SEB Trygg Liv is the market leader in Sweden in new

unit linked insurance (excluding IPS). Unit linked

insurance accounts for slightly over 90 per cent of the

company’s total sales and nearly 80 per cent of

paid-in insurance premiums. Unit linked insurance

did not achieve its breakthrough as a savings form

until the 1990s, at which point there was already a

substantial stock of traditional insurance. Since 1

March 2007 traditional insurance is no longer offered

by SEB Trygg Liv. In the last couple of years, however,

it has offered unit linked insurance with a guaranteed

amount where savings are invested in a special fund.

Customers are guaranteed 90 per cent of deposited

premiums.

Sweden’s corporate life insurance market has

quadrupled since 1998. The strong growth rate has

tailed off, however. In the retail market, volume

has fl uctuated greatly over the years and has been

affected by stock prices and changes in tax laws.

SEB Trygg Liv’s aim is to provide a complete range

of life insurance. This means that we must develop

and broaden our range of risk insurance (care

products). These products cover life situations such

as illness, medical care, death and accidents – for

companies and their employees. At the same time we

are seeing that attitudes towards, and demands on,

pension advice have changed radically. It is no longer

enough to talk about public pensions, pension solutions

and occupational pensions. Customers also want help

with their fi nancial situation, which includes issues of

health and housing.

Turn-key solutions for private individuals in SwedenFor most people, fi nancial security in old age has

three pillars: a national pension, occupational pension

and their own pension savings. The national pension

system is linked to future growth and demographic

trends. Based on demographic forecasts, with an

aging population and fewer wage earners supporting

more dependents, we anticipate growing demand for

individual pension savings. Pension savings are tax

deductible within certain limits. SEB Trygg Liv’s main

product for private pension savings is Individual

Pension Savings, IPS, where customers can choose to

save in funds, individual securities or a bank account.

IPS has no insurance component, but can be

complemented with group life insurance.

Another possibility is to take out pension

insurance. Here the choice is to save in unit linked

insurance or unit linked insurance with a guaranteed

amount, where 90 per cent of the premium is

guaranteed. Since this is insurance, it is possible to

add cover for survivors and waiver of premium

insurance.

With both IPS and pension insurance, the money

can be withdrawn from age 55. For those who prefer

to take their money out earlier, an alternative can be

to save in “kapitalspar,” a unit linked endowment

insurance. The premium is not tax deductible and

therefore the money is not taxed when paid out.

SEB Trygg Liv in Sweden has a complete range of life insurance products for companies and private individuals. Individual products include occupational pensions, private pension insurance, life insurance, disability insurance, health care insurance, rehabilitation insurance and pension foundations. Insurance advice and other consulting services are offered together with these solutions.

SEB Trygg Liv in Sweden

Competitive occupational pensionsA large percentage of the occupational pensions

covering employees in Sweden are collective plans

not open to competition. In contrast, the competitive

components are large and important target groups

for SEB Trygg Liv and comprise two market sectors:

complementary pensions and solutions for high

earners, known as ten-pointers.

Complementary pensions are the occupational

pension component where the employee can choose

the investment. The various agreement areas SAF-LO,

KAP-KL, ITPK and PA03 have such models. Solutions

for ten-pointers are mainly for salaried employees

who earn more than ten income base amounts.

Provided their employer approves, these employees

can in addition to complementary pensions choose

insurance solutions for the premiums related to

salaries above a certain amount.

Pension foundations – another alternativeSetting up a pension foundation can be an alternative

for companies seeking a solution other than insurance

for their employees’ occupational pensions. Interest in

foundation solutions has increased over the years,

mainly from large industrial groups. Companies

looking for advice or assistance in setting up and

administering pension foundations can turn to SEB

Trygg Liv Pensions Service, the leader in the fi eld.

Several contact channelsSwedish customers of SEB Trygg Liv can contact us

through several channels such as SEB’s bank branches,

Trygg Liv’s telephone service centre and our Internet

branch.

Investing premium pensionsThe national pension system comprises an income-

based pension, which is managed by the state and

indexed to economic growth, and a premium pension,

which allows people to invest in one or more of nearly

700 funds offered by the Premium Pension Authority.

SEB participates with some 20 funds. For younger

people in particular, the difference in pension can be

considerable depending on the funds selected, since

the premium pension may correspond to up to one

third of their future pension.

Infl uencing occupational pensionsA signifi cant portion of the future pension comes from

occupational pensions paid for by the employer. A

growing number of occupational pension agreements

contain a component that allows employees to decide

how it should be invested. The decision is whether to

invest in unit linked insurance, unit linked insurance

with a guaranteed amount or traditional insurance,

and which company to manage the assets. It is

important to understand which alternatives are

available, since the difference can be substantial

depending on the choices made.

Save and investSaving for fi nancial security is not only important

for retirement. For parents or grandparents, saving

for children and grandchildren is a way to give

them a good start in life. Saving in the “kapitalspar”

endowment insurance product can offer tax

advantages. Another possibility for large investments

offered by SEB Trygg Liv is Life Assurance Portfolio

Bond, an international endowment insurance that

provides certain benefi ts over investments in directly

owned shares or funds.

Complementing public welfareIncreased pressure on the social insurance system has

brought the issue of public welfare to the forefront.

Many people feel a need to complement with their

own private insurance. This includes disability

insurance to compensate for loss of income, health

insurance to provide faster access to medical care, life

insurance to compensate relatives when the insured

person dies, or mortgage insurance to allow surviving

family members to remain in their home.

Offering for Swedish companiesQuestions facing small businesses include choosing a

pension solution for the owners and employees and

creating fi nancial protection in the event of illness.

Employee absenteeism due to illness affects

companies in various ways. To reduce such absences

and related costs, SEB Trygg Liv offers the “Lönsam

Hälsa” (profi table health) concept to prevent absences

due to illness, as well as rehabilitation insurance and

insurance providing compensation for medical care

and treatment if illness has already occurred.

Simpler administrationIt is a major advantage if administration of employees’

insurance solutions is simple to handle. SEB Trygg

Liv’s occupational pension programme, TryggPlan,

requires little effort on the part of the client company

and provides considerable opportunities to add

different types of insurance cover. The company

reports personnel and salary changes to SEB Trygg

Liv, which takes care of all the paperwork. For large

companies there is a system that allows electronic

reporting directly to us. SEB Trygg Liv has online

services that allow even small companies to manage a

large part of their administration through SEB’s

website. This creates an even simpler process where

the insured’s details can be processed immediately.

Gamla Liv 528,000Nya Liv* 118,000Fondförsäkringsaktiebolaget SEB Trygg Liv 679,000SEB Trygg Life (UK) 7,000SEB Pension, Denmark 300,000Estonia 42,000Latvia 41,000 Lithuania 45,000

Total number of customers, approx. 1,760,000

* Merged with Fondförsäkringsaktiebolaget SEB Trygg Liv in October 2007.

Number of customers

(rounded off) 2007

6 7

Number of employees 1,218recalculated on a full-time basis

Sweden 20,426Denmark 10,561International (incl. Baltics) 1,072 32,059

Of which Baltics 321

Company-paid insurance

SEKm 2007

Sales1)

IPS 1,408Unit linked insurance 35,416Traditional life insurance 8,923 45,747Premium incomeUnit linked insurance 18,241Traditional life insurance anddisability/health insurance 8,129 26,370Assets under management Unit linked insurance 136,200Traditional life insurance anddisability/health insurance 272,200 408,400SalesPrivately paid, incl. IPS 13,688Company-paid 32,059 45,747

Volumes

incl. Baltics

1) Sales consist of new insurance business, extra deposits and increases in existing insurance policies. Sales are measured as single premiums + regular premiums x 10. Figures exclude PPM.

SEB Trygg Liv 22.1 (29.3)

Skandia 14.1 (15.7)

Swedbank 10.2 (11.3)

Folksam 7.7 (7.9)SHB and SPP 8.2 (7.7)

LF 12.7 (7.3)

Moderna Försäkringar 13.4 (6.7)

Nordea 4.2 (4.8)Danica 3.9 (5.3)

Other 0.2 (0.4)

AMF 3.3 (3.4)

Market shares for unit linked insurance, SwedenNew policies

Unit linked insurance dominates the retail market …In recent years the retail market in Denmark has not

generated much growth, since most people save in

some form of occupational pension, which they can

also contribute to themselves. SEB Pension’s

development has followed the overall trend. In the

retail market, unit linked insurance including Market

Pension is currently the dominant product for SEB

Pension in terms of new sales.

… and is growing in the corporate market as wellAlthough around 85 per cent of employees

in Denmark currently have some form of

complementary occupational pension, there is still

a relatively large need to save more, due to which

growth is expected to continue in the years ahead.

Only defi ned contribution pensions are available,

but employees can often contribute to their savings

by withholding a portion of their salaries. Strong

competition in the occupational pension market,

coupled with full transfer rights, has encouraged

customers to switch insurers. A large part of sales

to companies (slightly over 40 per cent) is through

insurance brokers, while the rest is handled through

SEB Trygg Liv’s own sales force and via a distribution

agreement with the former owner, Codan Forsikring.

Several contact channelsSEB Pension has around 300,000 customers. They can

reach us through our sales force and our call centre.

SEB Pension’s call centre responds to nearly 100,000

calls and e-mails from customers each year.

Measured in premium income, SEB Pension is the

fourth largest company in Denmark, with a market

share of around 10 per cent. In the unit linked market,

SEB Pension is the second largest company after

Danica.

Nearly 80 per cent of new business consists of

corporate sales. In the retail market unit, linked

insurance accounts for 85 per cent of sales, while the

corporate market consists to 50 per cent of traditional

insurance since some agreement areas do not yet offer

unit linked insurance as an investment alternative.

The Danish occupational pension market has had

an annual growth rate of around 10 per cent since 2000.

SEB Pension’s growth rate in occupational pensions has

been 15-20 per cent in recent years. In the retail market,

SEB Pension’s performance has followed the general

trend, where there has been a lack of signifi cant

growth.

SEB Pension’s assets under management are

increasing. In 2007, premiums rose by 11 per cent.

Growth has primarily been in unit linked insurance,

which rose by 16 per cent in 2007, while premiums

for traditional insurance increased by approximately

9 per cent.

In unit linked insurance, SEB Pension offers a

product called Market Pension for customers who want

assistance over time to align their investments with

their age and anticipated retirement date. Growth in

unit linked insurance is primarily driven by this

product.

SEB Pension sells savings, life and health insurance to private individuals and companies. Savings insurance comprises both unit linked and traditional insurance (in profit-distributing companies).

SEB Pension, Denmark

8 9

10 %

SEB Pension’s share of the Danish market Premium income

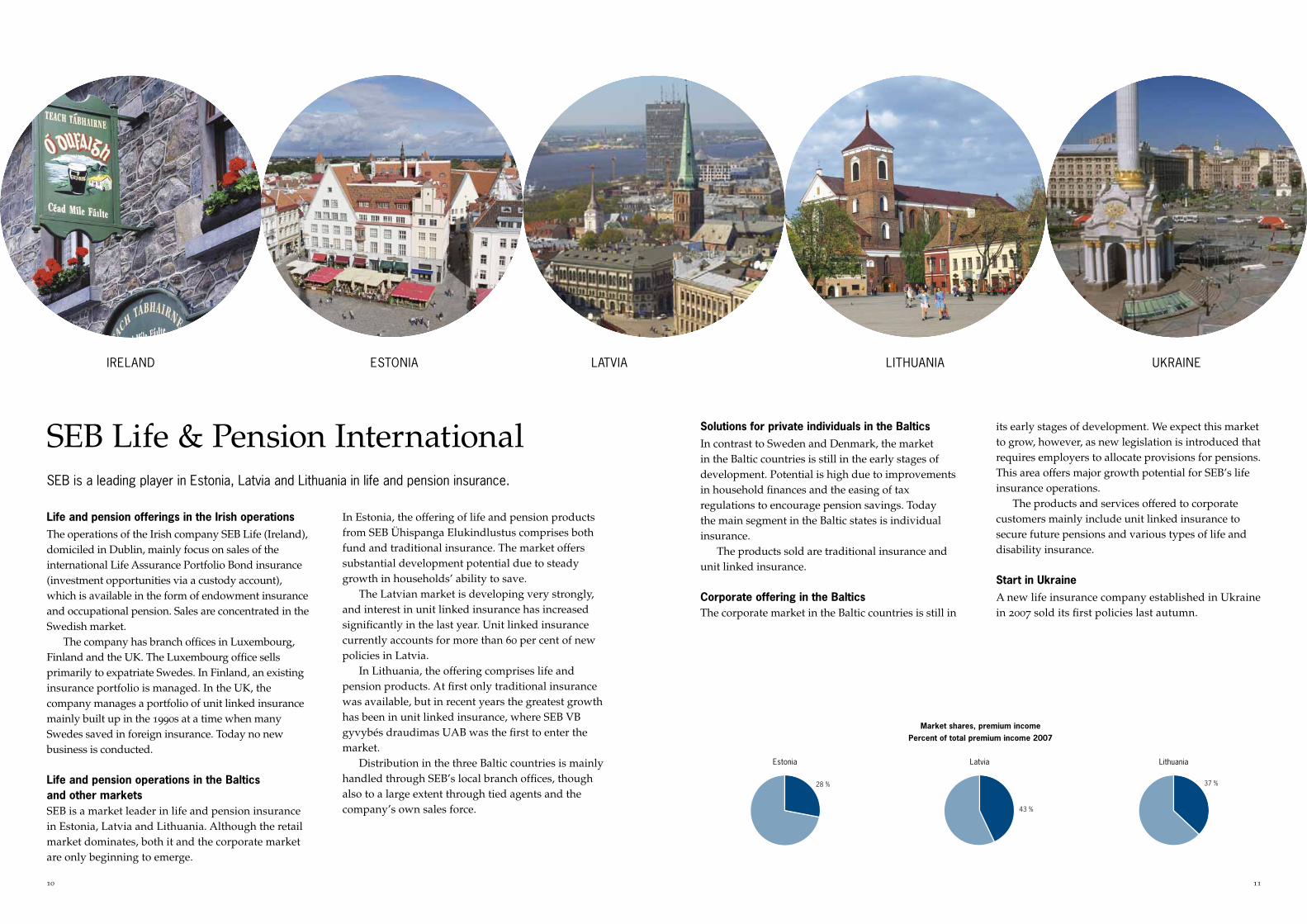

Life and pension offerings in the Irish operationsThe operations of the Irish company SEB Life (Ireland),

domiciled in Dublin, mainly focus on sales of the

international Life Assurance Portfolio Bond insurance

(investment opportunities via a custody account),

which is available in the form of endowment insurance

and occupational pension. Sales are concentrated in the

Swedish market.

The company has branch offi ces in Luxembourg,

Finland and the UK. The Luxembourg offi ce sells

primarily to expatriate Swedes. In Finland, an existing

insurance portfolio is managed. In the UK, the

company manages a portfolio of unit linked insurance

mainly built up in the 1990s at a time when many

Swedes saved in foreign insurance. Today no new

business is conducted.

Life and pension operations in the Balticsand other marketsSEB is a market leader in life and pension insurance

in Estonia, Latvia and Lithuania. Although the retail

market dominates, both it and the corporate market

are only beginning to emerge.

In Estonia, the offering of life and pension products

from SEB Ühispanga Elukindlustus comprises both

fund and traditional insurance. The market offers

substantial development potential due to steady

growth in households’ ability to save.

The Latvian market is developing very strongly,

and interest in unit linked insurance has increased

signifi cantly in the last year. Unit linked insurance

currently accounts for more than 60 per cent of new

policies in Latvia.

In Lithuania, the offering comprises life and

pension products. At fi rst only traditional insurance

was available, but in recent years the greatest growth

has been in unit linked insurance, where SEB VB

gyvybés draudimas UAB was the fi rst to enter the

market.

Distribution in the three Baltic countries is mainly

handled through SEB’s local branch offi ces, though

also to a large extent through tied agents and the

company’s own sales force.

SEB is a leading player in Estonia, Latvia and Lithuania in life and pension insurance.

SEB Life & Pension InternationalSolutions for private individuals in the BalticsIn contrast to Sweden and Denmark, the market

in the Baltic countries is still in the early stages of

development. Potential is high due to improvements

in household fi nances and the easing of tax

regulations to encourage pension savings. Today

the main segment in the Baltic states is individual

insurance.

The products sold are traditional insurance and

unit linked insurance.

Corporate offering in the BalticsThe corporate market in the Baltic countries is still in

its early stages of development. We expect this market

to grow, however, as new legislation is introduced that

requires employers to allocate provisions for pensions.

This area offers major growth potential for SEB’s life

insurance operations.

The products and services offered to corporate

customers mainly include unit linked insurance to

secure future pensions and various types of life and

disability insurance.

Start in UkraineA new life insurance company established in Ukraine

in 2007 sold its fi rst policies last autumn.

Market shares, premium incomePercent of total premium income 2007

10 11

IRELAND UKRAINE LITHUANIALATVIA ESTONIA

28 %

Estonia

43 %

Latvia

37 %

Lithuania

Unit linked insuranceIn unit linked insurance, the customer decides

whether to invest their money in one or more funds.

This gives them an opportunity to infl uence returns

and select a level of risk.

Unit linked insurance works the same way regardless

of the country where you as a customer reside.

Funds plus insuranceUnit linked insurance can be used for investment

purposes, private pension savings or a company’s

pension provisions. Other applications include

various types of target and fi nancial security savings.

By packaging funds in an insurance solution,

people can switch funds without charges or capital

gains tax. Such transfers do not have to be reported

on income tax returns.

The insurance solution also means that different types

of insurance cover can be added. Perhaps the insured

wants less restrictive form of survivors’ protection

rather than saving without an insurance component.

Perhaps they want to guarantee a level of savings

even if their fi nances suffer due to illness. Perhaps the

insured wants life insurance which provides a lump

sum in the event of death.

Range of fundsAvailable equity funds focus on either a region

or sector. Regional funds limit their investments

geographically – from individual countries to

the entire world. Sector-specifi c funds invest in

companies that belong to a particular sector regardless

of geographic region. One example of a sector fund is

SEB Läkemedelsfond (pharmaceuticals).

People who save in pension or endowment insurance can choose between unit linked, unit linked insurance with a guaranteed minimum value or traditional insurance.

Our products

Fixed-income funds move in the opposite direction to

interest rates. If rates rise, the value of fi xed-income

funds falls and vice versa. The shorter the remaining

maturity of a fund’s fi xed-income securities, the less

sensitive it is to interest rate fl uctuations. This means

that a long-term fi xed-income fund rises more than

a short one if interest rates fall. Fixed-income funds

can be listed in different currencies. Exchange-rate

fl uctuations often affect foreign fi xed-income funds

more than interest rate variations.

Blend funds invest in both equities and fi xed-

income securities.

Funds of funds invest in other equity funds. These

funds give customers access to a number of funds that

are not available for direct investments, but that the

manager feels are the best in their category.

Hedge funds have less restrictive investment

guidelines than other funds. Investments include

equities, bonds, foreign currencies and options. The

manager can also leverage the portfolio’s holdings.

Hedge funds are a way to access exclusive portfolios

normally available only to large institutional

investors.

Varying risk offered by fundsThe funds have been designed for investors with a

widely differing risk propensity. The lowest risk is

obtained by investing in a short fi xed-income fund,

while specialised equity funds take the highest risk.

Customers who save in funds with different

objectives reduce their exposure to downturns in a

specifi c sector or region. The longer the investment

timeframe, the more probable it is that temporary ups

and downs will even out.

The fund investment service can be added by unit

linked insurance policyholders without the time or

interest in choosing funds themselves. The customer

selects a portfolio based on a desired risk level. The

portfolio is then actively managed by SEB Trygg Liv’s

managers.

Unit linked insurance with guaranteed amount Unit linked insurance with a guaranteed amount is

designed for customers who want the security of a

guaranteed return but do not have the time or interest

in reallocating their savings among different funds

over time. With this insurance, the customer receives a

pension savings with a 90-percent guarantee on paid-

in premiums.

Savings are invested in an actively managed fund

with the opportunity to take advantage of stock

market gains throughout the insurance period.

Market Pension The Danish product, Market Pension, is a manage-

ment concept for customers who do not want the

responsibility for choosing their investments and

who want an investment profi le (risk profi le) that

matches their age and anticipated retirement date.

The proportion of equities – and thus the investment

risk – decreases with age. This product currently is

available only in the Danish market.

Traditional insuranceAs of March 1, 2007 SEB Trygg Liv no longer offers

traditional insurance in Sweden.

If customers in Denmark, Estonia, Latvia and

Lithuania choose traditional insurance for their

savings, their contributions are invested in something

Income 3,930 3,456 2,966Expenses -2,128 -1,936 -1,993Operating result 1,802 1,520 973Change in surplus values, net 1,264 2,111 2,929Total result 3,066 3,631 3,902

Profit and loss account – SEB Trygg Liv division

1) Holding group.2) Including Gamla Liv.3) Surplus values are the estimated present value of future profits from insurance contracts in force.

The Trygg Foundation

Gamla Livförsäkrings AB SEB Trygg Liv

SEB Life (Ireland) Assurance Co Ltd

CJSC SEB Life(Ukraine)

ForsikringsselskabetSEB Link A/S

SEB Pensions-forsikring A/S

Skandinaviska Enskilda Banken AB

Fondförsäkrings ABSEB Trygg Liv

SEB Trygg LivPensionstjänst AB

SEB Life & Pension InternationalSEB Pension (Denmark)SEB Trygg Liv (Sweden)

SEB Trygg Liv Holding AB

2

1

1 Policyholders in Gamla Livförsäkringsaktiebolaget SEB Trygg Liv are represented by the Trygg Foundation, which owns one share in the company, and a related shareholder agreement. The Trygg Foundation is entitled to appoint two members of the board and together with SEB appoint the Chairman of Gamla Liv’s board, comprising fi ve members, and to appoint the majority of members and the Chairman of the Finance Delegation, which is responsible for asset management within Gamla Liv. Every fi ve years policyholders are invited to vote for candidates to the Trygg Foundation’s Council.

2 The companies operate according to mutual principles and are not consolidated in SEB.

The companies in the Baltic countries are not listed in the fi gure since they are only included

on an operational basis in the division, not as legal entities in SEB Trygg Liv Holding AB.

16 17

SEB TRYGG LIV SWEDEN

Gamla Livförsäkringsaktiebolaget SEB Trygg Liv The operations of Gamla Livförsäkringsaktiebolaget

SEB Trygg Liv comprise traditional insurance, primar-

ily pension insurance. The company is closed for new

business. It operates according to mutual principles

and is not consolidated in SEB. The company’s insur-

ance administration and service are handled, against

payment, by Fondförsäkringsaktiebolaget SEB Trygg

Liv. SEB’s Wealth Management division handles the

large part of asset management.

Policyholders exercise infl uence through the Trygg

Foundation.

Fondförsäkringsaktiebolaget SEB Trygg LivFondförsäkringsaktiebolaget SEB Trygg Liv is respon-

sible for all Swedish unit linked insurance and unit

linked insurance with a guaranteed amount within

SEB Trygg Liv and offers endowment insurance,

private pension insurance, occupational pensions and

disability insurance.

On 1 October 2007 Nya Livförsäkringsaktiebolaget

SEB Trygg Liv merged with

Fondförsäkringsaktiebolaget SEB Trygg Liv, after

which the company Nya Liv ceased to exist and new

business is no longer written. Existing insurance

in the former Nya Liv is managed as traditional

insurance in the unit linked insurance company.

SEB Trygg Liv Pensionstjänst ABThe company dominates the Swedish market

for administration and management of pension

foundations. Administration services include managing

pension commitments from companies, forming,

operating and winding up foundations, handling

contacts with authorities and providing legal expertise

on issues relating to pension foundations. The customer

base covers every segment, from small family owned

businesses to listed companies and sports associations.