40

1 CONFIDENTIAL FOR INTERNAL USE ONLY AAA Memorial Day 2013 Travel Forecast Prepared for: Prepared for: American Automobile Association May 22, 2013

1 CONFIDENTIAL FOR INTERNAL USE ONLY

AAA Memorial Day 2013 Travel Forecast

Prepared for:

Prepared for:

American Automobile Association

May 22, 2013

1 IHS / AAA 2013 Memorial Day Forecast

Table of Contents

Table of Contents .................................................................................................................................................................... 1

Holiday Forecast Methodology: A Brief Overview ................................................................................................................... 2

2013Memorial Day HolidayTravel Forecast ............................................................................................................................ 3

Travel by Mode of Transportation ........................................................................................................................................... 5

Travel by Region: East North Central ..................................................................................................................................... 8

Travel by Region: East South Central ................................................................................................................................... 10

Travel by Region: Middle Atlantic ......................................................................................................................................... 12

Travel by Region: Mountain .................................................................................................................................................. 14

Travel by Region: New England............................................................................................................................................ 16

Travel by Region: Pacific ...................................................................................................................................................... 18

Travel by Region: South Atlantic ........................................................................................................................................... 20

Travel by Region: West North Central .................................................................................................................................. 22

Travel by Region: West South Central .................................................................................................................................. 24

Memorial Day 2013 Holiday Traveler Profile Survey Methodology ...................................................................................... 26

Change in the Average Memorial Day Traveler .................................................................................................................... 27

Travel Distances ................................................................................................................................................................... 28

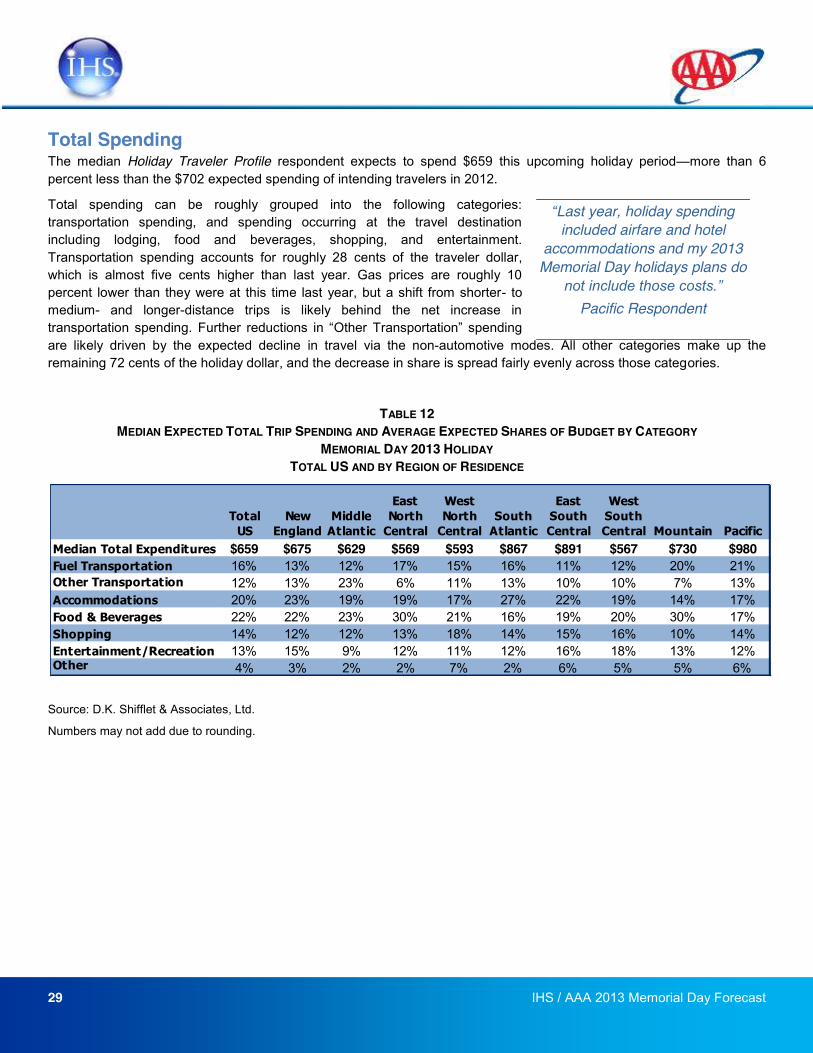

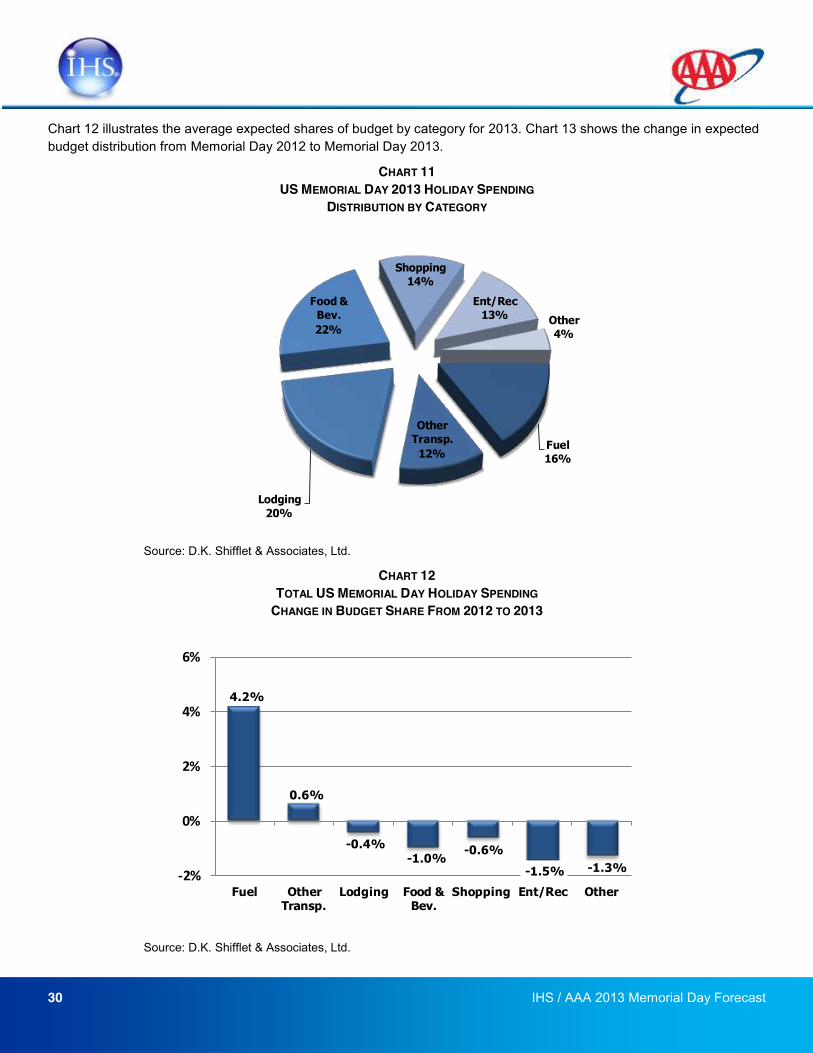

Total Spending ...................................................................................................................................................................... 29

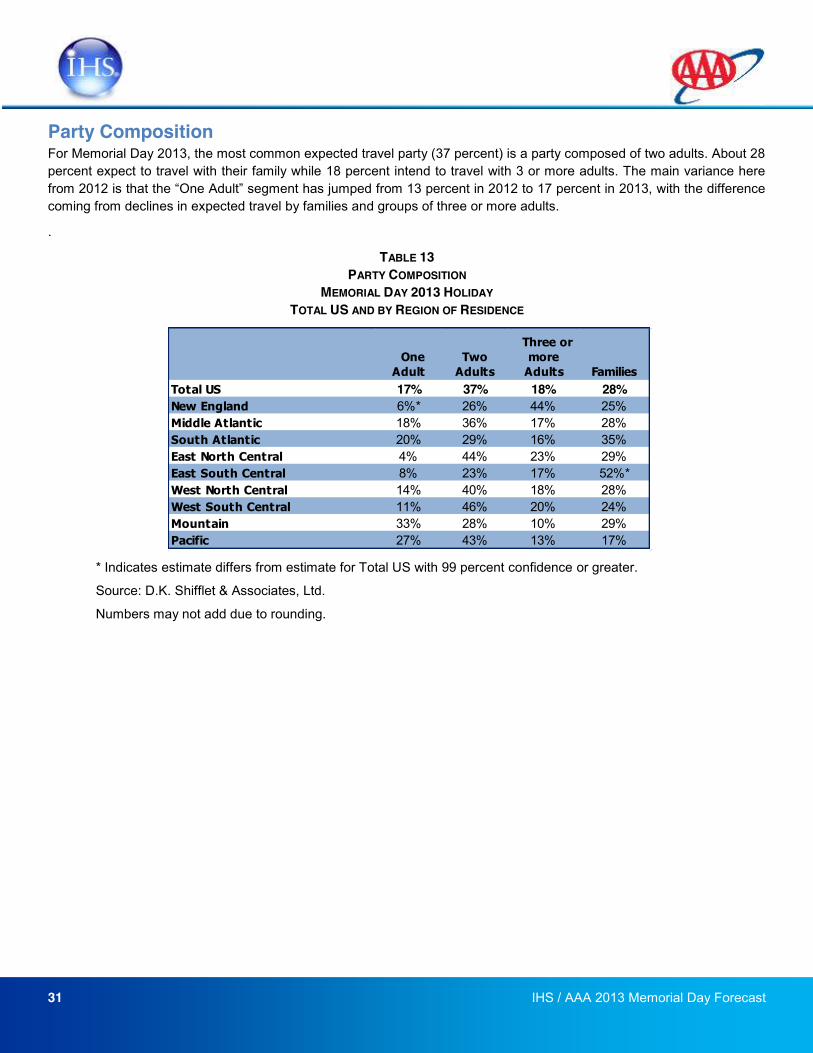

Party Composition ................................................................................................................................................................. 31

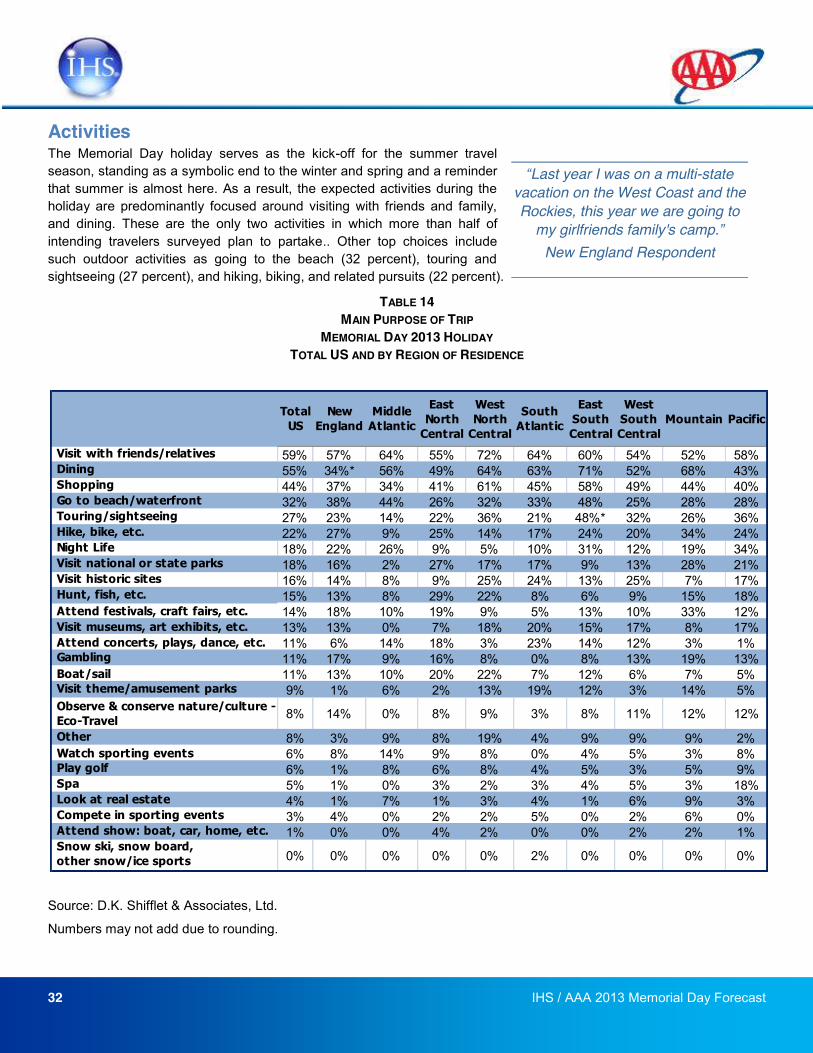

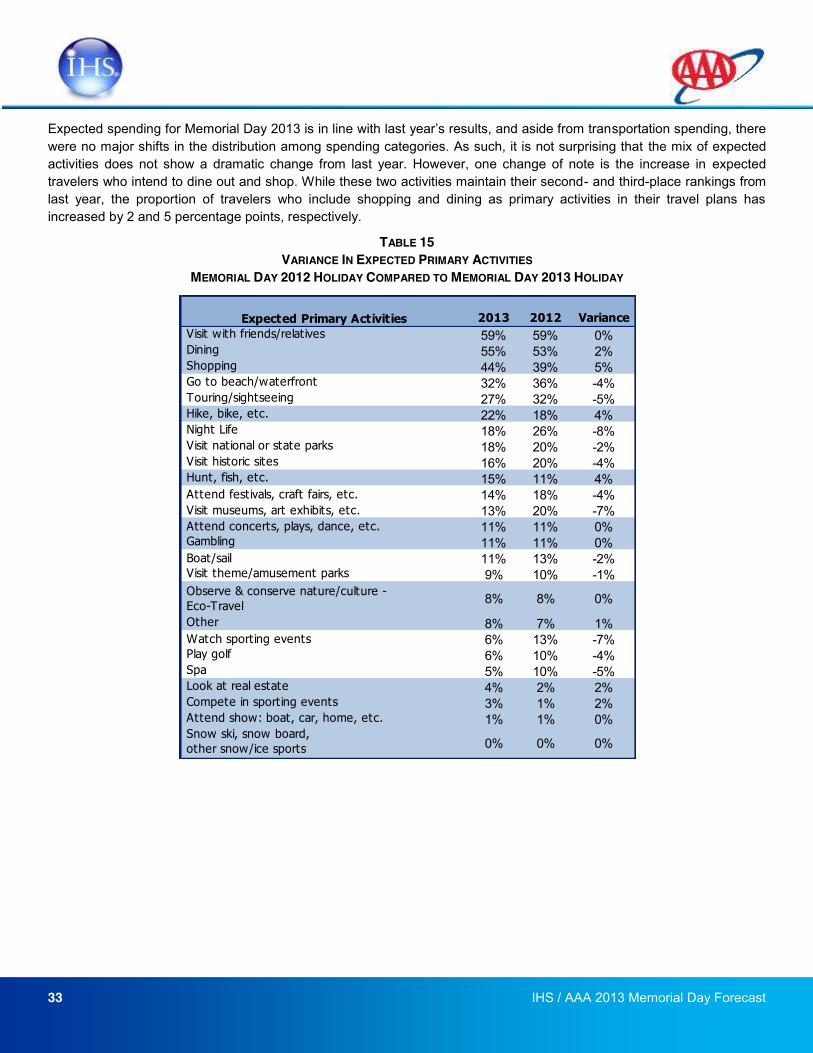

Activities ................................................................................................................................................................................ 32

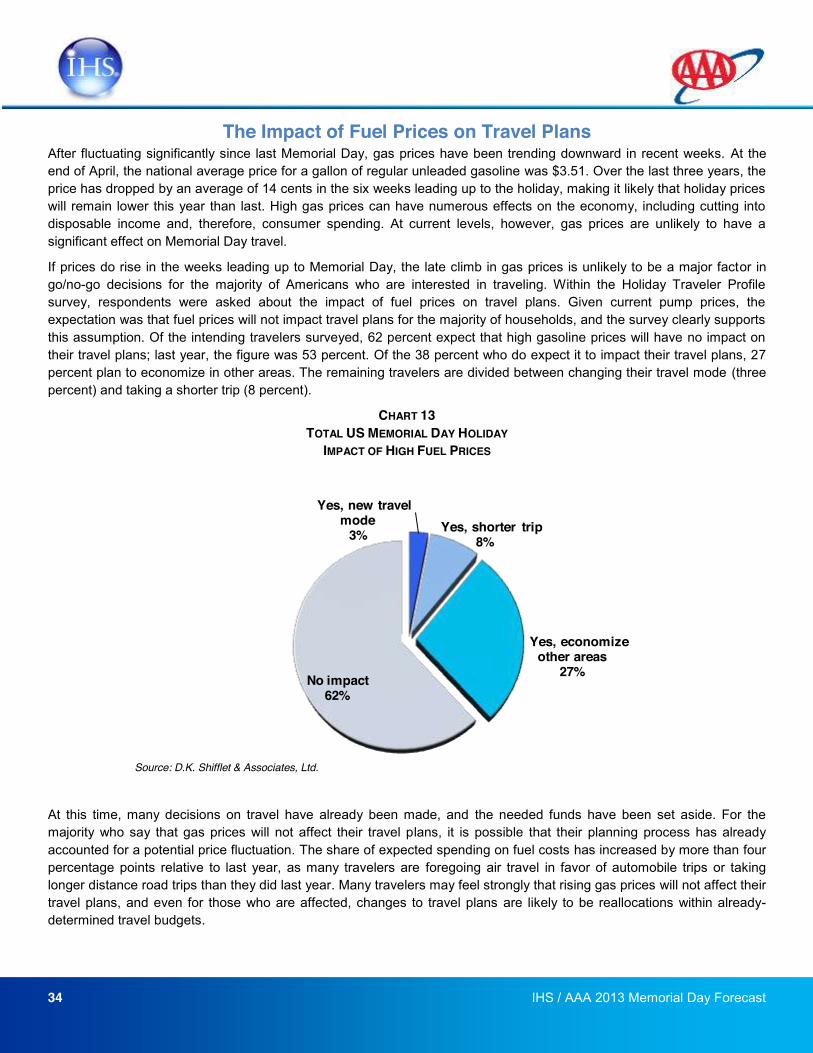

The Impact of Fuel Prices on Travel Plans ........................................................................................................................... 34

Addendum 1: US Economic Forecast Summary: ................................................................................................................. 35

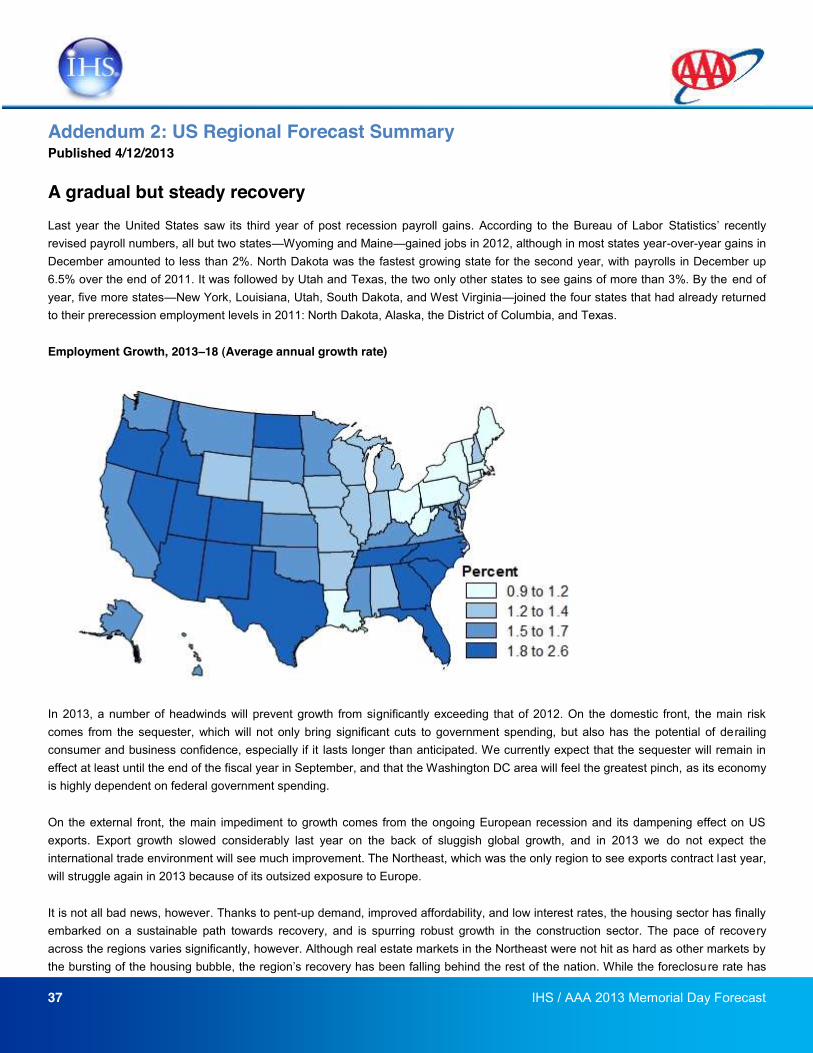

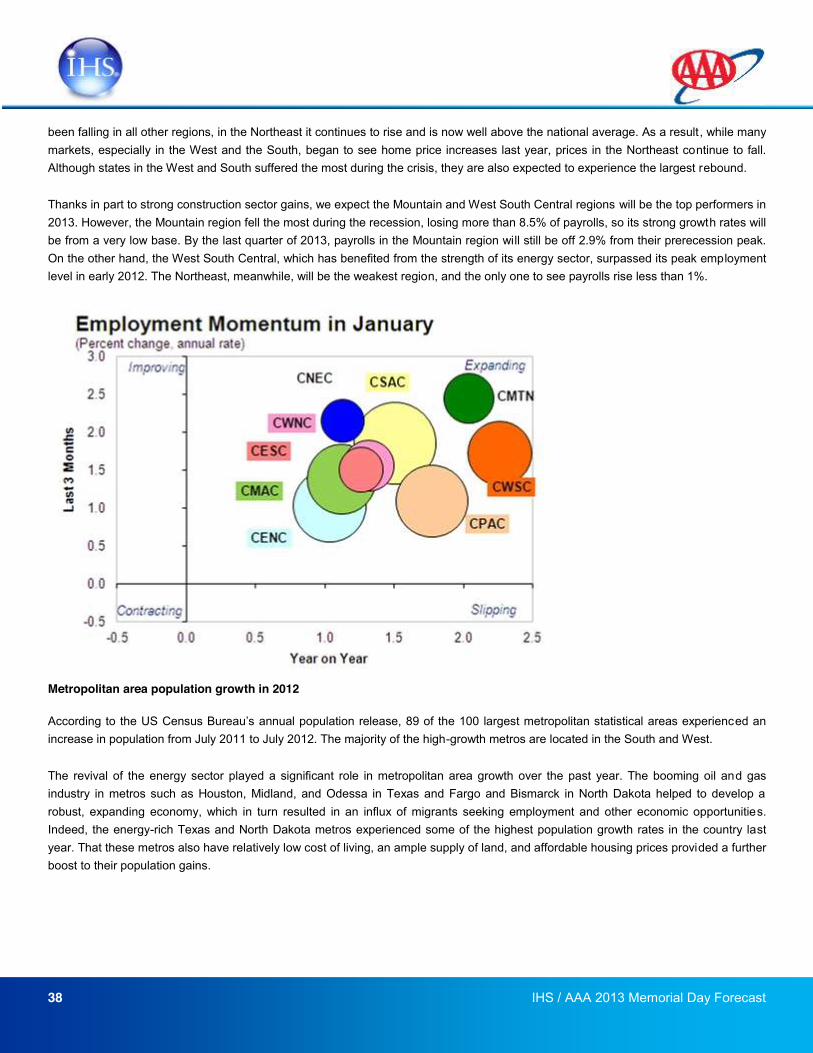

Addendum 2: US Regional Forecast Summary .................................................................................................................... 37

Regional definitions used throughout the report:

East North Central (ENC): IL, IN, MI, OH, WI

East South Central (ESC): AL, KY, MS, TN

Middle Atlantic (MATL): NJ, NY, PA

Mountain (MTN): AZ, CO, ID, MT, NM, NV, UT, WY

New England (NENG): CT, MA, ME, NH, RI, VT

South Atlantic (SATL): DC, DE, FL, GA, MD, NC, SC, VA, WV

West South Central (WSC): AR, LA, OK, TX

West North Central (WNC): IA, KS, MN, MO, ND, NE, SD

Pacific (PAC): AK, CA, HI, OR, WA

2 IHS / AAA 2013 Memorial Day Forecast

Holiday Forecast Methodology: A Brief Overview The AAA Memorial Day 2013 Travel Forecast combines information from several sources to provide a prospective assessment of likely travel patterns for the upcoming holiday weekend. This report comprises two key components: the travel forecast and the holiday traveler profile. The travel forecast is based on economic conditions while the holiday traveler profile is developed employing survey data on travel behaviors. This approach provides the most comprehensive and detailed understanding of holiday travel at both the national and regional levels. In addition, the regional travel sections in this report have been enhanced to incorporate information about the state of the local tourism industries throughout the United States.

Holiday Travel Forecast

In cooperation with AAA, IHS developed an approach to forecast domestic travel volumes. The economic variables used to forecast travel for the current holiday are leveraged from IHS. These data include macroeconomic drivers such as employment, output, household net worth, asset prices including stock indices, interest rates, housing market indicators, and variables related to travel and tourism, including prices of gasoline, airline travel, and hotel stays.

The historical travel volume estimates come from the ongoing travel survey database of D.K. Shifflet & Associates, the premier source of US resident travel volume and behavior. DKSA interviews over 50,000 US households per month tracking trip incidence, party composition, traveler behavior, and spending all after the trips have been taken.

Holiday travel is forecast by person-trips, where a person-trip is defined as a trip that involves travel of 50 miles or more away from home. In particular, AAA and IHS forecasts total US holiday travel, travel by mode of transportation, and travel by US census region. The Travel Forecast presented in this report was prepared the week of April 22.

Holiday Traveler Profile

The Holiday Traveler Profile is a survey of intended travel behaviors related to party composition, travel distances, trip expenditures, and vacation activities conducted by D.K. Shifflet & Associates. The initial survey includes 1,352 households, out of which only the respondents intending to travel during the designated holiday are interviewed in detail about their anticipated trips. For Memorial Day 2013, 306 respondents were interviewed in detail about their intended trips. The survey was in the field from Monday, April 8 to Friday, April 12, 2013.

Memorial Day Holiday Travel Period

For purposes of this forecast, the Memorial Day holiday travel period is defined as trips that include travel of 50 miles or more away from home during the five-day period from Thursday, May 23 to Monday, May 27.

3 IHS / AAA 2013 Memorial Day Forecast

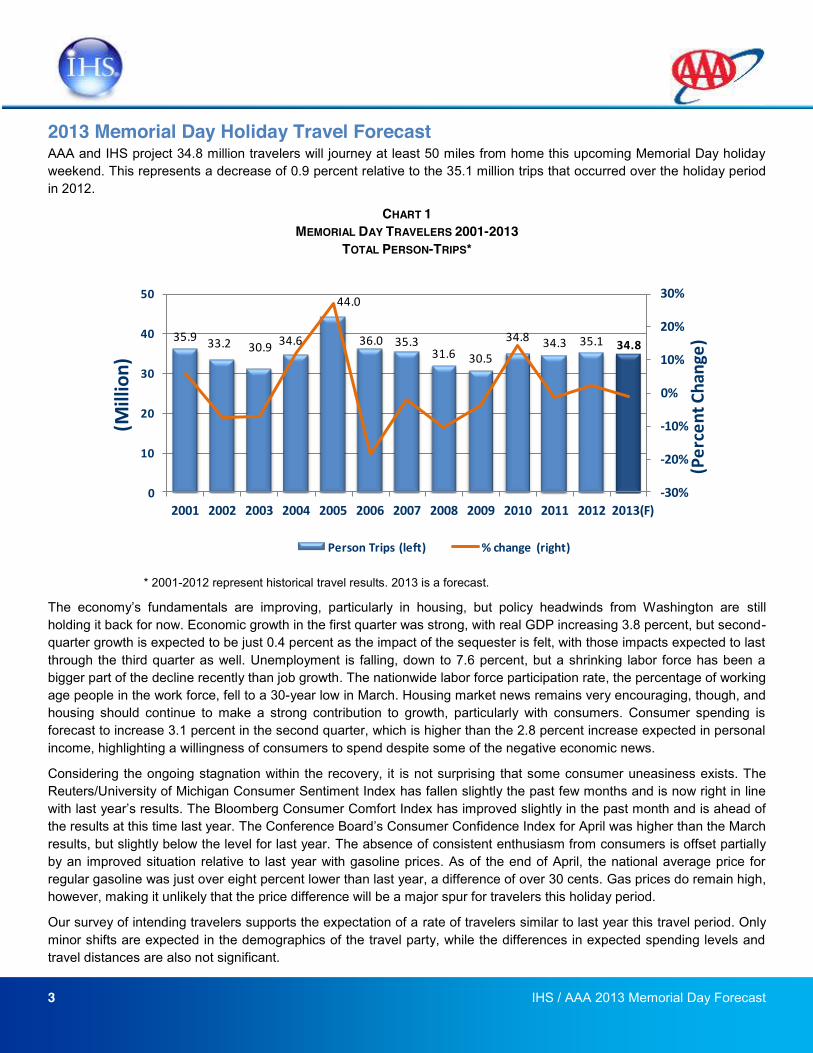

2013 Memorial Day Holiday Travel Forecast AAA and IHS project 34.8 million travelers will journey at least 50 miles from home this upcoming Memorial Day holiday weekend. This represents a decrease of 0.9 percent relative to the 35.1 million trips that occurred over the holiday period in 2012.

CHART 1 MEMORIAL DAY TRAVELERS 2001-2013

TOTAL PERSON-TRIPS*

* 2001-2012 represent historical travel results. 2013 is a forecast.

still holding it back for now. Economic growth in the first quarter was strong, with real GDP increasing 3.8 percent, but second-quarter growth is expected to be just 0.4 percent as the impact of the sequester is felt, with those impacts expected to last through the third quarter as well. Unemployment is falling, down to 7.6 percent, but a shrinking labor force has been a bigger part of the decline recently than job growth. The nationwide labor force participation rate, the percentage of working age people in the work force, fell to a 30-year low in March. Housing market news remains very encouraging, though, and housing should continue to make a strong contribution to growth, particularly with consumers. Consumer spending is forecast to increase 3.1 percent in the second quarter, which is higher than the 2.8 percent increase expected in personal income, highlighting a willingness of consumers to spend despite some of the negative economic news.

Considering the ongoing stagnation within the recovery, it is not surprising that some consumer uneasiness exists. The Reuters/University of Michigan Consumer Sentiment Index has fallen slightly the past few months and is now right in line

Bloomberg Consumer Comfort Index has improved slightly in the past month and is ahead of the results at this time last year. for April was higher than the March results, but slightly below the level for last year. The absence of consistent enthusiasm from consumers is offset partially by an improved situation relative to last year with gasoline prices. As of the end of April, the national average price for regular gasoline was just over eight percent lower than last year, a difference of over 30 cents. Gas prices do remain high, however, making it unlikely that the price difference will be a major spur for travelers this holiday period.

Our survey of intending travelers supports the expectation of a rate of travelers similar to last year this travel period. Only minor shifts are expected in the demographics of the travel party, while the differences in expected spending levels and travel distances are also not significant.

35.9 33.2 30.9 34.6

44.0

36.0 35.331.6 30.5

34.8 34.3 35.1 34.8

-‐30%

-‐20%

-‐10%

0%

10%

20%

30%

0

10

20

30

40

50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(F)

(Percent Change)

(Million)

Person Trips (left) % change (right)

4 IHS / AAA 2013 Memorial Day Forecast

The Memorial Day holiday commemorates those who have died in service to our country, while also serving as the unofficial kickoff of the summer season. AAA and IHS forecast a minor decline in travelers this Memorial Day holiday of 0.9 percent, with 34.8 million travelers expected. Now four years removed from the recessionary declines of 2009, pent-up demand has been largely satisfied. This figure is just above the average volume in the previous 12 years, which is 34.7 million.

5 IHS / AAA 2013 Memorial Day Forecast

Last year, holiday spending included airfare and hotel

accommodations and my 2013 Memorial Day holidays plans do

not include those costs. Pacific Respondent

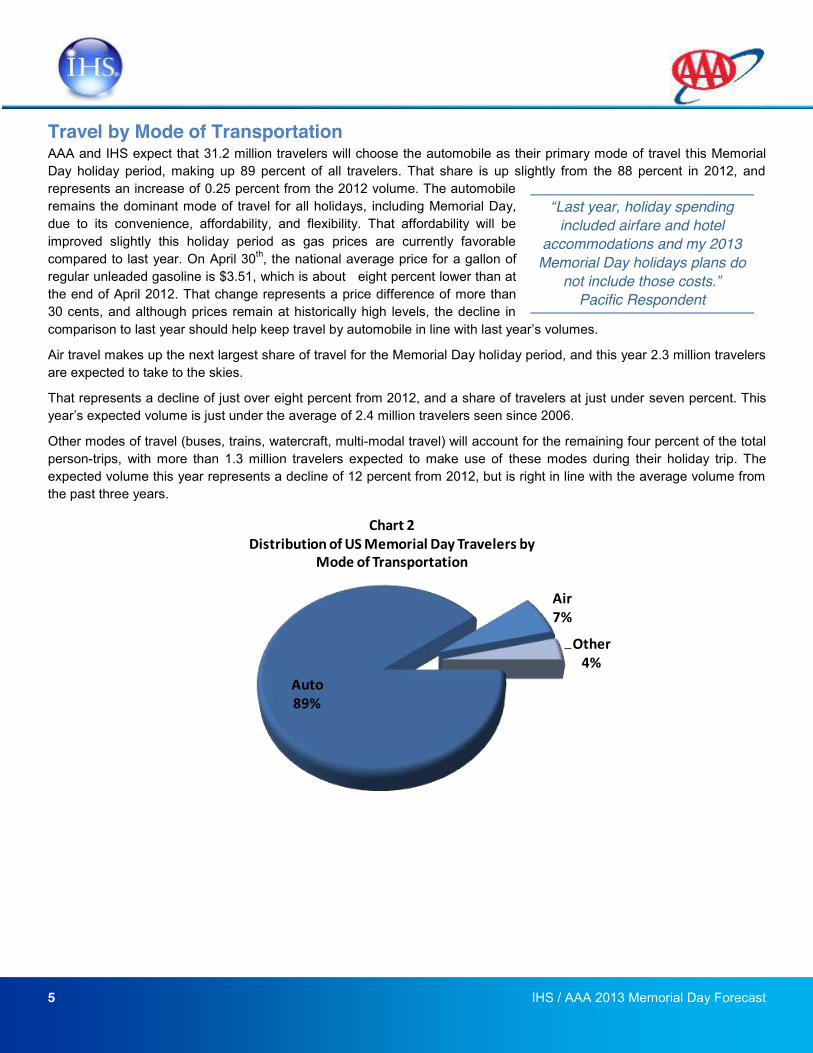

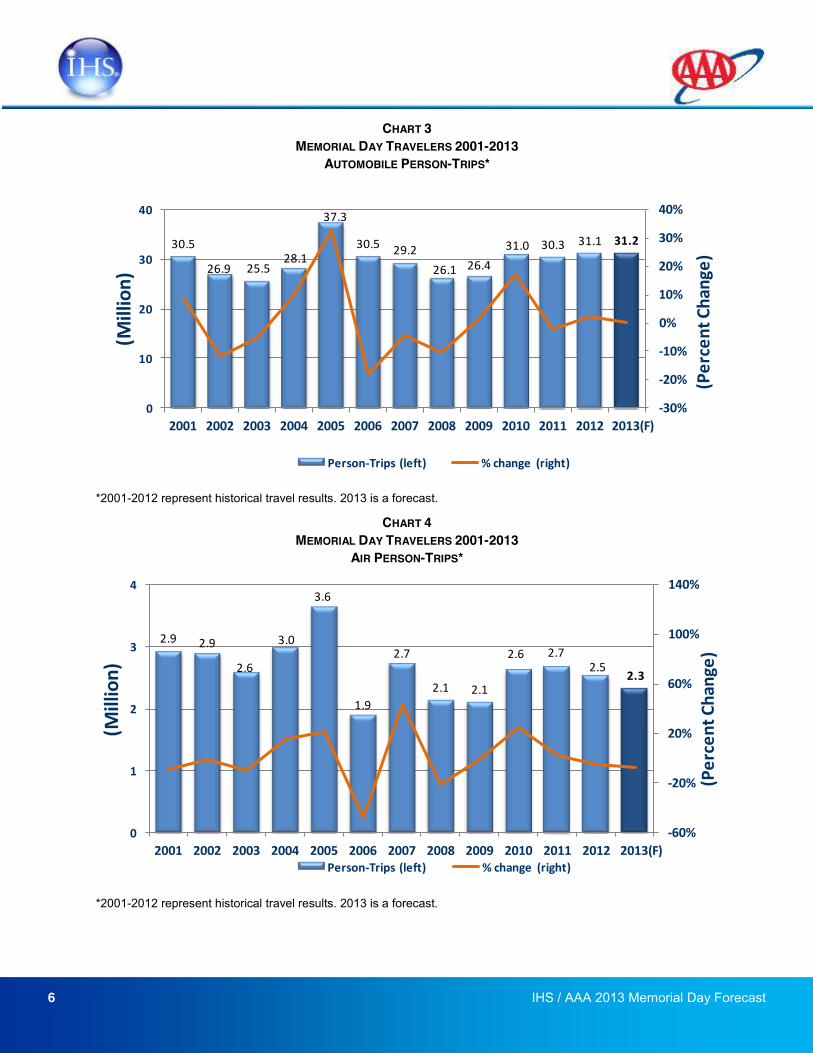

Travel by Mode of Transportation AAA and IHS expect that 31.2 million travelers will choose the automobile as their primary mode of travel this Memorial Day holiday period, making up 89 percent of all travelers. That share is up slightly from the 88 percent in 2012, and represents an increase of 0.25 percent from the 2012 volume. The automobile remains the dominant mode of travel for all holidays, including Memorial Day, due to its convenience, affordability, and flexibility. That affordability will be improved slightly this holiday period as gas prices are currently favorable compared to last year. On April 30th, the national average price for a gallon of regular unleaded gasoline is $3.51, which is about eight percent lower than at the end of April 2012. That change represents a price difference of more than 30 cents, and although prices remain at historically high levels, the decline in

Air travel makes up the next largest share of travel for the Memorial Day holiday period, and this year 2.3 million travelers are expected to take to the skies.

That represents a decline of just over eight percent from 2012, and a share of travelers at just under seven percent. This of 2.4 million travelers seen since 2006.

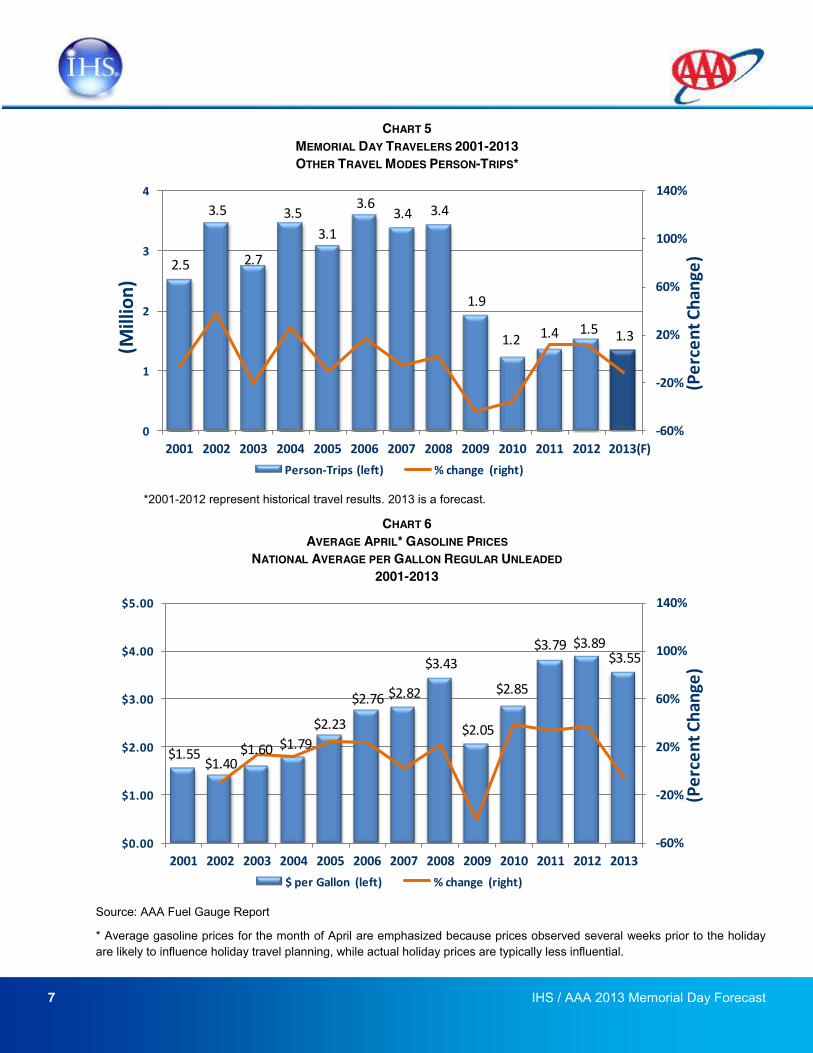

Other modes of travel (buses, trains, watercraft, multi-modal travel) will account for the remaining four percent of the total person-trips, with more than 1.3 million travelers expected to make use of these modes during their holiday trip. The expected volume this year represents a decline of 12 percent from 2012, but is right in line with the average volume from the past three years.

Auto89%

Air7%

Other4%

Chart 2Distribution of US Memorial Day Travelers by

Mode of Transportation

6 IHS / AAA 2013 Memorial Day Forecast

CHART 3 MEMORIAL DAY TRAVELERS 2001-2013

AUTOMOBILE PERSON-TRIPS*

*2001-2012 represent historical travel results. 2013 is a forecast.

CHART 4 MEMORIAL DAY TRAVELERS 2001-2013

AIR PERSON-TRIPS*

*2001-2012 represent historical travel results. 2013 is a forecast.

30.5

26.9 25.528.1

37.3

30.5 29.226.1 26.4

31.0 30.3 31.1 31.2

-‐30%

-‐20%

-‐10%

0%

10%

20%

30%

40%

0

10

20

30

40

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(F)

(Percent Change)

(Million)

Person-‐Trips (left) % change (right)

2.9 2.9

2.6

3.0

3.6

1.9

2.7

2.1 2.1

2.6 2.72.5

2.3

-‐60%

-‐20%

20%

60%

100%

140%

0

1

2

3

4

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(F)

(Percent Change)

(Million)

Person-‐Trips (left) % change (right)

7 IHS / AAA 2013 Memorial Day Forecast

CHART 5 MEMORIAL DAY TRAVELERS 2001-2013 OTHER TRAVEL MODES PERSON-TRIPS*

*2001-2012 represent historical travel results. 2013 is a forecast.

CHART 6 AVERAGE APRIL* GASOLINE PRICES

NATIONAL AVERAGE PER GALLON REGULAR UNLEADED 2001-2013

Source: AAA Fuel Gauge Report

* Average gasoline prices for the month of April are emphasized because prices observed several weeks prior to the holiday are likely to influence holiday travel planning, while actual holiday prices are typically less influential.

2.5

3.5

2.7

3.53.1

3.63.4 3.4

1.9

1.2 1.4 1.5 1.3

-‐60%

-‐20%

20%

60%

100%

140%

0

1

2

3

4

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(F)

(Percent Change)

(Million)

Person-‐Trips (left) % change (right)

$1.55$1.40

$1.60 $1.79$2.23

$2.76 $2.82

$3.43

$2.05

$2.85

$3.79 $3.89$3.55

-‐60%

-‐20%

20%

60%

100%

140%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(Percent Change)

$ per Gallon (left) % change (right)

8 IHS / AAA 2013 Memorial Day Forecast

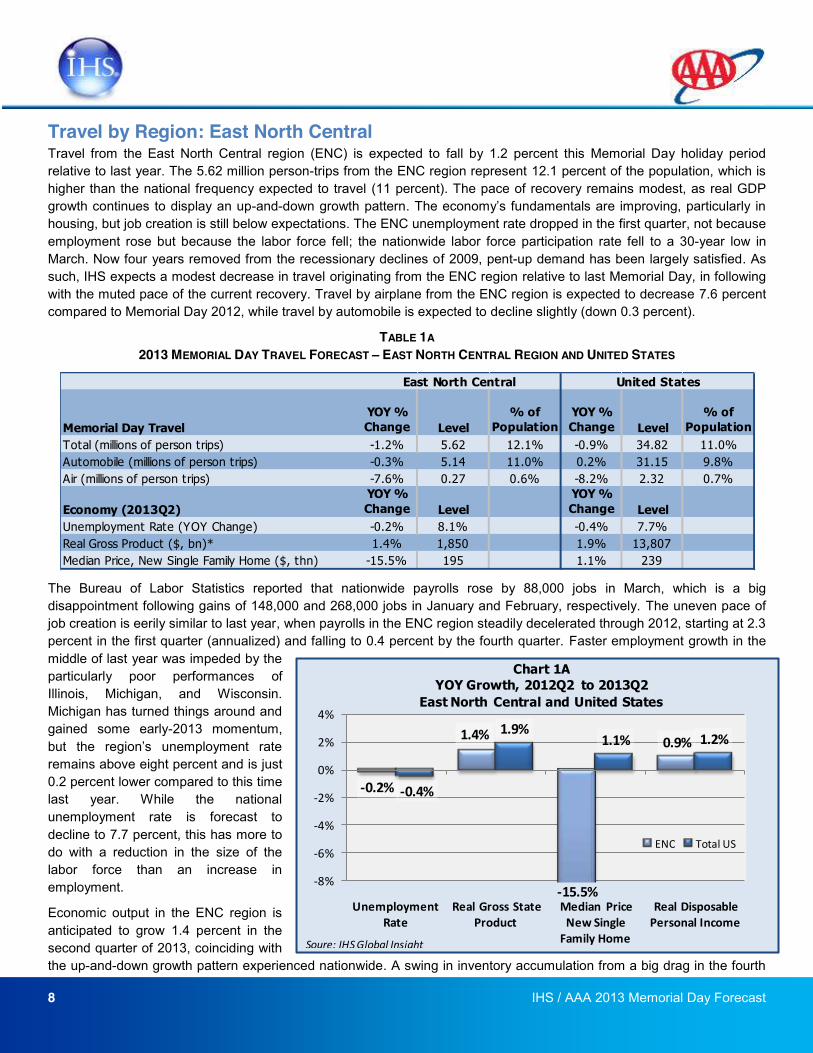

Travel by Region: East North Central Travel from the East North Central region (ENC) is expected to fall by 1.2 percent this Memorial Day holiday period relative to last year. The 5.62 million person-trips from the ENC region represent 12.1 percent of the population, which is higher than the national frequency expected to travel (11 percent). The pace of recovery remains modest, as real GDP growth continues to display an up-and-down growth patternhousing, but job creation is still below expectations. The ENC unemployment rate dropped in the first quarter, not because employment rose but because the labor force fell; the nationwide labor force participation rate fell to a 30-year low in March. Now four years removed from the recessionary declines of 2009, pent-up demand has been largely satisfied. As such, IHS expects a modest decrease in travel originating from the ENC region relative to last Memorial Day, in following with the muted pace of the current recovery. Travel by airplane from the ENC region is expected to decrease 7.6 percent compared to Memorial Day 2012, while travel by automobile is expected to decline slightly (down 0.3 percent).

TABLE 1A 2013 MEMORIAL DAY TRAVEL FORECAST EAST NORTH CENTRAL REGION AND UNITED STATES

The Bureau of Labor Statistics reported that nationwide payrolls rose by 88,000 jobs in March, which is a big disappointment following gains of 148,000 and 268,000 jobs in January and February, respectively. The uneven pace of job creation is eerily similar to last year, when payrolls in the ENC region steadily decelerated through 2012, starting at 2.3 percent in the first quarter (annualized) and falling to 0.4 percent by the fourth quarter. Faster employment growth in the middle of last year was impeded by the particularly poor performances of Illinois, Michigan, and Wisconsin. Michigan has turned things around and gained some early-2013 momentum,

remains above eight percent and is just 0.2 percent lower compared to this time last year. While the national unemployment rate is forecast to decline to 7.7 percent, this has more to do with a reduction in the size of the labor force than an increase in employment.

Economic output in the ENC region is anticipated to grow 1.4 percent in the second quarter of 2013, coinciding with the up-and-down growth pattern experienced nationwide. A swing in inventory accumulation from a big drag in the fourth

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -1.2% 5.62 12.1% -0.9% 34.82 11.0%Automobile (millions of person trips) -0.3% 5.14 11.0% 0.2% 31.15 9.8%Air (millions of person trips) -7.6% 0.27 0.6% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.2% 8.1% -0.4% 7.7%Real Gross Product ($, bn)* 1.4% 1,850 1.9% 13,807Median Price, New Single Family Home ($, thn) -15.5% 195 1.1% 239

East North Central United States

-‐0.2%

1.4% 0.9%

-‐0.4%

1.9%1.1% 1.2%

-‐8%

-‐6%

-‐4%

-‐2%

0%

2%

4%

Unemployment Rate

Real Gross State Product

Median Price New Single Family Home

Real Disposable Personal Income

Chart 1AYOY Growth, 2012Q2 to 2013Q2

East North Central and United States

ENC Total US

Soure: IHS Globql Insight

-‐15.5%

9 IHS / AAA 2013 Memorial Day Forecast

to a big plus in the first quarter accounted for most of the sway in national GDP growth. In the second quarter, inventory accumulation will probably slow and become a drag once again. Consequently, IHS sees no immediate end to the up-and-down pattern of growth in both the ENC region and the greater nation.

Real disposable personal income growth in the ENC is slightly below the national rate and is projected to rise 0.9 percent as compared to one year ago (versus 1.2 percent nationally). The increase in disposable income means that potential travelers will have more money in their pockets than last holiday, but the expiry of the payroll tax cut and the disappearance of special dividends are headwinds to discretionary spending growth. The regional housing market continues to struggle as the median price of new single-family homes is expected to fall 15.5 percent in the second quarter. In order for the housing market to improve significantly, there will need to be economic recovery to the extent of providing enough qualified borrowers and buyers to stimulate demand, which will clear the existing inventory from the market and drive new starts, sales and construction employment.

In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry. The following information provides a look into the state of the local tourism industry in the East North Central region

The tourism industry in the ENC region, as measured by leisure and hospitality industry output (the value of goods and services produced by the industry), has been decelerating since the first quarter of 2012, and increased by less than one percent in the first two quarters of 2013. Despite the deceleration, however, consumers are cautiously increasing their spending on tourism. As labor markets loosen, consumer spending growth will no longer be limited by weak disposable income gains, and the tourism industry will enjoy a more robust recovery.

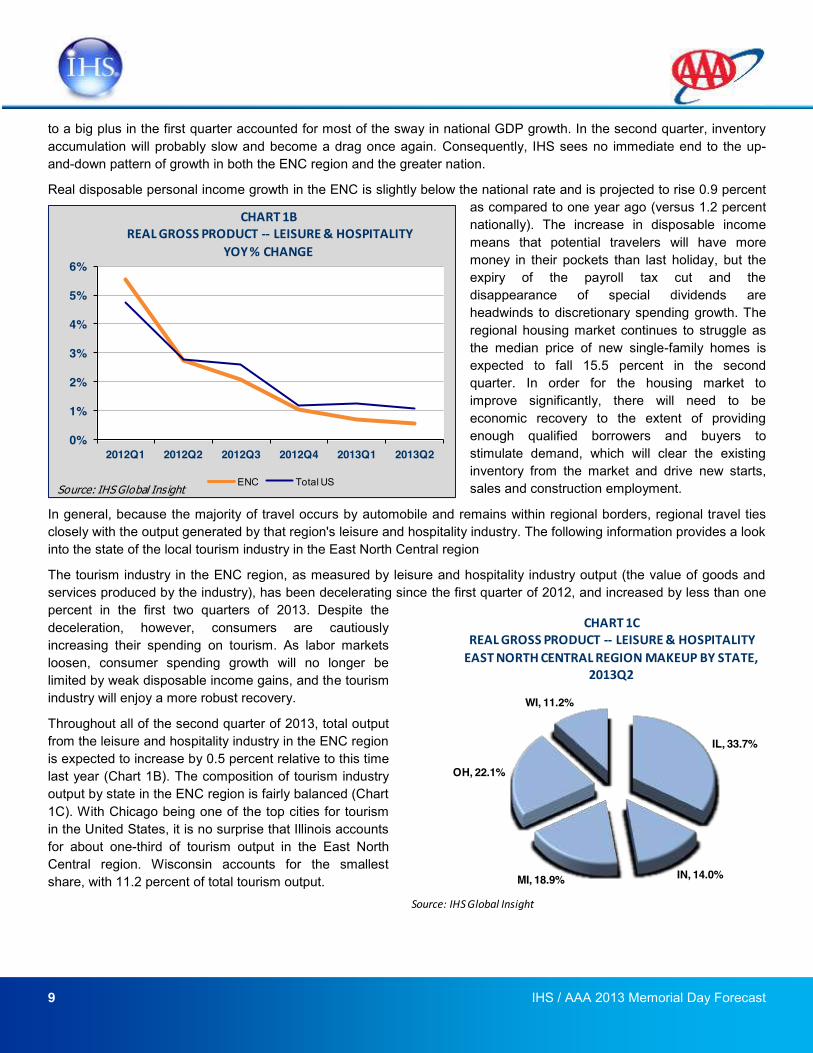

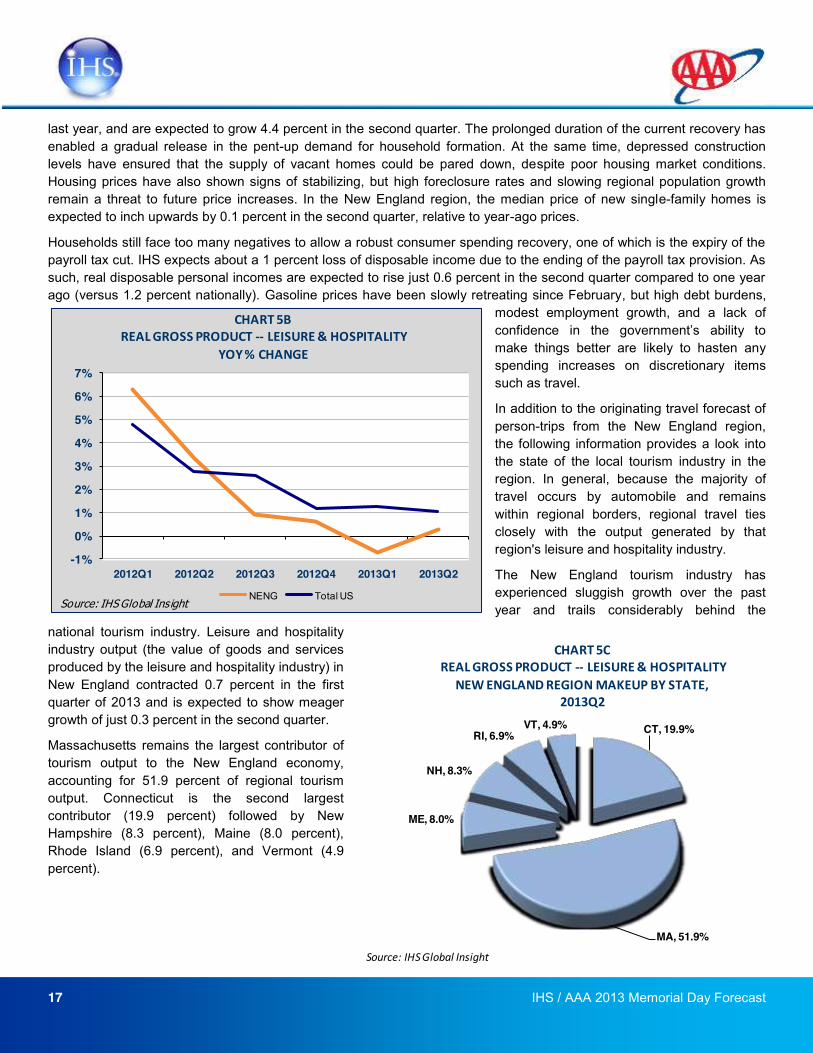

Throughout all of the second quarter of 2013, total output from the leisure and hospitality industry in the ENC region is expected to increase by 0.5 percent relative to this time last year (Chart 1B). The composition of tourism industry output by state in the ENC region is fairly balanced (Chart 1C). With Chicago being one of the top cities for tourism in the United States, it is no surprise that Illinois accounts for about one-third of tourism output in the East North Central region. Wisconsin accounts for the smallest share, with 11.2 percent of total tourism output.

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 1BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

ENC Total USSource: IHS Global Insight

IL, 33.7%

IN, 14.0%MI, 18.9%

OH, 22.1%

WI, 11.2%

CHART 1CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITYEAST NORTH CENTRAL REGION MAKEUP BY STATE,

2013Q2

Source: IHS Global Insight

10 IHS / AAA 2013 Memorial Day Forecast

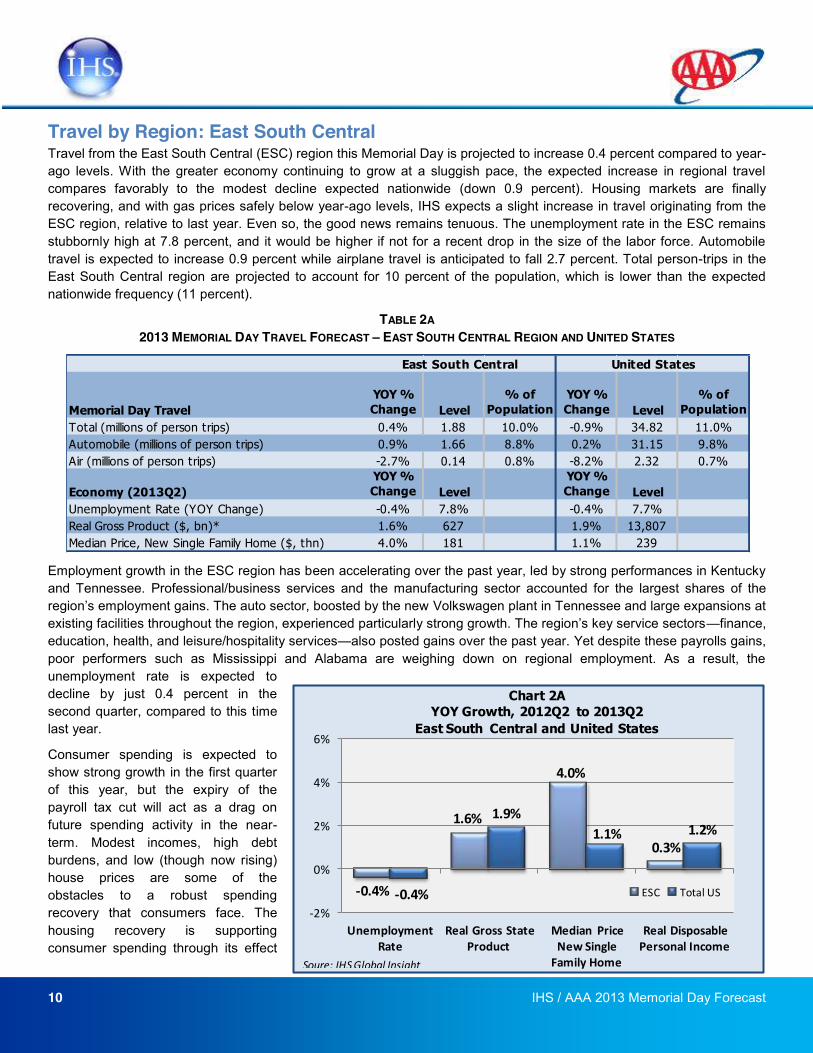

Travel by Region: East South Central Travel from the East South Central (ESC) region this Memorial Day is projected to increase 0.4 percent compared to year-ago levels. With the greater economy continuing to grow at a sluggish pace, the expected increase in regional travel compares favorably to the modest decline expected nationwide (down 0.9 percent). Housing markets are finally recovering, and with gas prices safely below year-ago levels, IHS expects a slight increase in travel originating from the ESC region, relative to last year. Even so, the good news remains tenuous. The unemployment rate in the ESC remains stubbornly high at 7.8 percent, and it would be higher if not for a recent drop in the size of the labor force. Automobile travel is expected to increase 0.9 percent while airplane travel is anticipated to fall 2.7 percent. Total person-trips in the East South Central region are projected to account for 10 percent of the population, which is lower than the expected nationwide frequency (11 percent).

TABLE 2A 2013 MEMORIAL DAY TRAVEL FORECAST EAST SOUTH CENTRAL REGION AND UNITED STATES

Employment growth in the ESC region has been accelerating over the past year, led by strong performances in Kentucky and Tennessee. Professional/business services and the manufacturing sector accounted for the largest shares of the

Volkswagen plant in Tennessee and large expansions at finance,

education, health, and leisure/hospitality services also posted gains over the past year. Yet despite these payrolls gains, poor performers such as Mississippi and Alabama are weighing down on regional employment. As a result, the unemployment rate is expected to decline by just 0.4 percent in the second quarter, compared to this time last year.

Consumer spending is expected to show strong growth in the first quarter of this year, but the expiry of the payroll tax cut will act as a drag on future spending activity in the near-term. Modest incomes, high debt burdens, and low (though now rising) house prices are some of the obstacles to a robust spending recovery that consumers face. The housing recovery is supporting consumer spending through its effect

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) 0.4% 1.88 10.0% -0.9% 34.82 11.0%Automobile (millions of person trips) 0.9% 1.66 8.8% 0.2% 31.15 9.8%Air (millions of person trips) -2.7% 0.14 0.8% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.4% 7.8% -0.4% 7.7%Real Gross Product ($, bn)* 1.6% 627 1.9% 13,807Median Price, New Single Family Home ($, thn) 4.0% 181 1.1% 239

East South Central United States

-‐0.4%

1.6%

4.0%

0.3%

-‐0.4%

1.9%1.1% 1.2%

-‐2%

0%

2%

4%

6%

Unemployment Rate

Real Gross State Product

Median Price New Single Family Home

Real Disposable Personal Income

Chart 2AYOY Growth, 2012Q2 to 2013Q2

East South Central and United States

ESC Total US

Soure: IHS Globql Insight

11 IHS / AAA 2013 Memorial Day Forecast

on wealth and on housing-related purchases, and is probably one of the reasons why consumer spending growth was strong in the first quarter. The median price of a new single-family home in the ESC region is expected to grow four percent in the second quarter relative to the same quarter last year. While we expect home prices to steadily rise, the impact of the housing recovery on consumer spending is unlikely to be maintained. As such, we expect a modest increase in ESC travel this coming Memorial Day.

The ES e region is back to a sustained growth track. Job creation continues to remain a concern and despite the housing recovery, consumers continue to experience a drag from high (though falling) debt burdens. With weak improvements in employment and output, the ESC region is expected to see a small 0.4 percent increase in total person-trips over the Memorial Day holiday, which compares favorably to the 0.9 percent decline that is forecasted nationwide.

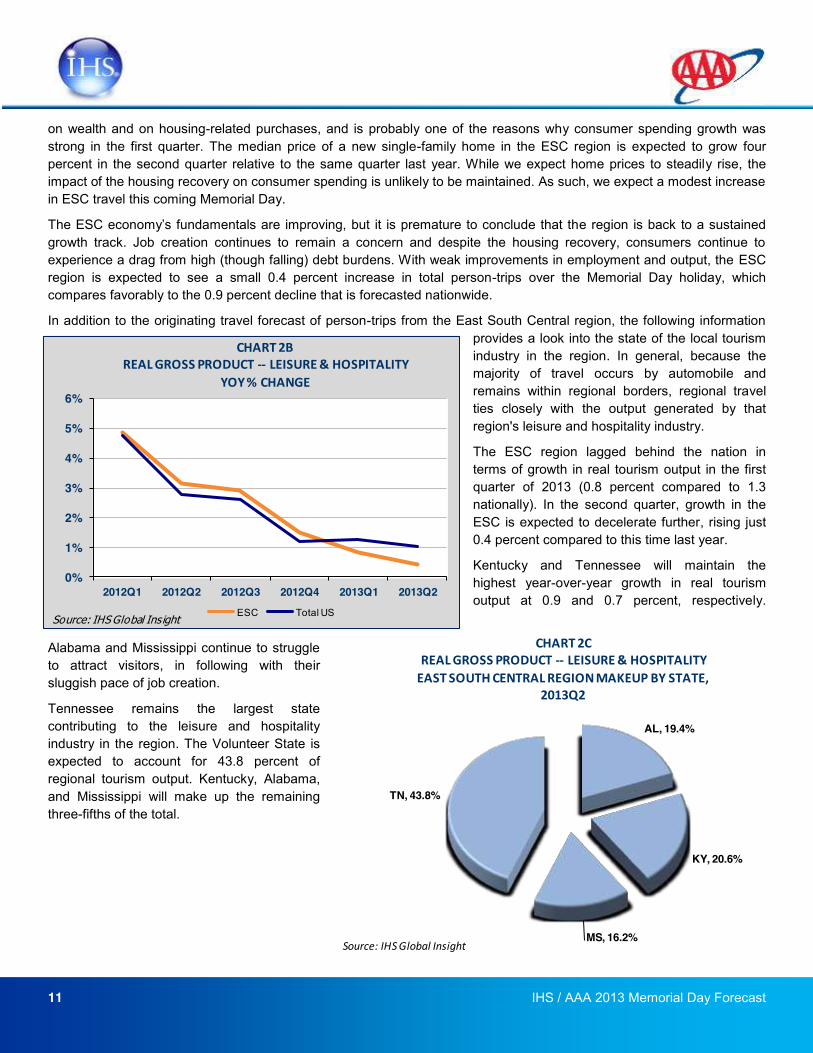

In addition to the originating travel forecast of person-trips from the East South Central region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

The ESC region lagged behind the nation in terms of growth in real tourism output in the first quarter of 2013 (0.8 percent compared to 1.3 nationally). In the second quarter, growth in the ESC is expected to decelerate further, rising just 0.4 percent compared to this time last year.

Kentucky and Tennessee will maintain the highest year-over-year growth in real tourism output at 0.9 and 0.7 percent, respectively.

Alabama and Mississippi continue to struggle to attract visitors, in following with their sluggish pace of job creation.

Tennessee remains the largest state contributing to the leisure and hospitality industry in the region. The Volunteer State is expected to account for 43.8 percent of regional tourism output. Kentucky, Alabama, and Mississippi will make up the remaining three-fifths of the total.

AL, 19.4%

KY, 20.6%

MS, 16.2%

TN, 43.8%

CHART 2CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITYEAST SOUTH CENTRAL REGION MAKEUP BY STATE,

2013Q2

Source: IHS Global Insight

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 2BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

ESC Total USSource: IHS Global Insight

12 IHS / AAA 2013 Memorial Day Forecast

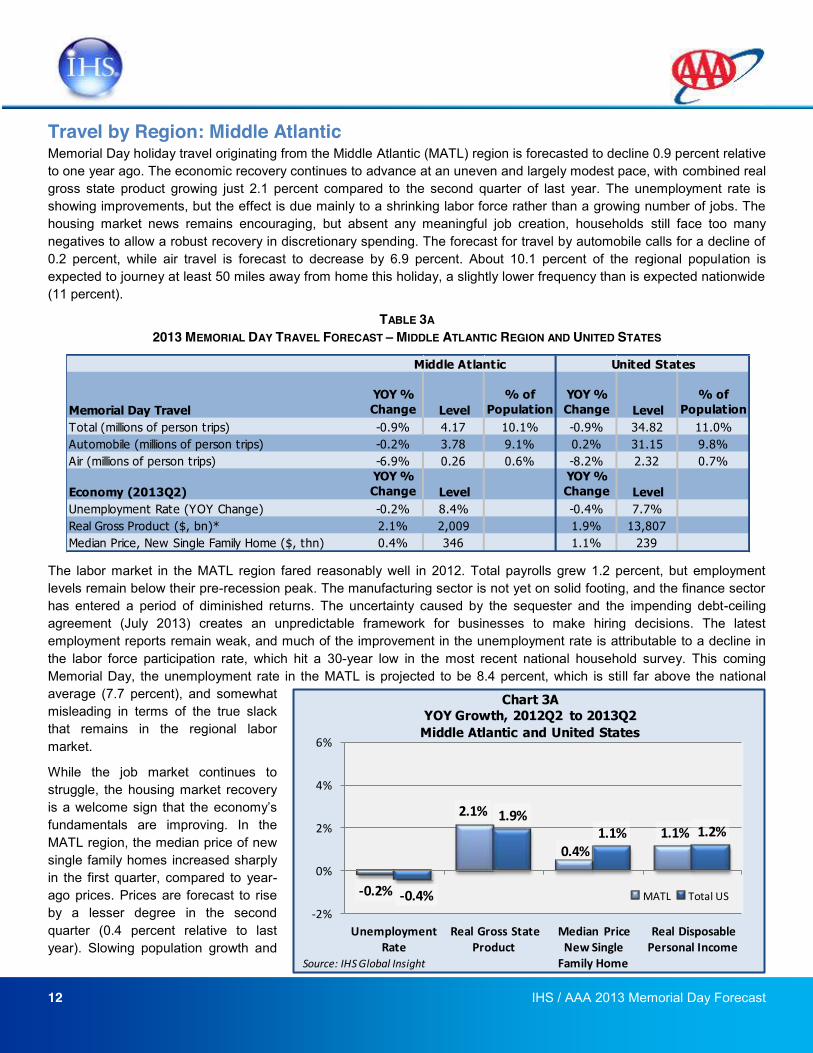

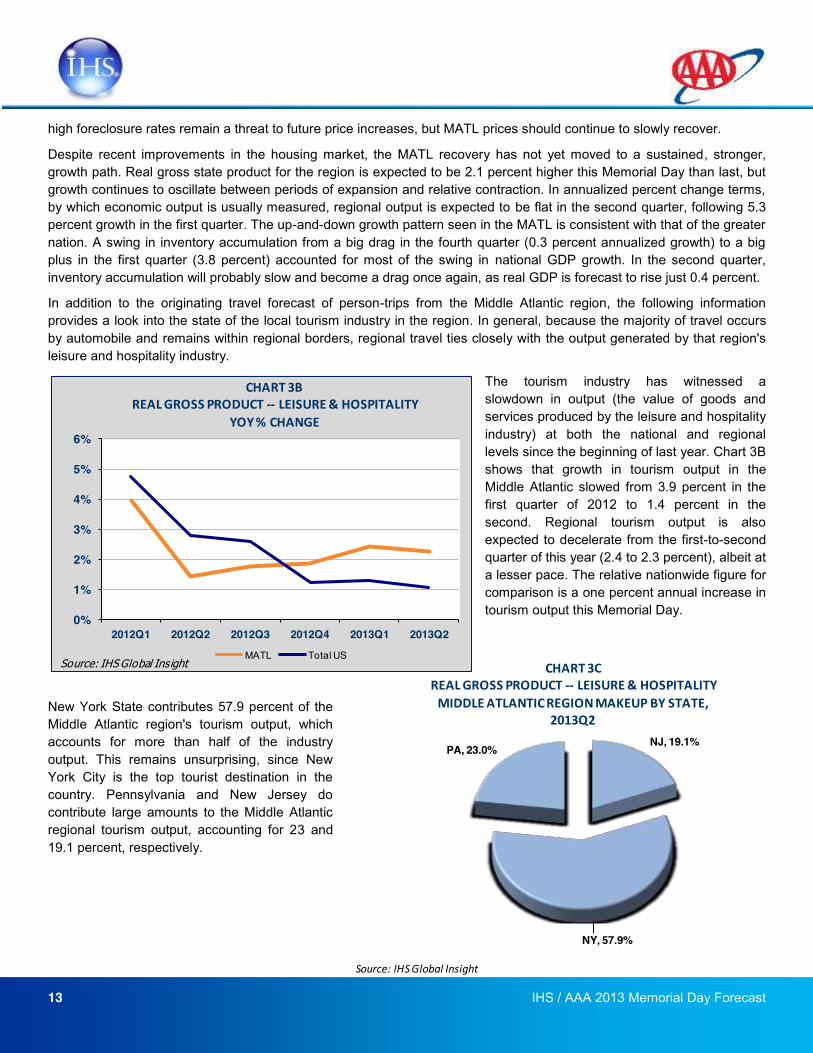

Travel by Region: Middle Atlantic Memorial Day holiday travel originating from the Middle Atlantic (MATL) region is forecasted to decline 0.9 percent relative to one year ago. The economic recovery continues to advance at an uneven and largely modest pace, with combined real gross state product growing just 2.1 percent compared to the second quarter of last year. The unemployment rate is showing improvements, but the effect is due mainly to a shrinking labor force rather than a growing number of jobs. The housing market news remains encouraging, but absent any meaningful job creation, households still face too many negatives to allow a robust recovery in discretionary spending. The forecast for travel by automobile calls for a decline of 0.2 percent, while air travel is forecast to decrease by 6.9 percent. About 10.1 percent of the regional population is expected to journey at least 50 miles away from home this holiday, a slightly lower frequency than is expected nationwide (11 percent).

TABLE 3A 2013 MEMORIAL DAY TRAVEL FORECAST MIDDLE ATLANTIC REGION AND UNITED STATES

The labor market in the MATL region fared reasonably well in 2012. Total payrolls grew 1.2 percent, but employment levels remain below their pre-recession peak. The manufacturing sector is not yet on solid footing, and the finance sector has entered a period of diminished returns. The uncertainty caused by the sequester and the impending debt-ceiling agreement (July 2013) creates an unpredictable framework for businesses to make hiring decisions. The latest employment reports remain weak, and much of the improvement in the unemployment rate is attributable to a decline in the labor force participation rate, which hit a 30-year low in the most recent national household survey. This coming Memorial Day, the unemployment rate in the MATL is projected to be 8.4 percent, which is still far above the national average (7.7 percent), and somewhat misleading in terms of the true slack that remains in the regional labor market.

While the job market continues to struggle, the housing market recovery

fundamentals are improving. In the MATL region, the median price of new single family homes increased sharply in the first quarter, compared to year-ago prices. Prices are forecast to rise by a lesser degree in the second quarter (0.4 percent relative to last year). Slowing population growth and

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -0.9% 4.17 10.1% -0.9% 34.82 11.0%Automobile (millions of person trips) -0.2% 3.78 9.1% 0.2% 31.15 9.8%Air (millions of person trips) -6.9% 0.26 0.6% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.2% 8.4% -0.4% 7.7%Real Gross Product ($, bn)* 2.1% 2,009 1.9% 13,807Median Price, New Single Family Home ($, thn) 0.4% 346 1.1% 239

Middle Atlantic United States

-‐0.2%

2.1%

0.4%1.1%

-‐0.4%

1.9%1.1% 1.2%

-‐2%

0%

2%

4%

6%

Unemployment Rate

Real Gross State Product

Median Price New Single Family Home

Real Disposable Personal Income

Chart 3AYOY Growth, 2012Q2 to 2013Q2Middle Atlantic and United States

MATL Total US

Source: IHS Global Insight

13 IHS / AAA 2013 Memorial Day Forecast

high foreclosure rates remain a threat to future price increases, but MATL prices should continue to slowly recover.

Despite recent improvements in the housing market, the MATL recovery has not yet moved to a sustained, stronger, growth path. Real gross state product for the region is expected to be 2.1 percent higher this Memorial Day than last, but growth continues to oscillate between periods of expansion and relative contraction. In annualized percent change terms, by which economic output is usually measured, regional output is expected to be flat in the second quarter, following 5.3 percent growth in the first quarter. The up-and-down growth pattern seen in the MATL is consistent with that of the greater nation. A swing in inventory accumulation from a big drag in the fourth quarter (0.3 percent annualized growth) to a big plus in the first quarter (3.8 percent) accounted for most of the swing in national GDP growth. In the second quarter, inventory accumulation will probably slow and become a drag once again, as real GDP is forecast to rise just 0.4 percent.

In addition to the originating travel forecast of person-trips from the Middle Atlantic region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

The tourism industry has witnessed a slowdown in output (the value of goods and services produced by the leisure and hospitality industry) at both the national and regional levels since the beginning of last year. Chart 3B shows that growth in tourism output in the Middle Atlantic slowed from 3.9 percent in the first quarter of 2012 to 1.4 percent in the second. Regional tourism output is also expected to decelerate from the first-to-second quarter of this year (2.4 to 2.3 percent), albeit at a lesser pace. The relative nationwide figure for comparison is a one percent annual increase in tourism output this Memorial Day.

New York State contributes 57.9 percent of the Middle Atlantic region's tourism output, which accounts for more than half of the industry output. This remains unsurprising, since New York City is the top tourist destination in the country. Pennsylvania and New Jersey do contribute large amounts to the Middle Atlantic regional tourism output, accounting for 23 and 19.1 percent, respectively.

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 3BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

MATL Total USSource: IHS Global Insight

NJ, 19.1%

NY, 57.9%

PA, 23.0%

CHART 3CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITYMIDDLE ATLANTIC REGION MAKEUP BY STATE,

2013Q2

Source: IHS Global Insight

14 IHS / AAA 2013 Memorial Day Forecast

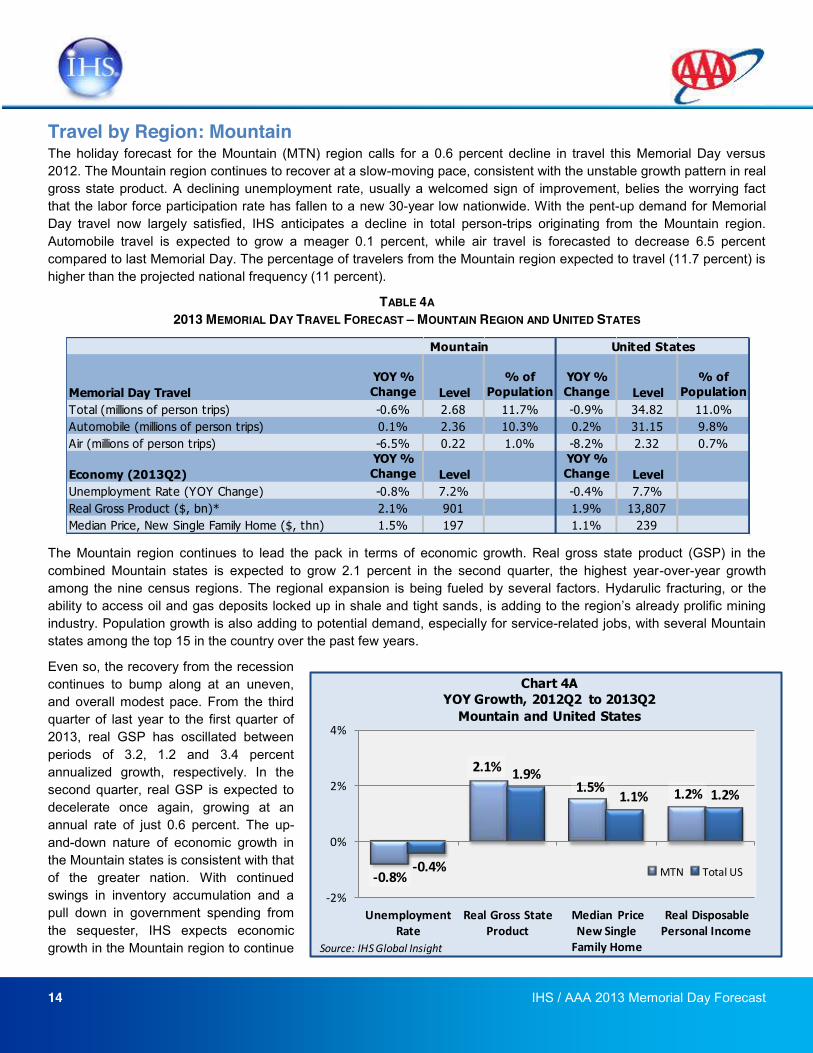

Travel by Region: Mountain The holiday forecast for the Mountain (MTN) region calls for a 0.6 percent decline in travel this Memorial Day versus 2012. The Mountain region continues to recover at a slow-moving pace, consistent with the unstable growth pattern in real gross state product. A declining unemployment rate, usually a welcomed sign of improvement, belies the worrying fact that the labor force participation rate has fallen to a new 30-year low nationwide. With the pent-up demand for Memorial Day travel now largely satisfied, IHS anticipates a decline in total person-trips originating from the Mountain region. Automobile travel is expected to grow a meager 0.1 percent, while air travel is forecasted to decrease 6.5 percent compared to last Memorial Day. The percentage of travelers from the Mountain region expected to travel (11.7 percent) is higher than the projected national frequency (11 percent).

TABLE 4A 2013 MEMORIAL DAY TRAVEL FORECAST MOUNTAIN REGION AND UNITED STATES

The Mountain region continues to lead the pack in terms of economic growth. Real gross state product (GSP) in the combined Mountain states is expected to grow 2.1 percent in the second quarter, the highest year-over-year growth among the nine census regions. The regional expansion is being fueled by several factors. Hydarulic fracturing, or the ability to access oil and gas deposits locked up in shale and tight sands, industry. Population growth is also adding to potential demand, especially for service-related jobs, with several Mountain states among the top 15 in the country over the past few years.

Even so, the recovery from the recession continues to bump along at an uneven, and overall modest pace. From the third quarter of last year to the first quarter of 2013, real GSP has oscillated between periods of 3.2, 1.2 and 3.4 percent annualized growth, respectively. In the second quarter, real GSP is expected to decelerate once again, growing at an annual rate of just 0.6 percent. The up-and-down nature of economic growth in the Mountain states is consistent with that of the greater nation. With continued swings in inventory accumulation and a pull down in government spending from the sequester, IHS expects economic growth in the Mountain region to continue

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -0.6% 2.68 11.7% -0.9% 34.82 11.0%Automobile (millions of person trips) 0.1% 2.36 10.3% 0.2% 31.15 9.8%Air (millions of person trips) -6.5% 0.22 1.0% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.8% 7.2% -0.4% 7.7%Real Gross Product ($, bn)* 2.1% 901 1.9% 13,807Median Price, New Single Family Home ($, thn) 1.5% 197 1.1% 239

Mountain United States

-‐0.8%

2.1%1.5% 1.2%

-‐0.4%

1.9%1.1% 1.2%

-‐2%

0%

2%

4%

Unemployment Rate

Real Gross State Product

Median Price New Single Family Home

Real Disposable Personal Income

Chart 4AYOY Growth, 2012Q2 to 2013Q2Mountain and United States

MTN Total US

Source: IHS Global Insight

15 IHS / AAA 2013 Memorial Day Forecast

to move at an uneven and modest pace.

The unemployment rate in the Mountain region (7.2 percent) remains the fourth-lowest among all census regions, and 0.8 percent lower than this time last year. This is partly due to an increase in energy activity (e.g., mining, oil and natural gas extraction) but is also, to some extent, merely a statistical artifact. The latest US household survey saw the labor force decline by 496,000 workers, while the number of people employed also fell, but by less than the size of the labor force. As a result, the labor force participation rate fell to a new 30-year low (63.3 percent), leading to a drop in the unemployment rate. Meanwhile, the March employment report, which comes from a different survey, was much worse than expected with only 88,000 new jobs created. Taken together, the reduction in unemployment is likely overstating the strength of the regional labor market.

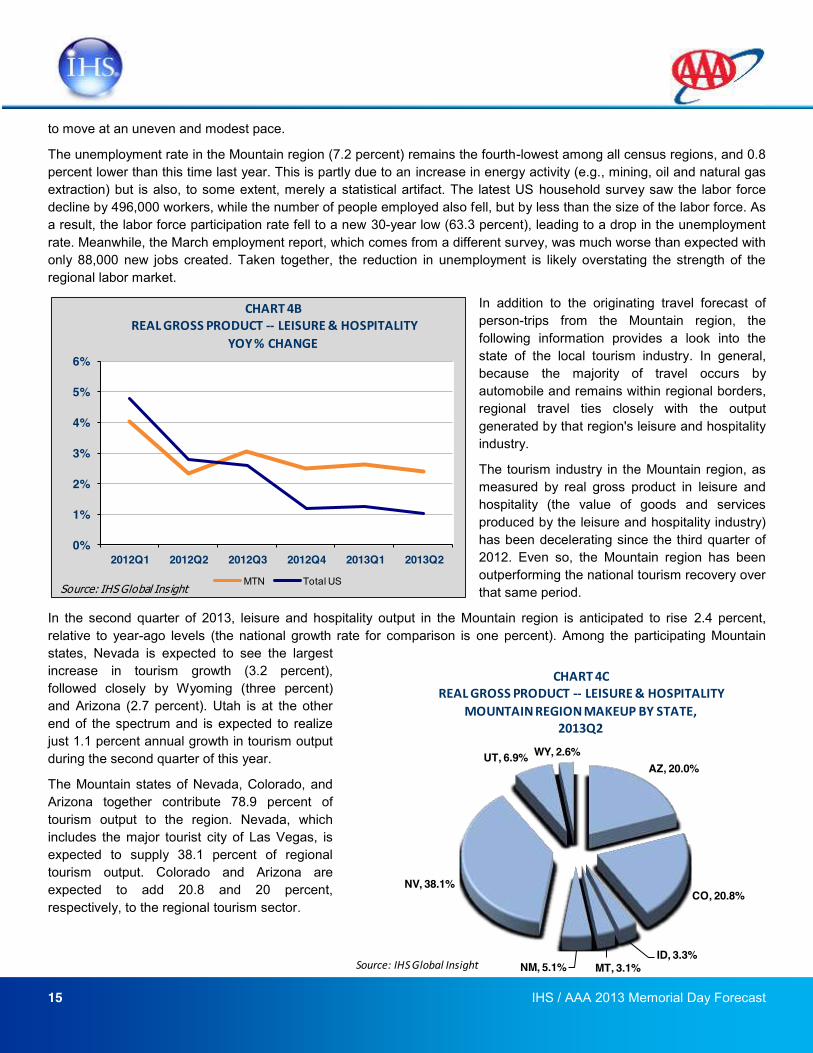

In addition to the originating travel forecast of person-trips from the Mountain region, the following information provides a look into the state of the local tourism industry. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

The tourism industry in the Mountain region, as measured by real gross product in leisure and hospitality (the value of goods and services produced by the leisure and hospitality industry) has been decelerating since the third quarter of 2012. Even so, the Mountain region has been outperforming the national tourism recovery over that same period.

In the second quarter of 2013, leisure and hospitality output in the Mountain region is anticipated to rise 2.4 percent, relative to year-ago levels (the national growth rate for comparison is one percent). Among the participating Mountain states, Nevada is expected to see the largest increase in tourism growth (3.2 percent), followed closely by Wyoming (three percent) and Arizona (2.7 percent). Utah is at the other end of the spectrum and is expected to realize just 1.1 percent annual growth in tourism output during the second quarter of this year.

The Mountain states of Nevada, Colorado, and Arizona together contribute 78.9 percent of tourism output to the region. Nevada, which includes the major tourist city of Las Vegas, is expected to supply 38.1 percent of regional tourism output. Colorado and Arizona are expected to add 20.8 and 20 percent, respectively, to the regional tourism sector.

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 4BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

MTN Total USSource: IHS Global Insight

AZ, 20.0%

CO, 20.8%

ID, 3.3%MT, 3.1%NM, 5.1%

NV, 38.1%

UT, 6.9% WY, 2.6%

CHART 4CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

MOUNTAIN REGION MAKEUP BY STATE, 2013Q2

Source: IHS Global Insight

16 IHS / AAA 2013 Memorial Day Forecast

Travel by Region: New England

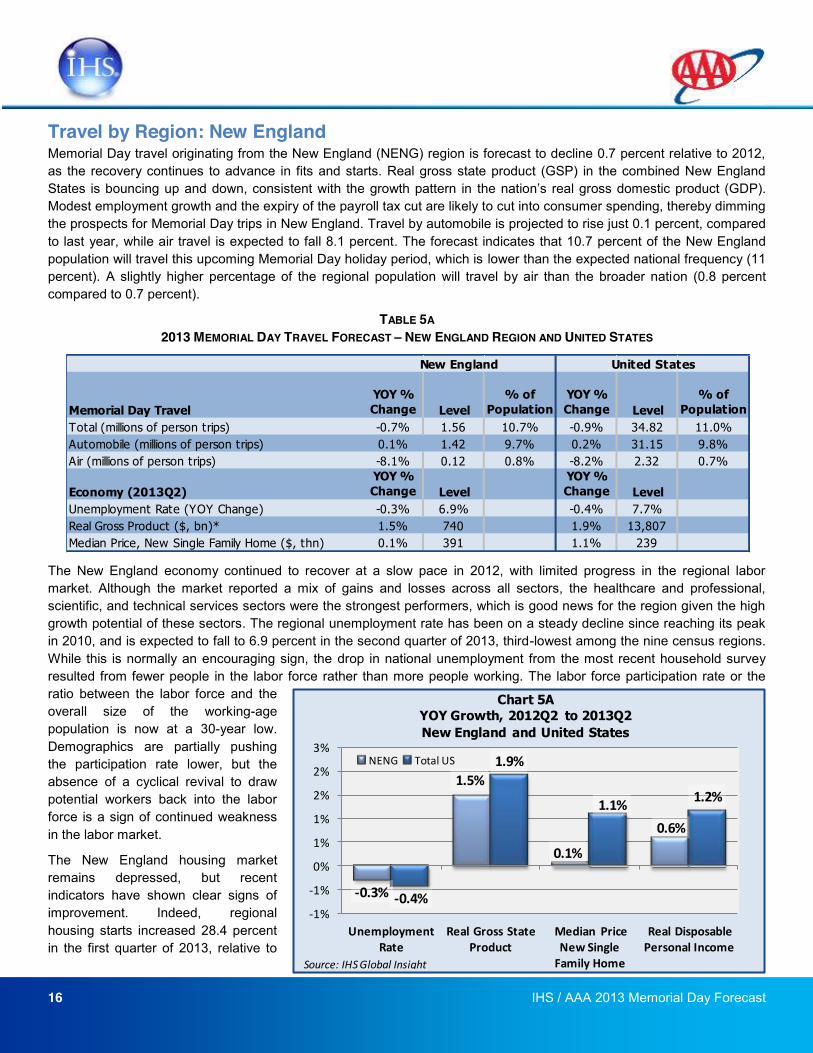

Memorial Day travel originating from the New England (NENG) region is forecast to decline 0.7 percent relative to 2012, as the recovery continues to advance in fits and starts. Real gross state product (GSP) in the combined New England States is bouncing up and down, consistent with the growth pattern in real gross domestic product (GDP). Modest employment growth and the expiry of the payroll tax cut are likely to cut into consumer spending, thereby dimming the prospects for Memorial Day trips in New England. Travel by automobile is projected to rise just 0.1 percent, compared to last year, while air travel is expected to fall 8.1 percent. The forecast indicates that 10.7 percent of the New England population will travel this upcoming Memorial Day holiday period, which is lower than the expected national frequency (11 percent). A slightly higher percentage of the regional population will travel by air than the broader nation (0.8 percent compared to 0.7 percent).

TABLE 5A 2013 MEMORIAL DAY TRAVEL FORECAST NEW ENGLAND REGION AND UNITED STATES

The New England economy continued to recover at a slow pace in 2012, with limited progress in the regional labor market. Although the market reported a mix of gains and losses across all sectors, the healthcare and professional, scientific, and technical services sectors were the strongest performers, which is good news for the region given the high growth potential of these sectors. The regional unemployment rate has been on a steady decline since reaching its peak in 2010, and is expected to fall to 6.9 percent in the second quarter of 2013, third-lowest among the nine census regions. While this is normally an encouraging sign, the drop in national unemployment from the most recent household survey resulted from fewer people in the labor force rather than more people working. The labor force participation rate or the ratio between the labor force and the overall size of the working-age population is now at a 30-year low. Demographics are partially pushing the participation rate lower, but the absence of a cyclical revival to draw potential workers back into the labor force is a sign of continued weakness in the labor market.

The New England housing market remains depressed, but recent indicators have shown clear signs of improvement. Indeed, regional housing starts increased 28.4 percent in the first quarter of 2013, relative to

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -0.7% 1.56 10.7% -0.9% 34.82 11.0%Automobile (millions of person trips) 0.1% 1.42 9.7% 0.2% 31.15 9.8%Air (millions of person trips) -8.1% 0.12 0.8% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.3% 6.9% -0.4% 7.7%Real Gross Product ($, bn)* 1.5% 740 1.9% 13,807Median Price, New Single Family Home ($, thn) 0.1% 391 1.1% 239

New England United States

-‐0.3%

1.5%

0.1%

0.6%

-‐0.4%

1.9%

1.1% 1.2%

-‐1%

-‐1%

0%

1%

1%

2%

2%

3%

Unemployment Rate

Real Gross State Product

Median Price New Single Family Home

Real Disposable Personal Income

Chart 5AYOY Growth, 2012Q2 to 2013Q2New England and United States

NENG Total US

Source: IHS Global Insight

17 IHS / AAA 2013 Memorial Day Forecast

last year, and are expected to grow 4.4 percent in the second quarter. The prolonged duration of the current recovery has enabled a gradual release in the pent-up demand for household formation. At the same time, depressed construction levels have ensured that the supply of vacant homes could be pared down, despite poor housing market conditions. Housing prices have also shown signs of stabilizing, but high foreclosure rates and slowing regional population growth remain a threat to future price increases. In the New England region, the median price of new single-family homes is expected to inch upwards by 0.1 percent in the second quarter, relative to year-ago prices.

Households still face too many negatives to allow a robust consumer spending recovery, one of which is the expiry of the payroll tax cut. IHS expects about a 1 percent loss of disposable income due to the ending of the payroll tax provision. As such, real disposable personal incomes are expected to rise just 0.6 percent in the second quarter compared to one year ago (versus 1.2 percent nationally). Gasoline prices have been slowly retreating since February, but high debt burdens,

modest employment growth, and a lack of

make things better are likely to hasten any spending increases on discretionary items such as travel.

In addition to the originating travel forecast of person-trips from the New England region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

The New England tourism industry has experienced sluggish growth over the past year and trails considerably behind the

national tourism industry. Leisure and hospitality industry output (the value of goods and services produced by the leisure and hospitality industry) in New England contracted 0.7 percent in the first quarter of 2013 and is expected to show meager growth of just 0.3 percent in the second quarter.

Massachusetts remains the largest contributor of tourism output to the New England economy, accounting for 51.9 percent of regional tourism output. Connecticut is the second largest contributor (19.9 percent) followed by New Hampshire (8.3 percent), Maine (8.0 percent), Rhode Island (6.9 percent), and Vermont (4.9 percent).

CT, 19.9%

MA, 51.9%

ME, 8.0%

NH, 8.3%

RI, 6.9%VT, 4.9%

CHART 5CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

NEW ENGLAND REGION MAKEUP BY STATE, 2013Q2

Source: IHS Global Insight

-1%

0%

1%

2%

3%

4%

5%

6%

7%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 5BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

NENG Total USSource: IHS Global Insight

18 IHS / AAA 2013 Memorial Day Forecast

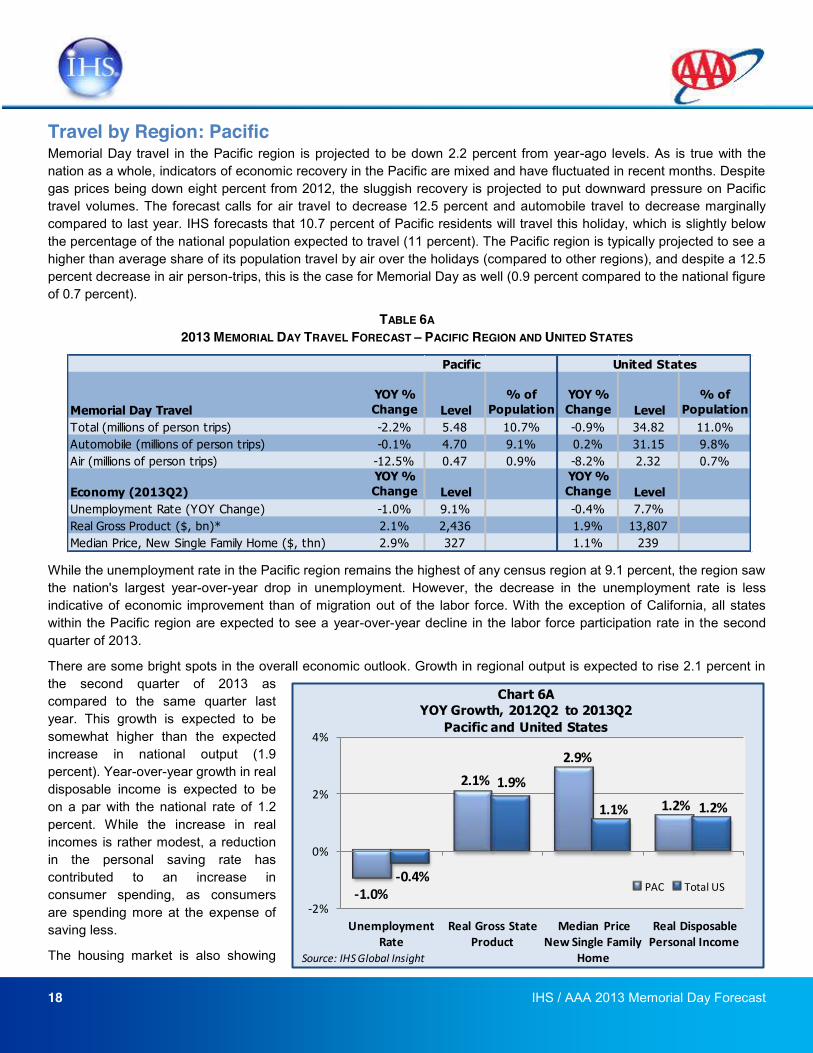

Travel by Region: Pacific Memorial Day travel in the Pacific region is projected to be down 2.2 percent from year-ago levels. As is true with the nation as a whole, indicators of economic recovery in the Pacific are mixed and have fluctuated in recent months. Despite gas prices being down eight percent from 2012, the sluggish recovery is projected to put downward pressure on Pacific travel volumes. The forecast calls for air travel to decrease 12.5 percent and automobile travel to decrease marginally compared to last year. IHS forecasts that 10.7 percent of Pacific residents will travel this holiday, which is slightly below the percentage of the national population expected to travel (11 percent). The Pacific region is typically projected to see a higher than average share of its population travel by air over the holidays (compared to other regions), and despite a 12.5 percent decrease in air person-trips, this is the case for Memorial Day as well (0.9 percent compared to the national figure of 0.7 percent).

TABLE 6A 2013 MEMORIAL DAY TRAVEL FORECAST PACIFIC REGION AND UNITED STATES

While the unemployment rate in the Pacific region remains the highest of any census region at 9.1 percent, the region saw the nation's largest year-over-year drop in unemployment. However, the decrease in the unemployment rate is less indicative of economic improvement than of migration out of the labor force. With the exception of California, all states within the Pacific region are expected to see a year-over-year decline in the labor force participation rate in the second quarter of 2013.

There are some bright spots in the overall economic outlook. Growth in regional output is expected to rise 2.1 percent in the second quarter of 2013 as compared to the same quarter last year. This growth is expected to be somewhat higher than the expected increase in national output (1.9 percent). Year-over-year growth in real disposable income is expected to be on a par with the national rate of 1.2 percent. While the increase in real incomes is rather modest, a reduction in the personal saving rate has contributed to an increase in consumer spending, as consumers are spending more at the expense of saving less.

The housing market is also showing

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -2.2% 5.48 10.7% -0.9% 34.82 11.0%Automobile (millions of person trips) -0.1% 4.70 9.1% 0.2% 31.15 9.8%Air (millions of person trips) -12.5% 0.47 0.9% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -1.0% 9.1% -0.4% 7.7%Real Gross Product ($, bn)* 2.1% 2,436 1.9% 13,807Median Price, New Single Family Home ($, thn) 2.9% 327 1.1% 239

Pacific United States

-‐1.0%

2.1%2.9%

1.2%

-‐0.4%

1.9%

1.1% 1.2%

-‐2%

0%

2%

4%

Unemployment Rate

Real Gross State Product

Median Price New Single Family

Home

Real Disposable Personal Income

Chart 6AYOY Growth, 2012Q2 to 2013Q2Pacific and United States

PAC Total US

Source: IHS Global Insight

19 IHS / AAA 2013 Memorial Day Forecast

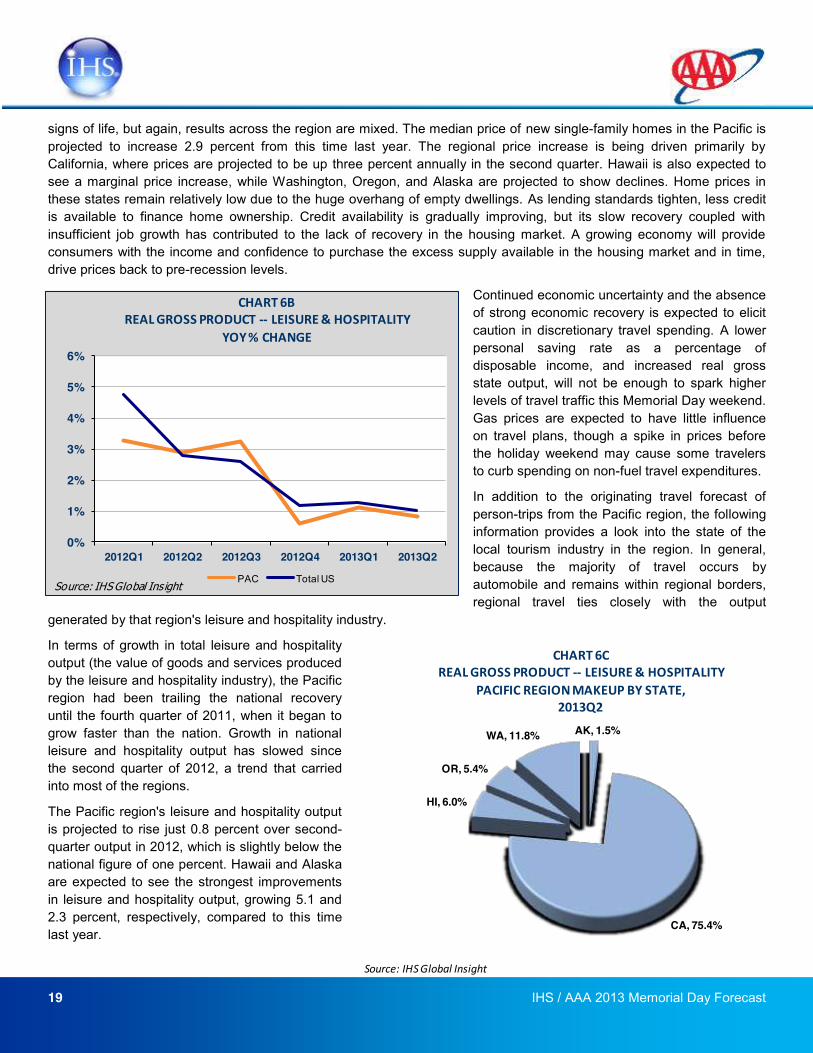

signs of life, but again, results across the region are mixed. The median price of new single-family homes in the Pacific is projected to increase 2.9 percent from this time last year. The regional price increase is being driven primarily by California, where prices are projected to be up three percent annually in the second quarter. Hawaii is also expected to see a marginal price increase, while Washington, Oregon, and Alaska are projected to show declines. Home prices in these states remain relatively low due to the huge overhang of empty dwellings. As lending standards tighten, less credit is available to finance home ownership. Credit availability is gradually improving, but its slow recovery coupled with insufficient job growth has contributed to the lack of recovery in the housing market. A growing economy will provide consumers with the income and confidence to purchase the excess supply available in the housing market and in time, drive prices back to pre-recession levels.

Continued economic uncertainty and the absence of strong economic recovery is expected to elicit caution in discretionary travel spending. A lower personal saving rate as a percentage of disposable income, and increased real gross state output, will not be enough to spark higher levels of travel traffic this Memorial Day weekend. Gas prices are expected to have little influence on travel plans, though a spike in prices before the holiday weekend may cause some travelers to curb spending on non-fuel travel expenditures.

In addition to the originating travel forecast of person-trips from the Pacific region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output

generated by that region's leisure and hospitality industry.

In terms of growth in total leisure and hospitality output (the value of goods and services produced by the leisure and hospitality industry), the Pacific region had been trailing the national recovery until the fourth quarter of 2011, when it began to grow faster than the nation. Growth in national leisure and hospitality output has slowed since the second quarter of 2012, a trend that carried into most of the regions.

The Pacific region's leisure and hospitality output is projected to rise just 0.8 percent over second-quarter output in 2012, which is slightly below the national figure of one percent. Hawaii and Alaska are expected to see the strongest improvements in leisure and hospitality output, growing 5.1 and 2.3 percent, respectively, compared to this time last year.

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 6BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

PAC Total USSource: IHS Global Insight

AK, 1.5%

CA, 75.4%

HI, 6.0%

OR, 5.4%

WA, 11.8%

CHART 6CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

PACIFIC REGION MAKEUP BY STATE, 2013Q2

Source: IHS Global Insight

20 IHS / AAA 2013 Memorial Day Forecast

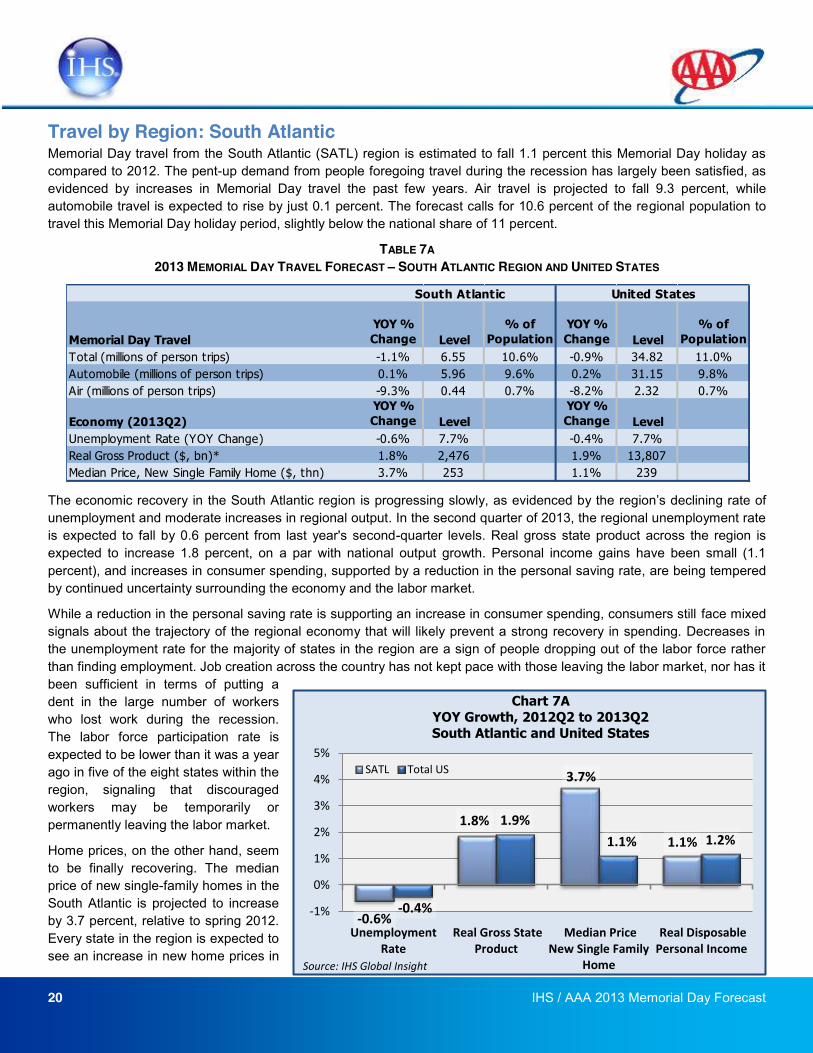

Travel by Region: South Atlantic Memorial Day travel from the South Atlantic (SATL) region is estimated to fall 1.1 percent this Memorial Day holiday as compared to 2012. The pent-up demand from people foregoing travel during the recession has largely been satisfied, as evidenced by increases in Memorial Day travel the past few years. Air travel is projected to fall 9.3 percent, while automobile travel is expected to rise by just 0.1 percent. The forecast calls for 10.6 percent of the regional population to travel this Memorial Day holiday period, slightly below the national share of 11 percent.

TABLE 7A 2013 MEMORIAL DAY TRAVEL FORECAST SOUTH ATLANTIC REGION AND UNITED STATES

The economic recovery in the South Atlantic region is progressing slowly, as evidenced by the declining rate of unemployment and moderate increases in regional output. In the second quarter of 2013, the regional unemployment rate is expected to fall by 0.6 percent from last year's second-quarter levels. Real gross state product across the region is expected to increase 1.8 percent, on a par with national output growth. Personal income gains have been small (1.1 percent), and increases in consumer spending, supported by a reduction in the personal saving rate, are being tempered by continued uncertainty surrounding the economy and the labor market.

While a reduction in the personal saving rate is supporting an increase in consumer spending, consumers still face mixed signals about the trajectory of the regional economy that will likely prevent a strong recovery in spending. Decreases in the unemployment rate for the majority of states in the region are a sign of people dropping out of the labor force rather than finding employment. Job creation across the country has not kept pace with those leaving the labor market, nor has it been sufficient in terms of putting a dent in the large number of workers who lost work during the recession. The labor force participation rate is expected to be lower than it was a year ago in five of the eight states within the region, signaling that discouraged workers may be temporarily or permanently leaving the labor market.

Home prices, on the other hand, seem to be finally recovering. The median price of new single-family homes in the South Atlantic is projected to increase by 3.7 percent, relative to spring 2012. Every state in the region is expected to see an increase in new home prices in

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -1.1% 6.55 10.6% -0.9% 34.82 11.0%Automobile (millions of person trips) 0.1% 5.96 9.6% 0.2% 31.15 9.8%Air (millions of person trips) -9.3% 0.44 0.7% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.6% 7.7% -0.4% 7.7%Real Gross Product ($, bn)* 1.8% 2,476 1.9% 13,807Median Price, New Single Family Home ($, thn) 3.7% 253 1.1% 239

South Atlantic United States

-‐0.6%

1.8%

3.7%

1.1%

-‐0.4%

1.9% 1.1% 1.2%

-‐1%

0%

1%

2%

3%

4%

5%

UnemploymentRate

Real Gross StateProduct

Median PriceNew Single Family

Home

Real DisposablePersonal Income

Chart 7A YOY Growth, 2012Q2 to 2013Q2 South Atlantic and United States

SATL Total US

Source: IHS Global Insight

21 IHS / AAA 2013 Memorial Day Forecast

the second quarter. Sales of existing homes, another indicator of the health of the housing market, are also projected to be higher than they were in the second quarter of 2012 in all nine South Atlantic states. Improving personal credit conditions are revitalizing the housing market by allowing more potential homebuyers to enter the market and reduce the quantity of excess empty homes.

Gas prices are expected to have a negligible impact on travel decisions this Memorial Day weekend. The average gasoline price is down more than eight percent from the second quarter of 2012. An increase in the gas price prior to the Memorial Day holiday is unlikely to influence the decision of whether or not to travel, but it may convince some travelers to

reallocate travel budgets to account for higher fuel costs by spending less in other areas.

In addition to the originating travel forecast of person-trips from the South Atlantic region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

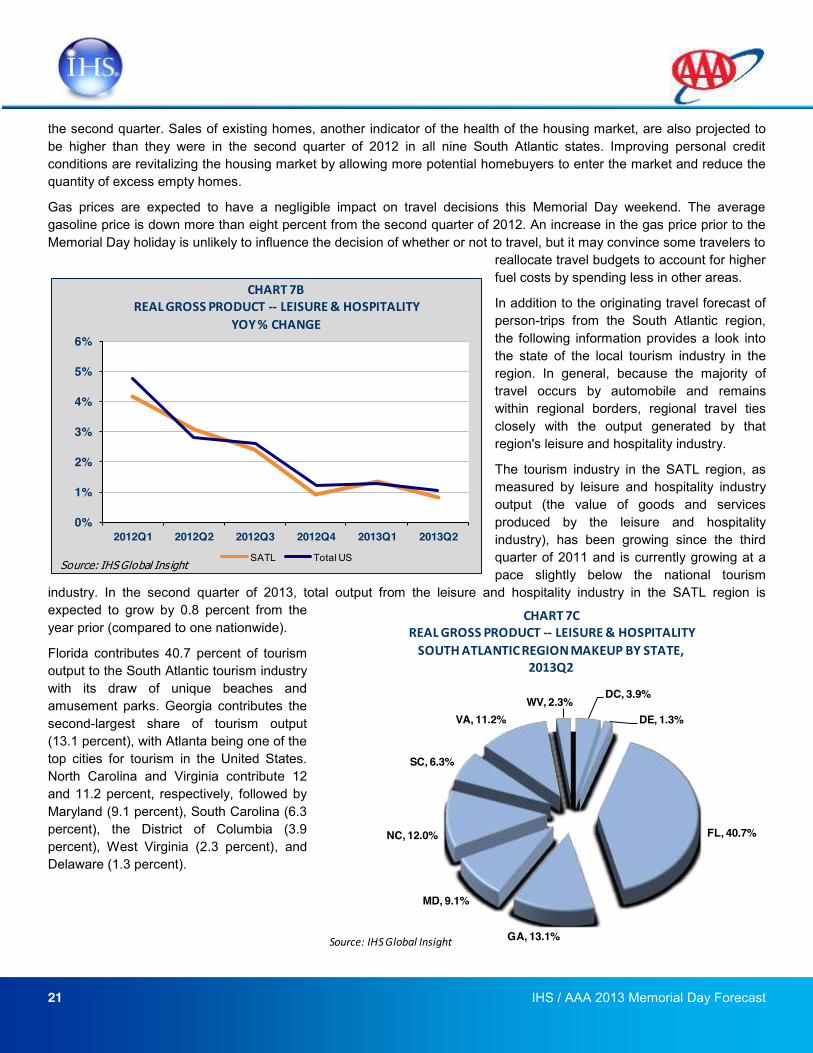

The tourism industry in the SATL region, as measured by leisure and hospitality industry output (the value of goods and services produced by the leisure and hospitality industry), has been growing since the third quarter of 2011 and is currently growing at a pace slightly below the national tourism

industry. In the second quarter of 2013, total output from the leisure and hospitality industry in the SATL region is expected to grow by 0.8 percent from the year prior (compared to one nationwide).

Florida contributes 40.7 percent of tourism output to the South Atlantic tourism industry with its draw of unique beaches and amusement parks. Georgia contributes the second-largest share of tourism output (13.1 percent), with Atlanta being one of the top cities for tourism in the United States. North Carolina and Virginia contribute 12 and 11.2 percent, respectively, followed by Maryland (9.1 percent), South Carolina (6.3 percent), the District of Columbia (3.9 percent), West Virginia (2.3 percent), and Delaware (1.3 percent).

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 7BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

SATL Total USSource: IHS Global Insight

DC, 3.9%

DE, 1.3%

FL, 40.7%

GA, 13.1%

MD, 9.1%

NC, 12.0%

SC, 6.3%

VA, 11.2%WV, 2.3%

CHART 7CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITYSOUTH ATLANTIC REGION MAKEUP BY STATE,

2013Q2

Source: IHS Global Insight

22 IHS / AAA 2013 Memorial Day Forecast

Travel by Region: West North Central

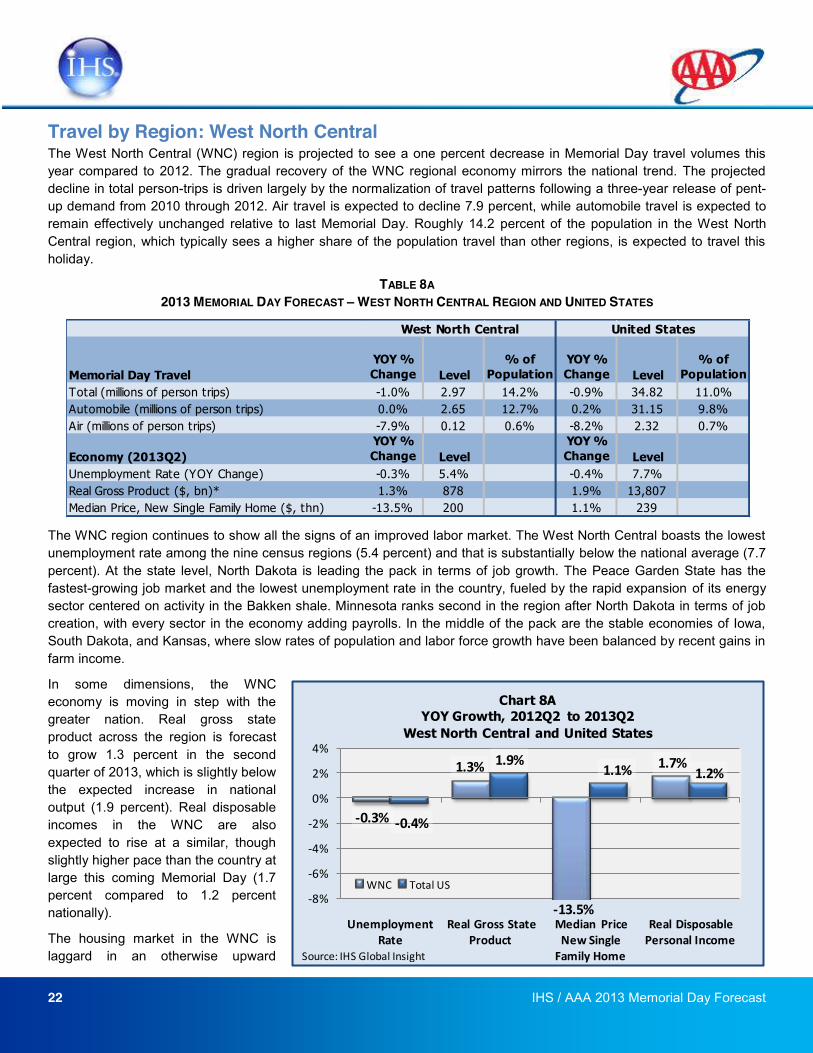

The West North Central (WNC) region is projected to see a one percent decrease in Memorial Day travel volumes this year compared to 2012. The gradual recovery of the WNC regional economy mirrors the national trend. The projected decline in total person-trips is driven largely by the normalization of travel patterns following a three-year release of pent-up demand from 2010 through 2012. Air travel is expected to decline 7.9 percent, while automobile travel is expected to remain effectively unchanged relative to last Memorial Day. Roughly 14.2 percent of the population in the West North Central region, which typically sees a higher share of the population travel than other regions, is expected to travel this holiday.

TABLE 8A 2013 MEMORIAL DAY FORECAST WEST NORTH CENTRAL REGION AND UNITED STATES

The WNC region continues to show all the signs of an improved labor market. The West North Central boasts the lowest unemployment rate among the nine census regions (5.4 percent) and that is substantially below the national average (7.7 percent). At the state level, North Dakota is leading the pack in terms of job growth. The Peace Garden State has the fastest-growing job market and the lowest unemployment rate in the country, fueled by the rapid expansion of its energy sector centered on activity in the Bakken shale. Minnesota ranks second in the region after North Dakota in terms of job creation, with every sector in the economy adding payrolls. In the middle of the pack are the stable economies of Iowa, South Dakota, and Kansas, where slow rates of population and labor force growth have been balanced by recent gains in farm income.

In some dimensions, the WNC economy is moving in step with the greater nation. Real gross state product across the region is forecast to grow 1.3 percent in the second quarter of 2013, which is slightly below the expected increase in national output (1.9 percent). Real disposable incomes in the WNC are also expected to rise at a similar, though slightly higher pace than the country at large this coming Memorial Day (1.7 percent compared to 1.2 percent nationally).

The housing market in the WNC is laggard in an otherwise upward

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) -1.0% 2.97 14.2% -0.9% 34.82 11.0%Automobile (millions of person trips) 0.0% 2.65 12.7% 0.2% 31.15 9.8%Air (millions of person trips) -7.9% 0.12 0.6% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.3% 5.4% -0.4% 7.7%Real Gross Product ($, bn)* 1.3% 878 1.9% 13,807Median Price, New Single Family Home ($, thn) -13.5% 200 1.1% 239

West North Central United States

-‐0.3%

1.3% 1.7%

-‐0.4%

1.9%1.1% 1.2%

-‐8%

-‐6%

-‐4%

-‐2%

0%

2%

4%

Unemployment Rate

Real Gross State Product

Median Price New Single Family Home

Real Disposable Personal Income

Chart 8AYOY Growth, 2012Q2 to 2013Q2

West North Central and United States

WNC Total US

Source: IHS Global Insight

-‐13.5%

23 IHS / AAA 2013 Memorial Day Forecast

trending regional economy. Unable to sustain the spike in home prices from this time last year, the median price of new single-family homes is forecast to decrease 13.5 percent in the second quarter of 2013, compared to year-ago levels. The price depreciation in the WNC region diverges from the upward trend seen in the national housing market, in which home prices are projected to grow 1.1 percent. The states in the WNC region saw home prices increase through the third quarter of 2012, but the market has since taken a downward turn. In South Dakota, median home prices are projected to be 17 percent lower in the second quarter of 2013 than they were one year ago.

Fuel prices in the region are higher than in January of this year but lower than they were in the second quarter of 2012. The decision to travel is unlikely to be influenced significantly by gas prices this year, but a price spike before the holiday weekend may encourage travelers to reallocate expenses to accommodate for an increase in fuel costs.

In addition to the originating travel forecast of person-trips from the West North Central region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

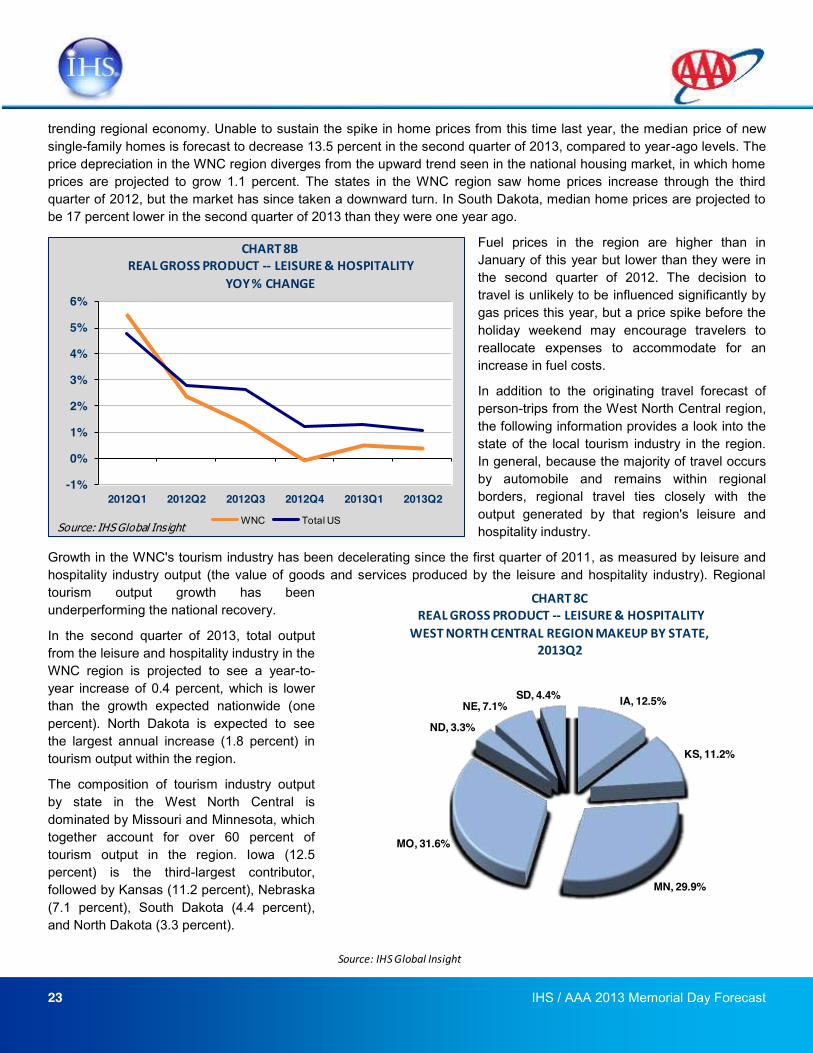

Growth in the WNC's tourism industry has been decelerating since the first quarter of 2011, as measured by leisure and hospitality industry output (the value of goods and services produced by the leisure and hospitality industry). Regional tourism output growth has been underperforming the national recovery.

In the second quarter of 2013, total output from the leisure and hospitality industry in the WNC region is projected to see a year-to-year increase of 0.4 percent, which is lower than the growth expected nationwide (one percent). North Dakota is expected to see the largest annual increase (1.8 percent) in tourism output within the region.

The composition of tourism industry output by state in the West North Central is dominated by Missouri and Minnesota, which together account for over 60 percent of tourism output in the region. Iowa (12.5 percent) is the third-largest contributor, followed by Kansas (11.2 percent), Nebraska (7.1 percent), South Dakota (4.4 percent), and North Dakota (3.3 percent).

-1%

0%

1%

2%

3%

4%

5%

6%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 8BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

WNC Total USSource: IHS Global Insight

IA, 12.5%

KS, 11.2%

MN, 29.9%

MO, 31.6%

ND, 3.3%

NE, 7.1%SD, 4.4%

CHART 8CREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

WEST NORTH CENTRAL REGION MAKEUP BY STATE, 2013Q2

Source: IHS Global Insight

24 IHS / AAA 2013 Memorial Day Forecast

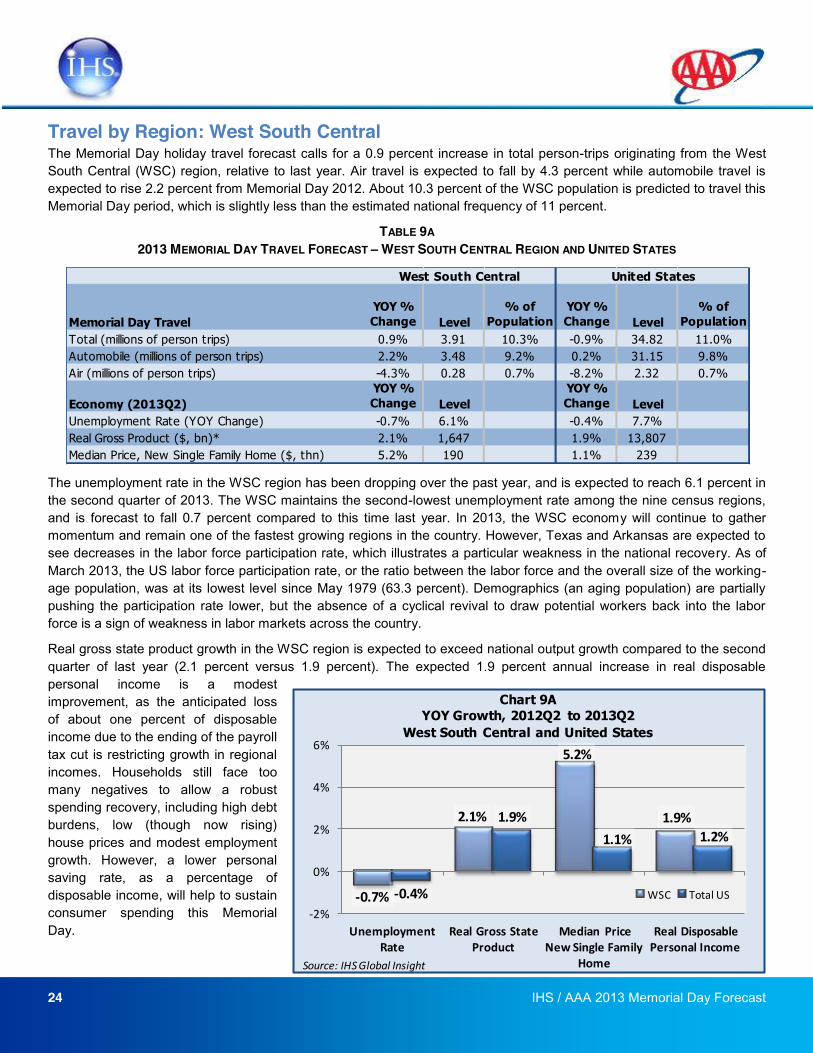

Travel by Region: West South Central The Memorial Day holiday travel forecast calls for a 0.9 percent increase in total person-trips originating from the West South Central (WSC) region, relative to last year. Air travel is expected to fall by 4.3 percent while automobile travel is expected to rise 2.2 percent from Memorial Day 2012. About 10.3 percent of the WSC population is predicted to travel this Memorial Day period, which is slightly less than the estimated national frequency of 11 percent.

TABLE 9A 2013 MEMORIAL DAY TRAVEL FORECAST WEST SOUTH CENTRAL REGION AND UNITED STATES

The unemployment rate in the WSC region has been dropping over the past year, and is expected to reach 6.1 percent in the second quarter of 2013. The WSC maintains the second-lowest unemployment rate among the nine census regions, and is forecast to fall 0.7 percent compared to this time last year. In 2013, the WSC economy will continue to gather momentum and remain one of the fastest growing regions in the country. However, Texas and Arkansas are expected to see decreases in the labor force participation rate, which illustrates a particular weakness in the national recovery. As of March 2013, the US labor force participation rate, or the ratio between the labor force and the overall size of the working-age population, was at its lowest level since May 1979 (63.3 percent). Demographics (an aging population) are partially pushing the participation rate lower, but the absence of a cyclical revival to draw potential workers back into the labor force is a sign of weakness in labor markets across the country.

Real gross state product growth in the WSC region is expected to exceed national output growth compared to the second quarter of last year (2.1 percent versus 1.9 percent). The expected 1.9 percent annual increase in real disposable personal income is a modest improvement, as the anticipated loss of about one percent of disposable income due to the ending of the payroll tax cut is restricting growth in regional incomes. Households still face too many negatives to allow a robust spending recovery, including high debt burdens, low (though now rising) house prices and modest employment growth. However, a lower personal saving rate, as a percentage of disposable income, will help to sustain consumer spending this Memorial Day.

Memorial Day TravelYOY % Change Level

% of Population

YOY % Change Level

% of Population

Total (millions of person trips) 0.9% 3.91 10.3% -0.9% 34.82 11.0%Automobile (millions of person trips) 2.2% 3.48 9.2% 0.2% 31.15 9.8%Air (millions of person trips) -4.3% 0.28 0.7% -8.2% 2.32 0.7%

Economy (2013Q2)YOY % Change Level

YOY % Change Level

Unemployment Rate (YOY Change) -0.7% 6.1% -0.4% 7.7%Real Gross Product ($, bn)* 2.1% 1,647 1.9% 13,807Median Price, New Single Family Home ($, thn) 5.2% 190 1.1% 239

West South Central United States

-‐0.7%

2.1%

5.2%

1.9%

-‐0.4%

1.9%1.1% 1.2%

-‐2%

0%

2%

4%

6%

Unemployment Rate

Real Gross State Product

Median Price New Single Family

Home

Real Disposable Personal Income

Chart 9AYOY Growth, 2012Q2 to 2013Q2

West South Central and United States

WSC Total US

Source: IHS Global Insight

25 IHS / AAA 2013 Memorial Day Forecast

The WSC housing market is beginning to turn around, as the median price of new single-family homes is projected to rise 5.2 percent from the second quarter of 2012. Of the four contributing states, Oklahoma is expected to see the largest increase in second-quarter prices (six percent), followed by Louisiana (5.8 percent), Texas (5.3 percent), and Arkansas (1.4 percent). Housing starts and sales of existing homes are also above year-ago levels in each of the WSC states. Homebuilders continue to break ground on more homes as household formation rates begin to pick up, while some of the excess existing supply is being gobbled up by investors and conventional homebuyers. Low interest rates will keep housing very affordable by historical standards, which should continue to boost home sales and new construction.

The price of gasoline is expected to have little effect on holiday travel from the WSC region this Memorial Day. April gas prices are down from a year ago. Any price increase that comes shortly before the holiday is unlikely to impact travel decisions, though it may compel travelers to reallocate their travel budgets to account for higher fuel prices.

In addition to the originating travel forecast of person-trips from the West South Central region, the following information provides a look into the state of the local tourism industry in the region. In general, because the majority of travel occurs by automobile and remains within regional borders, regional travel ties closely with the output generated by that region's leisure and hospitality industry.

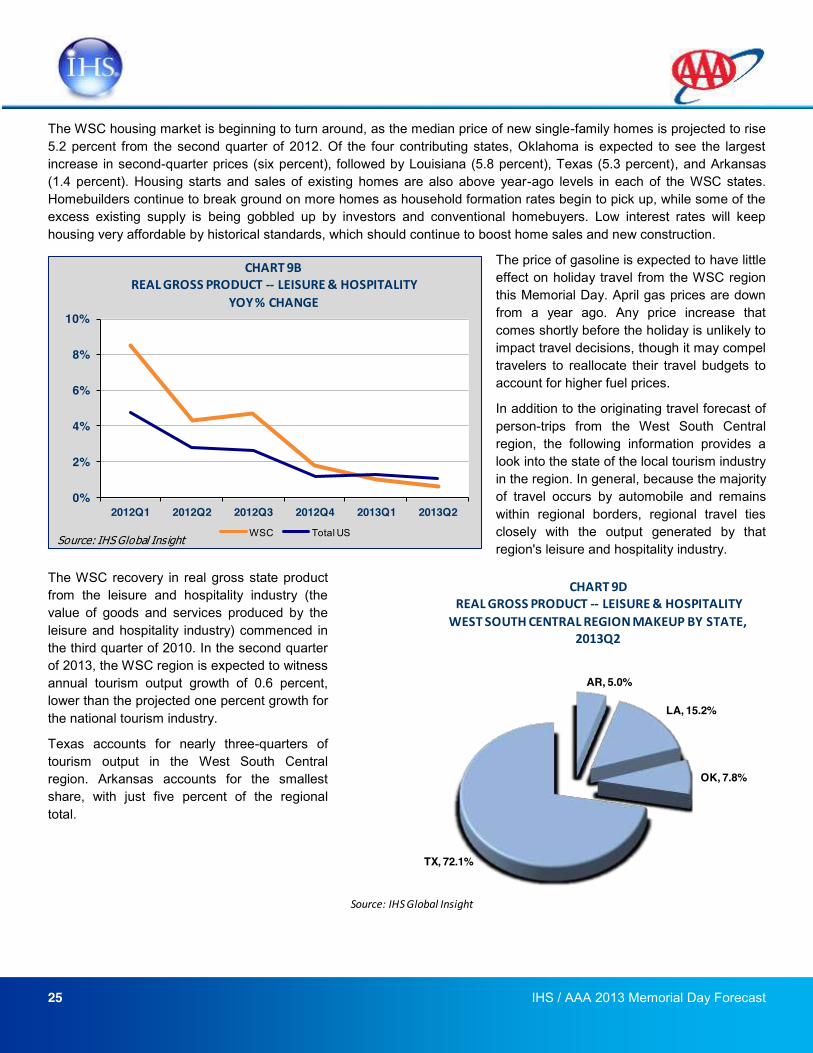

The WSC recovery in real gross state product from the leisure and hospitality industry (the value of goods and services produced by the leisure and hospitality industry) commenced in the third quarter of 2010. In the second quarter of 2013, the WSC region is expected to witness annual tourism output growth of 0.6 percent, lower than the projected one percent growth for the national tourism industry.

Texas accounts for nearly three-quarters of tourism output in the West South Central region. Arkansas accounts for the smallest share, with just five percent of the regional total.

0%

2%

4%

6%

8%

10%

2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

CHART 9BREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITY

YOY % CHANGE

WSC Total USSource: IHS Global Insight

AR, 5.0%

LA, 15.2%

OK, 7.8%

TX, 72.1%

CHART 9DREAL GROSS PRODUCT -‐-‐ LEISURE & HOSPITALITYWEST SOUTH CENTRAL REGION MAKEUP BY STATE,

2013Q2

Source: IHS Global Insight

26 IHS / AAA 2013 Memorial Day Forecast

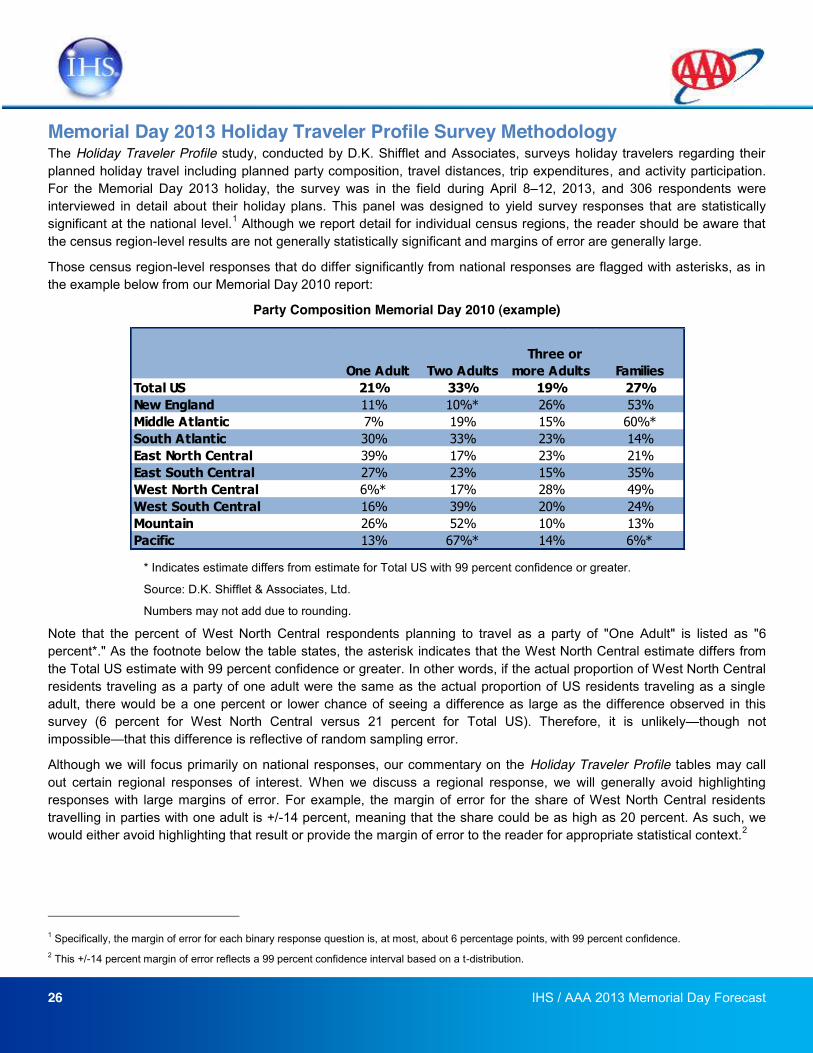

Memorial Day 2013 Holiday Traveler Profile Survey Methodology The Holiday Traveler Profile study, conducted by D.K. Shifflet and Associates, surveys holiday travelers regarding their planned holiday travel including planned party composition, travel distances, trip expenditures, and activity participation. For the Memorial Day 2013 holiday, the survey was in the field during April 8 12, 2013, and 306 respondents were interviewed in detail about their holiday plans. This panel was designed to yield survey responses that are statistically significant at the national level.1 Although we report detail for individual census regions, the reader should be aware that the census region-level results are not generally statistically significant and margins of error are generally large.

Those census region-level responses that do differ significantly from national responses are flagged with asterisks, as in the example below from our Memorial Day 2010 report:

Party Composition Memorial Day 2010 (example)

* Indicates estimate differs from estimate for Total US with 99 percent confidence or greater.

Source: D.K. Shifflet & Associates, Ltd.

Numbers may not add due to rounding.

Note that the percent of West North Central respondents planning to travel as a party of "One Adult" is listed as "6 percent*." As the footnote below the table states, the asterisk indicates that the West North Central estimate differs from the Total US estimate with 99 percent confidence or greater. In other words, if the actual proportion of West North Central residents traveling as a party of one adult were the same as the actual proportion of US residents traveling as a single adult, there would be a one percent or lower chance of seeing a difference as large as the difference observed in this survey (6 percent for West North Central versus 21 percent for Total US). Therefore, it is unlikely though not impossible that this difference is reflective of random sampling error.

Although we will focus primarily on national responses, our commentary on the Holiday Traveler Profile tables may call out certain regional responses of interest. When we discuss a regional response, we will generally avoid highlighting responses with large margins of error. For example, the margin of error for the share of West North Central residents travelling in parties with one adult is +/-14 percent, meaning that the share could be as high as 20 percent. As such, we would either avoid highlighting that result or provide the margin of error to the reader for appropriate statistical context.2

1 Specifically, the margin of error for each binary response question is, at most, about 6 percentage points, with 99 percent confidence. 2 This +/-14 percent margin of error reflects a 99 percent confidence interval based on a t-distribution.

One Adult Two Adults Three or more Adults Families

Total US 21% 33% 19% 27%New England 11% 10%* 26% 53%Middle Atlantic 7% 19% 15% 60%*South Atlantic 30% 33% 23% 14%East North Central 39% 17% 23% 21%East South Central 27% 23% 15% 35%West North Central 6%* 17% 28% 49%West South Central 16% 39% 20% 24%Mountain 26% 52% 10% 13%Pacific 13% 67%* 14% 6%*

27 IHS / AAA 2013 Memorial Day Forecast

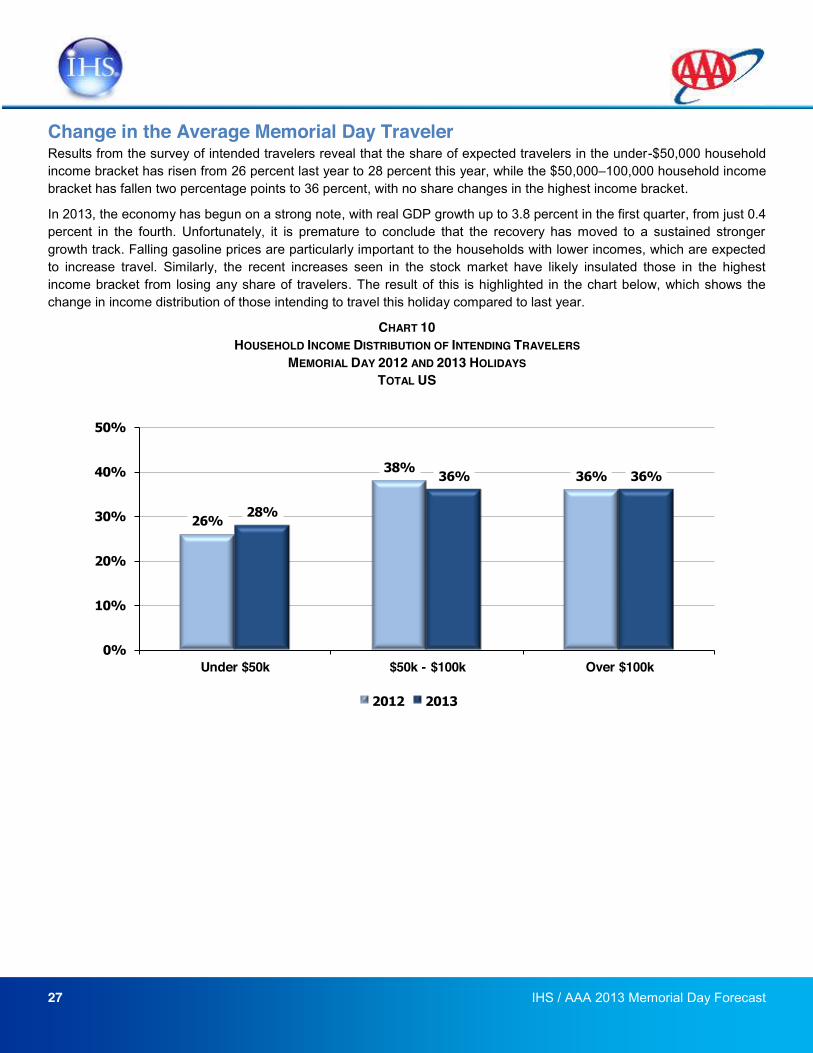

Change in the Average Memorial Day Traveler Results from the survey of intended travelers reveal that the share of expected travelers in the under-$50,000 household income bracket has risen from 26 percent last year to 28 percent this year, while the $50,000 100,000 household income bracket has fallen two percentage points to 36 percent, with no share changes in the highest income bracket.

In 2013, the economy has begun on a strong note, with real GDP growth up to 3.8 percent in the first quarter, from just 0.4 percent in the fourth. Unfortunately, it is premature to conclude that the recovery has moved to a sustained stronger growth track. Falling gasoline prices are particularly important to the households with lower incomes, which are expected to increase travel. Similarly, the recent increases seen in the stock market have likely insulated those in the highest income bracket from losing any share of travelers. The result of this is highlighted in the chart below, which shows the change in income distribution of those intending to travel this holiday compared to last year.

CHART 10 HOUSEHOLD INCOME DISTRIBUTION OF INTENDING TRAVELERS

MEMORIAL DAY 2012 AND 2013 HOLIDAYS TOTAL US

26%

38%36%

28%

36% 36%

0%

10%

20%

30%

40%

50%

Under $50k $50k - $100k Over $100k

2012 2013

28 IHS / AAA 2013 Memorial Day Forecast

Going on a longer trip to visit family/friends at the

Grand Canyon." ENC Respondent

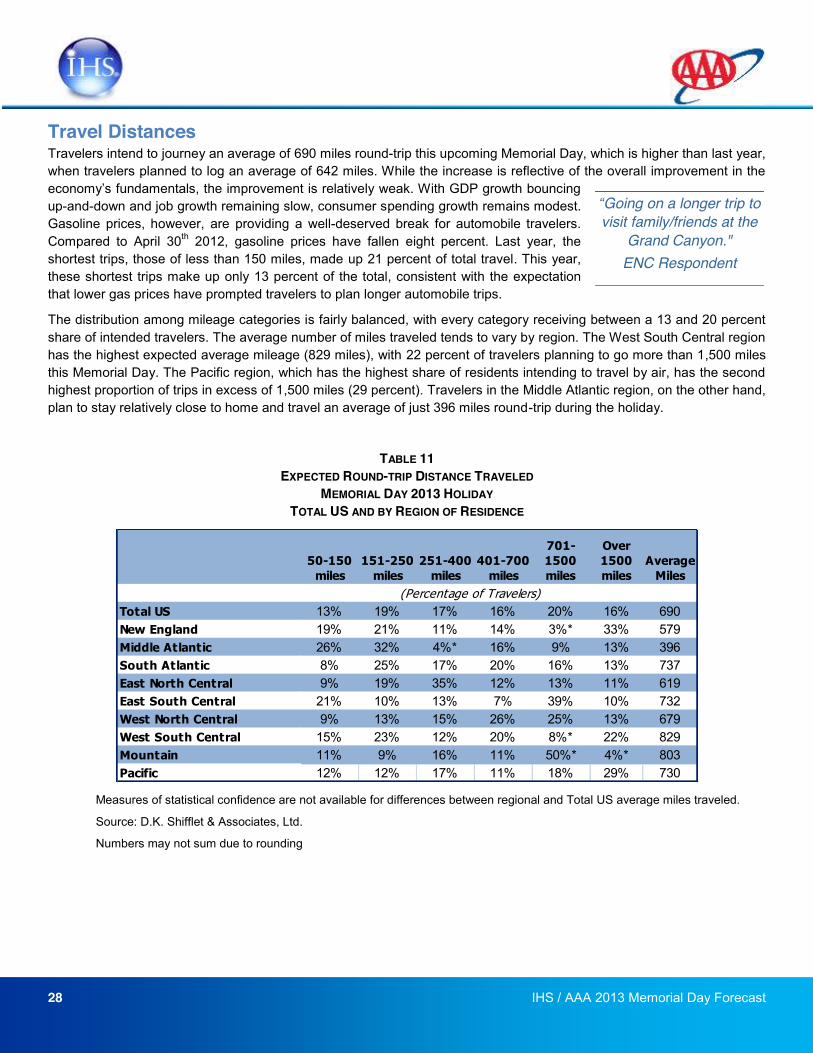

Travel Distances Travelers intend to journey an average of 690 miles round-trip this upcoming Memorial Day, which is higher than last year, when travelers planned to log an average of 642 miles. While the increase is reflective of the overall improvement in the

up-and-down and job growth remaining slow, consumer spending growth remains modest. Gasoline prices, however, are providing a well-deserved break for automobile travelers. Compared to April 30th 2012, gasoline prices have fallen eight percent. Last year, the shortest trips, those of less than 150 miles, made up 21 percent of total travel. This year, these shortest trips make up only 13 percent of the total, consistent with the expectation that lower gas prices have prompted travelers to plan longer automobile trips.

The distribution among mileage categories is fairly balanced, with every category receiving between a 13 and 20 percent share of intended travelers. The average number of miles traveled tends to vary by region. The West South Central region has the highest expected average mileage (829 miles), with 22 percent of travelers planning to go more than 1,500 miles this Memorial Day. The Pacific region, which has the highest share of residents intending to travel by air, has the second highest proportion of trips in excess of 1,500 miles (29 percent). Travelers in the Middle Atlantic region, on the other hand, plan to stay relatively close to home and travel an average of just 396 miles round-trip during the holiday.

TABLE 11 EXPECTED ROUND-TRIP DISTANCE TRAVELED

MEMORIAL DAY 2013 HOLIDAY TOTAL US AND BY REGION OF RESIDENCE

Measures of statistical confidence are not available for differences between regional and Total US average miles traveled.

Source: D.K. Shifflet & Associates, Ltd.

Numbers may not sum due to rounding

50-150 miles

151-250 miles

251-400 miles

401-700 miles

701-1500 miles

Over 1500 miles

Average Miles