Page 1

© Prismark Partners LLC

1

PRISMARK PRESENTATION

PREPARED FOR:

13th EUROPEAN MANUFACTURING TEST CONFERENCE

(EMTC) October 8, 2014

A RAPIDLY CHANGING TEST LANDSCAPE

PREPARED BY:

Brian Swiggett Managing Partner

PRISMARK PARTNERS LLC 130 Main Street Cold Spring Harbor NY 11724

Tel: 631 367-9187 Fax: 631 367-9223 e-mail: [email protected]

www.prismark.com

Page 2

© Prismark Partners LLC

2

N514.239bes-drivers2

$0

$500

$1,000

$1,500

$2,000

$2,500

$Bn

2009 2010 2011 2018F201720162012 2013 2014E 2015

THE DRIVERS OF THE ELECTRONICS INDUSTRY HAVE CHANGED

23%19% 6.5%

2.9%10% 0%

4.1%82%

91%

37% 29.1%10.2%

2.8%

5.1%

-0.1%

-1% 0.8%

3% 4.1%

-7%-3.3%

13%

9%

4.3%

$1,269Bn

$1,458Bn14.9%

$1,602Bn9.9%

$1,616Bn0.9%

$1,678Bn3.8%

$1,731Bn3.2%

$2,020Bn2013-2018

CAAGR 3.8%

Note: Includes value of PV modules in total electronics

Automotive Electronics

Other Electronics

Servers/Storage/Comm infrastructure

Smartphones and Tablets

Page 3

© Prismark Partners LLC

3

A MATURE ELECTRONICS INDUSTRY

GROWS FASTER AT THE PERIPHERY

• Electronics Infrastructure Builds Out First – Computing and communications convergence – Continuing evolution and improvement – performance driven – Cloud and fog backbone

• Access at the Periphery Accelerates Later – Greater proportion of “consumer” and portable products drives integration – Explosion of new access points (ubiquitous networks) – Sensors and microsystems – “Internet of Things”

514.9/280bes

Page 4

© Prismark Partners LLC

4

MOBILE PHONES: MORE FUNCTION PER AREA

260x

4x

100x

2,300x

3x

4,000x

35x

25x

9x

15x

4x

1x

0.3x

0.8x

0.25x

2x

1x

2003

Nokia 6650

2013

Apple iPhone 5S Wireless Data Rate

Wireless Bands/Modes

Processor Speed

User Memory

Display Size

Display Colors

Display Pixels

Camera Resolution

Sensors

Battery Size

Battery Life

Price

Volume

Weight

PCB Area

Silicon Area

Silicon Area (excl. Memory)

514.4/407mvc

The space and cost constraints associated with consumer devices drives electronic integration

Page 5

© Prismark Partners LLC

5

N314.146mvc-Segmentation

>$600

Apple

Samsung

LG

Lenovo

Huawei

Coolpad

ZTE

% of Smartphones

$450 - $600

$300 - $450

$150 - $300

<$150

2011

Smartphone ASPUnits

Premium segment remains But most growth in low-cost smartphones

475M$366

680M$338

1,190M$270

980M$295

1,700M$200

1,600M$210

1,500M$220

1,400M$240

2012 2013 2014F 2015F 2016F 2018F2017F

SMARTPHONE ASP SEGMENTATION

Center of gravity shifts to lower-priced smartphones

Page 6

© Prismark Partners LLC

6

Markets evolve and opportunity (units) increase

Internet of Computers

Mainframe Networking Cloud Fog

Internet of People Internet of Things

THE NEXT PHASE OF GROWTH

Devices becoming smaller and thinner

Infrastructure becomes pervasive

Minicomputer

1980 1990 2000 2010 2020

10M+Units

100M+Units

1Bn+Units

5Bn+Units

30Bn+

UnitsPC

Desktop

Internet

Mobile

Internet

Wearable/IoT

814.10/416rd

Page 7

© Prismark Partners LLC

7

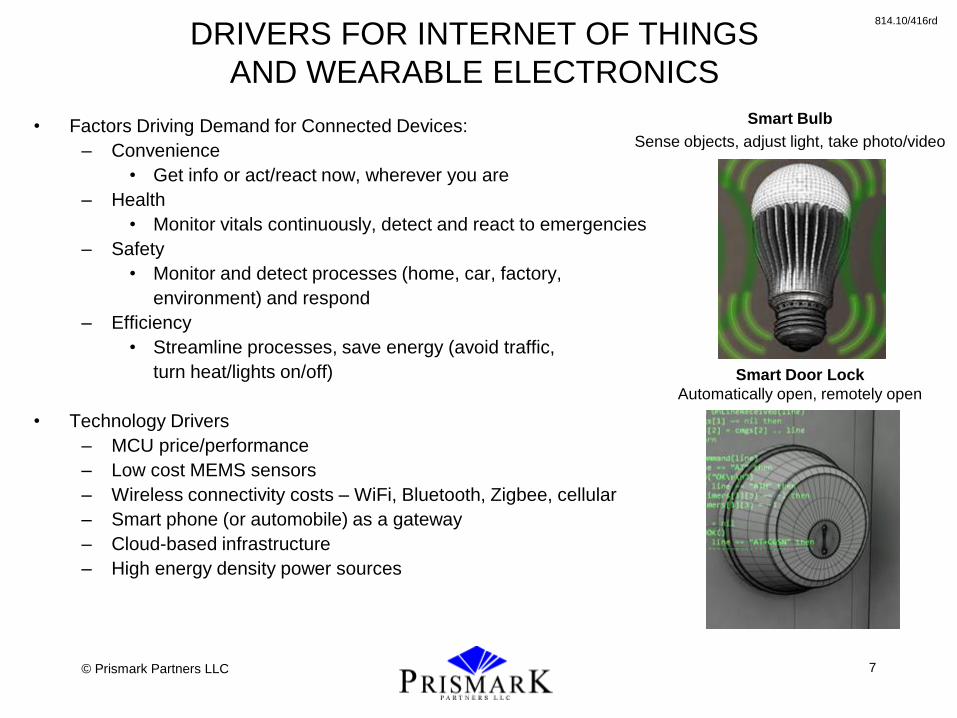

DRIVERS FOR INTERNET OF THINGS

AND WEARABLE ELECTRONICS

• Factors Driving Demand for Connected Devices:

– Convenience

• Get info or act/react now, wherever you are

– Health

• Monitor vitals continuously, detect and react to emergencies

– Safety

• Monitor and detect processes (home, car, factory,

environment) and respond

– Efficiency

• Streamline processes, save energy (avoid traffic,

turn heat/lights on/off)

• Technology Drivers

– MCU price/performance

– Low cost MEMS sensors

– Wireless connectivity costs – WiFi, Bluetooth, Zigbee, cellular

– Smart phone (or automobile) as a gateway

– Cloud-based infrastructure

– High energy density power sources

814.10/416rd

Smart Bulb

Sense objects, adjust light, take photo/video

Smart Door Lock

Automatically open, remotely open

Page 8

© Prismark Partners LLC

8

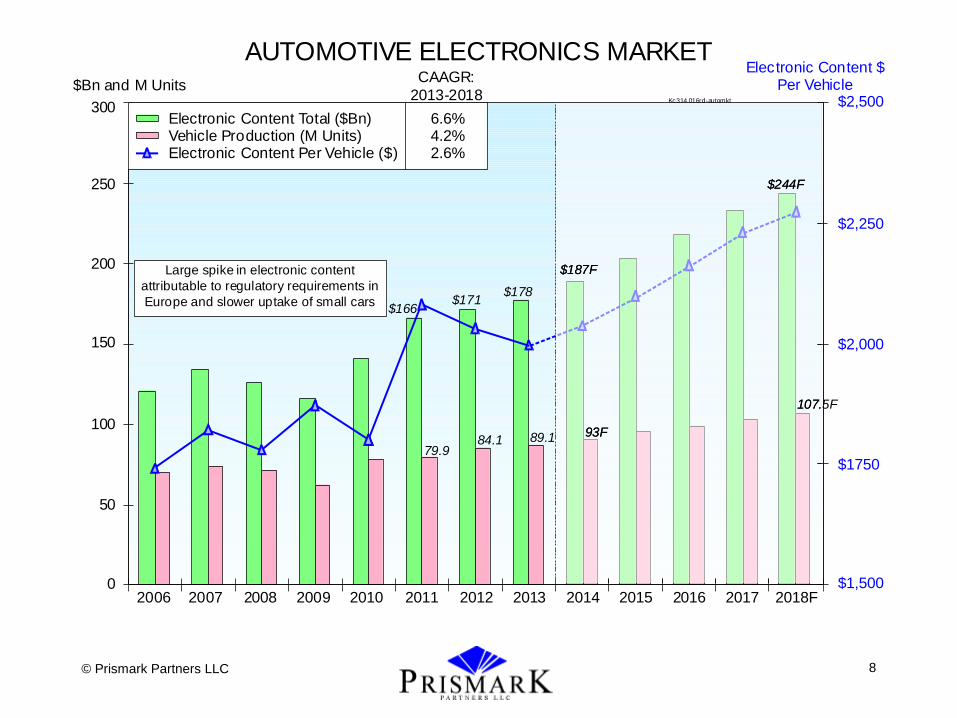

AUTOMOTIVE ELECTRONICS MARKET

0

50

100

150

250

200

300

$1,500

$1750

$2,000

$2,250

$2,500

2007 2009 2011 2013 2014 2017 2018F2015 20162006 2008 2010 2012

$Bn and M UnitsElectronic Content $

Per VehicleCAAGR:

2013-2018

Electronic Content Total ($Bn) 6.6%Vehicle Production (M Units) 4.2%Electronic Content Per Vehicle ($) 2.6%

Large spike in electronic content

attributable to regulatory requirements in

Europe and slower uptake of small cars

79.984.1

$171$166

Kc314.016rd-automkt

89.1

$178

$187F

$244F

107.5F

93F

AUTOMOTIVE ELECTRONICS MARKET

0

50

100

150

250

200

300

$1,500

$1750

$2,000

$2,250

$2,500

2007 2009 2011 2013 2014 2017 2018F2015 20162006 2008 2010 2012

$Bn and M UnitsElectronic Content $

Per VehicleCAAGR:

2013-2018

Electronic Content Total ($Bn) 6.6%Vehicle Production (M Units) 4.2%Electronic Content Per Vehicle ($) 2.6%

Large spike in electronic content

attributable to regulatory requirements in

Europe and slower uptake of small cars

79.984.1

$171$166

Kc314.016rd-automkt

89.1

$178

$187F

$244F

107.5F

93F

Page 9

© Prismark Partners LLC

9

CHANGING IC TEST LANDSCAPE

• Consequences of growth at the “periphery”

– Increasing small form factor IC content – WLP, FC, 3D, embedded

– SiP integration

– Wireless access

– Sensors proliferate

– High volume, low-cost pressure, time-to-market driven

– More complex packaging and test challenges

Page 10

© Prismark Partners LLC

10

300

Bn UnitsKc1013.088bp-ic shipments

250

150

50

0

1980 1985 1990 1995 2000 2005 2010 2020

By 2020, non-leaded packages will account formore than 50% of all ICs

2015

100

200

IC SHIPMENTS BY PACKAGE CATEGORY

3D

Bare Die (COB)

Through Hole (DIP)

Surface Mount (SO, QFP)

Modified Leadframe (QFN, MLF)

Wire Bond Array Package (BGA, CSP, LGA)

Flip Chip Array Package

Direct Flip Chip (DCA, WLCSP)

Page 11

© Prismark Partners LLC

11

314.1/267bp

IC PACKAGE UNIT GROWTH

Package Type

(Bn Units) 2011

% of

Total 2013 2018

% of

Total

CAAGR

2013-2018

Traditional Leadframe

(SO, TSOP, QFP) 101 54% 102 108 40% 1.2%

QFN 21 11% 27 56 21% 16%

Wire Bond CSP

(includes stacked & BOC/DRAM) 28 15% 27 29 11% 0.9%

Wire Bond BGA

(> 19mm package size) 1.1 0.6% 0.9 0.8 0.3% -2.3%

Wire Bond Bare Die

(COB) 11 6% 12 16 6% 5.3%

Flip Chip CSP

(includes DRAM) 1.5 0.8% 4.4 13.4 5% 25%

Flip Chip BGA/PGA/LGA

(> 19mm Package Size) 1.1 0.6% 1.0 1.0 0.4% 0%

Wafer CSP 15 8% 19 35 13% 13%

COF/COG for Display Drivers 7.9 4% 8.7 11.1 4% 4.1%

TOTAL 186.7 100% 202.1 269.4 100% 5.9%

Page 12

© Prismark Partners LLC

12

Kc314.088bp-pitch trends

ARRAY PACKAGE PITCH TRENDS (BGA, CSP, PGA, LGA, WLCSP)(Excludes Small Die DCA, Display Drivers, and RF Modules)

1.27mm0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

10

20

30

40

50

60

70

Bn Units

1.0mm

0.5mm

0.65-0.8mm

0.4-0.45mm

0.3-0.35mm

DCA in Module

Sub 0.5mm was 2% of overall volume in 2008. By 2018 this will increase to 28% or 19Bn units

Page 13

© Prismark Partners LLC

13

APPLE A7 PROCESSOR

• Found in iPhone 5S – 28nm, 1.3GHz – 1GB LPDDR3 as PoP (64-bit) – Top package has 456 balls @0.35mm pitch

• ~14 x 15.5 x 1.0mm PoP

– ~1330 balls @ 0.4mm pitch – LDP/TMV PoP with die back side exposed – Molded underfill

• 10.3 x 9.9mm die – 95µm thick – 150/170µm Sn bump pitch – 65µm bump height, 75µm bump diameter

• 2-2-2 substrate – 360µm thick – 75µm vias, 27µm L/S – Laser via in glass reinforced core – 25µm dielectric and copper thickness

1013.6/193bp

Photo source: Prismark/Binghamton University

400µm

650µm

Page 14

© Prismark Partners LLC

14

0Bn

5Bn

10Bn

15Bn

20Bn

Annual Volume

1995 2000 2005 2010 2015 2020

WLCSP/DCA TIMELINE

kc313.085bp-timeline

5x5-7x7mm5x5-6x6mm

4x4mm

Die Size

4x4mm

1x1-2x3mm

EEPROM, MCU,

Security Chips, Watches

AdditionalDevice Types:Analog, IPD,

MOSFET

Bluetooth,WLAN, TV Chip,

Transceiver

Transceiver, Power

Manager, Image Sensor, Audio Codec

Combo/Connectivity, MCU

Wider adoption outside portable products,

expect up to 8x9mm die size

Wide adoption in

smartphones

Nokia phones with 7-8WLCSP

Page 15

© Prismark Partners LLC

15

BUMPED WAFER PRODUCTION BY PITCH(300mm Equivalent)

2013 2018

50-80 m(TCB)

3%

µ50-80 m(TCB)

1%

µ

100-150 m35%

µ

130-170 m(Solder or

Copper Bump)20%

µ

150-200 m20%

µ

175-250 m

30%

µ(Solder or Copper Bump)

200-800 m30%

µ

300-800 m

30%

µ(Ball Placement)

20-40 m12%

µ30-50 m

(19%

µGold Bump)

Note: Excludes microbump for TSV applications

TOTAL: 14M Wafers TOTAL: 27M Wafers

CAAGR 14%

Kc314.261bp-pitch

Page 16

© Prismark Partners LLC

16

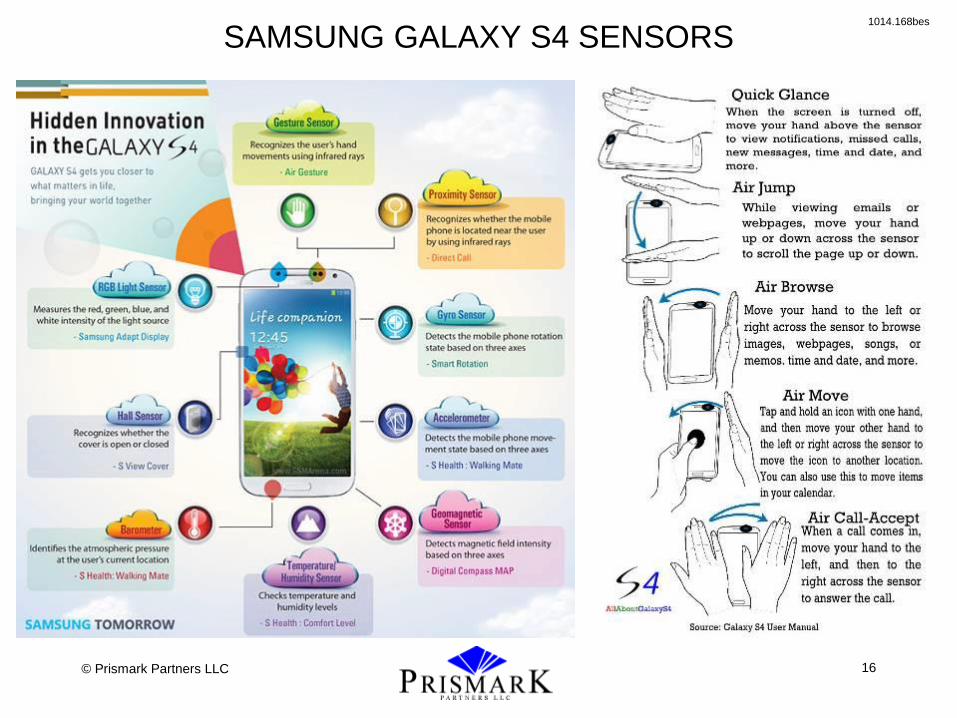

SAMSUNG GALAXY S4 SENSORS 1014.168bes

Page 17

© Prismark Partners LLC

17

GLOBAL MEMS MARKET

2013 2018 CAAGR

2013 – 2018

Units (Bn)

Value ($Bn)

Units (Bn)

Value ($Bn)

Units Value

Inkjet Heads 0.8 1.8 0.8 1.7 0% -1%

DLP 0.01 0.7 0.01 0.7 0% 0%

Pressure Sensors 0.7 1.9 1 2.5 7% 6%

MicroFluidics 0.5 1.2 1.2 2 19% 11%

Accelerometers 2.3 1.8 1.7 1.3 -6% -6%

Gyroscopes 0.65 1.5 0.7 1.5 1% 0%

Digital Compass 0.7 0.6 0.05 0.03 -41% -45%

Combo (Gyro/Accel/Compass) 0 0 1.9 3.7

MEMS Microphones 2.6 0.9 4 1.1 9% 4%

BAW Filters 1 0.3 1.5 0.4 8% 6%

RF MEMS 0.05 0.08 0.3 0.3 43% 30%

Others 0.2 0.3 0.5 0.6 20% 15%

TOTAL 9.51 11.1 13.7 15.8 8% 7%

613.6/099bp

Page 18

© Prismark Partners LLC

18

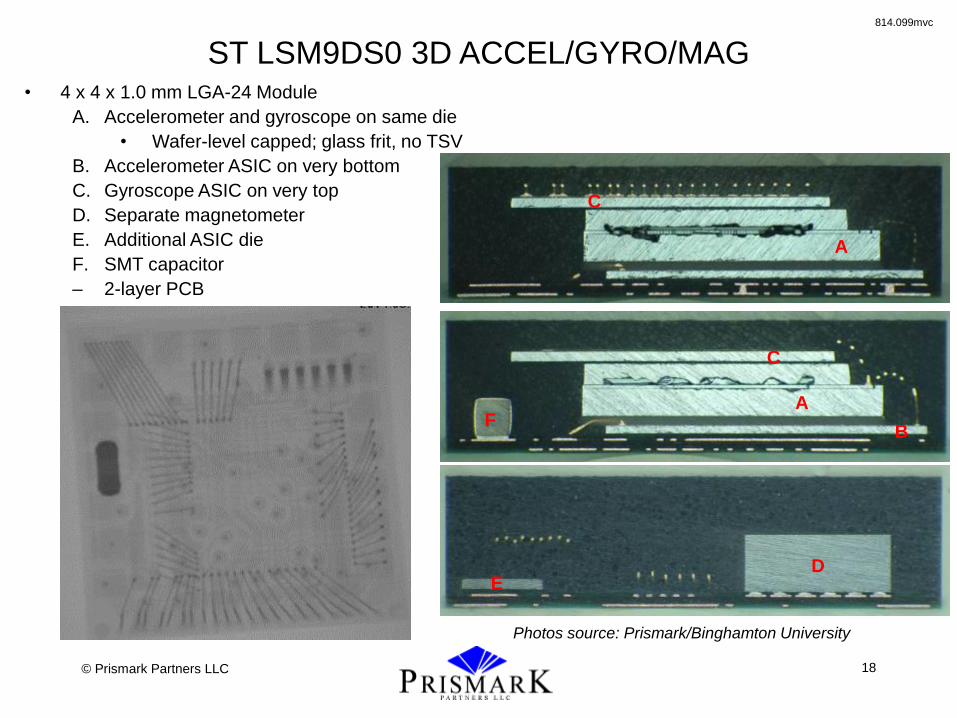

ST LSM9DS0 3D ACCEL/GYRO/MAG • 4 x 4 x 1.0 mm LGA-24 Module

A. Accelerometer and gyroscope on same die

• Wafer-level capped; glass frit, no TSV

B. Accelerometer ASIC on very bottom

C. Gyroscope ASIC on very top

D. Separate magnetometer

E. Additional ASIC die

F. SMT capacitor

– 2-layer PCB

A

C

C

A

B F

Photos source: Prismark/Binghamton University

E D

814.099mvc

Page 19

© Prismark Partners LLC

19

0214.1/105bp

SiP/MCP FORECAST

Product/Package Type Volume (Bn Units)

2013 2018

Forecast Leading Suppliers/Players

Stacked Die In Package and Memory Card

8 11 ASE, SPIL, Amkor, STATS ChipPAC, Samsung,

Micron, SKHynix, Toshiba, SanDisk

Stacked Package on Package – Bottom Package Only

0.8 1.3 Amkor, STATS ChipPAC, ASE, SPIL, Samsung,

Apple, Qualcomm, Sony, Panasonic

PA Centric RF Module 4.3 6.3 RFMD, Skyworks, Anadigics, Renesas,

TriQuint, Avago

Connectivity Module (Bluetooth/WLAN)

0.4 0.5 Murata, Taiyo Yuden, ACSIP, ALPS

Graphics/CPU or ASIC MCP 0.2 0.2 Intel, IBM, Fujitsu, Xlinx, Altera

Leadframe Module (Power/Other)

3 5 NXP, STMicro, TI, Freescale, Toshiba,

Infineon, Renesas, IR, ON Semi

MEMS and Controller 5 8 ST, Analog, Bosch, Freescale, Knowles,

SKHynix, InvenSense Denso

TOTAL 21.7 32.3

Page 20

© Prismark Partners LLC

20

DEVICE LEVEL TRENDS SUMMARY

• Package size reduction is ongoing, but pitch limitations draw a logical path

towards modular and 3D approaches

• A few clear trends are enabling miniaturization

– Fine Pitch Array Packages (0.5 0.4 0.35 0.3/0.25mm)

– Stacked Die (Memory) and Package Stacks (Logic/Memory)

– Wafer Level CSP

– Reduced Z-height Packages (0.3 to 0.6mm)

• 3D-TSV and Silicon Interposer approaches are still in development, with high-

volume products expected in the next three to five years

– Process integration and materials challenges remain

– Thermal, test, and logistics issues

1014.267bes

Page 21

© Prismark Partners LLC

21

PCB EMBEDDED COMPONENTS

• In Volume Production for Modules

Integration of passives and active die

Focus on camera, power management, connectivity, and RF modules

Over one decade of low-volume examples coming from Japan

Continued challenges in process (yield) and infrastructure

No current known production of embedded in main PCB

Embedded passives in IC packages now common for Samsung, Qualcomm, Apple; others such as MediaTek are following suit

• Market Estimates

Embedded actives approaching 200M modules on annual basis

Embedded passives in substrate will become standard practice in mobile products

A few key design wins drive high volumes

• Major Players

DNP, Unimicron, TDK-EPC, Taiyo Yuden, AT&S, SEMCO, CMK, Kyocera Circuit Solutions, Panasonic, Oki, Kinsus, Ibiden, Shinko, etc

Imbera-Daeduck JV lost funding and shut down; IP sold to GE

Historic Leaders such as DNP, CMK, and Kyocera Circuit Solutions have reduced focus

514.7/333bp

Page 22

© Prismark Partners LLC

22

EPCOS BLUETOOTH LE MODULE

• Smallest Module Using PCB Embedding Technology

– Bluetooth Smart (Bluetooth 4.0 Low Energy)

– Only needs power supply and antenna

– 4.6 x 5.6 x 1.0mm

– Targeted at wearable devices

• TDK’s Proprietary SESUB Technology

– Four-layer, 0.3mm thick SESUB substrate

– 0.1mm thick IC embedded between layers two and three

– Quartz resonator, bandpass filter, passives on top

– In volume production at 0.3M units per month

614.333mvc

11 x 6.8 x 1.85mm

Page 23

© Prismark Partners LLC

23

RAPIDLY CHANGING TEST LANDSCAPE

• Tester interfaces and handling systems will need to continue to adapt to evolving IC functional and physical packaging changes driven by high-volume consumer portables and emerging IoT applications

• Within five years, more than 50% of all devices will be delivered in non-traditional packages, WLP, bare die, or modules

• Sensor integration within high-volume, cost-sensitive applications will create especially difficult test challenges

• The good news is that these changes are creating opportunities for new test-related equipment and software solutions

Page 24

© Prismark Partners LLC

24

THANK YOU

The Ultimate Test Methodology?