A Review of developments in The Global & Indian Steel Industry Monthly edition Issue No. 45 December 2019 (Covering November 2019) Compiled on behalf of Indian Steel Association, By Mr. Anup Kashyap, Deputy Manager-Technical Strictly for Internal circulation

Transcript

A Review of developments in

The Global & Indian Steel Industry

Monthly edition

Issue No. 45

December 2019 (Covering November 2019)

Compiled on behalf of Indian Steel Association,

By Mr. Anup Kashyap,

Deputy Manager-Technical

Strictly for Internal circulation

About the Report

❑ The Indian Steel Association introduced a monthly report titled ‘A REVIEW

OF DEVELOPMENTS IN GLOBAL & INDIAN STEEL INDUSTRY’, from August

2016.

❑ The report provides general background information reviewing the status

of the developments in the global and Indian steel industry, pertaining to

raw material, production & consumption, trade, shipping, pricing &

forecasts, country reportage, policy developments, economic parameters

etc.

❑ The consistent format of the report provides an insight into the relevant

aspects of steel scenario globally and domestically .

❑ The information has been sourced from independent third party databases,

knowledge sources and news reports, and the authenticity of the same has

not been independently verified by ISA.

❑ The report is issued in the last week of each month to the members of

Indian Steel Association , various ministries / departments / institutions.

Contents of the Report

SI.

No

Title Page

Number

1. Global Economic Development 4-6

2. Global Steel Development 7-14

3. Domestic Steel Development 15-19

4. Indian Economic Development 20-23

5. About ISA 24-30

GLOBAL ECONOMIC DEVELOPMENTS

4

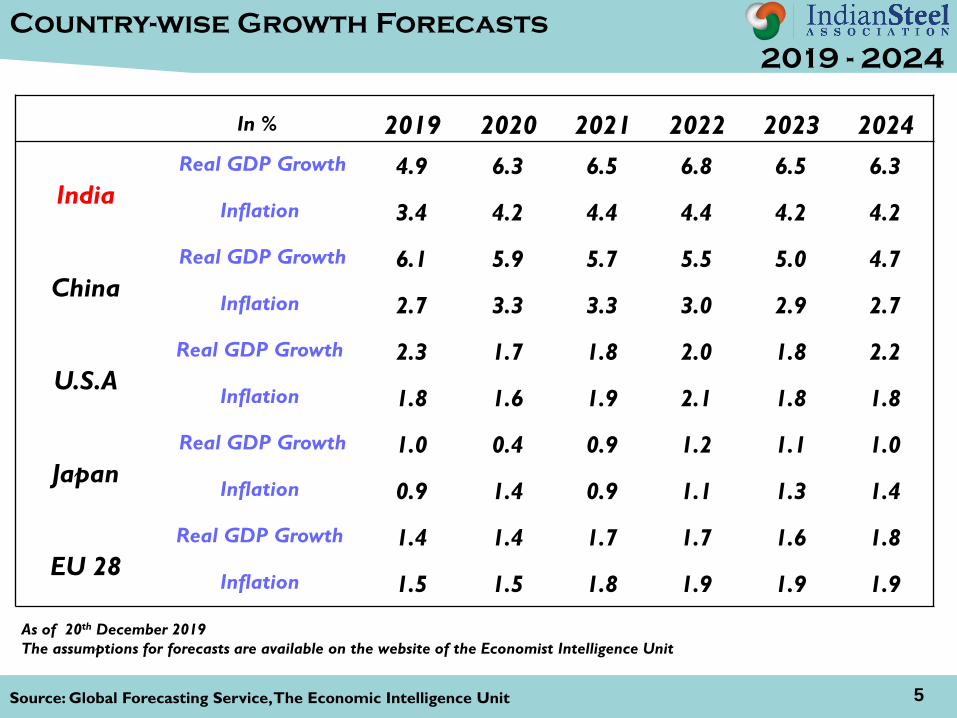

Source: Global Forecasting Service, The Economic Intelligence Unit 5

In % 2019 2020 2021 2022 2023 2024

India

Real GDP Growth 4.9 6.3 6.5 6.8 6.5 6.3

Inflation 3.4 4.2 4.4 4.4 4.2 4.2

China

Real GDP Growth 6.1 5.9 5.7 5.5 5.0 4.7

Inflation 2.7 3.3 3.3 3.0 2.9 2.7

U.S.A

Real GDP Growth 2.3 1.7 1.8 2.0 1.8 2.2

Inflation 1.8 1.6 1.9 2.1 1.8 1.8

Japan

Real GDP Growth 1.0 0.4 0.9 1.2 1.1 1.0

Inflation 0.9 1.4 0.9 1.1 1.3 1.4

EU 28

Real GDP Growth 1.4 1.4 1.7 1.7 1.6 1.8

Inflation 1.5 1.5 1.8 1.9 1.9 1.9

As of 20th December 2019

The assumptions for forecasts are available on the website of the Economist Intelligence Unit

Country-wise Growth Forecasts

2019 - 2024

Source: Global Forecasting service 6

Global Economic Scenario

DECEMBER 2019

▪ The year 2019 was a difficult one for the global economy, as geopolitical uncertainty and a

slowing Chinese economy combined to trigger a global manufacturing downturn.

▪ The Economist Intelligence Unit expects global growth to be marginally faster in 2020.

However, continued political instability-internationally and in many countries-will limit any

pick-up in business confidence and investment, and the balance of risks to the outlook

remains tilted to the downside.

▪ Global growth is forecast to be 2.4% in 2020- modestly higher than the 2.3% growth that

what is currently expected for 2019, but still close to decade lows.

▪ Economic growth in the developed world to slow marginally in 2020, to 1.5%, driven by a

moderation in US growth.

▪ Asia will record a stable growth rate of 4% in 2020, making it the world fastest-growing

region for the sixth consecutive year, with stronger growth in South and South-East Asia

making up for a continued slowdown in China.

▪ In the rest of the emerging world, it is expected a modest recovery from a torrid 2019,

including in Latin America, the Middle East and Sub-Saharan Africa.

GLOBAL STEEL DEVELOPMENTS

7

Source: World Steel Association 8

Global Steel Scenario

November 2019

➢ World crude steel production for the 64 countries reporting to the World Steel Association

(world steel) was 147.8 million tonnes (Mt) in November 2019, a 1.0% decrease compared to

November 2018.

➢ China’s crude steel production for November 2019 was 80.3 Mt, an increase of 4.0% compared

to November 2018.

➢ India produced 8.9 Mt of crude steel in November 2019, down 2.8% on November 2018.

➢ Japan produced 7.7 Mt of crude steel in November 2019, down 10.6% on November 2018.

➢ South Korea’s crude steel production was 5.9 Mt in November 2019, a decrease of 0.5% on

November 2018.

➢ The US produced 7.2 Mt of crude steel in November 2019, a decrease of 2.2% compared to

November 2018.

➢ In the EU, Italy produced 2.0 Mt of crude steel in November 2019, down by 9.8% on November

2018. France produced 1.1 Mt of crude steel in November 2019, an 18.2% decrease compared to

November 2018. Spain produced 1.1 Mt of crude steel in November 2019, down by 10.9% on

November 2018.

Source: World Steel Association

➢ Total Crude steel production from January to November - 2019 was 1684 MT.

➢ The region wise crude steel production is provided in chart below.

RegionJan –Nov. 2019 in

(MT)

Jan- Nov. 2018 in

(MT)

% Change

EU-28 148.451 154.895 -4.2

CIS 91.958 92.374 -0.5

N. America 110.115 110.753 -0.6

S. America 38.062 41.526 -8.3

Africa 12.487 13.383 -6.7

Middle East 33.733 32.552 +3.6

Asia 1209.584 1151.280 +5.1

Oceania 5.654 5.833 -3.1

World 1684.194 1640.234 2.7

Region wise Crude Steel Production

Nov. 2019

➢ Year onYear this reflects an increase of crude steel production over Jan-November 2018 of 2.7%.

9

Source: Chinese iron and Steel Association 10

➢ China’s crude steel output in 2020 is expected to ease from a record high this year to

981 million tonnes.

➢ In the first 10 months of the year, China has churned out 829.22 million tonnes of crude

steel, up 7.4% from a year earlier.

➢ Meanwhile, demand is seen rising 7.3% to 886 million tonnes in 2019, but was expected to

drop from that level by 0.6% in 2020.

➢ Demand for steel in the construction industry is expected to rise 11.2% this year to 478

million tonnes, but is seen slipping 0.6% in 2020.