16

A ROADMAP TO IMPROVE RULES FOR TAXING MULTINATIONALS A FAIRER FUTURE FOR GLOBAL TAXATION

| Date post: | 23-Apr-2018 |

| Category: |

Documents |

| Upload: | trinhquynh |

| View: | 215 times |

| Download: | 0 times |

A ROADMAP TO IMPROVE RULES FOR TAXING MULTINATIONALS

A FAIRER FUTURE FOR GLOBAL TAXATION

ABOUT ICRICT

The Independent Commission for the Reform of International CorporateTaxation aims to promote the international corporate tax reform debatethrough a wider and more inclusive discussion of international tax rulesthan is possible through any other existing forum; to consider reformsfrom a perspective of public interest rather than national advantage; andto seek fair, effective and sustainable tax solutions for development.ICRICT has been established by a broad coalition of civil society andlabor organizations including Action Aid, Alliance Sud, Christian Aid, theCouncil of Global Unions, the Global Alliance for Tax Justice, Oxfam,Public Services International, Tax Justice Network and the World Councilof Churches. ICRICT is supported by Friedrich-Ebert-Stiftung and by the Ford Foundation.

For more information, visit the ICRICT website at icrict.com.

© ICRICT February 2018

We came together as the IndependentCommission for the Reform of InternationalCorporate Taxation in March 2015 to considerways to reorient the existing system ofinternational taxation away from serving thewealthy few and to focus it instead onaddressing the needs of the vast majority ofthe population, in particular those living inpoverty, the vulnerable and the marginalized.

A dysfunctional international taxation systemhas allowed Multinational Enterprises (MNEs)to avoid bearing their fair share of taxation,with severe consequences in countries whereessential public services and infrastructurespending are cut, and the tax burden isshifted onto ordinary citizens, usually in theform of regressive consumption taxes such asvalue-added taxes (VAT).

Our aim was to promote a wider and moreinclusive discussion, which we believe isessential to ensure the creation of aninternational tax system that contributes tofunding sustainable development.

The existing system of international taxationhas been exploited by MNEs to shift largeportions of their overall profits to low taxjurisdictions. This system has furtherexacerbated tax competition, by pressuringcountries into lowering tax rates. While therehave been multiple global agreements toavoid double taxation of MNEs’ profits, thetransfer price rules used by these agreements

have been unsuccessful in avoiding theerosion of the tax base and ensuring thatprofits are taxed where the substantiveeconomic activities of the MNEs actually takeplace. These agreements have also failed tofind a common ground to avoid a race to the bottom.

Having taken into account the views of MNEsand their stakeholders, we called for a widerand more inclusive discussion of measures toreform the rules governing taxation of globalprofits of these enterprises, in our initialDeclaration (2015), in our evaluation of theOECD’s Base Erosion and Profit Shifting(“BEPS”) initiative (2015) and in our reporton Four Ways to Tackle Tax Competition(2016). In this paper we take stock of thestate of reform efforts and outline a path ahead.

In 2012, when the G20 called on the OECDto reform the international corporate taxsystem through the BEPS initiative, it askedfor a thorough reexamination of rules oninternational corporate taxation with the twingoals of instilling greater transparency and

INTRODUCTION

» THE INDEPENDENT COMMISSION FOR THE REFORM OF INTERNATIONAL CORPORATE TAXATION

// 3

“Our aim was to promote a wider

and more inclusive discussion, whichwe believe is essential to ensure thecreation of an international taxsystem that contributes to fundingsustainable development.

”

ensuring that profits are taxed whereeconomic activities occur, so enablingdeveloping countries to enhance theirrevenue capacity, as mobilizing domesticresources is critical to financing theirdevelopment. As a result of this initiative, theOECD has taken some steps in the rightdirection but much more needs to be done toaddress the core deficiencies of the existingsystem for taxing MNEs’ corporate profits.

The template for country-by-country reportingis a major step forward. Country by countryreporting can play an important role inensuring that profits are declared and taxesare paid where each MNE has a realeconomic presence. By making the basicrelevant information openly available,country-by-country reporting has the potential

of allowing governments and members of thepublic to identify misalignment of profits inrelation to actual economic activity. For thesereasons, we consider critical that thethreshold for country-by-country reporting belowered to apply to a large majority of MNEsand that these reports be made public. Ifproperly implemented, the information wouldbenefit not just tax administrators but alsocivil society and other stakeholders (e.g.shareholders, investors, regulators) inmonitoring whether income and corporationtax are aligned with the location of economicactivities. However, we regret that thearrangements for access to this information,especially by developing countries, are stillinadequate. We are convinced that the mosteffective solution would be open publicationof these reports.

» THE INDEPENDENT COMMISSION FOR THE REFORM OF INTERNATIONAL CORPORATE TAXATION

// 4

// 5

Unfortunately, we are of the view that untilnow the OECD’s proposals provide only apatch-up of existing failed approaches andhave failed to address the more fundamentalissue of profit shifting that was part of themandate for reform. In particular, therevisions to transfer pricing rules continue tocling to the underlying fiction that a MNEconsists of separate independent entitiestransacting with each other at arm’s length.The transfer pricing rules attempt toconstruct prices for the transactions amongentities that are part of MNEs as if they wereindependent, which is inconsistent with theeconomic reality of a modern-day MNE—aunified firm organized to reap the benefits ofintegration across jurisdictions. Large MNEsare oligopolies, and in practice there are notruly comparable independent local firms thatcan serve as benchmarks.

The OECD reform proposals, while helpful atthe margins, do not help resolve the basicchallenge of ensuring that MNEs pay taxeswhere they have real economic activities takeplace and create value. They still provide toomuch opportunity for profit shifting,especially through the exploitation ofintangible assets (intellectual property,trademarks, etc.). This is an issue for bothdeveloping and advanced countries, but sofar tax rules have prioritized the perspective

of advanced countries which are the homes ofMNEs. This is a major reason why they havefailed to ensure that profits are taxed whereactivities take place (at the “source”), infavour of where the companies that receiveincome are based (in the country of“residence”), which can easily bemanipulated.

We therefore reiterate our call for a paradigmshift in formulating rules for taxing MNEs. Ifnational taxing authorities and multilateralinstitutions truly wish to stop BEPS, theymust abandon the fiction that a MNE is madeof separate independent entities and can usetransfer prices to determine profit allocationand instead move towards a unitary taxationapproach. To contribute to such a change inpractice, we have evaluated a range ofproposals and ideas, which are outlined here.Our general conclusion is that globalformulary apportionment, coupled with aminimum corporate tax rate, would be themost effective and fairest version of unitarytaxation. Acknowledging the scale of thechallenge in such a move, and to support thereorientation of the rules towards this goal,we also endorse some more immediateoptions for improvement, especially fordeveloping countries.

“If national taxing authorities and multilateral institutions truly wish to stop

tax avoidance, they must abandon the fiction that a multinational is made ofseparate independent entities and can use transfer prices to determine profitallocation and instead move towards a unitary taxation approach

”

While each has advantage and drawbacks, inour view the fairest and most effectiveapproach would be unitary taxation withformulary apportionment.

A unitary approach should apportion theMNE’s global income to the differentjurisdictions based on objectively verifiablefactors rather than resort to the fiction ofarm’s-length transactions or that one couldpossibly calculate what arm’s-length pricesmight look like.

These factors, such as employment, sales,resources used, fixed assets, etc., should be

chosen to reflect the MNE’s real economicactivity in each jurisdiction. Just as important,these factors cannot be easily moved aroundthe group to avoid taxation. Relocatingemployees to a low-tax jurisdiction involvesmuch more than transferring intangible assetsto a letterbox company in such a jurisdiction,and a firm has even less power over thelocation of its customers.

Furthermore, these objective factors reflect indifferent ways actual economic activity, whilethe separate entity principle and transferpricing rules enable profit shifting to MNE’sentities lacking economic activities.

» THE INDEPENDENT COMMISSION FOR THE REFORM OF INTERNATIONAL CORPORATE TAXATION

// 6

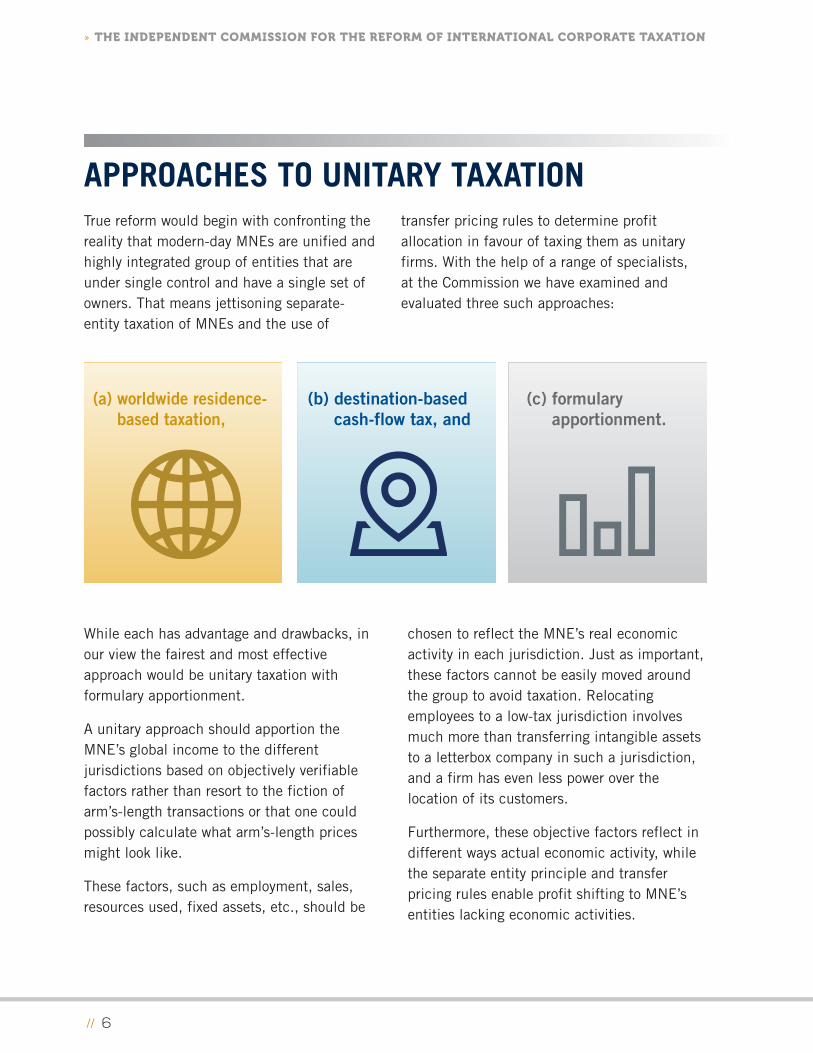

(a) worldwide residence-based taxation,

(b) destination-basedcash-flow tax, and

(c) formularyapportionment.

APPROACHES TO UNITARY TAXATIONTrue reform would begin with confronting thereality that modern-day MNEs are unified andhighly integrated group of entities that areunder single control and have a single set ofowners. That means jettisoning separate-entity taxation of MNEs and the use of

transfer pricing rules to determine profitallocation in favour of taxing them as unitaryfirms. With the help of a range of specialists,at the Commission we have examined andevaluated three such approaches:

It is the Commission view that globalformulary apportionment is the only methodthat allocates profits in a balanced way usingfactors reflecting both supply (e.g., assets,employees, resources used) and demand(sales). Neither can create value without the other.

We are aware of the two major criticismswhich are frequently made of formularyapportionment: first that states could notagree on a formula, and secondly that theenterprise could still play jurisdictionsagainst one another, by focusing on thefactors in the formula.

In the Commission’s view, both thesearguments overlook the point that, inchoosing a suitable formula and the corporatetax rate, states would need to take intoaccount interacting factors: not only the taxrevenue it would produce, but also the effectson inward investment. This creates a basis forcompromise and convergence between states.

Whilst the sales factor in the formula cannotbe manipulated, apportioning profitsaccording to other measures of economicactivity, such as employees and assets, mayaffect inward investment. This may pressurecountries to veer towards single factor (sales)formulary apportionment. However, salesbased apportionment may limit the tax baseof developing countries, where much incomeis generated by asset- and labor-intensiveactivities. A suitable formula will, therefore,need to reflect the different needs of, and benegotiated by, both advanced and developingcountries.

Unitary taxation with formulary apportionmentwould establish a much clearer, moreeffective, and fairer method of allocating thetax base of MNEs. Whilst formularyapportionment will effectively eliminate profitshifting, countries will still be able tocompete against each other by lowering thecorporate tax rate to incentivise investment or

// 7

“It is the Commission view that

global formulary apportionment isthe only method that allocatesprofits in a balanced way usingfactors reflecting both supply (e.g.,assets, employees, resources used)and demand (sales). Neither cancreate value without the other.

”

» THE INDEPENDENT COMMISSION FOR THE REFORM OF INTERNATIONAL CORPORATE TAXATION

// 8

the relocation of activities – pressures whichare, of course, also present in the currentsystem. It is therefore important to avoid aposition where a move to formularyapportionment further exacerbates the race tothe bottom in corporate tax rates.

To forestall this competition and the resultantdistortionary effects, global formularyapportionment should be accompanied by an

agreed minimum rate for taxing allapportioned profits. At the Commission webelieve that such a system of multi-factorglobal formulary apportionment, together witha minimum corporate tax rate, offers the bestmethod of ensuring that source countrieswhere the activities generating MNE’s profitstake place receive their fair share of taxrevenues from these profits.

As already indicated, the Commissionevaluated two other approaches which alsoentail unitary taxation: residence-basedworldwide taxation (RBWT); and a destination-based cash flow tax (DBCFT). However, weconcluded that they are both inadequate.

Under RBWT, the home country of a MNEwould tax the enterprise’s global profits, butwith full credit for foreign income taxes paid.Thus, instead of apportioning the MNE’sprofits to different jurisdictions, RBWTallocates the rights to tax those profits amongthe jurisdictions. It gives the initial right to taxto the source jurisdiction, retaining ultimatetaxing rights (net of credits due for foreigntaxed paid) for the country of residence of the

MNE’s parent company. This has theadvantage of removing the temptation forsource countries to offer tax incentives toattract investment, since the profits wouldanyway be taxed in the parent’s jurisdiction.However, RBWT is unlikely to be of benefit todeveloping countries, where fewer MNEsparent companies are resident.

Furthermore, RBWT’s critical taxconsequences would depend on identifying theresidence jurisdiction. Regrettably, however,no matter how the jurisdiction of residence isdefined, that definition would remain subjectto manipulation. Focusing on the place ofincorporation would be futile, as corporatecharters are easily relocated. Some have

“At the Commission we believe that a system of multi-factor global

formulary apportionment, together with a minimum corporate tax rate, offersthe best method of ensuring that source countries where the activitiesgenerating MNE’s profits take place receive their fair share of tax revenuesfrom these profits.

”

OTHER APPROACHES

suggested looking through to ultimate owners,by defining residence on the basis of themajority of shareholders. This would requirereliable and regularly updated share registers.Even this may not help much, as financialderivatives would allow individuals torenounce nominal ownership while continuingto receive the economic benefits. This wouldmake it easy for MNEs to relocate their homejurisdiction (or “invert”) to one which offers alow tax rate.

In our view, the manipulability of thedefinition of the residence jurisdiction, whichis central to an RBWT regime, is a fatal flawwhen it comes to taxing MNEs. But residenceshould continue to be the linchpin of asystem for taxing individuals. And for thatpurpose, the Commission encouragesreinforcing the definition of residency andadopting other measures to deteropportunistically timed moves to tax havenjurisdictions, and the abuse of corporatevehicles by individuals. One model is the US

“exit tax,” which is imposed on individualsrenouncing their residency and which valuestheir worldwide asset holdings at currentmarket prices.

A DBCFT would tax the MNE’s global profitsin the country where sales to the MNE’sultimate customers take place, after allowingimmediate expensing of all cash outlays,including capital investments and labor costs.It would be economically equivalent to asubtraction-method value added tax withdeduction of payroll expenses. Proposals forsuch an approach were put forward in the USin 2016, and extensively debated in the firstpart of 2017, but have now been rejected,due to a number of drawbacks.

First, it would raise difficult practicalquestions of taxing a MNE with little or nophysical presence in the jurisdiction, soeffective collection would need cooperationbetween states. Furthermore, disallowingdeduction of foreign production costs (theborder adjustment) would likely be treated

// 9

as protectionism under the rules of the WorldTrade Organization, leading to trade wars.

Finally, developing countries with smallconsumer markets, especially those relying onexports of mineral resources, would raise littlerevenue through DBCFT as exports would notbe taxable and profits will only be taxed in the

country where sales to the exporting MNE’sultimate customers take place.

We believe that these unattractiveconsequences also disqualify the DBCFT as afeasible alternative to global formularyapportionment with a minimum tax rate.

While a system of formulary apportionment isthe long-term aim, we are convinced thatadditional measures can be adopted in theshort term leading in this direction. Suchreforms can move the current system awayfrom the dysfunctional independent entityprinciple and use of transfer pricing rules, andrealign the rules to treating MNEs according tothe economic reality that they operate asunitary enterprises.

The EU draft legislation on the commonconsolidated corporate tax base (CCCTB) is atpresent the best move in the right direction. Itwould provide multi-factor formularyapportionment of the combined income of acommonly controlled group, although onlywithin the EU. ICRICT therefore stronglysupports this initiative. However, we believethe EU should adopt an approach thatprevents the shifting of profits outside the EU.

The Commission also supports approaches forallocating income to a MNE’s operatingsubsidiaries without the need for a search forso-called comparable transactions used to test

the arm's length nature of transactionsbetween MNE’s affiliates.

One approach that rejects the pursuit ofmythical “arms-length comparables” is theprofit-split method, which the OECD hasaccepted since 1995.This method apportionsthe combined profits of relevant relatedaffiliates of the MNE, based on “allocationkeys” which reflect each entity’s contributionto the generation of profit, albeit at atransaction-level rather than at an entity-level.Work is still continuing on this method as partof the BEPS project, and we recommend thatit should be systematized and extended.

Another alternative has been proposed,described as the shared net margin method.This would simply ascribe to a MNE’s localaffiliate a net profit rate set as an appropriatefraction of the global net profit rate of thecorporate group as a whole. The methodassumes, quite reasonably, that a MNE isunlikely to try to understate its globalprofitability in its consolidated accounts, asthat would put it at a disadvantage in thecapital markets. The benchmark fraction of the

» THE INDEPENDENT COMMISSION FOR THE REFORM OF INTERNATIONAL CORPORATE TAXATION

// 10

STEPS ALONG THE ROAD

group’s net profitability percentage which thelocal affiliate would be required to earn wouldbe set to ensure meaningful, although stillrelatively modest, tax revenue for the sourcejurisdiction. Since the profit rate would beapplied to earnings before interest, the taxbase would not be eroded by means ofintragroup loans.

Brazil currently applies a variant of thismethod, specifying different sets of rules forlocal affiliates to determine the maximumamounts of deductible expenses and theminimum amounts of taxable income, basedon fixed gross margins according to the typesof businesses or transaction. These rulesminimize the need for subjective judgmentand discretion, so they have proved easy toadminister, and have resulted in a limitednumber of conflicts and court cases betweenMNEs and the Brazilian tax authority.

These are essentially methods forapportioning profits, opting for the simplicityof a fixed margin over the malleability ofarm’s-length transfer pricing. They wouldprovide a more effective approach especiallyfor developing countries, where it would be awaste of scarce resources to try to developthe skills needed to apply other methods.

The Commission also proposes unilateraladoption of formulary apportion as a backstop

to arm’s-length transfer pricing results. In theabsence of global coordination andagreement, an individual country or regioncould consider implementing formulary

// 11

“While a system of formulary apportionment is the long-term aim, we are

convinced that additional measures can be adopted in the short term leadingin this direction. Such reforms can move the current system away from thedysfunctional independent entity principle and use of transfer pricing rules,and realign the rules to treating MNEs according to the economic reality thatthey operate as unitary enterprises.

”

apportionment as part of a domesticalternative minimum tax regime. In such aregime, formulary apportionment woulddetermine the income base for computing analternative minimum corporation tax.

The country could define the local corporationtax base by applying a multi-factor formula toa MNE’s global income, and compute theminimum tax payable on that apportionedincome, for example at 80 percent of theregular corporation tax rate. The minimum taxwould be payable if it exceeds thejurisdiction’s regular corporation tax payablecomputed on the MNE’s local income asdetermined under conventional arm’s-lengthtransfer pricing methods.

Such an alternative minimum tax regimecould be enacted as domestic legislationwithout the need to repudiate existingmultilateral agreements and commitments tothe arm’s-length principle, including theOECD transfer pricing guidelines. This wouldextend the concept of “safe harbors”

accepted by the OECD, which aresimplification measures that relieve eligibletaxpayers from certain obligations otherwiseimposed by general transfer pricing rules. Itwould be similar in effect to other unilateralanti-abuse measures, including the UnitedKingdom’s diverted profits tax, that alreadyserve as an adjunct to arm’s-length transfer pricing.

We believe that unilaterally adopted, either asan anti-abuse rule or a safe harbor, profitapportionment methods can play animportant role in ensuring that tax is paidwhere real economic activities take place.

» THE INDEPENDENT COMMISSION FOR THE REFORM OF INTERNATIONAL CORPORATE TAXATION

// 12

“We believe that unilaterally

adopted, either as an anti-abuserule or a safe harbor, profitapportionment methods can play animportant role in ensuring that tax ispaid where real economic activitiestake place.

”

// 13

Since its establishment, at the Commissionwe have highlighted the urgent need toreorganize the institutional architecture forinternational taxation in the light of economicglobalization. We believe that all countriesshould have a voice in reforming theinternational corporate tax system. The OECDshould not be the only body where thesediscussions should take place. Not allcountries have a seat at the table in theG20/OECD BEPS process. Moreover, thediscussions in BEPS public consultationmeetings have been dominated bymultinational corporations, who consistentlyoutnumber civil society, academic, labor, andcountry representatives combined, and areoften doubly represented by their tax advisersand special industry groups in addition tocorporate executives.

Hence, tax rules have prioritized theperspective of MNEs, and of advancedcountries which are the homes of MNEs. Thisis a major reason why they have failed toensure that profits are taxed at source, whereactivities take place, in favour of residence,

which can easily be manipulated. Only afterwidespread public pressure for reform did theOECD launch the BEPS project. It has soughtlegitimacy by obtaining support andparticipation from the G20 countries. Andonly after the main outputs were released,participation has now been offered to allstates through the Inclusive Framework onBEPS and some cooperation with otherrelevant organizations, including the UNCommittee, has now been establishedthrough the Platform for Collaboration on Tax.

This structure is disjointed and dysfunctional.It clearly falls far short of a truly global taxbody, for which repeated calls have beenmade. Only the UN’s universal membershipand open and democratic structure can givefull voice to the tax policymakers and theentire civil society from all countries. Wetherefore renew our call for internationaltaxation to be brought under the aegis of theUN, which alone can provide the legitimacyfor rules to coordinate such a central elementin the sovereignty of all states.

INSTITUTIONAL FRAMEWORK

“Only the UN’s universal membership and open and democratic

structure can give full voice to the tax policymakers and the entire civilsociety from all countries. We therefore renew our call for internationaltaxation to be brought under the aegis of the UN, which alone can providethe legitimacy for rules to coordinate such a central element in thesovereignty of all states.

”

In directing the OECD to come up with anaction plan against BEPS, the G20 leaderswere responding to the groundswell of publicsentiment in their countries against MNEs’dodging their fair share of taxes by attributingprofits artificially to subsidiaries in tax havenjurisdictions. The outputs of the BEPS projectso far have not really addressed the morefundamental issues of profit shifting that werepart of its mandate.

As members of this Commission, withbackgrounds in government, academia, andcivil society from across the globe, we seek tobe receptive to the voices of all MNE

stakeholders, including those who hadprompted the BEPS project but ironicallyseemed shut out from it. Having heard from awide cross-section of stakeholders and havinganalyzed the evidence, we renew our call tomove away from arm’s-length principle andtowards a unitary approach to taxing MNEs.The fairest and most effective version ofunitary taxation is multi-factor global formularyapportionment with a minimum corporate taxrate. We urge global leaders to adopt aroadmap towards this goal, including moreshort-term measures which would be moreeffective, easier to administer, and providegreater certainty, than the current defectivemethods.

The current system is feeding the historicallevels of inequality, impeding the fulfillment ofhuman rights, tearing away at the global socialfabric and endangering future economicgrowth prospects. We are convinced thatwithout a real global tax reform, the delivery ofpromises made in the 2030 Agenda forSustainable Development will be severelycompromised. The world’s leaders now need todecide whether or not they signed up to thosepromises in good faith.

“The fairest and most effective version of unitary taxation is multi-factor

global formulary apportionment with a minimum corporate tax rate. We urge global leaders to adopt a roadmap towards this goal, including moreshort-term measures which would be more effective, easier to administer,and provide greater certainty, than the current defective methods.

”

CONCLUSION

// 14

“ Tax policies of one country can have dire effects on other countries’

ability to mobilize tax revenues to educate their children, provide adequatehealthcare, and build safe roads and bridges.

// 15

ICRICT COMMISSIONERS

Ms. Eva Joly was born in Norwayand is a Member of the EuropeanParliament where she serves asVice-Chair of the SpecialCommittee on Tax rulings.

Rev. Suzanne Matale is the Head of the Zambian Council ofChurches.

Ms. Kim S. Jacinto Henares, from the Philippines, is an InternationalConsultant. Until recently, she served asthe Commissioner of the PhilippinesBureau of Internal Revenue andrepresented her country on the OECDGlobal Forum’s Transparency andExchange of Information and OECD GlobalForum’s Base Erosion and Profit Shifting.

Mr. Léonce Ndikumana was bornin Burundi and is a Professor ofEconomics at the University ofMassachusetts.

Thomas Piketty, from France, isprofessor of economics at the ParisSchool of Economics.

Mr. M. Govinda Rao is the formerMember of the FinanceCommission, Member of theEconomic Advisory Council to thePrime Minister of India, andDirector of the National Institute ofPublic Finance and Policy in India.

Ms. Magdalena SepúlvedaCarmona from Chile, is a HumanRights Lawyer and recentlyserved as the United NationsSpecial Rapporteur on ExtremePoverty and Human Rights.

Mr. Joseph Stiglitz is from theUnited States and UniversityProfessor at ColumbiaUniversity. In 2001, he wasawarded the Nobel MemorialPrize in Economics.

Mr. Edmund Fitzgerald, from theUnited Kingdom, is Professor ofInternational Development Finance,Oxford University and Fellow of StAntony’s College, Oxford.

Ms. Ifueko Omoigui Okauru served asCommissioner General of Nigeria’sFederal Inland Revenue Service andwas a Member of the Committee ofExperts on International Cooperationin Tax Matters. She is currentlyManaging Partner of ComplianceProfessionals Plc.

Mr. José Antonio Ocampo (Chairperson)is Colombian and former UnitedNations Under-Secretary General andformer Minister of Finance of Colombia.He is currently a Professor at ColumbiaUniversity.

Gabriel Zucman, from France, isassistant professor of economics atUniversity of California, Berkeley.

The Independent Commission for theReform of International CorporateTaxation

Contact: [email protected]