17

Accounting Practices 501 Chapter 6 Inventory (Periodic system) Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

| Date post: | 04-Jan-2016 |

| Category: |

Documents |

| Upload: | bertram-flynn |

| View: | 219 times |

| Download: | 4 times |

Accounting Practices 501

Chapter 6

Inventory

(Periodic system)

Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

Periodic System

Ch6B - Periodic system

This is a system, whereby the inventory is manually counted before

cost of sales can be calculated

Periodic System

• Regular stocktakes necessary• Uses a Purchases expense account• Cost of sales to be manually calculated• Inventory levels only known after a

physical stocktake is done• Closing inventory figure becomes the

opening inventory figure in the next period

Ch6B - Periodic system

Example of calculating COS

Ch6B - Periodic system

Opening inventory Add Purchases

Cost of Sales

$50,000

Less Closing inventory

60,000110,00

040,000$70,000

Other items could also be included

Ch6B - Periodic system

Opening inventory

Add Purchases

Cost of Sales

$50,000

Add Customs Duty

Add Freight In

Less Closing inventory

58,00010,0005,000

123,00040,000$83,00

0

Any costs incurred in getting the product ready for sale, are included in the cost of sales

Ch6B - Periodic system

Opening inventory

Add Purchases

Cost of Sales

$50,000

60,000110,00

040,000$70,000

Where did we get the Opening inventory figure from?

From last year’s Inventory figure

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

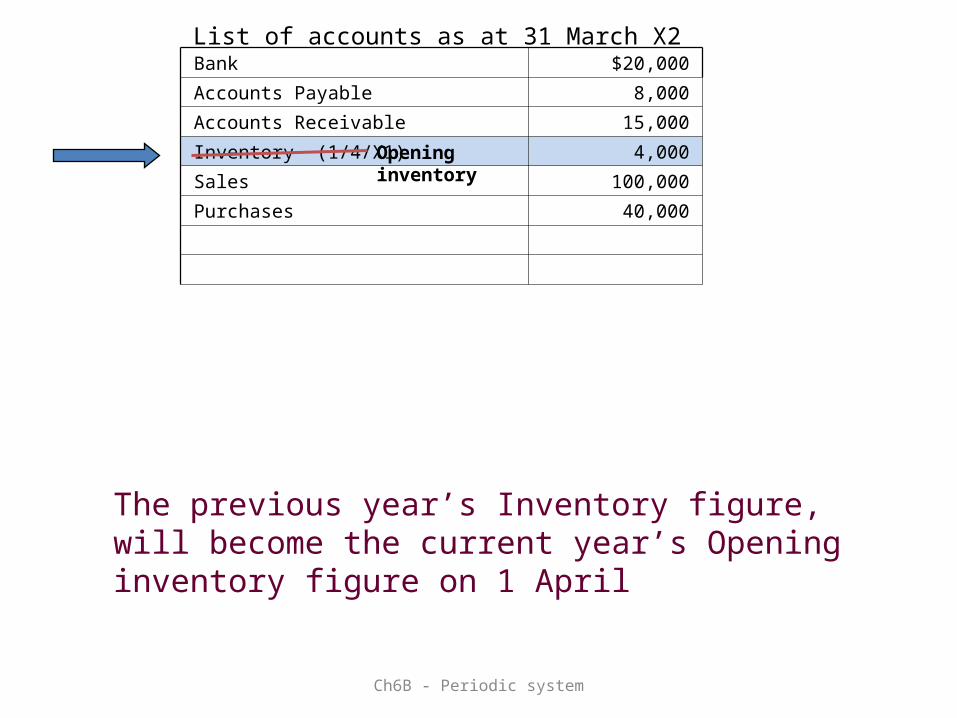

Let’s have a look at a list of accounts

List of accounts as at 31 March X2

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

The previous year’s Inventory figure, will become the current year’s Opening inventory figure on 1 April

List of accounts as at 31 March X2

Opening inventory

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

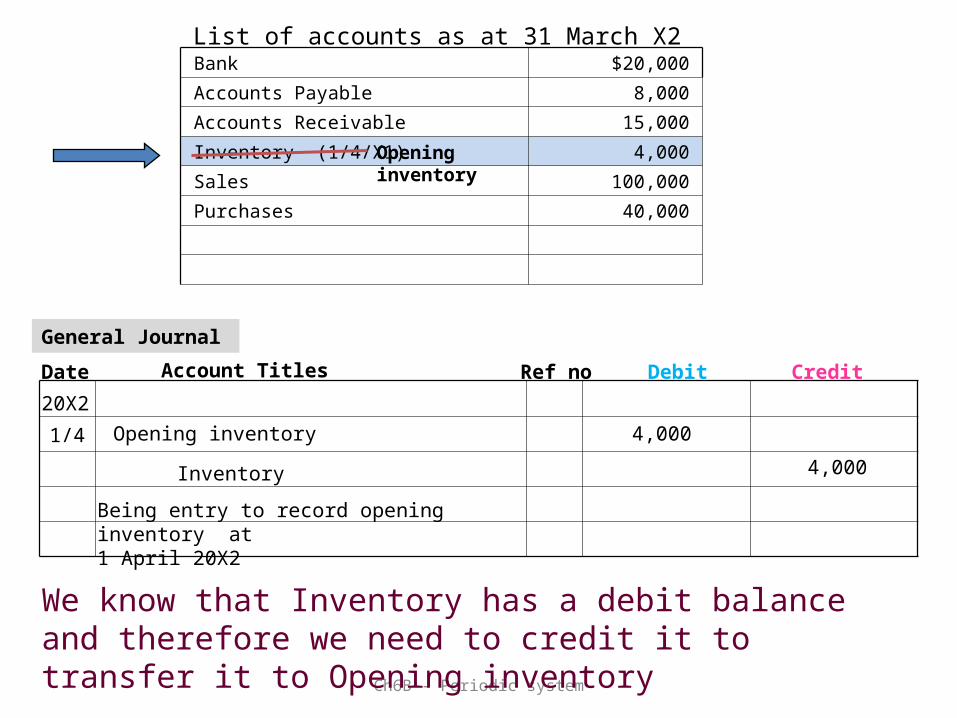

List of accounts as at 31 March X2

Opening inventory

We know that Inventory has a debit balance and therefore we need to credit it to transfer it to Opening inventory

General Journal

Date Account Titles Ref no Debit Credit

1/4 Opening inventory 4,000

Inventory 4,000

Being entry to record opening inventory at 1 April 20X2

20X2

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

List of accounts as at 31 March X2

Opening inventory

But, what about the Closing inventory figure?

After a stocktake has been done at the end of the period (31 March), we need to record the

value of the counted stock

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

List of accounts as at 31 March X2

Opening inventory

The Inventory account at this stage shows a zero balance after the transfer to the Opening inventory account

Closing inventory 15,000

15,000Inventory

The counted stock at 31 March represents the Inventory current asset of the business

The counted stock at 31 March also represents the Closing inventory used to calculate the cost of sales

Let’s say that the counted stock at 31 March X2 is $15,000

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

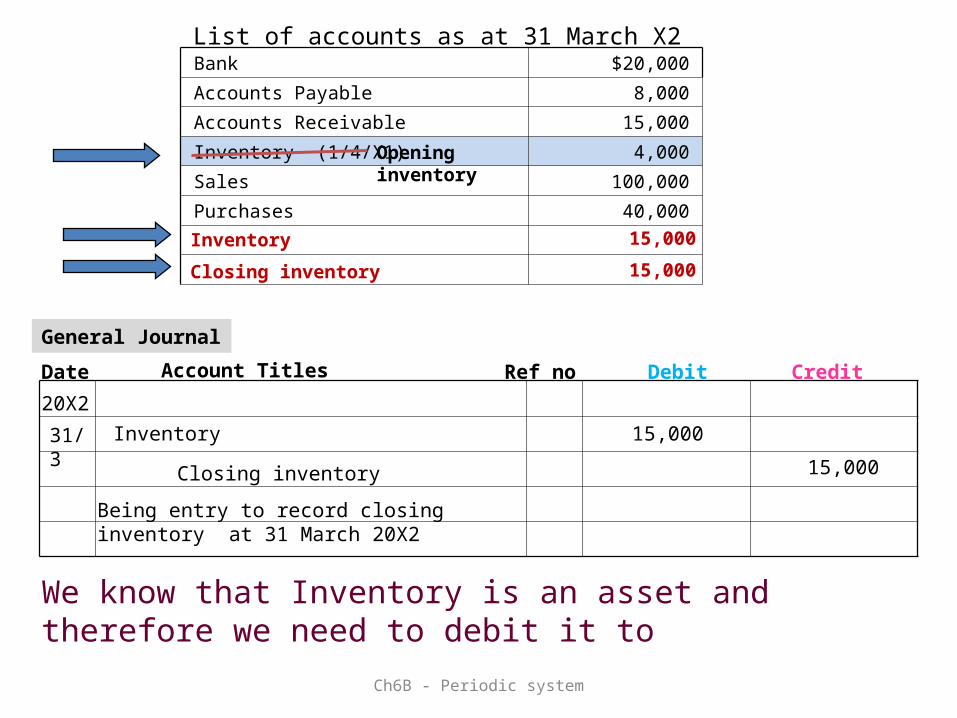

List of accounts as at 31 March X2

Opening inventory

Now let’s do it the proper way with debits and credits

Closing inventory 15,000

15,000Inventory

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

List of accounts as at 31 March X2

Opening inventory

We know that Inventory is an asset and therefore we need to debit it to

General Journal

Date Account Titles Ref no Debit Credit

31/3 Inventory 15,000

Closing inventory 15,000

Being entry to record closing inventory at 31 March 20X2

20X2

Closing inventory 15,000

15,000Inventory

Bank $20,000

Accounts Payable 8,000

Accounts Receivable 15,000

Inventory (1/4/X1) 4,000

Sales 100,000

Purchases 40,000

Ch6B - Periodic system

List of accounts as at 31 March X2

Opening inventory

Let’s see what we have so far!

Closing inventory 15,000

15,000Inventory

Date

General Ledger

Details BalINVENTORY

Opening Balance 4,000 Dr

OPENING INVENTORY

31/3Opening inventory NIL 4,000

1/4 Inventory 4,000 4,000 Dr

CLOSING INVENTORY31/3 Inventory 15,000 15,000 Cr

31/3 Closing inventory 15,000 15,000 Dr

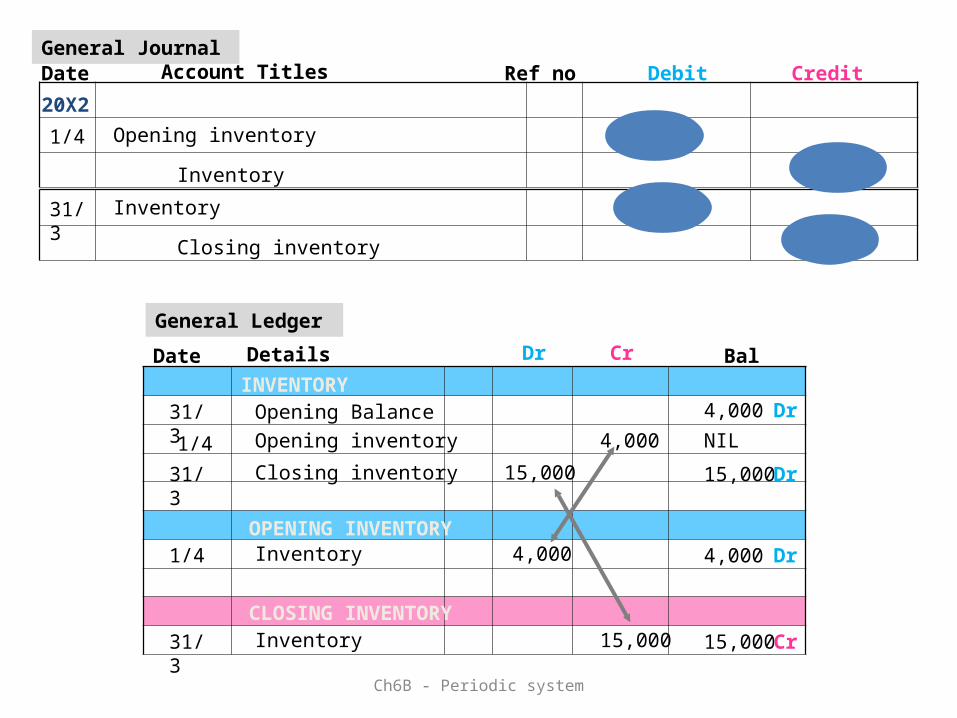

General JournalDate Account Titles Ref no Debit

1/4 Opening inventory 4,000

Inventory 4,000

20X2

Credit

31/3 Inventory 15,000

Closing inventory 15,000

1/4

Ch6B - Periodic system

Dr Cr

Closing inventory and Opening inventory figures are used to calculate the Cost of Sales in the Income Statement

Ch6B - Periodic system

Inventory is a current asset shown in the Balance Sheet

Date

General LedgerDetails Dr Cr BalINVENTORY

Opening Balance 4,000 Dr

OPENING INVENTORY

31/3Opening inventory NIL 4,000

1/4 Inventory 4,000 4,000 Dr

CLOSING INVENTORY

31/3 Inventory 15,000 15,000 Cr

31/3 Closing inventory 15,000 15,000 Dr

1/4

Don’t we justlove

Accounting?

Ch6B - Periodic system