John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 23 A STUDY ON CUSTOMER ATTITUDE TOWARDS INTERNET BANKING SERVICES IN KANNIYAKUMARI DISTRICT By Mohamed Umma, M., I. **Assistant Professor, Department of Commerce, Government Arts and Science College, Kovilpatti, Affiliated to Manonmaniam Sundaranar University, Tirunelveli, Tamilnadu, India. Abstract Banking transactions that takes place in a virtual ambience on the website of a banking company or a financial institution is termed as ‘Internet banking or E-Banking’. The essence of internet banking lies in on-line access by customers of banking and financial services. Online banking or Internet banking allows customers to conduct financial transactions on a secure website operated by their retail or virtual bank, credit union or building society. E- banking implies performing basic banking transactions by customer’s round the clock globally through Electronic Media. The important objectives of the study are: To analyze the difficulties in internet banking services and to evaluate the customer satisfaction towards internet banking services in Kanniyakumari District. The study was undertaken to analyze the customer attitude towards internet banking services in Kanniyakumari District and it is mainly based on both primary and secondary data. For the purpose of the study 50 bank customers who are using internet banking services are selected randomly from Kanniyakumari District on the basis of random sampling method. Keywords: internet banking, services, problems and benefits Introduction Banking transactions that takes place in a virtual ambience on the website of a banking company or a financial institution is termed as ‘Internet banking or E-Banking’. The essence of internet banking lies in on-line access by customers of banking and financial services. Online banking or Internet banking allows customers to conduct financial transactions on a secure website operated by their retail or virtual bank, credit union or building society. E-banking implies performing basic banking transactions by customer’s round the clock globally through Electronic Media. Modern banking is more information based, speedy and boundary less due to the impact of E-revolution modern banks

Transcript

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 23

A STUDY ON CUSTOMER ATTITUDE TOWARDS INTERNET

BANKING SERVICES IN KANNIYAKUMARI DISTRICT

By

Mohamed Umma, M., I.

**Assistant Professor, Department of Commerce, Government Arts and Science College, Kovilpatti,

Affiliated to Manonmaniam Sundaranar University, Tirunelveli, Tamilnadu, India.

Abstract

Banking transactions that takes place in a virtual ambience on the website of a banking

company or a financial institution is termed as ‘Internet banking or E-Banking’. The essence

of internet banking lies in on-line access by customers of banking and financial services.

Online banking or Internet banking allows customers to conduct financial transactions on a

secure website operated by their retail or virtual bank, credit union or building society. E-

banking implies performing basic banking transactions by customer’s round the clock

globally through Electronic Media. The important objectives of the study are: To analyze the

difficulties in internet banking services and to evaluate the customer satisfaction towards

internet banking services in Kanniyakumari District. The study was undertaken to analyze

the customer attitude towards internet banking services in Kanniyakumari District and it is

mainly based on both primary and secondary data. For the purpose of the study 50 bank

customers who are using internet banking services are selected randomly from

Kanniyakumari District on the basis of random sampling method.

Keywords: internet banking, services, problems and benefits

Introduction

Banking transactions that takes place

in a virtual ambience on the website of

a banking company or a financial

institution is termed as ‘Internet

banking or E-Banking’. The essence of

internet banking lies in on-line access

by customers of banking and financial

services. Online banking or Internet

banking allows customers to conduct

financial transactions on a secure

website operated by their retail or

virtual bank, credit union or building

society. E-banking implies performing

basic banking transactions by

customer’s round the clock globally

through Electronic Media. Modern

banking is more information based,

speedy and boundary less due to the

impact of E-revolution modern banks

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 24

have to be well versed in information

technology its users and applications.

Banking divisions have to be IT based,

with the spread of digital economy. E-

banking is more of a science than art.

E-banking is knowledge based and

mostly scientific in using electronic

devices of the computer revolution.

When most business and commercial

enterprises tend to become internet

banking organizations banking has to

be E-banking in the new century.

Services of Internet banking in India

Internet banking services offers

banking service on-line with the same

personal export that is received at the

branch. On-line requests are processed

by a proactive team of personal

banker’s adhering to service quality

standards.

Service offered includes the following:

Sending in request for a cheque

book from the convenience of

home.

Viewing accounting statements on-

line.

Notification of change of address so

as to update the records.

Requesting for a draft on-line to be

couriered at the mailing address

specified by the customer.

Transferring funds between one

accounts of the customer to

another account of the same

customer.

Viewing details of past 3 months

transactions.

Updating of foreign exchange

currency rates.

Intimating on-line about a stop

payment.

Notification of lost / stolen ATM

cards.

The internet banking service adds

more value to NRIs who can view their

balances on-line and also effect funds

transfer, just at the click of a mouse.

Moreover, internet banking has no

time zones and is accessible round the

clock without restricting to any

geographical boundary.

Objectives of the study

The important objectives of the study

are: To analyze the difficulties in

internet banking services and to

evaluate the customer satisfaction

towards internet banking services in

Kanniyakumari District.

Scope of the study

The study was undertaken to analyze

the customer attitude towards internet

banking services in Kanniyakumari

District. The approach of the study has

been from the point of view of the bank

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 25

customers. This study is designed to

give awareness to the customer

regarding internet banking services.

Methodology

The present study is mainly based on

both primary and secondary data. The

primary data needed for the study

have been collected by using personal

interview method. And the secondary

data have been mainly collected from

the books, journals, magazines and also

from internet.

Sampling design

For the purpose of the study 50 bank

customers who are using internet

banking services are selected

randomly from Kanniyakumari District

on the basis of random sampling

method.

Analysis and Interpretation

Age–wise classification of the

respondents

Age is an important factor which is

considered to study the customer

satisfaction towards internet banking

services. The following table reveals

that the age-wise classification of the

respondents.

Table 1. Age-wise classification of

respondents

Sl.

No. Age

No. of

Respon

dents

Percentage

1 Below

25 9 18

2 26-45 34 68

3 Above

45 7 14

Total 50 100

Source: Primary Data

The above table shows that 9 (18

percent) of the respondents comes

under the age group of below 25 years.

34 (68 percent) of the respondents

comes under the age group of 26 to 45

years and the remaining 7 (14 percent)

of them comes under the age group of

above 45 years.

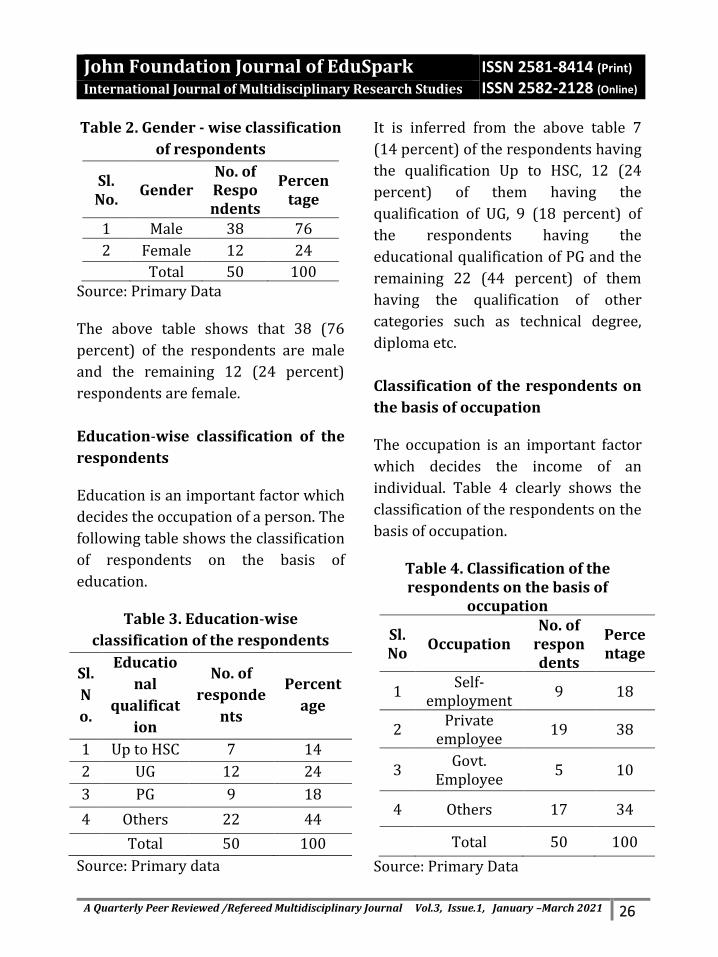

Gender-wise classification of

respondents

The Gender is an important factor

which considered for analyzing the

consumer satisfaction. The following

table shows the gender-wise

classification of the sample

respondents.

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 26

Table 2. Gender - wise classification

of respondents

Sl. No.

Gender No. of Respondents

Percentage

1 Male 38 76

2 Female 12 24

Total 50 100 Source: Primary Data

The above table shows that 38 (76

percent) of the respondents are male

and the remaining 12 (24 percent)

respondents are female.

Education-wise classification of the

respondents

Education is an important factor which

decides the occupation of a person. The

following table shows the classification

of respondents on the basis of

education.

Table 3. Education-wise

classification of the respondents

Sl.

N

o.

Educatio

nal

qualificat

ion

No. of

responde

nts

Percent

age

1 Up to HSC 7 14

2 UG 12 24

3 PG 9 18

4 Others 22 44

Total 50 100

Source: Primary data

It is inferred from the above table 7

(14 percent) of the respondents having

the qualification Up to HSC, 12 (24

percent) of them having the

qualification of UG, 9 (18 percent) of

the respondents having the

educational qualification of PG and the

remaining 22 (44 percent) of them

having the qualification of other

categories such as technical degree,

diploma etc.

Classification of the respondents on

the basis of occupation

The occupation is an important factor

which decides the income of an

individual. Table 4 clearly shows the

classification of the respondents on the

basis of occupation.

Table 4. Classification of the respondents on the basis of

occupation

Sl. No

Occupation No. of

respondents

Percentage

1 Self-

employment 9 18

2 Private

employee 19 38

3 Govt.

Employee 5 10

4 Others 17 34

Total 50 100

Source: Primary Data

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 27

The above table reveals that 9 (18

percent) of the respondents are self

employed, 19 (38 percent) of the

respondents are private employees, 5

(10 percent) of the respondents are

Government employees and the

remaining 17 (34 percent) of the

respondents comes under other

categories such as home maker,

students etc.

Monthly Income-wise classification

of the respondents

Income is a factor which decides the

standard of living of the people. The

following table 5 shows that monthly

income of the respondents.

Table 5. Monthly income of the

respondents

Sl. No

Monthly income

No. of respon dents

Perce ntage

1 Up to

10000 18 36

2 10001–25000

26 52

3 Above 25000

6 12

Total 50 100 Source: Primary Data

It is inferred from the table 4 that 18

(36percent) of the respondents

earning up to Rs.10,000 per month, 26

(52 percent) of them earning

Rs.10,001-25,000 and the remaining 6

(12 percent) respondents are earning

above Rs.25,000 per month.

Classification on the basis of the

bank in which they are account

holders

The customers select the bank to open

their account on the basis of their

convenient. The classification of the

respondents on the basis of the bank in

which they are account holders is

given in the table 6.

Table 6. Classification on the basis

of the bank in which they are

account holders

Sl. No.

Name of the bank

No. of respondents

Percen tage

1 SBI 19 38 2 IOB 11 22

3 Axis 8 16

4 Others 14 28 Total 50 100

Source: Primary Data

It is inferred from the table 6 that 19

(38 percent) of the respondents are

account holders in SBI, 11 (22 percent)

of them in IOB, 8 (16 percent) of them

in Axis bank and the remaining 14 (28

percent) of them holding accounts in

other banks such as TMB, SBT etc.

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 28

Classification on the basis of years of

holding account

The respondents are classified on the

basis of years of holding the account is

given in the table 7.

Table 7. Classification on the basis

of years of holding account

Sl.

No. Years

No. of respon dents

Percen tage

1 Up to 1

year 2 4

2 1-3

years 15 30

3 3-6

years 22 44

4 Above 6

years 11 22

Total 50 100

Source: Primary Data

It is inferred from the Table 7 that 2 (4

percent) of the respondents holding

the account up to 1 year, 15 (30

percent) of them holding 1 – 3 years,

22 (44 percent) of them holding the

account from 3 – 6 years, and the

remaining 11 (22 percent) of them

holding the account for above 6 years.

Classification on the basis of years of

using internet banking

The account holders mostly make their

banking transactions through internet

banking. The respondents are

classified on the basis of years of using

the internet banking is given in the

table 8.

Table 8. Classification on the basis

of years of using internet banking

Sl.

No. Years

No. of

respon

dents

Percen

tage

1 Less than

6 month 5 10

2 6 months

to 1 year 7 14

3 1 – 3

years 12 24

4 Above 3 years

26 52

Total 50 100

Source: Primary Data

It is inferred from the Table 8 that 5

(10 percent) of the respondents using

internet banking for less than 6

months, 7 (14 percent) of them using

for 6 months to 1 year, 12 (24 percent)

of them are using internet banking for

1 – 3 years, and the remaining 26 (52

percent) of them using internet

banking for above 3 years.

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 29

Classification on the basis of reason

for selecting internet banking

services

The table 9 indicates the classification

of the respondents on the basis of the

reason for selecting internet banking

services. The ranks assigned by the

respondents are converted into scores

using Garrett ranking technique.

Table 9. Ranking Table

Sl.

No. Reasons

Garrett mean score

Rank

1 Convenience 53.02 II

2 Service

Quality 45.42 V

3 Trust with bank

52.12 III

4 Security 48.32 IV

5 Nearness 43.46 VI

6 Time saving 57.54 I

Source: Primary Data

It is inferred from the table 9 that time

saving scores 57.54 and holds the first

rank in the reason for selecting

internet banking, convenience scores

53.02 and trust with the bank scores

52.12 and holds second and third rank

respectively in the reason for selecting

internet banking.

Classification on the basis where

they use internet banking services

The respondents use the internet

banking services in the place on the

basis of their convenient. The below

table 10 shows the classification of the

respondents on the basis of the place

where they are using internet banking

services.

Table 10. Classification on the basis

where they use internet banking

services

Sl.

No.

Place of using

internet banking

No. of respon dents

Perce

ntage

1 Home 33 66

2 Office 8 16

3 Browsing

centres 11 26

Total 50 100

Source: Primary Data

It is inferred from the table 10 that 33

(66 percent) of the respondents using

internet banking services at their

home, 8 (16 percent) of them in their

office and the remaining 11 (22

percent) of them using internet

banking services in browsing centres.

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 30

Medium through which the

respondents came to know about E-

banking

The respondents get the information

related to the internet banking through

many modes. The below table 11

shows the classification on the basis of

the medium through which the

respondents came to know about the

internet banking.

Table 11. Medium through which

the respondents came to know

about E-banking

Sl.

No. Medium

No. of respon dents

Perce ntage

1 Personal visit 11 22

2 Information

from staffs 6 12

3 Advertisement 29 58

4 Friends /

relatives 4 8

Total 50 100

Source: Primary Data

From the table 11 we came to know

that 11 (22 percent) of them get

information related to the internet

banking through personal visit to the

banks, 6 (12 percent) of them by the

staffs, 29 (58 percent) through

advertisements and the remaining 4 (8

percent) of them getting information

through their friends and relatives.

Classification on the basis of time of

using internet banking

The respondents use the internet

banking at the time they need. The

below table 12 shows the classification

of the respondents on the basis of the

time of using internet banking services.

Table 12. Classification on the basis

of time of using internet banking

Sl.

No. Time

No. of

respon

dents

Percen tage

1 12 am

to 6am 2 4

2 7 am to

1 pm 16 32

3 2pm to

7 pm 20 40

4 8pm to 12pm

12 24

Total 50 100

Source: Primary Data

It is inferred from the table 12 that 2 (4

percent) of them use internet banking

from 12 am to 6 am, 16 (32 percent) of

them use from 7 am to 1 pm, 20 (40

percent) of them use internet banking

within the time 2 pm to 7 pm and the

remaining 12 (24 percent) of them use

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 31

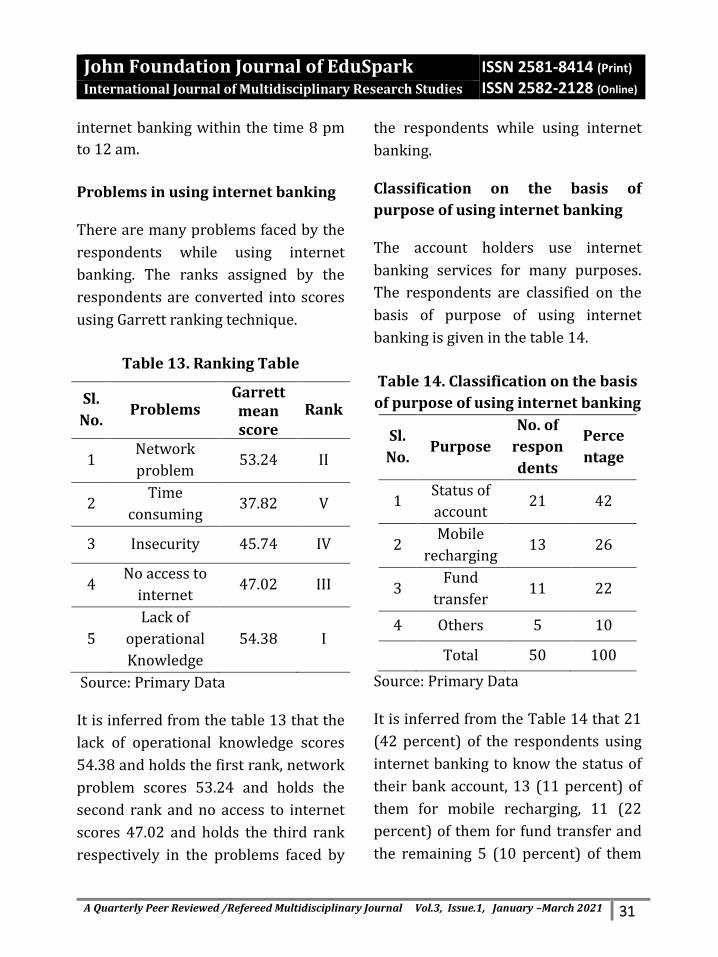

internet banking within the time 8 pm

to 12 am.

Problems in using internet banking

There are many problems faced by the

respondents while using internet

banking. The ranks assigned by the

respondents are converted into scores

using Garrett ranking technique.

Table 13. Ranking Table

Sl.

No. Problems

Garrett mean score

Rank

1 Network

problem 53.24 II

2 Time

consuming 37.82 V

3 Insecurity 45.74 IV

4 No access to

internet 47.02 III

5

Lack of

operational

Knowledge

54.38 I

Source: Primary Data

It is inferred from the table 13 that the

lack of operational knowledge scores

54.38 and holds the first rank, network

problem scores 53.24 and holds the

second rank and no access to internet

scores 47.02 and holds the third rank

respectively in the problems faced by

the respondents while using internet

banking.

Classification on the basis of

purpose of using internet banking

The account holders use internet

banking services for many purposes.

The respondents are classified on the

basis of purpose of using internet

banking is given in the table 14.

Table 14. Classification on the basis

of purpose of using internet banking

Sl.

No. Purpose

No. of

respon

dents

Perce

ntage

1 Status of

account 21 42

2 Mobile

recharging 13 26

3 Fund

transfer 11 22

4 Others 5 10

Total 50 100

Source: Primary Data

It is inferred from the Table 14 that 21

(42 percent) of the respondents using

internet banking to know the status of

their bank account, 13 (11 percent) of

them for mobile recharging, 11 (22

percent) of them for fund transfer and

the remaining 5 (10 percent) of them

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 32

using internet banking for other

purposes.

Classification on the basis of the

satisfaction of respondents

The below table 15 shows the

classification of the respondents on the

basis of the satisfaction of them using

the internet banking services.

Table 15. Classification on the basis

of the satisfaction of respondents

Sl.

No. Options

No. of respon dents

Perce ntage

1 Yes 44 88

2 No 6 12

Total 50 100

Source: Primary Data

From the table 15 we came to know

that 44 (88percent) of the respondents

are satisfied with the internet banking

services and the remaining 6 (12

percent) of them are not satisfied with

the internet banking services rendered

in the banks.

Findings of the study

The important findings are given

below as follows:

1. Majority 34 (68 Percent) of the

respondents comes under the age

group 26 – 45 years.

2. Most 38 (76 Percent) of the

respondents are Male.

3. 22 (44 Percent) of the respondents

having the educational qualification

comes under other category such

as technical degree, diploma etc.

4. Most 19 (38 Percent) of the

respondents are private employees.

5. Majority 26 (52 Percent) of the

respondents earning RS.10001 –

25000 per month.

6. Majority 19 (38 Percent) of the

customers having their account in

State Bank of India.

7. From the total respondents 22 (44

percent) of them holding the

account for 3 – 6 years.

8. Majority 26 (52 percent) of the

customers using the internet

banking services above three years.

9. From the respondents point of view

the time saving y scores high and

holds the first rank, convenience

and trust with the bank holds the

second and third rank respectively

in the reason for selecting internet

banking.

10. 33 (66 Percent) of the respondents

using internet banking services in

their home.

11. 29 (58 percent) of the respondents

came to know about the internet

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 33

banking services through

advertisements.

12. Majority 20 (40 percent) of the

respondents using internet banking

at the time of 2 pm to 7 pm.

13. From the respondents point of view

lack of operational knowledge

scores high and holds the first rank,

network problem and no access to

internet holds the second and third

rank respectively in the problems

faced by the respondents while

using internet banking.

14. Majority 21 (42 percent) of the

respondents using internet banking

to know about the status of their

account.

15. 44 (88 Percent) of the respondents

are satisfied with the services

rendered by the internet banking

services in the banks.

Conclusion

From the above study it is concluded

that the internet banking services is

very new to our society and it is fully

due to the technological development.

It plays a vital role in our daily life and

the internet banking service is very

essential for us in many ways. Most of

the people did not have adequate

knowledge about internet banking and

hence the banking companies and the

government must take essential steps

for the development of internet

banking services.

References

************

Aiyappan, A., Report on the Socio-Economic Conditions of the Aborginal Tribes of the Province of Madras, Superintendent, Govern ment Press, Madras, 1948, p.85.

Atreyi Biswas, Famines in Ancient India, Gyan Publishing House, New Delhi, 2000, p.167.

Atreyi Biswas, Famines in Ancient India, Gyan Publishing House, New Delhi, 2000, p.167.

Atreyi Biswas, Famines in Ancient India, Gyan Publishing House, New Delhi, 2000, p.168.

Baker, C.J., Politics of South India, Vikas Publishing House, New Delhi, 1976.

Hans Raj, Advanced History of India, Surjeet Publication, New Delhi, 2017, p.36.

Hunter, W.W., The Imperial Gazetteer of India, vol.I, Turbner & Co., London, 1881, p.158.

John Foundation Journal of EduSpark ISSN 2581-8414 (Print) ISSN 2582-2128 (Online) International Journal of Multidisciplinary Research Studies

A Quarterly Peer Reviewed /Refereed Multidisciplinary Journal Vol.3, Issue.1, January –March 2021 34

Krishnaswami, A., Topics in South Indian History (From early times upto 1565 A.D.), Published by the Author, Chidambaram, 1975, p.148.

Roy Choudhary, S.C., Social, Cultural and Economic History of India, Delhi, 2016, p.63.

Roy Choudhary, S.C., Social, Cultural and Economic History of India, Delhi, 2016, p.68.

Subrahmanian, N., History of Tamilnad upto 1336 A.D, Koodal Publishers, Madras, 1972, p.58.

Wagner, G. E., Plant remains from Oriyo Timbo. Harappan Civilization and Oriyo Timbo, Rissman, B.C., and Chirtalwala, Y. W., (ed.) New Delhi, 1990, p.123.

Wheeler, R. E., M. Early India and Pakistan to Ashoka, London: Thames and Hudson, 1959, p.88.

To cite this article *****************

Mohamed Umma, M., I. (2021). A Study on Customer Attitude towards Internet Banking Services in Kanniyakumari District. John Foundation Journal of EduSpark, 3(1), 23-34.

DR M. I. Mohamed Umma is an Assistant professor and Head of the Department of Commerce, Government Arts and Science, Kovilpatti. She holds a Post Graduate and Master of Philosophy degree in Commerce. She is a Doctorate in Commerce and possess more than 30 years of experience in teaching. She has participated in many National and international seminars and various faculty development programmes.