Academic year 2006 – 2007 WHO BENEFITS FROM THE “DENOMINACIÓN DE ORIGEN” TEQUILA ? Report Lucie Leclert Promotor: Prof. Han Wiskerke, Wageningen University Co-promotors: Dr. Hielke Van Der Meulen, Wageningen University And Prof. Guido Van Huylenbroeck, Ghent University Supervisors: Dr. Hielke Van Der Meulen Dr. Peter Gerritsen, Guadalajara University, CUCSUR Thesis submitted in partial fulfilment of the requirements for the joint academic degree of International Master of Science in Rural Development from Ghent University (Belgium), Agrocampus Rennes (France), Humboldt University of Berlin (Germany) and University of Cordoba (Spain) in collaboration with Wageningen University (The Netherlands), Slovak University of Agriculture in Nitra (Slovakia) and the University of Pisa (Italy). This thesis was elaborated and defended at Wageningen University within the framework of the European Erasmus Mundus Programme “Erasmus Mundus International Master of Science in Rural Development” (Course N° 2004-0018/001- FRAME MUNB123)

Transcript

Academic year 2006 – 2007

WHO BENEFITS FROM THE “DENOMINACIÓN

DE ORIGEN” TEQUILA ?

Report

Lucie Leclert

Promotor: Prof. Han Wiskerke, Wageningen University

Co-promotors: Dr. Hielke Van Der Meulen, Wageningen University And Prof. Guido Van Huylenbroeck, Ghent University

Supervisors: Dr. Hielke Van Der Meulen

Dr. Peter Gerritsen, Guadalajara University, CUCSUR

Thesis submitted in partial fulfilment of the requirements for the joint academic degree of International Master of Science in Rural Development from Ghent

University (Belgium), Agrocampus Rennes (France), Humboldt University of Berlin (Germany) and University of Cordoba (Spain) in collaboration with Wageningen University (The Netherlands), Slovak

University of Agriculture in Nitra (Slovakia) and the University of Pisa (Italy).

This thesis was elaborated and defended at Wageningen University within the framework of the European Erasmus Mundus Programme “Erasmus Mundus International Master of Science in Rural Development”

(Course N° 2004-0018/001- FRAME MUNB123)

3

This is an unpublished M.Sc. thesis and is not prepared for further distribution. The

author and the promoter give the permission to use this thesis for consultation and to

copy parts of it for personal use. Every other use is subject to the copyright laws, more

specifically the source must be extensively specified when using results from this thesis.

Place of Defence: Wageningen University

The Promoter(s) The Author

name(s) name

4

5

Preface

This report was prepared in collaboration with Wageningen University. It is the result of

7 months research: 4 months of field work in Guadalajara and Autlán and 3 months of

writing in Wageningen. This research is part of the SINER-GI project1, (Strengthening

International Research on Geographical Indications), and serves as a final thesis report

for the M.Sc. degree of International Master of Rural Development (Erasmus Mundus

program). This research received partial funding from the SINER-GI project, and from

the University of Guadalajara through the PROMEP research project on blue agave in

the South Coast region of Jalisco, coordinated by Dr. Peter R.W. Gerritsen and Dr. Luis

Manuel Martinez Rivera.

During my flight to Mexico, I was sitting next to a Dutch woman you had been going to

Mexico for a while now. While I was still a bit apprehensive for my stay and wondering

what I was actually doing in this plane, I will always remember what she told me:

“Don’t worry, after one week in Mexico, you will know what you came there for”. She

was right. Next to the thesis research, it was a fantastic cultural and social experience.

The title chosen for my thesis is actually the first question we had with Hielke van der

Meulen concerning the Denominación de Origen Tequila. But as my house owner

Rodolfo alarmed me the first day I arrived in Guadalajara.

Lucie, si vienes aquí para ver a quien beneficia la DOT, yo te puedo dar la respuesta. Tu informe va a ser de menos de una pagina: Son los tequileros. (If you come here to see who benefits from the DOT, I can give you the answer. Your report won’t even be a page long. They are the tequileros (distilleries)).

Even if the answer is clear, I decided to keep this title as it gives a good summary of

what I wanted to find out and how I organised my field work.

1 1 SINER-GI‘s objective is to build and share a coherent scientific basis world-wide, regarding economic, legal, institutional and socio-cultural conditions of success of GIs, in order to support their legitimacy in the framework of WTO negotiations (Source: http://www.origin-food.org; consulted the 22.05.07).

6

Thanks

Without the help of the following people I would not have been able to write this report.

I would therefore like to mention and thank their supervision and contribution: Dr

Hielke van der Meulen, who informed me about the SINER-GI project and who

supervised me during these 8 months; Thanks to the confidence he had in me and his

constructive comments and advice, I could carry out this investigation and make the

following report; Dr Peter Gerritsen for the pleasant collaboration, his enormous interest

and involvement during my field work and the writing of this thesis; Dr Ana

Valenzuela, for her supervision and help in Guadalajara.

I am also indebted to all the people I interviewed. Thanks to them, I could get part of

the information reported here. Special thanks to Salvador Maldonado, for his advice and

for showing some nice “cantinas” in Guadalajara; Benjamin Barba for helping me to

organize 2 group discussions with agave farmers (one in a very nice restaurant in

Atotonilco); Jose Maria Michel and his wife, for welcoming me in their house and the

nice meals they prepared for me; Ramon Gonzalez for his availability to meet me twice.

I lived in the house of the family Tena in Guadalajara (Ana, Rodolfo, Ana Delia, Ana

Rosa, Ana Belen), and with Laura and Ricardo in Autlán. I want to thank them for their

hospitality, for showing me their country and integrating me in their family, and for

giving me good advice about the “Mexican way of doing things”. Without Ana and her

good map of Guadalajara, I would have never arrived on time for my interviews.

Thanks also to Fabian in El Grullo for driving me around in the Amula region to visit

distillers.

I also want to express my gratitude to Pierre and Malu Pieck thanks to whom I could

experience la cata del tequila and typical Mexican food, for the nice time we spent

together (giving French courses was the excuse) and for being always there for me.

7

Table of Contents

Chapter 1: Introduction and literature review .......................................................... 11 1. Introduction ................................................................................................................ 11

1.1. Research objective............................................................................................... 12 1.2. Problem statement ............................................................................................... 13 1.3. Research questions (figure 1.3) ........................................................................... 14 1.4. Theoretical perspective........................................................................................ 15 1.5. Methodology........................................................................................................ 17

2. Tequila regulatory framework .................................................................................... 24 2.1. Towards a DO...................................................................................................... 24 2.2. Main requirements of the DOT ........................................................................... 28 2.3. Product differentiation possibilities in the scope of the DOT ............................. 29

3. Evolution of the tequila sector since the last century ................................................. 31 3.1. Land redistribution: a major setback for tequila distilleries ................................ 31 3.2. The international development of tequila and its consequences ......................... 34 3.3. From the 1990s: Change of scale and its consequences...................................... 35 3.4. Recent chance of political party and its consequences........................................ 37

Chapter 2....................................................................................................................... 39 Power relationships and internal mechanisms in the tequila sector........................ 39 1. Introduction ................................................................................................................ 39 2. How power relationships have shaped the tequila regulatory framework.................. 40

2.1. Why is the area of DOT so big? .......................................................................... 40 2.2. The evolution of the NOM, a way for distilleries to overcome crisis ................. 43 2.3. Why is it still allowed to export tequila in bulk and to bottle it abroad?............. 47

3. What does each actor think of the others?.................................................................. 49 3.1. Farmers: “what is the DOT?” .............................................................................. 49 3.2. Distilleries: Inequalities and divergent interests.................................................. 51 3.3. El CRT, a “young” certification and control body .............................................. 53

4. Conclusion.................................................................................................................. 55 Chapter 3. The cyclical price of agave:...................................................................... 59 Alternatives and solutions as proposed by actors involved...................................... 59 1. Introduction ................................................................................................................ 59 2. How does the price fluctuation affect the tequila sector?........................................... 61

2.1. Fluctuating power relationships between distilleries and farmers....................... 61 2.2. Different impacts depending on “farmers’ type”................................................ 62 2.3. The despair of small agaveros libres ................................................................... 63

3. Global crop planning, an obligatory step and its limits of.......................................... 64 implementation ............................................................................................................... 64

3.1. The registration of every farmer’s plantations.................................................... 65 3.2. Implementing a contract between farmers and distilleries: Why is it difficult ?. 66 3.3. The limits of implementation .............................................................................. 69

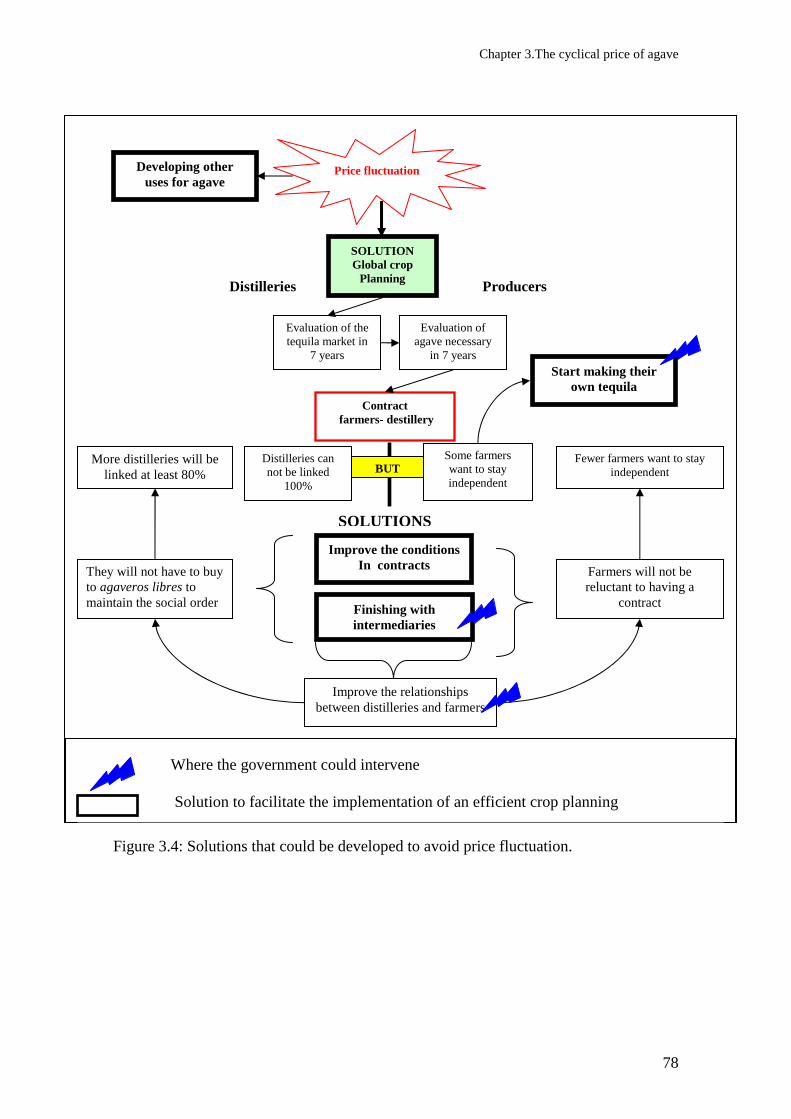

4. How to make a global crop planning possible?.......................................................... 70 4.1. Improving the conditions of the contracts between farmers and distilleries ....... 70 4.2. Finishing with intermediaries .............................................................................. 71 4.3. Evaluation of the potential of each region........................................................... 74

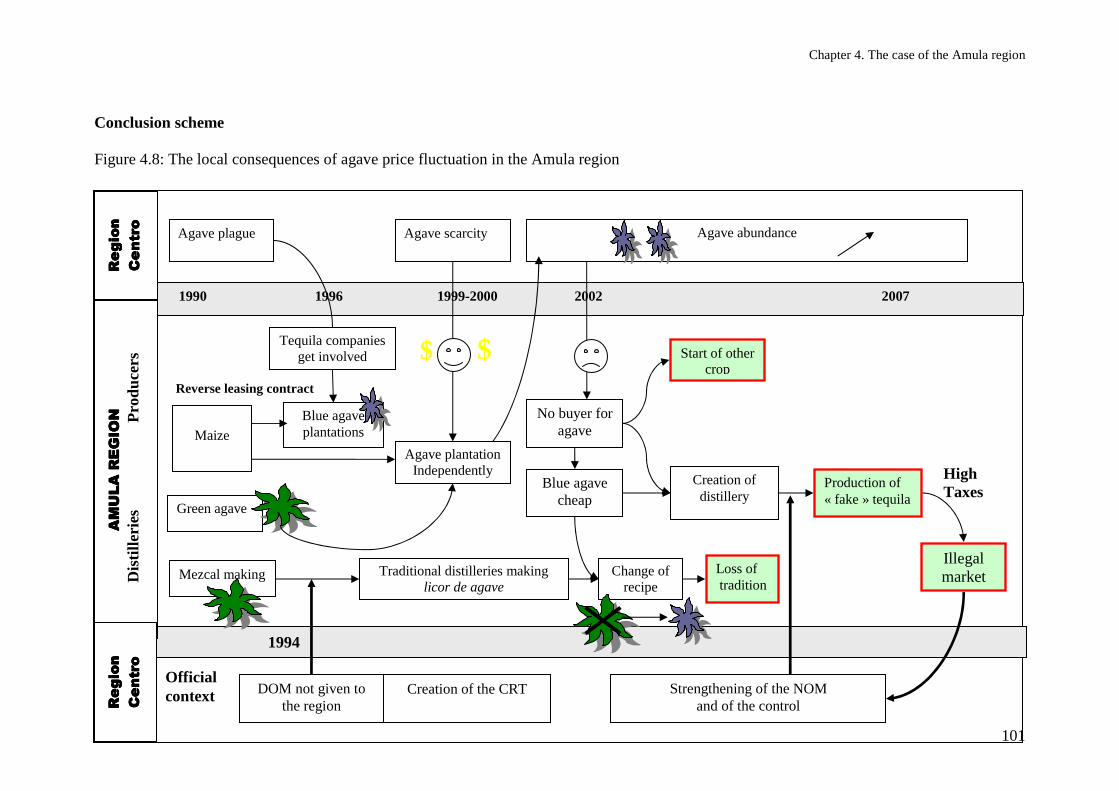

Chapter 4....................................................................................................................... 79 Regional dynamics in the tequila sector: the case of the Amula region .................. 79 1. Introduction ................................................................................................................ 79 2. The specific context of the Amula region .................................................................. 82

2.1. General characteristics of the Amula region ....................................................... 82 2.2. Expansion to other areas in times of scarcity: the case of the Amula region...... 83 2.3. Between the “mezcalera” tradition and the crisis of blue agave ......................... 84 2.4. From mezcal to licor de agave: impact of the DOM ........................................... 85

3. What are the local consequences of the international development of tequila? Local tradition vs. tequila domination...................................................................................... 86

3.1. Mezcalera tradition difficult to maintain ............................................................. 86 3.2. Making your “own tequila”, a way not to lose 7 years of investment................. 87 3.3. The development of informal market: a survival possibility?............................. 89

4. The future of local agave farmers and local distilleries.............................................. 91 4.1. A regulation framework that reduces the opportunities for small-scale enterprises.................................................................................................................................... 91 4.2. From “mezcal” to a nameless product: loss of tradition and prestige ................. 94 4.3. Change of land use again: return to previous situation?...................................... 96

5. Conclusion.................................................................................................................. 99 Chapter 5: conclusion................................................................................................. 103 1. Consequences of the geographical and power concentration................................... 103 2. Where do the benefits of the DOT go?..................................................................... 105

2.1. The unequal beneficiaries in the supply chain................................................... 105 2.2. The inequalities between “peripheral region” and “central region”.................. 105 2.3. The benefits relocated to the Northern countries............................................... 106

3. Recommendations .................................................................................................... 107 4. Discussion. Towards more differentiation possibilities or towards a homogenisation of product?.................................................................................................................... 109 References.................................................................................................................... 113

9

List of figures

Introduction

Figure 1.1: Localisation of Jalisco

Figure 1.2: The State of Jalisco

Figure 1.3: Representation of the problem statement and the research questions

Figure 1.4: Schematic representation of the different actors in the tequila sector

Figure 1.5: list of interviewed or visited distilleries.

Figure 1.6: Resume of the tequila regulatory framework

Figure 1.7: Principal actors of the tequila regulatory framework

Figure 1.8: Tequila categories

Figure 1.9: Different kinds of tequila depending on the time in oak barrels

Figure 1.10: Different part of a label

Chapter 2

Figure 2.1: Schematic representation of agave cycle of abundance and scarcity and its

consequences

Chapter 3

Figure 3.1: Agave inventory in the municipalities with DOT

Figure 3.2: Schematic representation of the reversing power of each group depending on

agave price

Figure 3.3: Limits of implementation of a global crop planning

Figure 3.4: Solutions that could be developed to avoid price fluctuation

Chapter 4

Figure 4.1: Location of the Amula region

Figure 4.2: Evolution of the number of distillery in the Amula region

Figure 4.3: Characteristics of the distilleries visited.

Figure 4.4: Cumulated surface of blue agave planted per municipality in the Zona Sur.

Figure 4.5: Evolution of the number of distillery per municipality

Figure 4.6: Characteristics of the distilleries per municipality

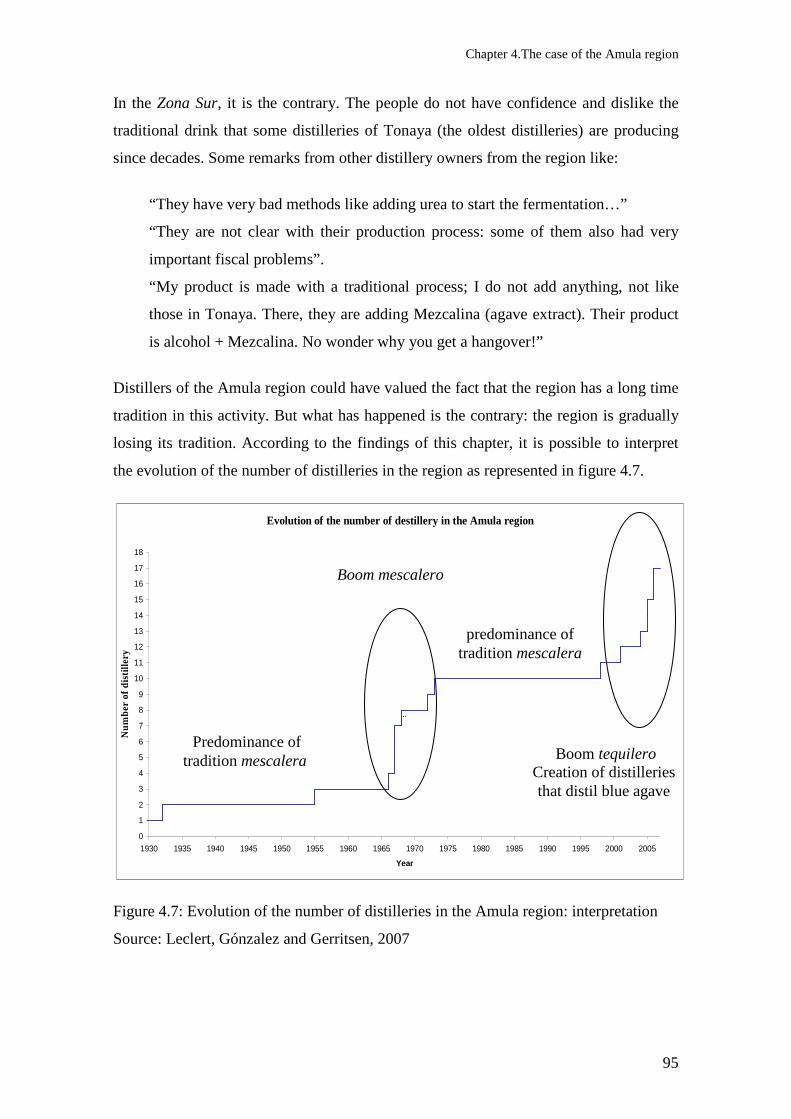

Figure 4.7: Evolution of the number of distillery in the Amula region: interpretation

Figure 4.8: The local consequences of the agave price fluctuation in the Amula region.

10

Chapter 5

Figure 5.1: Impact of the DOT and unequal repartition of benefits

Figure 5.2: International development of the tequila industry and its consequences

Figure 5.3: Different scales of solutions.

Figure 5.4: Tequila supply chain and the different entries for farmers to sell agave

Chapter 1. Introduction and literature review

11

Chapter 1: Introduction and literature review

1. Introduction Mexico is known for its distilled drinks. Historically, the art of distillation arrived with

the Spaniards, but natives’ skills and available resources had contributed to a well

developed tradition of intoxicating beverages. One kind is produced using agave juice.

Before, all distilled products of agave were called “mezcal1”.

Tequila2 is a specific sort of “mezcal”. Its production was geographically limited to

two small regions within the State of Jalisco in Western Mexico where blue agave

(Agave tequilana Weber variety blue) finds its best growing conditions: The city of

Tequila and its surroundings (called Zona Centro), and Los Altos (figure 1.2).

Figure 1.1: Localisation of Jalisco

Source: http://www.map-of-mexico.co.uk. Consulted the 22.05.07

1 The word “mezcal” comes from the Náhuatl “metl” which means maguey and “colli” which means cooked. In this report, when “mezcal” is used with “.”, it refers to distilled products of agave in general while when it is without, it refers to the mezcal according to the Denominación de Origen Mezcal (DOM), see Chapter 4, 5.1. 2 Tequila is also the name of a city. In this report, when it is about the drink, it will be written: tequila, and Tequila for the city.

Chapter 1. Introduction and literature review

12

Figure 1.2: The State of Jalisco

Source: http://www.maps.expedia.com, consulted the 22.05.07

While many “mezcales” are produced and consumed at very local scale (homebrew,

local distilleries), tequila has outgrown regional and national borders and is now a

popular drink consumed all around the world (Burman, 2000). In order to protect it

from imitation, it was granted a Denominación de Origen3 (DO; Appellation of Origin)

by the Mexican government in 1974.

1.1. Research objective

Specific objective in relation to this investigation: to examine how the DOT has

influenced (directly or indirectly) the tequila sector and more specifically the farmers’

strategies.

Research objective in relation to the SINER-GI project: to contribute to a better

understanding of what impacts the legal protection of a Geographical Indication (GI)

can have at the sectoral level and at local level.

3 Abbreviations are resumed in Appendix 1 and Spanish words used in this report are in Appendix 2.

Arandas Amatitán

Los Altos

Zona Centro

Zona Sur

Atotonilco

Chapter 1. Introduction and literature review

13

1.2. Problem statement

The highway from Guadalajara to the city of Tequila offers an unusual view since the

beginning of 2007: Long stalks are pointing to the sky in the blue agave fields: agave

plants are flowering. When the quiote (name of agave flower) is growing, the agave

plant is ready for the jima (harvest4). Once the quiote is cut, farmers have roughly one

year to start the jima, otherwise the plants start rotting. The amazing thing is that many

fields are flowering and the quiotes are not being cut: sign that there is an important

abundance crisis going on. Agave farmers can not find buyers for their produce.

Besides, the price of agave is so low that it is not even worth working in the fields to

cut the quiotes. And it is not just a few months or a single years’ investment that is at

risk, as could be the case with other crops like wheat or maize; it is 7 years that are

disappearing; 7 years of work and hope that the price would be high when agave will

be ready to harvest.

Hoping is what agave farmers have always done. Since agave cultivation is

characterised by cycles of abundance and scarcity, agave farmers and in particular

agaveros libres5 can never be sure to sell their produce at a good price after 7 years.

They “estan esperando”, which in Spanish reveals their situation as it means: they are

“waiting”, but also they are “hoping”, hoping that that the future price of agave will be

higher.

As there is no other opportunity but to sell agave for tequila production, the production

sector has always been controlled by a few distilleries6, initially family owned but now

mainly owned by multinational spirit manufacturers. The long tradition of producing

tequila, the opening to international markets combined with the implementation of the

DOT in 1974 has led to reconfirming their influence: They have leadership in the

definition of the rules that govern the structure of the sector and in particular the

contents of the DOT laws. As shown by the current crisis, the international recognition

and the increase in sales at the national and international markets do not benefit the

different actors of the tequila supply chain equally. Farmers do not have control over a

4 The harvest of agave consists of cutting the leaves and keeping only the piña, centre of the plant that looks like a pineapple. 5Agaveros libres refers to free farmers who do not have any contract with distillery. 6 In the literature, tequila distilleries are also called “tequila companies”, “tequila firms”, or “industrials” as they are often involved in different “functions” in the tequila supply chain (bottling, agave plantations…).

Chapter 1. Introduction and literature review

14

?

Direct impact?

Growing power of the main Tequila

companies

DOT implementation and contents

Increasingly international tequila

market

Agreement with foreign investors

What is happening at farmer level?

? Indirect impact?

part of the production process and thus do not have access to the added value that the

DOT generates.

1.3. Research questions (figure 1.3)

Considering the context of the tequila sector, my research questions are the following:

1. What are the power relationships and the internal mechanisms in the tequila

sector that can explain why the DOT does not benefit to all supply chain’s actors

equally?

2. What ways out are being developed and what solutions are proposed to escape

the vicious cycle of price fluctuation7 and make agave farmers and small scale

distilleries benefit from the DOT implementation (or find profitable non-DOT

markets)?

3. What are the local responses of farmers and distilleries to the worldwide

recognition of tequila and, as more agave is needed, to the expansion of agave

plantations in a non-traditional region?

Figure 1.3: Representation of the problem statement and the research questions

7 See Appendix 5

Chapter 1. Introduction and literature review

15

1.4. Theoretical perspective

A sociological study can be seen from different angles depending on the scale of the

problem and the scale of analysis focused on. The very title of this report: “Who

benefits from the DOT?” has guided the theoretical approach that I used for this

research.

(i)Who?

To answer that question, the supply chain has to be analysed as well as the

relationships between each “level” of the supply chain. But in my opinion, it is not

sufficient. I consider that the actors of a food supply chain can not decide by

themselves on their future and determine how to “share” the benefits of a GI. Their

decisions are embedded in a global structure, which can be both:

- An institutional and political context and

- The international context of market globalization.

Thus, I distanced myself from the theory of social constructivism and came closer to a

Durkheimian perceptive (functional). This structural approach is relevant if one looks

at the major consequences of the recent changes in scale of tequila production,

response to the globalisation process of food products: the international context is a

structure that shapes the tequila supply chain. Besides, farmers’ initiatives are clearly

embedded in a structure, as the first thing they talk about is “the low price paid by

distilleries that control them” or “the government”. However, the concept of structure

has to be taken with precaution and should not be considered as something fixed and

invariable. Indeed, one of the biggest structural factors for farmers is the “price of

agave”. When the price is high, their bargaining power is more important and they are

less “victim” of the structure above them. In case of low price, the farmers can not do

anything; they are constrained by the structural factor “price”.

Analysing the eminent conflicts in the sector and how they can be solved was also

indispensable to understand the current situation. For that aspect, I came closer to a

Marxist approach.

(ii) Benefit

Asking the question “Who benefits” suggests by itself that there is an unequal division

of benefits. Indeed, the specific norms to follow and the delimitated production area

Chapter 1. Introduction and literature review

16

constitute a structure that can benefit the ones who are in and disfavour the ones who

are out. The concept of inclusion and exclusion is important to keep in mind when

studying a GI (Rodriguez, 2004, p171). But in the delimitated area itself there are

some inequalities, and particularly for what concerns the wide delimitated area of the

DOT. Distilleries and institutions are geographically concentrated in the Zona Centro,

which made it interesting to look at the tequila sector with the centre periphery theory.

The distinction centre and periphery is often used to describe opposition between the

two areas: the one which is commanding and benefiting (the centre) and the one that

are subjected to it (peripheries) (Hypergeo, 2004). The centre-periphery theory can be

used in many different ways (Gren, 2003). For this study, it was used at different

geographic scales:

- At the level of the supply chain, where distilleries are the “centre of decision”

excluding farmers by not considering their importance.

- At regional level, comparing what is happening in the “central region” around

Guadalajara (Zona Centro and Los Altos) with a peripheral area,

- In a less extend, at international level, as more multinationals are buying

tequila companies, which are relocating the DOT benefits from Mexico to the

“North” countries (the “centre”).

To think in terms of centre(s) and periphery(ies) allows thinking on interactions

between places (Hypergeo, 2004): In the tequila sector, farmers are dependant on

distilleries as they are the only buyers of their produce. Reciprocally, distilleries, even

if they keep farmers down, also need them. At the regional level: the centre region

needs the peripheries to expand agave plantations in time of plague (for example) and

the periphery depends on the “central region” for selling their produce and receiving

information. Between the two, there are asymmetrical flows (capital, information,

decision…). The centre is central precisely because it benefits from this inequality and,

in turn, the periphery(ies) is(are) characterised by a deficit which maintains its (their)

dominated position (Gren, 2003, p2). Whereas some peripheries may become

abandoned, others may benefit from their situation. The tequila domination does not

mean that all marginal other traditions are being eradicated. As Murdoch et al stated

(2000, in Renting et al 2003), the alternatives strategies found in “marginal areas”

(peripheries) is catching the attention of researchers in “alternative” or “quality” or/and

“local” food network.

Chapter 1. Introduction and literature review

17

1.5. Methodology

To integrate all structural factors, more than a supply chain analysis (which consists of

studying all actors involved in the production of a product and their relations), I carried

out a sectoral analysis, which is broader and which integrates “secondary actors” such

as governmental institutions, control body... But I also consider that current facts are

determined by what had been done before: The current situation of the tequila sector is

a result of historic facts and a result of how the sector and the relations between actors

have evolved in time. Understanding the history of the sector was then an

indispensable step before to start talking about possible solutions. According to the

theoretical perspective chosen and the research questions, my field work followed 3

main steps:

Step 1: Understanding how the tequila sector has evolved over the past century

(and why) and how that has structured the current situation.

Step 2: Once the context is understood (and particularly the cyclical character of

the crisis), analysing actors’ perspectives on the situation and their solution for the

future.

Step 3: Studying a particular “peripheral region” by looking at how the centre has

an impact on it and how they adapted.

To start with, a literature review of the tequila sector history was necessary (for step

1). By looking at how problems were solved in the past, one can have an idea of what

should be done in case of a similar problem in the present. Reversely, sometimes,

some attempts were made but did not work out: that could show which mistakes

should not been done again. It enabled me to conduct my field work while being

already aware of some difficulties and limits.

For step 1. and 2., I stayed 3 months in Guadalajara (the “central region”). Interviews

were conducted between February, March and May 2007 with different actors

Chapter 1. Introduction and literature review

18

3. Big distilleries Medium

6. CRT

5. Mexican Government

SEDER (State)

SAGARPA (Federal)

SE (secretaria de economia)

1. Farmers

NOM

Register the new brands

control

COYOTES 2. Farmers associations

Influence

IMPI PROFECO

4.

Small

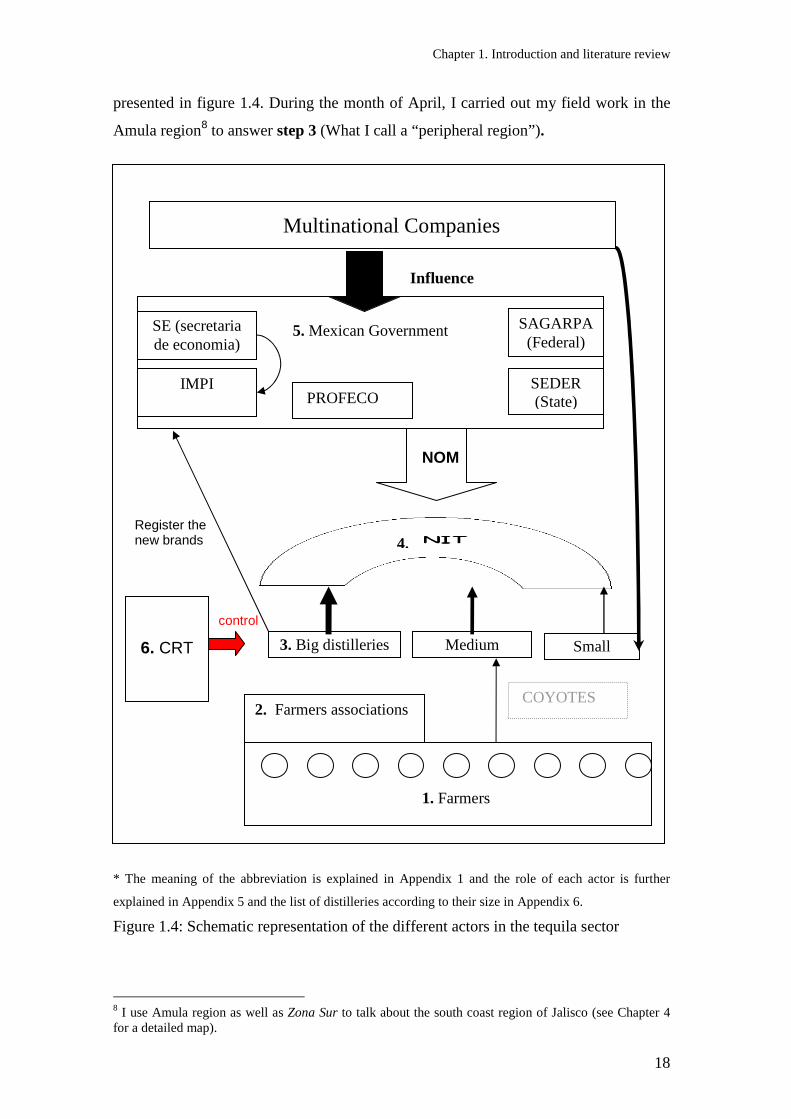

presented in figure 1.4. During the month of April, I carried out my field work in the

Amula region8 to answer step 3 (What I call a “peripheral region”).

Multinational Companies

* The meaning of the abbreviation is explained in Appendix 1 and the role of each actor is further

explained in Appendix 5 and the list of distilleries according to their size in Appendix 6.

Figure 1.4: Schematic representation of the different actors in the tequila sector

8 I use Amula region as well as Zona Sur to talk about the south coast region of Jalisco (see Chapter 4 for a detailed map).

Chapter 1. Introduction and literature review

19

Different data collection tools were used in the two regions:

- Focus group method (group discussion) with agave farmers

- Individual interviews with actors of the tequila sector (distilleries, Regulatory

Council, governmental institutions…)

The Focus group (FG) is a survey qualitative method appropriate to collect opinions or

attitudes of a group (of 7 to 10 participants) concerning a particular situation (IOWA

State University, 2004).

Collecting data from farmers via the FG method appeared to be appropriate as:

- It was relatively easy to gather 6 to 10 farmers to talk about a theme that

concerns them,

- The fact that they are all sharing the same problem facilitated the discussion,

- None of them was “scared” to talk or pressured by any hierarchical

relationships (as the groups were only constituted of farmers).

As far as other actors were concerned, individual semi-structured interviews were

conducted. This way, each actor could express his “real” opinion concerning the

current situation and the responsibility of other actors without having to take the

“institutional hat”. The detailed list of all the persons interviewed is in Appendix 7.

Bellow, the research process is further explained.

1.5.1. Getting information from distilleries and “institutional” actors

When I first arrived to Mexico, I had in mind the actors I wanted to interview but did

not know who exactly as it depends a lot on the willingness of each person to talk and

his availability. What I did first is get an interview with the director of the Consejo

Regulador del Tequila (Tequila Regulatory Council: CRT), Ramon Gonzalez, to get an

overview of the sector and its problematic. The CRT being in contact with every

distillery and with the governmental institutions, he could tell me who to interview

first and give me some names. Asking for a meeting saying that Ramon Gonzalez

advised me do to so, opened a lot of doors. At the end of my field work, I met Ramon

Gonzalez again to present him my findings and ask him some clarifications on certain

points.

Chapter 1. Introduction and literature review

20

In total, 25 interviews were conducted with actors from:

- Distilleries9 (3. in figure 1.4)

- Agave farmer associations (2. in figure 1.4)

- Tequila institutions (4. and 6.)

- Governmental institutions (5.)

- Academics

- Consumer representatives, tequila connoisseurs and liquor sellers

During each interview, different themes were raised (see Appendix 8 for the

questionnaire):

1. Organisation of the tequila sector in order to:

- Make clear who are the important actors

- Identify the relationships between them (In case of an interview of

distillery manager, questions relating to distillery’s strategy and its

relationships with farmers)

- Who determines the norm to follow to use the name tequila

- What are the current issues of the sector

2. Visions and opinions concerning:

- The cause of the crisis

- The solutions that could be developed against price fluctuation

- The solutions proposed by other actors (in order to confront different

perspectives and make people criticize each other)

- The product and local differentiation possibilities

3. To conclude:

- The impact of the DOT for the sector

- Perception of the future

Concerning the distilleries, the idea was to interview a representative sample of

distilleries in terms of size (total production) and strategy (focused on export or on

national market; type of product made: see Chapter 1, 2.3). According to the

classification of the Confederación Nacional de la Industria Tequilera (CNIT;

9 See Appendix 6; for the list of distilleries per size according to the production data from 2007.

Step 1

Step 2

Chapter 1. Introduction and literature review

21

National Confederation of the tequila industry), I interviewed or visited the distilleries

listed in the following table (figure 1.5). It would have been good to have interviewed

more micro distilleries to compare with the situation of micro-distilleries in the Amula

region (see Chapter 1, 5.3)

Big distilleries Medium distilleries Small distilleries Micro distilleries

Cuervo (V) La Cofradia (V) Tequila Partida Hacienda de Oro (V)

Sauza Cascahuin

Herradura

Casco Viejo

(V): only visited.

Figure 1.5: list of interviewed or visited distilleries.

Depending on the person that I interviewed, I adapted the questions. As much as

possible, I tried to make people talk about the others to understand the power

relationships (step 1). To do so, I could ask them to explain me again what I heard

from someone else or ask their opinion about the solutions proposed by other people.

Over the years, the norm to comply with in order to call the product tequila evolved. I

compared the different versions of the norm since 1949 and resumed the modifications

step by step in Appendix 12. The changes made have several “non rational” elements;

I enjoyed the interviews to ask the reasons for certain modifications or additions that I

considered “not logical”. When I got vague and variable answers, like “it’s political”

(what I often heard), it meant that I was on the right way to discover an interesting

element that would help understanding the “internal mechanisms” of the tequila sector.

After the individual interviews, I could have a clearer picture of how the sector

functions and its limits. That was an indispensable step before to start with farmers

interviews: the context had to be known to understand farmers’ perception and

strategies.

1.5.2. Getting information from farmers

As far as agave farmers were concerned, it was chosen to focus on the perception of

agaveros libres, independent farmers who sell agave on the open market (in opposition

to farmers who have signed a contract with a distillery that assures that their agave

Chapter 1. Introduction and literature review

22

plants will be bought). Indeed, they are the most hit by agave price fluctuation and are

the actors who need that a solution is found most urgently. It could have been

interesting to interview also farmers that have a contract with a distillery, but it would

have required some more time.

The idea was to interview agaveros libres from the 3 regions with most agave (Zona

Centro, Los Altos, Zona Sur). Before to start with a group interview, data concerning

the number of hectares and the experience in planting agave was asked, in order to

avoid bias. Indeed, farmers depending on these factors could respond differently to the

decrease in agave price and propose different solutions.

In total, 5 FGs were conducted:

- One with a group of 8 small agaveros libres from Tequila (Zona Centro)

- One with a group of 8 small agaveros libres from Amatitán (Zona Centro)

- One with 9 representatives of regional farmers association, all part of the

Confederación Nacional de Productores de Agave Tequilero (National

Confederation of Blue Agave Producers: CNPAT) in Guadalajara

- One with 4 agaveros libres of San Ignacio Cerro Gordo (Los Altos), all members

of the Consejo Nacional de Productores de Agave (farmers association of Los

Altos)

- One with 6 agaveros libres from the Zona Centro and Los Altos in Atotonilco

(Los Altos)

- One with 7 agaveros libres from La Cienega (Zona Sur)

Each FG lasted between 1 hour and 1 ½ hour, and the discussion subjects followed the

steps described underneath (the detailed questionnaire is in Appendix 9)

- Questions concerning the abundance crisis and the role of each actor in finding a

solution,

- Questions regarding their opinion about regional differentiation possibilities,

- Questions relating to their perceptive of the future and possible alternatives.

The discussions were recorded and transcribed in order to keep the exact words and

expressions of each participant. When possible, 2 persons10 organized the FG, one

10In the Zona Centro, 3 FG were conducted by Dra Ana Valenzuela and myself. The other 2, I organized them by myself. The FG in Autlán was organized by Dr Peter Gerritsen and myself.

Chapter 1. Introduction and literature review

23

responsible for leading the discussion and the other responsible for writing down each

detail that could not be recorded (like group reactions to a particular question, facial

expressions…). Unfortunately, at the date of writing this report, only 1 focus group

had already been transcribed. However, I could remember the key ideas of the other

FGs and use the findings (not optimally though) for this report.

1.5.3. Getting information from micro distilleries and “mezcal” traditional

distilleries

To respond to step 3, some local distilleries in a region with a mezcalera tradition

were interviewed. In total, eight individual interviews were conducted. The idea was to

meet a representative sample11 of regional distilleries depending on their size, types of

product, and time in the industry. Contrary to the methodology used for the tequila

distilleries in the “central region” (referring to 1.5.1.), I chose to do fewer but more in

depth interviews. Out of the eight distilleries visited, I spent more time with 3 of them.

By building a friendly relationship, I could collect more detailed information and grasp

their “sincere” opinions. I selected these 3 persons depending on their willingness to

talk and to share their experience with me, the specificity of their story, and their

geographical proximity.

After collecting this data, I interviewed a representative of the local office of

Secretaría de Agricultura, Ganadería, Desarrollo Rural, Pesca y Alimentación

(Ministry of Agriculture, Breeding, Rural Development, Fisheries and Food supply;

SAGARPA) and the CRT (for the second time). These 2 interviews enabled me to

confront them with my findings and to avoid risk of having a “one sided” analysis.

Extrapolation

My aim is to present some answers and visions of people and in that sense, these local

results can not be used to draw general conclusions about local consequences of the

recent evolution of the tequila sector, but can enable to assess deeper understanding of

what can be the impact of a (large) GI protected area.

11 To choose the sample, I was helped by Rodolfo Gónzalez, assistant researcher of Peter Gerritsen, who had visited each distillery and collected general data (year of creation of enterprise, number of litre produced, type of product…). He also advised me on whom to interview preferentially.

Chapter 1. Introduction and literature review

24

Tequila regulatory framework

1949 The first norm for tequila is published in the Diario Oficial 1958 Mexico signs the Lisbon agreement 1974 Tequila become a Denominacion de origen 1977 The name tequila became an intellectual property and is inscribed in the international register of denominations of origin in Geneva, Switzerland. 1994 The CRT is created 1994 DOT is recognized by Canada and the U.S. via the NAFTA 1997 Europe recognizes the DOT

The following section aims at presenting the context, regulatory in a first time and

historical, in a second time, in which the strategies of agave farmers as well as the

decisions of every actor are embedded.

2. Tequila regulatory framework

Figure 1.6 resumes the main step of the tequila regulatory framework.

Figure 1.6: Resume of the tequila regulatory framework

2.1. Towards a DO

Definition of GI and DO

The World Trade Organization (WTO), in its Agreement of Trade-Related Aspects of

Intellectual Property Rights (TRIPS), defines GIs as

“Indications which identify a good as originating in the territory of a Member, or a region or locality in that territory, where a given quality, reputation or other characteristic of the good is essentially attributable to its geographic origin.” (Art. 22.1)

The 31st of October 1958, 25 countries from the “Union for the protection of the

industrial property” (Mexico is part of it) met to come to a definition of “appellation of

origin” (Denominacion de Origen in Spanish). In Article 2, an appellation of origin

was defined as follows:

The “geographical name of a country, region, or locality, which serves to designate a product originating therein, the quality and characteristics of which are due exclusively or essentially to the geographic environment, including natural and human factors”

Chapter 1. Introduction and literature review

25

Such a name has to be registered by the WIPO (World Intellectual Property

Organization) in Geneva.

A DO is a specific kind of geographical indication used on products that have a

specific quality “exclusively or essentially due to the geographical environment”. It

constitutes a “legal framework” that regulates the supply chain of a geographically

embedded product and brings the security of the product origin.

From the 1970s, tequila started to be known worldwide. Its growing popularity made it

interesting for illegal opportunists to try to imitate the Mexican drink: There were

more than 30 brands of “tequila” from Spain, trying to give it an image as “Mexican”

as possible (Brands like “Taxco”, “Cuate”, and “Pachuca”…) (Blomberg, 2000, p127).

It happened also in Japan, where a company started to sell a drink made of rice and

maize under the name “Tequila Morozoff”. In order to protect tequila from worldwide

competition by imitation, tequila distilleries started to claim the right to a DO as

tequila corresponded with the definition established since:

- Tequila is the name of the volcano and the village where people have been

planting blue agave for decades,

- There is a tradition of producing a distilled drink from agave only in this

specific region,

- This drink is embedded in local culture, in costumes, in music, in folklore…

(Blomberg, 2000, p127).

Nevertheless, it is interesting to note that none of the arguments justify the

“characteristics of which are due exclusively or essentially to the geographic

environment”. That is one of the main weaknesses of the DOT. It is further explained

in Chapter 2, 2.1).

Declaración General de la Protección a la Denominación de origen “tequila”

Mexican tequila finally became a DO in 1974. For being an Appellation of Origin, the

name “Tequila” belongs to the Mexican State who grants its use to those persons or

companies involved in the production of this beverage, through clearly defined

regulations to protect its prestige. The Declaración General de la Protección a la

Denominación de Origen “tequila” (Declaration of Protection of the Appellation of

Origin Tequila) was published in the Diario Oficial de la Federación (Official Federal

Chapter 1. Introduction and literature review

26

Journal) the 9th of December 1974. The 13th of October 1977, the name tequila became

an intellectual property owned and controlled by the Mexican government and was

inscribed in the international register of DO in Geneva, Switzerland.

The Declaration basically establishes the protected territory where both the cultivation

of the tequilana Weber blue variety Agave and the production process of the beverage

must take place (see Appendix 4). As for the rest of the characteristics and

requirements that the production of the beverage must meet in order to bear the name

“Tequila”, the Declaration refers to the Official Standard that the Federal Government

has issued for the beverage which presently, is NOM-006-SCFI-2005 Alcoholic

Beveraged-Tequila-Specifications.

With time, the Declaration has suffered a few changes aimed toward adjusting the

demarcation of the protected territory (inclusion of some municipalities of the State of

Tamaulipas in 1977, see Chapter 2, 2.1).

International recognition of the DOT

At international level, the DOT was recognized bilaterally by countries like the U.S.,

Canada and the European Union, as well as by the WTO in matters of observance of

intellectual property rights. With the signing of NAFTA12 the 1st of January 1994,

Canada and the U.S. recognized the DOT, as written in the NAFTA, Part Two,

Chapter 3, Appendix 313-3:

“Canada and the United States shall recognize tequila and mezcal as distinctive products of Mexico. Accordingly, Canada and the United States shall not permit the sale of any product as Tequila or Mezcal, unless it has been manufactured in Mexico in accordance with the laws and regulations of Mexico governing the manufacture of Tequila and Mezcal. This provision shall apply to Mezcal, either on the date of entry into force of this Agreement, or 90 days after the date when the official standard for this product is made obligatory by the Government of Mexico, whichever is later”.

Besides, the European Union endorsed the DOT the 27th of May 1997. Mexican

authorities and distilleries are now working towards a recognition of the DOT by other

countries in Asia, Africa and some countries of Latin America. South Africa is indeed

12 The NAFTA called off the majority of tariffs between products traded among the US, Canada and Mexico, and gradually phased out other tariffs over a 15-year period. The treaty also protected intellectual property rights so amonst them the DOT (wikipedia).

Chapter 1. Introduction and literature review

27

the country with the most important case of production and distribution of

“speudotequilas”13, and in particular one named “Hacienda”. Figure 1.7 shows the role

of different national and international actors in terms of DOT regulation.

Source: Gonzalez, 2002.

Figure 1.7: Principal actors of the tequila regulatory framework

Evolution of the norm regulating the quality of tequila

The norm to comply with to use the name tequila is published by the Dirección

General de Normas (Norms General Direction), part of the ministry of economy. It is

called a Norma Oficial Mexicana (NOM; Mexican Official Norm). It is agreed upon

by different parties: Government, tequila companies, the CRT, Instituto Mexicano de

la Propiedad Industrial (Mexican Institute for Industrial Property: IMPI), Distilled

Spirit council of the U.S. (since 1997). It defines the conditions of production, bottling,

and commercialisation that refers to the DOT as well as all the rules, characteristics

and specifications which all the authorised entities need to comply with.

13 Even if the DO is not recognized by South Africa, a procedure can occur against illegal South African producers through the WTO (Blomberg, 2000, p130).

Chapter 1. Introduction and literature review

28

2.2. Main requirements of the DOT

Raw material

According to Flores and Zamora (2003, p10), 273 species of the family Agavaceae14

were described in the American continent. In Mexico, 205 species are registered, from

which 151 are endemic to the country. As defined in the NOM, tequila is a product of

blue agave (Agave tequilana Weber), which differentiates it from other licor de agave

(agave liquor) like sotol15 and mezcal (see Chapter 4) and from other products

localized in micro areas (like raicilla in West Jalisco for example).

Area of production

To be called tequila, the distilled product has to bee made of agave from the DOT

delimitated territory and since 2006, the number of agave planted should be inscribed

in a register controlled by CRT (according to the NOM-006-SCFI-2005). The territory

of the DOT is constituted by the entire State of Jalisco (124 municipalities), 9

municipalities in the State of Nayarit, 7 municipalities in the State of Guanajuato, 30

municipalities in the State of Michoacan and 11 in the State of Tamaulipas (only since

1977). It represents approximately 11.8 million hectares, of which only 3 % is

dedicated to the cultivation of blue agave (CNIT, 2004). But Jalisco concentrates about

92% of agave planted in the zone of DOT (see Appendix 13, figure 1) and 99% of the

firms producing tequila16.

Since the last 10 years, the Zona Sur of Jalisco has emerged as an agave cultivation

centre, although the production in the Zona Centro and Los Altos is still greater. In

2000, 8% of agave in Jalisco was grown there (CRT, 2006) (Appendix 13, figure 2).

14 Contrary to common belief, agave plant is not a cactus. 15 It is known as the drink of Chihuahua. There are few commercial examples available. It is produced in a manner similar to the more common artisanal “mezcales” of central Mexico. 16 According to the CNIT, in 2005, there were 120 distilleries and it employed 38,000 persons (CNIT, 2005).

Chapter 1. Introduction and literature review

29

100% Agave

Tequila mixed

Joven o oro (gold)

Bottled in production site in the

DO zone

¾ exported in bulk

Reposado (rested)

Añejo (aged)

Joven o oro (gold)

Blanco (silver)

Extra Añejo (extra aged)

Reposado (rested)

Añejo (aged)

Blanco (silver)

Extra Añejo (extra aged)

2.3. Product differentiation possibilities in the scope of the DOT

The current product differentiation of tequila only refers to the aging process in oak

barrels and the relative quantity of blue agave sugar: minimum 51 % (see figure 1.8

and figure 1.9).

Figure 1.8: Tequila categories

Figure 1.9: Different kinds of tequila depending on the time in oak barrels.

Dilution with water

Tequila blanco Tequila reposado Tequila añejo extra añejo

1 year 3 years 2 months 0

Tequila joven

2 Categories

5 Types 5 Types

Chapter 1. Introduction and literature review

30

Figure 1.10: Different part of a label (based on information from Jaime Villalobos)

On the label, the indication “100% agave” is put for tequila made of 100% agave sugar

(Figure 1.10). As far as “mixed” products are concerned, they are called “tequila” and

nothing informs about the percentage of agave sugar. This precision is important and

explains why consumers are actually not aware that the “tequila” they drink is actually

a “mix17”.

Concerning the differentiation relating to the time in oak barrel, there is 7 different

sorts of tequila and 2 categories (figure 1.8). But it could be a lot more if the time in

oak barrels would be indicated. For example, nothing differentiates a reposado of 2

months and a reposado of 6 months: A consumer can not understand the price

difference between these 2 products. However, the new category “extra añejo” (since

2005) is a step forward in product differentiation. Indeed, instead of calling a product

“Premio” because it is above a certain price (what was done before), the differentiation

is taking into account the time in oak barrel.

The NOM also allows certain additives to soften and smooth the taste of tequila:

caramel colouring, oak wood extracts, glycerine as well as corn sugar syrup. Tequila

with such additives is called abocado. Tequila could also be differentiated depending

17 According to the norm for tequila, what is called “tequila” is a product that can be made with a minimum of 51% of blue agave sugar. Officially, I do not need to give the precision “mixed”, but for more clarity and a better distinction, I will use “mixed” tequila to differentiate it from tequila 100% agave (that many actors consider as the “real” tequila).

Type of tequila

NOM indication, sometimes added on the bottle as a

sticker (for licor de agave, see Chapter 4.4.4.)

Registered trademark

Word tequila

Net content

Cathegory TEQUILA

TEQUILA 100

Percentage of alcohol “ % Alc. Vol ”

Chapter 1. Introduction and literature review

31

on the production methods (traditional or more industrial) as well as by recognizing

the differences between areas of production by considering the natural and physical

properties of an area (see Chapter 5, 4).

3. Evolution of the tequila sector since the last century

The structure of the tequila supply chain is a result of political changes (more

capitalist, more open to international market) and social struggles between farmers and

tequila distilleries. The following part is a historical overview. The objective is to

present the organization of the tequila sector in order to comprehend the relationships

between each actor and the eminent conflicts between the different parties. To

understand the changes in the tequila sector during the last century, it is chosen to

divide this part in 3 periods relating to the consequences of land redistribution in a first

time (1910-1970), the increase in export and the modernisation of distillation

equipment (1970-1990), the current change of scale of the sector and its consequences

(1990-now).

3.1. Land redistribution: a major setback for tequila distilleries

From big haciendas to small plots of land

In the 18th and the 19th century, the now largest and most influential tequila distilleries

(Cuervo, Sauza, and Herradura) were established by owners of large haciendas18. They

were self-sufficient in their supply of agave (Limón, 2000). Thus, a large part of land

was cultivated with blue agave in the Amatitán-Tequila valley. After the Mexican

revolution of 191019, a land reform took place; the government divided and

redistributed the land to farmers. Groups of villagers were able to request allowances

of expropriated land, thus creating an ejido20. The State retained ownership of the land

18 It is a large landholding which usually includes absentee ownership, a large resent labour force, an administrator, on extensive rather intensive agriculture. 19 Prior to 1910, approximately 260 families owned 80% of the Mexican territory (Young, 2002). 20 An ejido is a group landholding unit established after the Mexican revolution. It is cultivated by ejidatarios. Although the 1992 amendment to article 27 of the Mexican constitution legalized the rental and sale of previously inalienable ejido land, a large proportion of smallholders in Mexico are still organized into ejidos (Valenzuela, Bowen, 2006, p4).

Chapter 1. Introduction and literature review

32

but villagers (known as ejidatarios) were given the right to farm, either collectively or

through designation of individual plots of land (Bowen, Valenzuela, 2006, p3).

Land redistribution occurred principally in the central part of Jalisco (Regalado, 1988,

p116).The haciendas of Tequila, Amatitán and Arenal were redistributed into 30

ejidos21 (Bowen and Valenzuela, 2006, p3/p10). It was a major setback for large

companies became dependent on ejidatarios for their supply of agave while the

ejidatarios often chose to plant basic crops such as maize that they could use for their

own consumption. In addition, as blue agave plantations require an important initial

investment and a long time before the paybacks, it presented little advantage. It

resulted in the emergence of new actors (intermediaries, explained further) and new

power relationships between farmers and distilleries (Luna, 1991, p127-129).

Consequently, the first important shortage occurred: Between 1900 and 1940, the

number of agave decreased by 74 million plants to only 4 million plants (Luna, 1991,

p133).

A growing demand of tequila in the U.S. and its consequences

After the Second World War, there was an important international demand of tequila

(and particularly in the U.S.) while there was little tequila produced. From 21,000

litres exported in 1940, it reached 4 million litres in 1945 (Luna, 2003, p2). To protect

tequila quality and prevent it from adulteration, the first tequila norm, the DEN-R-9,

was published by SECOFI in the Diario Oficial in 1949. According to this norm,

tequila had to be made of 100% blue agave and forbade any mixing with alcohol

derived from other sugars.

From the 1960s onward, the demand in national and international market increased

even more (Luna, 2003, p2; Gonzalez, 2003, p31). In the U.S., the main international

market of tequila (especially California and New Mexico), the cocktails “Margarita”

and “tequila sunrise” became popular and tequila export to the U.S. represented 60%

of tequila imported in the country (Expensión, 12 of July 1972). Thus another scarcity

of agave occurred which had four principal consequences (Llamas, 1999, p12). 21 In Amatitán were given 6,989.75 hectares were given to 308 ejidatarios; In Arenal, 5,480 hectares were given to 439 ejidatarios received and in Tequila, 11,765.94 hectares were redistributed to 594 ejidatarios (Regalado, 1988, p212-213), which means respectively 33%, 30% and 8% of the total surface of the municipality (Santiago, 2004). Appendix 10 gives an overview of the land tenure system in Mexico.

Chapter 1. Introduction and literature review

33

i) Reduction of tequila quality

First, it led distilleries to ask to the Congreso Federal (Federal congress) a

modification of the authorised amount of agave sugar allowed to produce tequila.

Therefore, the norm DGN-R9-1964 was published in the Diario Oficial the 12th of

March 1964 allowing the introduction of 30% other sugars in tequila production

(Luna, 2003, p2). The same situation happened in the 70s: as the demand was

increasing more than the number of agave planted, it resulted in new negotiations

between industrials and the State to a reduction of blue agave sugar to 51%. This norm

(DGN-V-7-1970) was published in the 5th of December 1970.

ii) Credits available for agave farmers

Secondly, distilleries solicited banks to open credits for ejidatarios cultivating agave

as they needed financial support to cover the cost of planting and to subsist during the

period between planting and harvest (Valenzuela, Bowen, 2006, p9; Luna, 2003, p2).

From 1968, the Banco Nacional de Crédito Agricola (National Bank for credits for

agriculture) and the Banco Nacional Agropecuario (National Bank for farming) did so,

but these credits were very low and insignificant since these institutions were also

providing credits for more basic crops (according to the agro-alimentary policy of the

State). So, distilleries had to start looking for other ways to control ejidatarios (Torres,

1998). It often took the form in financing contracts22, where they provided credits

themselves and gave the insurance to buy from the contracted ejidatario. It helped the

cultivated surface of agave to increase from 11 million plants in 1960 to more than 57

million in 1970 (Luna, 1991, p173; Luna, 2003, p3). The problem was (and still is)

that distilleries usually first asked farmers to lease their land to them before

considering having another type of contract that could benefit more to farmers

(Gonzalez, 2002, p10; Llamas, 1999, p13).

iii) Development of intermediaries for the purchase of agave

Not all ejidatarios decided to sign a contract with tequila companies. Some decided to

stay independent for different reasons (lack of trust, will to keep on farming and not

only leasing land…see Chapter 3, 3.2), but the outcome was that they could not sell

their produce directly to tequila companies: Seeing that some farmers preferred to stay

independent, some distilleries developed a network of middlemen (also called

22 Luna gave an example of a contract (1991, p 157-ss) : 70% of the benefits for the distillery or the financial intermediary and 30% for the farmer.

Chapter 1. Introduction and literature review

34

intermediaries or coyotes) whose role was to buy large quantities of agave. The

objective was to exclude agaveros libres from the production process. Indeed,

intermediaries pay less for agave (actually they control the price) than when agave

farmers sell their produce directly to distilleries (Valenzuela, Bowen, 2006, p6).

iv) Abundance and price decline

In 1976, the price of agave started to fall because many agave plants were mature.

Thus, some farmers of the municipality of Amatitán created the Union de Productores

e Introductores de Mezcal Tequilero del Estado de Jalisco (Union of Producers and

Introducers of Mezcal23Tequilero of the State of Jalisco). It was the first union of blue

agave peasant farmers created to counterattack intermediaries. Helped by the

Dirección Nacional de la Confederación de Trabadores de Mexico (National Direction

of the Mexican Workers Confederation), they blocked 22 distilleries during 3 days in

Tequila; the blockade of the distilleries of Cuervo and Sauza lasted 22 days. They

managed to increase the price of agave (from 60 to 90 centavos per kilo), and to be

officially recognized by distilleries as a group via which the purchase of agave should

be negotiated (Llamas, 1999, p13; Luna, 1991, p181). But in 1989, it was broken up

into many local associations incapable of integrating themselves into one homogenous

organization (González, 2002, p33).

3.2. The international development of tequila and its consequences

From the 1970s, distilleries had more difficulties to face the increase in international

demand with their “traditional” production methods. Hence, they started to modernize

their distillation and bottling equipment to be able to export more. Besides, major

international firms started to get involved in the tequila sector by making agreements

such as trading partnership (As the company Cuervo who has a commercial alliance

with Diageo) or ownership, (as it is the case for the company Sauza which is owned by

Pedro Domecq) bringing capital and new technologies to tequila distilleries (Gonzalez,

2002, p18; Goddard, 1998, p7). According to El Análisis (economic newspaper) of

October-November 2006, only 60% of the total tequila production is still in hands of

Mexican companies. The most important and recent acquisition was at the end of

2006, when the company Herradura was bought by the U.S. company Brown Forman.

23 Mezcal is a term that can also be used as a synonym of agave plant. It is the case here.

Chapter 1. Introduction and literature review

35

As it provides international distribution channels, cooperating with international

companies has also the advantage to open the door of the international market

(González, 2002, p24): Tequila export jumped from 14% of the total production in

1970 to 58% in 2006 (Goddard, 1997, p3; Gonzalez, 2002, p18; CNIT, 2006; CRT,

2007). However, with the capital that multinationals can invest in marketing,

advertisement or innovation, it closes market segments and distribution channels to

smaller companies and concentrates even more the capital in hands of the biggest

distilleries.

3.3. From the 1990s: Change of scale and its consequences

The tequila golden years for industrials

In the early 1990s, a fungal infection24 struck agave. Therefore, tequila companies

started to initiate plantation in other non affected areas (the Amula region is one of

them).

In the late 1990s, the future looked better then ever before for tequila distilleries. The

demand for tequila increased considerably both in the international market and in the

national market (Bowen, Valenzuela, 2006, p6). Besides, as there was abundance, raw

material price was quite low, and new distilleries started up (see Appendix 11).

Tequila production rose by 74% from 104,3 to 190,6 million litres between 1995 and

1999 (Gonzalez, 2001, p21).

But for agave farmers, abundance means losing any negotiation power. During the

important abundance of the 90s, as they did not have a strong representative

organization able to defend their interests, agave farmers petitioned El Barzón25, a

social movement that arose due to the economic crisis in the Mexican countryside, in

order to have a strong representative organization able to defend their rights. Rene

Beas, one of the directors, agreed and in May 1995, El Barzón del Agave was created

24 Fusarium oxisporum was accompanied by a bacteria called erwinia caratavora, the pair raging through plantations. A 1997 survey conducted by the CRT estimated that 27% of the country's agave crop was infected with at least one of the diseases. Many farmers and scientists said that figure was actually much higher (Chadwick, 2004) 25 El Barzón AC : Union Nacional de productores agropecuarios, comercantes, industriales and prestadores de Servicio (Nacional Union of agricultural and livestock producers, merchants, industrialist and service labourers) was created as a result of the Mexican economic crisis of 1994. It is officially registered as a civil association.

Chapter 1. Introduction and literature review

36

(Gonzalez, 2002, p36). Its objective was to improve the situation of agave farmers by

avoiding intermediaries and by doing so that agave could be bought at a reasonable

price (In the beginning of 1999, the price even went down to 0.85 cents per kilo)

(Luna, 2003, p4).

The worst agave shortage in history and its consequences

In the 1990s, a few unfavourable factors interfered. Because of a few people planted

agave as price was the low and because of an early winter frost took place in 1997, it

resulted in the most devastating shortage in history (Gonzalez, 2003, p38). From 1997

to 2000, blue agave plants decreased by 50.7 % (Bowen, 2004, p12). The shortage was

accentuated also due to a skyrocketing demand, caused mainly by the recognition of

the DOT (and other Mexican DO) by the U.S. and Canada, with the NAFTA (North

American Free Trade Agreement) in 1993 and by the European Union in 1997. The

price of agave rose to more than 14 pesos26 per kilogram in 2000 and smallholders

with mature plantations became rich overnight (Martinez et al, 2003, p5). This

shortage lasted till 2003, and had major consequences for the tequila sector and for the

region:

i) Farmers from other regions starting to plant agave

Blue agave was first produced in the Zona Centro and in Los Altos but in the end of

the 1990s, a lot of farmers from other regions started to plant blue agave, as the price

at that moment made it an attractive crop. In addition, the CRT assessed that the area

planted with agave should be increased to 100,000 hectares to face the rising demand

(Ruiz-Corral et al, 2000; in Martinez et al., 2003). The Zona Sur of Jalisco (Amula

region) is one of them (Chapter 4).

ii) Intent to decrease the amount of agave sugar in tequila

In 2000, a repetition of the events in the mid-1960s took place: tequila distilleries

proposed another reduction of agave sugar proportion to 30%, but the government did

not accept it, since it would have led to a political scandal and would have damaged

the reputation of tequila (Luna, 2003, p3).

26 1 euros= 13 pesos

Chapter 1. Introduction and literature review

37

iii) Reduction of possibilities for small distilleries (Macias Macias, 2001, p64).

When the price is so high, small distilleries can not compete with big distilleries in

terms of price and many are constrained to close. That is what occurred during the last

scarcity. However, as Luna argued (1991), it is still surprising to see the capacity and

the maintenance of small and medium size distilleries.

Start of a period of extreme abundance

By 2006, a new phase of abundance started and the price of agave dropped to 0.5

pesos to 2.5 pesos, which is below production costs (estimated at 2.55 pesos per kilo

by the CRT in 2005). In May 2007, the price was around 1 peso. Agave farmers have

difficulties selling their produce and are searching for alternative solutions or more

precisely, they expect the government to take measure.

3.4. Recent chance of political party and its consequences

In Jalisco, policies changed quite a lot since 1994, when the PAN (Partido de Acción

Nacional27) was elected in the government of the State (Jalisco) and replaced the PRI

(Partido Revolucionario Institucional)28. From very paternalistic, the policies have

changed to more participatory, where farmers are considered as “entrepreneurs”. At

federal level, the PAN arrived in the government in 2000. As explained by a

representative of the Secretaría de Desarollo Rural (SEDER: Rural Development

Ministry of Jalisco), the change is being done slowly to more participatory policies, (as

farmers still receive previous subsidies such as PROCAMPO29) “but peasant farmers

don’t like that change”. Now, supports are provided to farmers that are organized and

that are carrying a project. But for each project, it requires an important initial

investment which can be a limiting factor. The change from top down to bottom up

policies in a country where people are not “used to” take initiatives and to organize

themselves after more than 40 years of PRI will need some time before to be accepted

27 National action party. PAN is a political party right orientated. http://www.pan.org.mx/?P=12. 28 Institutional revolutionary party. PRI is a political party left orientated. http://www.pri.org.mx/estadetulado/index.html 29 PROCAMPO is a program of direct subventions (per hectare) for farmers that the Federal State provides via SAGARPA. It was implemented in 1993 and its primary objective was to compensate national farmers for the subsidies that farmers from other countries receive. Once the plots of land are registered, no matter that is being planted. http://www.aserca.gob.mx/artman/publish/article_183.asp.

Chapter 1. Introduction and literature review

38

and to have a real impact. To stimulate people to “participate in the construction of

their future30”, the government is organizing different forums of public consultancy.

The large area with DOT is a result of power influences that are in place in the tequila

sector. After a literature overview to present the regulatory and historical context,

analysing these internal mechanisms and the power relationships in the past and now is

the first step to understand why the sector was shaped so that distilleries are those who

benefit from the DOT. It is particularly the case in times of crisis when farmers can not

sell their agave because of abundance, one of the consequences of the fact that there is

no “regulation” to plant agave. The second part is dedicated to analyse what solutions

can be developed to solve the problem of price fluctuation. Another point comes out

when talking about the large area with DOT. What is happening in a “peripheral

region” and more particularly what are the local responses to the “political” decision

that is the implementation of the DOT, and to which extend is it different from what

has occurred in the “central region”?

30 Expression taken from TV advertisements of the government.

Chapter 2. Power relationships and internal mechanisms in the tequila sector

39

Chapter 2.

Power relationships and internal mechanisms in the tequila sector

1. Introduction

Often, the best questions come from an outsider’s point of view. The 4th of March 2007,

the IMPI had the visit of Mpazi SINJELA, Doyen of the world academy of the WIPO.

In order to give him a recorrido (round) of the agave landscape classified as worldwide

patrimony of the UNESCO, a trip to Tequila was organized with some stops to admire

the view. During one of them, Mpazi SINJEL asked 2 questions to Theodore Schultz,

director of the IMPI:

M. SINJEL:“It is incredible all these plantations of blue agave…it is wonderful. But, are they all registered to be raw material for tequila?” T. Schultz: “Heu…yes, they are”.

It is true that all blue agave plants can be used for tequila production, but if the

plantations are “registered”, that is another question (see Chapter 3, 3.1)

M. SINJEL: It is so immense… and behind these mountains over there, that is not an area where agave can be produced, is it? T. Schultz: Heu… Yes, it is. The delimitated area goes to the coast even. M. SINJEL: Oh really?

These two questions revealed the two main weaknesses of the DOT:

- The large area that was granted the DOT,

- The non-existence of a proper regulation for planting agave.

To understand the logic behind the DOT regulations and the limits of the tequila sector,

it is indispensable to first get a clear vision of each actor’s role and the existing power

relationships. This part presents the institutional context and the internal mechanisms1

which can demonstrate who benefits from the DOT.

The internal mechanisms can not only be perceived by doing interviews. Each actor has

his own vision, his own version and interpretation of the reality. Often even, this reality

1 By internal mecanisms, it is meant the role of each actor in the decision making process, and particularly in the NOM modification process and the DOT rules.

Chapter 2. Power relationships and internal mechanisms in the tequila sector

40

is simplified at his advantage, which makes it difficult to stay objective and to

understand what really happened. Each time, a bit of the truth is hidden; my task was