25

Accounting Information: Users and Uses C H A P T E R 1

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | delphia-stephens |

| View: | 219 times |

| Download: | 0 times |

Accounting Information:Users and UsesAccounting Information:Users and Uses

C H A P T E R 1

Learning Objective 1

Describe the purpose of accounting and explain its role in business and society.

What are the functions of anaccounting system?

Analyze business events to determine if information should be captured by the accounting system.

Analysis

Day-to-day keeping track of things.

Bookkeeping

Use summary information to evaluate the financial health and performance of the business.

Evaluation

What is the Nature of Accounting? Explain What Each Term Means.

Deals with numbers.Quantitative

Focused on the financial dimension of business.

Financial

Supported by a theoretical conceptual framework.

Useful

Past information can only be useful if it impacts decisions about the future.

Decision Making

What Are the Four Steps of the Decision-making Process?

1Step

Identify the issue

2Step

Gather information

3Step

Identify alternatives

4Step

Select the option that will most

likely result in the

desired objective

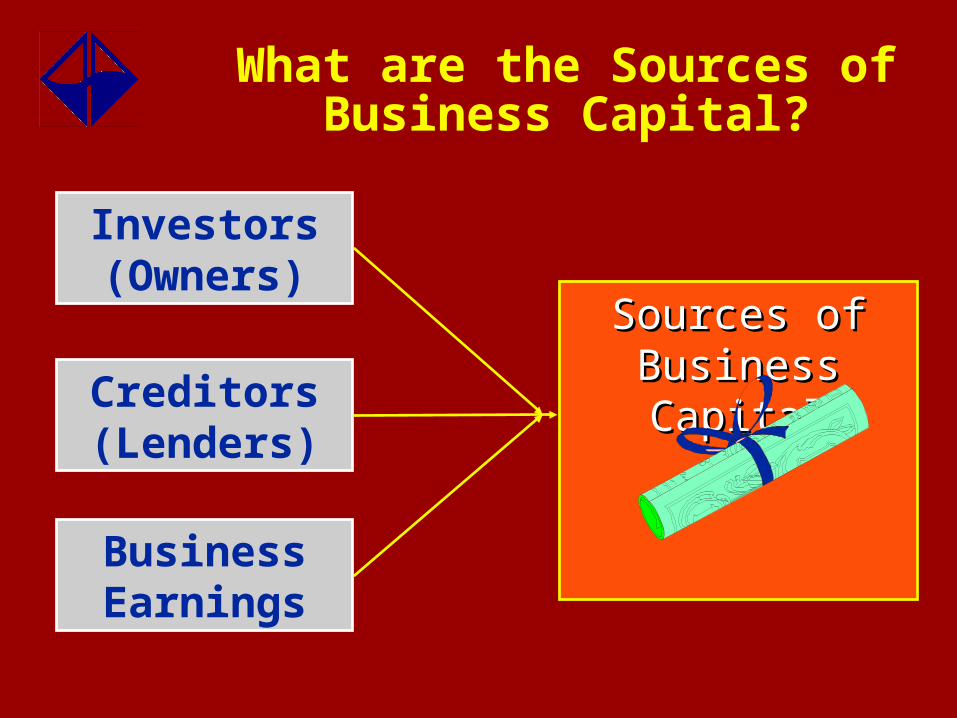

Sources of Sources of Business CapitalBusiness Capital

What are the Sources of Business Capital?

Creditors (Lenders)

Business Earnings

Investors (Owners)

Uses of Business Resources

What are Uses of Business Resources?

Buy materials and supplies

Buy land, buildings, and equipment

Pay employees

Pay other operating expenses

Why Do Businesses Perform the Following Functions?

To produce and market goods and services (resulting in revenues)

Buy materials and supplies

Buy land, buildings, and equipment

Pay employees

Pay other operating expenses

How is the Revenue a Business Generates Used?

Produce and market goods and services (resulting in revenues)

Pay a return to owners

Pay loans

Pay taxes

Continue business activity

Learning Objective 2

Identify the primary users of accounting information.

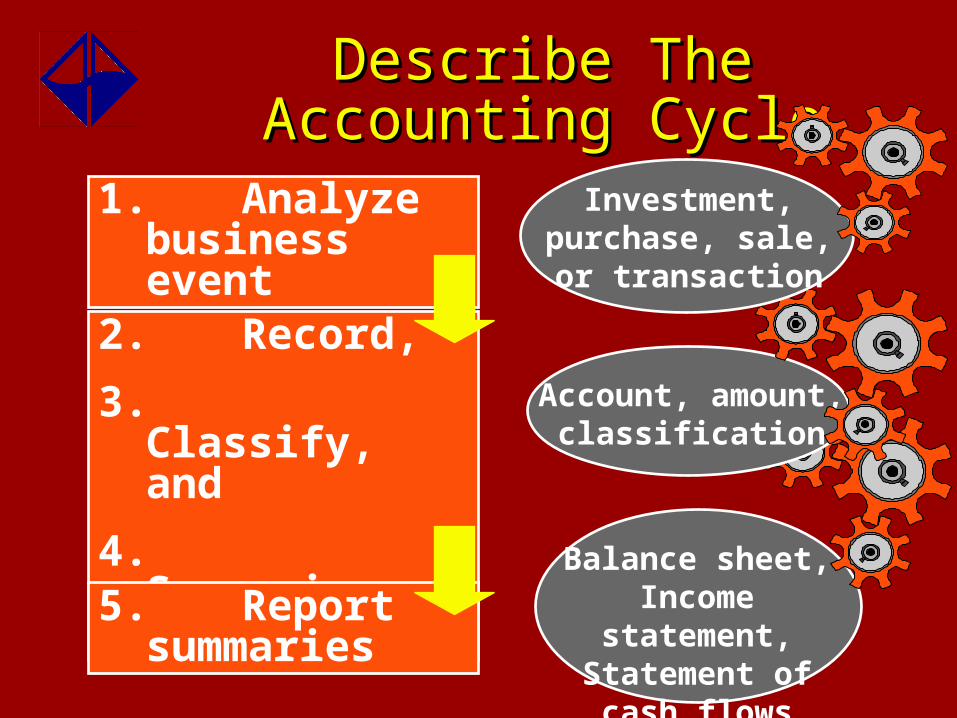

1. Analyze business event

Describe The Accounting Describe The Accounting CycleCycle

2. Record,

3. Classify, and

4. Summarize transaction

5. Report summaries

Balance sheet, Income statement, Statement of cash

flows

Account, amount, classification

Investment, purchase, sale, or

transaction

What are the Two Types of Reports from Accounting Information?

Internal Reports(Management Accounting)

External Reports(Financial Accounting)

Management

LendersInvestors

Suppliers/CustomersEmployees

CompetitorsGovernment Agencies

The Press

What Are Accounting Reports Used For?

Used by management for

• planning• implementing plans• controlling costs• making decisions

Used by external parties who have an economic interest in the firm.

• Balance sheet• Income statement• Statement of cash flows

Learning Objective 3

Describe the environment of accounting, including the effects of generally accepted accounting principles, international business, ethical considerations, and technology.

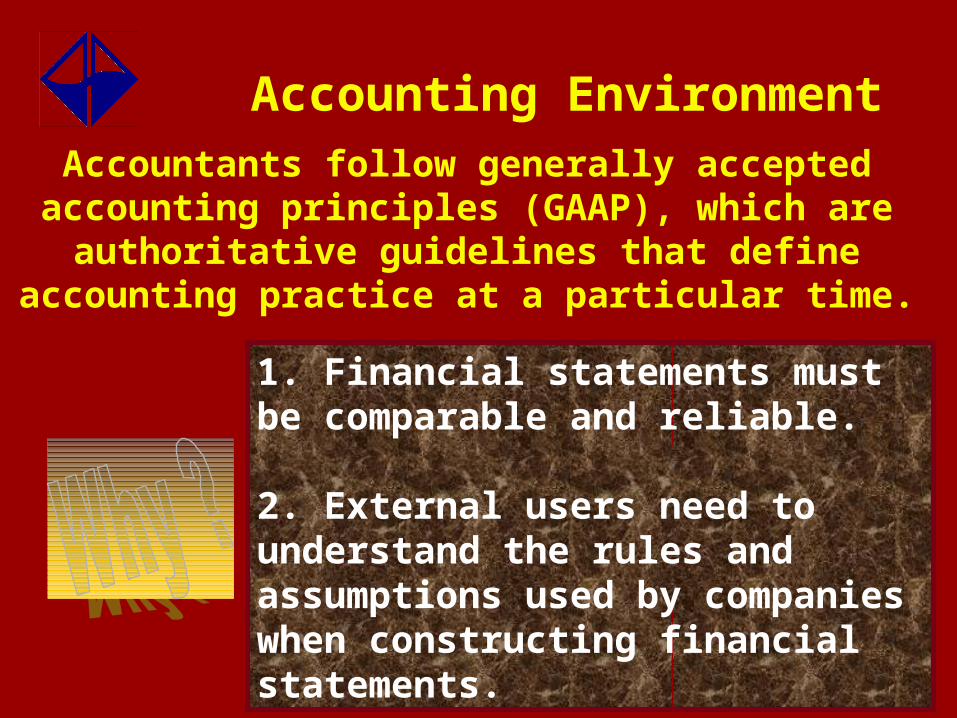

Accounting EnvironmentAccountants follow generally accepted accounting

principles (GAAP), which are authoritative guidelines that define accounting practice at a

particular time.

1. Financial statements must be comparable and reliable.

2. External users need to understand the rules and assumptions used by companies when constructing financial statements.

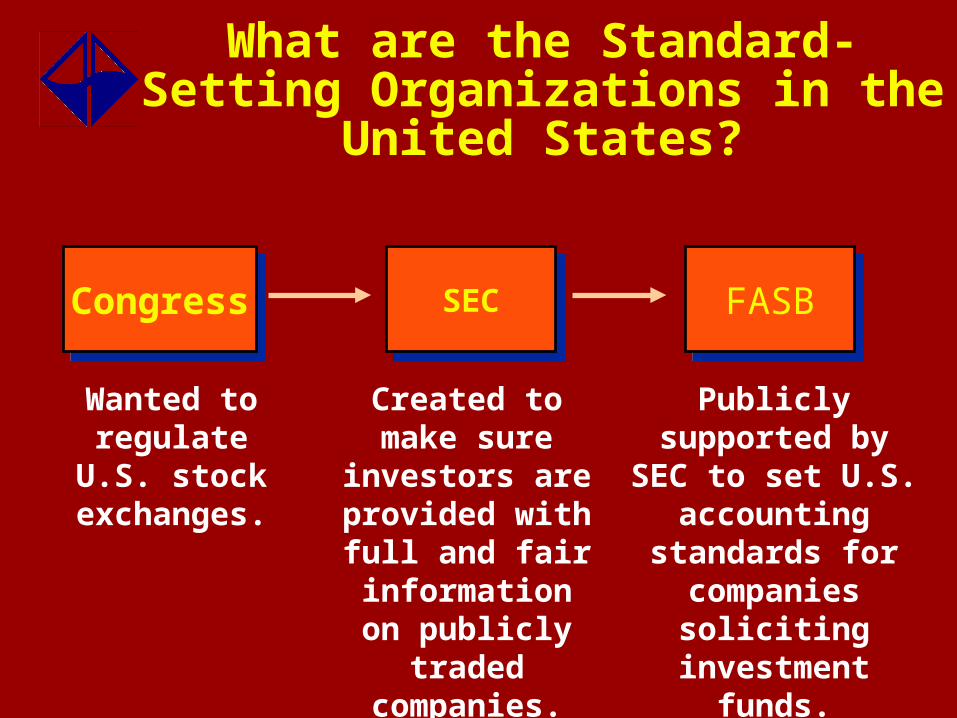

What are the Standard-Setting Organizations in the United States?

CongressCongress

Wanted to regulate U.S.

stock exchanges.

SECSEC

Created to make sure investors are provided

with full and fair information on publicly traded

companies.

FASBFASB

Publicly supported by SEC to set U.S.

accounting standards for

companies soliciting

investment funds.

What is a CPA?

CPA: Certified Public Accountant

• Has taken a minimum number of college-level accounting classes.

• Has passed the exam administered by the AICPA.• Has met other requirements set by his/her state.

AICPA: American Institute of Certified Public Accountants

• The national organization of CPAs in the U.S.• Not a government agency.

Name Some Other Accounting Organizations

AICPA: American Institute of Certified Public AccountantsNational organization of certified public accountants (CPAs)

IMA: Institute of Management AccountantsNational organization of management accountants (CMAs)

IRS: Internal Revenue ServiceGovernment agency--prescribes rules and regulates the collection of tax revenues in the U.S.

SEC: Securities and Exchange CommissionCreated by Congress to regulate U.S. stock exchanges.

IASC: International Accounting Standards CommitteeFormed to develop worldwide accounting standards.

The Code of Professional Conduct.

Adopted by the AICPA.

Holds to what three key principles?

Integrity

Objectivity

Independence

Ethics in Accounting

Members are subject to

disciplinary action.

What are Three Advantages of Technology?

Allows companies to easily gather vast amounts of information about individual transactions.

Allows large amounts of data to be compiled quickly and accurately, significantly reducing error.

Creditors and investors can receive and process large amounts of data.

Why Doesn’t Technology Replace People?

Because technology does not replace judgment.

People must still analyze situations and input results.

People must still analyze output.

Learning Objective 4

Analyze the reasons for studying accounting.

Why Study Accounting?

Everyone makes financial decisions.What types of decisions?

Budgeting Investing

Buying vs. leasing

Financing

Accounting Opportunities

Industry

Government or Nonprofit

GraduateEducation

PublicAccounting Auditor

Tax Consultant

Management Advisory Services

Consultant

Controller

Internal Auditor

Financial Executive

Government Agencies: GAO,

IRS, FBI

State and Local Agencies

Hospitals, Schools, Nonprofit

Organizations

J.D. (Law)

Ph.D.

M.Acc.

MBA

The End of Chapter One

![1-1 1 Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting is. [2] Identify the users and uses of accounting.](https://static.documents.pub/doc/80x56/56649dc55503460f94ab8f91/1-1-1-learning-objectives-after-studying-this-chapter-you-should-be-able-to.jpg)