20

Accounting Information Systems System Descriptions

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | antonia-manning |

| View: | 221 times |

| Download: | 3 times |

Accounting Information Systems

System Descriptions

The Cash Receipts Cycle

• The points to think about are– Why do we do all of the things that we do?– How can we tell this story more efficiently

and (perhaps) effectively?

• We will tell the story sort of like a “play” with characters acting out parts.

Why do we care about accounting information systems?

What do accounting information systems do as compared to “manual entry” systems?

Another way of asking this question is: What do we wish to accomplish with our system?

Why do we care about accounting information systems?

There are several related answers to this question, including the following:

• Make certain that the transaction information that is recorded fully and correctly reflects the transactions which have occurred.

• Provide some protection against theft and fraudulent financial statements.

• Provide managers with the type of information that they require to make decisions.

• The first two items are termed control characteristics of the system. How does the system (the way you process information) influence the likelihood of errors and fraud?

• The third item relates to the efficiency of the information system at providing useful information for management decisions.

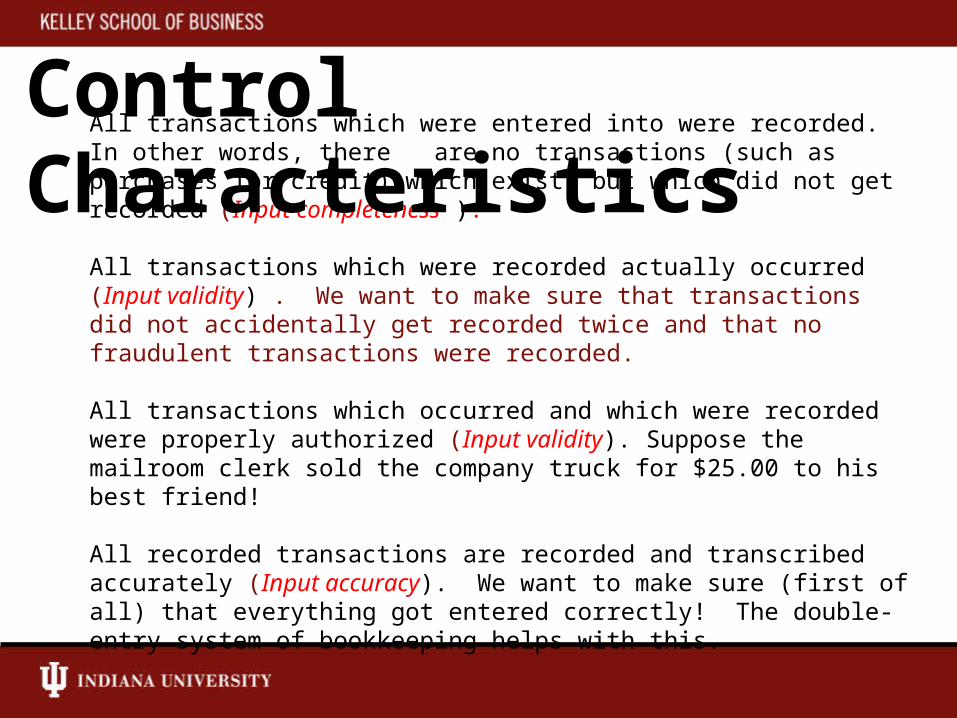

All transactions which were entered into were recorded. In other words, there are no transactions (such as purchases for credit) which exist, but which did not get recorded (Input completeness ).

All transactions which were recorded actually occurred (Input validity) . We want to make sure that transactions did not accidentally get recorded twice and that no fraudulent transactions were recorded.

All transactions which occurred and which were recorded were properly authorized (Input validity). Suppose the mailroom clerk sold the company truck for $25.00 to his best friend!

All recorded transactions are recorded and transcribed accurately (Input accuracy). We want to make sure (first of all) that everything got entered correctly! The double-entry system of bookkeeping helps with this.

Control Characteristics

Transaction cycles • When a company sells its product, it increases

one asset (either cash or accounts receivable) and decreases another (inventory).

• Profit comes from the difference in value between the asset received and the asset given up.

• We can think of the sale and purchase of inventory as cycles. You continually have to purchase new items to sell or you will go out of business.

Sale

Increase A/RDecrease Invty

Purchase/Acct.Payable/Cash Disbursements

Cycle

PurchaseInventory

Paymentof A/P

Cash Receipt

cashincreases

cashdecreases

Billing/Acct. ReceivableCash Receipts

Cycle

Invty increases

Knowledge about the relationships between sales, accounts receivable, and cash receipts (inventory, purchases, accounts payable, and cash disbursements) can be used to decrease the possibility of errors and theft.

Example ProblemA customer calls and says that he received an invoice from your company and that he never purchased anything.

SolutionEstablishing documentation procedures that tie recorded transactions to existing transactions.

The Sales Transactions Players•Sales manager

•Accounts Receivable clerk

•Shipping Clerk

•Mailroom clerk

•Cashier

•General Ledger Clerk

What role does each perform?

Sales and Cash

Receipts

Sales(approving the transaction)

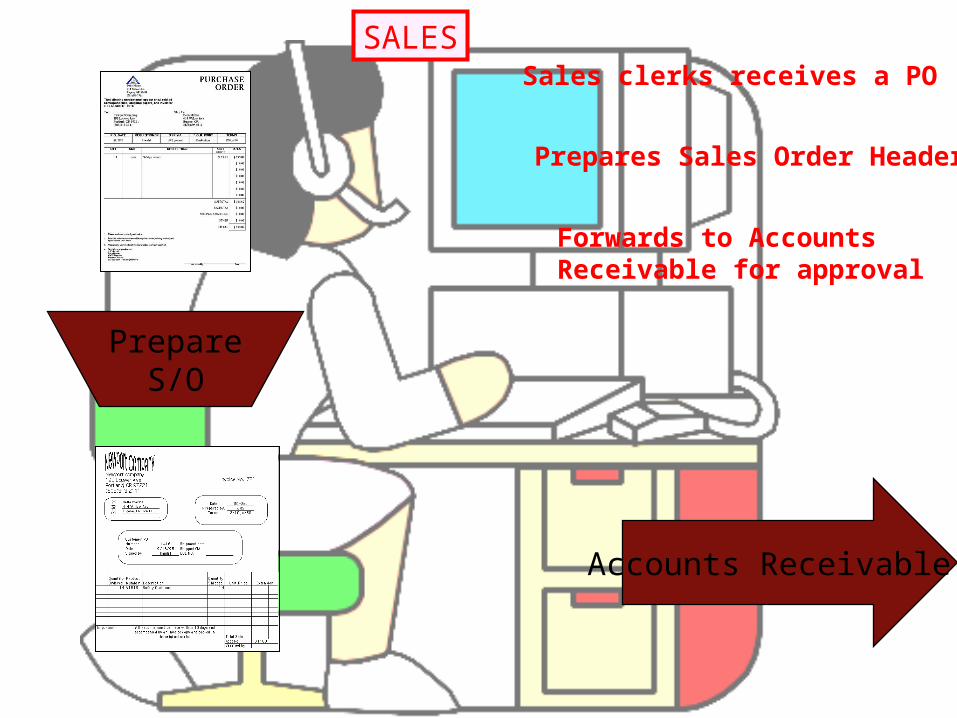

•Sales Dept: From the Purchase Order, fill out the Charge Sale Invoice document, leaving blank the “verified by” space then give it to A/R. This is a Sales Order Header.

•Accts Receivable: Approve the transaction and complete the Sales Order. This will be an invoice when the items have been shipped. Send 2 copies of the invoice to Shipping (one is a packing slip). Send an “approved” copy back to Sales.

•Sales Dept:Send the vendor acknowledgement back to the customer. Inform the customer of the sales order number for future correspondence, give them someone to contact and an estimated date.

Sales (executing the transaction)

•Shipping:

Fills the order, notes the quantity shipped and computes the extension and total sale. Sends a copy to the customer (as a packing slip).

Fills in the BOL# and returns to A/R.

•Accts Receivable:

Record the account receivable in the A/R subsidiary ledger (This is like a file for this particular customer).

Send a copy of the complete invoice to the G/L department.

Send a copy of the complete invoice to the customer.

Sales(recording the sale in the General Journal)

•G/L department (accounting)

Record the invoice from Accounts Receivable.

Sales clerks receives a PO

Forwards to Accounts Receivable for approval

Accounts Receivable

Prepares Sales Order Header

PrepareS/O

SALES

Approves the transaction and annotates the SO header makingit a Sales Order

Returns Sales Order to salesclerk.

Checks the A/R subsidiaryledger

Approved

Sales

Send copies to shipping (one isPacking Slip)

Sh

ipp

ing

A/R

Approved

Customer

PrepareV/A

Prepare vendor acknowledgement

Send to customer

SALES

Approved Fills the order, notes the quantity shipped and computes the extension and total sale. Sends a copy to the customer (as a packing slip).

Invoice

A/R

w/

BO

L

Cu

stom

er

Fills in the BOL# and returns to A/R.

SHIPPING

InvoiceRecord the account receivable in the A/R subsidiary ledger (This is like a file for this particular customer).

Send a copy of the complete invoice to the G/L department.

Send a copy of the complete invoice to the customer.

G/L

Invoice Invoice

Cu

stom

er

A/R

Record the invoice from Accounts Receivable.

Invoice

Accts. Rec XXX Sales XXX

G/L