Prepared for the Asian SBO by the Government Accounting & Finance Statistics Center Korea Institute of Public Finance Accounting Reform in the Korean Government John M. Kim Korea Institute of Public Finance

Transcript

Prepared for the Asian SBO by the Government Accounting & Finance Statistics Center

Korea Institute of Public Finance

Accounting Reform in the Korean Government

John M. Kim Korea Institute of Public Finance

Presenter

Presentation Notes

Distinguished Guests, Ladies and Gentlemen, Good morning.�I'm Jaeseek Park, Director General of the Treasury Bureau at the Ministry of Strategy and Finance. It is my great honor to be here with many renowned experts from home and broad at this conference, despite their busy schedules. In particular, President of CAPA, 주인기 (In-ki Joo) and Chief Executive, Brain Blood! I would like to extend my sincere appreciation for your hard work to prepare for this meaningful conference to be held in Korea. Also, I want to express my thanks to President of KICPA, 권오형 (O-hyoung Kwon), who put continuous support for successful venue of today’s conference. �Ladies and gentlemen, I would like to extend a heartfelt welcome to ‘2011 CAPA IPSAS Conference’ in Korea where spring changes everywhere with green leaves. We gathered here today at this conference to discuss an accounting standard in the public sector. Therefore, we highly hope that this conference will be a great help for government accounting not only in Korea, also in Asian region. We also believe that this conference will give a momentum to develop the accounting system in the public sector around the globe. Today, I'm delighted to be here to talk about the accrual-based accounting system implemented in the Korean government. So, from now on, let me explain the implementation of government accrual accounting system in Korea. Before we move on to the main session, I will brief on some background information of what we’ve achieved so far and future tasks in progress, first. .

Reform of national accounting system in Korea

Three-year roadmap for new national accounting system

Government Accounting and Finance Statistics Center

Financial Reporting

2

Presenter

Presentation Notes

I’m going to divide this talk into five parts. As you can see, first, I'll talk about the reform of Korea’s national accounting system and the legal framework for national accounting regulations. And then I’ll go on to a three-year roadmap for a new accrual-based accounting system and what we have achieved so far. Next, I'll talk about our tasks in progress. Lastly, I’m going to conclude by summing up the main points in our implementation of the new national accounting system.

I. Reform of national accounting system in Korea

From when accrual?

1. Background of the reform

The reform of national accounting system emerged as an issue during the

1997 economic crisis, in the context of the government’s counter-crisis reform

measures

Why accrual? Improve accuracy of the government’s financial position through objective

valuation of its assets and liabilities

Solidify the foundation for fiscal management, incorporating long-term

financial projections

3

Presenter

Presentation Notes

First, let me talk about the reform of Korea’s national accounting system. The reform of national accounting system has been discussed publicly since the 1997 economic crisis when the government made financial reforms to overcome the crisis. At that time, Korea used a cash-based accounting system but the system was ineffective in reflecting a complicated financial situation. The government has adopted an accrual-based national accounting system for establishing the foundation of long-term fiscal management through accurate analysis and projections of the national financial position.

History of accrual reforms

1998 The Ministry of Finance and Economy develops roadmap to introduce the accrual-based accounting to the entire government by 2003

2003 Roadmap revised to postpone introduction of accruals • To be phased in from 2009 to 2012 • Cash-based budgeting and accruals-based reporting

2007 The National Accounting Act enacted • Korean Financial Management Info. System (KFMIS) established • Accruals-based CFR required by FY2011

2009 Accrual-based national accounting begins (pilot basis until FY2011)

I. Reform of national accounting system in Korea

1. Background of the reform, continued

4

Presenter

Presentation Notes

Now let’s move on to the reform of Korea’s national accounting system. After the financial crisis of 1997, the Korean government publicly announced the introduction of an accrual-based national accounting system in May 1998. Subsequently, the Ministry of Finance and Economy developed a roadmap for the reorganization of governmental accounting system to introduce the accrual-based system to the entire government by 2003. However, it took an unexpectedly longer time to reorganize previous systems and establish new ones. The government revised the roadmap as there was a need for more research to introduce the accrual-based national accounting system. And some visible achievements were made as a result of sustained efforts by the government. These achievements include the establishment of the National Accounting Act and the Korean Financial Management Information System in 2007. In 2009, the Korean government fully implemented the accrual-based national accounting system.

National Accounting Standards

5 Supplementary

Standards

National Accounting Act and Enforcement Decree

• Process of settlement of accounts • Preparation of financial reports

• Types of financial statements and principles for preparation

• Recognition and valuation of national assets and liabilities, etc.

19 Technical Releases

• Technical guidance for certain transactions

I. Reform of national accounting system in Korea

2. Structure of the Korean national accounting system

5

Presenter

Presentation Notes

This slide shows the structure of the Korean national accounting system. A legal framework for the national accounting system has been established on the basis of the National Accounting Act, which deals with matters on the preparation of financial reports. National Accounting Act and its Enforcement Decree prescribe basic matters on the national accounting system. National Accounting Standards prescribe the types of financial statements and principles for preparation. They also cover matters on recognition and valuation of national assets and liabilities. In addition, there are 5 supplementary standards (Standards of Cost Accounting, Subsidized Loans, Pensions, Insurances, Guarantees) and 19 Technical Releases. These technical guidance play a role as technical guidance of accounting for significant transactions.

II. 3-yr roadmap for new national accounting system

6

Organizing operating system

Strengthening accounting personnel

Building infrastructure

2010

2011

2012

On-spot inspection and evaluation on Social Overhead Capital

Submission of CFR to the National Assembly

Completion of accounting methods regarding provisions

Development of indicators for financial analysis

Revision of the related laws to recruit officials specialized in accounting

Operation of TFT to support for preparing FS

Customized trainings for certain officials

Recruitment of officials specialized in accounting

Establishment of the National Accounting Standards Center

Inclusion of national accounting in the CPA examination Introduction of reinforcement program on national accounting for accounting firms

Introduction of certified professions in national accounting

Presenter

Presentation Notes

Now, let me go to the next slide, the roadmap from 2009 to 2011 for the new national accounting system. We prepared various strategies to improve reliability and transparency of the financial management system. First, we develop methodologies to prepare financial statements. Second, we secure the expertise of officials in charge of government accounting by recruiting those who are specialized in accounting. Of course, we also enhance the quality of relevant training programs. Third, we build infrastructure to support the new national accounting system for its continuous development. Fourth, we hold workshops for officials, carry out communication with people through the media, and publish booklets to help people’s understanding of the national accounting system. I’d like to expand on the current status of detailed programs under each strategy – in other words, main achievements and tasks in progress - from the next slide.

III. Government Accounting and Finance Statistics Center

What is the GAFSC?

GAFSC provides support in improving the national accounting system and producing reliable fiscal statistics

(July 26, 2010) Establishment of the National Accounting Standards Center(the NASC)

NASC begins as private-sector entity, legally entrusted by MoSF (Ministry of Strategy & Finance) with setting and improving national accounting standards (Article 11 of the National Accounting Act)

(Jan 2, 2014) NASC integrated into 'the Government Accounting and Finance Statistics Center' which is an affiliated organization of the Korea Institute of Public Finance (public sector)

7

Presenter

Presentation Notes

3개년 로드맵의 결과 탄생한 국가회계기준센터를 소개해 드리겠습니다. 국가회계기준센터는 한 마디로 국가회계기준의 설정과 개선을 지원하는 기관입니다. 기획재정부가 국가회계법 제11조에 의거하여 한국공인회계사회에 위탁한 기관으로, 주요 임무는 국가회계기준의 설정과 개선입니다. 국가회계기준센터는 2010년 7월 26일 설립된 이래 국가회계에 발생주의 기준을 성공적으로 정착시키기 위해 노력해왔습니다.

III. Government Accounting and Finance Statistics Center

Organization of GAFSC

※ Numbers in parenthesis refer to the number of persons in each team

Administration (2)

Director

National Accounting Standards Advisory Committee

National Accounting Team (13)

Finance Statistics Team (9)

8

Presenter

Presentation Notes

다음으로 국가회계기준센터의 조직구성을 소개해 드리겠습니다. 국가회계기준센터는 편호범 소장님의 지휘 아래 운영되고 있으며, 국가회계기준자문위원회가 자문을 제공합니다. 총 (22 )명으로 구성된 전체 조직은 크게 재무통계부, 평가분석부, 행정팀으로 나눠집니다. 재무통계부는 결산팀, 통계팀, 공공기관팀으로 이루어져 있고, 평가분석부는 원가팀, 자산팀, 부채팀으로 이루어져 있습니다. 괄호 안의 숫자는 각 팀별 인원수를 나타냅니다.

III. Government Accounting and Finance Statistics Center

Main Activities

1. Issuing/Revising Accounting Standards Accounting standard Issuing(3): Accounting standard for Pensions, Loan Guarantees and Insurance

Practical guidelines issuing(6) & revising(14): Accounting for subsidized loans, Revaluation of PP&E and Infrastructure Assets, etc.

2. Producing reliable financial information

Producing National government financial statement : including general account(1), special account(18) and fund(65)

3. Producing government finance Statistics

Compilation and presentation of general government finance statistics in accordance with ’01 GFS(Government Finance Statistics) IMF

Compilation and presentation of public sector debt statistics in accordance with PSDS(Public Sector Debt Statistics) OECD

9

Presenter

Presentation Notes

다음으로 국가회계기준센터의 비전과 임무, 그리고 목표를 소개해드리겠습니다. 국가회계기준센터의 비전은 정부의 재무정보가 완벽히 보고되도록 함으로써 회계책임성을 강화하고 의사결정에 필요한 정보를 충분히 제공하는 것입니다. 그리고 결산보고서 이용자들이 유용한 정보를 얻고, 일반 대중이 재무정보를 쉽게 이해할 수 있도록 국가회계기준을 설정하고 개선하는 것을 임무로 삼고 있습니다. 마지막으로 국가회계기준센터의 목표는 수준 높은 국가회계기준을 정착시켜 공공에 대한 국가의 회계책임성을 확보하고 의사결정에 유용한 정보를 생산하며 성공적인 결산업무를 지원하는 것입니다.

Q&A

FAQ

III. Government Accounting and Finance Statistics Center

Q & A System

10

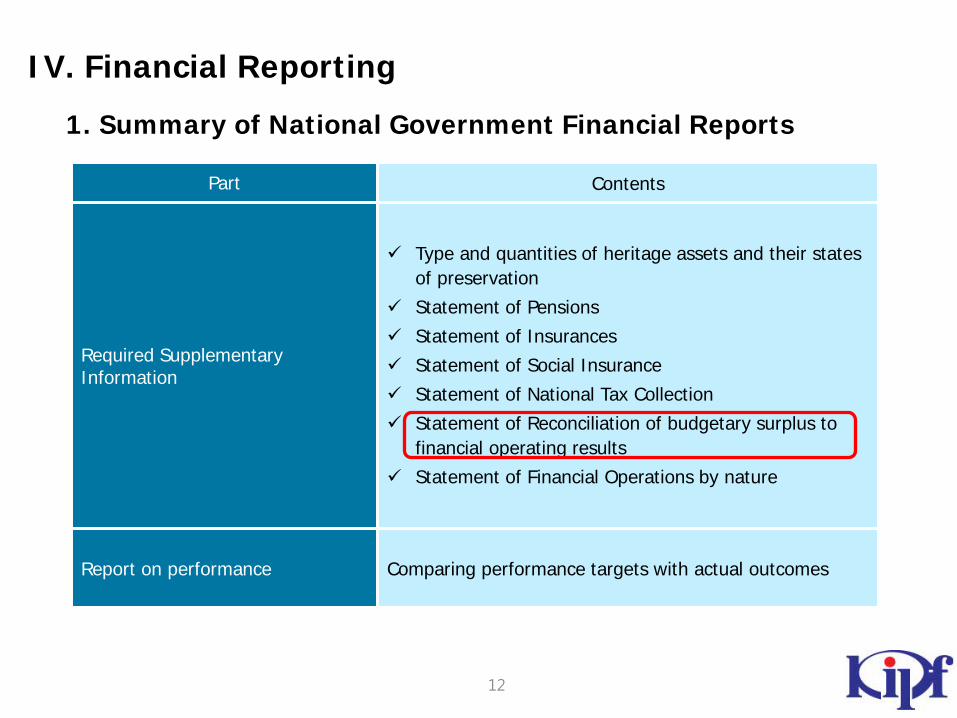

1. Summary of National Government Financial Reports

IV. Financial Reporting

Part Contents

MD&A Reporting on results of budget execution Summary of financial position and results of financial

operations

Budgetary Reports

Reporting on planned and actual budget realization in cash basis accounting

Presentation of all cash inflow and outflow including issuance or repayment of public debt

Financial Statements • Statement of Financial Position • Statement of Financial

Operations • Statement of Changes in Net

Assets

Preparation in accordance with the National Accounting Standards

No statement of cash flows Consolidated statements (requires FMIS, similarly to

TSA)

Notes and supplementary schedules

Explanation for major accounting policies and factors which have an significant impact on financial statements

11

1. Summary of National Government Financial Reports

IV. Financial Reporting

Part Contents

Required Supplementary Information

Type and quantities of heritage assets and their states of preservation

Statement of Pensions Statement of Insurances Statement of Social Insurance Statement of National Tax Collection Statement of Reconciliation of budgetary surplus to

financial operating results Statement of Financial Operations by nature

Report on performance Comparing performance targets with actual outcomes

12

IV. Financial Reporting

Corporate Income Statement Statement of Financial Operations at a Ministry or Agency level

Sales (revenues) Costs of sales Gross profit Selling and administrative expenses (classified by nature) Operating income Other income (expenses) Income (loss) before income taxes Income taxes Net income

xxx (xxx) xxx

(xxx)

xxx xxx xxx

(xxx) xxx

Program A Gross Costs less: exchange revenue Net costs Program B

.... Management expenses Non-distribution expenses less: non-distribution revenues Net operating costs Non-exchange revenues and others Financial operating results

xxx

(xxx) xxx xxx ... xxx xxx

(xxx) xxx xxx xxx

Unlike the corporate income statement, the statement of financial operations is focused on cost information by program. So, revenue is classified into exchange revenues and non-exchange revenues in calculating net cost of each program.

2. Statement of Financial Operations

Format of Statement of Financial Operations

13

IV. Financial Reporting

3. Financial statement for FY2013

14

Statement of Financial Position

Statement of Financial Operations

Current Assets

Investments

Property, Plant and Equipment

Infrastructure Assets

Intangible Assets

Other Non-Current Assets

275.9

533.6

481.9

279.0

1.1

7.5

Current liabilities

Long-term Debts

Provisions for Pension

Other Provisions

Other Non-Current Liabilities

102.9

329.6

565.0

35.6

26.3

Total Liabilities 1,059.4

Total Assets 1,579.0 Net Assets 519.6

(in billions of USD)

(in billions of USD)

Net Operating Costs

Non-exchange revenues

260.9

233.6

Fiscal Operating results 27.3

IV. Financial Reporting

4. Statement of Financial position FY2009 ~ FY2013

15

Statement of Financial Position (in billions of USD)

FY2009 FY2010 FY2011 FY2012 FY2013

Total Assets 863.1 936.5 1,445.1 1,497.5 1,579.0 Total Liabilities 321.9 354.5 733.0 854.8 1,059.4 Net Assets 541.2 582.0 712.1 642.7 519.6

Provisions for Pension - - 324.2 (VBO)

414.0 (ABO)

565.0 (PBO)

*Scope: budget accounts and state funds (central government “budgetary” in following slide)

IV. Financial Reporting

General Government Public Corporations

Public Sector

Central Government

Local Government

Budgetary nonmarket NPIs

Financial Public Corporations

NonFinancial Public Corporations

Budgetary nonmarket

NPIs ※ NPIs: nonprpfit institutions

Central Gov

General Gov

Public Sector

Gross Debt 442.2 478.2 778.1

GDP % 34.7 39.7 64.5

(in billions of USD)

5. Public Sector debt statistics for FY2012

16

※ CFR excludes financial public corporations

※ Public sector debt excludes pension provisions for National Pension and Private Teachers’ Pension, regarded as implicit liabilities