ACT 330 Sec: 03

Submitted By: Mega Mind Submitted To: Mrs. Nabila Nisha

Sourov Agarwal 113 0699 030 Mohammed Naeem 113 0512 030

Hussain Nabiul Mannan 141 1679 030 Khorsed Alam Prince 141 1765 030

MegaMind Page | 1

Letter of Transmittal

7th

August 2015

Mrs. Nabila Nisha

Lecturer,

Dept. of Accounting & Finanace (BBA)

North South University, Dhaka, Bangladesh.

Subject: Permission for submitting the Group Project Report

Dear Madam,

It is indeed a great pleasure to have the opportunity to submit the report. We have prepared

this report in accordance with the instructions given by you. You provided us

four Pharmaceuticals & Chemicals companies, which are Kohinoor Chemicals, Beximco

Pharma, Abbott Laboratories, Pharmstandard. We did accounting analysis and financial

analysis of those four companies and we think that, working on this topic was very interesting

and we have explored something remarkable through our report. This report is to describe our

observation, learning and recommendation based on the knowledge and the experiences

gained during the course under your supervision. This report has provided us learning

opportunity and compares theoretical knowledge with practical situations.

We hope that, you would be kind enough to accept our report and bless us.

Sourov Agarewal

Mohammed Naeem

Hussain Nabiul Mannan

Khorsed Alam Prince

MegaMind Page | 2

Abstract

The purpose of this project is to enhance our understanding of US GAAP, IFRS and BFRS

Financial statements and Analysis techniques for computation. We have got the chance to

apply all the knowledge that we have gathered from our class and tried to apply it to the best

of our knowledge. Firstly, we focused on doing accounting analysis for all four of our

selected companies. Then we analyzed on the financial stance of the companies. Besides that,

we have also interpreted and compared the ratios between the companies. We have observed

that despite operating in the same industry, there are many discrepancies in them, which is

why we have realized the need for international convergence.

The success of this project depended on the contribution of all the group members & their

thoughtful guidance and suggestions in an effort to provide a useful and reliable report

MegaMind Page | 3

Table of Contents

Introduction: Company Overview ......................................... 4-5

Appendix A .............................................................................. 6-7

Appendix B .................................................................................. 8

Appendix C ............................................................................ 9–12

Appendix C-1.1 ......................................................................... 9

Appendix C-1.2 ....................................................................... 10

Appendix C-1.3 ....................................................................... 11

Appendix C-1.4 ....................................................................... 12

Appendix D: Ratio analysis Table 1 ........................................ 13

Interpretations of Appendix D ........................................... 14–17

Appendix E: Ratio analysis Table 2 ........................................ 18

Interpretations of Appendix E ........................................... 19–22

Appendix F: Ratio analysis Table 3 ......................................... 23

Interpretations of Appendix F .......................................... 24– 27

MegaMind Page | 4

Introduction: Company Overview

Kohinoor Chemical Company (Bangladesh) Limited is popularly known by the legendary

beauty product under the brand "Tibet". For more than half a century Tibet has made its mark

in the hearts of millions. Kohinoor are the pioneer amongst the soap, cosmetics and toiletries

manufacturing industries of Bangladesh, producing highly value-added products with quality

in the center of focus. Kohinoor care for the customers and are determined to count extra

mileage to meet their daily needs. Kohinoor believe that it is the quality that has kept Tibet

going and growing for 55 years.

Beximco Pharmaceuticals Ltd (Beximco Pharma) is an emerging generic drug player

committed to providing access to affordable medicines. Company’s state-of-the-art

manufacturing facilities have been accredited by the regulatory authorities of USA, Australia,

European Union, Canada, and Brazil, among others, and it currently focuses on building

presence in many emerging and developed markets around the world. Beximco Pharma is

consistently building upon its portfolio and currently producing more than 500 products

encompassing broad therapeutic categories and the Company has created strong

differentiation by offering a range of high-tech, specialized products which are difficult to

imitate.

MegaMind Page | 5

Abbott Laboratories is an American pharmaceuticals and health care products company. It

has 72,000 employees and operates in over 130 countries. The company headquarters are in

Abbott Park, North Chicago, Illinois. The company was founded by Chicago physician

Wallace Calvin Abbott in 1888. In 1985, the company developed the first HIV blood-

screening test. The company's drug portfolio includes Humira, a drug for rheumatoid arthritis,

psoriatic arthritis, ankylosing spondylitis, Crohn's disease, moderate to severe chronic

psoriasis and juvenile idiopathic arthritis; Norvir, a treatment for HIV; Depakote, an

anticonvulsant drug; and Synthroid, a synthetic thyroid hormone. Abbott also has a broad

range of medical devices, diagnostics and immunoassay products as well as nutritional

products, including Ensure, a line of meal replacement shakes; and EAS, the largest producer

of performance-based nutritional supplements. The company's in-vitro diagnostics business

performs immunoassays and blood screening.

Pharmstandard is the leading Russian pharmaceutical company, it is headquartered in

Dolgoprudny. Pharmstandard portfolio includes over 200 products used in the treatment of

diabetes, growth hormone deficiency, cardiovascular diseases, gastroenterological and

neurological disorders, infectious diseases, cancer, etc. Over 90 products offered by

Pharmstandard are included in the List of Vital Pharmaceutical Products. The company has

six manufacturing facilities located in Moscow, Ufa, Nizhny Novgorod, Kursk, Tomsk and

Tyumen.

MegaMind Page | 6

Appendix A: Event Exhibit

Company Significant Transactions

Kohinoor Chemicals 1. Interest income has been separated on

the basis of accrual method.

2. Effect of inflation was not considered

in preparing the financial statements.

3. In 2013 they spent extra entertainment

expenditures.

4. No donations & subscriptions were

made this year.

5. No sales promotion expenses are

included.

6. Did not have liveries and uniform

expense.

Beximco Pharma 1. Office equipment not considered this

year.

2. Land, building and plant & machinery

was revalued using Current Cost

Method.

3. Bonus share issued in 2013 was only

10% of bonus shared issued in 2012

4. Prepaid expenses and Overseas

Liaison Office expenses acquired this

year.

5. Short term borrowings from AB Bank

and Noor Islamic Bank

Abbott Laboratories 1. Research-based proprietary

pharmaceuticals business is

discontinued.

2. Time to consolidate foreign

subsidiaries accounts has been

changed.

MegaMind Page | 7

3. Acquired 100 percent of IDEV

Technologies, net of debt, for $310

million, in cash.

4. Recorded goodwill of approximately

$274 million in 2013 related to the

acquisitions of IDEV Technologies

and OptiMedica.

5. Foreign subsidiaries enter into foreign

currency forward exchange contracts

to manage exposures to changes in

foreign exchange rates for anticipated

intercompany purchases by those

subsidiaries whose functional

currencies are not the U.S. dollar.

Pharmstandard 1. Adopted to new accounting policies

(IFRS 10, IFRS 11, IFRS 12, IFRS

13, IAS 19)

2. Accusation of Bever Pharmaceutical

Pte Ltd.

3. Acquired 11% of non-controlling

interests in Donelle Company

Limited.

4. OTCpharm was registered and its

shares were proportionally distributed

among the shareholders of the

Company.

5. Acquired Pharmstandard International

S.A.

6. Provided unsecured US$ denominated

short-term loan to Augment.

MegaMind Page | 8

Appendix B: Estimates Exhibit

Kohinoor

Chemicals

Beximco Pharma Abbott

Laboratories

Pharmstandard

Accrued expenses Depreciation Sales rebates Inflation rate

Income taxes Inventory valuation Income taxes Intangible assets

valuation

Depreciation Accrued expenses Pension Income Taxes

Inflation rate Selling price of

Inventories

Intangible assets

valuation

Leases

Payable valuation of

intangible assets

Allowance for

doubtful accounts

receivable

Deferred liability for

gratuity

Litigation Impairment

Derivative financial

instruments

Inventories to net

realizable value

Inventory Useful life of

property, plant and

equipment

Accounts receivable

exposures

Leases

MegaMind Page | 9

Appendix C 1.1: Comparison Exhibit

Accounting Policy IFRS Company:

Pharmstandard

U.S Company:

Abbott (GAAP)

Comment

Inventory

Valuation

Inventories are

recorded at the lower

of cost and net

realizable value. Cost

is determined on a

first in, first out basis.

Inventories are stated

at the lower of cost

(first-in, first-out

basis)

Same method for

valuation of

inventory. This is

because there are not

many differences

between the GAAP

and IFRS standards.

Property, Plant &

Equipment

straight-line basis straight-line basis Similar method. And

that is acceptable

because this method

is used by many

companies.

Cash Flow

Presentation

Indirect Indirect Same method by both

companies

Revenue

Recognition

Accrued basis -

Revenue is

recognized before

cash is received

Accrued basis -

Revenue is

recognized before

cash is received

Both company uses

cash basis for

revenue

reorganization.

Goodwill it is recorded using

impairment

Initially, fair value of

net assets. After

initial recognition, it

is recorded using

impairment.

In case of goodwill

both companies later

use impairment

however initially

Abbott uses fair

market value of net

asset but

Pharmstandard is not

given.

Other intangible

assets

Initially, fair value of

net assets. After

initial recognition, it

is recorded using

impairment.

Initially, fair value of

net assets. After

initial recognition, it

is recorded using

impairment.

Similar method to

record other

intangible assets.

MegaMind Page | 10

Appendix C 1.2

Accounting Policy Local Company:

kohinoor

U.S Company:

Abbott (GAAP)

Comment

Inventory Valuation ----- Inventories are stated

at the lower of cost

(first-in, first-out

basis)

We cannot compare

because not enough

data available.

Property, Plant &

Equipment

straight-line basis straight-line basis Similar method. And

that is acceptable

because this method

is used by many

companies.

Cash Flow

Presentation

Indirect Indirect Same method by

both companies

Revenue

Recognition

------- Accrued basis -

Revenue is

recognized before

cash is received

We cannot compare

because not enough

data available.

Goodwill Impairment Initially, fair value of

net assets. After

initial recognition, it

is recorded using

impairment.

In case of goodwill

both companies later

use impairment

however initially

Abbott uses fair

market value of net

asset but kohinoor

uses impairment all

the way.

Other intangible

assets

------- Initially, fair value of

net assets. After

initial recognition, it

is recorded using

impairment.

We cannot compare

because not enough

data available.

MegaMind Page | 11

Appendix C 1.3

Accounting Policy Local Company:

kohinoor

IFRS Company:

Pharmstandard

Comment

Inventory Valuation ----- Inventories are

recorded at the lower

of cost and net

realizable value. Cost

is determined on a

first in, first out basis.

We cannot compare

because not enough

data available.

Property, Plant &

Equipment

straight-line basis straight-line basis Similar method. And

that is acceptable

because this method is

used by many

companies.

Cash Flow

Presentation

Indirect Indirect Same method by both

companies

Revenue Recognition ------- Accrued basis -

Revenue is recognized

before cash is

received

We cannot compare

because not enough

data available.

Goodwill Impairment it is recorded using

impairment

In case of goodwill

both companies use

impairment.

Other intangible

assets

------- Initially, fair value of

net assets. After initial

recognition, it is

recorded using

impairment.

We cannot compare

because not enough

data available.

MegaMind Page | 12

Appendix C 1.4

Accounting Policy Local Company:

kohinoor

Industry

Benchmark:

Beximco

Comment

Inventory Valuation ----- Inventories are

recorded at the lower

of cost and net

realizable value. Cost

is determined on a

first in, first out basis.

We cannot compare

because not enough

data available.

Property, Plant &

Equipment

straight-line basis straight-line basis Similar method. And

that is acceptable

because this method is

used by many

companies.

Cash Flow

Presentation

Indirect Indirect Same method by both

companies

Revenue Recognition ------- Accrued basis -

Revenue is recognized

before cash is

received

We cannot compare

because not enough

data available.

Goodwill Impairment it is recorded using

impairment

In case of goodwill

both companies use

impairment.

Other intangible

assets

------- it is recorded using

impairment.

We cannot compare

because not enough

data available.

MegaMind Page | 13

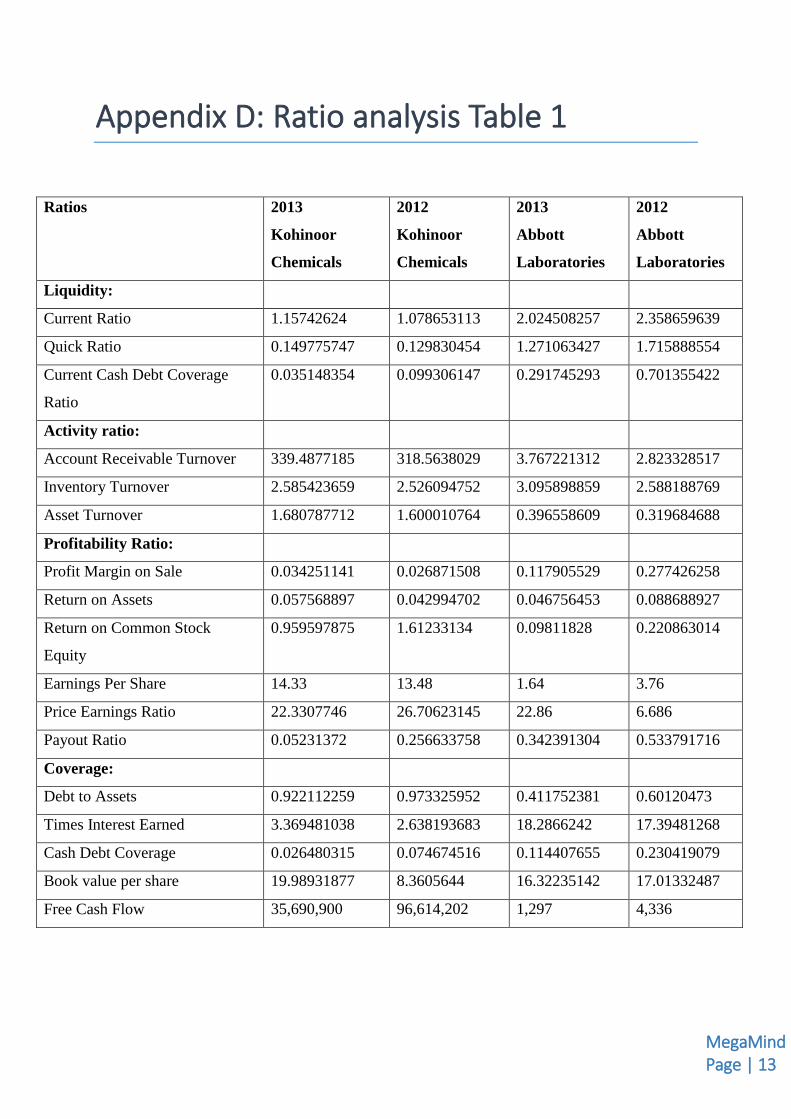

Appendix D: Ratio analysis Table 1

Ratios 2013

Kohinoor

Chemicals

2012

Kohinoor

Chemicals

2013

Abbott

Laboratories

2012

Abbott

Laboratories

Liquidity:

Current Ratio 1.15742624 1.078653113 2.024508257 2.358659639

Quick Ratio 0.149775747 0.129830454 1.271063427 1.715888554

Current Cash Debt Coverage

Ratio

0.035148354 0.099306147 0.291745293 0.701355422

Activity ratio:

Account Receivable Turnover 339.4877185 318.5638029 3.767221312 2.823328517

Inventory Turnover 2.585423659 2.526094752 3.095898859 2.588188769

Asset Turnover 1.680787712 1.600010764 0.396558609 0.319684688

Profitability Ratio:

Profit Margin on Sale 0.034251141 0.026871508 0.117905529 0.277426258

Return on Assets 0.057568897 0.042994702 0.046756453 0.088688927

Return on Common Stock

Equity

0.959597875 1.61233134 0.09811828 0.220863014

Earnings Per Share 14.33 13.48 1.64 3.76

Price Earnings Ratio 22.3307746 26.70623145 22.86 6.686

Payout Ratio 0.05231372 0.256633758 0.342391304 0.533791716

Coverage:

Debt to Assets 0.922112259 0.973325952 0.411752381 0.60120473

Times Interest Earned 3.369481038 2.638193683 18.2866242 17.39481268

Cash Debt Coverage 0.026480315 0.074674516 0.114407655 0.230419079

Book value per share 19.98931877 8.3605644 16.32235142 17.01332487

Free Cash Flow 35,690,900 96,614,202 1,297 4,336

MegaMind Page | 14

Interpretations of Appendix D:

Liquidity ratios:

2012

Liquidity Ratio measures the company’s short term ability to pay its maturing obligations.

The current ratio of Kohinoor Chemicals is 1.07:1, which should be at least (2:1), so, the

company is not in a good position. On the other hand, the current ratio of Abbott Laboratories

is 2.36:1, which seems that the company is in a good position compared to Kohinoor

chemicals. A case can be made against them for not utilizing more of their liquid asset to

obtain further investments. The quick ratio of Kohinoor Chemicals is 0.13:1, which should

have been at least (1:1). On the other hand, Abbott Laboratories has a quick ratio of 1.72:1,

which is above Kohinoor Chemicals. So, Abbott should try to get more investment with their

available most liquid assets. Cash Debt Coverage ratio shows how much debt can be

recovered through cash flows from operation. Abbott Laboratories (0.70:1) is in very good

position compared to Kohinoor chemicals (0.099:1).

2013

The current ratio of Kohinoor Chemicals has increased to 1.16:1 which is a good sign but it

should try to reach to industry benchmark. For Abbott, it has fallen to 2.02:1 which shows

that it is utilizing current assets more properly to obtain investment. It’s good for Kohinoor

chemicals that its quick ratio has increased to 0.15:1 and it should try to reach to benchmark.

On the other hand the quick ratio of Abbott has dropped to 1.27:1. So, it is utilizing its liquid

assets in a proper way. The Current Cash Debt Coverage Ratio for both the companies has

dropped. For Kohinoor Chemicals, it has dropped to 0.035 and for Abbott Laboratories, it has

dropped to 0.29.

MegaMind Page | 15

From our analysis above, we can state that Abbott Laboratories is in a very good position

compared to Kohinoor Chemicals in terms of liquidity.

Activity Ratios:

2012

Activity ratios are the measure of how effectively the company uses its assets to generate

sales. The accounting receivable turnover of Kohinoor chemicals is 319 times which is much

higher than that of Abbott Laboratories of only 2.82 times. So, it takes less time for Kohinoor

chemicals to collect account receivable than Abbott Laboratories. When it comes inventory

turnover, two companies are much similar. For Kohinoor Chemicals it is 2.53, whereas it is

2.59 for Abbott Laboratories. Asset Turnover for Kohinoor Chemicals is 1.6 times and for

Abbott Laboratories, it is only 0.32. Which implies that Kohinoor chemicals utilizes its assets

more effectively than Abbott Laboratories.

2013

The accounting receivable turnover of Kohinoor chemicals has increased to 339.48 and for

Abbott it has increased to 3.77. Inventory turnover for both the companies has increased. For

Kohinoor, it is now 2.59 times. And for Abbot it is 3.09. But Abbott can sale its inventory

more quickly than Kohinoor. Asset turnover has also increased for both the companies.

From our analysis above, we are seeing that Kohinoor Chemicals is in a better position than

Abbott Laboratories in terms of activity.

Profitability Ratios:

2012

It is a measure of the degree of success or failure of a given company for a given period of

time to generate profit. The profit Margin on Sale of Kohinoor Chemicals is 2.69%. Whereas,

it is 27.7% for Abbott. It implies that the profit garnered form Sales is higher for Abbott

MegaMind Page | 16

Laboratories. Return on Assets is also higher for Abbott. So, profit garnered form asset is

higher for Abbott Lab. But Return on Common Stock Equity is higher for Kohinoor than

Abbot so profit garnered form equity is higher for Kohinoor Chemicals. On the other payout

ratio and Price Earnings Ratio is higher for Abbot than Kohinoor. Which means Abbott pays

higher portion of its income as cash dividend than Kohinoor chemical does.

2013

Profit Margin on Sale, Return on Assets have increased for Kohinoor chemicals, but have

decreased for Abbott Lab. Earning Per Share for Kohinoor has also increased to tk. 14.33, but

has decreased for Abbott to $1.64. On the other hand Payout Ratio and Return on Common

Stock Equity for both the companies has decreased.

So, we are seeing that Kohinoor Chemicals performs better than Abbott Laboratories in terms

of profitability.

Coverage Ratios:

2012

It’s a measure of the degree of protection for long term creditors and investors. The Debt to

Assets ratio for Kohinoor Chemicals is higher than Abbott Lab. Kohinoor has 97% debt

against its assets where Abbott has 60% debt against its assets. Kohinoor Chemicals has the

ability to pay interest for 2.64 times where Abbott Lab. Can pay 17.4 times. Cash Debt

Coverage and Book value per share are also higher for Abbott Lab than Kohinoor Chemicals.

2013

Debt to Assets ratio has fallen for both the companies, but it is still less for Abbott Lab than

Kohinoor Chemicals. Times Interest Earned ratio for both the companies has increased, but

the value is much greater for Abbott than Kohinoor. Cash Debt Coverage for Kohinoor has

MegaMind Page | 17

fallen to 2.65% and for Abbott to 11.4%. Book value per share has increased for Kohinoor

but decreased for Abbott.

So, we are seeing that Abbott Laboratories performs better than Kohinoor Chemicals in terms

of Coverage Ratios.

MegaMind Page | 18

Appendix E: Ratio analysis Table 2

Ratios 2013

Kohinoor

Chemicals

2012

Kohinoor

Chemicals

2013

Pharmstandard

2012

Pharmstandard

Liquidity:

Current Ratio 1.15742624 1.078653113 1.4756387 2.841606658

Quick Ratio 0.149775747 0.129830454 1.238849258 2.172708454

Current Cash Debt Coverage

Ratio

0.035148354 0.099306147 0.585373704 0.828262955

Activity ratio:

Account Receivable Turnover 339.4877185 318.5638029 2.866657644 3.377381028

Inventory Turnover 2.585423659 2.526094752 4.082586708 3.794624203

Asset Turnover 1.680787712 1.600010764 0.966230478 0.956090526

Profitability Ratio:

Profit Margin on Sale 0.034251141 0.026871508 0.213757819 0.195590609

Return on Assets 0.057568897 0.042994702 0.20653932 0.187002328

Return on Common Stock

Equity

0.959597875 1.61233134 0.36216804 0.29076623

Earnings Per Share 14.33 13.48 340.914865 276.6940039

Price Earnings Ratio 22.3307746 26.70623145 3.048046463 2.667064223

Payout Ratio 0.05231372 0.256633758 0.001966247 No Cash

Dividend

Coverage:

Debt to Assets 0.922112259 0.973325952 0.535608616 0.261655307

Times Interest Earned 3.369481038 2.638193683 126.5036405 369.6178807

Cash Debt Coverage 0.026480315 0.074674516 0.570459592 0.776320057

Book value per share 19.98931877 8.3605644 0.731054302 0.994020814

Free Cash Flow 35,690,900 96,614,202 13,509,233 10,790,812

MegaMind Page | 19

Interpretations of Appendix E:

Liquidity:

2012

The current ratio of Pharmstandard (2.84:1) is higher than that of Kohinoor chemicals

(1.08:1), but it doesn’t necessarily mean that it is in a better position than Kohinoor

Chemicals. Rather it implies that Pharmstanderd doesn’t utilize its current assets properly.

The quick ratio of Kohinoor Chemicals (0.13) is far below than that of Pharmstandard

(2.17:1) and Kohinoor should try to raise it. On the other hand, Pharmstandard should try to

utilize its highly liquid assets properly. Current Cash Debt Coverage Ratio of Kohinoor

Chemicals (0.099) is also far below than that of Pharmstandard (0.83). So, pharmstandard can

recover most of its current debt by its cash flow from operation.

2013

The current ratio of Kohinoor Chemicals has increased to 1.16:1, but for Pharmstandard it has

decreased to 1.47:1 and it’s still better than Kohinoor Chemicals. It implies that

Pharmstandard is trying to utilize its current assets effectively. The quick ratio of Kohinoor

Chemical has also increased, but for Pharmstandard it has fallen because it is trying to utilize

its current assets properly. Current Cash Debt Coverage Ratio for both the companies has

fallen, but pharmstandard is in a better position.

From our analysis above, we can state that Pharmstandard is in a better position than

Kohinoor Chemicals in liquidity for both the year.

MegaMind Page | 20

Activity Ratios:

2012

Account Receivable Turnover of Kohinoor Chemicals is higher than Pharmstandard’s. So,

Kohinoor has higher ability to collect account receivable. Inventory Turnover ratio of

Pharmstandard (3.79) is higher than Kohinoor Chemical’s (2.53). So, the inventory needed to

support a given level of sales is better for Pharmstandard. Asset Turnover ratio of Kohinoor

(1.6) is also higher than Pharmstandard’s (0.96). So, Kohinoor can generate more sales using

its assets than Pharmstandard. So, in 2012 Kohinoor Chemicals is in better position in this

regards.

2013

Account Receivable Turnover for Kohinoor Chemicals has improved but reduced for

Pharmstandard. Inventory Turnover has increased for both the companies in a small amount,

but the increase is more for Pharmstandard. Asset Turnover for Kohinoor has improved but

has remain almost the same for Pharmstandard. So in 2013, Kohinoor Chemicals in in a

better position.

Profitability Ratios:

2012

Pharmstandard can generate more income from its sale than Kohinoor Chemicals which is

measured by Profit Margin on Sale. Return on Assets of Pharmstandard (0.187) is also

higher than Kohinoor Chemicals (0.043). Which means Pharmstandard can utilize its assets

more effectively. The EPS of Kohinoor is far below compared to Pharmstandard. The payout

ratio of Kohinoor Chemicals is 0.26, whereas Pharmstandard offers no cash dividend in 2012.

On the other hand, Return on Common Stock Equity and Price Earnings Ratio are higher for

Kohinoor. So, Pharmstandard is more profitable in 2012

MegaMind Page | 21

2013

Profit Margin on Sale for both the companies has increased in a small amount. The ROA and

EPS have also increased for both the companies. But the increase in EPS is very higher for

Pharmstandard than Kohinoor Chemicals. Payout Ratio has decreased for Kohinoor and

Pharmstandard has started offering cash dividend. Return on Common Stock Equity has

decreased for Kohinoor but increased for Pharmstandard. On the other hand, Price Earnings

Ratio has increased for Kohinoor but decreased for Pharmstandard. So, Pharmstandard is

more profitable than Kohinoor Chemicals in 2013

Coverage Ratios:

2012

Debt to Assets ratio is higher for Kohinoor than for Pharmstandard, which means Kohinoor

Chemicals generates more of its assets through creditors than pharmstandard does which is

risky for Kohinoor. On the other hand, Pharmstandard is not properly using its ability to take

more debt. But Times Interest Earned ratio of Kohinoor is less than Pharmstandard. So,

Kohinoor has less ability to pay interest than pharmstandard. On the other hand, Cash Debt

Coverage of Kohinoor (0.07) is far below than Pharmstandard (0.78). And Book value per

share is higher for Kohinoor. So, Pharmstandard is in a better position than Kohinoor

Chemicals in this regard in 2012.

2013

The portion of assets that has been generated from creditors (Debt to Assets) has decreased

for Kohinoor but increased for pharmstandard which means it is properly using its ability to

take debt from creditors. Times Interest Earned that measures the company’s ability to pay

interest has improved for Kohinoor but reduced for Pharmstandard but it is still very much

higher for Pharmstandard. Cash Debt Coverage ratio for both the companies has reduced.

MegaMind Page | 22

And Kohinoor Chemicals is in a very risky situation. Overall, Pharmstandard is in a better

position than Kohinoor Chemicals.

MegaMind Page | 23

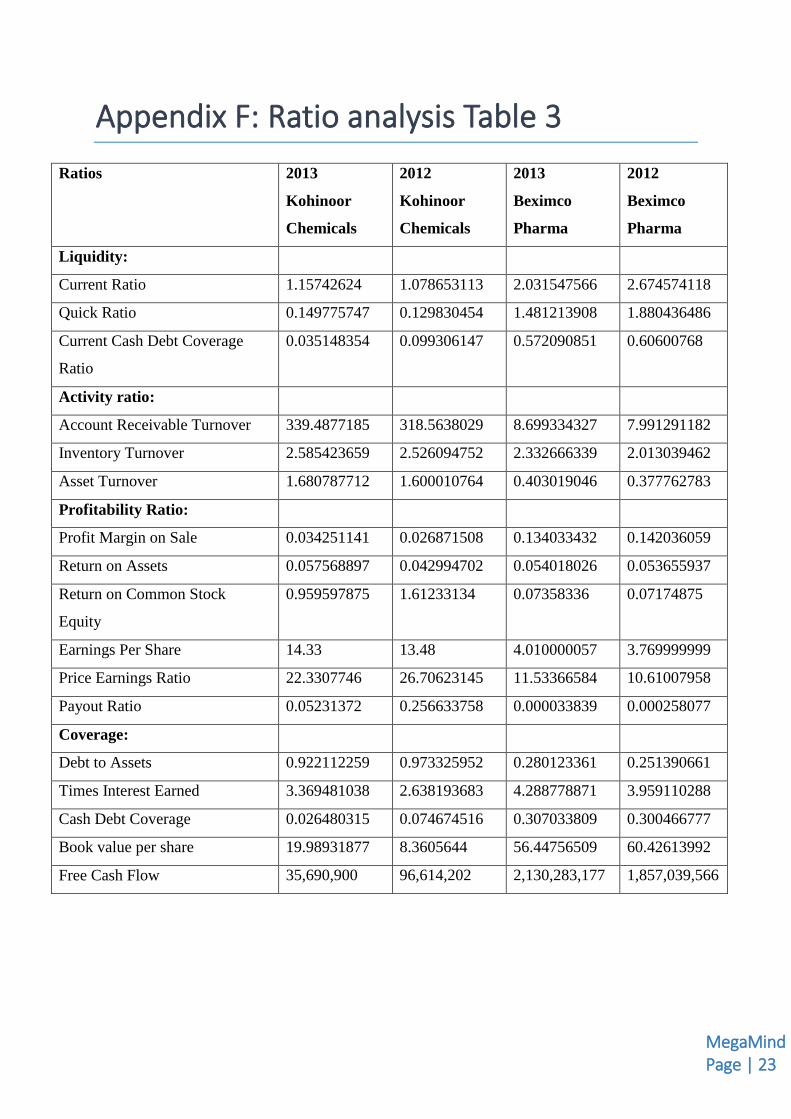

Appendix F: Ratio analysis Table 3

Ratios 2013

Kohinoor

Chemicals

2012

Kohinoor

Chemicals

2013

Beximco

Pharma

2012

Beximco

Pharma

Liquidity:

Current Ratio 1.15742624 1.078653113 2.031547566 2.674574118

Quick Ratio 0.149775747 0.129830454 1.481213908 1.880436486

Current Cash Debt Coverage

Ratio

0.035148354 0.099306147 0.572090851 0.60600768

Activity ratio:

Account Receivable Turnover 339.4877185 318.5638029 8.699334327 7.991291182

Inventory Turnover 2.585423659 2.526094752 2.332666339 2.013039462

Asset Turnover 1.680787712 1.600010764 0.403019046 0.377762783

Profitability Ratio:

Profit Margin on Sale 0.034251141 0.026871508 0.134033432 0.142036059

Return on Assets 0.057568897 0.042994702 0.054018026 0.053655937

Return on Common Stock

Equity

0.959597875 1.61233134 0.07358336 0.07174875

Earnings Per Share 14.33 13.48 4.010000057 3.769999999

Price Earnings Ratio 22.3307746 26.70623145 11.53366584 10.61007958

Payout Ratio 0.05231372 0.256633758 0.000033839 0.000258077

Coverage:

Debt to Assets 0.922112259 0.973325952 0.280123361 0.251390661

Times Interest Earned 3.369481038 2.638193683 4.288778871 3.959110288

Cash Debt Coverage 0.026480315 0.074674516 0.307033809 0.300466777

Book value per share 19.98931877 8.3605644 56.44756509 60.42613992

Free Cash Flow 35,690,900 96,614,202 2,130,283,177 1,857,039,566

MegaMind Page | 24

Interpretations of Appendix F:

Liquidity:

2012

The current ratio of Kohinoor Chemicals is 1.08:1 and Beximco Pharma is 2.67. So, Beximco

is in a better position than Kohinoor Chemicals. It also implies that Beximco doesn’t utilize

its current assets properly to obtain investment. The quick ratio of Kohinoor Chemicals

(0.13:1) is far below than that of Beximco Pharma (1.88:1). So, Kohinoor should try to

improve this and Beximco should utilize its current assets properly. Current Cash Debt

Coverage Ratio of Kohinoor Chemicals (0.099) is also far below than that of Beximco

Pharma (0.61). So, Beximco can recover most of its current debt by its cash flow from

operation that Kohinoor can’t do.

2013

The current ratio of Kohinoor Chemicals has increased to 1.16:1, but for Beximco Pharma it

has decreased to 2.03:1 and it’s still better than Kohinoor Chemicals. It implies that Beximco

is trying to utilize its current assets effectively. The quick ratio of Kohinoor Chemical has

also increased to 0.15:1, but for Beximco it has fallen to 1.48:1 because it is trying to utilize

its liquid assets properly. Current Cash Debt Coverage Ratio for both the companies has

fallen, but Beximco is in a better position.

So, from our analysis above, we can state that Beximco is in a better position than Kohinoor

Chemicals in liquidity for both the year.

MegaMind Page | 25

Activity:

2012

Account Receivable Turnover of Kohinoor Chemicals (318.56) is higher than that of

Beximco Pharma (7.99). So, Kohinoor has higher ability to collect account receivable than

Beximco. Inventory Turnover ratio of Kohinoor Chemicals (2.53) is higher than Baximco

(2.01). So, the inventory needed to support a given level of sales is better for Kohinoor

Chemicals. Asset Turnover ratio of Kohinoor (1.6) is also higher than Baximco (0.38) So,

Kohinoor can generate more sales using its assets than Beximco. Whereas Beximco can’t

utilize its assets efficiently to generate sales. So, in 2012 Kohinoor Chemicals is in better

position in this regards.

2013

Account Receivable Turnover for both the companies have improved. But Kohinoor

Chemicals is in a better position. Inventory Turnover has increased for both the companies.

Asset Turnover for both the companies has also improved. It means the ability of companies’

assets to generate sales has increased. Overall, Kohinoor Chemical is in a better position in

2013.

Profitability

2012

Beximco can generate far more income from its sale than Kohinoor Chemicals which is

measured by Profit Margin on Sale. Return on Assets of Beximco (0.054) is also higher than

Kohinoor Chemicals (0.043). Which means Beximco can utilize its assets more effectively to

generate income. Return on Common Stock Equity of Kohinoor (1.35) is higher than

Beximco (0.08). So, Kohinoor can generate more income by effectively using its equity.

Earnings Per Share of Kohinoor (13.48) is also higher than Beximco (3.77). Payout Ratio of

MegaMind Page | 26

Kohinoor is far more than Beximco. But Price Earnings Ratio is higher for Beximco. It’s hard

to take decision about which company is more profitable in this year.

2013

Profit Margin on Sale has increased for Kohinoor Chemicals by a small amount but has

reduced for Beximco. And it is still higher for Beximco. Return on Assets has increased for

Kohinoor but remain the same for Beximco. Return on Common Stock Equity has improved

for Kohinoor but almost the same for Beximco. EPS for both the companies has increased.

On the other hand, Payout Ratio has decreased for both. Price Earnings Ratio has increased

for Kohinoor but decreased for Beximco but it is still far higher for Beximco. So, Kohinoor

Chemicals is in a better position in 2013.

Coverage:

2012

Debt to Assets ratio is higher for Kohinoor than for Beximco, which means Kohinoor

Chemicals generates more of its assets through creditors than Beximco does which is risky

for Kohinoor Chemicals. On the other hand, Beximco is not properly using its ability to take

more debt. But Times Interest Earned ratio of Kohinoor is less than Beximco. So, Kohinoor

has less ability to pay interest than Beximco. On the other hand, Cash Debt Coverage of

Kohinoor (0.07) are far below than Beximco (0.30). And Book value per share is also higher

for Beximco than Kohinoor. So, Beximco is in a better position than Kohinoor Chemicals in

this regard in 2012.

2013

The portion of assets that has been generated from creditors (Debt to Assets) has decreased

for Kohinoor but increased for Beximco which means it is properly using its ability to take

debt from creditors. Times Interest Earned that measures the company’s ability to pay interest

has improved for both the companies. Cash Debt Coverage ratio has reduced for Kohinoor

MegaMind Page | 27

Chemicals but slightly increased for Beximco. And Kohinoor Chemicals is in a very risky

situation. Overall, Beximco is in a better position than Kohinoor Chemicals in 2013.