ACADIANA CRIMINALISTICS LABORATORY COMMISSION FINANCIAL REPORT DECEMBER 31, 2005 Under provisions of state law, this report is a public document, Acopy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and. where appropriate, at the office of the parish clerk of court. Release Date Q '"P-O £>

Transcript

ACADIANA CRIMINALISTICS

LABORATORY COMMISSION

FINANCIAL REPORT

DECEMBER 31, 2005

Under provisions of state law, this report is a publicdocument, Acopy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and. whereappropriate, at the office of the parish clerk of court.

Release Date Q '"P-O £>

C O N T E N T S

Exhibit

INDEPENDENT AUDITORS' REPORTON THE FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTSStatement of net assetsStatement of activities

FUND FINANCIAL STATEMENTSBalance sheet - governmental fundReconciliation of the governmental fund

balance sheet to the statement of net assetsStatement of revenues, expenditures, and

changes in fund balance - governmental fundReconciliation of the statement of revenues,

expenditures, and changes in fund balance ofthe governmental fund to the statement ofactivities

REPORT ON INTERNAL CONTROL OVER FINANCIALREPORTING AND ON COMPLIANCE AND OTHERMATTERS BASED ON AN AUDIT OF FINANCIALSTATEMENTS PERFORMED IN ACCORDANCE WITHGOVERNMENT AUDITING STANDARDS

Schedule of findings and questioned costs

Schedule of prior findings

Page

1 and 2

AB

C

D

E

G-lG-2

10

11

12

1314 - 21

2425

H-l

H-2

27 and 28

29

30

- i -

Other Offices:

Crowley, LA(337) 783-0650

Opelousas, LA(337) 942-5217

Abbeville, LA(337) 898-1497

New Iberia, LA(337) 364^554

Church Point, LA(337) 684-2855

Herbert Lemoine II, CPA*

Frank A. Stagno, CPA*

Scott J. Broussard, CPA*

L. Charles Abshire, CPA*

Kenneth R. Dugas, CPA*

P. John Blanche! Ill, CPA*

Craig C. Babineaux, CPA*

Peter C. Borrello, CPA*

George J. TVappey III, CPA*

S. Scott Soileau, CPA*

Patrick D. McCarthy, CPA*

Martha B. Wyatt, CPA*

Troy J.Breaux, CPA*

Fayetta T. Dupre, CPA*

Mary A. Castffle, CPA*

Joey L, Breaux, CPA*

Terrel P. Dressel, CPA*

Craig J. Viator, CPA*

BROUSSARD, POCHE, LEWIS & BREAUX, L.L.R

Retired:

Sidney L. Broussard, CPA 1925-2005

Leon K. Poche, CPA 1984

James H. Breaux, CPA 1987

Erma R. Walton, CPA 1988

George A. Lewis, CPA* 1992

Geraldine J. Wimberley, CPA* 1995

Larry G. Broussard, CPA* 1996

Lawrence A. Cramer, CPA* 1999

Ralph Friend, CPA* 2002

Eugene C. Gilder, CPA* 2004

Donald W. Kelley, CPA* 2005

C E R T I F I E D P U B L I C A C C O U N T A N T S

4112 West Congress • P.O. Box 61400 • Lafayette, Louisiana 70596-1400

We have audited the accompanying basic financial statements ofAcadiana Criminalistics Laboratory Commission as of and for theyear ended December 31, 2005, as listed in the table of contents.These financial statements are the responsibility of theCommission's management. Our responsibi1ity is to express anopinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standardsgenerally accepted in the United States of America and thestandards applicable to financial audits contained in GovernmentAuditing Standards, issued by the Comptroller General of the UnitedStates. Those standards require that we plan and perform the auditto obtain reasonable assurance about whether the financialstatements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimatesmade by management, as well as evaluating the overall financialstatement presentation. We believe that our audit provides areasonable basis for our opinion.

In our opinion, the financial statements referred to above presentfairly, in all material respects, the financial position ofAcadiana Criminalistics Laboratory Commission as of December 31,2005, and the results of its operations for the year then ended, inconformity with accounting principles generally accepted in theUnited States of America.

The Commission has not presented Management's Discussion andAnalysis that accounting principles generally accepted in theUnited States of America has determined is necessary to supplement,although not required to be part of the basic financial statements.

Members of American Institute ofCertified Public AccountantsSociety of Louisiana CertifiedPublic Accountants

*A Professional Accounting Corporation- 1 -

In accordance with Government Auditing Standards, we have also issued our report datedJune 14, 2006, on our consideration of Acadiana Criminalistics Laboratory Commission'sinternal control over financial reporting and our tests of its compliance with certainprovisions of laws, regulations, contracts and grant agreements and other matters. Thepurpose of that report is to describe the scope of our testing of internal control overfinancial reporting and compliance and the results of that testing and not to providean opinion on the internal control over financial reporting or on compliance. Thatreport is an integral part of an audit performed in accordance with Government AuditingStandards and should be considered in conjunction with this report in considering theresults of our audit.

Our audit was made for the purpose of forming an opinion on the basic financialstatements taken as a whole. The budgetary comparison information listed as requiredsupplementary information in the table of contents is presented for purposes ofadditional analysis and is not a required part of the basic financial statements ofAcadiana Criminalistics Laboratory Commission. Such information has been subjected tothe auditing procedures applied by us in the audit of the basic financial statementsand, in our opinion, such information is fairly stated in all material respects inrelation to the basic financial statements taken as a whole.

Lafayette, LouisianaJune 14, 2006

- 2 -

BASIC FINANCIAL STATEMENTS

- 3 -

This page intentionally left blank.

- 4 -

GOVERNMENT-WIDE FINANCIAL STATEMENTS

- 5 -

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

STATEMENT OF NET ASSETSDecember 31, 2005

Exhibit A

ASSETS

CashInvestmentsDue from other governmental agenciesOther receivablesCapital assets:

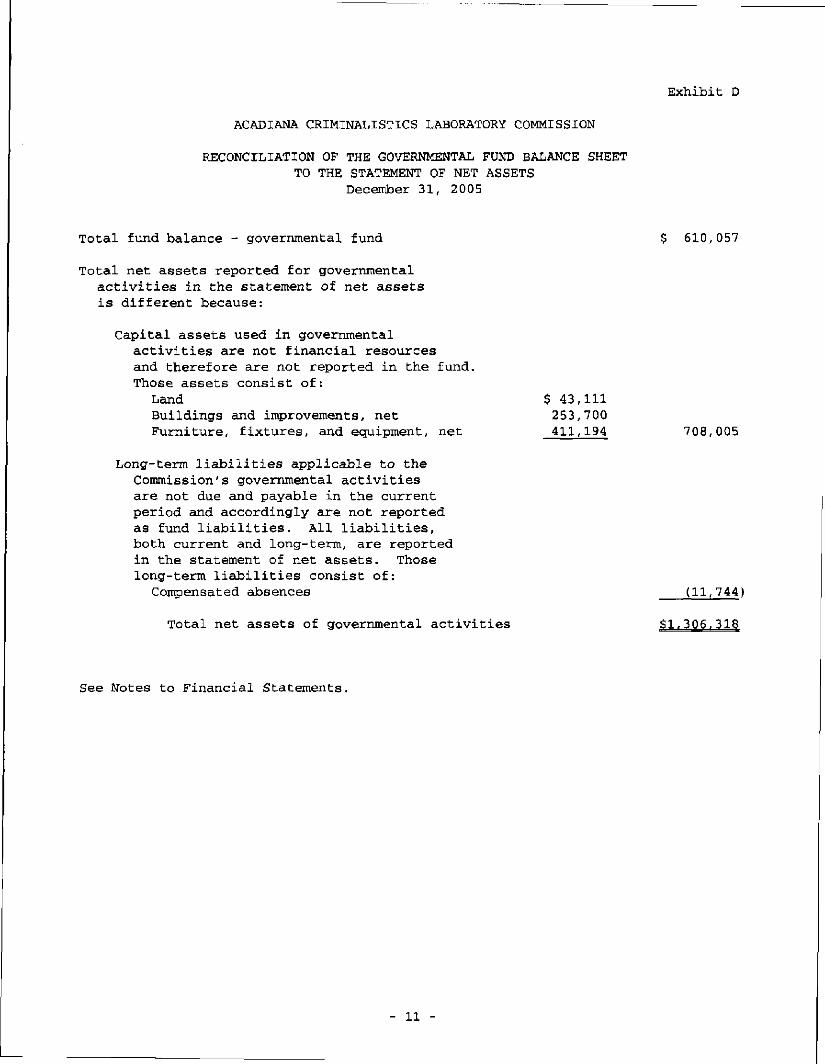

RECONCILIATION OF THE GOVERNMENTAL FUND BALANCE SHEETTO THE STATEMENT OF NET ASSETS

December 31, 2005

Total fund balance - governmental fund $ 610,057

Total net assets reported for governmentalactivities in the statement of net assetsis different because:

Capital assets used in governmentalactivities are not financial resourcesand therefore are not reported in the fund.Those assets consist of:

Land $ 43,111Buildings and improvements, net 253,700Furniture, fixtures, and equipment, net 411,194 708,005

Long-term liabilities applicable to theCommission's governmental activitiesare not due and payable in the currentperiod and accordingly are not reportedas fund liabilities. All liabilities,both current and long-term, are reportedin the statement of net assets. Thoselong-term liabilities consist of:Compensated absences (11,744)

Total net assets of governmental activities $1,306,318

See Notes to Financial Statements.

- 11 -

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGESIN FUND BALANCE

GOVERNMENTAL FUNDFor the Year Ended December 31, 2005

Exhibit E

Revenues:IntergovernmentalCharges for servicesInvestment earningsMiscellaneous

Total revenues

Expenditures:Current -

Public safetyCapital outlay

Total expenditures

Net change in fund balance

Fund balance, beginning

Fund balance, ending

GeneralFund

$ 734,258885,4734,7696,138

$1,630,638

$1,457,22153,474

S 610.057

See Notes To Financial Statements,

- 12 -

Exhibit F

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES,CHANGES IN FUND BALANCE OF THE GOVERNMENTAL FUND

TO THE STATEMENT OF ACTIVITIESFor the Year Ended December 31, 2005

AND

Net change in fund balance - governmental fund

The change in net assets reported for governmentalactivities in the statement of activities isdifferent because:

The governmental fund reports capital outlaysas expenditures; however, in the statementof activities the cost of those assets isallocated over their estimated useful livesand reported as depreciation expense.

Capital outlayDepreciation expense

Some expenses reported in the statement ofactivities do not require the use of currentfinancial resources; therefore, they are notreported as expenditures in the governmentalfund. The adjustment here relates to theadjustment for accrued compensated absences inthe current period.

Change in net assets of governmental activities

$ 119,943

$ 53,474(139,346) (85,872!

3,345

S 37.416

See Notes to Financial Statements.

- 13 -

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

NOTES TO FINANCIAL STATEMENTS

Note 1. Summary of Significant Accounting Policies

The financial statements of Acadiana Criminalistics Laboratory Commission(the "Commission") have been prepared in conformity with generally acceptedaccounting principles (GAAP). The Governmental Accounting Standards Board(GASB) is responsible for establishing GAAP for state and local governmentsthrough its pronouncements (Statements and Interpretations). The moresignificant of the Commission's accounting policies are described below.

Reporting entity:

The Commission was created in accordance with Louisiana Revised Statute40:2267.1. The Commission is governed by a 21 member board ofcommissioners, who serve without pay, comprised of the parish president ofIberia Parish, the sheriffs, district attorneys, and one council/policejury member appointed by the parish councils/police juries of Acadia,Evangeline, Iberia, Lafayette, St. Landry, St. Martin, St. Mary, andVermilion Parishes. The Commission is charged with crime detection,prevention, investigation, and other related activities in connection withcriminal investigation.

The operations of the Commission are administered through a director andare financed primarily through court costs collected by the varioussheriffs and city courts. The Commission serves the southwest Louisianaparishes enumerated above with operations located in Iberia Parish.

Basis of presentation:

The Commission's basic financial statements consist of the government-widestatements and the fund financial statements. The statements are preparedin accordance with accounting principles generally accepted in the UnitedStates of America as applied to governmental units.

Government-wide financial statements -

The government-wide financial statements include the statement of netassets and the statement of activities of the Commission. Thesestatements include the financial activities of the overall government.Governmental activities generally are financed throughintergovernmental revenues and other nonexchange transactions.

In the government-wide statement of net assets, the governmentalactivities are reported on a full accrual, economic resource basis,which recognizes all long-term assets and receivables as well aslong-term debt and obligations. The Commission's net assets arereported in two parts - invested in capital assets and unrestricted.

- 14 -

NOTES TO FINANCIAL STATEMENTS

The government-wide statement of activities reports both the gross andnet cost of the Commission's function. The function is also supportedby general government revenues (certain intergovernmental revenues,interest income, etc.). The statement of activities reduces grossexpenses (including depreciation) by related program revenues,operating and capital grants. Program revenues must be directlyassociated with the function. Operating grants includeoperating-specific and discretionary (either operating or capital)grants while the capital grants column reflects capital-specificgrants.

The net cost (by function) is normally covered by general revenue(intergovernmental revenues, interest income, etc.).

The government-wide focus is more on the sustainability of theCommission as an entity and the change in the Commission's net assetsresulting from the current year's activities.

Fund financial statements -

The fund financial statements provide information about theCommission's funds. The emphasis of fund financial statements is onmajor governmental funds. The Commission has only one fund, itsGeneral Fund. The General Fund is the Commission's general operatingfund. It is used to account for all of the financial resources of theCommission.

Basis of accounting:

Government-wide financial statements -

The government-wide financial statements are reported using the economicresources measurement focus and the accrual basis of accounting.Revenues are recorded when earned and expenses are recorded at the timeliabilities are incurred, regardless of when the related cash flows takeplace. Nonexchange transactions, in which the Commission gives (orreceives) value without directly receiving (or giving) equal value inexchange, include grants and donations. Revenue from grants,entitlements and donations is recognized in the fiscal year in which alleligibility requirements have been satisfied.

Fund financial statements -

Governmental funds are reported using the current financial resourcesmeasurement focus and the modified accrual basis of accounting. Underthis method, revenues are recognized when measurable and available."Measurable" means the amount of the transaction can be determined and"available* means collectible within the current period or soon enoughthereafter to be used to pay liabilities of the current period. Allreceivables collected within 60 days after year end are consideredavailable and recognized as revenue of the current year.

- 15 -

NOTES TO FINANCIAL STATEMENTS

Expenditures are recorded when the related fund liability is incurred,except for compensated absences, which are recognized as expenditures tothe extent they have matured. General capital asset acquisitions arereported as expenditures in governmental funds.

Cash and investments:

Cash consists of amounts in demand deposit accounts for the Commission.

State statutes authorize the Commission to invest in United States bonds,treasury notes, or certificates and time deposits of state banks organizedunder Louisiana law and national banks having principal offices inLouisiana. In addition, local governments in Louisiana are authorized toinvest in the Louisiana Asset Management Pool, Inc. (LAMP), a nonprofitcorporation formed by an initiative of the State Treasurer and organizedunder the laws of the State of Louisiana, which operates a local governmentinvestment pool.

In accordance with GASB Statement No. 31, investments meeting the criteriaspecified in the Statement are stated at fair value. Investments which donot meet the requirements are stated at cost. These investments includeamounts invested in LAMP.

Custodial credit risk:

Deposits -

The Commission is exposed to custodial credit risk as it relates to theirdeposits with financial institutions. The Commission's policy to ensurethere is no exposure to this risk is to require each financialinstitution to pledge their own securities to cover any amount in excessof Federal Depository Insurance Coverage. These securities must be heldin the Commission's name. Accordingly, the Commission had no custodialcredit risk related to its deposits at December 31, 2005.

Fixed assets:

The accounting treatment over property, plant, and equipment (fixed assets)depends on whether the assets are reported in the government-wide or fundfinancial statements.

Government-wide statements -

In the government-wide financial statements, fixed assets are accountedfor as capital assets. All fixed assets are valued at cost orestimated historical cost. Donated fixed assets are recorded at theirfair value at the date of donation. The cost of normal maintenance andrepairs that do not add to the value of the asset or materially extendassets lives are not capitalized. Depreciation on all capital assets,excluding land and improvements, is calculated on the straight-linemethod over the following estimated useful lives:

- 16 -

NOTES TO FINANCIAL STATEMENTS

Years

Buildings and improvements 1 5 - 3 9Furniture, fixtures and equipment 5-7

Fund financial statements -

In the fund financial statements, fixed assets used in governmentalfund operations are accounted for as capital outlay expenditures of thegovernmental fund upon acquisition.

Compensated absences:

Employees of the Commission earn vacation pay at the rate of 4 to 12 hoursper month. With the exception of the Director, employees may carry forwardvacation time earned but not taken with a 40 hour limitation. Any excessabove forty hours is automatically converted to sick leave. The Director'scarryforward hours are unlimited. Unused vacation is paid to an employeeupon retirement or resignation at the hourly rate being earned by thatemployee upon separation. No payment is made for accrued and unused sickleave.

In the government-wide statements, the Commission accrues accumulatedunpaid vacation and sick leave and associated related costs when earned {orestimated to be earned) by the employee. The current portion is the amountestimated to be used/paid in the following year. The remainder is reportedas non-current. At December 31, 2005, all was considered current. Inaccordance with GASB Interpretation No. 6, "Recognition and Measurement ofCertain Liabilities and Expenditures in Governmental Fund FinancialStatements," no compensated absences liability is recorded in thegovernmental fund financial statements.

Equity classifications:

Government-wide statements -

Equity is classified as net assets and displayed in two components:

a. Invested in capital assets - Consists of capital assets net ofaccumulated depreciation.

b. Unrestricted net assets - All other net assets that do not meet thedefinition of "invested in capital assets."

The Commission has no restricted net assets.

Fund statements -

Governmental fund equity is classified as fund balance. Fund balance isfurther classified as reserved and unreserved, with unreserved furthersplit between designated and undesignated.

- 17 -

NOTES TO FINANCIAL STATEMENTS

Use of estimates:

The preparation of financial statements in conformity with generallyaccepted accounting principles requires management to make estimates andassumptions that affect certain reported amounts and disclosures.Accordingly, actual results could differ from those estimates.

Note 2. Investments

As of December 31, 2005, the Commission had the following investment andmaturity:

State Investment Pool (LAMP) -maturity of less than one year S 148.198

LAMP is administered by LAMP, Inc., a nonprofit corporation organized underthe laws of the State of Louisiana, which was formed by an initiative of theState Treasurer in 1993. The corporation is governed by a board of directorscomprising the State Treasurer, representatives from various organizations oflocal government, the Government Finance Officers Association of Louisiana,and the Society of Louisiana CPA's. Only local governments having contractedto participate in LAMP have an investment interest in its pool of assets.The primary objective of LAMP is to provide a safe environment for theplacement of public funds in short-term, high-quality investments. The LAMPportfolio includes only securities and other obligations in which localgovernments in Louisiana are authorized to invest. Accordingly, LAMPinvestments are restricted to securities issued, guaranteed, or backed by theU.S. Treasury, the U.S. government, or one of its agencies, enterprises, orinstrumentalities, as well as repurchase agreements collateralized by thosesecurities. The dollar weighted average portfolio maturity of LAMP assets isrestricted to not more than 90 days, and consists of no securities with amaturity in excess of 397 days. LAMP is designed to be highly liquid to giveits participants immediate access to their account balances.

Credit Risk - Credit risk is defined as the risk that an issuer or othercounterparty to an investment will not fulfill its obligations. TheCommission does not have a formal investment policy that addresses this risk.LAMP is rated AAAm by Standard & Poor's at December 31, 2005.

- 18 -

NOTES TO FINANCIAL STATEMENTS

Note 3. Capital Assets

Capital assets activity for the year ended December 31, 2005 was as follow:

No compensation was paid to Commission members during the year endedDecember 31, 2005.

Note 6. Defined Benefit Pension Plan

All permanent employees of the Commission participate in the ParochialEmployees' Retirement System (PERS) of Louisiana, a multiple-employer publicemployee retirement system,

Plan description:

Members of the plan may retire with 30 years of creditable service regardlessof age, with 25 years of service at age 55, and with 10 years of service atage 60. Benefit rates are 1% of final compensation (average monthly earningsduring the highest 36 consecutive months, or joined months if service wasinterrupted) plus $2.00 per month for each year of service credited prior toJanuary 1, 1980, and 3% of final compensation for each year of service afterJanuary 1, 1980. The System also provides disability and survivor benefits.Benefits are established by state statue. PERS issues a publicly availablefinancial report that includes financial statements and required supplementalinformation. That report may be obtained by writing to Parochial Employees'Retirement System of Louisiana, Post Office Box 14619, Baton Rouge, Louisiana70898.

Funding policy:

Plan members are required to contribute 9.50% of their annual covered salaryto the plan and the Commission is required to contribute at an actuariallydetermined rate. The current rate is 12.75% of annual covered payroll. Thecontribution requirements of plan members and the Commission are establishedby statute. The Commission's contribution to PERS for the years endedDecember 31, 2005, 2004, and 2003 were $119,910, $104,838, and $67,717,respectively, equal to the required contribution each year.

- 20 -

NOTES TO FINANCIAL STATEMENTS

Note 7. Due From Other Governmental Agencies

Amounts due from other governmental agencies consist of the following atDecember 31, 2005:

State of Louisiana:Federal pass-through grant funds $ 7,987

Court costs due from various courts 60, 384

Note 8. Risk Management

The Commission is exposed to various risks of loss related to torts; theftof, damage to, and destruction of assets; errors and omissions; injuries toemployees; and natural disasters. The Commission purchases commercialinsurance to cover any claims related to these risks.

- 21 -

This page intentionally left blank.

- 22 -

REQUIRED SUPPLEMENTARY INFORMATION

- 23 -

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

BUDGETARY COMPARISON SCHEDULEGENERAL FUND

For the Year Ended December 31, 2005

Exhibit G-l

Variance WithFinal Budget

Revenues:Intergovernmental -

Federal grantOther

Charges for services -Court costs

Investment earningsMiscellaneous

Total revenues

Expenditures:Current -

Public safety:Personnel costsWorkers' compensationTravel and trainingPrintingTelephone and utilitiesEquipment rentalRepairs and maintenanceInsuranceOffice suppliesPostage and shippingLab suppliesVehicle and maintenance

suppliesProfessional servicesMiscellaneous

Capital outlay

Net change in fund balance

Fund balance, beginning

Fund balance, ending

OriginalBudget

$

$1,

$1,

$1,

$

600,

864,

20,

485,

160,14,26,2,21,2,

33,32,1,6,

53,

2,22,6,

100,

485,

000

28070720

070

239000656482982292528000210523113

058355632000

070

-0-

FinalBudget

$600,

864,

20,

$1,485,

$1,160,14,26,2,21,2,33,32,1,6,53,

2,22,6,

100,

$1,485,

$

000

28070720

070

239000656482982292528000210523113

058355632000

070

-0-

Actual

$ 134,600,

885,4,6,

$1,630,

$1,137,9,

15,

28,3,

35,30,15,3,

144,

2,22,6,53,

$1,510,

$ 119,

490,

$ 610,

147111

473769138

638

552908780478217884043513328595997

255831840474

695

943

114

057

Positive(Negative)

$ 134

214

(14

$ 145

$ 224102(6(1(11

(142

(91

46

$ (25

$ 119

,147111

,193,699,582)

,568

,687,092,876,004,235),592),515),487,118),928,884)

(197)(476)(208),526

,625)

,943

See Note to Budgetary Comparison Schedule.

- 24 -

Exhibit G-2

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

NOTE TO BUDGETARY COMPARISON SCHEDULE

Note 1. Budgets and Budgetary Accounting

The Acadiana Criminalistics Laboratory Commission follows the proceduresdetailed below in adopting its budget.

1. The budget for the General Fund is proposed by the Director and formallyapproved and adopted by the Commission. It is then sent to the eightparishes served by the Commission and must be approved by a majority.

2. Once adopted, any amendments must be approved by the Commission. Thebudget procedure is in accordance with Section E of Louisiana RevisedStatute 40:2266.1.

All budgeted amounts presented as supplementary information reflect theoriginal budget and the final budget {which is the same as the originalbecause there were no revisions during the year).

The General Fund had an excess of expenditures over appropriations of $25,625for the year ended December 31, 2005.

- 25 -

This page intentionally left blank.

- 26 -

BROUSSARD, POCHE, LEWIS & BREAUX, L.L.P.

Other Offices;

Crowley, LA(337) 783-0650

Opelousas, LA(337) 942-5217

Abbeville, LA(337) 898-1497

New Iberia, LA(337) 364-4554

Church Point, LA(337) 684-2855

Herbert Lemoine II, CPA*

Frank A. Stagno, CPA*

Scott J. BroiiBsard, CPA*

L. Charles Abshire, CPA*

Kenneth R. Dugas, CPA*

P. John Blanchet III, CPA*

Craig C. Babineaux, CPA*

Peter C. Borrello, CPA*

George J. TVappey HI, CPA*

S. Scott SoUeau, CPA*

Patrick D. McCarthy, CPA*

Martha B. Wyatl, CPA*

Troy J. Breaux, CPA*

Fayetta T. Dupre, CPA*

Mary A. Caatille, CPA*

Joey L. Breaux, CPA*

Terrel P. Dressel, CPA*

Craig J. Viator, CPA*

Retired:

Sidney L. Broussard, CPA 1925-2005

Leon K. Poche, CPA 1984

James H. Breaux, CPA 1987

Erma R. Walton, CPA 1988

George A. Lewis, CPA* 1992

Geraldine J. Wimberley, CPA* 1995

Larry G. Brouesard, CPA* 1996

Lawrence A. Cramer, CPA* 1999

Ralph Friend, CPA* 2002

Eugene C. Gilder, CPA* 2004

Donald W. Kelley, CPA* 2005

E R T I F I E D P U B L I C A C C O U N T A N T S

4112 West Congress • P.O. Box 61400 • Lafayette, Louisiana 70596-1400

REPORT ON INTERNAL CONTROL OVER FINANCIALREPORTING AND ON COMPLIANCE AND OTHER MATTERS BASEDON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED INACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To Acadiana CriminalisticsLaboratory Commission

New Iberia, Louisiana

We have audited the basic financial statements of AcadianaCriminalistics Laboratory Commission as of and for the year endedDecember 31, 2005, and have issued our report thereon datedJune 14, 2006. We conducted our audit in accordance with auditingstandards generally accepted in the United States of America andthe standards applicable to financial audits contained inGovernment Auditing Standards, issued by the Comptroller General ofthe United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered theCommission's internal control over financial reporting in order todetermine our auditing procedures for the purpose of expressing ouropinion on the financial statements and not to provide assurance onthe internal control over financial reporting. However, we noted acertain matter involving the internal control over financialreporting and its operation that we consider to be a reportablecondition. Reportable conditions involve matters coming to ourattention relating to significant deficiencies in the design oroperation of the internal control over financial reporting that, inour judgment, could adversely affect the Commission's ability torecord, process, summarize and report financial data consistentwith the assertions of management in the financial statements. Thereportable condition is described in the accompanying schedule offindings and questioned costs as item #2005-1.

A material weakness is a condition in which the design or operationof one or more of the internal control components does not reduceto a relatively low level the risk that misstatements in amountsthat would be material in relation to the financial statementsbeing audited may occur and not be detected within a timely periodby employees in the normal course of performing their assigned

Members of American Institute ofCertified Public Accountant*Society of Louisiana CertifiedPublic Accountants

*A Professional Accounting Corporation- 27 -

functions. Our consideration of the internal control over financial reporting wouldnot necessarily disclose all matters in the internal control over financial reportingthat might be reportable conditions and, accordingly, would not necessarily discloseall reportable conditions that are also considered to be material weaknesses. Thereportable condition described above is considered a material weakness.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Commission's financialstatements are free of material misstatement, we performed tests of its compliance withcertain provisions of laws, regulations, contracts and grant agreements, noncompliancewith which could have a direct and material effect on the determination of financialstatement amounts. However, providing an opinion on compliance with those provisionswas not an objective of our audit and, accordingly, we do not express such an opinion.The results of our tests disclosed no instances of noncompliance or other matters thatare required to be reported under Government Auditing Standards.

This report is intended for the information of management and those other governmentsfrom which financial assistance was received and should not be used for any otherpurpose. However, this report is a matter of public record and its distribution is notlimited.

Lafayette, LouisianaJune 14, 2006

- 28 -

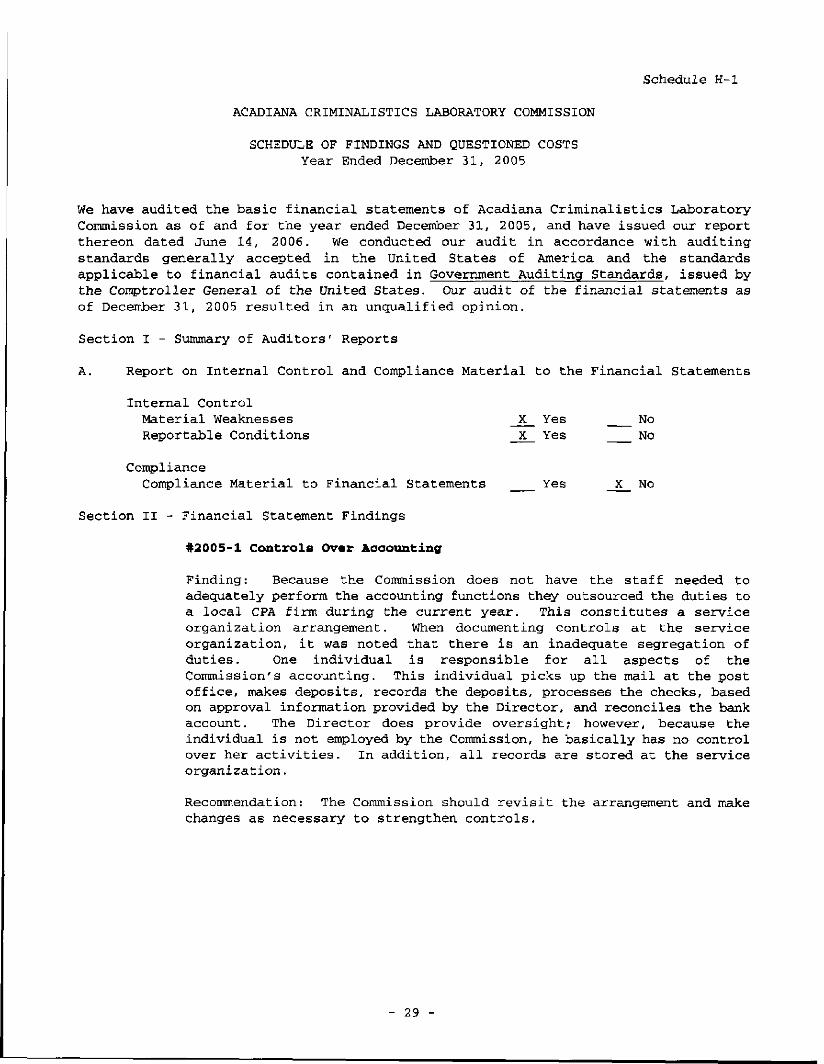

Schedule H-l

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

SCHEDULE OF FINDINGS AND QUESTIONED COSTSYear Ended December 31, 2005

We have audited the basic financial statements of Acadiana Criminalistics LaboratoryCommission as of and for the year ended December 31, 2005, and have issued our reportthereon dated June 14, 2006. We conducted our audit in accordance with auditingstandards generally accepted in the United States of America and the standardsapplicable to financial audits contained in Government Auditing Standards, issued bythe Comptroller General of the United States. Our audit of the financial statements asof December 31, 2005 resulted in an unqualified opinion.

Section I - Summary of Auditors' Reports

A. Report on Internal Control and Compliance Material to the Financial Statements

Internal ControlMaterial Weaknesses X Yes NoReportable Conditions X Yes No

ComplianceCompliance Material to Financial Statements Yes X No

Section II - Financial Statement Findings

#2005-1 Controls Over Accounting

Finding: Because the Commission does not have the staff needed toadequately perform the accounting functions they outsourced the duties toa local CPA firm during the current year. This constitutes a serviceorganization arrangement. When documenting controls at the serviceorganization, it was noted that there is an inadequate segregation ofduties. One individual is responsible for all aspects of theCommission's accounting. This individual picks up the mail at the postoffice, makes deposits, records the deposits, processes the checks, basedon approval information provided by the Director, and reconciles the bankaccount. The Director does provide oversight; however, because theindividual is not employed by the Commission, he basically has no controlover her activities. In addition, all records are stored at the serviceorganization.

Recommendation: The Commission should revisit the arrangement and makechanges as necessary to strengthen controls.

- 29 -

Schedule H-2

ACADIANA CRIMINALISTICS LABORATORY COMMISSION

SCHEDULE OF PRIOR FINDINGSFor the Year Ended December 31, 2005

Section I. Internal Control and Compliance Material to the Financial Statements

#2004-1 Segregation of Duties

Recommendation: Keeping in mind the limited number of employees to whichduties can be assigned, the Commission should monitor assignment ofduties to assure as much segregation of duties and responsibility aspossible.

Current Status: Similar finding in the current year at #2005-1.

#2004-2 CLIP Grant Reporting

Recommendation: Required reports should be filed in a timely manner.

Current Status: Reports are now being filed in a timely manner. Therewas no finding of this nature in the current year.

#2004-3 Bid Law Violation

Recommendation: Procedures should be established to follow the bid lawand the necessary documentation should be maintained on file.

Current Status: Procedures are now in place. There was no finding ofthis nature in the current year.

Section II. Internal Control and Compliance Material to Federal Awards

Not applicable.

Section III. Management Letter

The prior year's report did not include a management letter.

- 30 -

ACADIANA CRIMINALISTICS LABORATORY

5004 W. ADMIRAL DOYLE NEW IBERIA, LOUISIANA 70560 PHONE (337) 365-6671 FAX (337) 364-1834 AcadianaCL.com

June 20, 2006

Mr. Steve TheriotLegislative AuditorState of LouisianaPost Office Box 94397Baton Rouge, LA 70804^9397

Acadiana Criminalistics Laboratory Commission respectfully submits the followingcorrective action plan for the year ended December 31, 2005.

Name and address of independent public accounting firm:Broussard, Poche', Lewis & Breaux, L.L.P.Certified Public AccountantsPost Office Box 61400Lafayette, Louisiana 70596-1400

Audit period: January 1, 2005 through December 31, 2005.

The finding from the 2005 schedule of findings and questioned costs is discussed below.The finding is numbered consistently with the number assigned in the schedule. SectionI of the schedule, Summary of Auditors' Reports, does not include findings and is notaddressed.

Section II - Financial Statement Findings

#2005-1 Controls Over Accounting

Recommendation: The Commission should revisit the arrangement and makechanges as necessary to strengthen controls.

Action Taken:

The Director and the CPA firm that is engaged for the outsourcing of the accounting function have agreed on variouscontrols that will provide adequate segregation of duties. These controls will be implemented immediately. Althoughthe outsourcing has increased efficiency and timeliness of various reporting requirements, adequate segregation ofduties is also necessary. In addition, the Director will review the bank statements each month. The review of the bankstatements will include a review of the checks written each month and the deposits made each month. The review willalso check to see that the cash balance reported by the CPA firm is consistent with the bank statement balance. TheDirector will sign and date the bank statement to verify this review.

If the Legislative Auditor has questions regarding this plan, please call Kevin Ardoinat (337)364-1501.