72

December 2007 Royal Institute of Technology Karolinska Institutet Karolinska University Hospital Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

December 2007

Royal Institute of Technology

Karolinska Institutet

Karolinska University Hospital

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

For a digital version of this report (PDF), please visit www.ctmh.se

Table of contents

Introduction

1. Executive summary

2. About this report

3. The medical device industry is a large and increas- ingly important contributor to a modern economy

4. Sweden’s medical device industry has a proud his- tory, but the bar for success is rising and Sweden largely relies on aged inventions

5. Building a successful medical device industry requires purposeful collaboration between several stakeholders

6. Measured against international best practice, the Swedish environment for medical devices has important shortcomings

7. Each stakeholder needs to take action to ensure a strong future for the industry

Appendix

............................................................................................................................................................................................................................................. 4

.................................................................................................................................................................................................................................................. 5

........................................................................................................................................................................................................................................................ 8

................................................................................................................................................................11

...............................................................................................................................................................................................................15

.........................................................................................................................................................31

...................................................................................................................................................................................................................................45

........................................................................................................................................................................................................................55

........................................................................................................................................................................................................................................................................65

Partners and sponsors to the project

• Carl Bennet AB• CapMan• Chalmers University of Technology• Elekta AB• Gambro AB• Göteborg University• Innovationsbron• Karolinska Institutet (KI)• Karolinska University Hospital• Royal Institute of Technology (KTH)• Sahlgrenska Academy• VINNOVA

Project steering groupLars-Åke Brodin (Royal Institute of Technology)Bertil Guve, chairman (Royal Institute of Technology/Centre for Technology in Medicine and Health)Lars Kihlström (Karolinska University Hospital)Bo Norrman (Karolinska Institutet)Carl Johan Sundberg (Karolinska Institutet)

�

ThemedicaldeviceindustryisaveryimportantindustryforSweden–onthebasisofitscontributiontogrossdomesticproduct(GDP)andemployment.Theindustry’sinnovationsalsoelevatethelevelofhealthcareprovidedinSwedenandtherestoftheworld.

AsthreeofthemedicaldevicestakeholdersinSweden,weseegreatbenefitsinaclosercollaborationbetweenourownorganizationsandothers(e.g.,companies,government,finan-ciers,andindustry-networkorganizations).Primarybenefitsfromourperspectivewouldbeastrengthenedinnovationenvironmentandbetterhealthcare.

OverthelastfewyearsintheStockholmregionwehavemadeaneffortthroughthecreationofCentreforTechnologyinMedicineandHealth(CTMH)toidentifyandinitiateresearch,educationalprogramsandindustrialcollaborationfordevelopmentandimprovementofclinicalapplicationsandprocessesinhealthcare.Presentedinthisreportisacaseforfurtherstrengtheningoureffortsand,throughcollaborationwithotherstakeholders,increasingmedicaldeviceinnovationinSweden.Keycharacteristicsofourfuturecollaborationinthisareaarehighambition,focusandaction.

EventhoughweasinitiatorsofthisreportviewthisfromaStockholmperspectivewewouldliketostressthenationalrelevanceofthisreport.

Wewanttothankthesteeringgroup(Lars-ÅkeBrodin(RoyalInstituteofTechnology),BertilGuve(RoyalInstituteofTechnology/CTMH),LarsKihlström(KarolinskaUniversityHospital),BoNorrman(KarolinskaInstitutet),andCarlJohanSundberg(KarolinskaInstitutet))andalltheindividualswhohavecontributedtothiseffortthroughfunding,workshops,interviewsandguidance.Welookfor-wardtoanexcitingjourneytogetherandtobuildingonthemomentumcreatedduringthecreationofthisreport.

PeterGudmundson,President of the Royal Institute of Technology

BirgirJakobsson,CEO of Karolinska University Hospital

HarrietWallberg-Henriksson,President of Karolinska Institutet

5December,2007

Introduction

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

�

Executive summary

1Themedicaldeviceindustryislargeandfastgrowing,withveryattractivebenefitstoamoderneconomy.GlobalsalesamounttooverUSD200billionandcontinuedstronggrowthisexpectedtobedrivenbytheagingofthepopu-lation,theincreasedburdenoflife-stylerelateddiseases,productinnovation,growingwealthindevelopednationsandtheexpectedexpansionofhealthcareinunder-developedmarkets.Fromanationalperspective,astrongmedicaldeviceindustryisasourceofcompetitiveadvantageasitsupportsdistinctiveacademicenvironmentsandcreateshighincome,knowledge-intensivejobs.Moreimportantly,theindustrycontributestotheimprovementofhealththroughouttheworldthroughnewhealthcaresolutions.

Swedenhasaproudhistoryinmedicaldevices,basedongroundbreakinginnovationslikethegammaknife,dentalimplants,theimplantablepacemaker,andthedialysismach-ine.Theseandotherinnovationshavehelpedbuildleadingcompanies,aswellasanindustrythathasbeenastrongcontributortotheSwedisheconomy.From1999to2005,themedicaldeviceindustryinSwedenachievedconsistentGDPcontributiongrowthof10%peryeardrivenbyemployeegrowthof4%peryearandanoverallproductivityimprove-mentfarabovemostotherindustries.

Butthebarforsuccessintheglobalmedicaldevicearenaisrising,andSwedenisstillrelying,forthebulkofitsmedicaldevicerevenues,oninnovationsthatare30to50yearsold.Morecomplexinnovation,morestringentregulation,andincreasingcostpressureinthehealthcaresystemcontributetoamorechallengingenvironmentfordevicecompanies.Asthechallengetobringproductstomarketandtoachievetruedifferentiationincreases,andasthecustomerlandscapegrowsevenmorecomplexanddemanding,thequestioniswhetherSwedencankeeppacewiththebestintheindustry.WillSwedenseethecreationofnewgloballeadersandwillexis-tingleadersstrengthentheirpositionsthroughestablishingnew,attractivegrowthplatforms?

WhiletheSwedishindustrycontinuestoperformwell,therearesignsthatSwedenmaybelosingsomeofthedistinctive-nessithasachievedinthepast.Lookingacrossthemedicaldeviceindustrytoday,anumberofobservationsgivecauseforconcern.ItappearsthatSwedenisstartingtolosesomeofitsstrengthintherelevantresearchcommunities,andisstrugglingtoturngoodideasintoproductsandcompanies.ThesmallandmediumsizedSwedishcompaniesholdrela-tivelylimitedpotentialtogeneratenewgloballeaders.And,whileSwedenhassomelarge,globalcompanies,itseemstobeunabletomaximizethevalueofthesecompanieswhenitcomestobuildingstrongnetworksandinnovationclustersinthecountry.Overall,thelargecompaniesareactiveinmoreslowlygrowingsegmentsofthemedicaldevicemarket,andinsomecasesthereisariskofcontrolandownershipbe-cominglessSwedish.

Whatcanbedonebetter?Measuredagainstinternationalbestpracticecases,thecurrentenvironmentformedicaldeviceinnovationandcommercializationinSwedenhasimportantshortcomings.Ananalysisofinternationalsuccesscasesshowsthatbuildingastrongmedicaldeviceindustryrequiresstrongfocus,realcollaborationandlong-termcom-mitmentfromseveralkeystakeholders:academicinstitutions,leadinghospitals,government,financiers,networkorganiza-tionsandcompanies.Thereisnosingleformulaforsuccess,butdrawingonthesecases,fourcriticalenablersstandout:1)strongandalignedincentives2)worldclasscapabilities,3)activeindustrycollaborationandnetworks,and4)adequatefundingforresearchandearlycommercialization.Inaddi-tion,theexistenceorcreationofastrongandsophisticatedlocalhomemarkethasplayedanimportantrole.

TheincentivesysteminSwedendoesnotprovideenoughimpetusforphysiciansanduniversitiestodoenoughappliedresearchandcommercializeideas.Itistypicallyconsideredmoreacademicallyrewardingtoconductbasicmedicalresearchthanappliedresearch,andcommercializationof

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

�

researchoutputdoesnotprovidecareerbenefitsinthesamewayasinsomeothercountries,suchastheUS.Thistrans-latesintoaninsufficientlyentrepreneurialculture.Intermsofcapabilities,theshortageismainlyrelatedtocustomer-driveninnovationandcommercializationskillslikeinternationalmarketingandsalesandreimbursementmanagement.ThereisalsoageneralscarcityofconnectivityandnetworksinSwedentofacilitatecollaborationprojects,accessthehealth-caresystem,conductcross-disciplinaryR&Dandsupportcommercialization.Itisnoteworthyhowlittlethestakehol-dersknowabouteachother’sagendas,needsandassets.Ashortageoffundinghasalsoplayedarole,especiallythelimitedavailabilityofmedicaltechnology-specificresearchandproductdevelopmentfundingandearlyseedcapital.

Theseissuesarecomplex,andwhilemanyofthemhavebeenthesubjectofpastscrutiny,relativelylittleactionhasbeentaken.However,muchofwhatneedstobedonedoesnotrequiregrandreforms,andiswithinthereachandinfluenceofthekeystakeholders.Foreachstakeholder,aclearsetofactionsarerecommended.

Technical and medical universitiesneedto

1. Emphasizemedicaltechnologyinnovationandmake itahighpriorityontheirstrategicagendas,developcon- cretestrategicplanswithpriorityresearchareas,appoint medicaltechnologytaskforcestodeliveronthestrategic planandsecurefundingforresearchandcollaboration2. Mapandmarkettheirresearchcapabilitiestowardsthe industryandotheracademicinstitutionsanddevelop intellectualproperty(IP)sharingmodelstosimplifycol- laborationbetweenstakeholders3. Developmedicaltechnologyknowledgeplatforms,e.g., jointprofessorships,seminarsonhealthcareneeds, awardsformedicaltechnologyinnovationbasedoncross- disciplinarycollaboration4. Developandlaunchmedicaltechnologyeducational programsofrelevancetotheindustry5. Encourageandsupportresearchstafftofocusonmedi- caltechnologyresearchandproductdevelopment throughamedicaltechnology-targetedresearchfund6. Encourageandsupportcommercializationofresearch outputthroughhigh-qualitybusinessprogramsand incubators

University hospitals and county councilsneedto

1. Worktogethertoensurethatmedicaltechnologyinno- vationisahighpriorityontheirstrategicagendas, developconcretestrategicplanswithpriorityresearch areas,appointmedicaltechnologytaskforcestodeliver onthestrategicplanandsecurefundingforresearchand collaboration2. Increasecollaboration(productdevelopment,clinical researchandtesting,advisoryboards)with,andoutreach to,academiaandindustryandbetransparentabout clinicalproblemsinneedofmedicaltechnologysolutions3. Encouragehospitalstafftofocusonmedicaltechnology research,commercializationandclinicaltestingby includingcollaborationexperienceascriteriaforappoint- ingpositionswithinthehospital,makingfundingavail- able,creatingprestigiousinnovationawardsandmaking universities’businessprogramsavailableforhospitalstaff4. Ensurethathealtheconomicprioritiesaresetwithin countycouncilsandcommunicatedthroughouttheorga- nization

Companiesneedto

1. Identifyareasforinnovationsthatcanbesourced–and needtobesourced–fromoutsidethecompany2. Proactivelyreachouttoacademiaanduniversityhospitals inSwedentoexplorewhattheyhavetoofferinrelation totheseareas3. Buildbusinessorientedconnectionswithsmalland midsizedcompaniestoshareknowledgeinsalesandmar- keting,regulatoryandreimbursementissues4. EngageinaSwedish“focuscluster”

Governmentshouldconsider

1. Makingavailableasignificantmedicaltechnology- focusedclusterfundandmakeinvestmentssubjectto clearcommerciallyviableinvestmentcriteria2. Allocatingfundsforappiedmedicaltechnologyresearch withaneeds-drivenfocusforwhichindividualresearchers canapply3. Intentivizingacademicinstitutionstomotivateandsup- portresearchersincommercializationby,forexample, providingadditionalfundingforcommercialization,and reviewinganoptiontoincludeanadditionalregulated taskforuniversities(i.e.,commercializationofresearch output)

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

�

Althoughachievable,thesumoftheseactionsrepresentsasignificantchallenge.Tomovequicklytoaction,itissug-gestedthatstakeholdersshouldfindanumberoffocusareas(“focusclusters”)forinnovationandcommercializationwherethereisnaturalenergytobuildon.Theseshouldbeareasthatrepresentsignificantunmetcustomerneedandfitwiththecapabilitiesoftheacademicinstitutions,andwherethereisanexistingandmotivatedlargecompanywhichiswillingtocommitandinvest.Candidatesforsuchfocusareascouldbeelderlycare,aspecificcancersegment,e-healthorpatientaids.TheambitionlevelforSwedishleadershipshouldbesetveryhighinordertofocustheagendasofallkeystakehol-

ders.Stronglocalnetworksneedtobebuilttoorchestratethedevelopmentandresourcesettingofthesefocusclusters.Thesenetworkscaneitherbebasedonexistingones,liketheCentreforTechnologyinMedicineandHealth(CTMH)ortheyneedtobebuilttosuitthespecificneedsofeachcluster.

***Swedenhasastrongfoundationtobuildoninthemedicaldeviceindustry,butachievingtheambitousgoalslaidoutinthisreportwillrequirealevelofcollaborationandcollectiveenergythatisstarklydifferentfromtoday.Furtheranalysisisoflimitedvalue,andactionisoftheessence.

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

�

About this report

2Inrecentyears,medicaltechnologyinSwedenhasattractedmoreinterestfrompoliticians,venturecapitalists,themediaandotherinstitutionsthanbefore.Inearlyspring2007,theRoyalInstituteofTechnology(KTH)inStockholminvitedrepresentativesoftheSwedishmedicaltechnologyindustry,KarolinskaInstitutet(KI)andKarolinskaUniversityHospitalintodialogue.TheaimwastodiscussthechallengesandpotentialoftheSwedishmedicaltechnologyenvironment.Morespecifically,attentionwaspaidtotheconditionsneces-sarytocreateanefficientinnovationprocessthatincludestheindustry,theuniversitiesandthehealthcaresystem.Asaresultofthisdiscussion,KTHtooktheinitiativetocreatetheprerequisitesforamajornationalstudyonthesubject.Duringthespringof2007thevicepresidentcommissionedtotheCentreforTechnologyinMedicineandHealth,CTMH,(ownedbyKTH,KIandtheStockholmCountyCouncil)to

leadthestudy.Asteeringgroupwascreatedwithrepresen-tativesfromKTH(SchoolforTechnologyandHealth),KI(UnitforBioEntrepreneurship)andKarolinskaUniversityHospital(FoUU,DepartmentforResearch,DevelopmentandEducation).Thegroupgatheredfinanciersandpartnerstothestudyandlaunchedthestudyinthesummerof2007.

Thescopeoftheworkhasbeentoidentifyandigniteactionrelevanttoimprovingthepossibilitiesandtheclimateformedicaltechnologyindustry,researchandhealthcareinSweden.Asthereportanditsrecommendationsshow,thereareseveralactionsthatcanandneedtobetakenbytheinsti-tutionsandcompanies.Notallsolutionsarecomplex.Andthereisaneedforactingwithasenseofurgency.

Backgroundtothereport............................................................................................................................................................................................................................

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

�

ThemajorfocusofthisreporthasbeentoprovideaholisticreviewoftheSwedishmedicaldeviceindustrybydrawingonexperiencesfromtheformerandcurrentsituation,andnatio-nalandinternationalindustry.Themainquestionsaddressedinthereportare

• HowhastheSwedishmedicaldeviceindustryperformed overthelastfivetofifteenyears?• Whatarebestpracticeexamplesforcreatingastrong medicaldeviceindustry?• Whatlessonscanbelearnedfromtheseexamples?• WhatshouldSwedishstakeholdersdotosecurethe futuresuccessoftheindustry?

ManyexcellentreportshavebeenwrittenoverthelastfewyearsonhowSwedencanimproveitspharmaceutical/bio-

technology/medicaltechnologyindustryandresearch.Thisreportdiffersfromotherreportsinthreeways

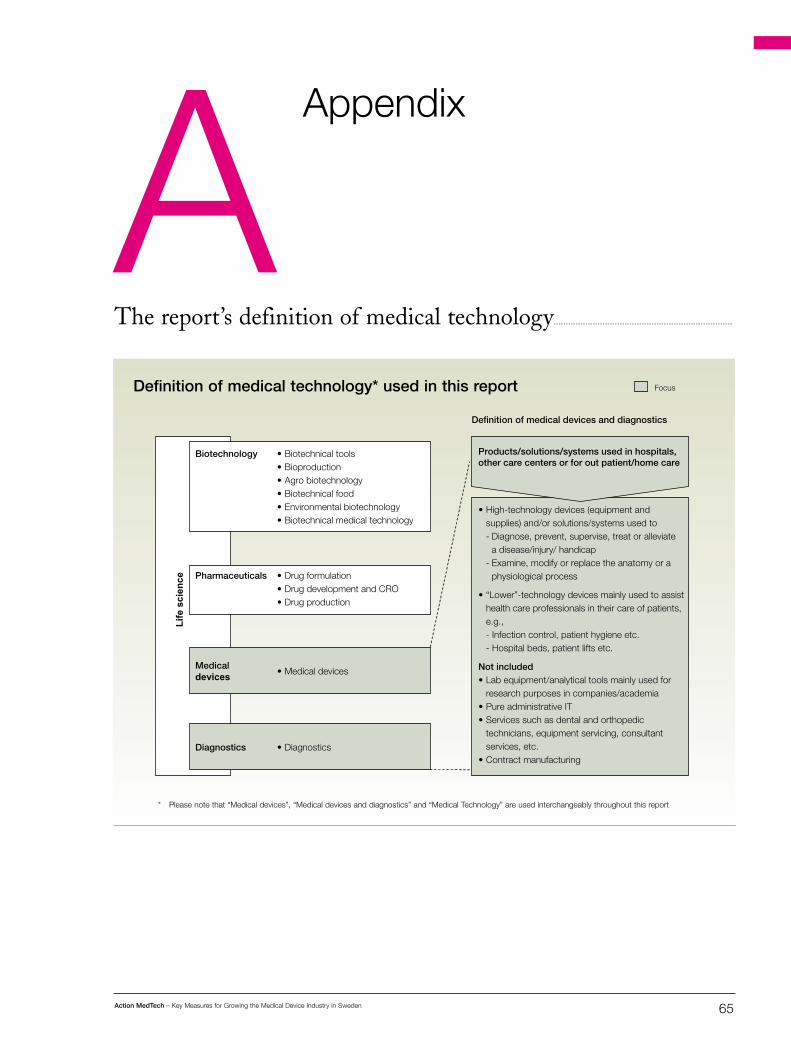

• First,itisfocusedsolelyonmedicaldevicesanddiag- nostics(fordefinitionpleaseseeappendix)• Second,itconcludesthattheexistingindustryisactually performingbetterthanmanyreportshavehighlightedas thereisapositivetrendinGDPcontribution,number ofemployees,productivity,andexports.Yetthereport doeshighlightthatthebarforsuccessintheindustryis goingupandthatSwedenlackssomekeyconditions, indicatingthatactionisneeded• Third,therecommendationsarefocusedoncollaboration andwhateachstakeholdercandotocontributerather thansolelyrelyingongovernmentintervention

Commentsonfocusandcontent..................................................................................................................................................................................

Thesteeringgroupfortheprojecthasconsistedofrepresen-tativesfromKTH,KIandKarolinskaUniversityHospital:Lars-ÅkeBrodin(KTH),BertilGuve,chairman(KTH/CTMH),LarsKihlström(KarolinskaUniversityHospital),BoNorrman(KI),andCarlJohanSundberg(KI).Theste-eringgrouphasreportedtothedeputypresidentofKTH,MargaretaNorellBergendahl.

McKinsey&Company,aninternationalmanagementcon-sultingfirm,hassupportedthesteeringgroupintasksoffactgatheringandanalysisby

• Conductingapproximately50interviewswithkeystake- holders(CEOsofmedicaldevicecompanies,hospital CEOs,presidentsofuniversities,researchers,etc.)• Conducting4workshopswithover40stakeholderrepre- sentatives• Interviewinginternationalmedicaldeviceexpertsto understandinternationalcases

TheultimateobjectivehasbeentomapoutthecurrentstateoftheSwedishmedicaldeviceindustryandoutlinerecom-mendationsforthefuture.

Modusoperandi...............................................................................................................................................................................................................................................................................

ForquestionsregardingthisreportpleasecontactBertilGuveattheCentreforTechnologyinMedicineandHealth(CTMH;KTH-KI-SLL).Foradigitalversionofthisreport(PDF)pleasevisitwww.ctmh.se

Contact................................................................................................................................................................................................................................................................................................................................

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

11

The medical device industry is a large and increasingly important contributor to a modern economy

3The medical device industry has seen strong growth in recent years, and has delivered innovations over the last �0 years that have improved the health and welfare of millions of people throughout the world.

The global medical device industry – an explosion in innovation

Note: See appendix for explanation of abbreviations and definitions

Source: Interviews with medical device industry representatives

1980 – 90s

1950s

1960s1970s

• External Defibrillator• Intra-ocular lens• Haemodialysis

• X-ray Angiography• External Pacing• Fixed rate implanted pacer• Charnley Intramedular hip• Heart/lung bypass

• Solid state X-ray• Mechanical Heart Valve• Intra-Aortic ballon pump• IPPV ventilators• Artificial heart implant• Fiber optic endoscopy• CABG procedure

• High quality Ultrasound• CT• PTCA• Diagnostic Electrophysiology• Trans-cut. nerve stimulator• Hollow fibre dialysis• PTFE vascular grafts• Pulse oximetry• Skin staplers• Radial Keratotomy

• Digital Subtraction Angiography• MRI• Nasal ventilation for sleep apnea• Bone stimulation• Implanted defibrillators• Epilepsy ‘pacers’• Coronary stenting• Radioablation• Endoscopic surgery• Intravenous oxygen therapy• Tissue growth factors• Drug eluting stents• Xeno-transplantation• Artificial bone

1940s

EXAMPLES

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

12

TheglobalmarketformedicaldevicestodayismorethanUSD200billionandisestimatedtogrowbyapproximately7%peryear1.Itemploys800,000individualsthroughouttheworld2(whereofapproximately10,000areinSweden).WhiletheUSishometothelargestshareoftheindustry,anumberofothercountries(e.g.,Germany,SwitzerlandandJapan)accountforasignificantshare,includingSweden3.Inaddi-tion,themedicaldeviceindustryhasdeliveredmoreshareholdervaluethanmanyotherindustriesoverthelast15years4.

Themedicaldeviceindustryisprojectedtocontinuetoachievestronggrowthandtobeacatalystforsubstantialjobcreation.Twomainfactorsfueltheindustry’sgrowth.First,theongoingdemographicshift,withanagingpopulationindevelopedcountries,islikelytoleadtoincreaseddemandforhealthcareandhealthcare-relatedproductsandservices.Second,thereisagrowingimportanceoflifestyle-relateddiseases(weight-relatedconditions,type2diabetes,heartattacks,etc.),whichinmanycasesincreasethedemandforbothpharmaceuticalsandmedicaldevices.Inadditiontothesetwofactors,increasingwealthindevelopednationsdrivesdemandforadvancedhealthcare,withtrendsshiftingtowardsgrowingimportanceofadvanceddiagnostics(e.g.,imagingtechnologies)andminimallyinvasivetechnologies.

Inthefuture,expansionofhealthcareinunder-developedmarketsisalsolikelytogrowthemedicaldevicemarket5.

Thereareseveralimportantbenefitsofthemedicaldeviceindustry.Inaglobalizedlabormarket,inwhichlow-skilledworkisincreasinglysubjecttooffshoring,countrieswillfindthatacomplexanddemandingindustrylikemedicaldevicescanbeanimportantsourceofcompetitiveadvantage.Theindustrycanalsoserveasasupportingmechanismforathrivingacademicenvironmentaswellascreateattractivehighincomejobs.Furthermore,thereisarippleeffect,witheveryjobintheindustrysupportingseveralotherbusines-sesinadjacentindustriesandtherebycreatingadditionaljobopenings.TheMilkenInstitute,anAmericanindependenteconomicthinktank,suggestsinastudyoftheSanDiegoareathateachjobinthemedicaldeviceindustrycreates1.5additionaljobsinotherindustries6.Applyingthisfactortotheoverallindustry,over2millionjobsaresupportedbythemedicaldeviceindustryglobally.

However,asbeneficialasthesecontributionstotheoveralleconomymayseem,themostobviousandmostimportantbenefitofthemedicaldeviceindustryisthatitsaveslivesandhelpscureandtreatdiseases.

Global annual growth in total return to shareholders* by industryCAGR 1��1–200�, percent

* Not adjusted for inflation

Source: Datastream

8

4

7

8

9

10

10

15Biotech

Medical devices

Telecom

Automotive

Total global market

Consumer goods

Pharmaceuticals

Pulp and paper

1 Opportunitiesinglobalmedicaldevicesanddiagnostics,HealthResearchInternational,2006

2 USCensusBureauannualsurveyofmanufacturers;Eurostatannualdetailedenterprisestatistics;MHLW

3 Opportunitiesinglobalmedicaldevicesanddiagnostics,HealthResearchInternational,2006

4 Datastream

5 Opportunitiesinglobalmedicaldevicesanddiagnostics,HealthResearchInternational,2006

6 America’sBiotechandLifeScienceClusters:SanDiego’sPositionandEconomicContributions,MilkenInstitute2004

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

13

Examples of remaining opportunities for breakthrough innovations

Note: See appendix for explanation of abbreviations and definitions

Source: Interviews with medical device industry representatives

Wound Management• Growth factors• Tissue engineering

In Vitro Diagnostics• Diabetes (glucose testing)• Molecular diagnostics

Neurology/Neurosurgery• Neurostimulation• Central nervous system (CNS) function monitors• See also under “vascular surgery”

Cardiology - medical• Biodegradable drug eluting stents • Cell therapy• Percutaneous valves

Vascular surgery• Vulnerable plaque • Transvascular drug delivery

Operating room support • Visualization• Robotics• Information

Urology surgery• Benign Prostatic Hyperplasia (BPH)• Incontinence• Brachytherapy

Obstetrics/Gynecology• Fertility• Endometrial ablation• Female incontinence

Orthopedic surgery• Disk/spine repair• Soft tissue repair• Accelerated fracture healing• Artificial bone

Emergingbreakthrough

areas

InSweden,anumberofstakeholderswouldbenefitfromthecontinuedsuccessofastrengthenedmedicaldeviceindustry7

Universitieswouldgaina)areasontodevelopworldclassskillsincoreareas,b)potentiallylargerbudgetsfromprofit-sharingwithfocusclusters8,aswellasc)additionalresearchfundingthroughincreasedcollaborationwithindustry.

County councils and university hospitalsmightgainadditionalfundsthroughcollaborationwithindustryonproductdeve-lopmentinitiativesandclinicaltesting.Theseinstitutionswouldalsobenefitfromamoreinnovativeenvironment,whichcouldleadtoearliertreatment(throughincreasedinvolvementinclinicaltrials)andbetter,morecost-efficienthealthcare.Healthtechnologywouldbeaddedaspartoftheregionaldevelopmentengine.Aconsciousmedicaltechno-logydevelopingenvironmentcouldhelptostimulateacon-tinuingqualityimprovementculture,whichbenefitspatientsimmediately.Swedishhospitalscouldfurtherstrengthentheirbrandasbeingasourceofkeyinnovations.Inaddi-tion,throughincreasedfocusonhigh-qualityneeds-drivenresearch,directorsofclinicaldepartmentswouldbeabletoattractclinicianswithsuperiorskillsinresearch.

Companies (domestic and foreign)wouldhaveanopportu-nitytoa)sourcetheinnovationandcoreworld-classskillsatSweden’suniversitiesandhospitals,b)testanddevelopproducts,andconductclinicaltesting,inamoreaccessibleandhigh-qualitycareenvironment,andc)developcloserrelationshipstoresearchers,cliniciansandothercompaniesthatwouldfacilitatetheirdevelopmentandgrowthaswellassecureeasieraccesstonewmanagementtalent.

Theeffectisthatthegovernmentwouldenjoynotonlyahigherdomesticemploymentinwell-payingjobs(whichwillstimulatefurtherjobcreationandgeneratemoretaxrevenue)butalsoanimprovedresearchenvironment,whichwouldbenefitrelatedindustriesandacademicfields.

Thefinalstakeholdergroup,investors,wouldalsoprofitviaa)newinvestmentopportunitiesinmedicaltechnologyaswellasotherindustriesandb)occasionstostrengthenexistingport-foliocompaniesthroughastrongermedicaltechnologynetwork.

Giventhesebenefits,thedevelopmentofastrongandvibrantmedicaldeviceindustryshouldbeactivelyencouragedbycountries,companies,academia,investors,thehealthcaresys-temandprivatecitizens.

7 Interviewsandworkshopspursuedduringthiseffort

8 Medicaldeviceclustersfocusedonsub-segments,e.g.,elderlycare,drivenjointlybykeystakeholders(forfurtherdescription,seechapter7)

NOT EXHAUSTIVE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

1�

Sweden’s medical device industry has a proud history, but the bar for success is rising and Sweden largely relies on aged innovations

�Historically, the Swedish economy has benefited from the

strength of the Swedish medical device industry. However,

many of the innovations that represent the backbone of the

industry today date back 30 to �0 years, which raises the

question of whether Sweden can sustain and strengthen its

position through a continued stream of innovation. The bar for

success is rising and there are signs that Sweden is starting

to lose some of the distinctiveness it has enjoyed in the past.

TheSwedishmedicaldeviceindustryisalarge(SEK60bil-lion)andhighlyconsolidatedsector(fivecompaniesrepresentapproximately75%ofrevenues9)–onewhichhasachievedconsiderablesuccessthroughouttheworld.WhileSwedenaccountsforlessthan1%oftheglobalmarketformedical

devices,theSwedishmedicaldevicecompanies10accountforapproximately4%oftheglobalmarketrevenues11.AndinanindustrydominatedbyUSplayers,Swedenhastwocompa-nies(GambroandGetinge)ontheglobaltop-50list12.

9 ReviewofmedicaldeviceanddiagnosticcompaniesinSwedenbasedondatafromStatisticsSweden,Odin,SwedishcompaniesRegistrationOffice,VINNOVA,SwedishMedtechand interviews.RevenuedatafromannualreportsorOdin

10DefinitionofSwedishcompaniesinthisreport:CompaniesownedbyaSwedishcitizenoraSwedishcompany,companieslistedontheSwedishstockexchangeandcompaniesoriginating fromandwithoperationsinSwedenandthatcurrentlyareownedbyany(domesticorforeign)privateequityfirm

11Opportunitiesinglobalmedicaldevicesanddiagnostics,HealthResearchInternational,2006;TheWorldMedicalMarketReport,EpsicomBusinessIntelligence,2005

12Opportunitiesinglobalmedicaldevicesanddiagnostics,HealthResearchInternational,2006

Swedenhasaproudhistory...............................................................................................................................................................................................................

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

1�

Annual sales of Swedish companies by company and by industry segmentSales from latest available year (200� or 200�); 100% = SEK ~�0 billion

Note: Based on 31� identified companies (identified from Swedish industry, SNI codes 33.101, �3.103, 2�.�2, 3�.�3, �1.��, �1.��1, interviews, trade organizations,

VINNOVA, and patent publications). Financials from latest available year (200�-200�)

* Data from 200�. Revenues from Gambro Healthcare US that were divested in 200� excluded. Revenues from remaining Gambro Healthcare (non-US clinics)

that were divested in 200� included (accounting for 13% of total revenues in 200�)

** Assuming �0% of AstraTech’s revenues are in urology and renal and 30% are in dental

Source: Statistics Sweden; Swedish Companies Registration Office; Odin; VINNOVA; Swedish Medtech; Interviews

7%

26% Urology & Renal

Surgical tables, lights andfixed systems

13% Dental

Energy-basedtechnologies

Infection control 7%

Surgicaldressings,drapes

Patient aids 4%

Wound care 4%

Blood processingand therapyproducts 4%

Other 14%

8% 12%

26% Gambro*

23% Getinge

12%MölnlyckeHealthcare

NobelBiocare 9%

Elekta 7%

Astra Tech 5%

Phadia 3%Permobil 2%

Other 13%

Sales by company Sales by segment**

Top 50 global medical device and diagnostics companies, 2006Revenues in USD billions

* Data from 200� (includes non-US dialysis clinics)

Source: Company filings -

20.21. J&J MD&D (US)

16.62. GE Healthcare (US)

12.73. Fresenius (GE)

12.34. Medtronic (US)

10.35. Siemens Medical (GE)

9.66. Tyco Healthcare (US)

9.37. Fuji Medical Systems (JP)

8.58. Philips Medical (NL)

8.39. Baxter (US)

7.810. Boston Scientific (US)

7.011. Roche Diagnostics (CH)

5.812. Becton Dickinson (US)

5.413. Stryker (US)

4.914. Alcon (CH)

4.215. B. Braun (GE)

4.016. 3M (US)

4.017. Abbott Labs (US)

3.518. Zimmer (US)

3.319. St. Jude Medical (US)

2.820. Smith & Nephew (UK)

2.621. Olympus (JP)

2.522. Beckman Coulter (US)

2.523. Eastman Kodak (US)

2.524. Terumo (JP)

2.325. Synthes (CH)

2.226. Schering AG (GE)

28. Gambro* (SE)

1.339. Kimberly Clark (US)

2.127. Biomet (US)

2.028. CR Bard (US)

1.929. Bayer Diagnostics (GE)

1.930. Dade Behring (US)

1.831. Cardinal Health (US)

2.0

1.833. Getinge (SE)

1.634. Varian Medical Systems (US)

1.635. Dräger Medical (GE)

1.536. Toshiba Medical (JP)

1.537. Guidant (US)

1.538. Invacare (US)

1.340. Biomerieux (FR)

1.341. Hill-Rom (US)

1.042. Respironics (US)

1.043. Hitachi Medical (JP)

1.044. Edwards Lifesciences (US)

0.945. Hospira (US)

0.546. Coloplast (DK)

0.547. Bristol Myers Squibb (US)

0.548. Dentsply (US)

0.549. Hartmann Group (GE)

0.450. Bracco Diagnostics (IT)

( ) = Nationality

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

1�

Themedicaldeviceindustryhashistoricallyperformedbet-terthanmanyotherindustrialsectorsinSweden(e.g.,tele-com,automotive,andpulpandpaper)inGDPcontributiongrowth,whichwasapproximately10%CAGR131999to2005(comparedto-6to5%forpharmaceuticals,automotiveandpulpandpaper).

Thishasbeendrivenbyanemployeegrowth,whichwasapproxroximately4%CAGR(comparedto-3%to2%fortheotherindustries)andstrongproductivityimprovementsof

CAGR11%14overthesameperiod.Currentlyapproximately10,000peopleareemployedinSwedeninthemedicaldeviceindustry15ofwhichalargeshareisemployedbythetopfiveSwedishcompaniesandlargeglobalcompanieswithopera-tionsinSweden.

Inaddition,theSwedishmedicaldeviceindustry’snetexportshavebeenfairlystablecomparedtomanyothercountriesandhavebeenexperiencingaslightoverallincrease.

Note: Value add as share of GDP. Sample of companies included in respective industry: Pharmaceuticals: AstraZeneca, Pfizer, Recip; Automotive:

Volvo, Scania, SAAB automobile; Pulp & Paper: StoraEnso, SCA, Billerud; Telecom: Ericsson, Flextronix, Powerwave technologies

* 1���–2003, numbers past 2003 are not disclosed by Statistics Sweden. Industry sector’s negative contribution to GDP in 2001 driven by

large losses by several players in the industry.

Source: Statistics Sweden

-0.2

0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

1999 2000 2001 2002 2003 2004 2005

Year

Industry share of Gross Domestic Product (GDP)Percent

Pulp & paper

Automotive

Pharmaceuticals

Medical devicesand diagnostics

Telecom

5.4%

-4.3%

-6.1%

9.7%

-26.9%*

CAGR 1999–2005

GDP contribution growth of Swedish medical device industry compared to other industries

13SeeappendixforexplanationofCAGR

14StatisticsSweden

15StatisticsSweden

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

1�

Note: Sample of companies included in respective industry: Pharmaceuticals: AstraZeneca, Pfizer, & Recip; Automotive: Volvo, Scania, SAAB automobile;

Pulp & Paper: StoraEnso, SCA, & Billerud; Telecom: Ericsson, Flextronix, & Powerwave technologies

Source: Statistics Sweden

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

1999 2000 2001 2002 2003 2004 2005

Year

Medical devicesand diagnostics

Pharmaceuticals

Automotive

Pulp & paper

Telecom

Number of employees in Sweden by industry

1.6%

-0.7%

-2.6%

3.5%

-8.5%

CAGR 1999–2005

Employee growth of Swedish medical device industry compared to other industries

93

145 160

49

Getinge AB

~200

~40~760b ~1,000Gambro

474Nobel Biocare

~100

~25

121

~300MölnlyckeHealthcare

71

52

28200Elekta

R&D

Marketing & sales

Manufacturing

Other

22733

750 251 1,306

~175

100

165

250~815dSt Jude Medical

20

70

1250c450

380 470Becton Dickinson

Johnson & Johnson

Medtronic

1,700GE Healthcare

~15430 120

Swedisha companies Foreign companies

128

66257eSiemens Medical

Solutions

63

Selection of Swedish and foreign medical device companies in Sweden by employee number and typeData as of November 200�

Note: a As defined in this report (see reference 10)

b Both manufacturing and other

c Both manufacturing, marketing & sales and other

d Two different companies

e Including 3�–�0 people in Finland

Source: Swedish Medtech; Interviews with company representatives; Corporate web sites; Annual reports

ESTIMATE

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

1�

* Not including sub suppliers

** 1���–2003, numbers past 2003 are not disclosed by Statistics Sweden

Source: Statistics Sweden; Swedish National Accounts

-20

0

20

40

60

80

100

120

140

160

180

200

Year

20042002

Medical devices

Automotive

Pulp & paper

Telecom

Sweden total

2000

Pharmaceuticals

Productivity, value add/hours workedIndex, 100 =1999

CAGR 1999–2005

11.1%

4.0%

10.3%

1.8%

-3.3%*

-17.5%**

Productivity of Swedish medical device industry compared to other industries and average

16UNComtradedatabaseSource: United Nations Comtrade database

0

500

-2,000

-1,500

-1,000

-500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1990 92 94 96 98 2000 02 04 2006

Sweden

Germany

Ireland

Japan

Netherlands

UK

US

Year

Net exports of medical instrumentsUSD millions

Swedish net exports of medical instruments compared to other countries

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

Source: United Nations Comtrade database

0

50

100

150

200

250

300

350

400

1990 92 94 96 98 2000 02 04

Year

2006

CAGR 90–06:2.8%

Net exports of medical instruments, SwedenUSD millions

Swedish net exports of medical instruments

Swedenhasasetofstronganduniqueprerequisites......................................................................

Interviewswithcompanyrepresentativesandworkshopsper-formedtosupportthiseffortrevealthatthelong-termcom-petitivenessoftheSwedishmedicaldeviceindustryhasbeenenabledbytwoprimaryfactors

• Highqualityhealthcaresystem.Swedenhasareputation forrigorousevidence-basedhealthcareresultingina healthypopulation.Ithasalsomeantthatmanycompa- nieswishtoleveragethe“approvedinSweden,usedby Swedes”brandasitincorporatesinternationally-renowned medicalresearcherswhostrivetoimprovemedicalcare. Thebrandalsorepresentsawell-educated,socio-econo- micallystablepopulation,withhightrustintheirhealth- caresystem,andagreaterwillingnesstoparticipatein clinicaltrialsthaninmanyothercountries• Anetworkoflarge,coordinateddiseasedatabasesthat captureinputfromextensive“patientregisters16”.These databasesareuniqueinternationallyandprovidenotonly agoodtoolformeasuringoutcomesofdevicesbeing testedbutalsomayindicateanareaofunmetneed (orroomforproductdevelopment)ifthereareareaswith pooroutcomes

Otherreports17havecitedadditionalfactorsbenefitingSweden’smedicaldeviceindustry.Thesefactorsinclude:

• Strongindustrytradition,withgoodengineers• Government-initiatedinstitutionsfocusedonearlystage commercializationfunding• Competentandefficientregulatoryauthorities,whoare knownforbeingefficientintheirapprovalprocess, leadingtoshorterleadtimesthaninsomeother Europeancountries• Teacher’sexemption18thatgivesresearchersandscientists atacademicinstitutionsapersonalincentivetocom- mercializefindings,sincetheyown100%oftheintellec- tualpropertyofanyfindings

ThequestioniswhetherSwedencankeepupthisstrongperformance.Theindustrytodaystillrelies,forthebulkofitsrevenues,oninnovationsthatare30to50yearsold(e.g.,thegammaknife,dentalimplantsandthedialysismachine).Inordertoensurecontinuedsuccess,acontinuedstreamofinnovationandglobalcommercializationisrequired.

16ManagedbySocialstyrelsen,www.socialstyrelsen.se

17E.g.,MedicinförSverige!Nyttlivienframtidsbransch,SNSförlag,2007

18Teacher’sexemption,seeappendix

20 Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

21

Overthepastfewdecades,theglobalmedicaltechnologyindustryhasdevelopedintoamuchmorechallengingenvi-ronment.

Rising bar to achieve product differentiationTherearemanymoreproductsonthemarkettodaycompa-redto30yearsago.Competitionforgroundbreakingideasisfierceandnewimprovementsarefightingforattention.Growthisincreasinglydrivenbyimprovementinexistingproducts,andasaresult,theclinicalandeconomicdifferenti-ationbetweenproductshaslessened.Manycompanies’R&Ddepartmentsarefocusedondevelopmentofintegratedsys-temsandsolutions,notsimplyproductsalone.Forexample,Kineticsdoesnotjustoffera“WoundV.A.C.”19productbutalsoprovideswoundcarenursestotrainhospitalsandhomecarenursesonitsuse,aswellasreimbursementspecialiststoassistwithbilling.Intoday’senvironment,foracompanytohaveacompetitiveadvantagewiththesemorecomplexoff-eringsitmustdependonheaviermarketingandsalesefforts,thusincreasingthecostofdoingbusiness.

Longer regulatory approval timesIntheEuropeanUnion,regulatorydemandsonmedicaldeviceshaveintensifiedduetotheintroductionoftheCEmarking20inthe1990s.WhiletheCEmarkingsimplifiestheoverallregulatoryprocessinEuropebyeliminatingtheneedfordevicestobecertifiedbyeverycountry,ithasledtostricterregulationsinseveralcountries.Theneteffectisthatahigherinvestmentisrequiredbeforenewproductsgeneraterevenues.

More complex customer landscapeWhilephysicianpreferenceisstillanimportantdecidingfactorforpurchasingmedicaltechnology,payors(e.g.,in-surancecompanies),providers(e.g.,hospitals)andpatientsareincreasinglyimportantcustomers.Hence,anexpandedandimprovedmarketingeffortthatcommunicatesproduct/therapybenefits,andmakescomplexclinicaloutcomedataunderstandabletothisdiversegroup,isrequired.Forexample,Johnson&Johnsondirectlymarketsitshipreplace-mentstopatientsintelevisionadsintheUnitedStates21.

Increasing regulatory demands, especially for combination pharma/device productsToday’sadvancedproductsoftencombinedevicecapabilitieswithpharmaceuticalcharacteristics(e.g.,drug-elutingstentsthattreatheartdisease).Thesecombinationproductsrequireamoreadvancedregulatoryapprovalthatincludesnotify-ingbodiesthatareabletoensuresafetyofboththedevicecomponent(traditionalCEmark)andthedrugportion(tra-ditionalEMEA22)withadvicefromrelevantpharmaceuticalauthorities.Manytimes,thedevicecompaniesarenotoffe-ringanewdrugbutareofferinganewdeliveryroute(drugisdeliveredbythedeviceasopposedto,forexample,orally)andthesafetyofthisnewroutemustbeassessed.AcombinationproducttypicallywillhaveanunpredictableroadaheadforregulatoryapprovalintheEU.Comparedwithpuredevices,moresophisticatedin-houseclinicalandregulatoryskillsarerequiredtotacklethecombinedpharmaceuticalapprovalpro-cess.Theresultislongertimelines.

Cost pressureTheincreasedcostpressureonhealthcaresystemschallengesthemedicaldeviceindustry.Hospitalsfacecostandmarginpressurefromdecliningreimbursementlevels,whilepayorsareconcernedaboutrisinghealthcarecostsgeneratedfromincreasedutilizationoftechnologyandincreasinglyrequireevidenceofhealth-economicbenefitsbeforepayingfornewerproducts.Financially-motivatedphysicians(viaphysicianownershipandprofitsharing)mayturnawayfrompremiumbrandsandalsodemandimprovedeconomicevidencebeforetheyagreetousecertainproducts.Hence,devicecompaniesareforcedtodelivercompellingeconomicdataaswellasclinicaldatatohospitals,payors,andphysicians,especiallyfornew,high-priceproductsandprocedures.Hospitalsalsogeneratepressureinanotherway:hospitalgroupsareforminglargerandincreasinglymoreskilledpurchasingorganizations.Asaresult,devicecompanieswillneedtobuildorenhancein-housecontractingcapabilitiestodirectlynegotiateandcontractwithbuyinggroupsandhospitals.Clearpricingstra-tegies,simplebutrobustcontracttemplates,andcommercialcapabilitiesofthesalesforcewillthusbecomeincreasinglyimportantfordrivingpricing/contractingdecisions.

Thebarforsuccessisrising:globaltrends..............................................................................................................................

19 WoundV.A.C.isalowtechnologydevicemadeofsponge,plasticsheetandvacuumdevicethatrevolutionizedthetreatmentoflargechronicwounds.KineticConceptsInc.,www.kcil.com

20CEmarking:seeEuropeanCommission,GuidetotheImplementationofDirectivesBasedonNewApproachandGlobalApproach,chapter7 (ec.europa.eu/enterprise/newapproach/legislation/guide/index.htm)

21Johnson&Johnson,www.jnj.com

22EMEA,EuropeanAgencyforEvaluationofMedicalProducts,www.emea.europa.eu

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

22

IsSwedenrisingtothechallenge?..........................................................................................................................................................................

Inmanyways,theSwedishmedicaldeviceindustrycontinuestodoverywellandmostoftheleadingcompaniesarekeep-ingtheirposition.WhentryingtoassesswhetherSwedenisontherighttrackitis,however,importanttotestthedyna-micsoftheentireindustry,fromideageneration,throughtotheestablishmentofnewandexcitingcompanies,aswellastheclimateforandperformanceoftheestablishedlargecom-panies.Inalloftheseareas,thepictureismixed.TherearesignsthatSweden’smedicaldeviceindustryisstartingtolosesomeofitsdistinctivenessintherelevantresearchcommuni-tiesandthatSwedishdevicecompaniesstruggletoturngoodideasintoproducts.ThesmallandmediumsizedSwedishcompanieshavearelativelylimitedpotentialtogeneratenewgloballeaders.And,whileSwedenhasstrong,leadingglo-balcompanies,itisnotabletomaximizethevalueofthesecompanieswhenitcomestobuildingstrongnetworksandinnovationclusters.Indeed,adisproportionateshareofthelargecompaniesisfocusedontheslower-growthpartsoftheindustry.

Distinctiveness in innovation and commercialization ThereviewofSweden’sstrengthsininnovationisbasedonanalysesoftwoindicators:articlespublishedandpatentsfiled23.Historically,Swedenhasbeenexceptionallysuccess-fulinbothareas,butothercountriesarecatchingupandSwedenhasdroppedtobeing“average”relativetoEuropeanpeercountries,suchasSwitzerland,Denmark,GermanyandtheNetherlands24.

Medical technology publicationsaredifficulttoanalyze,asthereisnoobviouswaytoselectpublicationsrelatedtotheverydiversefieldofmedicaltechnology.Therearefewjournalsdedicatedtomedicaltechnology,andjournalsthatpublishpapersonmedicaldevicedevelopmentspecializeeitherintherelatedtherapeuticarea,orintherelatedtech-nologyarea.ForthisanalysisthechoicewasmadetolookatpublicationsthatareindexedinMedline25underaselectionofMedicalSubjectHeadings26(commonlyknownasMeSHterms)thatcloselyrelatetoourdefinitionofmedicaldevicesanddiagnostics.Thisdoesnot,however,separatedevelop-mentofmedicaldevicesfromappliedresearchusingmedicaldevicesandtechnologies.

Usingthismethod,itisclearthatalthoughSwedishre-searchershavemaintainedahighlevelofpublicationsoverthepast15years,thepatternissimilartowhatwillbeshownforpatents.Swedishgrowthhasbeenslow,othercountriesarecatchingupandifthetrendcontinues,SwedenislikelytofallbehindEuropeanpeersinthenumberofmedicaltech-nologypublicationspercapita.

Swedishpublicationsrepresent1.2%ofallthemedicaltech-nologypublicationsinMedline.Sweden’sareasofstrengtharecloselylinkedtoitslargestcompanies,asshownbyreviewingpublicationsineachmedicaldevicesegment.Incomparisontotheaverage,Swedishpublicationsondentalandradiotherapysubjectsrepresentalargershareofthetotalpublicationsintheirrespectivefield,whichislikelytobedrivenbyNobelBiocareandElekta.Surprisingly,urologyandrenalmedicinedonotstandout,despitethepresenceofGambro,whichproducesrenalproducts.

23 Noneofthemeasureschosenareperfectgiventhediversenatureofthemedicaldevicefield.Usingexistingdatasources(e.g.,patentdatabasesandMedline)doesnotallowforacomple- telycomprehensiveandexclusiveanalysisofmedicaldevicepatentsandpublicationsasthedatabasesarenotcategorizedwellenough.Despitetheseconstraints,thebeliefisthattheseindi- catorstogethergiveagoodindicationontheinnovativeprojectsandkeyopinionleadersinSweden24Pleasealsoseea)theEuropeanInnovationScoreboard2006–ComparativeanalysisonInnovationPerformanceaccessedviahttp://trendchart.cordis.europa.eu/whichindicatesthat Swedenbelongstothe“Innovationleaders”butitsleadisdecliningb)InnovationIndicatorforGermany2007,DeutscheTelekomStiftungwhichindicatesthatSwedenisthecountry whichthegreatestcapacitytoinnovate

25Medline(MedicalLiteratureAnalysisandRetrievalSystemOnline),accessedviaPubMed,www.ncbi.nlmnih.gov/sites/entrez

26MeSHtermsusedarereviewedintheappendix

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

23

Note: Hits include medical technology development as well as applied medical technology

* Medline articles indexed by selected medical technology MeSH terms (see appendix)

Source: Medline accessed August 200�

Medical technology* publications by country and yearNumber of publications/million inhabitants, 1990–2005

0

50

100

150

200

250

300

1990 1995 2000 2005

Year

Sweden

Denmark

Germany

Netherlands

Switzerland

UK

1.7%

2.2%

4.7%

8.0%

11.2%

7.3%

CAGR1991–2005

Medical technology* publications by country and yearNumber of publications/million inhabitants, 1��0–200�

Note: Index explanation: E.g., index 10� means that in this segment, the country has �% higher share of segment specific articles in Medline (as share of total

segment specific articles in Medline) than the country’s overall share of medical technology articles in Medline

* Medline articles indexed by selected medical technology MeSH terms (see appendix). Include medical technology development as well as applied medical technology

Source: Medline accessed August 200�

Therapeutic areas

High share of publications (index >105)Average share of publications (index 95–105)Low share of publications (index <95)

Denmark

Sweden

Switzerland

Cardio-vascular

Urology andrenal

Netherlands

Radio-therapyOrthopaedics

DrugdeliveryRespiratory Dental

Diagnosticimaging

Surgicalinstruments

Nobel Biocare ElektaGambro

Philips

Novo Nordisk

Ireland

Korea

Synthes Straumann,Nobel Biocare

Dentium(bone implants)

Listem, Huvitz,Prosonic, DR Tech

Strength of research areas and correlation with local industryNumber of publications from national scientists/Total number of publications in the country, 200� Index, country share of all medical technology articles in Medline* = 100

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

2�

On patents,SwedenrankedsecondinEuropeintheearly90’s,basedonthenumberofmedicaltechnologypatentspercapita,closelybehindSwitzerland,butclearlyaheadofpeercountriessuchasDenmark,GermanyandtheNetherlands.Throughoutthe1990’sseveralofthesecountrieshaveincreasedtheirnumberofmedicaltechnologypatentsbymorethan10%annually,whileSwedishgrowthhasbeensignificantlylower,6.4%27.Today,SwedenisonthesamelevelasitsEuropeanpeers,andifthecurrenttrendcontinuesSwedenwillsoonseeitselffallingbehind28.

AbreakdownofthefiledpatentsbytypeofassigneeshowsthatinSweden,privateindividualsaccountforahigherpro-portionofthepatents(14%)thantheydoinpeercountries.Thebreakdownalsoshowsthatthisnumberhasdeclinedoverthepastsevenyears.However,thegreatestshareofpatentscomesfromcompanies,manyofthemactiveinthemedicaldeviceindustry2930.

27EuropeanPatentOffice,www.epo.org;WorldIntellectualPropertyOrganization,www.wipo.int

28Thisanalysisisbasedonaselectionofclasses(e.g.,A61B,A61C,A61D,A61F,A61G,A61H,A61J,A61L,A61M,H01J,H05G)intheInternationalPatentClassification(IPC)system thatmatchesourdefinitionofmedicaldevicesanddiagnostics.However,astheIPCclassesarenotdefinedtoseparatemedicaldevices,therearesomepatentsincludedthatarenot devices(e.g.absorbentpads)andsomethatareexcludedastheyarecategorizedundervariousotherIPCclasses(e.g.hearingaidsclassifyasloudspeakers)

29ReviewofallpatentsfiledtoWIPOinIPCclassesA61B,A61C,A61D,A61F,A61G,A61H,A61J,A61L,A61M,H01J,H05G,indexedbynationalityinDelphionPatentdatabase, www.delphion.com

30InSweden,roughly45%ofthepatentsfromotherindustriescomefromSCAHygieneProducts,astheIPCsystemunfortunatelydoesnotallowseparationofwoundcareproductsfrom absorptivehygieneproducts(diapers,femininehygieneproducts).IfexcludingSCAfromtheanalyses,privateindividuals’shareofpatentswouldbeevenhigherthan14%

* International Patent Classification (IPC) subclasses A�1B, A�1C, A�1D, A�1F, A�1G, A�1H, A�1J, A�1L, A�1M, A�1N, H01J, H0�G

Source: World Intellectual Property Organization; European Patent Office

0

10

20

30

40

50

60

70

80

90

100

110

120

130

Germany

Denmark

UK

Netherlands

US

Sweden

Switzerland

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

CAGR1991– 2006

14.4%

12.1%

6.4%

10.9%

9.0%

7.2%

12.6%

Medical technology patents by country and year Number of patents filed to the European Patent Office and to the World Intellectual Property Organization in medical technology* per million inhabitants, 1��� –200�

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

2�

a International Patent Classification (IPC) subclasses A�1B, A�1C, A�1D, A�1F, A�1G, A�1H, A�1J, A�1L, A�1M, A�1N, H01J, H0�G

b Sample includes, for example, SCA Hygiene Products and pharmaceutical companies

c ��% taken by Philips Electronics

d ��% taken by Novo Nordisk and Coloplast. Hearing aids however not included, as their IPC classification is loudspeakers etc.

Source: Delphion; Corporate web sites; Interviews

416

Israel

Other

International company,medtech

National company,medtech

Technology transfercompany

University/research institution

Private individuals

100% = 524276 560

NetherlandsSwitzerland

211

DenmarkSweden

Share of patents filed to World Intellectual Property Organization in medical technologya by assignee type, 2006

Percent

INDICATIVE

48

31 41

20

44

18

6

113

14

1

4

21

43b

13

9

4

79c

63

71d

34

4

8

Private individuals’ share of patents in Sweden compared to peer countries

* International Patent Classification (IPC) subclasses A�1B, A�1C, A�1D, A�1F, A�1G, A�1H, A�1J, A�1L, A�1M, A�1N, H01J, H0�G

** Sample includes, for example, SCA Hygiene Products and pharmaceutical companies

*** Companies in other industries include companies like Ericsson, SKF, AGA etc. Companies closely related to medical devices include biotech,

safety equipment, dental/orthopedic technicians etc.

Source: Delphion; Corporate web sites; Interviews

Share of Swedish medical technology patents* filed to World Intellectual Property Organization by assignee type and yearPercent

36 3731

127

11

3441 43

16

1

14

280

2003

276

2006

International company,medtech

Other**

Technology transfercompany

National company,medtech

100% =

Private individuals

0

17

0

2000

241Increased number of medical technology patents from contract manufacturers, companies in other industries, and companies closely related to medical devices***

Increase in patents from Elekta, Getinge, Mölnlycke, Gambro and Astra Tech, decline in patents from Nobel Biocare and small Swedish medtech companies

6.4%

20.1%

CAGR (numberof patents) Driver

2.3%

-0.2%

-1.2%

0.0%

INDICATIVE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

2�

Dynamics of small and medium sized companiesThereare310smallandmid-sizedmedicaldeviceanddiagnosticcompaniesinSwedentoday(revenues<2000MSEK),butitappearsasfew,ifany,havethepotentialtogrowintolarge,globalplayers.

TobetterunderstandthesecondtieroftheSwedishmedicaldeviceindustry,areviewwasconductedofthemedicaltech-nologypatentsthatwerefiledbyprivateindividualsin2000,andoftheperformanceofasampleofexistingsmall/mid-sizedcompanies.

Thereviewof17ofthe42patentsregisteredbySwedishprivateindividualstotheWorldIntellectualPropertyOrganizationin2000showsthattenofthesepatentshavebecomecommercializedinsomeway.Threeofthemhaveresultedincompaniesbeingstarted,threeareincorporatedinexistingcompaniesandfourhavebeensold.Theresthavenotbeencommercializedinanyway.

Ananalysisoftheexisting310smallandmidsizedcom-paniesrevealsthatmost(208)areverysmall(revenueslessthanSEK10million31).AmongthecompanieswithrevenuesbetweenSEK10and2000million,growthhasaveraged15%peryearoverthepast8yearsandtheaverageEBITin2006was6%32.

31 Revenuedataismissingfor37ofthe208companies.AssumptionmadeinthiseffortisthatthesecompaniesaresmallwithrevenueslessthanSEK10million

32ReviewofmedicaldeviceanddiagnosticcompaniesinSwedenbasedondatafromStatisticsSweden,Odin,SwedishCompaniesRegistrationOffice,VINNOVA,SwedishMedtechand interviews.RevenuedatafromannualreportsorOdin

Note: Patents were randomly selected from total group of privately filed patents

* IPC classes A�1B, A�1C, A�1D, A�1F, A�1G, A�1H, A�1J, A�1L, A�1M, A�1N, H01J, H0�G

** Contact details to patent holders not found

Source: Delphion; Patent holder interviews

Frequency of commercialization

3

3

3110

717

Medicaltech-nologypatents2000 fromselectedand foundpatent holders

Notcommer-cialized

Commer-cialized

Sold,not usedtoday

Sold,likelyusedtoday

Incorp-orated in existingcompany

Base fornewstart-up

17%

Selected forinvestigation –patentholders found40%

Selected forinvestigation –patent holdersnot found**

Not selectedfor investigation

Medical technology* patents in WIPOfrom private Swedish inventors, 2000100% = 42 patents

Number of patents

3 companies active today based on patent taken in 2000, all on a small scale

INDICATIVE

(%)= percent of total

(59%)

(18%)

43%

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

2�

Despitethisgrowth,manycompanies33findexpansiondif-ficult,astheyarelackingcommercializationcapabilities(e.g.,reinbursementmanagement)andarefocusedonmarginalinnovationsinsmallorslowgrowingsegmentsofthedeviceindustry(e.g.,makingapatientbedthatisslightlybetter).Yetrevolutionaryinnovationsarepossibleineventheslo-wergrowingsegments(e.g.,the“WoundVacuum-AssistedClosure,V.A.C.,system,”34byKineticConcepts,Inc.impro-vedthelivesofmanypatientswithpreviouslylargewoundsthatwouldnotheal).ExamplesofmedicaldevicesegmentswheresmallandmidsizedSwedishcompaniesarepresentincludethefollowing

Patient aids(25%ofaggregatedsalesofSwedishsmallandmidsizedcompanies,39Swedishcompanies)containalargenumberofslowergrowthcompanies.Modestgrowthisexpected(3.6%CAGR2004-2010)particularlywithintheadvancedpersonalmobilitysector,wherePermobilisthelar-gestcompany.

In vitro diagnostics(17%ofaggregatedsalesofSwedishsmallandmidsizedcompanies,20Swedishcompanies)containsthe7thlargestSwedishmedicaldevicecompany,Phadia,drivingthesizeofthesegment,andanumberofverysmall

companies,mostofwhichhavebeenstartedoverthepastthreeyears.Thesecompaniesfocusontraditionalinvitrotesting,point-of-caretestingandadvancedmoleculardiag-nostics,allofwhicharestronggrowthsegments.

Diagnostic imaging(10%ofaggregatedsalesofSwedishsmallandmidsizedcompanies,30Swedishcompanies)iswheremostofthenewadvancedtechnologiesarelocated;however,thesecompaniesarestillverysmallandmostarefocusedontheX-raysegment,whichhasthelowestprojectedfuturegrowthwithintheimagingsegment.

Dental(10%ofaggregatedsalesofSwedishsmallandmid-sizedcompanies,29Swedishcompanies)hasthemostsigni-ficantgrowthopportunitiesintheimplantssegment,wherethereisastrongtraditionthroughNobelBiocare.However,successinthissegmentmightbechallengingasmostplayersareactiveinveryfragmented,slowergrowthsegments.

Cardiovascular(8%ofaggregatedsalesofSwedishsmallandmidsizedcompanies,16Swedishcompanies),especiallythetrans-cathetersegment,hasahighpotentialforgrowthbutthereisahighdegreeofcompetitionwithinthissegmentfromdevicecompaniesheadquarteredinothercountries.

* Companies in this revenue segment represent approxemately 30% of all small and midsized medical device and diagnostics companies in Sweden

** Based on �� of 102 companies in revenue segment (lack of data for 2� companies). �0 companies with data from 1���–200�; four companies with data

from 1���–200�, two companies with data from 2000–200�

*** See appendix for explanation

Source: Odin

Performance of Swedish medical device and diagnostic companies with 2006 revenues in the range of SEK 10–2,000 million*Revenue**

5,313

4,7854,4564,438

4,018

3,436

2,7352,376

1999 2000 2001 2002 2003 2004 2005 2006

Aggregated revenuesSEK million

Average EBIT***percent of revenues -29% -16% -13% -1% 4% 7% 7% 6%

14.6% averageCAGR

3333companieswerecalledandinterviewedregardinge.g.,thefocusoftheirproductdevelopmentandpercievedmajorchallenges

34WoundV.A.C.isalowtechnologydevicemadeofasponge,plasticsheetandvacuumdevicethatrevolutionizedthetreatmentoflargechronicwounds.KineticConceptsInc., www.kcil.com

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

3546%arefoundedbyengineersorinnovatorsnotaffiliatedtoacademiaand25%byphysicians.Approximatelyone-fifthofthesecompanieshavelaunchedtheirproductsinternationally, halfofthemwerelaunchedinSwedenandarereadytomovebeyondthenationalmarket,andonequarterwereintheprocessoflaunchandscaleupdomestically.Theremainingcompanies werestillintheprocessofclinicaltestingandproductdevelopment.

36Me-tooproducts;productswithverysimilarformandfunctiontoexistingproducts,competingwithminimaldifferentiation

37TolearnmoreaboutlargeSwedishcompanies(revenues>SEK2billion)forGambrovisit:www.gambro.com,Getingevisit:www.getinge.com,NobelBiocarevisit:www.nobelbiocare.com, Elektavisit:www.elekta.com,MölnlyckeHealthCarevisit:www.molnlycke.com,AstraTechvisit:www.astratech.com

Note: Only includes top eight segments (that together represent ��% of aggregated revenues and ��% of number of Swedish small and midsized companies).

Financials from latest available year (200�–200�)

Source: Health Research International; Odin

Aggregated revenues and number of Swedish small and midsized companies by segment, mapped versus global market size and growth

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

Patientaids

In vitrodiagnostics

Diagnosticimaging

Dental

Cardiovascularmanagement

Surgical tables,instrumentsfixed systems

Orthopedicsand spine

Surgicalinstruments

Aggregated revenues in segment, Swedish small and midsized companies

0 1 10 11 122 3 4 5 6 7 8 9

Expected growth, globalCAGR (2004–2010)

Percent

Segment size, globalUSD billions; 2004

(30)

(20)

(16)

(29)

(12)

(39)

(22)

(30)

( ) Number of Swedish smalland midsized companies

Onamoregranularlevel,managementinterviewswith33randomlyselectedcompanies35revealthatonly16%ofthecompaniesarecompetingwithuniqueproductsinalargeorgrowingmarket,whiletheothersareeitherfocusingonlowgrowthmarkets,orworkingwithgenericorme-tootypeproducts36.

Giventhesecircumstances,itisnotsurprisingthatfewsmallcompaniesmanagetogrowanddevelopintopromisinglargerinternationalcompanies.

Leverage of large companiesLarge37companiesarecrucialtothecontinuinggrowthanddevelopmentoftheindustry.Inmostsuccessfulinternationalcases,thesecompaniesactas“engines”forthelocalinnova-tionclusters(moreonthisinthenextchapter).InSweden,companieslikeGambroandElektahaveplayedthisroletosomeextentinthepast.ThequestioniswhetherSwedenisfullyleveragingtheseleadingcompanies.Therearesignsthat

wouldsuggestthisisnotthecase.ManyoftheinterviewswithseniormanagementofthesecompaniesrevealedthatSwedenisoftennotviewedasapriorityforresearchcol-laborationsandclinicaltesting.Thereareweaktiesbetweenthesecompanies,academicinstitutionsandhospitals–andsuchtiesarecriticaltoensuringawellfunctioninginnova-tioncluster.Anecdotally,Swedenmayalsobelosingsomeofitshistoricdistinctivenessasaplacetobasemedicaldeviceresearchanddevelopment–perhapsillustratedbySiemens’recentdecisiontoleavethecountry.

Itisalsocriticalforlargecompaniestoactasvehiclesforcommercializationofideasgeneratedbysmallercompaniesorbyindividuals.Itisverydifficulttogrowalargecompanyfromscratch,andgrowinganewbusinessareaaspartofanestablishedglobalcompanyisoftenamorefeasibleroute.Forexample,Medtronic’ssuccessinaddingnewareasofbusi-nesshashadahugeimpactonthelocalinnovationclusters.

2�

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

2�

38http://bostonscientific.mediaroom.com/index.php?s=43&item=691”BostonScientificacquiredtheCardiacSurgerybusinessinApril2006aspartoftheGuidanttransaction.TheCardiac Surgerybusinessisaleadingdeveloperofmedicaltechnologiesdesignedforuseinsurgicalcardiacprocedures,includingbeating-heartbypasssurgerysystemsandendoscopicvesselhar vestingforcoronarybypasssurgery.Thebusinessemploysapproximately450people.BostonScientificacquiredtheVascularSurgerybusinessin1995.TheVascularSurgerybusinessdevelops syntheticgraftsandpatchesusedtosurgicallytreatvasculardisease,includingtherepairofabdominalaorticaneurysmsandperipheralvascularanatomy.Thebusinesshasapproximately 250employees.Thecombinedrevenuesofthetwobusinessesin2006wereapproximately$275million.”

Thisprocessisalsoimportanttoensureacontinuousupgra-dingoftheportfolioofproductsandbusinessareas,suchthatthelargecompaniespreservethepotentialforfastgrowthandhighmargins.

AlookatSwedensuggestslimitedsuccessinthisarea.Somecompanieshaveriddensuccessfuls-curves(i.e.,beenabletogrowbytheextensionofbusinessintonon-coreareas)andthushavebeenabletoaddnew,vibrantbusinessareaswhileothershavenot.ArecentexampleofsuccessisGetinge,whichhasacardiacperfusionbusiness,andwhichrecentlyacquiredBostonScientific’scardiacandvascularsurgerydivi-sions38.ThetopsixSwedishmedicaldevicecompaniesarerepresentedinninedifferentmedicaldevicesegments

(bytechnologyarea).ExceptforGetinge’sparticipationinthelargeandhigh-growthcardiovascularsegmentandElekta’sparticipationinthehigh-growthenergybasedtechnologiessegment,noneofthesesegmentsarerepresen-tingeitherthehighestgrowthorlargestmarketsegments.LeadingSwedishcompaniesare,intheaggregate,notamongthehighestspendersonresearchanddevelopment.

ThereisariskofthatcontrolandownershipofcompaniesarebecominglessSwedishasacoupleofSweden’slargestcompaniesarecurrentlyprivateequityownedandonehasstronglinkstoSwitzerland.

Note: Based on top six companies: Gambro, Getinge, Nobel Biocare, Mölnlycke Health Care, Elekta and AstraTech. Assuming �0% of AstraTech’s revenues are

in urology & renal segment and 30% are in dental segment

* Gambro revenues from 200�

Source: Health Research International; Annual reports; Odin

Presence of top six Swedish companies

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

Diagnostic Imaging

Orthopedics & Spine

Surgical instrumentsDrug delivery Endoscopy

Home respiratory

NeuromodulationOpthalmic surgery

Patient aids

Segments where top six Swedishcompanies are present.Size of circle represent aggregatedrevenues 2006*

0 1 10

Energy-basedtechnologies

12 13 14 15 16 17 18 192 3

Urology andrenal

Surgical tables,lights &fixed systems

Dental

Infectioncontrol

Surgicaldressings,drapes

Woundcare

Critical careproducts

Cardiovascularmanagement

In Vitro diagnostics

Segment size, globalUSD billions; 2004

115 6 7 8 9

Expected growth, globalCAGR (2004–2010)

Percent

4

Segments where top six Swedish

companies are not present

ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

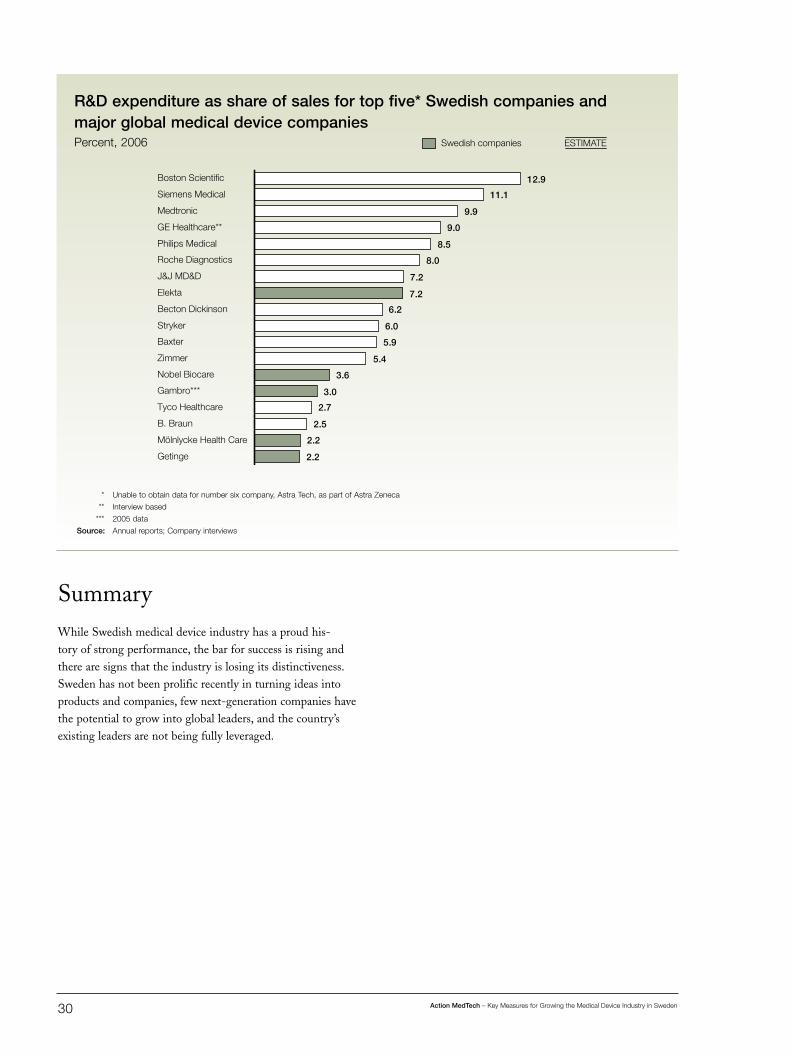

SummaryWhileSwedishmedicaldeviceindustryhasaproudhis-toryofstrongperformance,thebarforsuccessisrisingandtherearesignsthattheindustryislosingitsdistinctiveness.Swedenhasnotbeenprolificrecentlyinturningideasintoproductsandcompanies,fewnext-generationcompanieshavethepotentialtogrowintogloballeaders,andthecountry’sexistingleadersarenotbeingfullyleveraged.

30

* Unable to obtain data for number six company, Astra Tech, as part of Astra Zeneca

** Interview based

*** 200� data

Source: Annual reports; Company interviews

R&D expenditure as share of sales for top five* Swedish companies and major global medical device companiesPercent, 200�

2.2

2.2

2.5

2.7

3.0

3.6

5.4

5.9

6.0

6.2

7.2

7.2

8.0

8.5

9.0

9.9

11.1

12.9

GE Healthcare**

Nobel Biocare

Zimmer

Mölnlycke Health Care

Getinge

Baxter

Stryker

Becton Dickinson

Elekta

J&J MD&D

Roche Diagnostics

Philips Medical

Medtronic

Siemens Medical

Boston Scientific

Gambro***

B. Braun

Tyco Healthcare

Swedish companies ESTIMATE

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

31

Building a successful medical device indus-try requires purposeful collaboration between several stakeholders

�In order to understand how a well functioning medical device cluster comes about and functions, a number of international case examples have been studied (in addition to the workshops and interviews described in Chapter 2) where a strong innovation environment and a flourishing medical device industry exist.

Eachcaseisuniqueandprovidesvaluableinsights

• SouthKoreahasdevelopedastrongpositionintheima- gingsegmentbasedontechnologyskillsdevelopedinthe country’sotherindustries• Denmarkhasalonghistoryinhearingaidsbasedon governmentinterventionand,morerecently,joint collaboration• SanFranciscohasbuiltavibrantbiotechnology/medical deviceclusterandleveragedthestrengthsoftheexisting semi-conductorindustry• Minneapolishasbuiltaworld-leadingmedicaldevice clusterleveragingthelocalpresenceofmajormedi- caldevicecompaniessuchasMedtronic,Guidant (BostonScientific)andStJude• Irelandhasattractedmedicaldevicemanufacturingand R&Dthroughamajorgovernmentledeffortincluding taxbreaksandstrongfocusonnetworkbuilding

Acrosstheseexamples,thereisnosinglerecipeforsuccess,butratheranumberofdifferentmodelsthatcanleadtosuc-cess.Commontoallofthemseemstobestrongfocus,highdegreeofcollaborationanddedicationfromthestakeholdersdrivingtheeffort.Inaddition,giventhecross-diciplinaryessenceofappliedmedicaltechnology,thestakeholdersneedtorepresentdifferentinstitutions(hospital,universities,andcompanies)aswellasdifferentdepartmentswithintheseinstitutions.Thebestpracticeexamplesthathavebeenre-viewed,andtheinterviewsconductedwithindustryexpertsandstakeholdersinSweden,suggestthattherearefourcri-ticalelementsor“enablers”contributingtoeachsuccessfulstory:strongandwellalignedincentives,worldclasscapabi-lities,activeandwellconnectednetworks,aswellasadequatefundingforresearchandearlycommercialization.

Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

• Formal evaluation of publications/patents• IP ownership by professor and/or university• Culture of positive recognition for commercial activities

• Formal evaluation of clinical research and patents• Culture of positive recognition for commercial activities (incl. clinical trials)• IP ownership

• Tax breaks and cost efficient labor• Strong local research capabilities• Strong local market• Governmental support of 1st time R&D investments

• Strong academic talent within focused field• Cross-disciplinary capabilities with experience in finding techni- cal solutions to unmet customer needs• Educational programs• Commercialization skills

• Clinical testing and commercialization skills• Process for identification and articulation of unmet clinical needs• Health economics skills

• Core commercialization skills - Sales and marketing - Regulatory - Reimbursement• Business development skills• Internal R&D skills• Innovation sourcing skills

• Targeted research funding for selected medical technology segments, both internal and external (i.e., public institutions and private foundations)

• Targeted funding for applied medi- cal technology research and product development

• Sufficient funding for R&D• Contribution to funding of joint collaboration projects

• Encouragement of start ups through use of technology transfer office and incubators• Portal towards industry and hospitals

• Creation (and marketing) of primary point of contact for aca- demics, companies and individual inventors (e.g., portal to increase collaboration)

• Active contribution to innovation clusters• Participation in job rotations and fellowships between universities and industry

Universities University hospitals Companies Facilitators

Ince

ntiv

es

Cap

abili

ties

Dire

ct f

und

ing

Co

llab

ora

tion

an

d n

etw

ork

Go

vern

men

t

Net

wo

rk o

rgan

izat

ion

Inve

sto

rs

Focus & Collaboration!

Source: Interviews with international and Swedish medical device industry representatives

Example of enablers needed

IncentivesTheinternationalcaseexamplesstudiedrevealthatinordertocreateastrongandvibrantmedicaldevicecluster,anum-berofstakeholders(individualresearchers,physicians,acade-micinstitutions,hospitals/providers,andcommercialcompa-nies)needbeincentivizedtocontributewiththeirknowledgeandexpertise.

UniversitiesAcademicsinmedicineandtechnologyshouldbemotivatednotonlytoperformhighquality,innovativeresearchthataimstosolvechallengesfacingthehealthcareenvironmentbutalsotocommercializeideassotheywillbesharedandotherscanbenefitfromthem.Thiscanbeachievedinseveralways.

Formal evaluation of publications and patents.Oneoptionistoensurethatinnovationandqualityarepartoftheformalevaluationofscientificresearchers.InSouthKorea(box1),researchintomedicaldeviceswasincentivizedbygivingmoreattentiontopublicationininternationallyrecognizedjournalsaspartoftheevaluationcriteriaofresearchers.ThisinitiativehasledtoadramaticincreaseinthenumberofmedicaltechnologyarticlesinMedline,asprofessorsstrivetoachievebetterevaluations(and,indirectly,moreresearchfunding).InSweden,wherethisincentiveisdeeplyrootedinthescienti-ficsociety,thesameincentivemayhavetheoppositeeffect,drivingresearcherstowardsbasicratherthanappliedresearch,sincebasicresearchismorelikelytobepublishedinhighstatusjournals.

32 Action MedTech – Key Measures for Growing the Medical Device Industry in Sweden

33

Expertinterviewsemphasizethatitwouldbebeneficialifpatentactivitywasalsopartoftheformalevaluationofresearchers,eventhoughthishasnotbeenthecaseintheinternationalcaseexamplesstudied.

Intellectual property ownership.Incentivizingcommerciali-zationcanbeachievedusingseveraldifferentmodels.InSweden,theteacher’sexemption39givesresearchersandscientistsatacademicinstitutionsapersonalincentivetocommercializefindings,sincetheyown100%oftheintel-lectualproperty.ThiscanbecontrastedwiththeUSwhereuniversitiesgenerallyhavethefullownershipoftheintel-lectualpropertydevelopedbyemployedresearchers,whilenetincomeisoftenshared.Forexample,StanfordUniversityowns100%ofanypatentfiledandanypotentialroyaltiesaresharedequallybetweentheinventor,theinventor’sdepart-

mentandtheuniversity.ThesameprincipleisappliedattheUniversityofCalifornia.AtNorthwesternUniversityinChicagoadifferentmodelforsharingroyalty/licensingfeeshasbeendeveloped:30%ofthenetincomegoestotheinventor,20%toauniversityaccounttosupporttheinventor’sfurtherresearch(shouldtheinventorleavetheuni-versity,thisamountremainswiththeuniversity),10%tothedepartmentordepartmentsinwhichtheinventorserves,5%totheschoolorcenterinwhichtheinventorservesand35%tothecentraladministration.

Culture of positive recognition for commercial activities.Inmanycountries,suchastheUS,thereareculturalincentivestocommercializeinnovation,assuccessfulcommercializationgiveshighstatusinthesurroundingresearchcommunityandcanleadtoasignificantaccumulationofwealth.

* Medline articles indexed by selected medical technology MeSH-terms (see appendix). Hits include medical technology development as well as applied

medical technology

Source: Interviews; Press clippings; Ministry of Science and Technology; Korea Health Industry Development Institute; Medline accessed August-September 200�;

Delphion

Box 1: South Korea

In South Korea, a major government effort known as the G-� Highly Advanced Nation program was introduced in the early 1��0’s aiming to bring the level of Korean science and techno-logy to the level of the G-� countries. Total investment of USD 1�0 million (1���–2001) was made. Medical technology was one of the selected investment areas, with a focus on imaging technologies. The result has been a virtual explosion of the medical device industry, particularly in diagnostic imaging, where publications, patents, number of companies and sales have all grown in excess of 1�% annually

Share of Medline articles in medical technology* with Korean affiliation, 1990–2005Percent