ACCT 5908 AUDITING AND ASSURANCE SERVICES Course Outline Semester 1, 2012 Part A: Course-Specific Information Part B: Key Policies, Student Responsibilities and Support Part C: Seminar Programme Australian School of Business School of Accounting

Transcript

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Course Outline Semester 1, 2012

Part A: Course-Specific Information Part B: Key Policies, Student Responsibilities and Support Part C: Seminar Programme

Australian School of Business School of Accounting

Table of Contents PART A: COURSE-SPECIFIC INFORMATION 1

1 STAFF CONTACT DETAILS 1

2 COURSE DETAILS 1

2.1 Teaching Times and Locations 1 2.2 Units of Credit 1 2.3 Summary of Course 2 2.4 Course Aims and Relationship to Other Courses 2 2.5 Student Learning Outcomes 2

3 LEARNING AND TEACHING ACTIVITIES 3

3.1 Approach to Learning and Teaching in the Course 3 3.2 Learning Activities and Teaching Strategies 3

4 ASSESSMENT 4

4.1 Formal Requirements 4 4.2 Assessment Details 4 4.3 Quality Assurance 4 4.4 Mini Quizzes 5% 4 4.5 Major Quiz 20% 4 4.6 Final Exam 55% 5 4.7 Group Assignment 20% 5

ASSIGNMENT COVER SHEET 9

5 COURSE RESOURCES 11

6 COURSE EVALUATION AND DEVELOPMENT 11

7 COURSE SCHEDULE 12

PART B: KEY POLICIES, STUDENT RESPONSIBILITIES AND SUPPORT 13

1 ACADEMIC HONESTY AND PLAGIARISM 13

2 STUDENT RESPONSIBILITIES AND CONDUCT 13

2.1 Workload 13 2.2 Attendance 13 2.3 General Conduct and Behaviour 14 2.4 Key Dates and Responsibilities 14 2.5 Occupational Health and Safety 14 2.6 Keeping Informed 14

3 SPECIAL CONSIDERATION AND SUPPLEMENTARY EXAMINATIONS 15

4 STUDENT RESOURCES AND SUPPORT 16

PART C: SEMINAR PROGRAMME 17

PART D: REVISION 34

ACCT 5908 – Auditing and Assurance Services 1

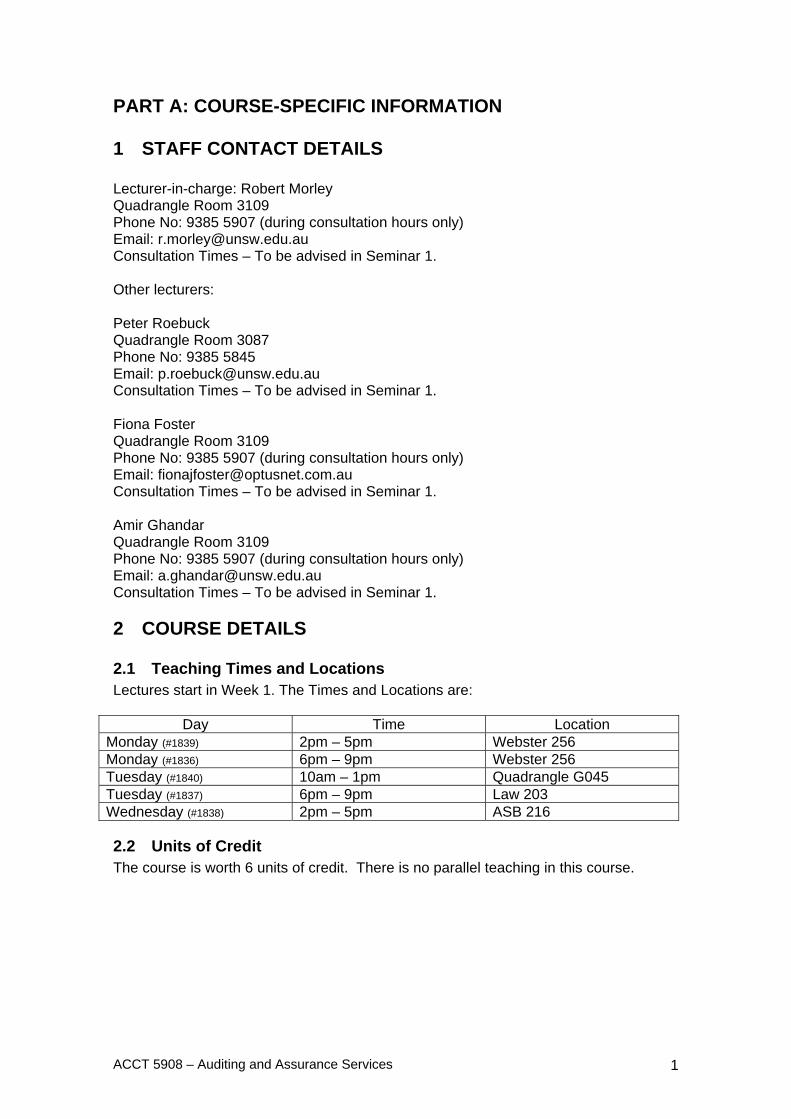

PART A: COURSE-SPECIFIC INFORMATION

1 STAFF CONTACT DETAILS Lecturer-in-charge: Robert Morley Quadrangle Room 3109 Phone No: 9385 5907 (during consultation hours only) Email: [email protected] Consultation Times – To be advised in Seminar 1. Other lecturers: Peter Roebuck Quadrangle Room 3087 Phone No: 9385 5845 Email: [email protected] Consultation Times – To be advised in Seminar 1. Fiona Foster Quadrangle Room 3109 Phone No: 9385 5907 (during consultation hours only) Email: [email protected] Consultation Times – To be advised in Seminar 1. Amir Ghandar Quadrangle Room 3109 Phone No: 9385 5907 (during consultation hours only) Email: [email protected] Consultation Times – To be advised in Seminar 1.

2 COURSE DETAILS

2.1 Teaching Times and Locations Lectures start in Week 1. The Times and Locations are:

2.2 Units of Credit The course is worth 6 units of credit. There is no parallel teaching in this course.

ACCT 5908 – Auditing and Assurance Services 2

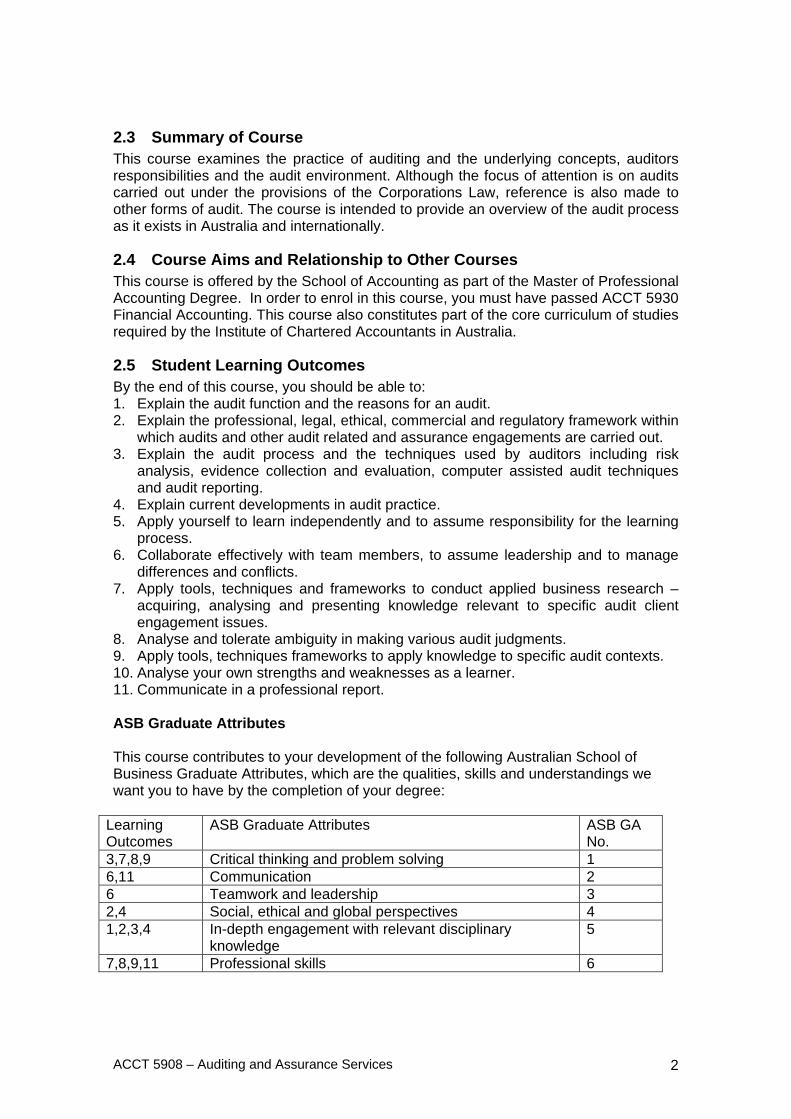

2.3 Summary of Course This course examines the practice of auditing and the underlying concepts, auditors responsibilities and the audit environment. Although the focus of attention is on audits carried out under the provisions of the Corporations Law, reference is also made to other forms of audit. The course is intended to provide an overview of the audit process as it exists in Australia and internationally.

2.4 Course Aims and Relationship to Other Courses This course is offered by the School of Accounting as part of the Master of Professional Accounting Degree. In order to enrol in this course, you must have passed ACCT 5930 Financial Accounting. This course also constitutes part of the core curriculum of studies required by the Institute of Chartered Accountants in Australia.

2.5 Student Learning Outcomes By the end of this course, you should be able to: 1. Explain the audit function and the reasons for an audit. 2. Explain the professional, legal, ethical, commercial and regulatory framework within

which audits and other audit related and assurance engagements are carried out. 3. Explain the audit process and the techniques used by auditors including risk

analysis, evidence collection and evaluation, computer assisted audit techniques and audit reporting.

4. Explain current developments in audit practice. 5. Apply yourself to learn independently and to assume responsibility for the learning

process. 6. Collaborate effectively with team members, to assume leadership and to manage

differences and conflicts. 7. Apply tools, techniques and frameworks to conduct applied business research –

acquiring, analysing and presenting knowledge relevant to specific audit client engagement issues.

8. Analyse and tolerate ambiguity in making various audit judgments. 9. Apply tools, techniques frameworks to apply knowledge to specific audit contexts. 10. Analyse your own strengths and weaknesses as a learner. 11. Communicate in a professional report. ASB Graduate Attributes This course contributes to your development of the following Australian School of Business Graduate Attributes, which are the qualities, skills and understandings we want you to have by the completion of your degree:

Learning Outcomes

ASB Graduate Attributes ASB GA No.

3,7,8,9 Critical thinking and problem solving 1 6,11 Communication 2 6 Teamwork and leadership 3 2,4 Social, ethical and global perspectives 4 1,2,3,4 In-depth engagement with relevant disciplinary

knowledge 5

7,8,9,11 Professional skills 6

ACCT 5908 – Auditing and Assurance Services 3

To see how the ASB Graduate Attributes relate to the UNSW Graduate Attributes, refer to the ASB website (Learning and Teaching >Graduate Attributes).

3 LEARNING AND TEACHING ACTIVITIES

3.1 Approach to Learning and Teaching in the Course At university, the focus is your self-directed search for knowledge. Seminars, textbooks, exams and other resources are all provided to help you learn. You are therefore required to attend all seminars and read all required readings in order to fully grasp and appreciate the concepts of Auditing and Assurance Services. It is up to you to choose how much work you do in each part of the course: preparing for seminars; completing assignments; studying for exams; and seeking assistance or extra work to extend and clarify your understanding. You must choose an approach that best suits your learning style and goals in this course. Seminar discussion questions as well as case studies with solutions are provided to guide your learning process.

3.2 Learning Activities and Teaching Strategies Instruction in this course consists of one, three hour seminar each week. Methods of presentation may include lectures, videos, discussion of case study material and student presentations. It should be emphasised that attendance at classes is a necessary but not sufficient condition for adequate examination preparation. All students should study the relevant textbook, materials prescribed, auditing standards and/or other relevant professional pronouncements, and participate in seminar discussions. The seminars constitute the core learning experience of this course. During seminars, students will be encouraged to discuss various steps in the audit process in a team environment and may be asked to present their findings in front of the class, as well as applying their knowledge to specific audit issues and situations via homework questions and class exercises. Seminar discussion questions are included as a part of this Course Outline booklet distributed during seminar 1. It is essential to your learning that, prior to a seminar, you read the relevant course materials. To assist in the development of key research and analytical skills, some of these discussion questions may require students to conduct additional research. Self study Self study is a key element of the learning design of this course. Self study materials include the auditing standards, the case studies and discussion questions included in the Course Outline. The aim of this material is to encourage students to assume responsibility in the learning process and to make the seminars more effective. Thus, onus is on students to review and complete these materials. Staff will be available in consultation hours to assist with difficulties experienced with the self study materials, but not as a substitute for seminar attendance.

ACCT 5908 – Auditing and Assurance Services 4

4 ASSESSMENT

4.1 Formal Requirements In order to pass this course, you must:

achieve a composite mark of at least 50%; and achieve a mark of at least 50% in the final exam; and make a satisfactory attempt at all assessment tasks (see below).

Major Quiz 20% 1,2,3,4,5 2,5 45 minutes Week 7 Group Assignment

20% 3,4,9 2,3,5,6 10 pages Week 10

Final Exam 55% 1,2,3,4,5,6,7,8

2,5 2 hours University Exam Period

Total 100%

4.3 Quality Assurance The ASB is actively monitoring student learning and quality of the student experience in all its programs. A random selection of completed assessment tasks may be used for quality assurance, such as to determine the extent to which program learning goals are being achieved. The information is required for accreditation purposes, and aggregated findings will be used to inform changes aimed at improving the quality of ASB programs. All material used for such processes will be treated as confidential and will not be related to course grades.

4.4 Mini Quizzes 5% Mini Quizzes will be held during seminars 4 and 11, covering material from preceding seminars. Each Mini Quiz is worth 2.5% of overall assessment. The aim of the Mini Quizzes is to provide you with the opportunity to apply material learned on the course on an on-going basis. Mini Quizzes will be graded in the seminar in which they are conducted.

4.5 Major Quiz 20% The Major Quiz will be held during seminar 7, covering material from seminars 1-6 inclusive. The Major Quiz is worth 20% of overall assessment. The aim of the Major Quiz is to provide you with ongoing feedback relating to your understanding and learning progress within the course. The Major Quiz will be a combination of short answer written and multiple choice questions aimed at testing both technical and analytical skills learned in this course. Further information regarding the Major Quiz will be provided in seminar 6.

ACCT 5908 – Auditing and Assurance Services 5

4.6 Final Exam 55% Students are required to sit for a final examination paper in this course. The exam is worth 55% of overall assessment. It will be of two hours duration and will cover the entire course, although emphasis will be given to those areas not previously examined.

4.7 Group Assignment 20% The aim of the group assignment is to test students’ ability to integrate skills learnt in Auditing and Assurance Services to analyse a real company from the auditor’s perspective and within the framework of auditing standards. The successful completion of this assignment requires extensive research on internal and external environments, operations, strategies and analysis of the annual report and other relevant information, including financial information. Students are expected to demonstrate their ability to critically evaluate various pieces of information and apply analytical skills to critically evaluate potential audit risks. An important aspect of the assignment will be to demonstrate your ability to present a written report in a professional manner. The assignment will be undertaken by groups of four/five students within the same class. Please note that it is the student’s responsibility to organise a group. Details regarding the nature of the assignment and its assessment will be provided during the first seminar. Self and peer (S&P) assessment will be involved in the determination of the final assignment mark. The aim of the S&P assessment procedure is to encourage students to co-operate with their team members, to understand the importance of managing differences and conflicts in a team environment in order to ensure the effectiveness of teamwork. Furthermore, the S&P procedures can also be used to create productive dialogues among team members, allowing students to reflect on the strengths and weaknesses of both the team and the individuals comprising the team. For more details regarding the S&P methodology refer below. The actual assignment will be distributed in seminar 2. Additional Information 1. A Group Assignment Work Plan is included below to assist your completion of this

assignment. 2. An Assignment Group Allocation Form is included below. This form will be

collected in Seminar 2 by your lecturer. 3. A Group Assignment Peer Evaluation Form is included below. Each group member

is to complete and submit this form with the group assignment (in a sealed envelope if you wish to keep the information confidential).

4. You are required to submit a half page Assignment Status Report (Refer Course Schedule). There are no marks for doing this but failure to submit or below standard submissions will incur a penalty of 5 marks for the assignment.

Submission Details 1. A hardcopy of the assignment is to be submitted to your lecturer at the beginning

of your Seminar in week 10. Any assignments received after this time will be considered late and subject to the penalty described in point 5. below. Last minute printing difficulties, computer failure or transportation problems will not constitute an adequate excuse for lateness.

2. Please keep a copy of your work.

ACCT 5908 – Auditing and Assurance Services 6

3. In accordance with University policy, each assignment must use an assignment cover sheet and all students must sign the declaration on the front of the cover sheet. A copy of this cover sheet is available within this Course Outline. No marks will be awarded to any student who does not sign the cover sheet.

4. The title page should clearly indicate the names of your team members and their student numbers, your seminar leader and the time and location of your seminar.

5. Late submissions will incur a 3 mark penalty for every day of late submission (including weekends).

Group assignment work plan

By : Seminar Activity Deliverable

2 Finalise groups of 4/5. Hand in completed ‘Assignment Group Allocation Form’ to your lecturer during Seminar 2

5 Problem scoping, gather relevant information. Prepare detailed timetable and member responsibilities to ensure timely completion.

6 – 8 Assignment near completion. Identify areas for further work and adjust timetable/responsibility allocation to ensure timely and high quality delivery.

Prepare Group Assignment Status Report for submission in week 6

10 Completion of all Assignment requirements.

Hand in assignment at the beginning of Seminar 10, along with peer assessments from each student.

ACCT 5908 – Auditing and Assurance Services 7

Assignment Group Allocation Form Seminar Details Circle as appropriate:

Day and Time: Monday 2-5/Monday 6-9/Tuesday 10-1/Tuesday 6-9/Wednesday 2-5

Lecturer: Robert Morley / Fiona Foster / Amir Ghandar / Peter Roebuck

Group Details:

Group Name: (Optional)

Group Members:

Student Names: Student Numbers:

1

2

3

4

5

ACCT 5908 – Auditing and Assurance Services 8

GROUP ASSIGNMENT COVER SHEET Overleaf – tear out and attach to the front of your group assignment

Note: All students MUST sign the declaration on the cover sheet. Failure to do so will result in a mark of zero being awarded.

I declare that this assessment item is my own work, except where acknowledged, and has not been submitted for academic credit elsewhere, and acknowledge that the assessor of this item may, for the purpose of assessing this item: Reproduce this assessment item and provide a copy to another member of the University; and/or, Communicate a copy of this assessment item to a plagiarism checking service (which may then retain a copy of the assessment item on its database for the purpose of future plagiarism checking). I certify that I have read and understood the University Rules in respect of Student Academic Misconduct. Student Signature: Date:

ACCT 5908 – Auditing and Assurance Services 10

GROUP ASSIGNMENT PEER EVALUATION FORM

The purpose of this form is to allow you to assess the amount of effort each member of your group has put into the completion of the assignment. This will have the effect of directly impacting your individual assignment mark.

You should take care to complete this form honestly.

Individual responses will be kept confidential.

In the spaces provided, list all members of your group (including yourself) and allocate a mark out of 10 to each group member to indicate their effort in completing the assignment.

Each group member’s mark will be determined using the following formula:

Assume the assignment was awarded a mark of 6/10 and you were awarded a peer evaluation average of 8/10. This would result in you receiving a final mark of 4.8 out of 10, calculated as 80 percent of 6. If you were awarded a peer evaluation average of 10/10 you would receive the full 6 marks out of 10.

Please note that the marks are NOT allocated proportionally across the group members. In other words if all the group members receive a peer evaluation average of 10/10 then using the above example everyone will receive 6 out of 10.

Seminar Details:

Seminar Day and Time:………………………………………………………………

Lecturer:…………………………………………

Group Details: Group Name (Optional): …………..……………..

Group Members: Student Names: Student Numbers: Mark out of 10:

1. Your Name and Student Number:

………………………………………………….. ….………………. ……………

Other Group Members:

2. …………………………………………………. …………………… ….………..

3. …………………………………………………. …………….. ……. ……………

4. …………………………………………………. ………………...…. ……….......

5. …………………………………………………. ………………...…. ……….......

EACH INDIVIDUAL STUDENT MUST HAND THIS FORM TO YOUR LECTURER DURING SEMINAR 10.

ACCT 5908 – Auditing and Assurance Services 11

5 COURSE RESOURCES The website for this course is on UNSW Blackboard at: http://lms-blackboard.telt.unsw.edu.au/webapps/portal/frameset.jsp 1. Prescribed Textbooks:

Roebuck P. and N. Martinov-Bennie “Case Studies in Auditing and Assurance” Lexis Nexis, 5th Edition 2010.

2. Highly Recommended References: Gay G, and R. Simnett “Auditing and Assurance Services in Australia”, McGraw-Hill, revised 4th edition, 2007.

3. The ASA Clarity Standards (Australian Auditing Standards), which may be

downloaded from the AUASB website. Students should be aware that there were significant changes in the ASA’s, effective from 2010. Consequently the purchase of previous edition textbooks should be avoided.

Both the prescribed textbook and the highly recommended reference book are available from the UNSW Bookshop.

6 COURSE EVALUATION AND DEVELOPMENT Each year feedback is sought from students and other stakeholders about the courses offered in the School and continual improvements are made based on this feedback. UNSW's Course and Teaching Evaluation and Improvement (CATEI) Process is one of the ways in which student evaluative feedback is gathered. In this course, we will seek your feedback through end of semester CATEI evaluations. As a result of this feedback, improvements are incorporated in the following semester’s programme.

ACCT 5908 – Auditing and Assurance Services 12

7 COURSE SCHEDULE

COURSE SCHEDULE Week Lecture Topic Other Activities/

Assessment Week 1 27 Feb

Introduction to the Audit Function, Assurance Framework, Professional Standards and Structure of the Profession.

Week 2 5 March

Introduction to the Audit Process – Understanding the Entity and Assessing Risk.

Week 3 12 March

Internal Control Evaluation, Mitigating Controls and Fraud Risk.

Week 4 19 March

Analytical Procedures, Risk Assessment and Materiality. Mini Quiz 1

Week 5 26 March

Audit Evidence and Use of Assertions (Part 1).

Week 6 2 April

Audit Evidence and Use of Assertions (Part 2). Assignment Status Report due

Mid-Session Break: 9 - 13 April

Week 7 16 April

Auditors Response to Risks, Audit of Complex Balances and Transactions.

Major Quiz

Week 8 23 April

Using the Work of Others, Internal Audit and Public Sector Auditing. Note: Wednesday 25th is a holiday. All Wednesday seminar students will need to attend another seminar for this week only.

Week 9 30 April

Auditing in an IT Environment – Internal Control and Substantive Testing.

Week 10 7 May

Completing the Audit Process and Audit Reporting. Group Assignment due

Week 11 14 May

Ethic, Legal Liability and Corporate Governance. Mini Quiz 2

Week 12 21 May Course Review.

Week 13 28 May NO LECTURES

ACCT 5908 – Auditing and Assurance Services 13

PART B: KEY POLICIES, STUDENT RESPONSIBILITIES AND SUPPORT

1 ACADEMIC HONESTY AND PLAGIARISM The University regards plagiarism as a form of academic misconduct, and has very strict rules regarding plagiarism. For UNSW policies, penalties, and information to help you avoid plagiarism see: http://www.lc.unsw.edu.au/plagiarism/index.html as well as the guidelines in the online ELISE and ELISE Plus tutorials for all new UNSW students: http://info.library.unsw.edu.au/skills/tutorials/InfoSkills/index.htm. To see if you understand plagiarism, do this short quiz: http://www.lc.unsw.edu.au/plagiarism/plagquiz.html For information on how to acknowledge your sources and reference correctly, see: http://www.lc.unsw.edu.au/onlib/ref.html

For the ASB Harvard Referencing Guide, see ASB Referencing and Plagiarism webpage (ASB >Learning and Teaching>Student services>Referencing and plagiarism)

2 STUDENT RESPONSIBILITIES AND CONDUCT Students are expected to be familiar with and adhere to university policies in relation to class attendance and general conduct and behaviour, including maintaining a safe, respectful environment; and to understand their obligations in relation to workload, assessment and keeping informed. Information and policies on these topics can be found in the ‘A-Z Student Guide’: https://my.unsw.edu.au/student/atoz/A.html. See, especially, information on ‘Attendance and Absence’, ‘Academic Misconduct’, ‘Assessment Information’, ‘Examinations’, ‘Student Responsibilities’, ‘Workload’ and policies such as ‘Occupational Health and Safety’.

2.1 Workload It is expected that you will spend at least ten hours per week studying this course. This time should be made up of reading, research, working on exercises and problems, and attending classes. In periods where you need to complete assignments or prepare for examinations, the workload may be greater. Over-commitment has been a cause of failure for many students. You should take the required workload into account when planning how to balance study with employment and other activities.

2.2 Attendance Your regular and punctual attendance at lectures and seminars is expected in this course. University regulations indicate that if students attend less than 80% of scheduled classes they may be refused final assessment.

ACCT 5908 – Auditing and Assurance Services 14

2.3 General Conduct and Behaviour You are expected to conduct yourself with consideration and respect for the needs of your fellow students and teaching staff. Conduct which unduly disrupts or interferes with a class, such as ringing or talking on mobile phones, is not acceptable and students may be asked to leave the class. More information on student conduct is available at: https://my.unsw.edu.au/student/atoz/BehaviourOfStudents.html

2.4 Key Dates and Responsibilities It is your responsibility to ensure that: 1. You are recorded by the University as being correctly enrolled in all your courses. 2. You have successfully completed all prerequisite courses. Any work done in

courses for which prerequisites have not been fulfilled will be disregarded (unless an exemption has been granted), and no credit given or grade awarded.

3. You abide by key dates:

You must enrol by Sunday 26th February. Monday 27th February is the first day of Semester 1 lectures. Sunday 4th March is the last day you can change your enrolment and timetable via myUNSW, and is also the due date for Semester 1 fees. Saturday 31st March (end Week 5) is the last day to discontinue without financial penalty (census date). FEE-HELP applications must also be lodged before this date. Sunday 22nd April (end Week 7) is the last day to discontinue without academic penalty.

4. You organise your affairs to take account of examination and other assessment dates where these are known. Be aware that your final examination may fall at any time during the semester’s examination period. The scheduling of examinations is controlled by the University administration. No early examinations are possible. The examination period for Semester 1, 2012, falls between Friday 8th June and Monday 25th June (provisional dates subject to change).

5. When the provisional examination timetable is released, ensure that you have no clashes or unreasonable difficulty in attending the scheduled examinations.

6. Schools in the ASB schedule a common date for any supplementary exams that may be required. For Semester 1, the relavant date is:

10th July 2012 – exams for the School of Accounting

A full list of UNSW Key Dates is located at: https://my.unsw.edu.au/student/resources/KeyDates.html

2.5 Occupational Health and Safety UNSW Policy requires each person to work safely and responsibly, in order to avoid personal injury and to protect the safety of others. For more information, see http://www.ohs.unsw.edu.au/.

2.6 Keeping Informed You should take note of all announcements made in lectures, tutorials or on the course web site. From time to time, the University will send important announcements to your university e-mail address without providing you with a paper copy. You will be deemed to have received this information. It is also your responsibility to keep the University informed of all changes to your contact details.

ACCT 5908 – Auditing and Assurance Services 15

3 SPECIAL CONSIDERATION AND SUPPLEMENTARY EXAMINATIONS

You must submit all assignments and attend all examinations scheduled for your course. You should seek assistance early if you suffer illness or misadventure which affects your course progress. General Information on Special Consideration:

1. For assessments worth 20% or more, all applications for special consideration must go through UNSW Student Central (https://my.unsw.edu.au/student/academiclife/StudentCentralKensington.html) and be lodged within 3 working days of the assessment to which it refers.

2. If an assessment task is worth less than 20% of the total course assessment, UNSW Student Central will not accept the special consideration unless the student can provide a Medical Certificate that covers three consecutive days.

3. Applications will not be accepted by teaching staff, but you should notify the lecture-in-charge when you make an application for special consideration through UNSW Student Central;

4. Applying for special consideration does not automatically mean that you will be granted a supplementary exam;

5. Special consideration requests do not allow lecturers-in-charge to award students additional marks.

Special Consideration and the Final Exam: Applications for special consideration in relation to the final exam are considered by an ASB Faculty panel to which lecturers-in-charge provide their recommendations for each request. If the Faculty panel grants a special consideration request, this will entitle the student to sit a supplementary examination. No other form of consideration will be granted. The following procedures will apply:

1. Supplementary exams will be scheduled centrally and will be held approximately two weeks after the formal examination period. The date for ASB supplementary exams for Session 1, 2012 is 10 July 2012. If a student lodges a special consideration for the final exam, they are stating they will be available on the above dates. Supplementary exams will not be held at any other time.

2. Where a student is granted a supplementary examination as a result of a request for special consideration, the student’s original exam (if completed) will be ignored and only the mark achieved in the supplementary examination will count towards the final grade. Failure to attend the supplementary exam will not entitle the student to have the original exam paper marked and may result in a zero mark for the final exam.

If you attend the regular final exam, you are extremely unlikely to be granted a supplementary exam. Hence if you are too ill to perform up to your normal standard in the regular final exam, you are strongly advised not to attend. However, granting of a

ACCT 5908 – Auditing and Assurance Services 16

supplementary exam in such cases is not automatic. You would still need to satisfy the criteria stated above. Special consideration and assessments other than the Final exam: No supplementary assessments are available other than for the final exam.

4 STUDENT RESOURCES AND SUPPORT The University and the ASB provide a wide range of support services for students, including:

ASB Education Development Unit (EDU) (www.business.unsw.edu.au/edu) Academic writing, study skills and maths support specifically for ASB students. Services include workshops, online and printed resources, and individual consultations. EDU Office: Room GO7, Ground Floor, ASB Building (opposite Student Centre); Ph: 9385 5584; Email: [email protected]

Blackboard eLearning Support: For online help using Blackboard, follow the links from www.elearning.unsw.edu.au to UNSW Blackboard Support / Support for Students. For technical support, email: [email protected]; ph: 9385 1333

UNSW Learning Centre (www.lc.unsw.edu.au ) Academic skills support services, including workshops and resources, for all UNSW students. See website for details.

Library training and search support services: http://info.library.unsw.edu.au/web/services/services.html

IT Service Centre: Technical support for problems logging in to websites, downloading documents etc. https://www.it.unsw.edu.au/students/index.html UNSW Library Annexe (Ground floor)

UNSW Counselling and Psychological Services (http://www.counselling.unsw.edu.au) Free, confidential service for problems of a personal or academic nature; and workshops on study issues such as ‘Coping With Stress’ and ‘Procrastination’. Office: Level 2, Quadrangle East Wing; Ph: 9385 5418

Student Equity & Disabilities Unit (http://www.studentequity.unsw.edu.au) Advice regarding equity and diversity issues, and support for students who have a disability or disadvantage that interferes with their learning. Office: Ground Floor, John Goodsell Building; Ph: 9385 4734.

ACCT 5908 – Auditing and Assurance Services 17

PART C: SEMINAR PROGRAMME

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Course Introduction Introduction to Audit Function, Assurance Framework, Professional Standards and Structure of the Profession

SEMINAR 1: 27 February 2012

Reading Guide:

References:

Gay and Simnett, Chapters 1 and 2.

Standards:

*ASA 200: Overall Objectives of the Independent Auditor and the conduct of an Audit in Accordance with the Australian Auditing Standards.

Discussion Questions:

1. Discuss the concept of “assurance” in an audit setting.

2. With reference to Woolworths Limited Financial statements:

(a) Describe the objective of an independent audit.

(b) Distinguish between (1) management's and (2) auditor's responsibility for the financial reports being audited.

(c) Explain the meaning of ‘true and fair’/’fairly’ presented in the audit report.

* Please note, it is essential that students familiarise themselves with the key references (identified by *) prior to each seminar.

Note: This course requires students to apply their skills learnt in Auditing and Assurance Services to analyse a real company from the auditor’s perspective and within the framework of the auditing standards. As such we require students to download / review the 2011 Woolworths Group Limited annual report from either the Woolworths (www.woolworthslimited.com.au) or ASX websites, to be used in class from next seminar to answer various seminar discussion questions.

ACCT 5908 – Auditing and Assurance Services 18

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Introduction to the Audit Process - Understanding the Entity and Assessing Risk

SEMINAR 2: 5 March 2012

NOTE: COMPLETE AND HAND IN ‘ASSIGNMENT GROUP ALLOCATION FORM’.

Reading Guide:

References:

Roebuck and Martinov-Bennie, Chapter 1, Introductory Readings, (pp.2-6)

Gay and Simnett, Chap.6 (pp.177-179 and 265-275)

Standards:

* ASA 240 The Auditor’s Responsibility to consider Fraud in an Audit of a Financial Report

* ASA 300: Planning an Audit of a Financial Report

ASA 320: Materiality in Planning and Performing an Audit

* ASA 315: Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatements

Discussion Questions

1. Roebuck and Martinov-Bennie, Chapter 8, Question 5 (p.162).

2. Identify the types of information in the client's minutes of the board of directors' meetings that are likely to be relevant to the auditor. Explain why it is important to read the minutes early in the engagement.

3. When an auditor has accepted an engagement from a new client who is a manufacturer, it is customary for the auditor to tour the client's plant facilities. Discuss the ways in which the auditor's observations made during the course of the plant tour will be of assistance as he/she plans and conducts the audit.

4. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 2, Question 3, part 1 (p.240).

5. Prepare a SWOT analysis (Strengths, Weaknesses, Opportunities, Threats) of Woolworths’ to present in the class. For the purposes of the SWOT analysis:

(a) Refer to the entire Woolworths group of companies within the one SWOT analysis.

(b) Assess at least five(5) key issues for each of the SWOT factors.

ACCT 5908 – Auditing and Assurance Services 19

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Internal Control Evaluation, Mitigating Controls and Fraud Risk

SEMINAR 3: 12 March 2012

Note : Mini Quiz 1 will be held in seminar 4.

Reading Guide:

References:

* Gay and Simnett, Chapter 8 (pp.352-380), Chapter 9 (pp.420-450).

* Roebuck and Martinov-Bennie, Chapter 2 Readings (pp.32-35).

* Roebuck and Martinov-Bennie, Cases 2-2 (p.36) and Solution (p.266); Chapter 10, Mock Final Examination 1, Question 3 (p.230) and Solution (p.235).

Standards:

* ASA 315: Understanding the Entity and Its Environment and Assessing the Risk of Material Misstatements.

* ASA 240: The Auditor’s Responsibilities Relating to Fraud in an Audit of a Financial Report.

Discussion Questions

1. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 3, Question 1 part 1 (p.244).

2. Roebuck and Martinov-Bennie, Case 2-4 Parts 1 and 2 (p.40).

3. Roebuck and Martinov-Bennie, Case 2-1 (p.36).

4. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 2, (Mid Semester) Question 2 (p.239).

5. Review the Corporate Governance note for Woolworths Limited and comment on the relevance of the information provided on the auditor’s control evaluation, and complete Roebuck and Martinov-Bennie Case 1-7, section 3 (p.25).

6. Roebuck and Martinov-Bennie, Chapter 2, Case 2-5, p.41.

ACCT 5908 – Auditing and Assurance Services 20

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Analytical Procedures, Risk Assessment and Materiality

SEMINAR 4: 19 March 2012

Note : Mini Quiz 1 will be held in this seminar. Reading Guide: References: Gay and Simnett Chp.6 (pp.275-287). * Roebuck and Martinov-Bennie, Chapter 1, (p.4-5) * Roebuck and Martinov-Bennie, Chapter 10, revise Practice Examination 1, Question 1 and Solution (p.227, p234).

Standards: * ASA 315: Understanding the Entity and Its Environment and Assessing the Risks

of Material Misstatements. * ASA 320: Materiality in Planning and Performing an Audit. * ASA 520: Analytical Procedures. Discussion Questions 1. Planning is critical to the conduct of a financial statement audit. (The attached

five (5) year statistical summary should be used to answer the following). Required: Determine relevant areas and issues for consideration for the 2010 audit.

2. Analytical procedures provide a means of identifying unusual fluctuations caused by potential material errors or irregularities. For each of the following "unusual fluctuations", describe an error or the situation that could have occurred, given no change in circumstances. (a) The number of employees has increased along with total wage

expenses. However, the provision for long service leave account balance has reduced significantly.

(b) Sales for a retail store have increased by 20% during the year.

However, merchant fees (credit card charges) have remained constant.

3. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 2 (Mid-Session), Question 1 (p.238).

ACCT 5908 – Auditing and Assurance Services 21

4. During the course of an audit engagement, an independent auditor must address the concept of materiality. This concept is inherent in the work of the independent auditor and is important for planning, evidence gathering, error evaluation and in the audit opinion formation process.

Required:

(a) Briefly describe what is meant by the independent auditor's concept of materiality.

(b) Outline the relevance of materiality during each of the following stages of the audit process:

Planning Evaluation of the results of audit testing Forming an audit opinion

(c) Discuss the process of setting audit materiality.

5. Roebuck and Martinov-Bennie, Case 1-7 complete section 5 (p.25-27).

6. Roebuck and Martinov-Bennie, Chapter 8, Question 45 (p.167).

7. Roebuck and Martinov-Bennie, Case 3-5, Part B (p.57-58).

8. How should the auditor go about determining “Performance Materiality” as defined in ASA 320.9?

ACCT 5908 – Auditing and Assurance Services 22

GROUP STATISTICS

NOT FORMING PART OF THE ACCOUNTS

2011 $(unaudited)mil

2010 $mil

2009 $mil

2008 $mil

2007 $mil

Revenue items SALES

1,323.8

1,265.9

1,275.7

1,512.1

1,739.0

Profit before interest, tax and extraordinary item Net interest

92.4 (19.6)

109.0 (25.8)

145.6 (32.6)

135.3 (26.9)

139.7 (44.0)

Profit before tax and extraordinary item Income tax expense before extraordinary & material items

72.8 (16.5)

83.2 (11.0)

113.0 (18.9)

108.4 (25.0)

95.7 (28.2)

Profit after tax but before extraordinary item & material items Outside equity interests

56.3 (0.6)

72.2 (0.6)

94.1 (3.8)

83.4 (4.9)

67.5 (0.4)

NET OPERATING PROFIT BEFORE extraordinary item and material items Extraordinary and material items

55.7

(49.8)

71.6

-

90.3

-

78.5

(16.5)

67.1

(90.4) Net profit/(loss) attributable to shareholders 5.9 71.6 90.3 62.0 (23.3) Dividends 38.2 49.1 50.4 41.0 45.4 Balance sheet items Paid-up capital Reserves and unappropriated profits

77.8 Total shareholders’ equity Borrowings Creditors and provisions

755.0 398.5 401.8

685.2 469.6 339.3

615.0 667.4 334.7

580.2 489.6 317.8

605.2 646.2 377.9

Total shareholders equity and liabilities 1,555.3 1,494.1 1,617.1 1,387.6 1,629.3 Cash, deposits and negotiable securities Other tangible assets Intangibles and deferred tax assets

214.6 1,265.7 75.0

168.6 1,281.7 43.8

287.2 1,292.3 37.6

176.4 1,197.9 13.3

233.0 1,374.6 21.7

Total assets 1,555.3 1,494.1 1,617.1 1,387.6 1,629.3 Other items Dividends per share: unadjusted

12.0¢

17.0¢

20.0¢

19.0¢

18.0¢ Adjusted [1] 12.0¢ 17.0¢ 18.9¢ 16.9¢ 15.1¢ Earnings per share: Unadjusted [2] 15.6¢ 21.2¢ 27.5¢ 28.5¢ 28.2¢ Adjusted [3] 15.7¢ 21.0¢ 27.7¢ 25.2¢ 22.4¢ Dividend payout ratio [4] 76.2% 80.8% 69.2% 67.8% 67.6% Cash payout ratio [5] 67.8% 69.3% 59.6% 54.9% 59.5% Return on shareholders’ funds [6] 8.4% 11.3% 15.7% 14.7% 12.5% Return on capital employed [7] 9.6% 11.0% 15.4% 14.2% 14.6% Liabilities to tangible assets ratio 54.1% 55.8% 63.4% 58.7% 63.7% Net tangible assets per share [8] 165.0¢ 183.0¢ 175.0¢ 171.0¢ 169.0¢ Number of shareholders at year-end 21,998 21,198 21,209 22,773 21,284 Number of convertible notes holders at year-end - 1,315 1,397 2,068 2,151

Notes:

[1] Adjusted for bonus issues. [6] Net operating profit as a percentage of average [2] Based on the net operating profit and the number opening and year-end shareholders’ equity.

of shares on issue at year-end. [7] Profit before interest, tax divided by the sum of [3] Based on the net operating profit and the average average shareholders’ equity and average borrowings

number of shares on issue during year and net of cash and deposits. adjusted for bonus issues. [8] Shareholders’ equity (less deferred tax assets

[4] Dividends declared per share as a percentage and intangibles) divided by the number of shares on of earnings per share. issue at year end, adjusted for bonus issues.

[5] Dividends paid per share, after recognising elections under the Bonus Share Plan, as a percentage of earnings per share.

Note: It is acknowledged that the accounting standards no longer refer to extraordinary items. In 2006 this was not the case, and so for the purposes of highlighting this significant amount, the term “extraordinary item” has remained relevant.

ACCT 5908 – Auditing and Assurance Services 23

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Audit Evidence and the Use of Audit Assertions (Parts 1 & 2)

SEMINAR 5: 26 March 2012 (Part 1)

SEMINAR 6: 2 April 2012 (Part 2)

Note: Group assignment status report is due in Seminar 6. Major Quiz held in seminar 7. Reading Guide: References: *Gay and Simnett, Chapter 5 (pp.199-208), Chapter 9 (pp420-454), Chapter 10. *Roebuck and Martinov-Bennie, Chapter 3 Readings (pp.48-51). *Roebuck and Martinov-Bennie, Case 3-4 (p.56) and Solution, Chapter 11, p270,

Chapter 10, Practice Examination 1, Question 1 and Solution (p.227). *Roebuck and Martinov-Bennie, Chapter 3, Question 3-7 (p.59) and Solution (p.270). Standards: * ASA 315: Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment. * ASA 500: Audit Evidence. * ASA 520: Analytical Procedures. Discussion Questions Seminar 5 1. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 2 (Mid

Semester), Question 4, Part B (p.242). 2. Roebuck and Martinov-Bennie, Chapter 3, Case 3-9 part 1 (p.62). 3. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 4, Question 1

(pp.249-50).

ACCT 5908 – Auditing and Assurance Services 24

4. For each of the two (2) key audit risks described below complete the following: (i) provide a brief explanation as to why the situation constitutes an audit

risk (ii) identify the key account balance affected (iii) identify the prime audit assertion to be tested.

The situations are independent of each other and are to be treated separately in

your answers. (a) Slim and Fit Limited is a manufacturer of sporting equipment. The

majority of the merchandise is highly desirable, easily handled and of relatively high dollar value. Stealing has been an ongoing problem.

(b) Holford Limited is a manufacturer of cars. Their new range of sports

coupe ‘EAGLE’ has been a great success with huge sales in the last twelve months. However, there has been a great number of customer complaints and a dramatic increase in the servicing and repairs of this model in the last three months. It appears that the material used in the brake linings which is unique to ‘EAGLE’ is defective after 8,000 kilometres. There is no stock of ‘EAGLE’ at year end due to a waiting list as a result of the popular demand for the car.

5. With regards to Woolworths Limited 2010 Financial Report for the following

accounts, determine: i. The significant audit risks that may be associated with the account; ii. For each risk in (i), the relevant assertions;

Current Assets Current Liabilities Cash Trade and other payables Trade and other receivables Borrowings Inventory Provision for self-insured risks Non-current assets Equity Property, plant and equipment Foreign currency translation reserve Liquor and gaming licenses

Seminar 6 1. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 2 (Mid

Semester), Question 4, Part A (p.242). 2. Roebuck and Martinov-Bennie, Chapter 8, Question 30 (p.166). 3. For the account balance and the assertion listed in Seminar 5, Question 4 parts

(ii) and (iii), describe in specific terms the substantive audit procedure which would best provide sufficient and appropriate audit evidence.

4. For each assertion in Seminar 5, Question 5, part (ii), provide the most

appropriate substantive audit procedures (give details). 5. Roebuck and Martinov-Bennie, Chapter 8, Questions 19, 20, 23 and 24,

(p.165). 6. Roebuck and Martinov-Bennie, Practice Exam 4, Question 3, Part A&B, (p.251)

ACCT 5908 – Auditing and Assurance Services 25

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Auditors Response to Risks, Audit of Complex Balances and Transactions

SEMINAR 7: 16 April 2012

Note: Major Quiz held in this seminar. Reading Guide: References: * Roebuck and Martinov-Bennie, Chapter 3, Readings (pp. 48-51). * Roebuck and Martinov-Bennie, Chapter 1, (p.5-6). Standards: *ASA 540: Auditing Accounting Estimates including Fair value Accounting

Estimates and Related Disclosures. AASB 118: Revenue. AASB 138: Intangible Assets. AASB 116: Property, Plant and Equipment. AASB 136: Impairment of Assets. Discussion Questions

1. Revenue recognition, expense vs. capitalisation, valuation of brand names along with valuation of non-current assets have all been issues raised in recent corporate collapses and overstatement of profits e.g., Enron, Harris Scarf, World.com. Select two issues and relate them back to the relevant accounting standard and the auditing standards to determine how the balances for each of the issues chosen could be misstated. Also, outline the audit procedures that you would adopt in order to verify the account/balance.

2. With regard to intangibles such as trademarks, patents, etc. can an audit

determine the market value for such assets? Outline what the relevant accounting standard states in regard to carrying forward the value of such assets. What issues do you consider are of most concern to the auditor?

ACCT 5908 – Auditing and Assurance Services 26

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Using the Work of Others/Internal Audit/Public Sector Auditing

SEMINAR 8: 23 April 2012

Note: Wednesday 25 April 2012 is a holiday. All Wednesday seminar students will need to attend another seminar for this week only.

Reading Guide: References: Gay and Simnett, Chapter 8 (pp.395-397), Chapter 15. * Roebuck and Martinov-Bennie, Chapter 6, Readings (pp122-124). * Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 1, Question 4, Part A (p.230) and Solution. Standards: * ASA 315: Using the Work of another Auditor * ASA 330: The Auditors’ Procedures in Response to Assessed Risks. * ASA 610: Considering the Work of Internal Auditors * ASA 620: Using the Work of an Auditor’s Expert * ASAE 3500: Performance engagements * Roebuck and Martinov-Bennie, chapter 6, Case 6-7, part B (p.137) and solution (p.290). Discussion Questions 1. Roebuck and Martinov-Bennie, Chapter 8, Questions 42, 43 and 44 (p.167). 2. Review Woolworths Limited financial report and identify any areas in which the

auditor may need to engage an expert. 3. Your accounting firm has recently acquired a new audit client, which operates a

major industrial plant. Coal is the main raw material used to generate power for the plant.

(a) Consider whether the use of an independent expert will be necessary to

determine the quantity of coal held in stockpiles at the plant. (b) Assuming an independent expert is required, outline the broad procedures

that are necessary for you to be able to rely on the expert's work. 4. Explain how the objectives of public sector auditing differ from that of the private

sector. What implications do these differences have for auditing the public sector in terms of the application of the risk methodology and the ASAs.

5. The private sector auditor must be 'independent and seen to be independent'.

Is the same true of the public sector auditor? 6. Discuss the main independence features prevalent in a public sector audit.

ACCT 5908 – Auditing and Assurance Services 27

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Auditing in an IT Environment — Internal Control and Substantive Testing

SEMINAR 9: 30 April 2012

Note: Group Assignment and Peer Evaluation Forms due in seminar 10. Reading Guide: References: * Gay and Simnett, Chapter 8 (pp.382-393), Chapter 9 (pp.454-458), Chapter

10 (pp.525-529).

* Roebuck and Martinov-Bennie, Chapter 4, Readings (pp.70-77).

* Roebuck and Martinov-Bennie, Case 4-3 (p.80) and Solution, Chapter 11, Cases 4-5 (p.83), 4-6 (p.85), and Chapter 10, Practice Examination 1, Question 2 (p.245) and Solution.

Standards: * ASA 315: Understanding the Entity and Its Environment and Assessing the Risk of

Material Misstatements. Discussion Questions 1. (a) What are the implications of the existence of a computer environment at

a client’s place of business for an auditor? (b) What are the differences between general and application controls in an IT environment?

2. Roebuck and Martinov-Bennie, Case 4-1, Part 2 (p. 78). 3. Roebuck and Martinov-Bennie, Case 4-2, Part 2 (p. 78). 4. Roebuck and Martinov-Bennie, Chapter 10, Practice Examination 3, Question 2

(p.245).

ACCT 5908 – Auditing and Assurance Services 28

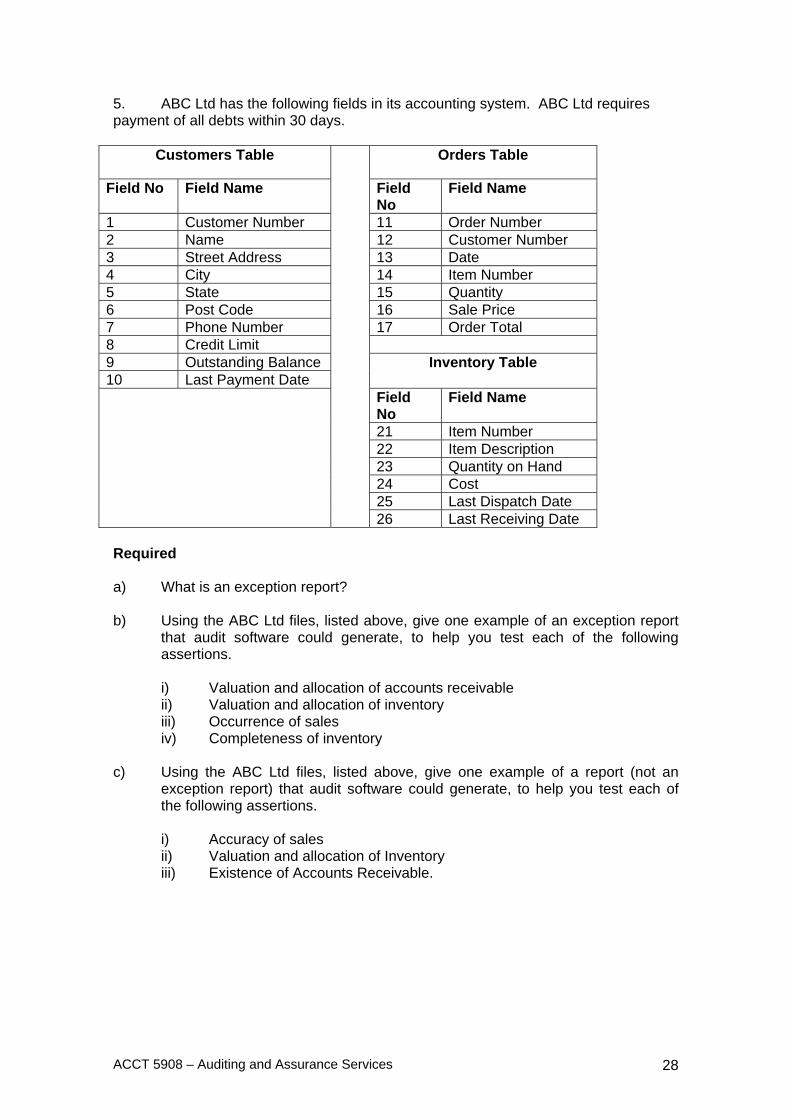

5. ABC Ltd has the following fields in its accounting system. ABC Ltd requires payment of all debts within 30 days.

Customers Table Orders Table

Field No Field Name Field No

Field Name

1 Customer Number 11 Order Number 2 Name 12 Customer Number 3 Street Address 13 Date 4 City 14 Item Number 5 State 15 Quantity 6 Post Code 16 Sale Price 7 Phone Number 17 Order Total 8 Credit Limit 9 Outstanding Balance Inventory Table 10 Last Payment Date Field

No Field Name

21 Item Number 22 Item Description 23 Quantity on Hand 24 Cost 25 Last Dispatch Date 26 Last Receiving Date

Required a) What is an exception report? b) Using the ABC Ltd files, listed above, give one example of an exception report

that audit software could generate, to help you test each of the following assertions.

i) Valuation and allocation of accounts receivable ii) Valuation and allocation of inventory iii) Occurrence of sales iv) Completeness of inventory

c) Using the ABC Ltd files, listed above, give one example of a report (not an exception report) that audit software could generate, to help you test each of the following assertions.

i) Accuracy of sales ii) Valuation and allocation of Inventory iii) Existence of Accounts Receivable.

ACCT 5908 – Auditing and Assurance Services 29

6. Toan & Associates are a firm of solicitors specialising in commercial law. An audit is required under the solicitors’ trust regulations. Recent changes in government regulation have deregulated the fees of commercial lawyers, with the result that legal fees have decreased by 20% over the past year. The firm has 4 partners, 90 associates and 6 support staff. All financial records are contained on a personal computer. A general ledger software package that is widely used by legal firms is used by the organisation. The general ledger package also contains an accounts receivable subsidiary ledger, a work-in-progress file (which shows current status of legal cases) and a payroll subsidiary ledger. All financial records, including all payroll documentation, are maintained by the ledger clerk. The payroll details entered consist of changes to standing data, and transactions. The changes to standing data are additions and deletions of staff to the payroll master file, change of address, variation of approved fortnightly pay, and change to approved overtime rate. Any such changes are contained on a pre-numbered variation of payroll information form which is approved by the personnel partner and one other partner. After being entered into the system, the variation of payroll information forms are filed in numerical sequence. The transaction data is entered each fortnight when the partners and staff complete a pay sheet which assigns their time to jobs. This is entered into the computer package by the ledger clerk and is used to update the work-in-progress file and the payroll file. If any staff work overtime, which must be approved by the partner in charge of the case (evidenced by the partner initialling the pay sheet), this is entered and the overtime is paid at the approved set rate. The following reports are produced each fortnight and are reviewed and authorised by all partners, at fortnightly partners’ meetings: • Printout of year-to-date payroll master file. • Payroll transactions file for the last fortnight. • List of staff who have undertaken overtime in the last fortnight. • Current status of all cases in progress. • Cases in progress where additional work has been undertaken over the last

fortnight. • Cases completed, but not billed over the last fortnight. • List of accounts receivable master file. Required: (a) Identify any controls that exist in the payroll area. For the controls identified,

detail the relevant assertion that each control addresses. (b) The client’s software package contains a programmed range check on the

payroll file. No associate’s fortnightly pay (before overtime) should be outside the range of $2,200-$4,000. Identify and illustrate by example with respect to this control the technique(s) by which the auditor could obtain direct evidence that this programmed control is working.

(c) Some of the reports generated by the client each fortnight are exception

reports. Identify which of the reports generated are exception reports.

ACCT 5908 – Auditing and Assurance Services 30

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Completing the Audit Process and Audit Reporting

SEMINAR 10: 7 May 2012

Note: Group Assignment and Peer Evaluation Forms due at the beginning of this seminar. Mini Quiz 2 held in seminar 11. Reading Guide: References: Gay and Simnett, Chps.12 and 13. * Roebuck and Martinov-Bennie, Chp.10, Practice Examination 1, Question 4 Part C (p.231) and Solution. Standards: * ASA 560: Subsequent Events. * ASA 570: Going Concern. * ASA 700: Forming an Opinion and Reporting on a Financial Report. * ASA 705: Modifications to the Opinion in the Independent Auditor’s Report. * ASA 706: Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report. Discussion Questions 1. Review Woolworths Limited audit report and directors’ declaration. Comment as

to the date each one is signed. 2. Roebuck and Martinov-Bennie, Case 5-3 (p.103).

3. Roebuck and Martinov-Bennie, Case 5-6 (i), (iv), (v), (vi), (vii), (viii) (p.107).

4. Roebuck and Martinov-Bennie, Case 5-5 (i), (ii), (iii) (p.105).

Note: Mini Quiz 2 held in this seminar. Reading Guide: Ethics References: Gay and Simnett, Chps. 3 and 4. * Roebuck and Martinov-Bennie, Chapter 7, Readings (pp.142-150). * Roebuck and Martinov-Bennie, Cases 7-3 (p.153) and 7-9 (p.160) and Solutions, Chapter 10, Practice Examination 1, Question 4B (p.231) and Solution. Standards: APES 110: Code of Ethics for Professional Accountants (Part A and s290) APES 320: Quality Control for Firms Discussion Questions - Ethics:

1. The following each involve a possible violation of the professional bodies’ (ICAA

and CPAA) ethical rules. For each situation determine if the current ethical

standards have been compromised (cite references where applicable).

(a) John Brown is a chartered accountant, but not a partner, with three years of professional experience with Lyle and Lyle Chartered Accountants, a one-office firm. He owns 2,500 shares in an audit client of the firm, but he does not take part in the audit of the client and the amount of stock is not material in relation to his total wealth.

(b) A client requests assistance of J. Bacon, Chartered Accountant, in the installation of a computer system for maintaining production records. Bacon had no experience in this type of work and no knowledge of the client's production records, so he obtained assistance from a computer consultant. The consultant is not in the practice of public accounting, but Bacon is confident of his professional skills. Because of the highly technical nature of the work Bacon is not able to review the consultant's work.

ACCT 5908 – Auditing and Assurance Services 32

(c) Five small Sydney public accounting firms have become involved in an

information project by taking part in an interfirm working paper review program. Under the program, each firm designates two partners to review the working papers, including the tax returns and the financial statements of another public accounting firm taking part in the program. At the end of each review, the auditors who prepared the working papers and the reviewers have a conference to discuss the strengths and weaknesses of the audit. They do not obtain authorisation from the audit client before the review takes place.

Discussion Questions – Law: 1. In his comprehensive judgement in Pacific Acceptance Corporation v Forsyth,

Moffit J. set out the duties of the auditor. Briefly outline these duties. Consider also the relationship between these common law duties and the auditing standards.

2. What was the significance for the auditors of the AWA Limited v Daniels

(trading as Deloitte, Haskins and Sells) and other recent decisions? 3. What is the 'proximity test' with regard to auditor's liability to third parties?

Support your explanation with relevant legal cases.

ACCT 5908 – Auditing and Assurance Services 33

THE UNIVERSITY OF NEW SOUTH WALES

SCHOOL OF ACCOUNTING

ACCT 5908 AUDITING AND ASSURANCE SERVICES

Course Review

SEMINAR 12: 21 May 2012

No set readings. Students will work on a practice exam distributed in class.

ACCT 5908 – Auditing and Assurance Services 34

PART D: REVISION

MULTIPLE-CHOICE ANSWERS Students may access the most recent past exam papers (for the semesters shown below) via the Library Catalogue. No solutions are available to written questions. Answers to multiple-choice questions are shown below: