[email protected] | www.gartlyadvisory.com.au | www.ggassociates.com.au Liability limited by a scheme approved under Professional Standards Legislation

The relief package of legislation consisted of several separate bills, which were all introduced to Parliament within a short period of time. The legislation has now passed both houses, with most applying from mid-March.

The government further announced at the end of March a further massive subsidy for businesses to help them retain employees so they are ready to get back to business when the current coronavirus issues subside. The new subsidy is called the JobKeeper payment.

The key points of the JobKeeper payment follow, with the relief package explained after that.

Covid-19: Your stimulus and rescue package explained

A legislative package has been pushed through Parliament which contains a number of bills that implement the government’s economic response to the spread of the coronavirus.

continued overleaf a

Liability limited by a scheme approved under professional standards legislation Your full financial needs and requirements need to be assessed prior to any offer or acceptance of a loan product. Credit Representative 490117 is authorised under Australian Credit Licence 389328.

Beyond Numbers monthly tax newsletterWelcome to our latest newsletter with our compliments. We hope you find the topics informative and assist you in understanding your tax obligations and changes world of tax. Any matter you find relates to your circumstance we welcome you to contact us to discuss further.T: 03 9597 9966 | E: [email protected]

1 The payment will be made to eligible employers for eligible employees. The payment will be $1,500 per fortnight per employee for a period of six months. It will be paid in respect of full time and part time employees who were employed as at 1 March 2020. Also, casual employees will be eligible if they have been with their employer on a regular basis for at least the pervious 12 months as at 1 March 2020.

2 The employees must continue to be engaged by the business. If an employee has been stood down or has had their employment terminated, they can still be eligible. If an employee’s employment has been terminated, the employee must be re-engaged by the business.

3 Not all employers are eligible for the payment. A business will be eligible:a. If the business has a turnover of less

than $1 billion and its turnover will be reduced by more than 30% relative to a comparable period a year ago, of at least one month; or

b. If the business has a turnover of $1 billion or more and its turnover will be reduced by more than 50% relative to a comparable period a year ago, of at least one month; and

c. If the business is not subject to the Major Bank Levy.

4 Employers must elect to receive the JobKeeper payment and provide supporting information. This can be done through the ATO website.

5 Employers must report the number of eligible employees employed by the business on a monthly basis.

6 Where an employee is accessing support through Services Australia because they have been stood down or had their hours reduced and the employer is eligible for the JobKeeper payment, the employee will need to advise Services Australia of their new income. An individual cannot receive both the JobKeeper and JobSeeker payments.

7 If an employee has more than one employer, only one JobKeeper payment will be made to one employer. The employer claiming the JobKeeper payment will usually be the one from whom the employee claims the tax-free threshold.

8 Superannuation Guarantee contributions (9.5%) need not be made on the JobKeeper payments. However, to the extent an employee is paid their normal salary or wages, the 9.5% contributions still need to be paid as normal.

9 If an employee ordinarily receives less than $1,500 in income per fortnight before tax, their employer must pay their employee, at a minimum, $1,500 per fortnight, before tax.

10 If an employee has been stood down, their employer must pay the employee, at a minimum, $1,500 per fortnight, before tax.

11 If an employee was employed on 1 March 2020, subsequently ceased employment with their employer, and then has been re-engaged by the same eligible employer, the employee will receive, at a minimum, $1,500 per fortnight.

12 With regard to the timing of payments, the payments will be made to an employer monthly in arrears by the ATO. The Prime Minister has pointed out that this should not delay employers from making payments to employees. This is because the employer can make payments to their employees in the knowledge that the employer will receive the JobKeeper payment. Of course, this assumes that the employer has the cashflow to make the payment in the first place!

13 The JobKeeper entitlement will start on 30 March 2020, with the first payments to be received by employers in the first week of May.

14 For most businesses, the ATO will use the Single Touch Payroll system data to pre-populate the employee details for the business.

15 Employers must notify all eligible employees that they are receiving the JobKeeper payment.

16 The JobKeeper payment will be available for not-for-profit organisations.

17 The JobKeeper payment will also be available for the self-employed where they expect to suffer a 30% decline in turnover relative to a comparable prior period. g

The income tax law was amended to increase the cost threshold below which certain business entities can access an immediate deduction for the full cost of depreciating assets from $30,000 to $150,000. This change to the rules is only available from 12 March 2020 to 30 June 2020. For an asset to be eligible for the instant asset write-off it must be first used for a taxable purpose in the period 12 March 2020 to 30 June 2020. Alternatively, the asset must be installed and ready for use in that period.

In the Federal Budget announced on 2 April 2019, the Federal Government extended the instant asset write-off to businesses that have a turnover of between $10 million and $50 million. This was in addition to small businesses that have a turnover of less than $10 million.

The instant asset write-off will now also apply to businesses with an aggregated turnover of less than $500 million. However, it will only apply to these businesses for the period 12 March 2020 to 30 June 2020.

This means that there will be two periods that you will need to consider in relation to purchases of assets in the year ending 30 June 2020. The first period is from 1 July 2019 to 11 March 2020. Eligible assets costing less than $30,000 can be written off completely in this period by businesses that have an aggregated turnover of less than $50 million. From 12 March 2020 to 30 June 2020, eligible assets costing less than $150,000 (GST exclusive), can be written off by businesses that have an aggregated turnover of less than $500 million.

It should be noted that from 1 July 2020, the instant asset write-off threshold will revert to its original level of $1,000 and will only be applicable for businesses with an aggregated turnover of less than $10 million. Accordingly, the coronavirus measures offer a strong incentive for most businesses to obtain a significant tax deduction that will no longer exist in the new financial year.

This provides an incentive for businesses with aggregated turnovers of less than $500 million a year to invest in plant and equipment and other depreciating assets.

Specifically, the bill amends the income tax law to temporarily allow businesses with aggregated turnovers of less than $500 million in an income year to deduct capital allowances for depreciating assets at an accelerated rate of 50% of the cost of an asset. This will be in addition to the normal depreciation that is claimed on the cost of the asset after deducting the 50% amount.

Generally, to be eligible to apply the accelerated rate of deduction, the depreciating asset must satisfy a number of conditions, including that the asset:■ is new and has not previously been held by another

entity (other than as trading stock or for testing and trialling purposes);

■ is an asset for which an entity has not claimed depreciation deductions, including under the instant asset write-off rules; and

■ is first held, and first used or installed ready for use, for a taxable purpose between 12 March 2020 and 30 June 2021 (inclusive).

BOOSTING CASH FLOW FOR EMPLOYERS

The cash flow boost provides for payments to support employers by boosting their cash flow. Another intention with this measure is to encourage the retention of employees through any follow-on downturn.

Undoubtedly, this part of the stimulus package is the most confusing. Unfortunately, it also has the potential to be rorted by unscrupulous people. That is why the measures contain an anti-avoidance provision.

Before explaining the detail, here are a number of statements about this part of the package that will assist with explaining certain aspects of what is known as the “cash flow boost”.

1. There are two rounds of cash flow boost.

2. The second cash flow boost is determined from the amount of the first cash flow boost.

3. The amount of the first cash flow boost is determined by the amount of withholdings from (broadly) wages or the minimum cash flow boost payment ($10,000), whichever is larger.

4. The maximum first cash flow boost amount is $50,000.

5. If eligible, the minimum “payment” to an entity will be $20,000 and the maximum will be $100,000 from the two cash flow boost payments.

6. The “payments” are actually credits given to the entity through the lodgement of activity statements. If credits exceed the amount owing, a refund will be paid by the ATO to the entity within 14 days of the due date for lodgement of the activity statement.

7. The payments will operate in a different manner for monthly and quarterly lodgers of activity statements. The examples below will explain this.

Entities with an aggregated turnover under $50 million are generally eligible to receive the first cash flow boost for a period if:■ the entity makes a payment that is subject to

withholding obligations (broadly, a payment of wages or salary or similar remuneration), whether or not any amount is actually withheld, in the period; and

■ the period is one of the following:● the quarters ending in March 2020 or June 2020

for quarterly payers; and● the months of March 2020, April 2020, May 2020

or June 2020 for monthly payers; and■ if the entity:

● held an ABN on 12 March 2020; and● either derived assessable income from carrying

on a business in the 2018-19 income year or made one or more supplies for consideration in the course of an enterprise it carried on within Australia in tax periods commencing after 1 July 2018 and ending before 12 March 2020 and notice of the income or supplies was held by the Commissioner on or before 12 March 2020 or within such further time as the Commissioner allows (this notice appears to be either activity statements or an income tax return); and

■ the entity (or an associate or agent of an entity) has not engaged in a scheme for the sole or dominant purpose of seeking to make the entity entitled to the first cash flow boost or increase the entitlement of the entity to the first cash flow boost.

There are some other conditions that we can help work through if you are an eligible business.

The timing of the cash flow boost needs to be noted as well. Quarterly lodgers will be eligible to receive the payment for the quarter ending March 2020 and June 2020. Monthly lodgers will be eligible to receive the payment for the March 2020, April 2020, May 2020 and June 2020 lodgements. To provide a similar treatment to quarterly lodgers, the payment for monthly lodgers will be calculated at three times the rate (300%) in the March 2020 activity statement.

The minimum payment [$10,000] will be applied to the entities’ first lodgement.

The additional payment [the second cash flow boost] will be applied to a limited number of activity statements. Where this places the entity in a refund position, the ATO will deliver the refund within 14 days.

Quarterly lodgers will be eligible to receive the additional payment for the quarters ending June 2020 and September 2020. Each additional payment will be equal to half of their total initial Boosting Cash Flow for Employers payment (up to a total of $50,000).

Monthly lodgers will be eligible to receive the additional payment for the June 2020, July 2020, August 2020 and September 2020 lodgements. Each additional payment will be equal to a quarter of their total initial Boosting Cash Flow for Employers payment (up to a total of $50,000).

THE ANTI-AVOIDANCE PROVISION

Be aware that the cash boost legislation contains an anti-avoidance provision. This states: “Neither the entity nor any associate or agent of the entity has entered into or carried out a scheme or part of a scheme for the sole or dominant purpose of achieving any of the following:

1. making the entity entitled to the cash flow boost for the period;

2. increasing the amount of the cash flow boost to which the entity is entitled (disregarding this paragraph) for the period.

Many taxpayers however may wonder about those owners of businesses (through trusts or otherwise) that don’t pay themselves a wage. Instead they take trust distributions, receive dividends or simply draw on the profits of the business. As legislated, the cash flow boost is only available in respect of (broadly) employment related withholdings. There may be a strong risk of falling foul of the anti-avoidance provision if someone who has not been paid salary or wages for a long period is now put on wages.

The ATO is veryaware that schemes are being entered into to take advantage of this handout, and we will let clients know if an announcement is made in this regard.

SUPERANNUATION CONTRIBUTIONS

Employers should note that there are no changes to the requirement to make superannuation contributions in accordance with the Superannuation Guarantee law.

SGC AMNESTY

The SGC amnesty period started on 6 March 2020 and will conclude at midnight on 7 September. No change has been made to this period. It should be remembered that payments after 7 September 2020 in relation to the SGC amnesty will not be tax deductible.

STIMULUS PAYMENTS TO HOUSEHOLDS

Also provided for is the payment of the first economic support payment of $750 to Social Security and Veterans’ income support recipients, Farm Household Allowance recipients, Family Tax Benefit recipients and holders of a Pensioner Concession Card, Commonwealth Seniors Health Card or Commonwealth Gold Card.

There will also be a second economic support payment of $750 to the above people who receive a qualifying payment or hold a qualifying concession card on 10 July 2020. This second payment will not be paid to a person who receives, on 10 July 2020, the new Coronavirus supplement detailed below.

ADDITIONAL SUPPLEMENT FOR INCOME

SUPPORT RECIPIENTS

The stimulus package also amends the Social Security legislation to provide financial assistance to people who are affected by the COVID-19 crisis. Australians can claim Jobseeker payment or Youth Allowance (other) if they are an Australian resident (or exempt from the residence requirements). If qualified, a person receives the current rate of Jobseeker payment or Youth Allowance (other) along with a fortnightly supplement of $550 or such other amount determined by legislation.

The supplement is also available to existing recipients of Jobseeker payment, Youth Allowance (other), Parenting Payment, Special Benefit, and the Farm Household Allowance. The Minister for Families and Social Services may extend the supplement to other social security payments by legislative instrument should a need arise.

The supplement is available for an initial six month period, although this may be extended depending on how the current crisis unfolds.

Recipients of Jobseeker payment or Youth Allowance (other) (which includes new and existing recipients) and Parenting Payment are also exempt from the assets test, liquid assets waiting period, ordinary waiting period, newly arrived resident’s waiting period and seasonal worker preclusion periods. The exemption from the newly arrived resident’s waiting period also applies to special benefit. The supplement and exemptions also apply to recipients of the Farm Household Allowance.

Note that the date of effect for these measures is 27 April.

SUPERANNUATION DRAWDOWNS

The bill amends the regulations to give effect to the Government’s announced measure to reduce the minimum payment amounts for account-based pensions (and for the equivalent annuity products) by half for the 2019-20 and 2020-21 financial years.

EARLY RELEASE OF SUPERANNUATION

The stimulus legislation allows individuals affected by coronavirus to have up to $10,000 released from their superannuation or retirement savings account on compassionate grounds. Each person is permitted to have up to two releases – one for an application made during the 2019-20 financial year and another for an application made during the 2020-21 financial year. The amounts that are released are not subject to tax.

From mid-April eligible individuals will be able to apply online through myGov to access up to $10,000 of their superannuation before 1 July 2020. They will also be able to access up to a further $10,000 from 1 July 2020 until 24 September 2020.

The legislation states that to apply for the determination for such early releases, the person must satisfy any one of the following requirements about their employment or business status.

At the time the person applies for the determination, they are:■ unemployed;■ eligible to receive a Jobseeker payment, Youth

Allowance, Parenting Payment (which includes the single and partnered payments) or special benefit under the Social Security Act; or

■ eligible to receive the Farm Household Allowance; or

On or after 1 January 2020 the person:■ was made redundant;■ their working hours were reduced by 20% or more; or■ if the person is a sole trader – their business was

suspended or there was a reduction in their turnover of 20% or more. g

Covid-19 stimulus and rescue package cont

This information has been prepared without taking into account your objectives, financial situation or needs. Because of this, you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation or needs.

Commercial Tenancies

The Prime Minister released the following

Statement on 2nd April.

National Cabinet made further progress on the issue of commercial tenancies. They have agreed that a mandatory code of conduct guided by certain principles will be developed and subsequently legislated by State and Territory Governments to apply for tenancies where the tenant is eligible for the Commonwealth Government’s JobKeeper assistance and is a small- or medium-sized enterprise (less than $50 million turnovers).

The principles that guide the code will be:

a. Where it can, rent should continue to be paid, and where there is financial distress as a result of COVID-19 (for example, the tenant is eligible for assistance through the JobKeeper program), tenants and landlords should negotiate a mutually agreed outcome

b. There will be a proportionality to rent reductions based on the decline in turnover to ensure that the burden is shared between landlords and tenants

c. There will be a prohibition on termination of leases for non-payment of rent (lockouts and eviction) d. There will be a freeze on rent increases (except for turnover leases) e. There will be a prohibition on penalties for tenants who stop trading or reduce opening hours f. There will be a prohibition on landlords passing land tax to tenants (if not already legislated) g. There will be a prohibition on landlords charging interest on unpaid rent h. There will be a prohibition on landlords from making a claim to a bank guarantee or security deposit for

non-payment of rent i. Ensure that any legislative barriers or administrative hurdles to lease extensions are removed (so that a

tenant and landlord could agree on a rent waiver in return for a lease extension) For landlords and tenants that sign up to the code of conduct, States and Territories have agreed to look at providing the equivalent of at least a three-month land tax waiver and three month land tax deferral on application for eligible landowners, with jurisdictions to continue to monitor the situation. Landlords must pass on the benefits of such moves to the tenants. In cases where parties have signed to the code of conduct, the ability for tenants to terminate leases as mentioned in the National Cabinet Statement on 29 March 2020 will not apply. Mediation will be provided as needed through existing State and Territory mechanisms.

The proposed code of conduct will be discussed at the next meeting of the National Cabinet on Tuesday 7 April.

Our tips

• Talk to your landlord or tenant earlier rather than later

• Document any new agreements in writing – this includes rental holidays, lease

extensions

• Be fair on both sides of the fence asking for no rent in most cases won’t work

• Seek legal advice if facing times of Landlord pressure

• As a tenant review your lease and lease expiry dates

Apprentice subsidy

Eligibility The subsidy will be available to small businesses employing fewer than 20 full-time employees who retain an apprentice or trainee. The apprentice or trainee must have been in training with a small business as at 1 March 2020.

Employers of any size and Group Training Organisations that re-engage an eligible out-of-trade apprentice or trainee will be eligible for the subsidy. Employers will be able to access the subsidy after an eligibility assessment is undertaken by an Australian Apprenticeship Support Network (AASN) provider.

This measure will support up to 70,000 small businesses, employing around 117,000 apprentices.

YOU CANT APPLY UNTIL 5th April 2020

Victorian Government announces $1.7 billion rescue package for businesses hit by coronavirus pandemic By state political reporter Bridget Rollason and staff -- Updated 21 Mar 2020, 12:31pm

Premier Daniel Andrews has announced a three-stage assistance package worth about $1.7 billion to assist Victorian businesses struggling amid the coronavirus pandemic.

Key points:

• Businesses will be able to access the payroll tax cash refunds by next Friday

• Payroll tax that was paid by eligible businesses in the first three quarters of this financial year will be handed back

• It will provide businesses with up to $113,975 in cash, with most receiving about $23,000

Mr Andrews said the first stage of the business survival package would consist of $550 million which would go to 24,000 small and medium-sized enterprises with a payroll of less than $3 million as a payroll tax refund.

It is hoped the cash will help keep about 400,000 workers employed and ease the growing stress being felt by the entertainment and hospitality industry.

"This is not a tax cut," Mr Andrews said today.

"It is a refund back in the accounts of businesses in just a few days' time, cash that will be critical to them being able to support their workers and in turn those workers being able to support their families."

Coronavirus update: Follow the latest news in our daily wrap

He said another $500 million would be put into a fund for hardship payments, small grants and tailored support which would be distributed in consultation with the Victorian Chamber of Commerce and Industry, the Australian Hotels Association, the Australian Industry Group and other industry representatives.

This money will go towards sectors that "really are doing it tough" who may not pay payroll tax and require more tailored support to survive.

The third component of the package, worth more than $600 million, included a range of measures such as the waiving of 12,5000 venues' liquor licence fees due this month and worth a total of $30 million, he said.

"The balance of the package will also support people who have lost their jobs, and we acknowledge there are many people who have lost their jobs and many more who will lose their jobs in the weeks and months ahead," he said.

Commercial tenants in government buildings will also be able to apply for rent relief, a measure the Government is encouraging private landlords to offer as well.

Businesses will be in one of the following positions by the end of April:

1. Completely closed

2. Working on a reduced scale

3. Trading but not necessarily doing well

4. Trading as per normal

We are told by Governments that we are in this together and that they will do as much to assist as

possible.

For some it’s not that easy and is an impossible task to resurrect a successful business in six months’

time. Take time to implement your business survival plan. Seek taxation benefits available from the

Stimulus Packages. Remember this will pass and you will need to focus beyond today and how you

can be the first out of the gates when we are told it’s over.

Here are a few tips to help your business through this time:

✓ Reduce overhead costs and focus on aspects of the business to produce income

✓ Cut spending costs where able to do so

✓ Delay capital outlays that can wait

✓ Focus on spending costs that will increase sales and prepare the business for Growth

✓ Innovate with new ways to do business, keep customers engaged

✓ Follow up debtors, renegotiate payment terms

✓ Prepare revised cash-flow statements – stress test your scenarios

✓ Negotiate with the ATO for repayment plans, interest remissions – talk to us we specialise in

helping with negotiation

✓ Negotiate with financiers and landlords

✓ Change yearly cost expenses to monthly DD if possible

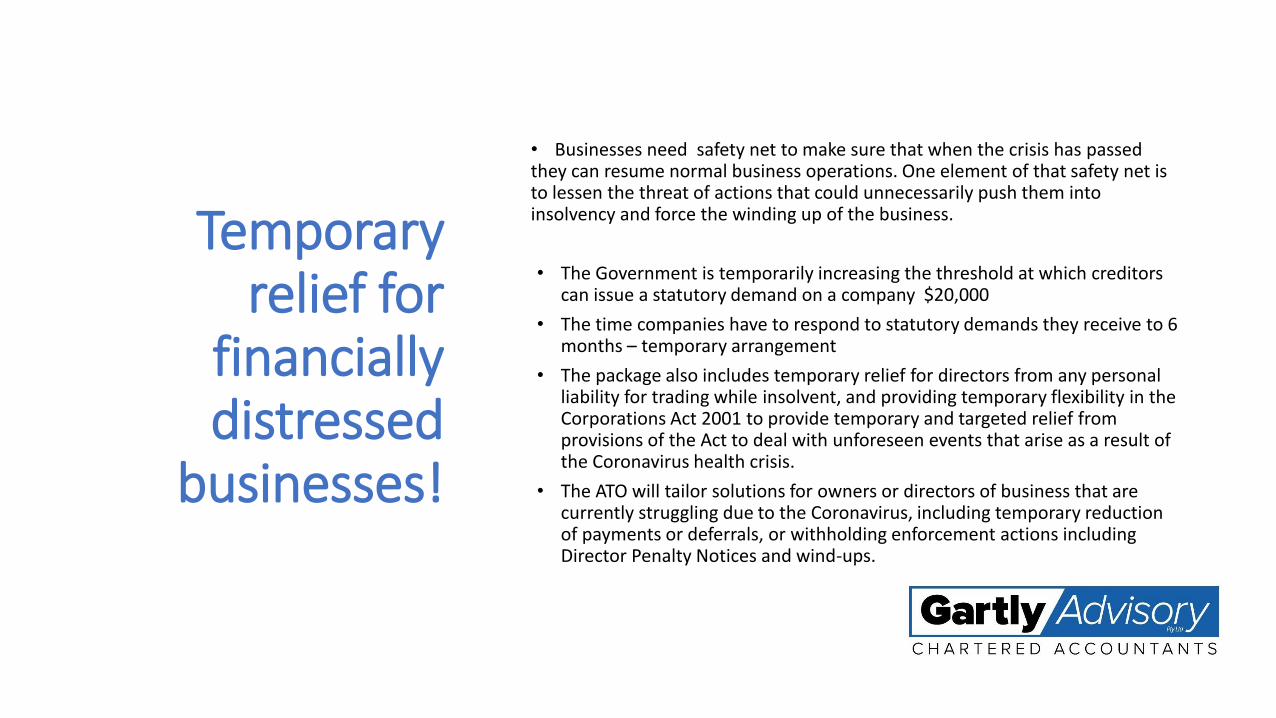

Temporary relief for

financially distressed

businesses!

• Businesses need safety net to make sure that when the crisis has passedthey can resume normal business operations. One element of that safety net is to lessen the threat of actions that could unnecessarily push them into insolvency and force the winding up of the business.

• The Government is temporarily increasing the threshold at which creditors can issue a statutory demand on a company $20,000

• The time companies have to respond to statutory demands they receive to 6 months – temporary arrangement

• The package also includes temporary relief for directors from any personal liability for trading while insolvent, and providing temporary flexibility in the Corporations Act 2001 to provide temporary and targeted relief from provisions of the Act to deal with unforeseen events that arise as a result of the Coronavirus health crisis.

• The ATO will tailor solutions for owners or directors of business that are currently struggling due to the Coronavirus, including temporary reduction of payments or deferrals, or withholding enforcement actions including Director Penalty Notices and wind-ups.

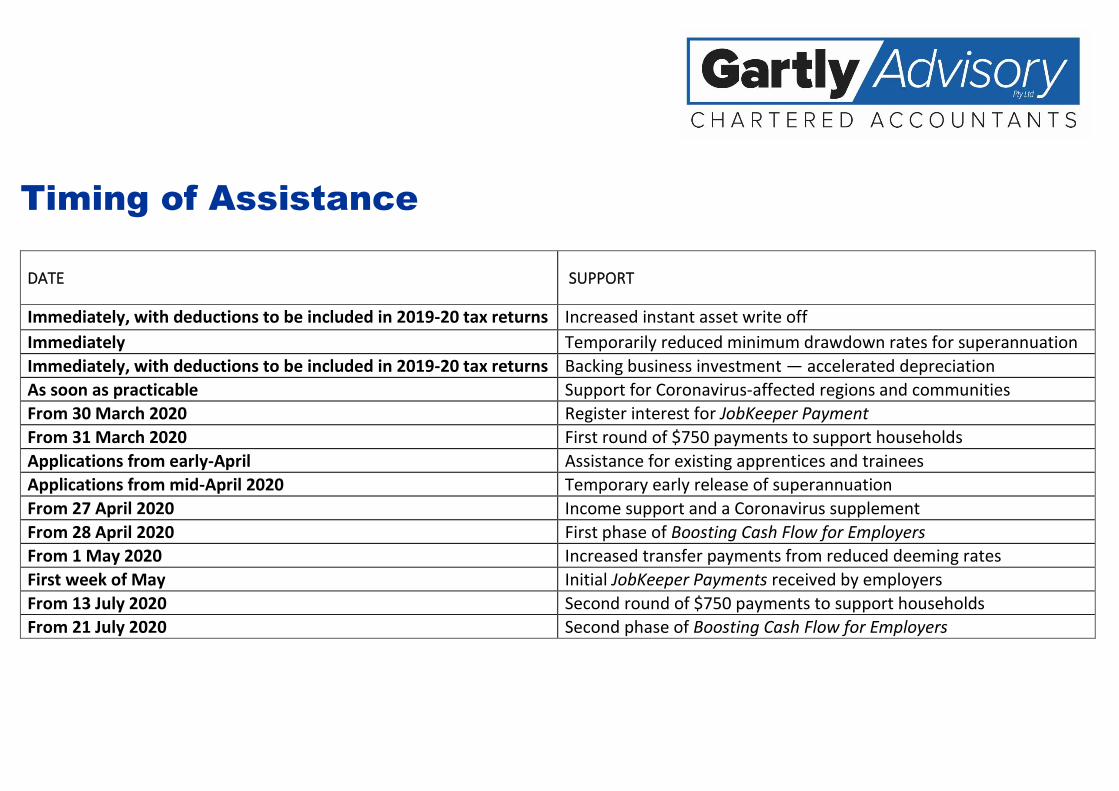

Timing of Assistance

DATE SUPPORT

Immediately, with deductions to be included in 2019-20 tax returns Increased instant asset write off

Immediately Temporarily reduced minimum drawdown rates for superannuation

Immediately, with deductions to be included in 2019-20 tax returns Backing business investment — accelerated depreciation

As soon as practicable Support for Coronavirus-affected regions and communities

From 30 March 2020 Register interest for JobKeeper Payment

From 31 March 2020 First round of $750 payments to support households

Applications from early-April Assistance for existing apprentices and trainees

Applications from mid-April 2020 Temporary early release of superannuation

From 27 April 2020 Income support and a Coronavirus supplement

From 28 April 2020 First phase of Boosting Cash Flow for Employers

From 1 May 2020 Increased transfer payments from reduced deeming rates

First week of May Initial JobKeeper Payments received by employers

From 13 July 2020 Second round of $750 payments to support households

From 21 July 2020 Second phase of Boosting Cash Flow for Employers

Keeping the team on the bus in your business

Your options to look after your team: ➢ Continue employment

➢ Reduce hours of employment

➢ Use up Leave entitlements

➢ Register for JobKeeker

➢ Stand-down completely - no work can be done - but obtain JobKeeker

➢ Stand-down but reinstate due to $$$ subsidy under JobKeeker

➢ Redundancy – Fair work regulations applies

Things to think about ➢ How to keep your team motivated and connected

➢ Keeping your team informed

➢ Using the time to train your team

➢ How your staff can work from home and setting the boundaries

➢ Providing a safe environment either at work or home

➢ Use of zoom and other Apps to stay connected

Articles enclosed ✓ Information for Employers – Argus Legal

✓ Ending Employment – Fair Work Australia extract

✓ Ten working from home issues to consider during COVID-19 – Institute Chartered

Accountants Australia

Argus Lawyers Level 4, 34 Queen Street Melbourne Victoria 3000

Telephone:03 9252 7500

Vital information for Employers - Health Checks and Pay Cheques

Exclusive briefing for clients of Gartly Advisory Pty Ltd from

Matthew Clarke of Argus Lawyers

As of 25th March 2020 – general information please seek your own professional advice.

Matthew has assisted and continues to help a number of my clients over many years on commercial and employer legal matters. Matthew has made this exclusive information

available to you to assist in this challenging time.

Almost everyone in the community expects the coronavirus pandemic to weigh heavily on

Australian business for many months to come. Business owners and managers will have to

accept and adapt to a new evolving workplace environment if they are to survive. We are

witnessing schools closing, cancellations of non-essential services and remote working to avoid

spreading or catching the coronavirus. Warnings have been issued to expect to have to care

for those close to us who are unfortunate enough to be afflicted by effects of the coronavirus.

What rights and responsibilities does the law impose for employers and employees in these

circumstances?

Can the employer remain in operation but close its business premises?

Under occupational health and safety legislation, an employer must, so far as is reasonably

practicable, provide and maintain a working environment that is safe for staff and without risks

to the health of staff. The duty extends to employees and staff engaged as contractors and their

employees or sub-contractors. All employers must, on an ongoing basis, consider whether the

coronavirus will render their workplaces unsafe and, if so, whether business premises should

be closed, staff density reduced or whether other changes are required. If an employer directs

or allows staff to work from home, the employer must ensure the home is suitable for work to

be performed and, if necessary, modify the nature of work expected to be performed to ensure

it is suitable for the staff member's home.

Employees and contractors also have obligations under OH&S legislation. For example, such

persons must take reasonable care for their own health and safety and that of other persons

who may be affected by their acts or omissions at a workplace (including their home).

Remote working for desk-bound office workers will become the new normal. In an

environment in which most such employees will have an employer-provided computer and an

existing residential internet connection, it is unlikely that the employer can be made to bear

the cost of setting up a home office. Conversely, it is reasonably likely that a remote employee

can seek employer reimbursement for the cost of consumables such as printer paper and print

cartridges.

Under some modern awards or employment agreements, employers may have the power to

require an employee to take annual leave during periods in which work cannot reasonably be

performed.

What happens if an employee has to care for an ill relative or children whose school has

been closed?

The Fair Work Act 2009 ("FWA") largely regulates this topic.

The FWA prevents an employer from unreasonably refusing flexible working arrangements that

are requested by an employee where the employee is the parent, or has responsibility for the

care, of a child who is of school age or younger; a carer (a defined term); has a disability; is 55

or older or is affected by domestic violence. The employee's request must be in writing and, if

refused, the employer must give reasons in writing.

For each year of service with the employer, an employee (excluding a casual employee) is

entitled to 10 days of paid medical leave (called personal / carer's leave in the legislation). The

entitlement accrues progressively during the year and accumulates from year to year. Such

leave may be taken if the employee is ill or injured, to provide care or support to a member of

the employee's immediate family or household, who requires care or support due to illness,

injury or an unexpected emergency. Notice must be given. The employer is entitled to request

evidence that would satisfy a reasonable person that the leave is warranted.

If the above personal / carer's leave entitlements are exhausted, an employee may take a

further two days unpaid carer's leave to provide care or support to a member of the employee's

immediate family for the above reasons.

Are employees in self-isolation entitled to be paid?

Recently, employees have been in self-isolation due to government directions, government

recommendations or employer requirements. In these circumstances, an employee is entitled

to be paid if the self-isolation is in response to the employer's direction and the employee is

otherwise willing and ready to work. Arguably, if the employee refuses a reasonable direction

to work from home, while in isolation, pay may be withheld. Where the self-isolation is at the

direction or recommendation of the government, the employee is not entitled to pay unless the

absence is treated as a period of annual leave or the employee would be entitled to personal /

carers' leave or compassionate leave.

If a business continues to operate from its premises, can the employer screen staff?

In the present environment, OH&S obligations permit (and likely require) employers to direct

employees to disclose recent travel and close contact to recognised high-risk individuals.

Employers are likely to be duty-bound to implement social distancing policies and ensure staff

are able to minimise the risk of contaminating other staff (e.g. by having access to regular

handwashing facilities, etc.). In addition an employer is likely to be entitled to require staff

undergo checks for coronavirus symptoms, particularly where the staff are members of, or in

contact with members of, high-risk groups. Thermal scanners like those seen at airports and

other public places may be used, provided they do not operate in private areas such as toilets or

washrooms and do not record private conversations, failing which their operation is likely to

contravene the Surveillance Devices Act 1999 (Vic) and any equivalent legislation in other states

and territories.

Must salary be paid to an employee performing duties for an emergency management

body?

The FWA allows employee absences to engage in a "voluntary emergency management

activity" under provisions normally associated with a employees that are members of the SES

or volunteer fire brigades. The FWA also permits employee absences to perform functions for

organisations intended to respond to an emergency or natural disaster. We may see more

employees requesting absences to respond to the wider impacts of the coronavirus in the

coming months. In Victoria, there is no obligation to pay the employee during these periods of

absence.

Can staff be stood down?

The FWA permits an employer to stand down employees without pay "during a period in which

the employee cannot usefully be employed because of … a stoppage of work for any cause for

which the employer cannot reasonably be held responsible." Before an employer elects to stand

down an employee, the employer must ask (a) whether the employee cannot usefully be

employed and (b) whether the employer cannot reasonably be held responsible for the

stoppage. Employees and employers are under a mutual obligation to act fairly, so alternatives

to standing down employees, such as paid annual leave or agreed cuts to working hours, must

be considered. Standing down employees due to a business slow-down caused by the

coronavirus pandemic is unlikely to be allowed by the FWA. In such a case, the business will

have to consider terminating employment or initiating a stand-down with the employees'

agreement. A stoppage due to a government order closing the workplace or inability to source

necessary materials is likely to be allowed by the FWA. Ordinarily, even if the stand down

proceeds, it must be temporary as stand downs are only intended to operate for as long as is

necessary for an employer to respond to the changed circumstances. The following statement

in a 2011 Fair Work Australia decision ordering an end to a stand down due to a factory catching

fire is apt: "While I appreciate the circumstances that gave rise to the stand down were beyond

the control of [the employer] the stand down cannot continue indefinitely. The employees are

rightly entitled to either return to work or be made redundant in accordance with the [applicable

processes]". Unfortunately, the worsening economic impact of the corona virus suggests many

stand downs will be a prelude to a redundancy.

Long service leave entitlements may, in theory, operate as a paid "stand down". Long service

leave is governed by state and territory legislation. The legislation is fairly consistent between

jurisdictions, although details differ between jurisdictions. Victorian legislation allows an

employee (including some casual employees) to take long service leave after completing seven

years of continuous employment with one employer (although where an employee was

employed in a business acquired by the current employer, the continuous employment is

treated as occurring with one employer). Employees may consume all of their long-service leave

at once or over multiple periods of not less than one day. An employer can refuse an employee's

request to take long service leave if the employer has reasonable business grounds for the

refusal. An employer cannot direct an employee to take long service leave unless at least 12

weeks' written notice is given. If notice is less than 12 weeks, the long service leave can only

occur with the employee's agreement.

Employees currently on, or about to commence, long service leave may consider themselves

relatively fortunate in the coming months. While any travel plans are likely to have been

thwarted, they will remain entitled to be paid during the period of their long service leave,

perhaps unlike some of their colleagues.

Termination of Employment

Sadly, this pandemic will result in widespread terminations of employment. These terminations

are likely to attract the operation of the redundancy provisions of the FWA, the relevant

employment contract, modern award or other applicable instrument.

Businesses that have sought to engage staff as contractors in the expectation that doing so

would avoid the impact of the FWA and other employment law legislation should tread carefully.

Termination of such staff may be risky. An individual that has been directly engaged as a

contractor by a business (i.e. without an interposed corporate entity) and who has become

closely integrated with the business and under its direction may in fact be classified as an

employee by the courts or employment tribunals. Any perceived "contractor" who successfully

argues that he or she was in fact an employee will in all probability be able to claim any one or

more of pay in lieu of notice, redundancy pay, accrued leave entitlements, superannuation and

other entitlements or benefits generally reserved for employees.

Ten working from home issues to consider during the COVID-19 pandemic Coronavirus is rapidly emerging as a workplace health and safety issue, and many businesses are considering employee work from home arrangements. IN BRIEF

• Employers should be cognisant of relevant employment agreements, enterprise agreements and awards

• The work from home policy should be seen as part of a broader HR policy response to coronavirus

• Ensure you claim the correct amount of deductions when preparing your annual income tax return this year

Some employees are also proactively suggesting they work from home and not just because of personal health concerns. Coronavirus may disrupt established childcare and school arrangements, requiring working parents to tend to their children at home or elderly relatives may need to be cared for. Some businesses have established processes and systems which allow for this however there will be many employers who need to quickly grasp the many issues involved, according to CA ANZ Australian Tax Leader Michael Croker. And while we recommend you contact your local Chartered Accountant for general business advice during tough times, there are some specific issues to bear in mind.

1. The legal side of things Workplace health and safety laws in Australia generally require businesses to eliminate or minimise risks to the health and safety of workers in a way that is reasonably practicable.

Sending workers home because of coronavirus concerns may fall into this broad duty of care. However, employers who let their employees work from home or remotely also need to assess the risks and ensure employee safety in that external environment. This can be challenging without established processes, and in some cases, it will be a matter of balancing competing risks. Employers should also be cognisant of relevant employment agreements, enterprise agreements and awards when either mandating work from home arrangements or responding to employee requests to do so. Where an employee initiates the request, note that the Fair Work Act caters for flexible working arrangement requests where the employee has worked for the same employer for 12 months. In the context of coronavirus, such requests can be made by carers and workers aged 55 or older. The employer can decline the request but only on reasonable business grounds and must provide a written response with reasons within 21 days. Communicating work from home policies relevant to coronavirus is essential. Ideally, these policies should be online, readily accessible to the workforce and a "question and answer" document should be developed to address commonly raised issues. As always on employment law issues, seek legal advice.

2. Workers compensation, public liability and professional indemnity cover Regardless of the location, employers must provide a safe workplace. Employees should have access to workers compensation insurance if any injuries or illnesses arise while working remotely, but it may also be prudent to review the scope and cover of other insurances, such as public liability, professional indemnity and other business protection policies. Normally, employers should carry out a home workplace safety assessment if only to address workplace health and safety issues, but the spread of coronavirus makes this more difficult. Some written guidance or checklist on safe home workplace practices backed by telephone check-ins might be a more appropriate response. Check with your State or Territory health and safety regulator and your insurer. Public liability cover should also be reviewed if a home-based employee conducts face-to-face business activity from home, for example they see suppliers or customers.

Businesses offering professional services may need to review their professional indemnity cover (or at least notify their insurer that employees are now working from home due to coronavirus). Professional indemnity insurers may seek details of the supervision arrangements for work from home employees.

3. Develop a robust work from home policy Much of what follows falls under this heading, but it's important for employers to have guidance to which employees can refer. For example, not all employee roles lend themselves to home-based work, so eligibility criteria should be developed. Importantly, the work from home policy should be seen as part of a broader HR policy response to coronavirus, dealing with issues such as:

• Informing the employer of illness • Staying away from work if feeling unwell (even if the worker has no sick leave

entitlements) • Assurances around the confidentiality of health-related information • Sick leave entitlements • Mandating work from home arrangements • Remuneration where no leave entitlements remain • Leave without pay • Reduced paid work hours • Compliance with hygiene standards

4. Be clear about work from home ground rules Employees generally rate highly a business that offers flexible work arrangements and working from home can boost productivity. With no commuting time, it's possible to get more done on both work and domestic fronts. But unstructured, poorly supervised work from home arrangements can be detrimental not just for the business but also for workplace relations if some employees perceive they are working harder than others. So it's important to clearly state the employer's expectations and boundaries around work from home arrangements. For example, the employee should commit to working the same work hours (although not necessarily a standard "9 to 5" work day where there are family care obligations) with the same level of output. They should plan their day, set goals and focus on outputs just as they would if supervised in the employer's workplace.

Managers and supervisors should schedule regular check-ins. For employees, remaining "visible" in a virtual sense, contactable and fully engaged in the business should be a key objective. Good communication is vital. Use instant messaging functions not just to communicate down-time (e.g. "away from desk, leave voicemail"), but the reasons and expected time when back online (e.g. "picking up the kids from school 3pm to 4pm"). Here are some other tips for employees:

• Be "present" by your work "presence" and equate working from home with working from the office. Multi-tasking work and domestic chores is great, but not when you need to be a fully engaged participant in a teleconference with an important client.

• Establish a home workspace that helps you work efficiently. Remember, standards around data security apply just as equally at home.

• Keep track of tasks and accomplishments. Communicate with supervisors regularly and succinctly. Be mindful of email fatigue and keep using the telephone to maintain personal rapport (and remember the mute button to cancel out domestic background noise).

5. Home workplace tools, technology and systems Work-related telephone and internet access is fairly widespread these days, but employers should check that home technology is adequate for work purposes. At the very least, employers should ensure employees have sufficient reception or connectivity to contact emergency services if needed. Systems access should also be tested. Nowadays employees need access to much more than office emails. Access to business and document databases, accounting systems, HR, payroll and client marketing software are just some examples where different personnel may need differing levels of access, and for commercial software used in the business, the licences to do so. As always, cyber awareness is vital. For example, logging into workplace systems via public networks (e.g. the coffee shop just around the corner) should be discouraged. If the employee's own computer is being used for work, check that workplace IT standard, compatible anti-virus software has been installed.

6. Insurance of work equipment Every business should have records of workplace equipment, their location and the name of the worker responsible for them. The employer's general property insurance policy should cover business equipment regardless of its location but check the policy to see if there are exclusions relevant to equipment taken home for work use. A risk and insurance coverage "gap" may arise if the employee's property is being used for work purposes. That is, the employee's property isn't covered by the employer's policy, and the employee's home and contents insurance policy doesn't cover the employer's business equipment. Damage suffered due to data loss etc (e.g. due to malware downloaded accidentally onto the employee's home computer) may also fall into this kind of insurance gap. Seek advice from your insurer or insurance broker.

7. Build, maintain and encourage a "virtual" workplace network We all sometimes take for granted the intangible but valuable networking benefits which workplaces provide. Apart from the social aspect, there's also the sharing of insights and problem-solving that comes from personal contact. Virtual collaboration technologies such as WhatsApp groups can help fill the void, as can participation in chat rooms and posts with suppliers and customers. Managers should schedule one-on-one and group "check-ins" to foster a virtual sense of belonging and teamwork. Remember, coronavirus is a community-wide, health-related emergency. When it comes to successful workplace relations and keeping good employees onboard, managers are the eyes and ears of the business. They need to demonstrate empathy with members of their work teams and be empowered to make decisions which convey the employer's concern for the welfare of all employees, their families and the broader community.

8. Tax issues – Employee perspective Unfortunately, tax raises its ugly head when income producing activity occurs in the home.

What's tax deductible? "Home office" expenses such as running expenses, phone and internet costs are deductible provided detailed ATO guidance is followed and substantiating records are kept. Tax depreciation deductions may be available on some assets used for work purposes. There's even a home office deduction calculator available on the ATO website. Home to work travel costs are a confusing area of tax law. Deductions are generally not available, but there are limited exceptions. Assuming the employee is simply working from home – as distinct from running a business from home – the main residence exemption under the capital gains tax (CGT) rules will not be impacted. What's not deductible? In some cases, expenses associated with working from home will be paid for or reimbursed by the employer (e.g. work-related telephone calls and internet usage, postage and courier charges). Where the employer foots the bill, such expenses are not deductible to the employee. Private and domestic expenditure – such as house cleaning, hiring a carer for children or elderly parents – is not deductible. Your accountant will be able to help you claim the correct amount of deductions when preparing your annual income tax return.

9. Tax issues – Employer perspective Fringe Benefits Tax (FBT) No FBT should apply where an employer reimburses or pays for an employee's work-related expenses arising from working from home arrangements. Similarly, equipping an employee solely for the purpose of enabling them to work from home should not attract FBT. However, these employee benefits should be documented to evidence that they relate solely to work. Some FBT may apply where benefits have a dual work and private nature. Importantly, the FBT law contains exemptions which may apply (subject to satisfying various conditions) where an employer provides an employee with:

• Tools of trade, a laptop, mobile phone or protective clothing (e.g. face masks);

• Medical examinations, screening, preventive health care, screening or counselling;

• "In-house" health care;

• Taxi travel (e.g. from work to home – or vice versa – or to a GP or hospital). The minor benefits FBT exemption may also apply for minor, infrequent and irregular benefits of less than $300 provided in response to the coronavirus emergency. Specific FBT exemptions and concessions apply to benefits provided to workers in the health care sector. What's tax deductible? For income tax purposes, the employer’s expenditure enabling work from home arrangements should be tax deductible as an expense of employing labour and as an expense necessarily incurred in carrying on business. Employers should seek detailed FBT and tax advice from their accountant.

10. The longer term… The potential longer-term ramifications of coronavirus related work from home arrangements should not be overlooked in the rush to cope with the current crisis. Management should monitor the benefits and downsides of working from home arrangements and, after the threat of coronavirus has dissipated, review the outcomes. Those businesses who successfully switch-on such arrangements now may well embrace more permanent work from home policies after the coronavirus emergency subsides. If that happens, the ramifications for workplaces, productivity and the demand for business accommodation (e.g. leased office space) will be very interesting to monitor.

2 X 1 . 5 H O U R

I n t e r a c t i v e o n l i n eg r o u p c o a c h i n gs e s s i o n s t o b u i l d' r e m o t e r e a d y 'l e a d e r s w h o :

· Agree expectations with

team members for this

new way of working

· Create a sense of

community & continuity

through team routines

and commitments

· Manage performance &

workloads remotely

· Run engaging team

meetings using online

platforms to ensure

productive collaboration

· Support team members

through this challenging

time of change &

isolation so that they can

be productive

LEADING REMOTELYBuilding 'remote ready ' leaders

Pe r f o rmance Cu l t u r e Consu l t i ng

ARE YOU A REMOTE READY LEADER?Worried about leading your team remotely when

this is new to all of you?

Not sure how to maintain effective collaboration

and communication when everyone is working

remotely (often for the first time)?

How can you be sure people are ok and on track?

Having the technology is only the starting point. ‘Remote Ready’ leaders know how to create a connection,bring the team along and support staff to be productiveduring this huge change in the way we work. In this practical online program, the facilitator will modeleffective online meeting practice whilst helping leaders tocreate their personal ‘Remote Ready Leadership Playbook’ –their tailored strategy to implement these approaches withtheir team as soon as possible. For more information visit:https://performanceculture.com.au/leading-remotely/ or call Justine Coleman - 0434674669

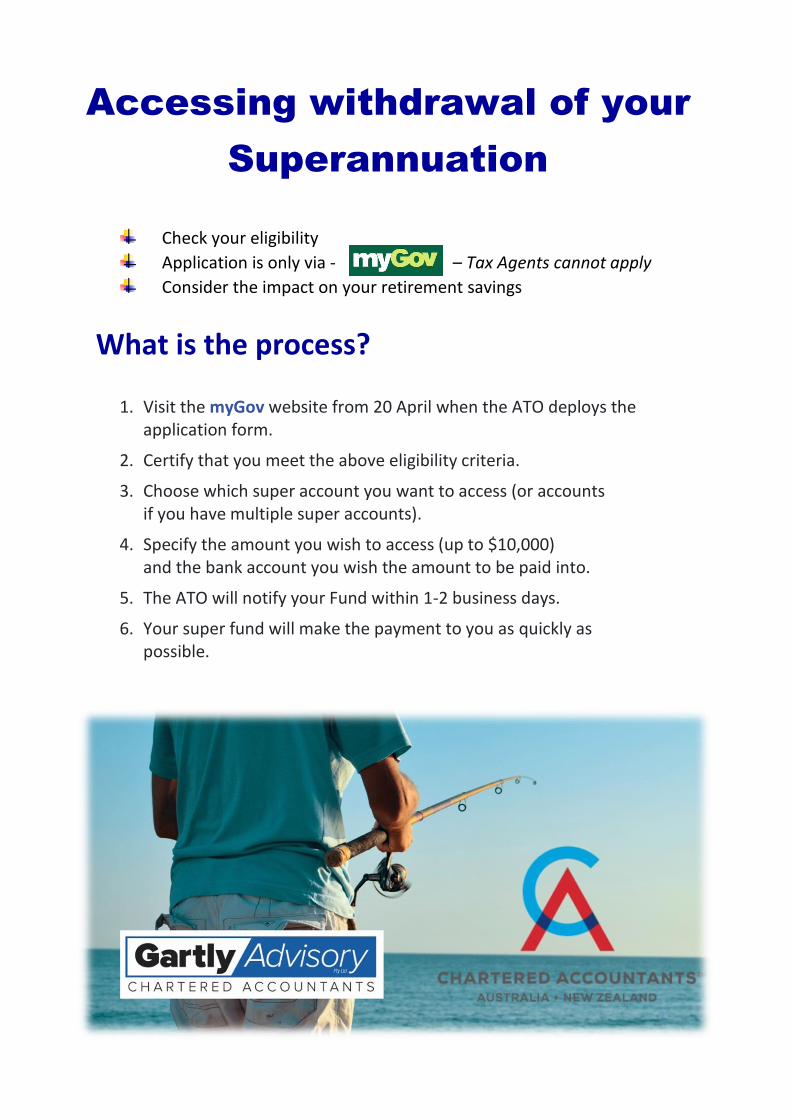

Accessing withdrawal of your

Superannuation

Check your eligibility

Application is only via - – Tax Agents cannot apply

Consider the impact on your retirement savings

What is the process?

1. Visit the myGov website from 20 April when the ATO deploys the application form.

2. Certify that you meet the above eligibility criteria.

3. Choose which super account you want to access (or accounts if you have multiple super accounts).

4. Specify the amount you wish to access (up to $10,000) and the bank account you wish the amount to be paid into.

5. The ATO will notify your Fund within 1-2 business days.

6. Your super fund will make the payment to you as quickly as possible.

Guidance for Advisers where clients wish to access $10,000 of their superannuation as a consequence of the Covid 19 stimulus package.

Advice guidance

Early access to superannuation as a consequence of Covid 19 is client directed and you should limit what you provide to your client to general advice, and provide them with the necessary information to access their super.

If a client does require personal financial advice then you must document that in a Record of Advice or SOA, dependant on the circumstances.

Information on how to access superannuation under the Covid 19 provisions

We recommend you provide your clients with the following information fact sheet https://treasury.gov.au/sites/default/files/2020-03/Fact_sheet-Early_Access_to_Super_1.pdf

This information is summarised below:

The Covid 19 Pandemic is an unprecedented event in all of our lifetimes. As a consequence, the Federal Government has released a number of stimulus packages to keep the economy and Australians financially afloat. One of these packages provides the opportunity for eligible Australians to withdraw up to $10,000 of their super before 1 July 2020. A further $10,000 can be accessed from 1 July 2020 for approximately three months from July 2020.

To be eligible to access lump sums from super, a person must be:

• unemployed• eligible for a Jobseeker payment, Youth Allowance for job seekers, Parenting Payment

(including the single and partnered payments), special benefit or farm householdallowance

• on or after 1 January 2020:o made redundanto had their working hours reduced by 20% or moreo be a sole trader and had their business suspended or there was a reduction in

business turnover of 20% or more.

These payments are tax-free and not treated as income under the Centrelink or DVA income test.

Due to COVID-19, the Government has expanded the Jobseeker and Youth Allowance for job seeker’s criteria,

meaning more people are now eligible. extract ABC news

From April 27, you'll be eligible if you're:

• A permanent employee who has been stood down or sacked

• A sole trader, self-employed, casual worker or contract worker who now earns less than $1,075 a fortnight as a result of the economic downturn

• You're caring for someone who has COVID-19

The Jobseeker and Youth Allowance payments are tapered, meaning if you earn $0 for the fortnight you'll get the full welfare payment, but if you still have some income (but remain below the income threshold) you will receive a portion of the payment.

But even if you're only eligible for a tiny Jobseeker or Youth Allowance payment, you will receive the full $550 a fortnight Coronavirus Supplement. It is an additional top-up payment for people on welfare, which effectively doubles the full Jobseeker (formerly known as Newstart) allowance.

The Government initially announced people receiving the following payments would automatically get the supplement:

• JobSeeker Payment

• Youth Allowance for job seekers

• Parenting Payment

• Farm Household Allowance

• Special Benefit

But later added these payments to the list:

• Youth Allowance for students

• Austudy for students

• ABSTUDY for students

The Coronavirus Supplement will be automatically added to your welfare payment for six months from April 27.

Who gets the $750 Economic Support Payments?

There's a long list of people who will receive the $750 Economic Support Payment, which includes carers, parents and veterans. You don't need to apply for this payment; it will automatically be paid to eligible recipients. Eligible recipients include anyone already receiving Centrelink payments and those new to Centrelink who apply by April 13. Those who aren't eligible for the Coronavirus Supplement, such as disability or age pensioners, may also get a second Economic Support Payment to be paid around July.

![SMSF Borrowing Rules[1]](https://static.documents.pub/doc/80x56/577d20e71a28ab4e1e93feca/smsf-borrowing-rules1.jpg)

![SMSF webinar Sep 14.pptx [Read-Only]notchabove.com.au/wp-content/uploads/2014/09/SMSF... · •SMSF trustees have an obligation to consider whether they need to provide insurance](https://static.documents.pub/doc/80x56/5fca48aacae2a7533069a246/smsf-webinar-sep-14pptx-read-only-asmsf-trustees-have-an-obligation-to-consider.jpg)