Professional Accounting Education

Provided by Academy of Professional Accounting (APA)

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台

ACCA P2 Corporate reporting(INT.)

Chapter 5 IAS19 Employee benefit

ACCA Lecturer: Roy Wang

ACCA Research Institute

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 2

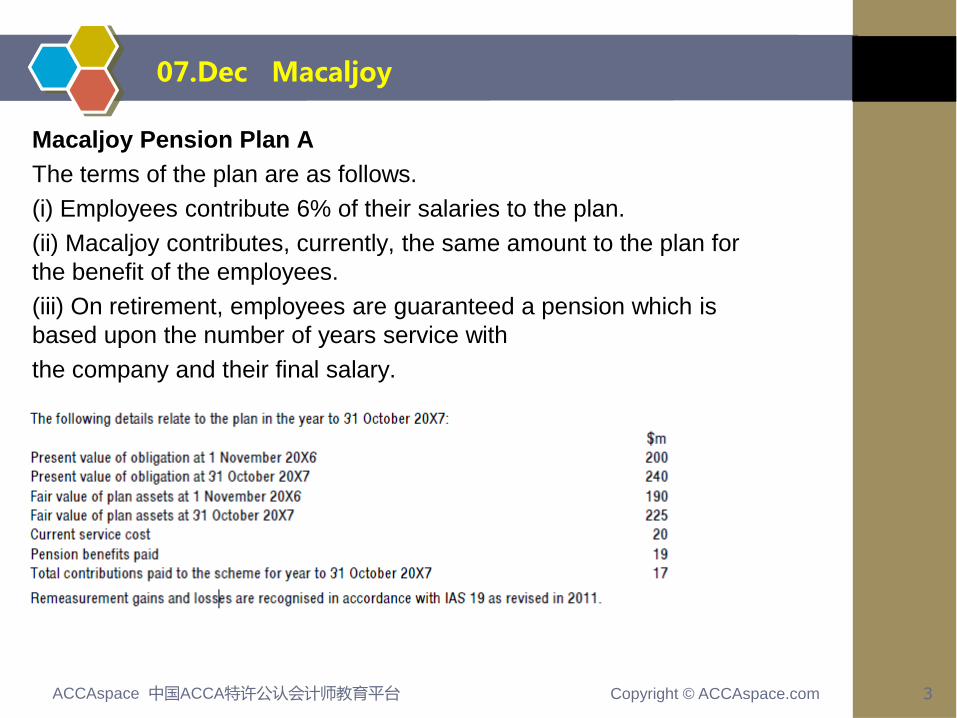

07.Dec Macaljoy

Macaljoy, a public limited company, is a leading support services

company which focuses on the building industry.

The company would like advice on how to treat certain items under

IAS 19 Employee benefits and IAS 37 Provisios, contingent liabilities

and contingent assets. The company operates the Macaljoy Pension

Plan B which commenced on 1 November 20X6 and the Macaljoy

Pension Plan A, which was closed to new entrants from 31 October

20X6, but which was open to future service accrual for the

employees already in the scheme. The assets of the schemes are

held separately from those of the company in funds under the control

of trustees. The following information relates to the two schemes.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 3

07.Dec Macaljoy

Macaljoy Pension Plan A

The terms of the plan are as follows.

(i) Employees contribute 6% of their salaries to the plan.

(ii) Macaljoy contributes, currently, the same amount to the plan for

the benefit of the employees.

(iii) On retirement, employees are guaranteed a pension which is

based upon the number of years service with

the company and their final salary.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 4

07.Dec Macaljoy

Macaljoy Pension Plan B

Under the terms of the plan, Macaljoy does not guarantee any

return on the contributions paid into the fund. The

company's legal and constructive obligation is limited to the

amount that is contributed to the fund. The following

details relate to this scheme:

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 5

07.Dec Macaljoy

Draft a report suitable for presentation to the directors of Macaljoy which:

(a) (i) Discusses the nature of and differences between a defined

contribution plan and a defined benefit plan with specific reference to the

company's two schemes. (7 marks)

(ii) Shows the accounting treatment for the two Macaljoy pension

plans for the year ended 31 October 20X7 under IAS 19 Employee

benefits (revised 2011). (7 marks)

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 6

07.Dec Macaljoy

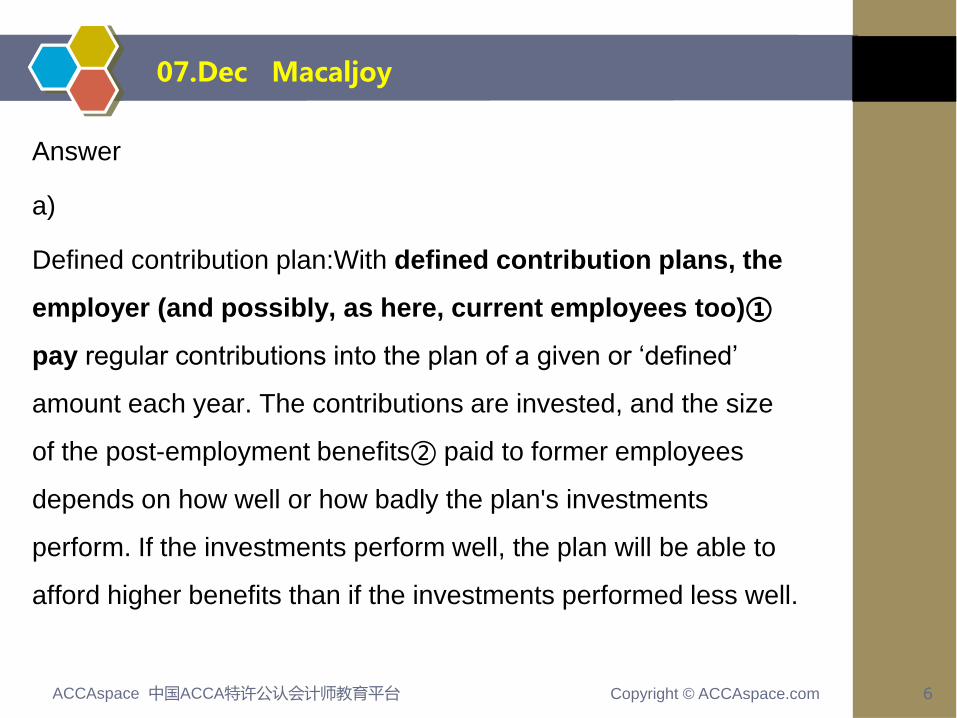

Answer

a)

Defined contribution plan:With defined contribution plans, the

employer (and possibly, as here, current employees too)①

pay regular contributions into the plan of a given or ‘defined’

amount each year. The contributions are invested, and the size

of the post-employment benefits② paid to former employees

depends on how well or how badly the plan's investments

perform. If the investments perform well, the plan will be able to

afford higher benefits than if the investments performed less well.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 7

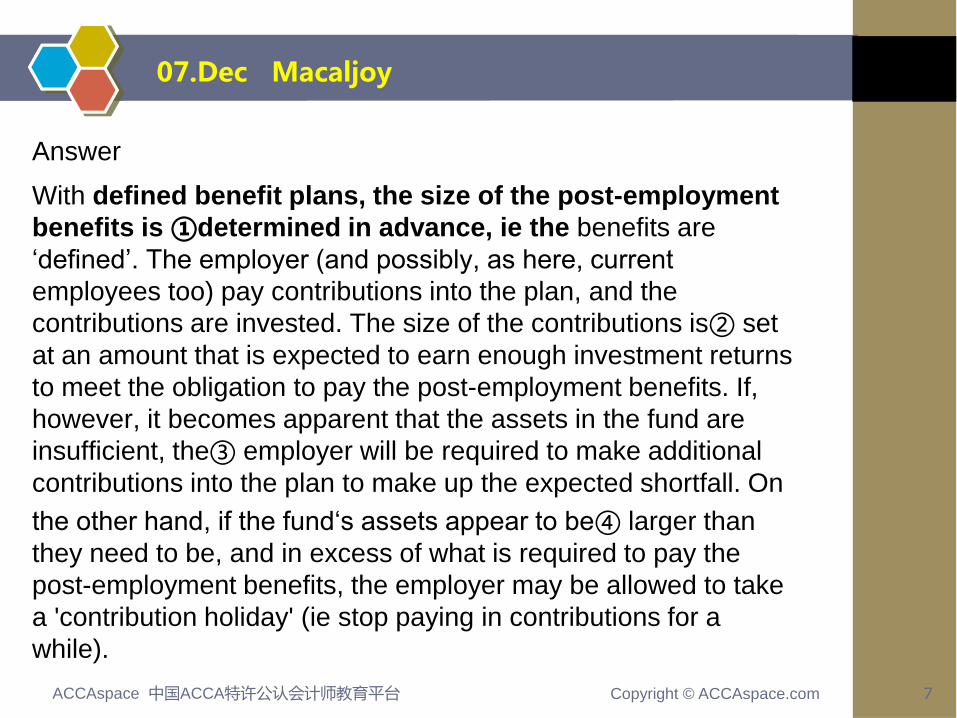

07.Dec Macaljoy

Answer

With defined benefit plans, the size of the post-employment

benefits is ①determined in advance, ie the benefits are

‘defined’. The employer (and possibly, as here, current

employees too) pay contributions into the plan, and the

contributions are invested. The size of the contributions is② set

at an amount that is expected to earn enough investment returns

to meet the obligation to pay the post-employment benefits. If,

however, it becomes apparent that the assets in the fund are

insufficient, the③ employer will be required to make additional

contributions into the plan to make up the expected shortfall. On

the other hand, if the fund‘s assets appear to be④ larger than

they need to be, and in excess of what is required to pay the

post-employment benefits, the employer may be allowed to take

a 'contribution holiday' (ie stop paying in contributions for a

while).

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 8

07.Dec Macaljoy

Difference

1.Risk

The risks of defined contribution plan are retained to

employees.

The risks of defined benefit plan are afforded by employers.

2.Amounts

The contribution of defined contribution scheme is fixed.

The contribution of defined benefit scheme is determined by

the investment,if investment bad,pay more contribution to the

pool.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 9

07.Dec Macaljoy

Reference

A: The A scheme is a defined benefit scheme. Macaljoy, the

employer, guarantees a pension based on the service lives of

the employees in the scheme. The company's liability is not

limited to the amount of the contributions. This means that the

employer bears the investment risk: if the return on the

investment is not sufficient to meet the liabilities, the company will

need to make good the difference.

B: The B scheme is a defined contribution plan. The

employer's liability is limited to the contributionspaid.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 10

07.Dec Macaljoy

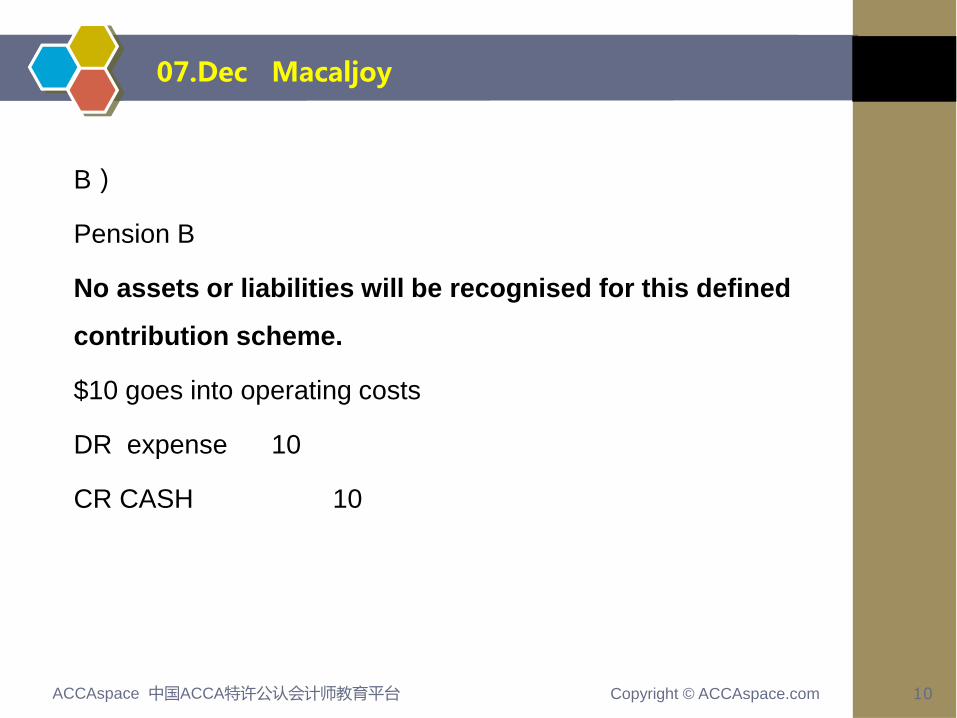

B)

Pension B

No assets or liabilities will be recognised for this defined

contribution scheme.

$10 goes into operating costs

DR expense 10

CR CASH 10

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 11

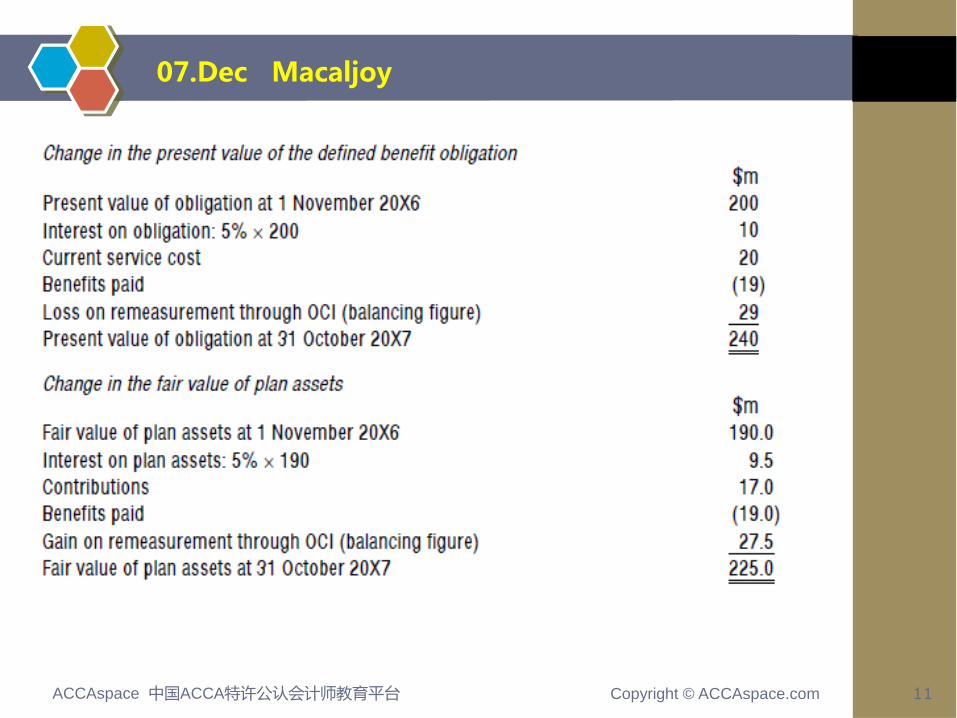

07.Dec Macaljoy

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 12

07.Dec Macaljoy

Professional Accounting Education

Provided by Academy of Professional Accounting (APA) ACCA Research Institute