HAL Id: halshs-00389789 https://halshs.archives-ouvertes.fr/halshs-00389789 Submitted on 29 May 2009 HAL is a multi-disciplinary open access archive for the deposit and dissemination of sci- entific research documents, whether they are pub- lished or not. The documents may come from teaching and research institutions in France or abroad, or from public or private research centers. L’archive ouverte pluridisciplinaire HAL, est destinée au dépôt et à la diffusion de documents scientifiques de niveau recherche, publiés ou non, émanant des établissements d’enseignement et de recherche français ou étrangers, des laboratoires publics ou privés. A Risk Management Approach for Portfolio Insurance Strategies Benjamin Hamidi, Bertrand Maillet, Jean-Luc Prigent To cite this version: Benjamin Hamidi, Bertrand Maillet, Jean-Luc Prigent. A Risk Management Approach for Portfolio Insurance Strategies. 2009. halshs-00389789

Transcript

HAL Id: halshs-00389789https://halshs.archives-ouvertes.fr/halshs-00389789

Submitted on 29 May 2009

HAL is a multi-disciplinary open accessarchive for the deposit and dissemination of sci-entific research documents, whether they are pub-lished or not. The documents may come fromteaching and research institutions in France orabroad, or from public or private research centers.

L’archive ouverte pluridisciplinaire HAL, estdestinée au dépôt et à la diffusion de documentsscientifiques de niveau recherche, publiés ou non,émanant des établissements d’enseignement et derecherche français ou étrangers, des laboratoirespublics ou privés.

A Risk Management Approach for Portfolio InsuranceStrategies

Benjamin Hamidi, Bertrand Maillet, Jean-Luc Prigent

To cite this version:Benjamin Hamidi, Bertrand Maillet, Jean-Luc Prigent. A Risk Management Approach for PortfolioInsurance Strategies. 2009. halshs-00389789

Documents de Travail duCentre d’Economie de la Sorbonne

A Risk Management Approach for Portfolio

Insurance Strategies

Benjamin HAMIDI, Bertrand MAILLET, Jean-Luc PRIGENT

2009.34

Maison des Sciences Économiques, 106-112 boulevard de L'Hôpital, 75647 Paris Cedex 13http://ces.univ-paris1.fr/cesdp/CES-docs.htm

ISSN : 1955-611X

“A Risk Management Approach

for Portfolio Insurance Strategies”∗

Benjamin Hamidi† Bertrand Maillet‡ Jean-Luc Prigent§

- May 2009 -

Abstract

Controlling and managing potential losses is one of the main objec-tives of the Risk Management. Following Ben Ameur and Prigent (2007)and Chen et al. (2008), and extending the first results by Hamidi et al.(2009) when adopting a risk management approach for defining insuranceportfolio strategies, we analyze and illustrate a specific dynamic portfolioinsurance strategy depending on the Value-at-Risk level of the coveredportfolio on the French stock market. This dynamic approach is derivedfrom the traditional and popular portfolio insurance strategy (Cf. Blackand Jones, 1987; Black and Perold, 1992): the so-called “Constant Pro-portion Portfolio Insurance” (CPPI). However, financial results producedby this strategy crucially depend upon the leverage – called the multiple– likely guaranteeing a predetermined floor value whatever the plausiblemarket evolutions. In other words, the unconditional multiple is definedonce and for all in the traditional setting.The aim of this article is to further examine an alternative to the standardCPPI method, based on the determination of a conditional multiple. Inthis time-varying framework, the multiple is conditionally determined inorder to remain the risk exposure constant, even if it also depends uponmarket conditions. Furthermore, we propose to define the multiple as afunction of an extended Dynamic AutoRegressive Quantile model of theValue-at-Risk (DARQ-VaR). Using a French daily stock database (CAC40and individual stocks in the period 1998-2008), we present the main per-formance and risk results of the proposed Dynamic Proportion PortfolioInsurance strategy, first on real market data and secondly on artificialbootstrapped and surrogate data. Our main conclusion strengthens theprevious ones: the conditional Dynamic Strategy with Constant-risk expo-sure dominates most of the time the traditional Constant-asset exposureunconditional strategies.

Following Ben Ameur and Prigent (2007), Chen et al. (2008) and Hamidi et al.(2009), we apply the usual Risk Management approach to a particular type ofportfolio insurance: the Constant Proportion Portfolio Insurance (CPPI - Cf.Black and Jones, 1987; Black and Perold, 1992). In other words, the risk of thenew insured strategy is the true target and not the global asset weight exposureto risky assets as in the traditional approach.The standard general method crucially depends upon the leverage – called themultiple – guaranteeing a predetermined floor whatever the plausible marketevolutions. However, the unconditional multiple is defined once and for all inthe traditional CPPI setting. We propose in this article an alternative to thestandard CPPI method, based on the determination of a conditional multiple.In a time-varying framework, the multiple is conditionally determined in orderthe risk exposure to remain constant, but to depend on market conditions.In other words, while the traditional strategy is indeed a Constant-exposureProportion Portfolio Insurance strategy, the strategy we examine has the maincharacteristic of being a Constant-risk Proportion Portfolio Insurance one.Moreover, we propose to define the conditional multiple as a function of theValue-at-Risk (VaR) of the protected portfolio, which itself is modelled in a time-series framework following Engle and Manganelli (2004) and Gourieroux andJasiak (2008) through a Dynamic AutoRegressive Quantile modelling (DARQ-VaR model). Thus, when the forecasted risk increases, the leverage of the CPPIshould decrease and vice-versa.The paper is organized as follows. After having recalled some basics aboutProportion Portfolio Insurance (PPI), we describe in section 3 the way we modelthe conditional multiple. In section 4, we present and estimate a particularspecification of the general model presented in section 3 and compare it to thetraditional unconditional strategy using real and several realistic artificial seriesbased on the CAC40 Index and its components. Section 5 concludes. Appendix1 justifies the proposed time-varying approach in an Insurance Portfolio context,whilst we briefly present in Appendix 2 the performance measures we use forevaluating the interest of a risk management approach for the Insurance ofPortfolios.

2 Basics about Proportion Portfolio Insurance

The general Portfolio Insurance principle aims to allow investors to recover, atmaturity, a given proportion of their initial capital. One of the standard PPImethods is the Constant Proportion Portfolio Insurance (CPPI). This strategyis based on a specific simple dynamic allocation on a risky asset and on a riskless

2

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

one, aiming to guarantee a predetermined value at the end of the investmentperiod.The management of a cushioned portfolio follows a dynamic portfolio alloca-tion and it is based on the definition of three virtual quantities: the floor, thecushion and the multiple. The floor is the minimum value of the portfolio thatis acceptable for an investor at maturity. The value of the insured portfolio isinvested in a risky asset and in a non-risky asset, in a proportion that varies inorder to insure at any time the guaranteed floor value. Hence, the investmentself-financed strategy aims that the portfolio has, at a certain maturity, a valueequal, at minimum, to the floor, (i.e., a predetermined percentage of the capitaldeposit at the beginning of the management period). The so-called cushion isdefined as the difference between the portfolio value and the guaranteed floor.It represents a certain amount of the value of the portfolio that is dedicated toabsorb some potential market shocks. Its size should be large enough for rep-resenting, each day, the maximum theoretical amount that can be lost withoutcompromising the guaranteed capital.The ratio between the risk-exposed asset value and the cushion corresponds, atany time, to the so-called multiple (defined once for all in the standard strat-egy). The multiple thus reflects the exposure of the portfolio. In its traditionalversion, the cushioned management strategy continuously targets a constantproportion of (unconditional) risk exposure. It means that the amount investedin the risky asset is determined by multiplying the cushion by the multiple.However, the crucial point of this simple strategy is to choose the targeted mul-tiple. For instance, if the risky asset price drops, the value of the cushion mustremain (by definition) superior or equal to zero. Therefore, the portfolio basedon the cushion method will have (theoretically) a value superior or equal to thefloor. Nevertheless, if the (fixed) multiple is too high (and/or the cushion istoo low), a large fall in price of the risky asset may damage the value of theportfolio, which may fall below the guaranteed value. The cushion should thusallow the portfolio manager to absorb a market shock inferior or equal to theinverse of the multiple.In a PPI framework, the multiple has to be at any time below the maximum ofthe (negative) realizations of the underlying risky asset return. The guaranteeis thus perfect in the only case where the unconditional multiple is equal to one.In all other cases (for conditional or unconditional multiples), the guarantee isonly provided according to plausible market conditions, that have to be definedby a set of assumptions regarding the potential loss on the risky asset one mayface.The probabilistic approach offers a pseudo-guarantee, mainly consisting in therespect, at any time, of the guarantee condition at a predefined significance levelof probability. Using the quantile hedging approach, the guarantee constraintis associated to a significance level and the multiple must be lower than theinverse of the conditional quantile of the asset return distribution.Thus, the target multiple can be re-interpreted as the inverse of the maximumloss that can bear the cushioned portfolio before the re-balancing of its riskycomponent, at a given confidence level. Hamidi et al. (2009) propose a first

3

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

conditional multiple model based on Value-at-Risk (VaR). This risk measureis based on a quantile function (i.e., an inverse of the cumulative distributionfunction), and measures the potential loss of a portfolio over a defined periodat a given confidence level. We complement hereafter their first results.

3 From the Extended DARQ-VaR Model to theConditional Multiple in a CPPI Framework

Since it reflects the maximal exposure of the portfolio, the multiple is the cru-cial parameter of CPPI strategies. For a perfect capital guarantee, the multiplemust be lower or equal to the inverse of the maximum loss of the risky assetreturn, until the portfolio manager can rebalance his position. For instance,if the risky asset drops drastically, the cushion must remain positive otherwisethe predetermined floor is passed and the guarantee violated, (i.e., the spread– varying across time – between the portfolio value and the guaranteed floormust be positive). Nevertheless, before the manager can re-adjust his position,the cushion allows the portfolio manager, by construction, for the absorption ashock smaller or equal to the inverse of the (superior limit of) the multiple.Several unconditional multiple determination methods have been developed inthe literature, but they all reduce the risk dimension of the strategy to the riskyasset exposure (see Black and Perold, 1992). Thus, these traditional uncondi-tional methods do not fully take into consideration the risk of the underlyingasset that changes according, for instance, to market conditions. In other words,the risk of the risky asset proportion is considered as a constant through thewhole life of the structured product. Looking at the time-variation of the ampli-tude and intensity of risk (see for instance Longin and Solnik, 1995), we proposeto model the conditional multiple as a function of the VaR. The target multipleis then:

mt = |V aRt (rt−1; β) + dt|−1 (1)

where V aRt (rt−1; β) is the first percentile of the conditional distribution ofdaily returns of the underlying asset, rt corresponds to the periodic return ofthe risky part of the portfolio covered, β is the vector of unknown parameters ofthe conditional percentile function, and dt represents the exceeding maximumreturn during the estimation period.

When modelling the conditional multiple, we hereafter adopt a probabilis-tic quantile hedging approach, based on an extended Dynamic AutoRegressiveValue-at-Risk model (DARQ-VaR), which is written in a particular extendedAsymmetric Slope CAViaR specification - chosen for illustration purposes (seeEngle and Manganelli, 2004), such as:

V aRt (rt; β) = β1 + β2 × V aRt−1 (rt−1; β) + β3 × max (0; rt−1)+β4 × [−min (0; rt−1)]

(2)

where the βi, i = [1, . . . , 4], are several parameters to estimate and rt is the

4

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

risky asset return at time t.The probability of 1% associated to the DARQ-VaR was chosen not only forfocusing on true extremes but also for having enough data points for recoveringgood estimations. Without introducing the parameter dt, the probability ofviolating the floor would have been equal to 1%. Working here at a daily fre-quency, this probability would thus have been too high for describing a realisticinvestor’s demand (a multiple often equal to 30 or so). However, for a lowerrebalancing time frequency (weekly or monthly), values of conditional multiplesbecome more realistic. Moreover, if we assume that the portfolio manager cantotally rebalance his position in one day, this particular estimation of the condi-tional multiple allows the portfolio manager for guaranteeing the predeterminedfloor defined by the investor. More generally, if the centile is well modelled (hitratio not significantly different from 1%, no cluster of exceeding times, and lim-ited exceeding maximum return from the centile) then the guarantee is (almost)insured (see Appendix 1). Finally, since the multiple is here modelled as afunction of DARQ-VaR, it can also be interpreted in terms of Expected Short-fall. The parameter dt allows for taking into account the risky asset dispersionof return in the (fat-)tail of the distribution of the risky asset returns. Thisparameter represents the highest failure of the model, and corresponds to oneof the highest negative returns in the sample. The combination of both VaRand dt is then closely linked to a measure of the Expected Shortfall. The VaRis here monitored (the risky asset allocation depending upon it), and extremereturns are taken into consideration through the parameter dt. The proposedstrategy can then be viewed as an application of Risk Management principlesinto a Portfolio Insurance context: the conditional multiple depends upon theforecasted Value-at-Risk, which depends on its turn to the lagged Value-at-Risk(and returns) and the highest failure of the model over the past. We propose inthe next section to observe what type of results this kind of conditional approachcan provide.

4 Data, Implementation Methods and Empiri-

cal Evidence of the Dynamic Strategy on theFrench Stock Market

We compare hereafter the performances of cushioned portfolios using a previ-ously presented DARQ-VaR specification, and some of the traditional uncondi-tional leveraged CPPI strategies associated to several levels of risk defined byan unconditional multiple fixed once and for all to values ranging from 3 to 13.We use CAC40 daily returns and single returns of its fifty main componentssince inception (stocks changing during the history of the series). The sampleperiod consists of 21 years of daily data, from the 9th of July 1987 to 30th ofApril 2008. This total period consists of 5,242 returns which we split in twoperiods: we use a rolling window of 2,785 returns for dynamically in-sampleestimating the parameters and a post-sample period consisting of 2,457 returns

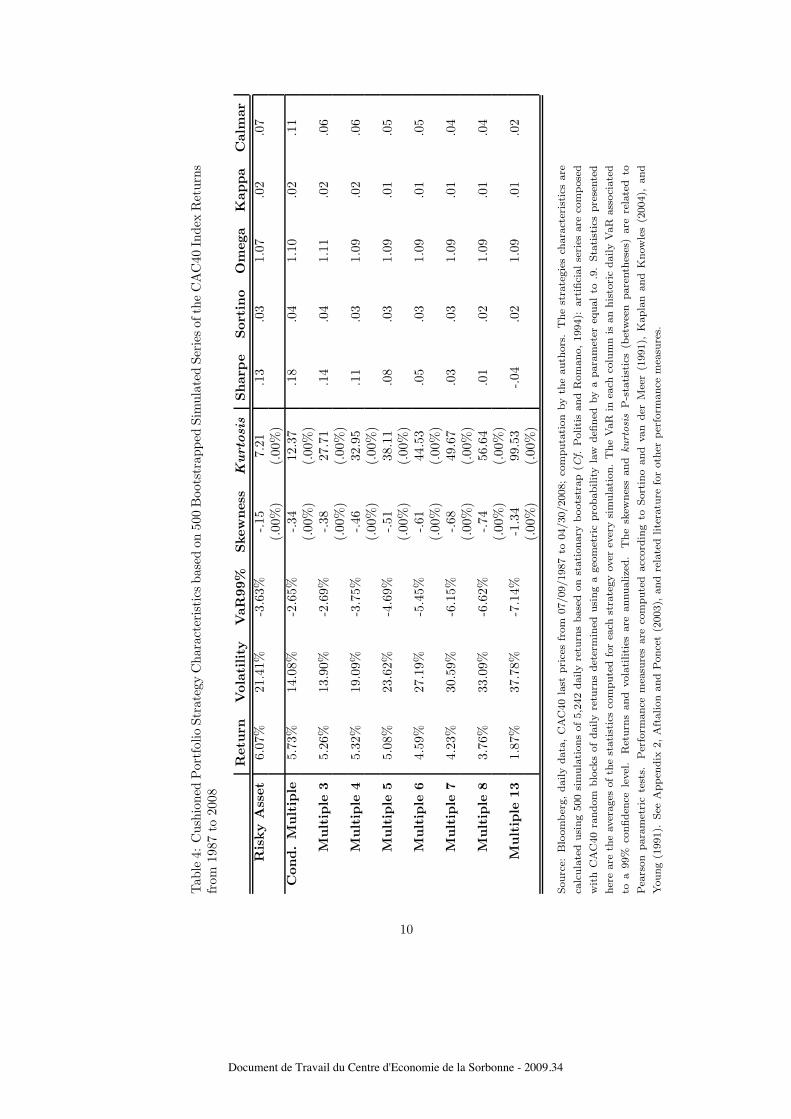

5

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

for out-of-sample testing the various strategies. The following application onthe CAC40 provides only a statistical illustration of the comparison betweenunconditional and conditional multiple-based portfolios built with the same se-ries of returns. However, the proposed self-financed Dynamic PPI strategy canbe easily applied using, for instance, an Exchange Trading Fund on the FrenchIndex, with some transaction costs; moreover, it is worth noticing that a fairbuy-and-hold benchmark should also include the dividends.After having estimated the DARQ-VaR model, we use it for defining daily con-ditional multiples and the related time-varying strategy. We then compare itwith traditional CPPI strategies based on an unconditional multiple used inpractice (between 3 and 13). Comparisons between the conditional multiplestrategy and unconditional methods are presented in Tables 1 to 5. The firstcomparisons are based on observed prices: the CAC40 Index (see Table 1 and2). For limiting the potential impact of the Index construction method, wecomplement the results of the former table by those of Table 3, that concern anequally weighted portfolio based on the fifty main components of the CAC40 In-dex since inception. Table 4 and 5 are related to comparisons based on realisticartificial series rebuilt from the CAC40 series, following first a simple stationarybootstrap (Politis and Romano, 1994) and secondly a surrogate data simulationprocedure (Schreiber and Schmidzt, 2000).All results, however, converge in the same way: the conditional Dynamic Strat-egy with Constant-risk exposure dominates most of the time the traditionalConstant-asset exposure unconditional strategies in terms of return per unit ofrisk, combining a return close to the one of the best unconditional strategy,with a volatility amongst the lowest. While the risk of the conditional strategyis defined ex ante (with an almost Constant-risk exposure), it, however, appears- ex post - among the best portfolio strategies.

5 Concluding Remarks

The model and estimation methods proposed in this article provide a rigorousframework for fixing, at each date, a conditional multiple, preserving a con-stant exposition to risk defined by a shortfall constraint within an actual RiskManagement approach. The dynamic setting starts with the conditioning ofthe time-varying multiple, through an extended DARQ-VaR for monitoring thetrue risk exposure of the structured product.Hamidi et al. (2009) show that this strategy proves efficiency in the Americanstock market, whilst we complement here their results by both using CAC40and a basket of French stocks, and artificial series built using bootstrap andsurrogate techniques (thus limiting the dependency of the results to startingdates and asset price paths). This work will be improved in the near future,explicitly replacing the function of the conditional centile by a coherent measureof risk - namely the Expected Shortfall, expressed in a quantile regression condi-tional setting, for having a more robust and flexible estimation of the conditionalmultiple.

6

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

Tab

le1:

Cus

hion

edPor

tfol

ioSt

rate

gyC

hara

cter

istics

onth

eC

AC

40In

dex

from

1998

to20

08

Ret

urn

Vol

atility

VaR

99%

Ske

wnes

sK

urto

sis

Shar

pe

Sor

tino

Om

ega

Kap

pa

Cal

mar

Ris

ky

Ass

et3.

07%

23.0

3%-4

.14%

-.02

5.90

.00

.02

1.04

.02

.05

(.00

%)

(.00

%)

Con

d.

Mult

iple

3.03

%13

.18%

-2.6

5%-.36

10.0

3.0

0.0

31.

06.0

2.1

0(.00

%)

(.00

%)

Mult

iple

32.

13%

6.80

%-1

.36%

-.76

12.1

8-.13

.03

1.07

.02

.11

(.00

%)

(.00

%)

Mult

iple

41.

79%

9.00

%-1

.98%

-.78

11.1

8-.13

.02

1.05

.01

.07

(.00

%)

(.00

%)

Mult

iple

51.

43%

11.7

0%-2

.58%

-.83

10.4

1-.13

.01

1.04

.01

.04

(.00

%)

(.00

%)

Mult

iple

61.

02%

13.6

4%-3

.11%

-.82

9.85

-.15

.01

1.03

.01

.03

(.00

%)

(.00

%)

Mult

iple

7.6

7%17

.07%

-3.9

3%-.84

10.5

9-.14

.01

1.03

.01

.02

(.00

%)

(.00

%)

Mult

iple

8.4

3%19

.13%

-4.4

5%-.88

11.2

5-.13

.01

1.03

.01

.01

(.00

%)

(.00

%)

Mult

iple

13.1

3%20

.67%

-4.5

6%-2

.02

29.9

4-.14

.01

1.03

.00

.00

(.00

%)

(.00

%)

Sourc

e:B

loom

ber

g,

daily

data

,C

AC

40

last

pri

ces

from

07/09/1987

to04/30/2008;

com

puta

tion

by

the

auth

ors

.R

eturn

sand

Vola

tiliti

esare

annualize

d.

The

VaR

ofea

chco

lum

nis

an

his

tori

cdaily

VaR

ass

oci

ate

dto

a99%

confiden

cele

vel

.T

he

skew

nes

sand

kurt

osi

sP

-sta

tist

ics

(bet

wee

n

pare

nth

eses

)are

rela

ted

toPea

rson

para

met

ric

test

s.Per

form

ance

mea

sure

sare

com

pute

dacc

ord

ing

toSort

ino

and

van

der

Mee

r(1

991)

and

Kapla

n

and

Know

les

(2004).

See

Appen

dix

2,A

ftalion

and

Ponce

t(2

003)

and

rela

ted

lite

ratu

refo

roth

erper

form

ance

mea

sure

s.

7

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

Tab

le2:

Con

dition

alM

ultipl

eSt

rate

gyR

anki

ngvs

Unc

ondi

tion

alSt

rate

gies

acco

rdin

gto

Per

form

ance

Mea

sure

s

Shar

pe

Sor

tino

Om

ega

Kap

pa

Cal

mar

Info

rmat

ion

Fam

aJe

nse

nC

ondit

ional

Mult

iple

Ran

kin

g1

12

12

11

3

Sourc

e:B

loom

ber

g,daily

data

,C

AC

40

last

pri

ces

from

07/09/1987

to04/30/2008;co

mputa

tion

by

the

auth

ors

.In

sure

dst

rate

gie

spre

sente

din

table

1are

ranked

acc

ord

ing

tose

ver

alper

form

ance

mea

sure

s(f

or

defi

nit

ions,

see

refe

rence

sin

Table

1,A

ppen

dix

2and

Aft

alion

and

Ponce

t,2003).

8

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

Tab

le3:

Cus

hion

edPor

tfol

ioSt

rate

gyC

hara

cter

istics

onan

Equ

ally

Wei

ghte

dC

ompo

nent

sps

eudo

-CA

C40

Por

tfol

iofr

om19

98to

2008

Ret

urn

Vol

atility

VaR

99%

Ske

wnes

sK

urto

sis

Shar

pe

Sor

tino

Om

ega

Kap

pa

Cal

mar

Ris

ky

Ass

et9.

96%

20.1

7%-3

.75%

-.03

7.16

.33

.05

1.11

.03

.20

(.00

%)

(.00

%)

Con

d.

Mult

iple

4.59

%12

.93%

-2.5

1%-.68

9.1

.10

.03

1.08

.02

.13

(.00

%)

(.00

%)

Mult

iple

33.

58%

8.29

%-1

.86%

-.86

10.8

6.0

4.0

41.

10.0

2.1

6(.00

%)

(.00

%)

Mult

iple

43.

36%

11.3

1%-2

.56%

-.91

11.8

4.0

1.0

31.

07.0

2.1

1(.00

%)

(.00

%)

Mult

iple

52.

81%

14.7

7%-3

.34%

-1.0

112

.00

-.03

.02

1.06

.01

.07

(.00

%)

(.00

%)

Mult

iple

62.

85%

19.0

9%-4

.19%

-.97

12.1

5-.02

.02

1.05

.01

.06

(.00

%)

(.00

%)

Mult

iple

72.

65%

23.7

4%-5

.31%

-.94

11.8

9-.03

.02

1.05

.01

.05

(.00

%)

(.00

%)

Mult

iple

82.

24%

29.4

1%-6

.20%

-1.0

512

.84

-.04

.02

1.05

.01

.03

(.00

%)

(.00

%)

Mult

iple

13.3

1%45

.46%

-9.9

3%-1

.42

17.4

-.07

.02

1.06

.01

.00

(.00

%)

(.00

%)

Sourc

e:B

loom

ber

g,daily

data

,C

AC

40

fift

ym

ain

com

ponen

tla

stpri

ces

from

12/31/1987

to01/16/2008;

com

puta

tion

by

the

auth

ors

.T

he

equally

wei

ghte

dport

folio

isbase

don

the

fift

ym

ain

CA

C40

com

ponen

tssi

nce

itsin

cepti

on

and

isre

bala

nce

dea

chday

.R

eturn

sand

vola

tiliti

esare

annualize

d.

The

VaR

inea

chco

lum

nis

an

his

tori

cdaily

VaR

ass

oci

ate

dto

a99%

confiden

cele

vel

.T

he

skew

nes

sand

kurt

osi

sP

-sta

tist

ics

(bet

wee

npare

nth

eses

)

are

rela

ted

toPea

rson

para

met

ric

test

s.Per

form

ance

mea

sure

sare

com

pute

dacc

ord

ing

toSort

ino

and

van

der

Mee

r(1

991),

Kapla

nand

Know

les

(2004),

and

Young

(1991).

See

Appen

dix

2,A

ftalion

and

Ponce

t(2

003)

and

rela

ted

lite

ratu

refo

roth

erper

form

ance

mea

sure

s.

9

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

Tab

le4:

Cus

hion

edPor

tfol

ioSt

rate

gyC

hara

cter

isti

csba

sed

on50

0B

oots

trap

ped

Sim

ulat

edSe

ries

ofth

eC

AC

40In

dex

Ret

urns

from

1987

to20

08

Ret

urn

Vol

atility

VaR

99%

Ske

wnes

sK

urto

sis

Shar

pe

Sor

tino

Om

ega

Kap

pa

Cal

mar

Ris

ky

Ass

et6.

07%

21.4

1%-3

.63%

-.15

7.21

.13

.03

1.07

.02

.07

(.00

%)

(.00

%)

Con

d.

Mult

iple

5.73

%14

.08%

-2.6

5%-.34

12.3

7.1

8.0

41.

10.0

2.1

1(.00

%)

(.00

%)

Mult

iple

35.

26%

13.9

0%-2

.69%

-.38

27.7

1.1

4.0

41.

11.0

2.0

6(.00

%)

(.00

%)

Mult

iple

45.

32%

19.0

9%-3

.75%

-.46

32.9

5.1

1.0

31.

09.0

2.0

6(.00

%)

(.00

%)

Mult

iple

55.

08%

23.6

2%-4

.69%

-.51

38.1

1.0

8.0

31.

09.0

1.0

5(.00

%)

(.00

%)

Mult

iple

64.

59%

27.1

9%-5

.45%

-.61

44.5

3.0

5.0

31.

09.0

1.0

5(.00

%)

(.00

%)

Mult

iple

74.

23%

30.5

9%-6

.15%

-.68

49.6

7.0

3.0

31.

09.0

1.0

4(.00

%)

(.00

%)

Mult

iple

83.

76%

33.0

9%-6

.62%

-.74

56.6

4.0

1.0

21.

09.0

1.0

4(.00

%)

(.00

%)

Mult

iple

131.

87%

37.7

8%-7

.14%

-1.3

499

.53

-.04

.02

1.09

.01

.02

(.00

%)

(.00

%)

Sourc

e:B

loom

ber

g,daily

data

,C

AC

40

last

pri

ces

from

07/09/1987

to04/30/2008;

com

puta

tion

by

the

auth

ors

.T

he

stra

tegie

sch

ara

cter

isti

csare

calc

ula

ted

usi

ng

500

sim

ula

tions

of5,2

42

daily

retu

rns

base

don

stati

onary

boots

trap

(Cf.

Politi

sand

Rom

ano,1994):

art

ifici

alse

ries

are

com

pose

d

wit

hC

AC

40

random

blo

cks

of

daily

retu

rns

det

erm

ined

usi

ng

ageo

met

ric

pro

bability

law

defi

ned

by

apara

met

ereq

ual

to.9

.Sta

tist

ics

pre

sente

d

her

eare

the

aver

ages

ofth

est

ati

stic

sco

mpute

dfo

rea

chst

rate

gy

over

ever

ysi

mula

tion.

The

VaR

inea

chco

lum

nis

an

his

tori

cdaily

VaR

ass

oci

ate

d

toa

99%

confiden

cele

vel

.R

eturn

sand

vola

tilities

are

annualize

d.

The

skew

nes

sand

kurt

osi

sP

-sta

tist

ics

(bet

wee

npare

nth

eses

)are

rela

ted

to

Pea

rson

para

met

ric

test

s.Per

form

ance

mea

sure

sare

com

pute

dacc

ord

ing

toSort

ino

and

van

der

Mee

r(1

991),

Kapla

nand

Know

les

(2004),

and

Young

(1991).

See

Appen

dix

2,A

ftalion

and

Ponce

t(2

003),

and

rela

ted

lite

ratu

refo

roth

erper

form

ance

mea

sure

s.

10

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

Tab

le5:

Cus

hion

edPor

tfol

ioSt

rate

gyC

hara

cter

istics

base

don

500

Surr

ogat

edSi

mul

ated

Seri

esof

the

CA

C40

Inde

xR

etur

nsfr

om19

87to

2008

Ret

urn

Vol

atility

VaR

99%

Ske

wnes

sK

urto

sis

Shar

pe

Sor

tino

Om

ega

Kap

pa

Cal

mar

Ris

ky

Ass

et6.

39%

21.3

8%-3

.62%

-.15

7.32

.15

.03

1.07

.02

.09

(.00

%)

(.00

%)

Con

d.

Mult

iple

4.92

%14

.64%

-2.7

6%-.21

14.2

8.1

1.0

41.

09.0

2.0

9(.00

%)

(.00

%)

Mult

iple

34.

17%

14.2

6%-2

.75%

-.46

29.8

7.0

6.0

31.

09.0

2.0

7(.00

%)

(.00

%)

Mult

iple

43.

65%

19.2

5%-3

.78%

-.53

38.1

2.0

2.0

21.

07.0

1.0

5(.00

%)

(.00

%)

Mult

iple

52.

97%

23.3

7%-4

.61%

-.56

46.3

9-.01

.02

1.07

.01

.04

(.00

%)

(.00

%)

Mult

iple

62.

31%

26.4

2%-5

.24%

-.56

55.3

7-.04

.02

1.06

.01

.03

(.00

%)

(.00

%)

Mult

iple

71.

76%

28.5

4%-5

.62%

-.62

67.4

6-.05

.02

1.06

.01

.02

(.00

%)

(.00

%)

Mult

iple

81.

38%

29.8

2%-5

.78%

-.69

82.2

4-.06

.02

1.06

.01

.01

(.00

%)

(.00

%)

Mult

iple

13.4

7%32

.16%

-5.3

6%-.52

185.

63-.09

.02

1.08

.01

.00

(.00

%)

(.00

%)

Sourc

e:B

loom

ber

g,

daily

data

,C

AC

40

last

pri

ces

from

07/09/1987

to04/30/2008;

com

puta

tion

by

the

auth

ors

.T

he

stra

tegy

chara

cter

isti

csare

calc

ula

ted

usi

ng

500

sim

ula

tions

of

5,2

42

daily

retu

rns

base

don

asu

rrogate

data

tech

niq

ue

(Cf.

Sch

reib

erand

Sch

mid

zt,

2000):

ori

gin

alse

ries

of

daily

retu

rns

are

firs

tra

ndom

lyto

tally

re-o

rder

edand

then

seco

nd

pair

-wis

eper

mute

dunti

lth

enew

seri

essh

are

som

esi

milari

ties

wit

hth

eori

gin

al

one

(±10%

of

firs

tco

rrel

ati

on

coeffi

cien

tsand

of

the

long

mem

ory

para

met

erof

vola

tility

).T

he

stati

stic

spre

sente

dher

eare

the

aver

ages

of

the

stati

stic

sco

mpute

dfo

rea

chst

rate

gy

over

ever

ysi

mula

tion.

The

VaR

inea

chco

lum

nis

an

his

tori

cdaily

VaR

ass

oci

ate

dto

a99%

confiden

cele

vel

.T

he

skew

nes

sand

kurt

osi

sP

-sta

tist

ics

(bet

wee

npare

nth

eses

)are

rela

ted

toPea

rson

para

met

ric

test

s.Per

form

ance

mea

sure

sare

com

pute

dacc

ord

ing

toSort

ino

and

van

der

Mee

r(1

991),

Kapla

nand

Know

les

(2004),

and

Young

(1991).

See

Appen

dix

2,

Aft

alion

and

Ponce

t(2

003)

and

rela

ted

lite

ratu

refo

roth

erper

form

ance

mea

sure

s.

11

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

6 References

Aftalion F. and P. Poncet, (2003), Les techniques de mesure de performances,Economica, 139 pages.

Ben Ameur H. and J.-L. Prigent, (2007), “Portfolio Insurance: Determinationof a Dynamic CPPI Multiple as Function of State Variables”, THEMA WorkingPaper, University of Cergy, 22 pages.

Bertrand Ph. and J.-L. Prigent, (2002), “Portfolio Insurance: the ExtremeValue Approach to the CPPI Method”, Finance 23(2), 69-86.

Black F. and R. Jones, (1987), “Simplifying Portfolio Insurance”, Journal ofPortfolio Management 14(1), 48-51.

Black F. and A. Perold, (1992), “Theory of Constant Proportion Portfolio In-surance”, Journal of Economic Dynamics and Control 16(3), 403-426.

Bontemps Ch. and N. Meddahi, (2005), “Testing Normality: A GMM Ap-proach”, Journal of Econometrics 124(1), 149-186.

Chen J., C. Chang, J. Hou and Y. Lin, (2008), “Dynamic Proportion PortfolioInsurance using Genetic Programming with Principal Component Analysis”,Expert Systems with Applications: An International Journal 35(1), 273-278.

Engle R. and S. Manganelli, (2004), “CAViaR: Conditional AutoRegressiveValue-at-Risk by Regression Quantiles”, Journal of Business and EconomicStatistics 22(4), 367-381.

Gourieroux Ch. and J. Jasiak, (2008), “Dynamic Quantile Models”, Journal ofEconometrics 147(1), 198-205.

Hamidi B., E. Jurczenko and B. Maillet, (2009), “A CAViaR Modelling for aSimple Time-Varying Proportion Portfolio Insurance Strategy”, Bankers, Mar-kets & Investors, forthcoming 2009, 21 pages.

Kaplan P. and J. Knowles, (2004), “Kappa: A Generalized Downside Risk-adjusted Performance Measure”, Journal of Performance Measurement 8(3),42-54.

Longin F. and B. Solnik, (1995), “Is the Correlation in International EquityReturns Constant: 1960-1990?”, Journal of International Money and Finance14(1), 3-26.

Politis D. and J. Romano, (1994), “The Stationary Bootstrap”, Journal of theAmerican Statistical Association 89(428), 1303-1313.

Schreiber T. and A. Schmidtz, (2000), “Surrogate Time-series”, Physica D 142,346-382.

Sortino F. and R. van der Meer, (1991), “Downside Risk”, Journal of PortfolioManagement 17(4), 27-31.

Young T., (1991), “Calmar Ratio: A Smoother Tool”, Futures 20(1), 40.

12

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

7 Appendix

Appendix 1: Proportion Portfolio Insurance based on a Quantile Cri-terion in a Marked Point Process Framework

As we argue in the text, despite the fact that the multiple is conditional andthus time-varying, the portfolio is still guaranteed under some conditions. In-deed, a guaranteed portfolio is defined so that the portfolio value will always beabove a predefined floor at a given high probability level. Assume that the riskyprice follows a marked point process, which is characterized by the sequence ofmarks (Sl)l∈N∗

+and the increasing sequence of times (Tl)l∈N∗

+at which the risky

asset varies.In the CPPI framework, the first following “global” quantile hedging conditioncan be considered (see Bertrand and Prigent, 2002):

Prob [∀t ≤ T, Ct ≥ 0] ≥ 1 − δ (3)

where Ct is the cushion defined as the spread between the portfolio value and theguaranteed floor, Prob[.] stands for the unconditional probability and (1 − δ) fora probability confidence level. Splitting the complete period, denoted [0, ..., T ],into various L successive subperiods [Tl, Tl+1[, the previous equation is equiva-lent to define the multiple m as such (see Bertrand and Prigent, 2002):

m ≤ [f−1

T (1 − δ)]−1

(4)

where f−1T (.) is the quantile function, evaluated at a risky asset return for

which the inverse function - denoted fT (.), is equal to (1 − δ) - a specifiedunconditional quantile, as such:

fT (r) =+∞∑

l=1

Prob [Ml ≤ r | Tl ≤ T < Tl+1] × Prob [Tl ≤ T < Tl+1] (5)

with Prob[. | Tl ≤ T < Tl+1] denoting the conditional probability given the eventTl ≤ T < Tl+1 and:

Ml = Maxk=[1,...,L]

−r1, ...,−rk (6)

where rt = (St − St−1) /St−1 is the risky asset return at time t.

Following the same principle in a time-varying framework now, another “lo-cal” quantile condition can also be introduced, based this time on a conditionalquantile corresponding to a conditional probability confidence level denoted(1 − α), such as, for any time t ∈ [Tl, Tl+1[ with t ≤ T :

Prob[CTl

> 0 | ΩTl−1

] ≥ 1 − α (7)

where ΩTl−1 is the σ-algebra generated by the set of all intersections ofCTl−1 > 0

with any subset ΩTl−1 of the σ-algebra generated by the observation of themarked point process until time Tl−1.

13

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

From previous condition (7), an upper bound on the multiple can be deducedaccording to specific assumptions (see Ben Ameur and Prigent, 2007, for thespecial case of GARCH-type models with a deterministic transaction-time).

Appendix 2: About some Performance Measures

Sharpe RatioThe Sharpe ratio is one of the most popular performance measures. It is de-fined as the ratio between the excess return about the risk free rate over thevolatility of the analysed portfolio. However, use of the Sharpe ratio in perfor-mance measurement is subject to some criticisms since returns do not displaya normal distribution. For example, the use of dynamic strategies results in anasymmetric return distribution, as well as fat tails, leading to the danger thatthe use of standard risk and performance measures will underestimate risk andoverestimate performance per unit of risk.

Sortino, Omega and Kappa MeasuresLower partial moments measure risk by negative deviations of the realized re-turns, to a minimum acceptable return. The lower partial moment of order n iscalculated using power n. Because lower partial moments consider only nega-tive deviations to a minimal acceptable return (which could be zero), they are amore appropriate measure of risk than the standard deviation, which considersnegative and positive deviations from expected return (see Sortino and van derMeer, 1991). The choice of the order n determines the extent to which the de-viations are weighted. The lower partial moment of order 0 can be interpretedas the shortfall probability, the lower partial moment of order 1 as the expectedshortfall, and the lower partial moment of order 2 as the semi-variance. Theorder of the lower partial moment to be chosen is linked to the downside-riskaversion of the investor. The more he is averse, the higher the order (since itgives extra weights to extreme pay-offs). The Omega (see Shadwick and Keat-ing, 2002), the Sortino ratio (see Sortino and van der Meer, 1991), and Kappa3 (see Kaplan and Knowles, 2004) make use respectively of the lower partialmoments of order 1, 2 and 3.

Calmar RatioAs the Sharpe ratio, the Calmar ratio is defined as the ratio between the excessreturn about the risk free rate over a risk measure of the analysed portfolio. TheCalmar ratio (see Young, 1991), uses the maximum drawdown over a three-yearperiod as the risk measure at the denumerator instead of the standard devia-tion of returns. The drawdown being the loss incurred over a certain investmentperiod (peak-to-valley price difference), drawdown-based performance measuresare particularly popular in practice, since they are better connected to the over-all loss that can face an investor (without any reference to a specific observationfrequency).

14

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34

Jensen MeasureThe Jensen measure considers the average return above what is explained bythe capital asset pricing model. The beta factor is generally calculated usingthe correlation between the returns of a market index and the returns of theinvestment fund. The Jensen measure is, however, often criticized because itcan be manipulated by leveraging the fund return, and because it is based onthe assumption that alpha and beta can be clearly split.

15

Document de Travail du Centre d'Economie de la Sorbonne - 2009.34