28

1 BANK INDONESIA Managing Editor, Journal of Islamic Monetary Economics and Finance A s c a r y a

1

BANK INDONESIAManaging Editor, Journal of Islamic Monetary Economics and Finance

A s c a r y a

2

1 . I N T R O D U C T I O N

2. ISLAMIC MICROFINANCE

3. BAITUL MAAL WAT TAMWIEL

4. BMT for SDGs in INDONESIA

5. CONCLUSION & RECOMMENDATION

O U T L I N E

3

1. INTRODUCTION

▪ Under current secular economic system, conventional finance is mainly commercial finance whichexcludes social finance. The objective of maximizing profit in commercial finance is mostly conflictingwith the objective of triple bottom-line (outreach, sustainability and welfare impact) in socialfinance. Meanwhile, conventional commercial finance is inherently unstable (Summer, 2002), whiletriple bottomline in conventional social finance is impossible to be achieved (Zeller and Meyer, 2002)due to mission drift (Armendariz, et al., 2013) and commercialization (Hamada, 2010), so that theintegration between conventional commercial finance and conventional social finance to achieve thewellbeing of the society is very unlikely.

4

1. INTRODUCTION

▪ Under Islamic economic system, Islamic finance is not only about commercial finance, but also coverssocial finance with similar objective to achieve falah (wellbeing and prosperity in this world and inthe hereafter). Meanwhile, Islamic commercial finance is inherently stable (Aziz, 2010), while Islamicsocial finance could simultaneously achieve triple bottom-line (Ascarya, et al., 2015).

▪ Moreover, Islamic finance encompass Islamic commercial finance (such as partnership, real activities,governance and ethical), as well as Islamic social finance (such as zakat and waqf), which couldaddressed SDG’s goals.

5

▪ The idea of Sustainable Development Goals were inspired by the success of Millennium DevelopmentGoals (MDGs), which seemed to be uneven across regions and countries, especially the most vulnerable byvirtue of their sex, age, disability, ethnicity or geographic location (Thakkar, 2015, p. 1).

▪ The goals of SDGs are to achieve a combination of economic development, environmental sustainability,and social inclusion (triple bottom line approach to human wellbeing), which are in line with thedevelopmental motives of nations (Sachs, 2012, p. 2206).

▪ This short presentation aims to show that Islamic microfinance in Indonesia, could better addressed SDG’sgoals, especially in improving the wellbeing of the poor and micro enterprises.

1. INTRODUCTION

6

1. INTRODUCTION

2. ISLAMIC MICROFINANCE2.1 The Concept of Islamic Microfinance

2.2 Micro Enterprises in Indonesia

3. BAITUL MAAL WAT TAMWIEL

4. BMT for SDGs in INDONESIA

5. CONCLUSION & RECOMMENDATION

O U T L I N E

7

2.1 ISLAMIC MICROFINANCE

▪ Islamic microfinance can be viewed as a combination of microfinance and Islamic finance, so that itretains mainstream microfinance best practices and models, while modifying the conducts, productsand services to make them comply with Shari’ah, which promote justice, fairness and equity. Islamicmicrofinance can range from fully charity-based, a certain combination of charity-based and market-based, to fully market-based models.

▪ Islamic microfinance provides a variety of Islamic micro-financial products and services to fulfill avariety financial need of poor and low income people which in accordance with Islamic teachings,including micro financing, micro saving, micro investment, micro takaful, qardh (free loan), billpayment, money transfers for a variety of purpose, and other newer form of financial services.

Poor Clients Needs

Microfinance Services

Working Capital Education, birth,

marriage Death, asset protection

Access to funds sent by relatives

Old age Illness and other emergencies

Microenterprise loans

Save place to save

Insurance Remittances and

Transfers Pensions

Loan for emergencies

needs

8

2.2 MICRO ENTERPRISES IN INDONESIA

▪ Micro Enterprises (ME) in Indonesia have always been playing an important role in Indonesianeconomy. After 1998 Asian crisis, especially in rural area, ME considered as a safety valve in theprocess of national economic recovery in enhancing economic growth, reducing unemployment rateand aleviating poverty. Number of ME accounts for 98.8% (or 55.9 million) of total enterprises inIndonesia in 2012.

▪ With its specialties – especially with its low financial capital –, ME could produce in the short-termprocess. Having simple management and huge unit volume scattered in the whole nation, broughtabout ME to have better resistant toward the fluctuation of business cycle.

Number GDP Labor Export*

Micro 55.856.176 98.79% 35.81% 99.859.517 90.12% 1.51%

Small 629.418 1.11% 9.68% 4.535.970 4.09% 3.45%

Medium 48.997 0.09% 13.59% 3.262.023 2.94% 11.48%

Large 4.968 0.01% 40.92% 3.150.645 2.84% 83.56%

MSMEs 56.534.592 99.99% 59.08% 107.657.509 97.16% 16.44%

Source: Ministry of Cooperation and SMEs, 2012; * 2011 data.

9

1. INTRODUCTION

2. ISLAMIC MICROFINANCE

3. BAITUL MAAL WAT TAMWIEL3.1 Baitul Maal and Baitut Tamwiel

3.2 BMT as a Sustainable IMFI Model

3.3 BMT as Agent of Holistic Financial Inclusion

3.4 BMT as Integrated Islamic Microfinance Model

3.5 Compare the Practice of IIMF Model by BMT

4. BMT for SDGs in INDONESIA

5. CONCLUSION & RECOMMENDATION

O U T L I N E

10

▪ Baitul Maal collects zakat, infaq, shadaqah, and waqf funds from their respective donor, i.e., muzakki(zakah), munfiq (infaq/shadaqah) and wakif (waqf). These funds subsequently are distributed to theirrespective recipients. Zakah can only be distributed to 8 groups of people (asnaf). Zakat could be used forrecovery, empowerment and development programs of the recipients.

3.1 Baitul Maal wat Tamwiel (BMT)Baitul Maal

11

▪ Baitut Tamwil collects fund from its members. Initial capital comes from its members, just likecooperatives. Meanwhile, voluntary deposits and safe keeping could come from members and non-members. When funding is short, BT could find it from external sources, such as Apex institutions, Islamicbanks or foreign sources. Subsequently, BT could extend financing to its members customers mainly forproductive purposes using various equity-based and debt-based Islamic contracts.

Baitut Tamwiel3.1 Baitul Maal wat Tamwiel (BMT)

12

▪ There are 4 (four) sustainable MFI model, including: 1) Grameen Model; 2) Cooperative-BMT Model; 3)Rural Bank Model; and 4) Micro Banking Unit Model (Ascarya, 2014).

▪ BMT (Grameen model as well as Individual model) is a sustainable IMFI model for the poor and MicroEnterprise – ME (Ascarya, 2014).

3.2 BMT as a Sustainable IMFI Model

MFI MODEL Extreme Poor Active Poor Low MEs Med MEs High MEs SEs

Grameen Rp0-1 M Rp1-5 M

Coop-BMT Rp1-5 M Rp5-10 M

Rural Bank Rp5-10 M Rp10-50 M

MBU Rp10-50 M Rp50-100 M

13

▪ Holistic Financial Inclusion (HFI) is an integration of social inclusion carried out by Baitul Maal division andfinancial inclusion carried out by Baitut Tamwil division under the scope of Shariah objectives (Ascarya,2016).

3.3 BMT as Agent of Holistic Financial Inclusion

14

▪ BM collects ZIS and waqf (including cash waqf) and deposits the cash funds in BT. BT could treat the cashwaqf as Waqf Investment Deposits and/or Waqf Equity. Direct cash waqf of γ will be used according to theoriginal contracts to build social waqf facilities, such as Islamic boarding school (Pesantren), Mosque,Orphanage House, etc. Indirect cash waqf of β will be invested in the real sector as intended initially, suchas plantation, agriculture, farming, Islamic school, restaurant, convenient store, etc. meanwhile anotherindirect cash waqf of α will be used to extend micro-small financing to members and micro-smallenterprises. To mitigate the credit risk, it will be covered by micro-small takaful (Ascarya, 2017).

3.4 BMT as Integrated Islamic Microfinance Mod.

15

ASSETS LIABILITIES Cash Wadiah/Mudharabah Saving Deposits

Islamic Bank Deposits Mudharabah Investment Deposits

Receivables (Murabahah, Qardh, etc.) Islamic Bank Financing

Financing (Mudharabah, Musharakah, etc.)

Islamic Microfinance Services

Fixed Assets Capital

▪ BMTs, prior to managing ZIS-Waf funds, generally have structural issues on low capital and lowfunding (or high financing to deposit ratio, which could reach more than 200%), so that they havelimitation to expand and they rely on Islamic bank financing to meet their funding needs. Inaddition, asset-liability mismatch and liquidity issues (especially in certain period of times, such asthe beginning of the school year, fasting, Eid Al-Fitr, etc.) are also some other ongoing problems ofBMT without any real solution.

3.4 BMT as Integrated Islamic Microfinance Mod.

16

▪ BMTs, after managing ZIS-Waf funds, slowly but surely have alternative source of funds from cashwaqf (Waqf Long-Term Investment Deposits) that can replace the dependence of Islamic bankfinancing. The BMT may still has Islamic bank financing for emergency purposes, or for mitigatingliquidity risk. The nature of cash waqf which continuously increasing and perpetual maturity, wouldmake mismatch and liquidity problems of BMT resolved. In addition, cash waqf can also be placedas equity participation (Waqf Equity) which, in addition to low-cost funds, can also strengthen thecapital structure of BMT and improve its ability to expand. Moreover, zakat and infaq in Zakat/InfaqSaving Deposit will improve the liquidity of BMT.

ASSETS LIABILITIES Cash Wadiah/Mudharabah Saving Deposits

Islamic Bank Deposits Zakat/Infaq Saving Deposits

Receivables (Murabahah, Qardh, etc.) Waqf Saving Deposits

Financing (Mudharabah, Musharakah, etc.) Mudharabah Investment Deposits

Islamic Microfinance Services Islamic Bank Financing

Waqf LT Investment Deposits

Long-term Investments Waqf Equity

Fixed Assets Capital

3.4 BMT as Integrated Islamic Microfinance Mod.

17

3.5 Compare the Practice of IIMF in BMTs

No BMT Asset (Bn)

Zakat (Mn)

Infaq (Mn)

Waqf (Mn)

ZI/Asset (%)

W/Asset (%)

ISF/Asset (%)

1 NU Sumenep 95.24 - 17.7 00.0 0.02 0.00 0.02

2 Amanah Ummah 11.68 19.4 4.5 5.7 0.20 0.05 0.25

3 Manfaat 2.40 29.0 24.0 18.0 2.21 0.75 2.96

IIMF-1 0.81 0.27 1.08

4 Hudatama 40.00 500.0 300.0 1.25 0.75 2.00

5 Mardlotillah 19.65 23.8 29.7 10.1 0.27 0.05 0.32

6 Mustama 5.27 6.1 52.9 1.1 1.12 0.02 1.14

IIMF-2 0.88 0.27 1.15

7 Beringharjo 135.00 3000.1 202.0 2.22 0.15 2.37

8 L-Risma 103.00 115.7 201.2 1845.0 0.31 1.79 2.10

9 Surya Abadi 101.00 18.2 70.2 566.3 0.09 0.56 0.65

10 Bina I. Fikri 78.60 233.5 95.7 247.0 0.42 0.31 0.73

11 Barrah 37.48 90.9 749.5 80.7 2.24 0.22 2.46

IIMF-3 1.06 0.61 1.66

12 Tamzis 527.00 410.0 704.0 119.0 0.21 0.02 0.23

13 ItQan 39.04 253.0 1060.0 525.0 3.36 1.34 4.71

IIMF-4 1.79 0.68 2.47

IIMF Activity in Various Structure of BMTs (in Rupiah)

▪ Four IIMF models: 1) IIMF-1 where ISF activity is handled by Contact Person; 2) IIMF-2 where ISF activity ishandled by a small unit of Baitul Maal; 3) IIMF-3 where ISF activity is handled by a division of Baitul Maalequal to its division of Baitut Tamwil; and 4) IIMF-4 where ISF is handled by separate Baitul Maal.

▪ There seems to be no relation between the structure of Baitul Maal and the ISF activity. The same can alsobe said for ZI and W activities of individual BMT.

18

1. INTRODUCTION

2. ISLAMIC MICROFINANCE

3. BAITUL MAAL WAT TAMWIEL

4. BMT for SDGs in INDONESIA4.1 Islamic Finance and SDG Alignment

4.2 BMT and SDG Alignment

4.3 BMT and SDG Alignment

5. CONCLUSION & RECOMMENDATION

O U T L I N E

19

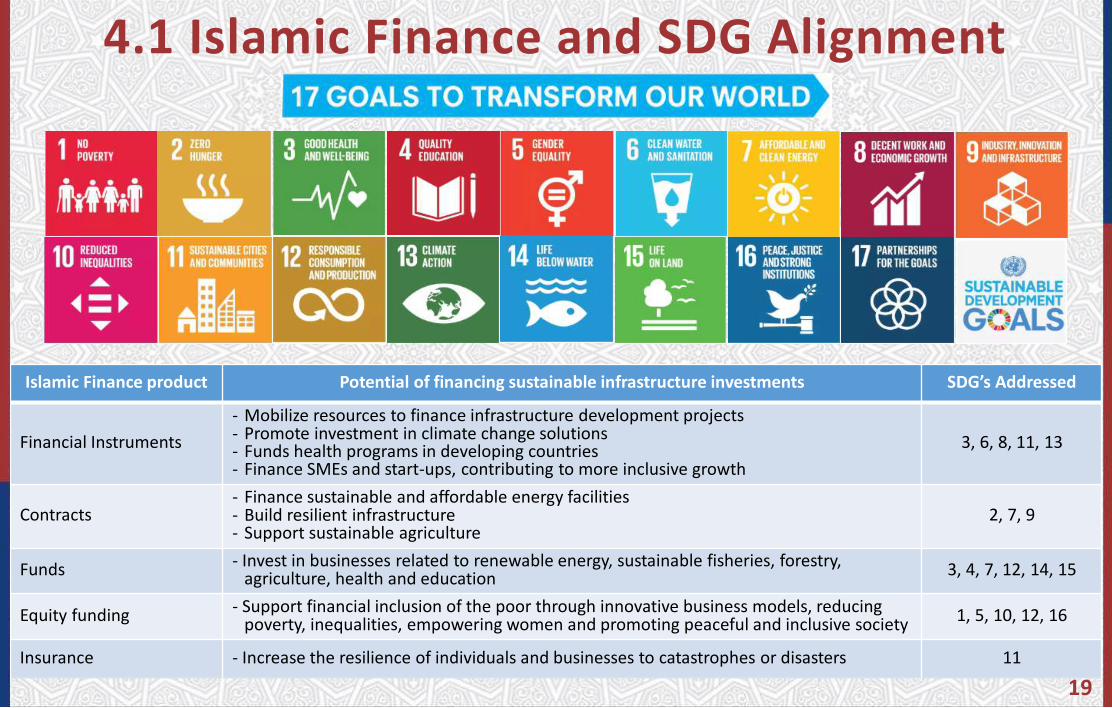

4.1 Islamic Finance and SDG Alignment

Islamic Finance product Potential of financing sustainable infrastructure investments SDG’s Addressed

Financial Instruments

- Mobilize resources to finance infrastructure development projects- Promote investment in climate change solutions- Funds health programs in developing countries- Finance SMEs and start-ups, contributing to more inclusive growth

3, 6, 8, 11, 13

Contracts- Finance sustainable and affordable energy facilities- Build resilient infrastructure- Support sustainable agriculture

2, 7, 9

Funds - Invest in businesses related to renewable energy, sustainable fisheries, forestry, agriculture, health and education 3, 4, 7, 12, 14, 15

Equity funding - Support financial inclusion of the poor through innovative business models, reducing poverty, inequalities, empowering women and promoting peaceful and inclusive society 1, 5, 10, 12, 16

Insurance - Increase the resilience of individuals and businesses to catastrophes or disasters 11

20

4.2 BMT and SDG Alignment

Islamic Social Finance Potential of financing sustainable programs and investments SDG’s Addressed

Zakat

- Consumptive program of zakat to provide basic needs (food, clothing, housing, education, healthcare, etc.).

- Productive program of zakat to provide Qardh micro-financing to develop ME.- Support social inclusion of the poor, empowering women and promoting peaceful and

inclusive society.

1, 2, 3, 4, 5, 6, 8, 10, 12, 16, 17

Infaq, sadaqa, hibah - Support consumptive and productive programs of zakat- Build resilient social infrastructure

3, 4, 5, 6, 7, 8, 9, 10, 17

Waqf – Social - Build resilient infrastructure, school, hospital, Islamic center, city park, cemetery, etc. 3, 4, 5, 6, 7, 8, 9, 10, 11, 17

Waqf – Productive - Invest in businesses related to renewable energy, sustainable fisheries, forestry,

agriculture, health and education, as well as Invest in resilient infrastructure.- Promote investment in climate change solutions.

3, 4, 5, 7, 8, 9, 12, 13, 14, 15, 16, 17

21

4.2 BMT and SDG Alignment

Islamic Commercial Finance product Potential of financing sustainable infrastructure investments SDG’s Addressed

Micro-Funding- Support financial inclusion of the poor through innovative business models, reducing

poverty, inequalities, empowering women and promoting peaceful and inclusive society- Support the quality of health, education, life

1, 5, 10, 12, 16

Micro-Financing- Finance MSEs, contributing to more inclusive growth- Finance sustainable and affordable simple/appropriate technology and energy facilities- Support sustainable agriculture, farming, fisheries, trade, simple manufacture

2, 3, 6, 7, 8, 9, 11, 13

Funds - Invest in businesses related to renewable energy, sustainable fisheries, forestry, agriculture, health and education 3, 4, 7, 12, 14, 15

IMF Services - Support commercial and social transactions- Support cash-less payment system 11

Micro Takaful - Increase the resilience of individuals and businesses to catastrophes or disasters 11

22

4.2 BMT and SDG Alignment

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Funding.

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Financing,.

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Financing, Micro-Takaful.

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Funding, Micro-Takaful.

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Financing, IMF-Services.

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Financing.

ISF: Infaq, sadaqa, waqf.ICF: Micro-Funding.

ISF: Infaq, sadaqa, waqf.ICF: Micro-Financing,.

ISF: Waqf.ICF: Micro-Financing.

ISF: Zakat, infaq, sadaqa, waqf.ICF: Micro-Funding.

ISF: Waqf.ICF: Micro-Financing, IMF-Services, Micro-Takful.

ISF: Zakat.ICF: Micro-Financing.

23

4.2 BMT and SDG Alignment

ISF: Waqf.ICF: Micro-Financing.

ISF: Waqf.ICF: Funds.

ISF: Waqf.ICF: Funds.

ISF: Zakat, waqf.ICF: Micro-Funding.

ISF: Zakat, infaq, sadaqa, waqf.ICF: -

24

4.2 BMT and SDG Alignment

25

1. INTRODUCTION

2. ISLAMIN MICROFINANCE

3. BAITUL MAAL WAT TAMWIEL

4. BMT for SDGs in INDONESIA

5. CONCLUSION & RECOMMENDATION

O U T L I N E

26

5.1 CONCLUSION▪BMT is a unique Islamic microfinance in Indonesia which plays an important

roles as: 1) sustainable IMFI model providing financing and other IMF servicesto the poor and MSEs; 2) agent of holistic financial inclusion (HFI) combiningsocial inclusion and financial inclusion to alleviate poverty and improve thewellbeing of the poor and MSEs; and 3) integrated Islamic commercial andsocial finance (IICSF), which could better achieve triple bottom-line of SDGs,including economic development, environmental sustainability, and socialinclusion, especially for the poor and MSEs in the rural area.

▪Zakat, infaq, sadaqa and waqf can play the role in achieving GOAL 17 ‘Revitalizeglobal partnership for sustainable development.

27

5.2 RECOMMENDATION▪BMT can be replicated in other countries to achieve triple bottom-line of SDGs,

including economic development, environmental sustainability, and socialinclusion, especially for the poor and MSEs in the rural area.

▪Islamic social finance, including zakat, infaq, sadaqa and waqf, should beemphasized, developed and given appropriate attention to catch up with thedevelopment of Islamic commercial finance.

▪Government must take its role in developing and mainstreaming Islamic socialfinance in the country.

28

Wallahu a’lam

© Khalil Bendib, January 2009, Source: http://euraktiva786.wordpress.com/2009/06/17