Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 1

Accrual accounting and budgetary accounting

reflecting on current reform Flemish local

governments (PMC = BBC) cycle

Prof. dr. Johan Christiaens

Ghent University Belgium

Accounting Research Public Sector UGent – EY

Registered auditor EY

Seminar EY 13th May 2016 – UGent © 2016

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 2

Agenda

1. Introduction

2. Balance sheet and profit / loss account

3. Accrual accounting

4. Budgetary accounting

5. Reform Flemish local governments

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 3

1. Introduction

• Since years mid ‘80: worldwide governmental reforms (Hood, 1991 and 1995):

New Public Management (NPM) - Outputoriented instead of input- or processingoriented

- Management techniques from entreprises

- Quantifying service providing and performance measurement

- Transparency

- Efficiency and value-for-money audit

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 4

1. Introduction (2)

• Heterogeneous governmental accounting systems – Within countries:

• Different approaches and rules for national, regional and local governments; musea, schools, health care,

• “Diverging” convergence New Public Management

• Different combinations budgetary accounting – accrual accounting

– Amongst countries:

• Heterogeneity due to differing reforms and differing subsidizing

• Different accounting frameworks: for economic info, for oversight bodies, for macro-economic purposes, for world bank, etc.

– International organisations

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 5

1. Introduction (3)

• Dissatisfaction about government’s

– Accounting practices

– Reporting to Parliament, citizens and stakeholders

– Need for transparency and reporting financial

position and financial performance (accrual

accounting)

• Criticism

– “Home made”, too heterogeneous

– Incomplete, often changing

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 6

1. Introduction (4)

• Cornerstone of New Public Management:

Reform of the accounting system and financial reporting

Adoption of businesslike accrual accounting next to

existing, traditional budgetary accounting (often wrongly

named ‘cash accounting’; budgetary accounting is a

system of authorizing budgets and recording

encumbrances and finally receipts and disbursements to

control the public purse whereas cash accounting is only

recording receipts and disbursements)

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 7

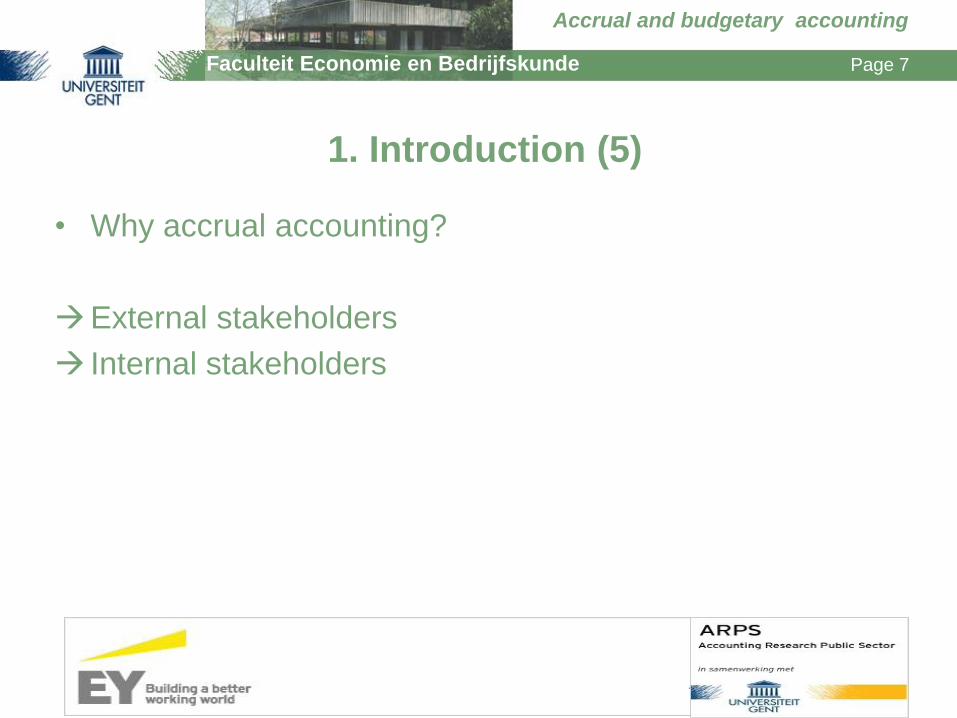

1. Introduction (5)

• Why accrual accounting?

External stakeholders

Internal stakeholders

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 8

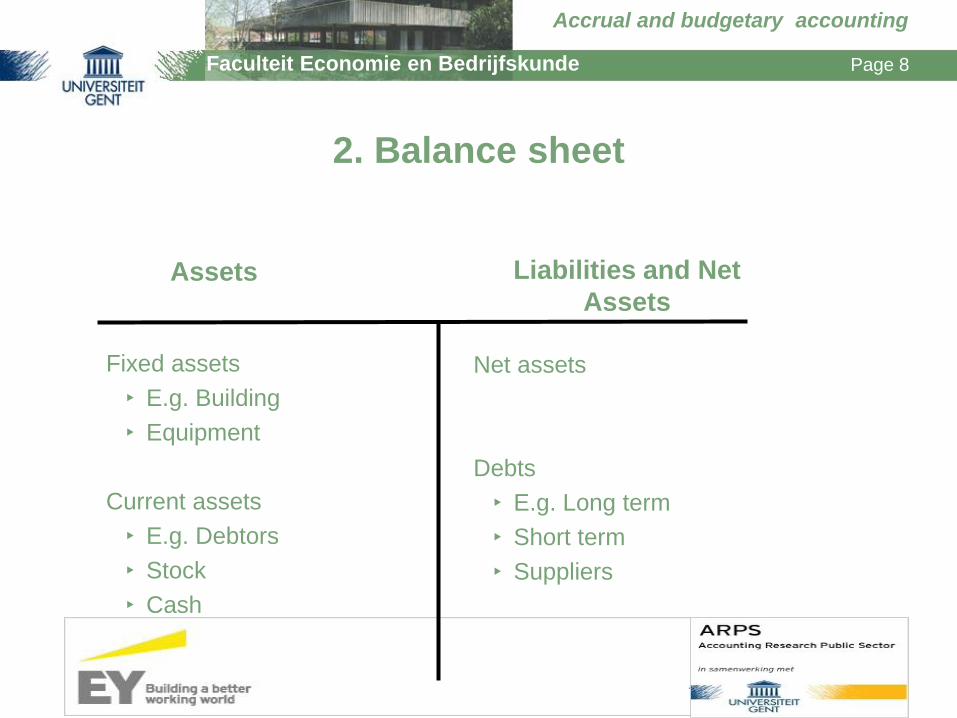

2. Balance sheet

Fixed assets

‣ E.g. Building

‣ Equipment

Current assets

‣ E.g. Debtors

‣ Stock

‣ Cash

Net assets

Debts

‣ E.g. Long term

‣ Short term

‣ Suppliers

Assets Liabilities and Net

Assets

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 9

2. Balance sheet and profit/loss account

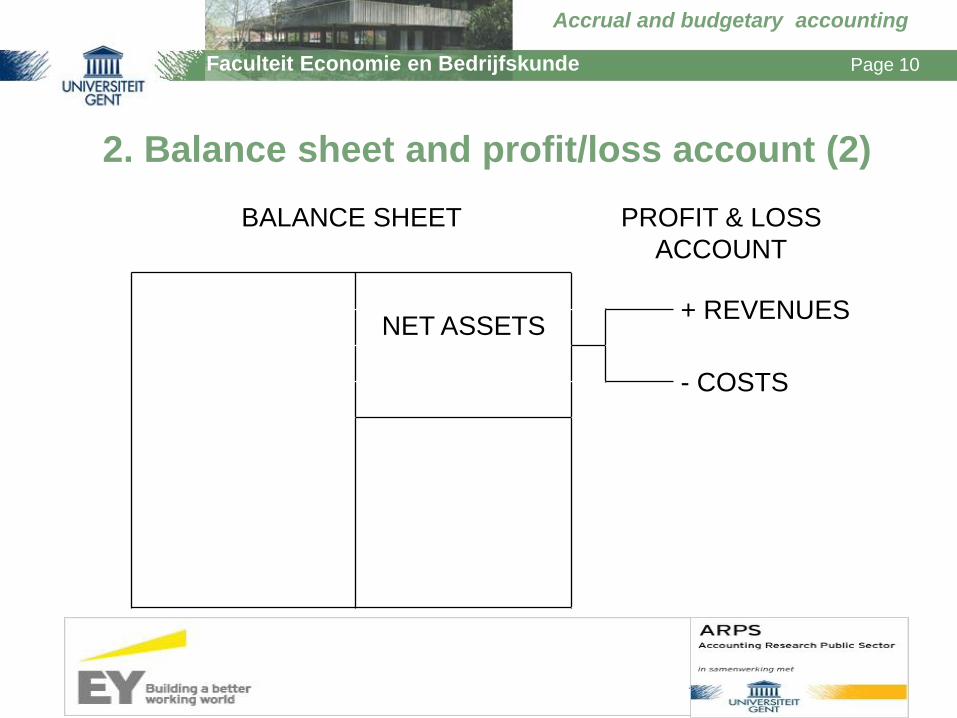

Total assets = Total liabilities + net assets

Or

Total assets – Total liabilities = Net assets

Balance sheet is like a photo at a certain moment,

e.g. as of 31st December 20N0

During the accounting period, balance sheet

undergoes changes by financial-economic

transactions, also influencing the net assets

= Revenues – Costs disclosed in the profit/loss

account

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 10

2. Balance sheet and profit/loss account (2)

BALANCE SHEET

PROFIT & LOSS

ACCOUNT

+ REVENUES

NET ASSETS

- COSTS

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 11

3. Accrual accounting

• Profit & loss account provides an overview of all revenues

and costs influencing the net assets over the accounting

period, mostly 1 year

• During the accounting period an entity will face numerous

transactions belonging to a number of administrative

cycles, e.g. purchasing cycle, investment cycle, cycle

HRM, revenues cycle, subsidy cycle, etc.

• Instead of registering alle transactions directly to the

balance sheet / profit & loss account transactions are

recorded on accounts

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 12

3. Accrual accounting (2)

General ledger

Asset account Credit Debet

Start Increase

Decrease

Liabilities and net assets account Credit Debet

Decrease Start

Increase

Cost account Credit Debet

Increase Decrease

Revenue account Credit Debet

Decrease Increase

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 13

3. Accrual accounting (3)

•Steps in accounting progress

Start accounting year:

Opening balance sheet on the accounts general ledger

During accounting year:

Recording of transactions: journal entry and posting on the accounts

End of accounting year: Provisionary balance of accounts

End of year adjustments

Definite balance of accounts

Treatment of the accounting profit or loss

Disclosure of annual accounts: balance sheet, proifit & loss account ans notes

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 14

4. Budgetary accounting

• Different aim: Authorization of budgets to spend /

to receive

• Different budgetary accounting principles

• Revealing budgetary surplus of budgetary deficit, which

≠ profit and loss

• Budgetary accounting always from budget (ex ante) to

budget accounts (ex post)

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 15

4. Budgetary accounting – accrual accounting

• In a government the approval of a budget for purchase

goods took place January 20N0 € 5,000

• 10th May 20N0 government decides that certain goods

will be ordered for estimated amount € 2,000 and these

coming spendings are “warranted”

• Purchase itself takes place 15th June 20N0 € 1,900

• After performing certain checks, the recognition of the

purchase by the treasurer happens 7th July 20N0 and

the payment will be made at the end of coming month

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 16

4. Budgetary accounting – accrual accounting

• Budgetary accounting (cameralistics) is meant to record

these stages whereas accrual accounting is only

interested in posting the consequences to P/L and

balance sheet as shown in the following table

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 17

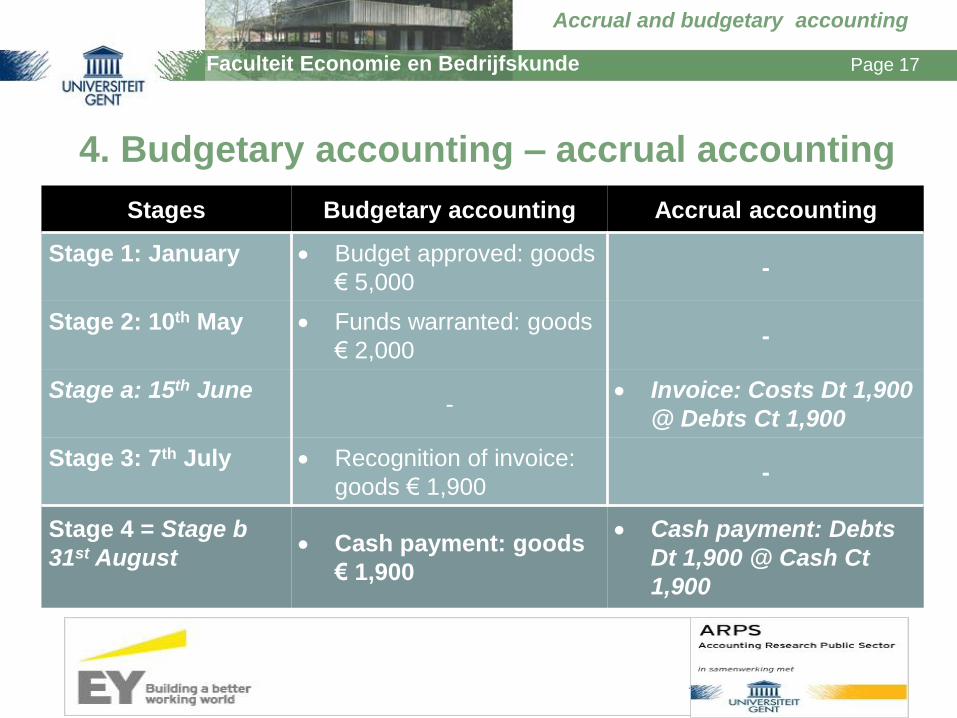

4. Budgetary accounting – accrual accounting

Stages Budgetary accounting Accrual accounting

Stage 1: January

Budget approved: goods

€ 5,000 -

Stage 2: 10th May

Funds warranted: goods

€ 2,000 -

Stage a: 15th June

-

Invoice: Costs Dt 1,900

@ Debts Ct 1,900

Stage 3: 7th July

Recognition of invoice:

goods € 1,900 -

Stage 4 = Stage b

31st August

Cash payment: goods

€ 1,900

Cash payment: Debts

Dt 1,900 @ Cash Ct

1,900

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 18

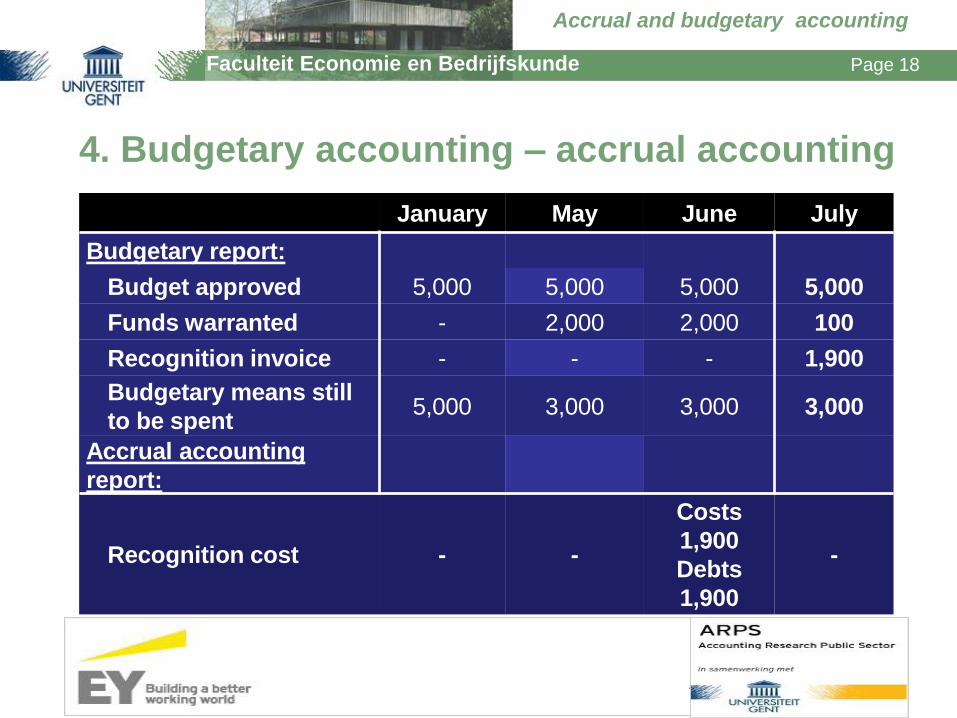

4. Budgetary accounting – accrual accounting

January May June July

Budgetary report:

Budget approved 5,000 5,000 5,000 5,000

Funds warranted - 2,000 2,000 100

Recognition invoice - - - 1,900

Budgetary means still

to be spent 5,000 3,000 3,000 3,000

Accrual accounting

report:

Recognition cost - -

Costs

1,900

Debts

1,900

-

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 19

4. Budgetary accounting – accrual accounting

• Budgetary accounting:

– Used to be the mainstream accounting and financial

reporting system in the public sector

– Still actively used in different governments / jurisdictions:

recording of different phases: approval of budgets,

appropriations, encumbrances, disbursements

– Few information concerning liabilities and the future

potential benefits of assets

– Need for better accounting information

Need for accrual accounting

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 20

4. Budgetary accounting – accrual accounting

• Accrual accounting, particularly IPSAS:

– Better suited for planning, financial management and decision-making;

– Provides a greater (internal and external) accountability of the public resources;

– Improves cost awareness (efficiency);

– Facilitates asset & cash management;

– Facilitates the recognition of risks and opportunities;

– Supports the calculation of governmental fees and charges;

– Better view on the (financial) impact of public policies;

– …

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 21

5. Reform Flemish local governments

• Since 2014, Flemish local governments are obliged to

implement the BBC-reform (‘Beleids- en Beheerscyclus’

or further referred to as PMC - Policy and Management

Cycle)

• PMC is management & accounting reform (IPSAS):

– result-orientedness

– the expression of objectives

– multi-annual planning

– transparency, decentralization, accountability, citizen

satisfaction, competition, efficiency and effectiveness

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 22

5. Reform Flemish local governments

Multi-annual Strategic plan Annual Budget Annual Accounts Strategic report Policy report Policy report

- Targets - Targets realization

Financial report

- Financial multi-annual targets - Targets budget - Targets budgetary account

- Financial equilibrium - Financial situation - Financial situation

Financial report

- Operational budget

- Investment budget

- Cash budget

Financial report

- Operational budgetary account

- Investment budgetary account

- Cash budgetary account

General accounts

- Balance sheet

- Statement of revenues and

expenses

Notes

Accrual and budgetary accounting

Faculteit Economie en Bedrijfskunde Page 23

Questions?

…