unemployment rates not by decreasing

these rates but rather by offering the unemployed a wider scope of opportunities. Van

Parijs (2004, p. 17-21), a well-known Belgian proponent of basic income, argues that basic

income enables individuals to comfortably look for a desirable job corresponding to their

capabilities and preferences, perhaps, more importantly, it also stimulates

entrepreneurship due to lower failure anxiety, encourages individuals to engage in training

and sharpen their existing skillset, facilitating the possibility to “take a break between two

jobs and reducing working time” (Van Parijs, 2004, p.19). This reduction in working time,

in turn, will allow individuals to dedicate themselves to academic research, volunteer work,

domestic work and charity. Furthermore, proponents argue that basic income empowers

22 | P a g e

the position of employees in negotiations leading to improved working conditions.

(Melzochová & Špeciána, 2015, p. 551-552)

Second, basic income is expected to eliminate the disincentives to work as unlike with

unemployment benefits, individuals do not lose this guaranteed income when deciding to

join the workforce. Basic income detaches the relationship between the amount of support

and the earned income. (Soininvaara, 2000, p. 8)

2.2.3 The administrative efficiency argument

Next to these policy-oriented arguments for basic income, the argument of basic income

emancipating the poor, and the classic ethical argument by Van Parijs (1995) of basic

income ensuring “real freedom for all”, there is another argument which is of particular

interest when considering the financial feasibility of basic income: the efficiency

implications brought forward by the characteristics of basic income. (Melzochová &

Špeciána, 2015, p. 551; Soininvaara, 2000, p. 8)

As basic income is unconditional without a means-test or work requirement, proponents

argue that basic income economizes on administration costs compared to other income

support schemes: there is no longer a need to verify whether an individual is eligible for

income support or not and there is no urge of cheating under the scheme of basic income. It

goes without saying that the more complex the initial social protection system set in place

is, the more savings that accumulate on administration costs when substituting the former

system by a simplified and more transparent scheme of basic income. This is a significant

argument in the European context considering how the social safety net in advanced

economies, such as in Western Europe and the Scandinavian countries, has grown into a

complex construct. However, while basic income may be more administratively efficient in

comparison to conditional income support schemes, the extent of its efficiency should be

still put under scrutiny. (De Wispelaere & Stirton, 2011, p. 115-116, p. 125-126;

Melzochová & Špeciána, 2015, p. 551)

23 | P a g e

Overall, the two aforementioned obstacles and the complexity of the social safety net faced

by Europe are also concerns shared by Belgium: Belgium had an unemployment rate of

8.48% in 2015 and 51.7% of those individuals were unemployed for longer than twelve

months (OECD, 2016a; OECD, 2016b). Furthermore, Belgium is known to have a very

elaborate social security net (Belgium, n.d. a). This makes Belgium ripe for considering

basic income. The next section focuses on the academic and political attention that basic

income has received in Belgium.

2.3 Basic income in Belgium

In Belgium, the topic of basic income first emerged in academic and intellectual circles,

before receiving attention in the field of politics. (Vanderborght, 2000, p. 277)

Among the Belgian scholars who have delved into basic income, Philippe Van Parijs stands

out the most, being a firm proponent of basic income and one of the founders of Basic

Income Earth Network (BIEN, n.d. b). Van Parijs (1995) is especially known for his book

“Real Freedom For All”, in which he argues that capitalism has introduced inequalities in

our society which he deems as unacceptable. To fight against these inequalities, Van Parijs

places freedom on a pedestal and specifically advocates for “real-libertarianism, or real-

freedom-for-all”, which is different from formal freedom as he describes “real freedom not

only [being] a matter of having the right to do what one might want to do, but also a matter

of having the means for doing it” (Van Parijs, 1995, p.4). Van Parijs further argues that the

regime which best incorporates this type of freedom is “the highest sustainable

unconditional income”(Van Parijs, 1995, p.30), with the level of basic income set

sufficiently high to guarantee the means to put an end to the inequalities imposed by

capitalism and ensure real freedom.

In politics, there is a division of proponents versus opponents of basic income not only

between political parties and labor unions but also between individuals within a single

party or union. (Evenepoel, 2016)

24 | P a g e

First, regarding the political parties, there are currently only two Belgian small-scale

political parties of which the members have collectively agreed to explicitly take up basic

income in their program: Piratenpartij and B.U.B. (Belgische Unie – Union Belge) (B.U.B.,

2016; Piratenpartij, 2014). Other parties who have supported basic income in the past are

Vivant and two green parties, ECOLO and AGALEV (Vanderborght, 2000). Furthermore, a

number of individuals belonging to the well-known parties, Open VLD and sp.a, have shown

interest in the radical proposal, although their personal interest does not necessarily

correspond to their affiliation (Cornillie & Kherbache, 2016; “Open VLD: Basisinkomen”

2015).

Piratenpartij (2014, p. 19, own translation) contended through their program of 2014 that

“labor should be more than just a mean to obtain income, and should instead primarily

contribute to the self-realization of individuals”. Piratenpartij pleads for basic income as

the long-term solution towards achieving that goal. “As a first step, the party implores an

assessment of the feasibility of implementing and financing basic income on European and

Belgian soil while accounting for the administrative efficiency brought upon by

bureaucratic simplification” (Piratenpartij, 2014, p. 19, own translation).

The party urging for a unified Belgium, B.U.B. (2016, p.10), is a supporter of basic income in

order to guarantee an equal treatment of all Belgians. They propose a scheme of basic

income at a subsistence level of €800 per month, which is to be implemented as a complete

substitute for existing social benefits. Similar to Piratenpartij, B.U.B. emphasizes the

administrative efficiency argument as a method of partially financing basic income, which

is maximized by abolishing the current social protection system. The basic income proposal

by B.U.B. is one of the proposals of which I will assess the costs.

“The green parties ECOLO and AGALEV supported basic income since the mid-1980s.

Compared to ECOLO who considered basic income as a medium-term objective more

belonging to the theoretical horizon than a policy proposal, the support by AGALEV was

more outspoken as it was promoted as a short-term reform” (Vanderborght, 2000, p.276).

The parties’ resolute support, however, is a remnant of the past. Groen left the name of its

25 | P a g e

predecessor AGALEV behind with the idea of basic income in 2003 (Groen, n.d.; Llc, 2003).

In comparison with AGALEV’s commitment to basic income, today Groen (n.d.) merely

labels basic income as an interesting proposal worth exploring on the long-term. For the

case of ECOLO, the already limited presence of basic income seems like it will further

disappear into the background as the idea was mainly upheld by the economist Philippe

Defeyt who recently retired in March 2016 (Dupriez & Khattabi, 2016). The resolute

proponent of basic income, however, is still going strong as he independently released a

concrete basic income proposal as of June 2016 (Van Horenbeek & Wauters, 2016). A cost

estimation of his proposal will be provided.

Vivant, although currently retired from the political scene, is a unique party with a sole

focus on basic income. The basic income proposal made public by Vivant is well-developed

compared to its counterparts and will therefore be elaborated upon next to other basic

income proposals, such as those by B.U.B. and Defeyt. (Vanderborght, 2000; Vivant, n.d.)

Notable individuals who have shown their interest for basic income and are requesting for

a thorough investigation are, but not limited to, Nele Lijnen, federal parliament member of

Open VLD, Yasmine Kherbache, Flemish parliament member of sp.a, Jan Cornillie, director

of the research affiliation of sp.a, and Karel Van Eetvelt, the managing director of an

Špecián, 2015, p. 555-556; Statistics Belgium, n.d.; and own calculations)

Table 3: The B.U.B. proposal, Belgium, 2010

Scheme Monthly cash grant (€)

Adults / Minors

Yearly expenditures

(million €)

Cost comparison

(BI scheme as % of present social protection

expenditures)

Social integration

income

730.63 / 0 75,627 80.24

Poverty threshold

973.20 / 0 100,735 106.88

Breakeven 910.52 / 0 94,247 100

Source: Own creation based on Melzochová & Špecián, (2015, p. 555-556), B.U.B. (2016, p.

10), and my own calculations.

44 | P a g e

In this basic income scheme, everybody would receive the same sum and would thus be

treated equally, irrespective of their gender, race, household situation, status of

employment… However, is it truly appropriate to simply grant everyone the same amount

of money? In other words, is it socially desirable and correct to treat two different

individuals, say a healthy person and a disabled person, one and the same? The answer is

undeniably no. Following the wisdom of Amartya Sen’s capability approach, I am convinced

that one of the motives of basic income should be not to equalize the functionings, which

are “certain beings and doings that together constitute what makes a life valuable”

(Robeyns, 2011), but to respect the choice of the individual and instead equalize

capabilities, which are “a person’s real freedoms or opportunities to achieve functionings”

(Robeyns, 2011) (Odekon, 2015, p. 513). For example, if both a healthy person and a

disabled person were to be given the same amount of resources, e.g. the same level of basic

income, with these given resources the healthy person would be able to achieve more

functionings than a disabled person. In order to equalize the capabilities between the two

individuals, it is necessary to divert more resources to the disabled person and thus grant

the people who are most vulnerable in society a higher level of basic income. The current

social protection system acknowledges this and therefore diverts resources to the

vulnerable social groups, such as the sick, the disabled, the unwillingly unemployed and the

old. Thus while the basic income scheme by B.U.B. might be a system in which we treat

everyone equally, it is not the most equitable system. Furthermore, the basic-income-to-

substitute-everything scheme might be the most financially feasible, but again it is not the

most socially desirable system. We should thus strive for a basic income scheme that is

socially desirable yet financially feasible, a scheme which accommodates an equality of

opportunities. For this reason, many supporters push for basic income schemes which are

partially complementary to the social protection system. This is especially the case if basic

income is not at a sustainable level. (Van Parijs, 2004, p. 14)

45 | P a g e

In addition, I would like to draw attention to the fact that there exists a trade-off between

financial feasibility and social desirability. Basic income schemes that incorporate the

ethical principles of the social protection system by granting the socially vulnerable groups

a higher level of basic income, is socially desirable but leads to higher costs. The higher

costs are explained by two reasons.

First, the fact that a selective number of individuals receive a higher level of basic income

without changing the level of basic income for the remainder population evidently

increases the cost compared to the case in which everyone receives an equal level of basic

income. Naturally, a cost-reducing measure would be to decrease the level of basic income

for the remainder of the population. Alternatively, one can reduce the current levels of the

maintained social benefits for vulnerable social groups (Groot, 2004, p. 14) or subject the

social benefits to a ceiling which they may not exceed. (Defeyt, 2016)

Second, there is an opposition between basic income schemes which are substitutable and

basic income schemes which are complementary to the social protection system. While the

former basic income scheme incorporates the aspect of ‘unconditionality’, the latter basic

income scheme re-introduces ‘conditionality’ due to the need to verify whether the

individual in question meets the conditions to acquire a higher level of basic income, as

currently is the case with the social protection system. The latter basic income scheme has

higher administration costs because the efficiency gains on administration can no longer be

maximized as these are the result of a basic income scheme which is purely unconditional.

Possible cost-reducing measures in this regard would be to keep “conditional transfers in

simplified forms” (Groot, 2004, p. 14). (De Wispelaere & Stirton, 2011)

Overall, finding the balance between financial feasibility and social desirability brings us to

the following basic income proposals, which are more complex, more ethical, but also more

challenging to finance.

46 | P a g e

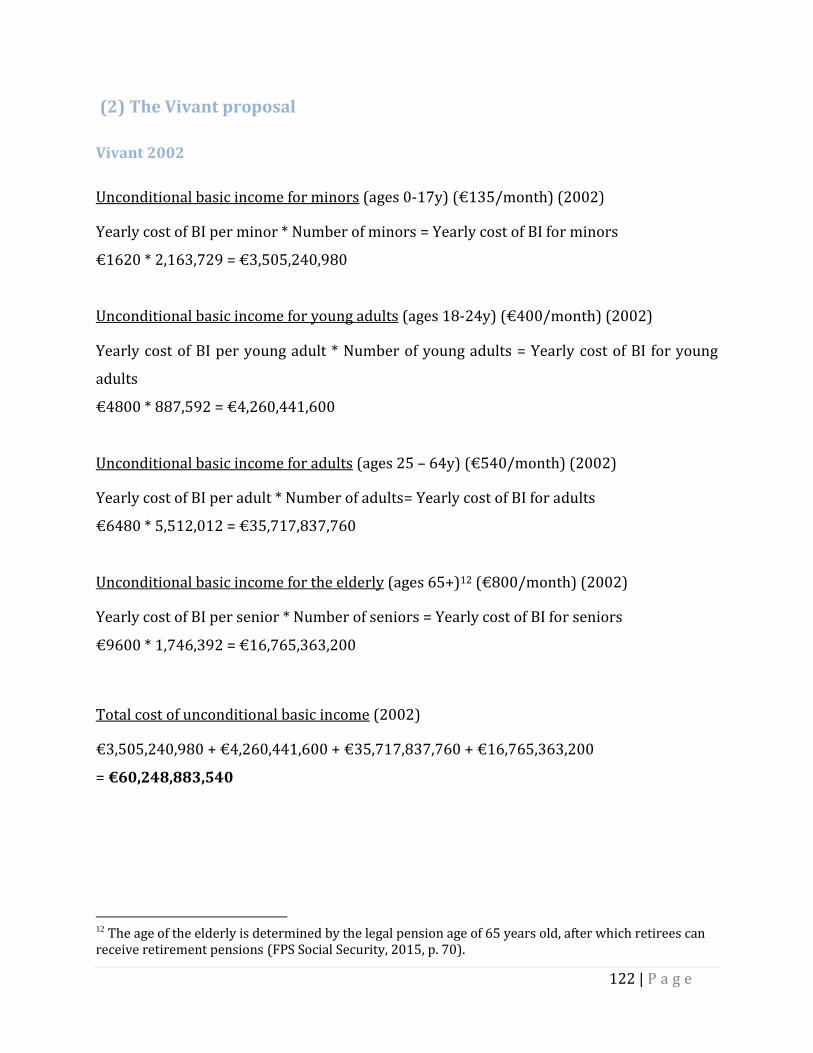

3.4.2 The Vivant proposal

The basic income proposal by Vivant (n.d.) can be to a large extent considered as a ‘basic-

income-to-substitute-everything’ scheme (Melzochová & Špeciána, 2015, p. 554-555). The

political party proposes basic income as a substitute for currently existing social benefits,

such as “retirement pensions, unemployment benefits, the social integration income, family

benefits, scholarships, compensations for career interruption, …”(Vivant, n.d., p. 8, own

translation). There are, however, two crucial aspects that differentiate Vivant’s proposal

from the pure basic-income-to-substitute-everything scheme of B.U.B. (2016, p. 10).

First, Vivant (n.d., p. 42) introduced a diversified basic income scheme with the levels of

basic income increasing throughout the four different age categories. The suggested

monthly levels of basic income for the year 2002 (2010) were €135 (€163) for minors,

€400 (€482) for young adults, €540 (€651) for adults, and €800 (€964) for seniors. In

total, the basic income proposal would cost €60 billion (€77 billion). This diversified basic

income scheme is opposed to the uniform basic income scheme by B.U.B. (2016, p. 10) that

grants every Belgian adult an equal amount of basic income.

Second, while B.U.B. (2016, p. 10) replaces health care and other social benefits by basic

income, Vivant (n.d., p. 9) believes that health care should be maintained and health

insurance should become unconditional just as basic income. According to the political

party, the persons who currently do not receive health care are limited in number and the

implied additional costs are modest compared to the current budget of health care. Vivant

further argues that the administration costs will decrease greatly by modifying the

conditional health insurance to one that is unconditional, as there is no longer a need to

verify whether an individual has the right to health care. As a result, Vivant suggests that

the cost savings should even out the extra implied costs, bringing about heath care

expenditures that are unchanged in level. Assuming Vivant’s suggestion is correct, the cost

of health care would remain at €23 billion for the year 2010. (Vivant, n.d., p. 9)

47 | P a g e

These two aspects contribute to the social desirability of Vivant’s basic income proposal.

The diversified basic income scheme across the different age categories provides seniors a

higher level of basic income as it substitutes their retirement pensions. Minors are also

given a basic income of which the level is approximated by the level of family benefits.

Furthermore, young adults receive a level of basic income, which is less than of adults but

more than of minors, that allows them to pursue higher education. Lastly, the sick are

protected thanks to unconditional health insurance. (Vivant, n.d. p. 7-24)

Table 4: The Vivant proposal, Belgium, 2002 and 2010

Scheme Monthly cash grant (€)

Minors / Young adults

Adults / Elderly

Yearly expenditures

(million €)

Cost comparison

(BI scheme as % of present social protection

expenditures)

Unconditional basic income

(2002)

135 / 400

540 / 800

60,249 N.A.

Unconditional basic income

(2010)

162.65 / 481.93

650.63 / 963.85

76,776 81.46

Health care

(2010)

N.A. 22,827 24.22

Basic income proposal and health care

(2010)

N.A.

99,603

105.68

Note: The dataset provided by FOD Sociale Zekerheid (2011, 2012, 2013) does not cover the year 2002,

thus no cost comparison is made for this year. I refrained myself from using data on social protection

expenditures provided by other sources as there is a wide diversity of which social categories are to be

included and which not.

Source: Own creation based on Melzochová & Špecián, (2015, p. 555-556), Vivant (n.d.),

and my own calculations.

48 | P a g e

In total, Vivant’s basic income proposal and unconditional system of health care would cost

€100 billion for the year 2010. The costs of Vivant’s proposal would exceed the social

protection expenditures by €5 billion (5.68%). At a first glance, the proposal by Vivant can

be thus considered as one that is financially feasible if their proposal were to replace the

social protection system of Belgium and if additional funds are sought for the remaining €5

billion. An overview of the preceding costs and cost comparisons is given in Table 4. (FOD

Sociale Zekerheid, 2011, 2012, 2013; Vivant, n.d.; and own calculations)

Lastly, I would like to make two remarks. First, I have only presented what Vivant had

planned regarding the basic income scheme and the social protection system. Vivant’s

political proposal, however, includes more policy proposals, such as a reform of the labor

market. Second, Vivant’s basic income proposal also includes a transition phase that

imposes different costs in comparison to the final phase. During this transition phase,

recipients should be able to retain their benefits if the level thereof is higher than the level

of basic income. The transition phase plays an important role for the political feasibility:

with basic income being a radical reform in comparison to the existing social protection

system, it cannot be simply implemented overnight. Implementing such a phase smoothens

the transition from the current social protection system to a scheme of basic income,

allowing for the people to adjust and thus leading to higher political feasibility. The costs

from this transition phase will not be considered. However, as will be seen in the upcoming

basic income proposals, the basic income proposal by Raventos et al. is comparable to the

transition phase of Vivant, thus we will still have an idea of the temporary high costs of

such a transition phase. But overall to simplify the analysis I have only addressed the cost

implications of the final phase. (Melzochová & Špecián, 2015, p. 553-554; Vivant, n.d., p.7-

18)

49 | P a g e

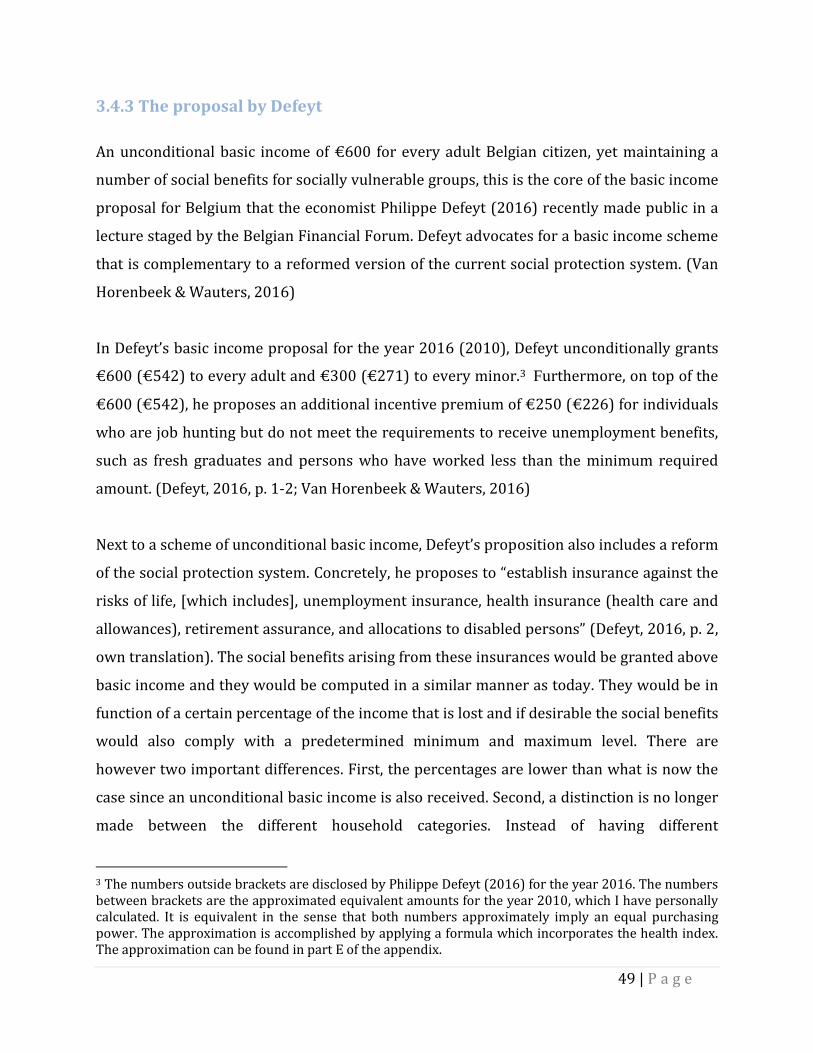

3.4.3 The proposal by Defeyt

An unconditional basic income of €600 for every adult Belgian citizen, yet maintaining a

number of social benefits for socially vulnerable groups, this is the core of the basic income

proposal for Belgium that the economist Philippe Defeyt (2016) recently made public in a

lecture staged by the Belgian Financial Forum. Defeyt advocates for a basic income scheme

that is complementary to a reformed version of the current social protection system. (Van

Horenbeek & Wauters, 2016)

In Defeyt’s basic income proposal for the year 2016 (2010), Defeyt unconditionally grants

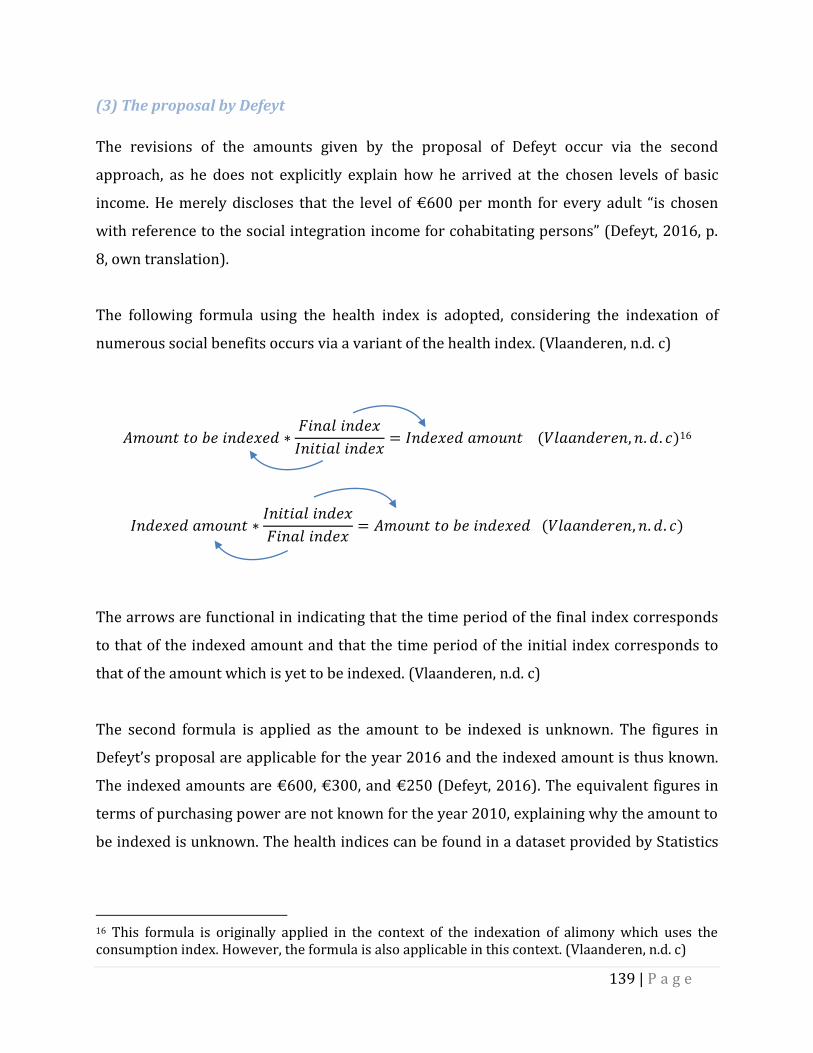

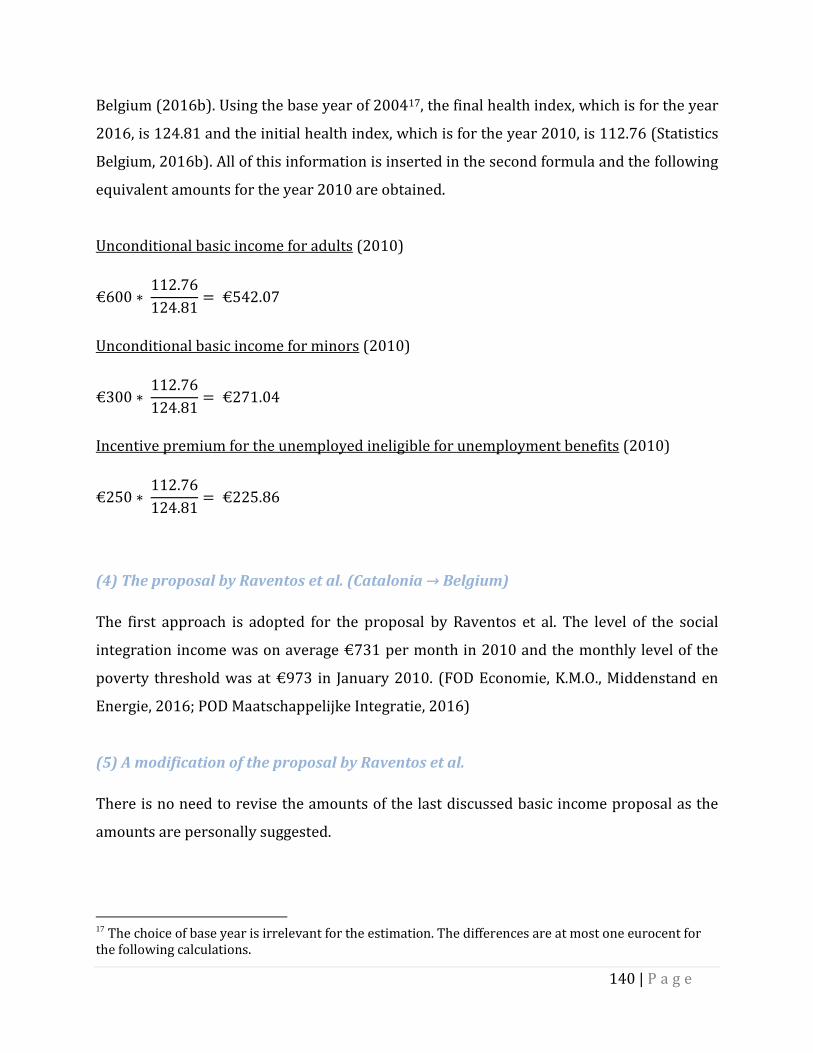

€600 (€542) to every adult and €300 (€271) to every minor.3 Furthermore, on top of the

€600 (€542), he proposes an additional incentive premium of €250 (€226) for individuals

who are job hunting but do not meet the requirements to receive unemployment benefits,

such as fresh graduates and persons who have worked less than the minimum required

amount. (Defeyt, 2016, p. 1-2; Van Horenbeek & Wauters, 2016)

Next to a scheme of unconditional basic income, Defeyt’s proposition also includes a reform

of the social protection system. Concretely, he proposes to “establish insurance against the

risks of life, [which includes], unemployment insurance, health insurance (health care and

allowances), retirement assurance, and allocations to disabled persons” (Defeyt, 2016, p. 2,

own translation). The social benefits arising from these insurances would be granted above

basic income and they would be computed in a similar manner as today. They would be in

function of a certain percentage of the income that is lost and if desirable the social benefits

would also comply with a predetermined minimum and maximum level. There are

however two important differences. First, the percentages are lower than what is now the

case since an unconditional basic income is also received. Second, a distinction is no longer

made between the different household categories. Instead of having different

3 The numbers outside brackets are disclosed by Philippe Defeyt (2016) for the year 2016. The numbers between brackets are the approximated equivalent amounts for the year 2010, which I have personally calculated. It is equivalent in the sense that both numbers approximately imply an equal purchasing power. The approximation is accomplished by applying a formula which incorporates the health index. The approximation can be found in part E of the appendix.

50 | P a g e

arrangements for cohabitants, single persons, and persons living together with a

dependent family, there will only remain a single arrangement which is strictly individual.

On a side note, Defeyt wishes to keep the current system of health care and allocations to

handicapped persons as they are. (Defeyt, 2016, p.2)

The unconditional basic income proposal by Defeyt would cost €73 billion in the year 2016

and €63 billion in the year 2010. The reformed social protection system is estimated at €30

billion by Defeyt for the year 2016.4 It is, however, unclear from his proposal whether

Defeyt includes the costs of health care in this estimation. I suspect that his estimate of €30

billion does not include health care as health care cost €23 billion and social benefits cost

€56 billion for the year 2010. That aside, in total, Defeyt’s proposal would cost about €103

billion for the year 2016. An overview of these costs is shown in Table 5. (Defeyt, 2016, p.

8)

Lastly, I would like to make a remark that the proposal by Defeyt is an excellent example of

a basic income proposal that attempts to find a balance between financial feasibility and

social desirability. The vulnerable social groups are protected in his proposal thanks to the

different types of insurances and remaining social benefits, which contributes to the social

desirability of the proposal. At the same time, Defeyt recognizes the increased costs of a

basic income proposal partially complementary to the social protection system. To

promote financial feasibility, he advocates for a lower level of basic income, lower levels of

social benefits, and a reform of the current social protection system. (Van Horenbeek &

Wauters, 2016)

4 Unfortunately, Defeyt (2016, p.8) does not provide calculations nor an exact description of how high the social benefits would be. He merely provides a total cost estimation for the reformed social protection system. For this reason, I cannot make a similar cost estimation of the remaining social benefits for the year 2010.

51 | P a g e

Table 5: The proposal by Defeyt, Belgium, 2010 and 2016

Scheme Monthly cash grant (€)

Adults / Minors

Yearly expenditures

(million €)

Cost comparison

(BI scheme as % of present social

protection expenditures)

Unconditional basic income as

specified by Defeyt

(2016)

600 / 300

72,901

N/A

Social protection system as

specified by Defeyt

(2016)

N/A ± 30,000* N/A

Basic income proposal and

remaining social protection system

(2016)

N/A ± 102,901 N/A

Unconditional basic income as

dictated by Defeyt

(2010)

542.07 / 271.04 63,311 67.18

Note: (1) As the year 2016 has yet come to pass, data on the social benefits have yet to be published.

There is therefore no cost comparison for the year 2016. (2) The figure with an asterisk is an estimation

provided by Defeyt (2016).

Source: Own creation based on Defeyt (2016), Melzochová & Špecián, (2015, p. 555-556),

and my own calculations.

52 | P a g e

3.4.4 The proposal by Raventos et al.

The last basic income proposal to be considered is by Raventos and his co-authors,

Arcarons and Torrens, for the territory of Catalonia in the year 2010 (Arcarons, Raventos

Pañella & Torrens Mèlich, 2014). Their proposal is an example of a basic income scheme

that lies closely to the extreme ‘basic-income-purely-as-a-complement scheme’

(Melzochová & Špecián, (2015, p. 554-555), as there is an intertwining of the currently

existing social benefits and basic income. The following three points formulate how

existing social benefits are to be treated after an introduction of basic income.

“1.) Basic income replaces any existing public cash benefit of a lesser quantity.

“2.) When the public cash benefit is of a greater amount, the basic income must be topped

up to an equal quantity.

“3.) The basic income model allows for the financing of all extant services, such as health,

education, and all the others covered by public spending, as well the BI that is proposed

here.” (Arcarons, Raventos Pañella & Torrens Mèlich, 2014, p. 80)

Regarding the level of basic income, Raventos et al. grant a different amount to the minors

and the adults of Catalonia. In the first basic income scheme, the level of the Sufficient

Income Indicator for Catalonia was granted to adults (€664 per month) and a fifth of this

amount was granted to minors (€133 per month) for the year 2010 (Arcarons, Raventos

Pañella & Torrens Mèlich, 2014, p. 80-81). In the second basic income scheme, the

minimum wage was foreseen for adults (€451 per month), and minors were alternatively

allocated a basic income worth 100%, 50%, 30% of the basic income for adults for the year

2003 (Raventos, 2007, p. 158). As a general guideline, the authors suggest that the level of

basic income for adults should be above the poverty threshold (Arcarons, Raventos Pañella

& Torrens Mèlich, 2014, p. 80).

In the conditions of Belgium 2010, I will examine the proposal by Raventos et al. which

accords to the first proposed basic income scheme and which fulfills the three points

summed up earlier. Alternatively to the Sufficient Income Indicator for Catalonia, I will

examine the social integration income for Belgium, which can be considered as its Belgian

53 | P a g e

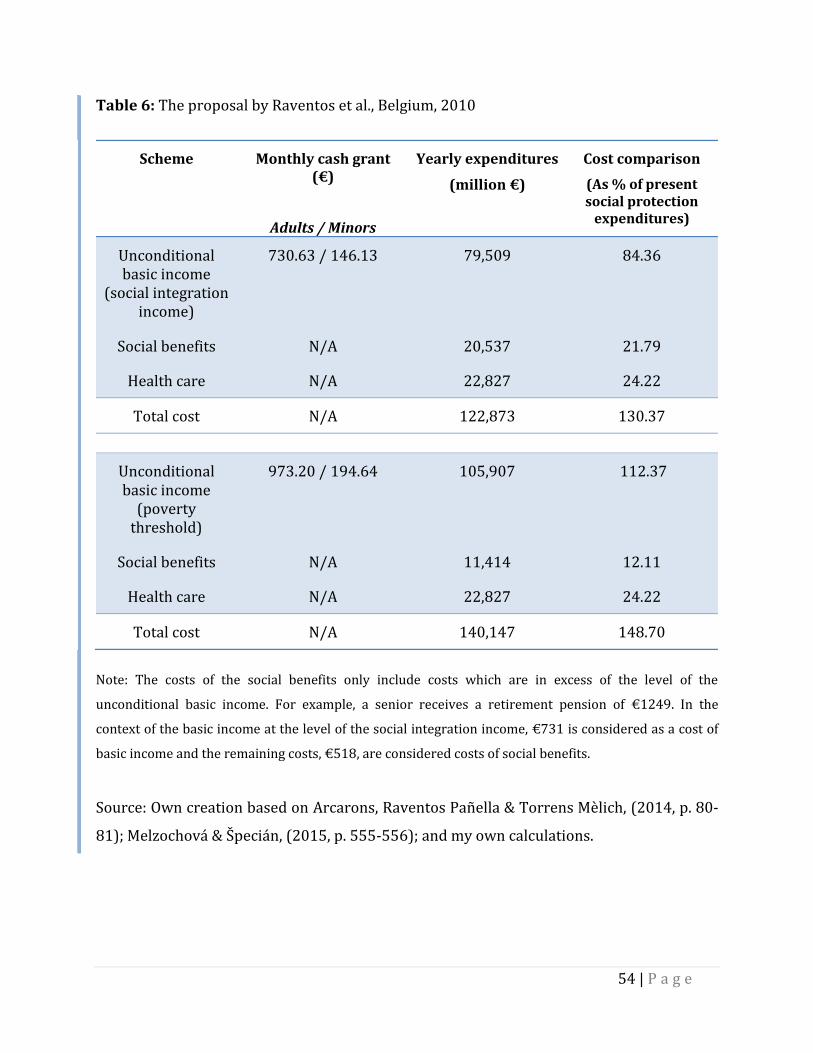

equivalent as this amount is supposed to be sufficiently high to guarantee a decent

existence (FPS Social Security, 2015, p. 155). The social integration income, however, is

consistently lower than the poverty threshold in Belgium. For this reason, I will also

consider the poverty threshold of Belgium 2010, as the guidelines by Raventos et al.

requires the level of basic income for adults to be at least as high as the poverty threshold

(Arcarons, Raventos Pañella & Torrens Mèlich, 2014, p. 80). Concretely, this brings about

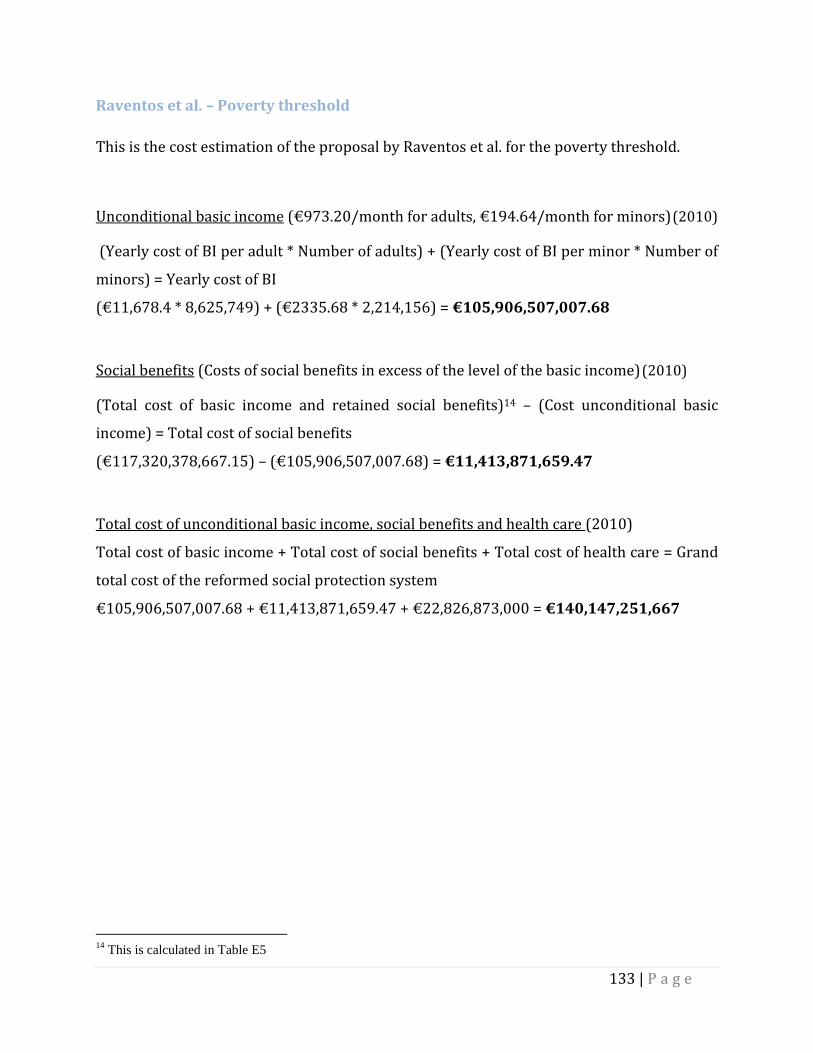

the following two basic income proposals for Belgium, 2010: (1) Basic income proposal by

Raventos et al. using the social integration income, €731 per month for adults and €146

per month for minors; (2) Basic income proposal by Raventos et al. using the poverty

threshold, €973 per month for adults and €195 per month for minors.

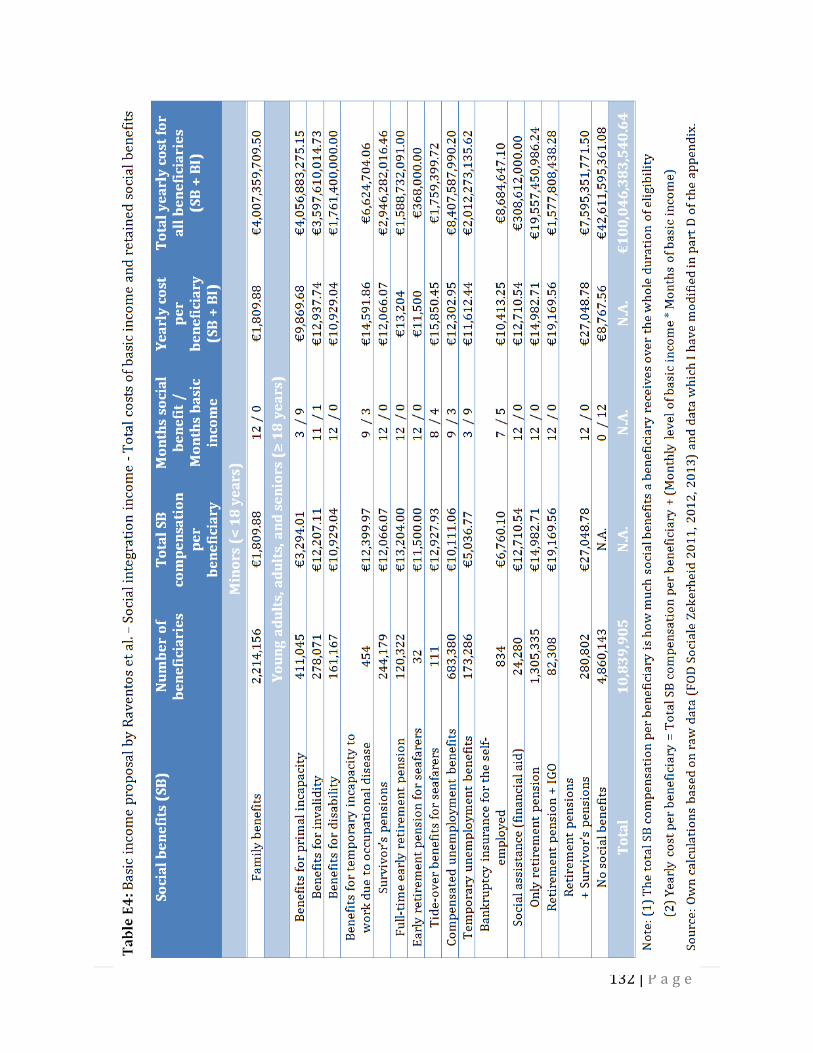

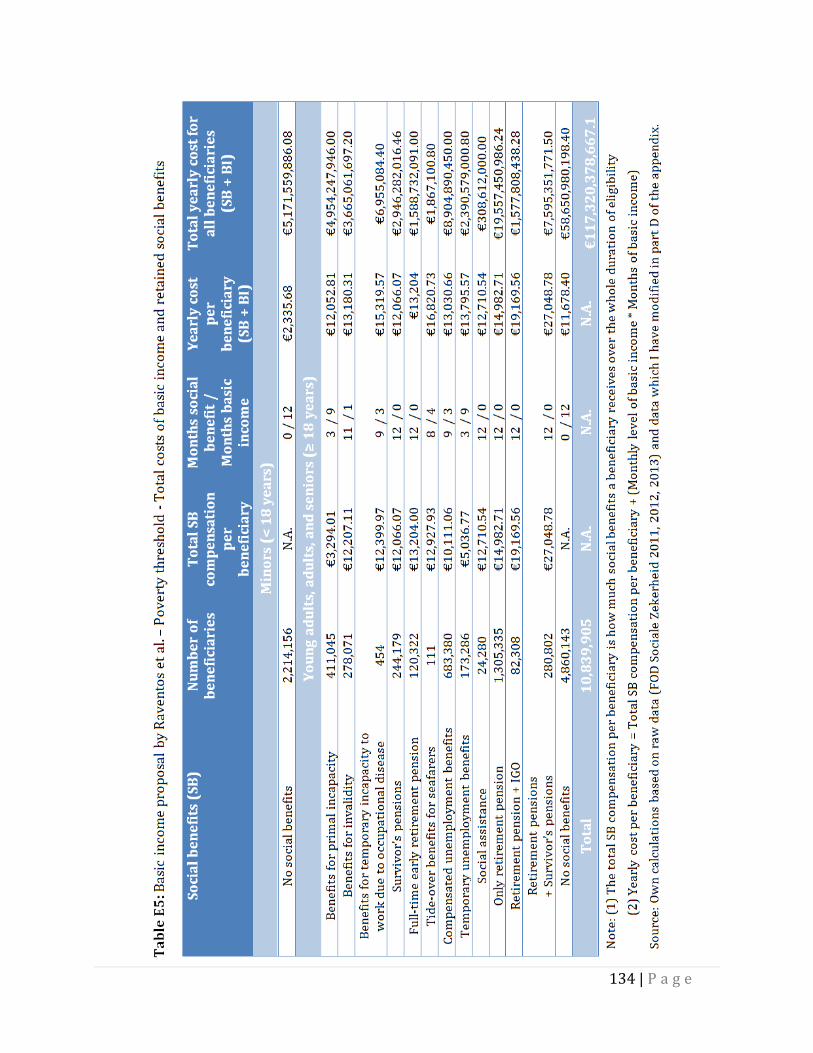

The cost estimation of both schemes is illustrated in Table 6. The unconditional basic

income alone would cost €80 billion for the first proposal and €106 billion for the second.

The retained social benefits, which exceed the level of basic income, are respectively

estimated at €21 billion and €11 billion. In total, including the costs of unconditional basic

income, the remaining social protection system, and health care, the implementation of the

proposal would require €123 billion for the basic income proposal using the social

integration income and €140 billion for the basic income proposal using the poverty

threshold. (FOD Economie, K.M.O., Middenstand en Energie, 2016; POD Maatschappelijke

Integratie, 2016; and Steunpunt tot bestrijding van armoede, bestaansonzekerheid en

sociale uitsluiting, 2016).

54 | P a g e

Table 6: The proposal by Raventos et al., Belgium, 2010

Scheme Monthly cash grant (€)

Adults / Minors

Yearly expenditures

(million €)

Cost comparison

(As % of present social protection

expenditures)

Unconditional basic income

(social integration income)

730.63 / 146.13

79,509

84.36

Social benefits N/A 20,537 21.79

Health care N/A 22,827 24.22

Total cost N/A 122,873 130.37

Unconditional basic income

(poverty threshold)

973.20 / 194.64

105,907

112.37

Social benefits N/A 11,414 12.11

Health care N/A 22,827 24.22

Total cost N/A 140,147 148.70

Note: The costs of the social benefits only include costs which are in excess of the level of the

unconditional basic income. For example, a senior receives a retirement pension of €1249. In the

context of the basic income at the level of the social integration income, €731 is considered as a cost of

basic income and the remaining costs, €518, are considered costs of social benefits.

Source: Own creation based on Arcarons, Raventos Pañella & Torrens Mèlich, (2014, p. 80-

81); Melzochová & Špecián, (2015, p. 555-556); and my own calculations.

55 | P a g e

The cost estimation of the basic income proposal by Raventos et al. is more complex than

the previously discussed proposals. The three points that were put forward by Raventos et

al., have an important implication on the cost estimation: a comparison between the level

of current social benefits and the level of basic income will become necessary to determine

which social benefits are retained and which social benefits are replaced by basic income.

Due to this additional technicality, based on information from part C of the appendix, I have

generated statistical figures that show the average (monthly, yearly) level of social benefits

per beneficiary in part D of the appendix, creating the data that is needed to make such a

comparison possible. A cost estimation of the basic income proposals by Raventos’ for the

year 2010 followed the comparison. To understand how the comparison and the cost

estimation of the basic income proposal by Raventos et al. were achieved, I recommend

consulting part E of the appendix. (Arcarons, Raventos Pañella & Torrens Mèlich, 2014)

The cost estimation that I provide of Raventos et al.’s proposal is innovative in two aspects.

First, the comparison preceding the cost estimation is of a comprehensive nature because

35 social benefits will be considered and not only the retirement pensions, as was done in a

cost estimation of Raventos’ proposal by Melzochová and Špecián (2015, p. 556) for the

Czech Republic. Furthermore, the extensive comparison is mandatory because in Belgium

many beneficiaries receive social benefits of which the levels tower over that of the social

integration income and the poverty threshold (FOD Sociale Zekerheid, 2011). Second, a

cost estimation of a basic income proposal which “replaces any existing public cash benefit

of a lesser quantity [and] is topped up to an equal quantity when the public cash benefit is

of a greater amount”(Arcarons, Raventos Pañella & Torrens Mèlich, 2014, p. 80) has not yet

been realized for Belgium. Cost estimations have been largely limited to proposals in which

basic income is seen as a stand-alone with respect to currently existing social benefits. One

exception is the basic income proposal by Defeyt (2016) as he urges for a basic income

scheme which co-exists with a reformed version of the social protection system. Defeyt,

however, does not provide calculations for the reformed social protections system, he

merely gives an estimate. Overall, the cost estimation of Raventos’ proposal for Belgium

will allow for an assessment of a basic income scheme that safeguards the existing social

Monnier & Vercellone, 2014, p. 71-73; and own calculations)

In order to assess the cost savings implied by the criterion provided by Raventos et al., a

comparison is necessary between the level of social benefits and the level of basic income.5

This comparison identifies which socials benefits are on average higher or lower than the

level of basic income. In order to make such a comparison possible, based on the dataset

provided by the FPS Social Security (FOD Sociale Zekerheid; 2011, 2012, 2013) (of which

an overview is shown in part C of the appendix), I calculated the average level for 35 social

benefits in part D of the appendix. After the comparison, an estimation of the cost savings

that are realized on the total cost of unconditional basic income (excluding the remaining

5 An elaborate explanation on how this comparison occurs can be found in part E of the appendix, under point (4), the proposal by Raventos et al. The comparison already took place in order to obtain cost estimations.

64 | P a g e

costs of social benefits and health care) can be calculated by the summation of (1) the total

expenditures on social benefits of which the average level is lower than the level of basic

income and (2) the summation of the following product for every social benefit of which

the average level is higher than the level of basic income: the product of the monthly level

of basic income level multiplied by the number of beneficiaries who receive the specific

social benefit which in turn is multiplied by the average number of months during which

this specific social benefit is received.6 The first part of the summation reflects the

complete replacement of social benefits by basic income and the second part reflects the

partial replacement of social benefits by basic income. Note that this calculation can be

considered as a general formula when only the cost of the universal basic income has been

calculated.

6 Note that the average number of months during which the social benefit is received differs between social benefits. This explains why the product should be calculated for each social benefit separately. The average number of months is also calculated in part D of the appendix.

Figure 12: Comparison of the cost savings and the grand total cost of the basic income

proposal by Raventos et al., in million euro, Belgium, 2010

Source: Own creation based on Arcarons, Raventos Pañella & Torrens Mèlich, (2014);

Defeyt (2016), FOD Sociale Zekerheid (2011, 2012, 2013), and my own calculations.

65 | P a g e

Concerning the modified version of Raventos et al. the implied cost savings are easier to

assess as the grand total cost estimation of basic income was calculated. The costs of social

benefits, the costs which are the result of social benefits in excess of the basic income level,

and the costs of health care additional to the costs of unconditional basic income are

included. As is illustrated in Figure 12, the cost savings of this grand total estimation (€114

billion) is €79 billion, the summation of the initial total expenditures of all social benefits

(€56 billion) and health care (€23 billion). The grand total cost estimation namely replaces

all costs of the initial social protection system. (Arcarons, Raventos Pañella & Torrens

Mèlich, 2014)

Alternatively, the cost savings realized on the cost of unconditional basic income (€66

billion), caused by an entire and partial replacement of social benefits, is €30 billion. This

can be calculated by the general formula aforementioned or it can be alternatively

calculated by the difference of the initial costs of social benefits (€56 billion) and the

remaining costs of social benefits under the basic income scheme (€25 billion), the costs

which are the result of social benefits in excess of the basic income level.7 Expressed in

percentages, the cost savings constitute 45% of the costs of unconditional basic income.

As concluded by Tirez (2014b, own translation), “the costs of basic income may be

enormous, but so are the savings”. The partial and complete replacement of social benefits

led to the realization of these significant cost savings. The remaining cost gap that has to be

financed is brought down to €36 billion.8

7 When the grand total cost estimation of basic income has already been calculated, this shortcut can be taken instead of the elaborate approach mentioned earlier. 8 Note that this cost gap is evidently equal for the ‘grand total cost of basic income’ and the total cost of

unconditional basic income. The cost gap is calculated as the following in million euro. (1) Grand total cost of basic income: Cost gap = 114,241 – 78,454 = 35,787 (2) Total cost of unconditional basic income: Cost gap = 66,091 – 30,304 = 35,787

66 | P a g e

3.5.3 Additional financing measures

The second step is to implement additional measures in order to finance the remaining cost

of €36 billion. A wide diversity of measures has been suggested by proponents of basic

income and there has been considerable progress of how basic income can be financed. Due

to a focus on providing improved estimations of basic income proposals and the implied

cost savings, a discussion of the diverse measures as well as a concrete assessment of how

the remaining cost gap can be financed is beyond the scope of my paper. However, I would

like to briefly discuss the administrative efficiency argument, which is brought up routinely

by proponents, and the tax-increasing measures, which are naturally considered the

primary measures in closing the cost gap. (Raventos, 2007)

Cost savings realized by administrative efficiency

Besides the cost savings realized by the replacement of social benefits, proponents of basic

income turn to cost savings which are the product of administration efficiency. As opposed

to social benefits which are conditional in nature, basic income is unconditional. Under

basic income, there is no longer the need to verify whether an individual is eligible or not,

leading to a simplification of the administration process. The extent of the cost savings,

however, depends on the one hand on the initial administrative (in)efficiency of the social

protection system and on the other hand on the implied efficiency of a specific basic income

proposal. (De Wispelaere & Stirton, 2011)

On the one hand, the Belgian social protection system is relatively inefficient in comparison

to a scheme of basic income mainly due to three reasons. First, the current responsibilities

of the social protection system are spread over the different government levels, varying

from the federal level to the three communities (Flemish, French, and German speaking)

and the Common Community Commission of the Brussels Capital Region (FPS Social

Security, 2015, p. 13). With the introduction of basic income, basic income can be simply

organized at the federal level. Second, the organization of the social protection system is

made possible by a significant number of institutions. There are currently 15 ‘central

institutions’ and these are only the “institutions that are responsible for one or more

67 | P a g e

branches of a specific system” (FOD Sociale Zekerheid, 2012, p. 59-61). There are thus

additional institutions, called ‘primary institutions’, which are responsible for the specific

branches. A scheme of basic income will lead to the replacement of many social benefits

and a number of these institutions will be made redundant as a consequence. Third, as

mentioned in part D of the appendix that is dedicated to an analysis of social benefits, there

exists a great variation in the level of social benefits due to a wide range of criteria due to

which the amount may differ. With basic income, these criteria are no longer enforced.

Overall, this leads to the insight that the efficiency gains are more significant if one were to

departure from an inefficient social protection system. (De Wispelaere & Stirton, 2011)

On the other hand, the implied efficiency of basic income depends on the type of basic

income scheme. Schemes of the type ‘basic-income-to-substitute-everything’ are naturally

more cost efficient than schemes leanings towards the type of ‘basic-income-purely-as-a-

complement’ (Melzochová & Špecián, 2015, p. 554). The cost efficiency namely depends on

how many social benefits are retained. For example, in the case of the proposal by Raventos

et al., there are efficiency gains due to the complete replacement of a number of social