Page 1

A presentation to – Association of School Business Administrators (Vic)

Wednesday 20 March 2013

Presented by:

Andrew Marks

–Director William Buck Audit (Vic) Pty Ltd

Stephen Rooke

-Principal William Buck (NSW) Pty Ltd

Not-for-profit Reform:

Accounting and Finance briefing for Schools

Page 2

Overview

– Not-for-profit Reform Update – Accounting and Finance Issues – Taxation and Registration Issues – Practicalities and Examples – Business Manager’s Checklist

Page 3

Not-for-profit Reform Agenda

Not-for-profit sector reforms are designed to:

— Reduce complexity, red tape and compliance costs for

operators in the not-for-profit sector; and

— Increase public confidence in the sector through increased

Your problem

governance, transparency, accountability and

ACNC Brief

education.

Page 4

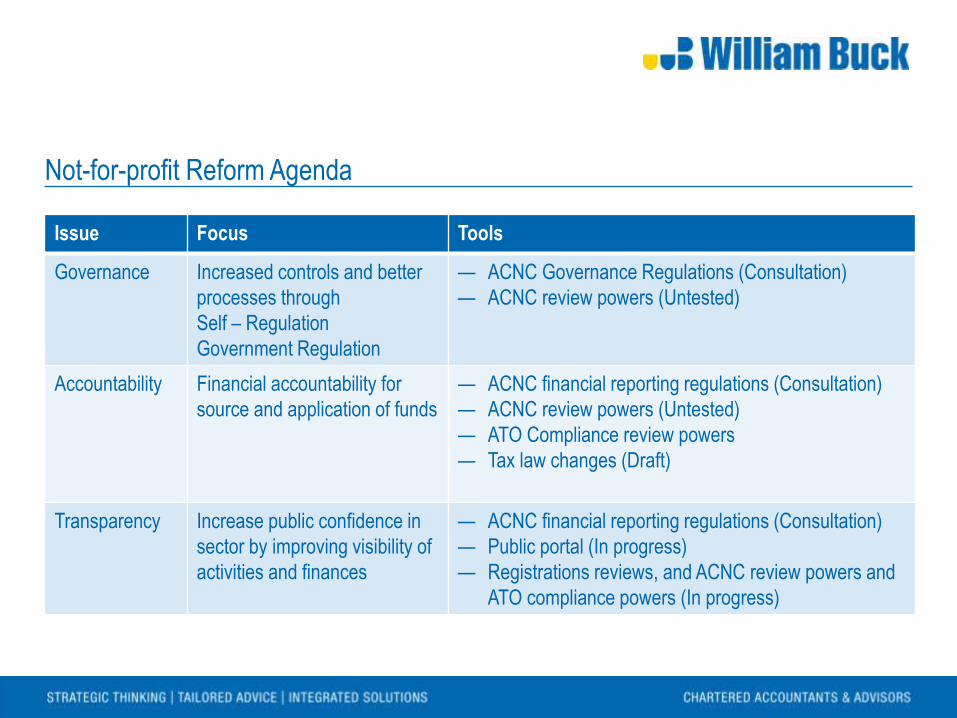

Not-for-profit Reform Agenda

Issue Focus Tools

Governance Increased controls and better

processes through

Self – Regulation

Government Regulation

— ACNC Governance Regulations (Consultation)

— ACNC review powers (Untested)

Accountability Financial accountability for

source and application of funds

— ACNC financial reporting regulations (Consultation)

— ACNC review powers (Untested)

— ATO Compliance review powers

— Tax law changes (Draft)

Transparency Increase public confidence in

sector by improving visibility of

activities and finances

— ACNC financial reporting regulations (Consultation)

— Public portal (In progress)

— Registrations reviews, and ACNC review powers and

ATO compliance powers (In progress)

Page 5

Legislative Changes and Timing

Act Status

Australian Charities and Not-for-profits Commission Bill

2012 (and transitional bill)

Passed into Law on 3 December 2012

Tax Laws Amendment (Special Conditions for Not-for-profit

Concessions) Bill 2012

First reading in August 2012. Now on hold

pending timetable of pre-election parliament.

Charities Definition Act Undrafted, in consultation phase

NFP Working Group Review of sector concessions Consultation closed in December. Report due in

2013

Taxation of Commercial Activities No legislation, but still aiming for

commencement from 1 July 2014

Page 6

Accounting and Finance Implications

Registered Entities are regulated by ACNC and include:

— Corporations which operate charities

— A charitable trust which has one or more corporate trustees

— Any other entity which seeks charitable endorsement for federal

taxation concessions – i.e. income tax exemption, deductible gift

recipient, FBT concessions

EM to the Bill provides for other Not-for-profit entities to be added to

the list of Registered Entities in later stages.

Page 7

Accounting and Finance Implications

Key transitional timelines arising from commencement of ACNC:

— 6 month window for an entity opt out of the system if you no longer need

charitable endorsement – 3 June 2013

— 6 month window for a Registered Entity to notify the commissioner that

they have an Australian Law requirement to prepare financial reports

ending on a day other than 30 June – 3 June 2013

— 12 month window for an entity to be identified as a basic religious charity

– 2 December 2013

— Governing Council / Board of Directors to be notified to ASIC

— From 1 July 2013 all changes in officeholders to be notified to ASIC

Note: The approved forms to make the 3 June 2013 declarations were mailed out in late January and February 2013 and in most

cases were mailed to the address last updated in the ATO database (likely one of your activity statement addresses)

Page 8

Accounting and Finance Implications

Proving a 31 December year end for schools:

— The Schools Assistance Act is the Australian Law that requires a

school to report on a 31 December year end

— This act does not, however, cover other entities associated with the

school (foundations, scholarship funds, investment vehicles, building

funds)

Page 9

Accounting and Finance Implications

Financial Reporting for Registered Entities

Important – Check constitution as this may mandate an audit.

Note – Commissioner may allow an entity to remain at lower reporting threshold if it can show that the increased turnover is temporary.

Entity Lodgement pack to include

Small Registered Entity

— Turnover under $250,000

— Annual information statement

Medium Registered Entity

— Turnover between $250,001 and $1,000,000

— Annual information statement

— Financial statements

— Audit report or reviewer report

Large Registered Entity

— Turnover greater than $1,000,000

— Annual information statement

— Financial statements

— Audit report

Page 10

Accounting and Finance Implications

Financial Year -

30 June year end

Financial Year -

School

Lodgement requirements

1 July 2012 to

30 June 2013

1 January 2013 to

31 December 2013

Annual information statement to be provided

within 6 months of financial year end. Lodgement

of financial statements is voluntary. Mandatory

lodgement of financial statements with ASIC by 30

April 2014.

1 July 2013 to

30 June 2014

1 January 2014 to

31 December 2014

Annual information statement, Financial

statements with at least one year of correct data

and Auditor/reviewer report to be provided to

ACNC within 6 months year end

1 July 2014 to

30 June 2015

1 January 2015 to

31 December 2015

Annual information statement and Financials with

2 years (current year and comparative) with

ACNC 6 months after year end

Page 11

Accounting Implications from ACNC

Other Rules

Schools

Schools are able to lodge their Schools Assistance Act annual reports

in lieu of formal financial statements for at least the first 3 years of the

new regime.

Other Entities

The ACNC may accept any financial reports

prepared specifically to report under another

government act, but no word yet on the list of

acceptable reports.

Page 12

Accounting Implications from ACNC

Other Rules

Consolidations

The Commission of the ACNC may allow group reporting, subject to

an evaluation of the public benefit. If approved, the level of reporting

will be determined by the turnover of the largest member of the group,

rather than the aggregate.

To consolidate, expect that the regulator would need to see that there

was a public benefit to showing only consolidated data and the

normal rules are likely to apply that all entities applying for

consolidation have the same beneficiaries and year end date.

Page 13

Accounting and Finance Implications

Summary

— The ACNC is open for business from 2 December 2012

— Registered Entities will have lodgement requirements starting with

financial years ended 30 June 2013 or later

— Financial governance requirements will start from 1 July 2013 or later

— Registration - and therefore lodgement - is

compulsory to retain tax endorsements

— The window to make amendments to

registrations expires on 3 June 2013 for

most entities

Page 14

Taxation Implications

Tax Law changes for Not-for-profit entities are proposed in three areas:

— Changes to rules for income tax exempt and deductible gift recipient

entities

— Proposed reform of income tax exempt, charitable GST free and Fringe

benefit tax concessions

— Proposed taxation of commercial operations

The fact that these are proposed laws makes it difficult to give specific

guidance, but there are some clear trends that can be included in planning.

Page 15

Taxation Implications

Summary of Proposed Taxation Rules for ITE and DGR entities

Income Tax Exempt Entity Deductible Gift Recipient

Must be a not-for-profit entity

(no member benefits, retention of profits)

Must operate at all times in accordance with objects

(all activities to be in accordance with objects that were submitted at registration)

Operates Principally in Australia

- Trace 50% or more of income, profits and activities

are within Australia for the benefit of Australian

recipients in the class set out in your objects

Operates solely in Australia

All activities are undertaken to benefit recipients in

Australia

Some exclusions from tracing rules Minor activities outside Australia may be allowed if

they benefit Australian recipients

Page 16

Taxation Implications

Income Tax Exempt Entities (the school)

New Tracing Rules in the ‘Principally in Australia Test’

The organisation must be:

– Established in Australia

– Operate Principally in Australia

– Pursue it’s purposes Principally in Australia

Page 17

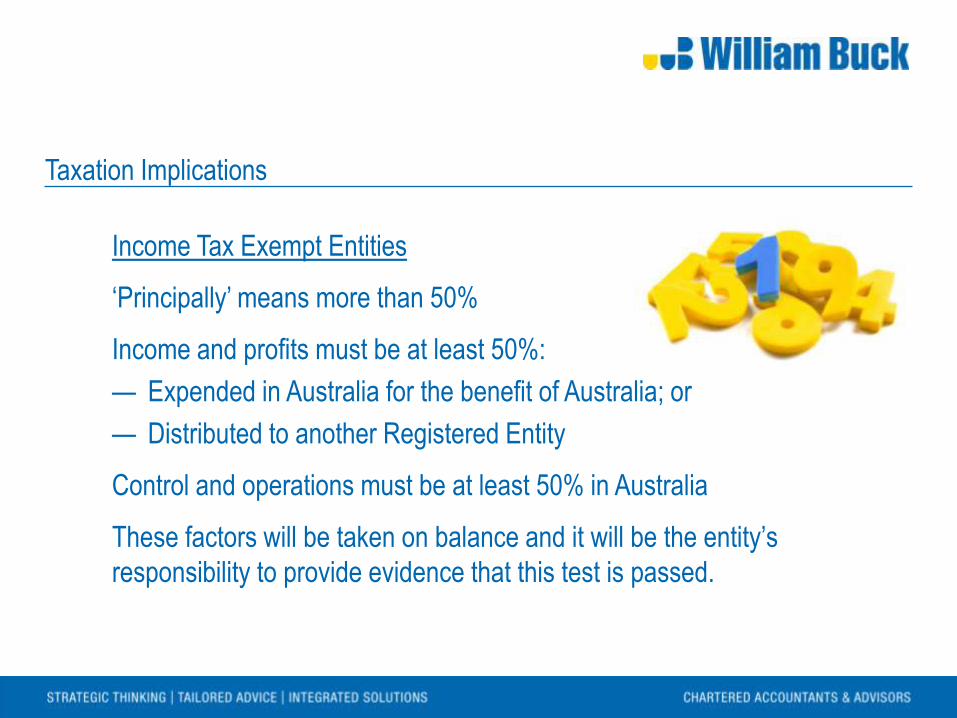

Income Tax Exempt Entities

‘Principally’ means more than 50%

Income and profits must be at least 50%:

— Expended in Australia for the benefit of Australia; or

— Distributed to another Registered Entity

Control and operations must be at least 50% in Australia

These factors will be taken on balance and it will be the entity’s

responsibility to provide evidence that this test is passed.

Taxation Implications

Page 18

Taxation Implications

Income Tax Exempt Entities

The tracing rules contain exclusions for the tracing of income from:

— Government grants

— Sources which did not claim a

deduction under Division 30 of the

Tax Act (which deals with

donations, gifts and contributions)

Page 19

Taxation Implications

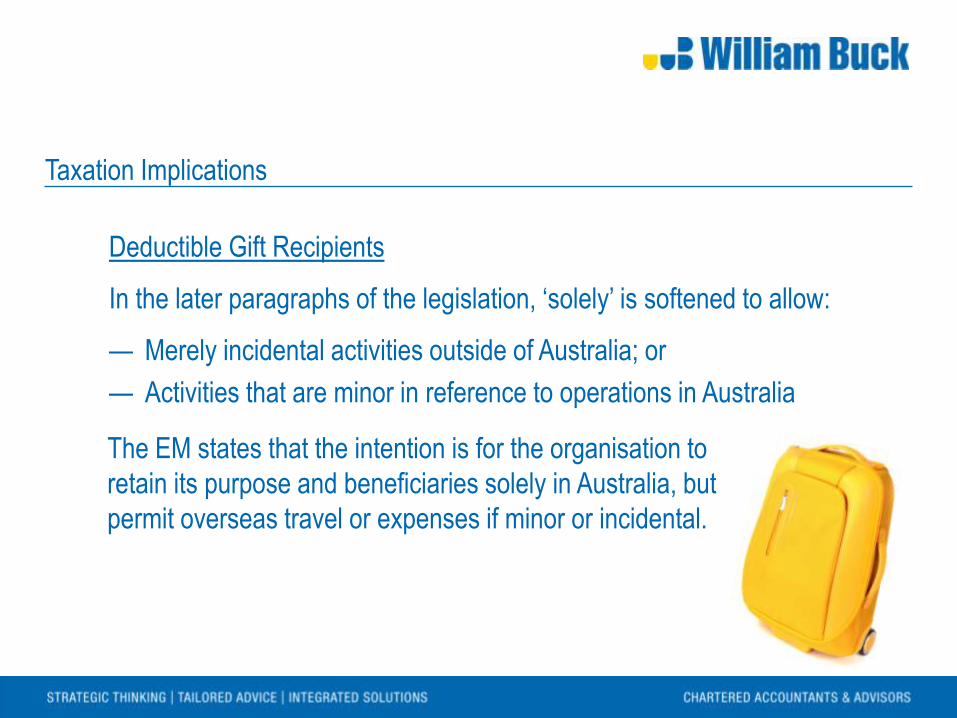

Deductible Gift Recipients

New ‘Solely’ in Australia Test. A DGR entity must be:

— Established in Australia

— Operate Solely in Australia

— Pursue its purposes Solely in Australia

Page 20

Taxation Implications

Deductible Gift Recipients

In the later paragraphs of the legislation, ‘solely’ is softened to allow:

— Merely incidental activities outside of Australia; or

— Activities that are minor in reference to operations in Australia

The EM states that the intention is for the organisation to

retain its purpose and beneficiaries solely in Australia, but

permit overseas travel or expenses if minor or incidental.

Page 21

Taxation Implications

Deductible Gift Recipients

Funds paid out of a DGR entity must go toward:

— Direct expenses of DGR entity in furthering it’s objects in Australia;

— A Registered Entity that also has DGR status with the ACNC

(note, an income tax exempt entity is not sufficient – it must have

DGR status); or

— Another Registered Entity that is registered as an Overseas Aid

Fund or Environmental Organisation and named by parliament Note: Even if funds are paid to another DGR or overseas Aid fund, the objects of your DGR entity must be aligned with

that entity. It is no good having a foundation for advancing education in Australia and giving money to an aid fund that will

send the money overseas – the Australian education fund has exceeded the scope of its objects if it makes the payment.

Page 22

Taxation Implications

NFP Working Group

Reform of NFP sector concessions, including:

— Availability of Income tax exempt and DGR status

— GST free status

— FBT Concessions

— Access to charitable endorsements

— Has the potential to make the biggest impact on day to day

function and costs for the School

Page 23

Taxation Implications

Taxation of commercial operations

— Proposed to commence

between 1 July 2014 and 1 July

2015.

— Final form of proposed regime

is not available

Page 24

Taxation Implications

Preparing for change without having the details:

— Review existing accounting ledgers, processes and controls and

make sure that the information relating to each type of income,

expense, activity and legal entity is able to be reported separately

— Collect information on existing access to GST, FBT and Income

tax concessions so this is on hand if the issues crystallise

— Fix any issues identified in the review process that don’t match the

current rules and be ready to adapt in the future

Page 25

Taxation Implications

Summary

— Tax endorsement requires registration with the ACNC

— Once registered, the ACNC will have line of sight on your activities

through financial reporting requirements

— Endorsed entities will need to demonstrate that they meet the tests for

ITE or DGR entities, including changes to these rules over time

— Other not-for-profit entities are expected to be included in the process

at a later point in time

— Planning and internal review is the best approach for the moment.

Page 26

Practicalities and Examples

Beyond the theory, what are the practical issues for Schools that

emerge when we combine the information that is already available?

Page 27

Practicalities

Financial Reporting

— Is your current financial system up to the challenge?

— Do you have an auditor for all entities and/or do you need one?

— Do you currently have year end accounts for non-school entities

finalised before 31 October? (This gives your auditor a chance to

finalise in the 5-7 working weeks before 31 December.)

— Are your accounting policies up to date or has it been a long time

since your accounts were subject to external review?

Page 28

Practicalities

Tracing Rules for ITEEs

— Does your current accounting process allow you to

separate government grants, not-for-profit income,

commercial income and donations?

— Are these activities formally separated or managed

through a joint bank account account/shared

general ledger?

— Do you need to revisit your contracts and

relationships with third parties non-charitable

suppliers to help with the tracing rules?

Page 29

Practicalities

Deductible Gift Recipients

Can you prove the Solely in Australia test? Sound easy?

If you say yes to any of the following the answer may not be straight forward:

— Do you deliver services or benefits through third parties? Can you prove that

your payments were delivered to your organisation’s beneficiaries?

— Do you have a mixed investment fund (holding the reserves of more than

one not-for-profit entity)? How do you allocate income between the entities?

— Do you deal with or provide funds to ITEE entities that send funds offshore?

— Do you have accounting policies and systems that keep separate ledgers for

the income and activities of your commercial and charitable operations?

Page 30

Practicalities

Specialist Regulator

With a single, specialist regulator in place to administer the Federal

Not-for-profit sector in Australia, the chances are much higher that

previously unreported issues or variations to the rules will be picked

up.

Now would be a good time to review your organisation’s operations

and make sure that the passage of time has not allowed issues to

arise.

Discrepancies between Commonwealth and State Not-for-profit

regimes will still arise in the short term as these regimes remain

managed by State Authorities, with different charitable definitions.

Page 31

Practicalities

Other issues that are coming for Not-for-profit entities:

— Trickle down of Director responsibilities issues – ‘Centro’, WH&S

— AASB Changes – recognition of income in AASB 1004

Page 32

Examples

ABC Student

Association Ltd

(ITEE)

Turnover - $1.2million in student education

and community services; Surplus - $200,000

Education for

disabled students

Fund (ITEE)

African Education fund (all monies

directed to fund schools in Africa)

$70,000 $130,000

Registered entity size for annual statements is

large as turnover is greater than $1million

Per the EM - ABC student Association

does not meet ‘primarily in Australia’

test as more than 50% of profits from

commercial activities have been

directed to overseas entity

Page 33

Examples

Mixed Revenue: Typical School

XYZ School Bank

Account

(ITEE)

Receipt of Schools fees

plus Building Fund Donation

Building Fund

Bank Account

(DGR)

Transfer of net donations

at end of month

Quick Questions:

— Is income accounting process correct?

— Are correct amounts transferred to DGR entity?

— How long are funds held in trust for DGR entity?

— Do they earn any interest whilst held?

— Is this interest also passed to DGR?

— Is the net gain or loss minor or incidental for

DGR entity?

Page 34

Examples

School with mixed investment fund

XYZ School Bank

Account

(ITEE)

Receipt of Schools fees

plus Building Fund Donation

Building Fund

Bank Account

(DGR)

Transfer of net donations

at end of month Shared Investment

Fund for surplus

cash

Quick Questions:

— How are investment proceeds split

between DGR and ITEE entity?

— Does DGR meet income and assets

test?

Page 35

Examples

Foreign Income

ABC Wellness

Association

Donations from foreign

benefactors

Receipts from Australian

Benefactors Services to Australian Beneficiaries

Funds transferred to Foreign Beneficiaries

Page 36

Examples

Foreign Income ITEE

ABC Wellness Association

Donations from foreign

benefactors

Receipts from Australian

Benefactors Services to Australian Beneficiaries

Funds transferred to Foreign Beneficiaries

Income from foreign sources needs to be tracked and excluded under tracing rules,

then ITEE entity passes ‘primarily in Australia Test’ through application of Australian

income to purpose

Page 37

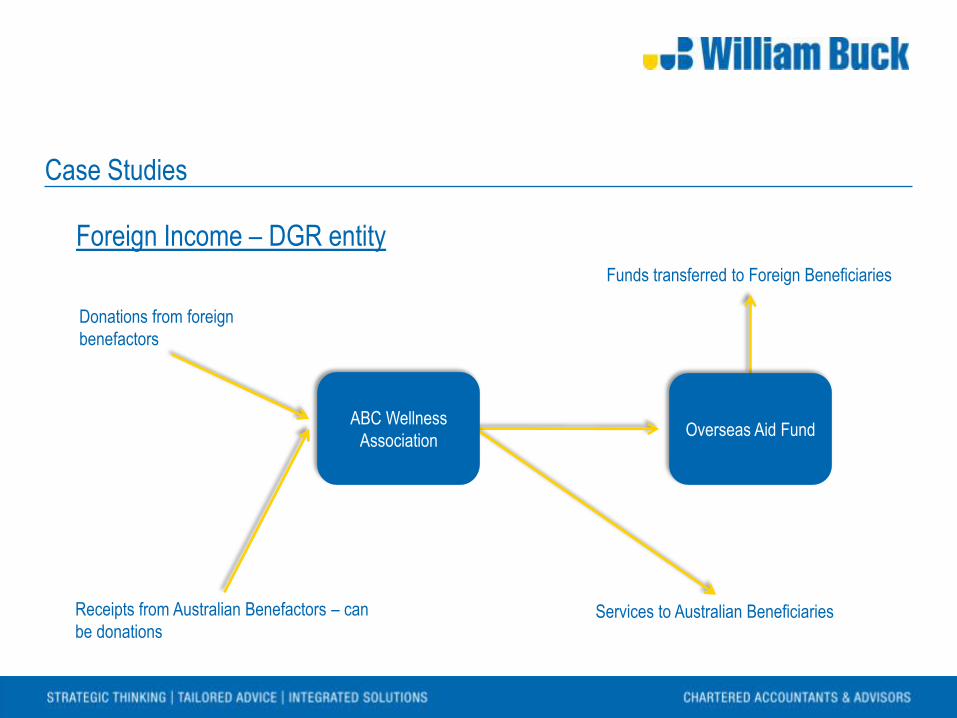

Case Studies

Foreign Income – DGR entity

Funds transferred to Foreign Beneficiaries

Overseas Aid Fund

Donations from foreign

benefactors

Receipts from Australian Benefactors – can

be donations Services to Australian Beneficiaries

ABC Wellness

Association

Page 38

Business Manager’s Checklist

Helping your school to prepare:

— The final details of the reforms are not yet available , including the

ACNC regulations, details of financial disclosures and approved forms

— The goals, processes and timelines,

however, are available now and

should be assumed to be correct

— Start now to avoid being rushed

when the final regulations and tax

legislation is released

Page 39

Business Manager’s Checklist

An orderly approach would include:

— Identify income, activities and operations and put them into

categories

— Review financial policies and systems to understand treatments

that are below best practice

— Source education or advice for directors/trustees/Boards if needed

— Consider early appointment of an auditor

— Fix any immediate issues and wait for the next wave of regulation

and clarifications before making pre-emptive changes

Page 40

Conclusion

Most organisations in the not-for-profit sector should expect higher

standards of governance, accountability and transparency to apply in

coming years.

Endorsed Charities will be the first entrants to the system, with other

entities to follow later.

The good news is that there is time for all entities to tackle these

issues in an orderly manner.

Some changes are going to be more fundamental than others

(updating systems and policies, changing legal structures), so should

be started earlier.

Page 41

Contact Details

Andrew Marks

Director

William Buck Audit (Vic) Pty Ltd

Level 1, 465 Auburn Road

HAWTHORN EAST VIC 3123

(03) 9824 8555

[email protected]

Page 42

Contact Details

Stephen Rooke

Principal

William Buck

Level 29, 66 Goulburn Street

SYDNEY NSW 2000

(02) 8263 4000

[email protected]