31

2015 Global Risk Management Study Industry: Insurance

| Date post: | 26-Jul-2015 |

| Category: |

Business |

| Upload: | accenture-insurance |

| View: | 443 times |

| Download: | 2 times |

2015 Global Risk Management StudyIndustry: Insurance

2Copyright © 2015 Accenture All rights reserved.

Key findings

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

5 key priorities

Risk Management in the Insurance Sector

1 2

3 4

Making more of data and analytics

66%of surveyed insurers are increasing investment in data and analytics.

30%plan to grow investment by more than 20%.

Getting to grips with digital

79%of insurance respondents believe digital will be a major risk.

32%say their risk function has a high level of expertise to influence strategy and major decisions on social media.

Using operational risk to deliver growth

74%of insurance respondents expect cyber and IT risks to become more severe.

65%expect fraud and financial crime to pose a greater concern.

Building a culture to withstand disruptive change

7%of surveyed insurers say they have a strong and consistent risk culture today.

23%think they can achieve this over the next two years.

5Ramping up recruitment and retention

7% of insurance respondents saytheir teams have sufficientresources in specialized areas.

21% hope to have themin two years’ time.

86% expect to invest more in risk capabilities in next two years.

For more information, please visit: www.accenture.com/riskstudy2015 Source: Accenture 2015 Global Risk Management Study – Insurance respondents

© 2015 Accenture. All rights reserved.

Growth and digital

44%For insurance respondents to the Accenture 2015 Global Risk Management Study growth is back on the agenda and digital presents new opportunities.

of surveyed insurers have a greater appetite for new product development.

43%have a greater appetite for new alliances and partnerships.

85%say risk function can leverage digital to become a business partner.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

61%of risk masters believe their risk function can play a critical role in enabling profitable growth.

54%of risk masters believe they can help enable this growth “to a great extent”.

35%of non-masters reportthe same view.

Around 1 in 10 respondents to the Accenture 2015 Global Risk Management Study are “risk masters”.

10%

61%of risk masters agree strongly that emerging risks, such as cyber and digital, are consuming a greater proportion of the CRO’s time.

35%of non-risk masters feel stronglyabout this.

61%of risk masters agree strongly that they employ dedicated technology specialists to help manage digital risk.

27%of non-masters feel the same.

Stronger focus on profitable growth

Stronger focus on emerging risks Growing digital experience

For more information, please visit: www.accenture.com/riskstudy2015 Source: Accenture 2015 Global Risk Management Study – all respondents

What makes a risk master?

© 2015 Accenture. All rights reserved.

Better handle on regulatory and compliance

More extensive use of analytics

37%of risk masters believe strongly that regulatory change is receding in relation to other requirements.

25%of non-risk masters see regulatory change receding in the same way.

36%of non-masters feel the same.

More risk masters make extensive use of analytics to manage key risk categories including fraud and financial crime, cyber and IT risk, and credit, market and regulatory risks.

Risk masters are also more likely to be investing heavily in digital technologies.

Copyright © 2015 Accenture All rights reserved.

Contents

5

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Contents

6

A Our methodology

B Understanding the evolving environmentand context for risk management

1. Risk functions to get to grips with digital

2. Strengthen data and analytics capabilities

3. Agile and effective operational risk management adding to future business growth

4. Increase recruitment and retention efforts

5. Cultivate a consistent, resilient and integrated risk culture

C Bridging the gap

Copyright © 2015 Accenture All rights reserved.

Our methodology

7

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Introduction4th iteration of our Global Risk Management Study (2009, 2011, 2013)

2015 Global Risk Management Study: Paths to Prosperity

For the 2015 study, we surveyed 470 CFOs, CROs, CEOs, CCOs and CDOs involved in their organization’s risk decisions

Respondents came from North America, Europe and the Asia Pacific regions

Survey focused on three industry sectors: Insurance, Banking, Capital Markets

In addition to the survey we conducted 50 qualitative client interviews

8

2015: Paths to Prosperity

9Copyright © 2015 Accenture All rights reserved.

Risk management continues to make a crucial shift but choices need to be made.

Seen as a collaborative partner to enable business goals instead of a controlling function to be circumnavigated.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

10Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Study demographics

We surveyed 470 C-suite officers across all geographies and 12 countriesCountry Geography Regional

target Respondents

Australia

Asia Pacific 150

30

China 30

Hong Kong 30

Japan 30

Singapore 30

UK

Europe 170

50

Germany 30

France 30

Spain 30

Italy 30

USA North America 150

100

Canada 50

Total 470 470

Company size Total

Between US$1bn and US$5bn 235

Revenues over US$5bn 235

Total 470

Respondent Total

Chief Risk Officer 141

Chief Executive Officer 78

Chief Financial Officer 147

Chief Compliance Officer 28

Chief Operations Officer 31

Chief Data Officer/CIO 45

Total 470

Sectors Sector count Asia Pacific Europe North America

Banking 150 50 50 50

Capital Markets 170 50 70 50

Insurance 150 50 50 50

Total 470 150 170 150

Copyright © 2015 Accenture All rights reserved.

Understanding the evolving environment and context for risk management

11

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

12

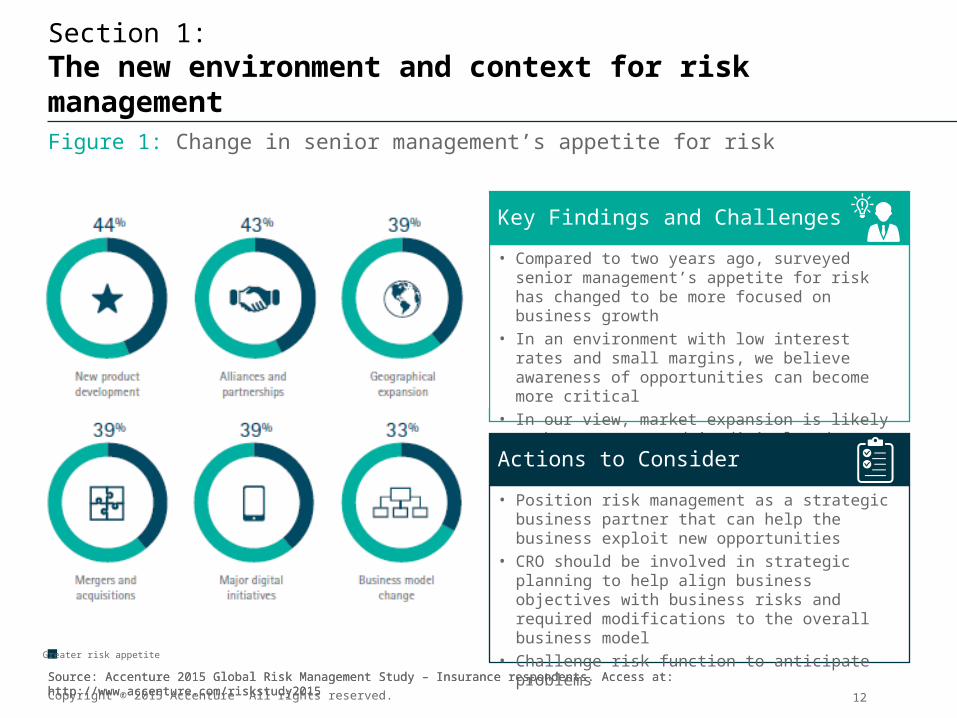

Section 1:The new environment and context for risk managementFigure 1: Change in senior management’s appetite for risk

Key Findings and Challenges

• Compared to two years ago, surveyed senior management’s appetite for risk has changed to be more focused on business growth

• In an environment with low interest rates and small margins, we believe awareness of opportunities can become more critical

• In our view, market expansion is likely to be concentrated in digital endeavors

Actions to Consider

• Position risk management as a strategic business partner that can help the business exploit new opportunities

• CRO should be involved in strategic planning to help align business objectives with business risks and required modifications to the overall business model

• Challenge risk function to anticipate problems

Greater risk appetite

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

13

Section 1:The new environment and context for risk managementFigure 2: Involvement of the CRO in various aspects of the organization's decision-making process

Key Findings and Challenges

• According to insurance respondents, risk management plays a vital role in providing oversight across the business and connecting the dots between different strategic plans

• The CRO (and risk management) is a key decision maker in many areas such as capital management, strategic planning, business and operating model changes

Actions to Consider

• Use the risk organization to help identify and share its insight into the portfolio level view of risks inherent to the business

• Position risk capability as a steering function rather than a reporting function

• Develop skill sets that encourage a more dynamic and less static approach to the ambiguity that may surround business issues

%

Key decision maker Among the decision makers

The CRO plays no role in major business decisions Don’t know

Advisor to the decision maker(s)

Selection and implementation of IT platforms and tools

% % %%% 33 17 31037

Capital management % % % %%46 35 12 25

Strategic planning 41% 15% 16%37%

Business model change %37% 36% 15% 111%

Digital initiatives %30% 41% 19% 37%

Product development 35% 37% 19% 1%7%

Pricing 39% 20% 1%9%32%

Alliances and partnerships 44% 17% 2%6%31%

Marketing/branding initiatives 37% 17% 1%11%35%

Changes to operating model 43% 14% 1%6%37%

Recruitment/talent strategy %35% 18% 213%33%

Human capital 35 21 2935 % % %%%

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Figure 3: Expectation that the organization will meet the compliance deadline for solvency regulation in its region

14

Section 1:The new environment and context for risk management

Key Findings and Challenges

• Less than a third of insurance respondents are confident that they are on track to meet compliance deadlines

• More than half believe they will still require improvements in order to meet expected compliance deadlines

Actions to Consider

• Assess the areas for improvement early in process to allow for adequate time for implementation to meet deadlines

• Understand readiness and identify potential areas for IT investment to support compliance requirements

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

15

Section 1:The new environment and context for risk managementFigure 4: Estimated total cost (in its region), including internal resources to comply with Solvency/other primary regulation, up to and including implementation in 2014 and beyond

Key Findings and Challenges

• Cost of compliance has been significant; nearly 30% of insurance respondents have invested between $26-50 million

• 15% say they have spent more than $100 million to comply

• Seven out of 10 surveyed insurers say that the cost of complying with primary regulation has been higher than expected

Actions to Consider

• Seek additional returns on investment by increasing the efficiency and effectiveness of the compliance process

• Leverage compliance as a source of competitive advantage by examining the threats and opportunities embedded in the regulatory environment

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

16

Section 1:The new environment and context for risk management

Key Findings and Challenges

• According to insurance respondents, risk functions have made large strides in enabling long-term profitable growth and contributing to innovation and product development

• In our view, risk functions have used the increased visibility around Solvency II compliance to make gains in their level of involvement in more strategic/growth goals

Actions to Consider

• Use enterprise risk management frameworks embedded into governance and decision making processes to strengthen cross-functional business relationships

• Leverage additional visibility into C-suite to continue gains in risk management’s role around revenue generating agenda of the business – look to produce portfolio-wide views of risks

Figure 5: How risk management contributes to the organization achieving its various targets

63%

78%

77%

76%

76%

78%

NA in 2013

NA in 2013

81%

72%

79%

69%

82%

78%

84%

74%

83%

74%

85%

85%

74%

75%

73%

82%

Infusing a risk culture in the organization

Reducing operational, credit, or market losses

Innovation and product development

Improving capital allocation

Reducing the cost of capital

Improving accuracy and integrity of data

Managing the increasing volatility of the economic and financial environment

Managing liquidity and cash flow

Risk-adjusted performance management

Enabling long-term profitable growth

Reconciling the need for global coordination and local regulatory coverage

Managing reputation with stakeholders (including analysts, the media and the public)

2015 2013

Copyright © 2015 Accenture All rights reserved.

Bridging the gap

17

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

18

Bridging the gapTo cope with the rising pace of digital and competitive industry challenges, risk management should focus on five key priorities

Risk functions to get to grips with digital

Strengthen data and analytics capabilities

Agile and effective operational risk management adding to future business growth

Increase recruitment and retention efforts

Cultivate a consistent, resilient and integrated risk culture

1 2 3 4 5

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

19

Priority 1: Risk functions to get to grips with digital

Copyright © 2015 Accenture All rights reserved.

Key Findings and Challenges

• Digital initiatives in our view represent an opportunity for risk management to bring its strengths and capabilities as a partner to the overall insurance business

• However, insurance respondents indicate the level of digital experience within their risk functions is currently not high

Actions to Consider

• Become a voice to improve the understanding of risk/reward tradeoffs in new digital business endeavors

• Evolve the risk organization and proactively position it for greater agility to address the expected business and organizational changes triggered by emerging digital technologies

Note: “Guevara, a ‘revolutionary’ P2P car insurance service launches in the UK, The Next Web, July 1, 2014.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

20

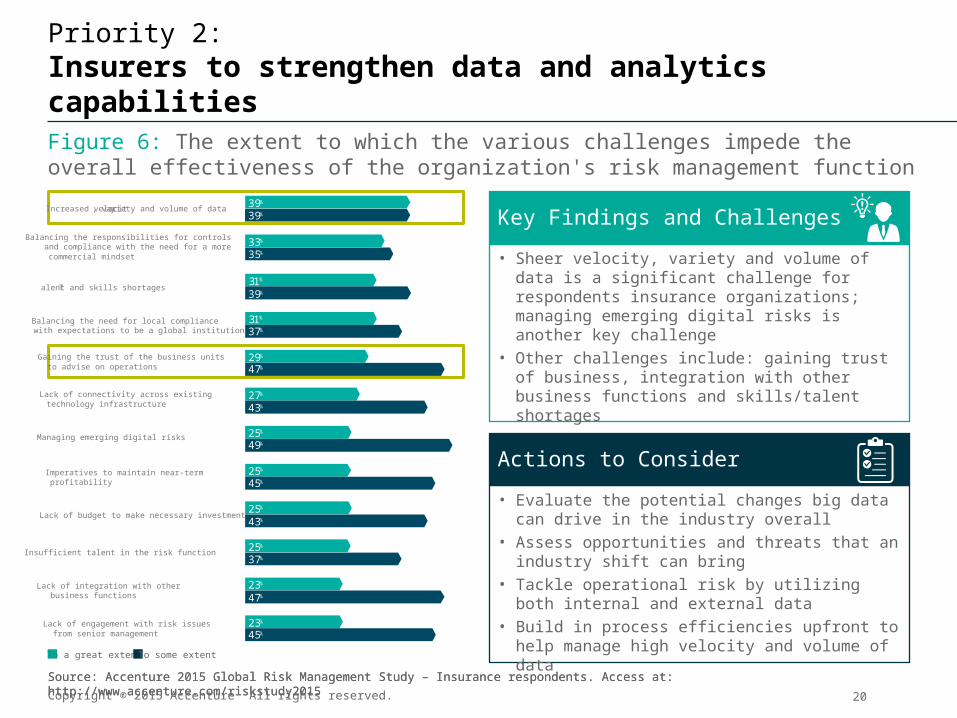

Priority 2: Insurers to strengthen data and analytics capabilities

Key Findings and Challenges

• Sheer velocity, variety and volume of data is a significant challenge for respondents insurance organizations; managing emerging digital risks is another key challenge

• Other challenges include: gaining trust of business, integration with other business functions and skills/talent shortages

Actions to Consider

• Evaluate the potential changes big data can drive in the industry overall

• Assess opportunities and threats that an industry shift can bring

• Tackle operational risk by utilizing both internal and external data

• Build in process efficiencies upfront to help manage high velocity and volume of data

Balancing the need for local compliance with expectations to be a global institution

Lack of budget to make necessary investments

Lack of engagement with risk issues from senior management

Imperatives to maintain near-term profitability

Lack of connectivity across existing technology infrastructure

Managing emerging digital risks

Talent and skills shortages

Lack of integration with other business functions

Gaining the trust of the business units to advise on operations

Increased velocity, variety and volume of data

Balancing the responsibilities for controlsand compliance with the need for a more

commercial mindset

31%

37%

25%

43%

45%

23%

25%

45%

27%

43%

25%

49%

31%

39%

23%

47%

47%

29%

39%

39%

35%

33%

25%

37%Insufficient talent in the risk function

Figure 6: The extent to which the various challenges impede the overall effectiveness of the organization's risk management function

To a great extent To some extent

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

21

Priority 2: Insurers to strengthen data and analytics capabilitiesFigure 7: Risk management’s use of data and analytics to address the various types of risk

40%

Key Findings and Challenges

• Data and analytics are most often used for market risk, liquidity risk, operational risk and regulatory risk by insurance respondents

• Fraud and financial crime, and operational and regulatory risks are the most extensive users of risk data and analytics

• IT platform selection and implementation are heavy users of risk data and analytics

Actions to Consider

• Increase use of risk data and analytics to be more extensive in key parts of the business; there are significant opportunities for additional use of data and analytics

• Work towards migrating data accessibility beyond the walls of specific siloes in order to lay the foundation for more significant future use of analytics

Extensive Moderate

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Priority 3: Agile and effective operational risk management adding to future business growth

22

Key Findings and Challenges

• We are seeing an increase in regulations concerning the protection of customer data

• Operational risk is an increased area of focus according to insurance respondents

• Cyber/IT risks top the ranking – probably due to growing use of/and skills in social media by criminal entities

• Legal risks continue to rank highly

Actions to Consider

• Minimize the historic silo dynamic between fraud and IT risk management to help counter the threats with both the CRO and CIO

• Understand cyber and IT security as criminals mature rapidly in sophistication

• Increase transparency and timeliness of operational risk processes to help create reports offering relevant business insight

Figure 8: Expected changes to the severity of the various operational risks facing the business over the next two years

Significant/slight increase

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

11%

13%

7%

21%18%

10%

33%

12%

36%

1 2 3

38%

23

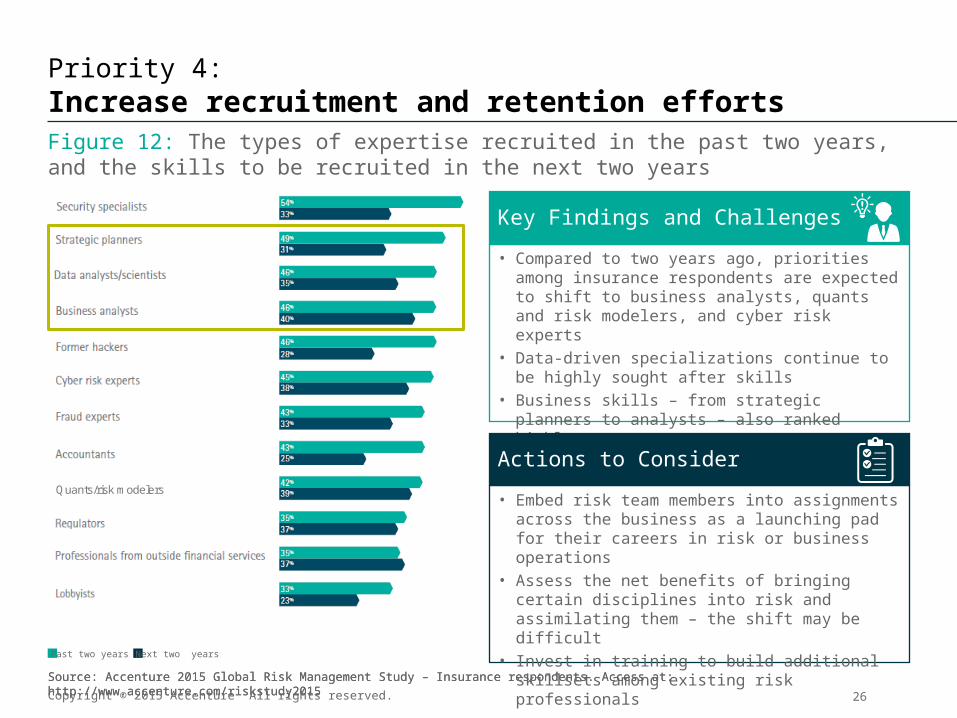

Priority 4: Increase recruitment and retention efforts

The risk team has insufficient talent resources to carry out the functions it is asked to perform

The risk team lacks internal resources in some specialized areas (modeling, emerging risks)

The risk team has internal resources even in specialized areas (modeling, emerging risks)

Key Findings and Challenges

• Only 7% of insurance respondents have resources/skills necessary to fulfill the evolving role

• Recruitment and retention of risk talent remains a challenge according to respondents

• Areas with the greatest gaps coincide with areas of greatest need (data management, cyber risk)

Actions to Consider

• Develop specialist teams to help address emerging areas of risk (cyber, digital, social media) head-on and learn by monitoring and analyzing real-time data

• Embed risk framework on an integrated, group-wide platform. This favors contribution from all employees in discussions on new risks – input can be reviewed

Figure 9: Statement that best describes the stage of maturity of insurer’s talent management

Today Two years’ time

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

24

Priority 4: Increase recruitment and retention effortsFigure 10: Over the next two years, the skills and capabilities that will be most in demand by the risk management function

Key Findings and Challenges

• According to insurance respondents, data management and analysis, and cyber risk understanding are skills that will be most in demand by risk functions

• Insurance is a data-driven sector and the transformation taking place around big data should continue to drive in our view the need for data specialist functions

Actions to Consider

• Retain advantage over banks – 50% of insurance respondents say they have data management skills to a great extent versus 40% among banking respondents

• Enhance retention and development of scarce specialized resources by offering cross-border, cross-functional career path opportunities

Modeling

Knowledge and understanding of digital technologies

33%

33%

29%

27%

26%

25%

21%

20%

19%

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

25

Priority 4: Increase recruitment and retention effortsFigure 11: The expected change to the total level of investment in risk management capabilities in the next two years

Key Findings and Challenges

• Over 85% of insurance respondents expect to increase their investment in risk management capabilities

• 56% of respondents expect a moderate increase (<20%) of investment in risk management capabilities in the next two years

• Only 12% reported no change

Actions to Consider

• Consider recruiting specialist skills from non-traditional recruiting pools, such as security specialists, strategic planners and data analysts

• Invest in building cross-functional skills in existing risk personnel

• Invest in digital technologies and analytics that can drive insight from fewer professionals

2015 2013

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

26

Priority 4: Increase recruitment and retention efforts

Quants/risk modelers 78

Key Findings and Challenges

• Compared to two years ago, priorities among insurance respondents are expected to shift to business analysts, quants and risk modelers, and cyber risk experts

• Data-driven specializations continue to be highly sought after skills

• Business skills – from strategic planners to analysts – also ranked highly

Actions to Consider

• Embed risk team members into assignments across the business as a launching pad for their careers in risk or business operations

• Assess the net benefits of bringing certain disciplines into risk and assimilating them – the shift may be difficult

• Invest in training to build additional skillsets among existing risk professionals

Figure 12: The types of expertise recruited in the past two years, and the skills to be recruited in the next two years

Past two years Next two years

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

1

22%

13%

2

16%

19%

3

31%

39%

4

18%

13%

5

23

27

Priority 5:Cultivate a consistent, resilient and integrated risk culture

Key Findings and Challenges

• 2015 study respondents across all financial services sectors struggle with implementing an enterprise-wide risk culture

• Only 7% of insurance respondents report a strong, consistent culture and 22% report they are still at the early stages of development

• Optimism is limited as only 23% believe they can have a strong culture in two years time

Actions to Consider

• Rethink the organizational model so risk is embedded within the business. This may mean going from a centralized to a decentralized operating model.

• Include risk-based approaches in strategic decision-making

• Staff risk personnel across businesses or include in informal working groups

Figure 13: Statement that best describes the stage of maturity of the insurer’s risk culture

We are at the early stages of developing and implementing a risk culture

We have made improvements in embedding our risk culture, but we still have work to do and face barriers to its full implementation

We have a strong and consistent risk culture that is understood and implemented across the entire organization

Today Two years’ time

To learn more about the study and to obtain your copy of the Insurance Report please go to: www.accenture.com/insurance-riskstudy2015

28Copyright © 2015 Accenture All rights reserved.

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

Copyright © 2015 Accenture All rights reserved.

An evolving landscape

29

Source: Accenture 2015 Global Risk Management Study – Insurance respondents. Access at: http://www.accenture.com/riskstudy2015

2005

2015

VS

Decisions informed by past events

Risk only outlook

Focused on credit, market and operational risk

Narrow definition of operational risk

Clear demarcation between three lines of defense

“Left brain” – quantitative; analytical approach

Prioritized control and prevention

Tactical attitude: centered on day-to-day risks

Spreadsheet-based management

Digital? What’s digital?

Looking forward, with “next day” thinking

Recognizing risk AND inherent opportunity

Aware of a growing range of emerging risks

More comprehensive definition of operational risk

Three lines of defense, with fluid interaction embedded in the business

“Left AND right brain” – creative, innovative understanding

A balance of control, prevention, and enablement

Strategic awareness: focused on long-term business challenges

Increasingly integrated data sources

Emphasis on digital risks and opportunities

The Risk Landscape

Risk management in 2025Analytics now permeates decision

makingCompanies are exploring robotics and artificial intelligence to manage transactional risks

Behavior prediction helps to effectively inform risk management

Rise of the Chief Risk and Return Officer

Risk management is the career path to the C-suite

Single data source drives reporting and analytics activities

For more information, please visit: www.accenture.com/riskstudy2015 © 2015 Accenture. All rights reserved.

Copyright © 2015 Accenture All rights reserved.

2015 Global Risk Management StudyIndustry: Insurance

31

Disclaimer:

This presentation is intended for general informational purposes only and does not take into account the reader’s specific circumstances, and may not reflect the most current developments. Accenture disclaims, to the fullest extent permitted by applicable law, any and all liability for the accuracy and completeness of the information in this presentation and for any acts or omissions made based on such information. Accenture does not provide legal, regulatory, audit, or tax advice. Readers are responsible for obtaining such advice from their own legal counsel or other licensed professionals.

About Accenture

Accenture is a global management consulting, technology services and outsourcing company, with more than 323,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$30.0 billion for the fiscal year ended Aug. 31, 2014. Its home page is www.accenture.com.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.