Nordson Corporation August 21, 2017 | Fiscal 2017 3Q Results & 4Q Outlook : NDSN A premier industrial technology company focused on precision dispensing, fluid control and related processes Investor Presentation Nordson Corporation

Transcript

Nordson Corporation

August 21, 2017 | Fiscal 2017 3Q Results & 4Q Outlook

: NDSN

A premier industrial technology company

focused on precision dispensing, fluid

control and related processes

Investor Presentation

Nordson Corporation

2

Safe Harbor Statement Under the Private Securities

Litigation Reform Act of 1995

Information in this presentation may contain “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “projects,” or “potential” or the negative of these words and phrases or similar words or phrases which are predictions of or indicate future events or trends and which do not relate solely to historical matters.

All statements regarding our future performance, earnings projections, events or developments are forward-looking statements. These forward-looking statements are made based on known events and circumstances at the time of release, and as such, are subject in the future to unforeseen uncertainties and risks that could cause actual results to differ materially from those contained in any forward-looking statement. Such risks and uncertainties are described under “Risk Factors” in Item 1A of our annual report on Form 10-K and any updates to those factors set forth in our subsequent quarterly reports on Form 10-Q or current reports on Form 8-K. We make these statements as of the date of this disclosure, and undertake no obligation to update them unless otherwise required by law.

Nordson at a GlanceA premier industrial technology company focused on precision dispensing,

fluid control and related processes

3

Founded in 1954

FY16 sales = $1.8 billion

7,200 employees

Direct presence in 35+ countries

Best-in-class technology

Diversified, growing end markets

Market leading positions

Sustained financial performance

Outstanding long-term returns

Parts & Consumables

40%

Standard Product

39%

Engineered Systems

21%

4

USA29%

Americas7%

Europe28%

Japan7%

Asia Pacific29%

Product Type

High percentage of

recurring revenue

from parts and

consumables

Diversified Sources of RevenueFY2016 Profile - $1.8 billion

Industrial Coating

14%

Advanced Technology

37%

Adhesive Dispensing

49%

Consumer Non-Durables

38%

Consumer Durables

17%

Industrial6%

Automotive7%

Medical8%

Electronic Components

9%

Semiconductor6%

PCB Assembly9%

Geography

Very global. 71% of

revenue outside USA.

Direct presence in

nearly 40 countries.

Diverse End Markets

Consumer non-durables,

durables, industrial,

medical and technology

Operating Segments

Three segments with leading

product lines and brands

Investment Highlights

5

8%

CAGR

2011-2016

Strong

growth:

organic and

acquisitive

Excellent

operating

margins

Strong cash

returns to

shareholders

Reliable and

consistent

dividend

Outstanding

long term

Total

Shareholder

Returns

22%

Operating

Margin

Average

2011-2016

$1.1 billion

Share

repurchases &

dividends

2011-2016

53 Yearsof annual

increases

(21% payout

ratio in 2016)

$1.4 billion

101% of

net income

2011-2016

High level of

free cash

flow before

dividends

124%

TSR*

2011-2016

Outstanding

gross

margins

57%

Gross

Margin

Average

2011-2016

*((Share Price at 10/31/2016 – Share Price at 10/31/2011 + dividends) / Share Price at 10/31/2011 ) = (($100.13 - $46.37 + $3.81) / $46.37 ) = 1.24 = 124%

Assumes $100 invested on 11/1/2011, dividends reinvested, fiscal year ending 10/31/2016Source:

Why invest in Nordson?

7

Outstanding Culture and Values

Leading Global Businesses

Clear Strategy and Goals

Strong Execution and Performance

Numerous Growth Opportunities

Common Themes of our 2017-2022 Strategic Plan Continue to be a Premier Industrial Technology Company

Product innovation

New applications

Emerging markets

Recapitalize

installed base

Segmentation

Accelerate

organic

growth

Embed Nordson

Business System

Expand margins

Working capital

initiatives

Drive synergies

with acquisitions

Further

optimize our

business

Targeted spaces

Growth and

technology

Cultivate

proprietary deals

Execute and close

deals effectively

Disciplined pricing

Fast integration

Add key

acquisitions

Deepen bench

strength

Leadership

development

Rotational

assignments

Diversity

Enhance

and expand

organization

capability

Deliver top quartile total shareholder returns

Support our communities & good corporate citizenship

Revenue Operating Profit

2017-22 Strategic Plan TargetsFocused initiatives drive premium sales growth and expand profitability

~2x global GDP%

Outpace Revenue

Growth %

Underlying

Markets

Growth

Initiatives

Continuous

Improvement

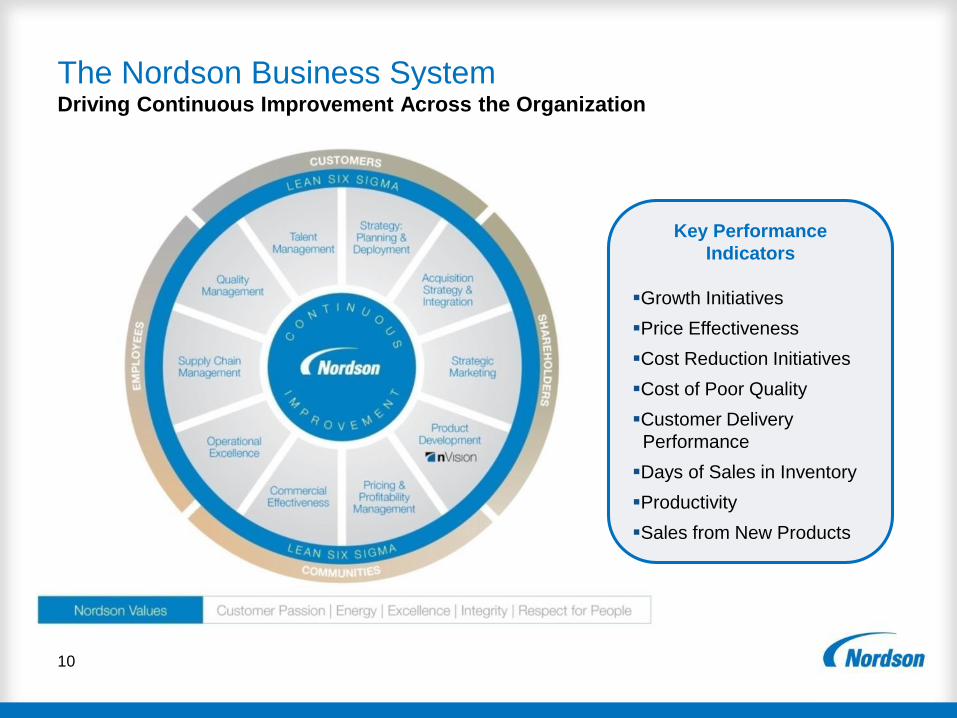

The Nordson Business System Driving Continuous Improvement Across the Organization

10

Key Performance

Indicators

Growth Initiatives

Price Effectiveness

Cost Reduction Initiatives

Cost of Poor Quality

Customer Delivery

Performance

Days of Sales in Inventory

Productivity

Sales from New Products

Why invest in Nordson?

11

Outstanding Culture and Values

Leading Global Businesses

Clear Strategy and Goals

Strong Execution and Performance

Numerous Growth Opportunities

0

300

600

900

1,200

1,500

1,800

2,100

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

0%

5%

10%

15%

20%

25%

30%

06 07 08 09* 10 11 12 13 14 15 16

12

Strong Top Line Growthorganic and acquisitive

0%

10%

20%

30%

40%

50%

60%

70%

06 07 08 09 10 11 12 13 14 15 16

Industry Leading Gross MarginsConsistently mid 50s and above

Mill

ions o

f $

Financial Highlights

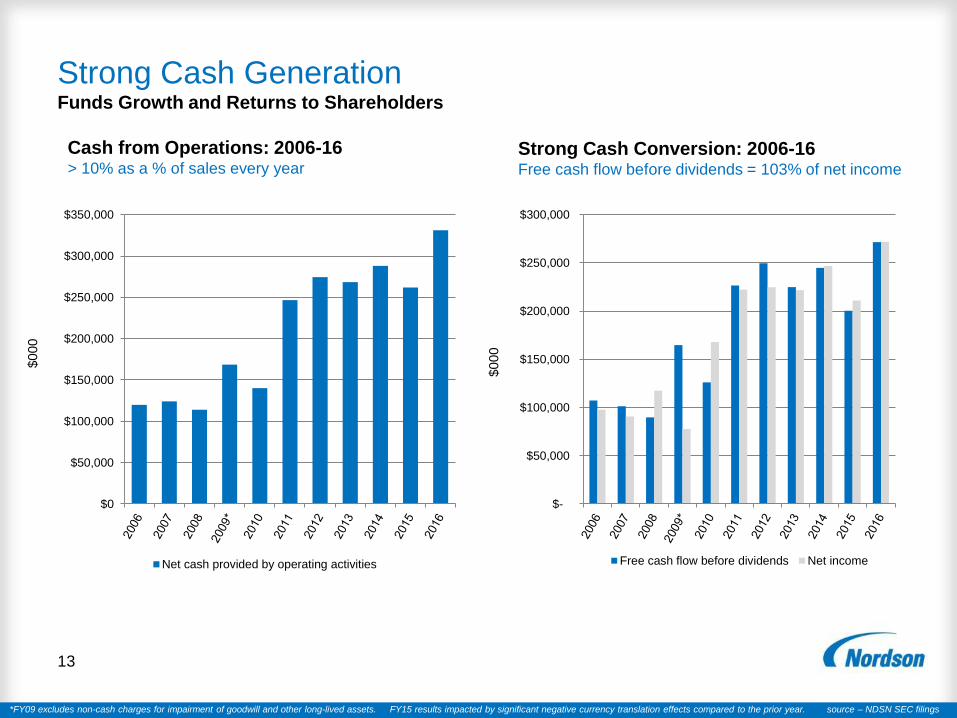

*FY09 excludes non-cash charges for impairment of goodwill and other long-lived assets. FY15 results impacted by significant negative currency translation effects compared to the prior year. source – NDSN SEC filings

Strong Cash Generation Funds Growth and Returns to Shareholders

13

Strong Cash Conversion: 2006-16Free cash flow before dividends = 103% of net income

Cash from Operations: 2006-16> 10% as a % of sales every year

$000

$000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

Net cash provided by operating activities

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Free cash flow before dividends Net income

*FY09 excludes non-cash charges for impairment of goodwill and other long-lived assets. FY15 results impacted by significant negative currency translation effects compared to the prior year. source – NDSN SEC filings

$24.8 $30.0

$49.2 $49.1 $66.7

$64.6

$284.4

$293.0

$441.7 $176.3

$186.4

$75.6

$42.7

$1,215.7

$29.8

$33.8

$40.5

$48.4

$54.8

$56.4

$263.7

$138.0

$88.5 $33.4

$166.4

$383.9

$33.4 $843.6

$28.5 $20.2 $25.8 $40.6 $37.7

$21.3 $174.1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 TOTAL

Disciplined Capital Deployment

14

PP&E/Leases

10%

Acquisitions

44%

Dividends

10%

Share Repur.

30%

Working Cap.

6%

40% or $1.1 billion

to shareholders via share repurchases

and dividends

Self funding business model generates excess cash

Low Working Capital Requirements

Low Capital Expenditures (approx. 3% of sales)

Strong free cash

54 consecutive years of dividend increases - 14th among publicly traded companies

$ millions

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

15

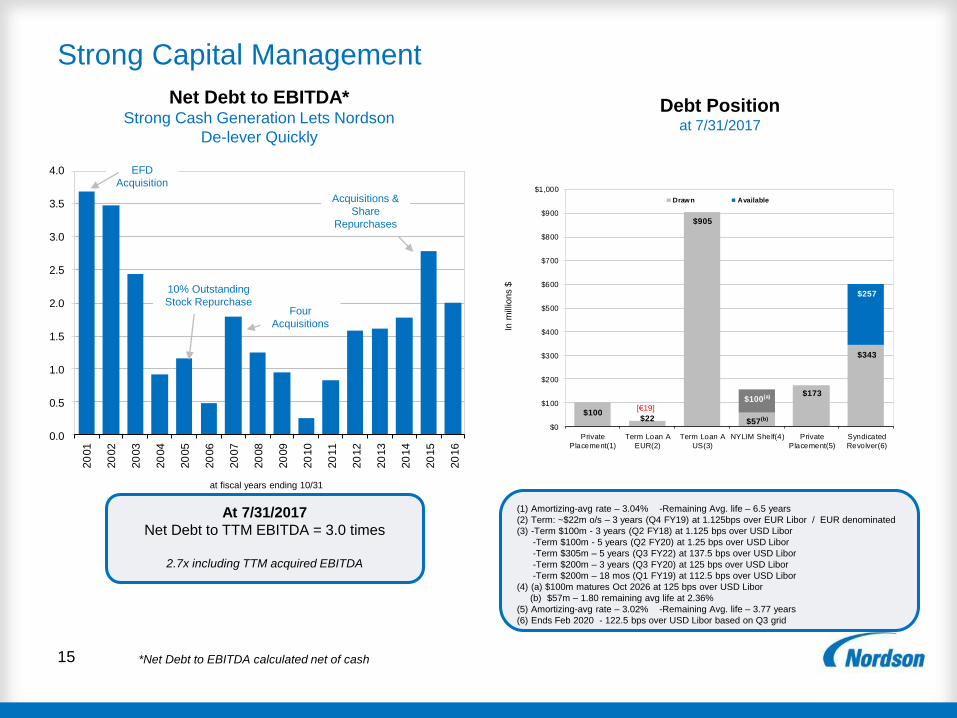

Strong Capital Management

Four

Acquisitions

10% Outstanding

Stock Repurchase

$100$22

$905

$57(b)

$173

$343

$100(a)

$257

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

Private

Placement(1)

Term Loan A

EUR(2)

Term Loan A

US(3)

NYLIM Shelf(4) Private

Placement(5)

Syndicated

Revolver(6)

Drawn Available

Net Debt to EBITDA*Strong Cash Generation Lets Nordson

De-lever Quickly

EFD

Acquisition

*Net Debt to EBITDA calculated net of cash

In m

illio

ns $

Acquisitions &

Share

Repurchases

at fiscal years ending 10/31

Debt Positionat 7/31/2017

[€19]

At 7/31/2017

Net Debt to TTM EBITDA = 3.0 times

2.7x including TTM acquired EBITDA

(1) Amortizing-avg rate – 3.04% -Remaining Avg. life – 6.5 years

(2) Term: ~$22m o/s – 3 years (Q4 FY19) at 1.125bps over EUR Libor / EUR denominated

(3) -Term $100m - 3 years (Q2 FY18) at 1.125 bps over USD Libor

-Term $100m - 5 years (Q2 FY20) at 1.25 bps over USD Libor

-Term $305m – 5 years (Q3 FY22) at 137.5 bps over USD Libor

-Term $200m – 3 years (Q3 FY20) at 125 bps over USD Libor

-Term $200m – 18 mos (Q1 FY19) at 112.5 bps over USD Libor

(4) (a) $100m matures Oct 2026 at 125 bps over USD Libor

(b) $57m – 1.80 remaining avg life at 2.36%

(5) Amortizing-avg rate – 3.02% -Remaining Avg. life – 3.77 years

(6) Ends Feb 2020 - 122.5 bps over USD Libor based on Q3 grid

Fiscal Year 2017 3Q Results and 4Q Guidanceas reported in August 21-22, 2017 press release and webcast

16

Nordson Corporation Reports Record Quarterly Revenue, Operating Profit, Diluted EPS

and EBITDA in Third Quarter of Fiscal Year 2017

Sales increase 20 percent from prior year’s third quarter to $589 million, with all three segments contributing to

11 percent organic growth

Operating profit increases 24 percent to $153 million and operating margin improves by 1 percentage point to

26 percent, both compared to the prior year’s third quarter and both inclusive of $6 million of intangible asset

amortization expense for fiscal 2017 acquisitions

GAAP diluted EPS increases 19 percent to $1.74 and adjusted diluted EPS increases 21 percent to $1.78,

both compared to the prior year’s third quarter

EBITDA increases 29 percent to $179 million, EBITDA margin improves 2 percentage points to 30 percent,

and EBITDA per diluted share increases 27 percent to $3.08, all compared to the prior year’s third quarter

Free cash flow before dividends increases 14 percent compared to the prior year’s third quarter to $55 million

Order Rates and Guidance

Pro-forma 12 week order rates decrease 2 percent over same period a year ago

Fourth quarter 2017 guidance: sales expected to increase 4 to 8 percent over prior year; GAAP diluted EPS in the

range of $1.18 to $1.32; EBITDA in the range of $133 to $144 million, or $2.27 to $2.46 per diluted share

See Nordson press release, conference call transcript, presentation Appendix, and SEC filings reconciling adjusted amounts to reported amounts

Why invest in Nordson?

17

Outstanding Culture and Values

Leading Global Businesses

Clear Strategy and Goals

Strong Execution and Performance

Numerous Growth Opportunities

We Win with Unique Competitive AdvantagesCommon across our businesses

Strategic Assets

Customer relationships with leaders

Product breadth

Technology position

Premier brand reputation

Large installed product base

Global footprint (distribution, support)

Balance sheet / ability to scale production

Core Competencies

Application development

Precision manufacturing

Engineering strength

Technical expertise

Direct global sales and service

Customer “touch” / solutions provider

18

Customer Value Proposition

Product reliability = more uptime

Speed = greater productivity and yield

Efficiency = lower material usage

Leading product features = ease of operation

Unmatched global support

Lower Cost of

Ownership

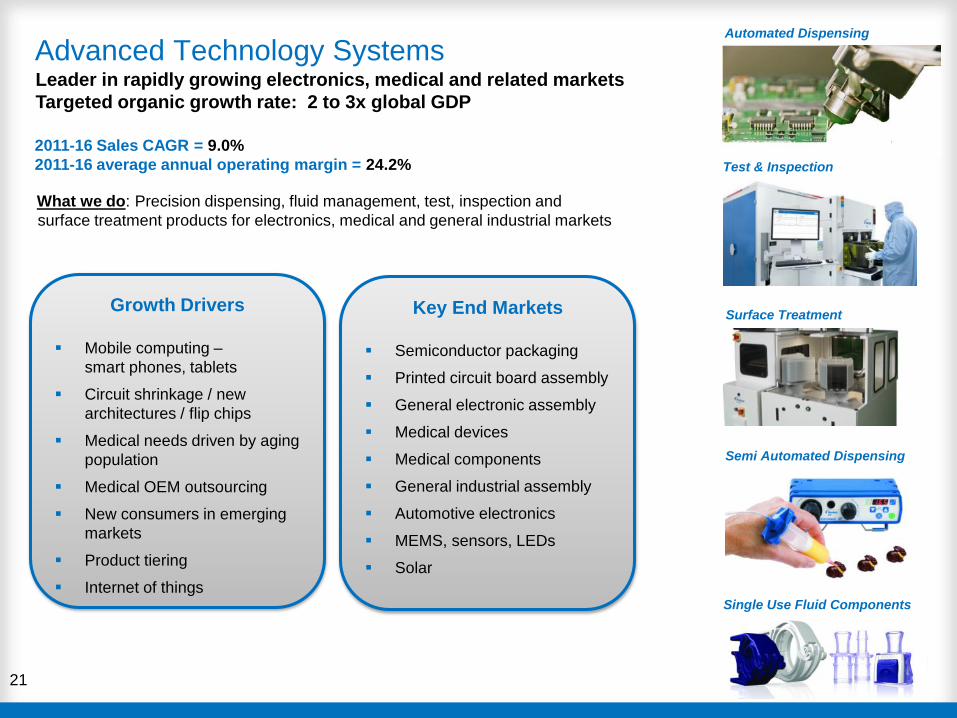

Industrial Coating Systems: durable goods and industrial market focus

Advanced Technology Systems: electronics, medical and industrial market focus

Innovation Drives Organic GrowthSteady stream of new products

25

Granted

Emerging Markets Drive Organic GrowthGrowing middle class drives increased consumption

26

baby diapers, disposable hygiene products

packaged foods, beverages, convenience items

appliances and other durable goods

electronic devices

medical products

plastic goods

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

2006 2011 2016

Asia Pacific Americas

Nordson Sales (000s)

• Americas reporting includes Canada, but not US -Asia Pacific excludes Japan -Eastern Europe, Middle East and Africa are reported in Europe and not broken out separately

Biopharmaceuticals

Orthobiologics

Minimally invasive catheters

Bottle labeling

Pipe coating

Flexible packaging

New Applications Drive Organic GrowthLeveraging our expertise – numerous emerging opportunities over last five years

Total Sales by Geographic Region 589,438$ 489,899$ 20.7% -0.4% 20.3% 1,493,044$ 1,299,711$ 16.0% -1.1% 14.9%

Year-to-Date

FREE CASH FLOW BEFORE DIVIDENDS 2017 2016 2017 2016

Net income 101,456$ 84,214$ 215,967$ 195,976$

Depreciation and amortization 25,954 17,662 65,366 52,824

Other non-cash charges (8,592) 4,455 3,041 13,213

Changes in operating assets and liabilities (41,991) (38,485) (68,183) (67,279)

Net cash provided by operating activities 76,827 67,846 216,191 194,734

Additions to property, plant and equipment (22,295) (19,931) (49,324) (45,452)

Proceeds from the sale of property, plant and equipment 308 173 3,906 1,044

Free cash flow before dividends 54,840$ 48,088$ 170,773$ 150,326$

Adjustments:

Acquisition costs and adjustments, net of tax (1) 1,597 - 12,564 1,325

Free cash flow before dividends, adjusted 56,437$ 48,088$ 183,337$ 151,651$

(1) Represents one-time costs, net of tax, associated with our 2017 and 2016 acquisitions, including the step up in the value of acquired inventory and acquisition

transaction costs that are required to be expensed as incurred.

Third Quarter Year-to-Date

Third Quarter

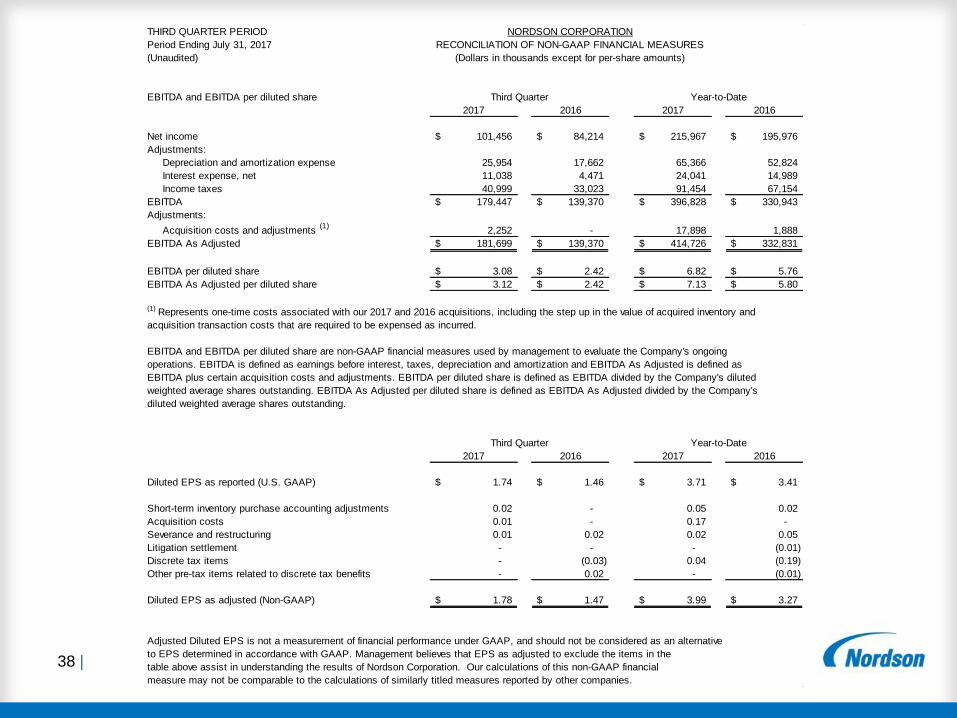

38 |

THIRD QUARTER PERIOD NORDSON CORPORATION

Period Ending July 31, 2017 RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

(Unaudited) (Dollars in thousands except for per-share amounts)

EBITDA and EBITDA per diluted share Third Quarter Year-to-Date

2017 2016 2017 2016

Net income 101,456$ 84,214$ 215,967$ 195,976$

Adjustments:

Depreciation and amortization expense 25,954 17,662 65,366 52,824

Interest expense, net 11,038 4,471 24,041 14,989

Income taxes 40,999 33,023 91,454 67,154

EBITDA 179,447$ 139,370$ 396,828$ 330,943$

Adjustments:

Acquisition costs and adjustments (1)

2,252 - 17,898 1,888

EBITDA As Adjusted 181,699$ 139,370$ 414,726$ 332,831$

EBITDA per diluted share 3.08$ 2.42$ 6.82$ 5.76$

EBITDA As Adjusted per diluted share 3.12$ 2.42$ 7.13$ 5.80$

(1) Represents one-time costs associated with our 2017 and 2016 acquisitions, including the step up in the value of acquired inventory and

acquisition transaction costs that are required to be expensed as incurred.

EBITDA and EBITDA per diluted share are non-GAAP financial measures used by management to evaluate the Company's ongoing

operations. EBITDA is defined as earnings before interest, taxes, depreciation and amortization and EBITDA As Adjusted is defined as

EBITDA plus certain acquisition costs and adjustments. EBITDA per diluted share is defined as EBITDA divided by the Company's diluted

weighted average shares outstanding. EBITDA As Adjusted per diluted share is defined as EBITDA As Adjusted divided by the Company's

diluted weighted average shares outstanding.

Third Quarter Year-to-Date

2017 2016 2017 2016

Diluted EPS as reported (U.S. GAAP) 1.74$ 1.46$ 3.71$ 3.41$