14

Actuarial Services in Microinsurance: Joint IAA-IAIS Project Nigel Bowman, IAA, and Jules Gribble, IAIS IAA President’s Forum, Cape Town 21 November 2016

Actuarial Services in Microinsurance:

Joint IAA-IAIS Project

Nigel Bowman, IAA, and Jules Gribble, IAIS

IAA President’s Forum, Cape Town

21 November 2016

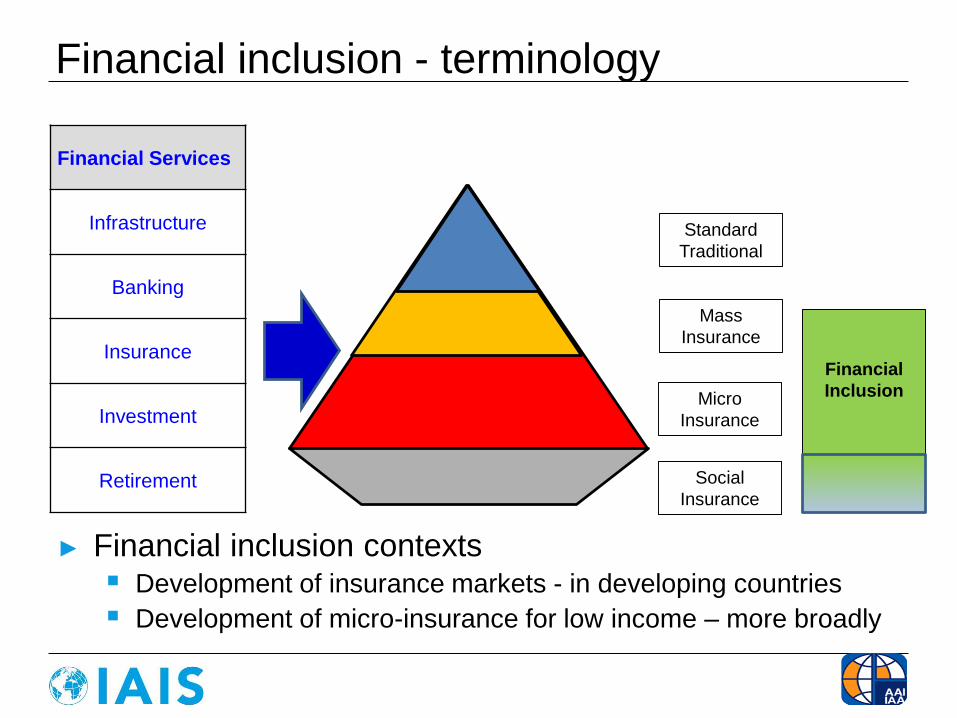

Financial Services

Infrastructure

Banking

Insurance

Investment

Retirement

Financial

Inclusion

Standard

Traditional

Mass

Insurance

Micro

Insurance

Social

Insurance

Financial inclusion - terminology

► Financial inclusion contexts Development of insurance markets - in developing countries

Development of micro-insurance for low income – more broadly

Prior IAA IRC material

► Develop an International Actuarial Guidance Note on Microinsurance

► Include microinsurance in existing IAA education and awareness initiatives and develop a medium term strategy for training

► Expand actuarial education efforts in microinsuranceto include non-actuaries, particularly in countries where local actuarial associations do not exist

► Provide additional application guidance to national insurance regulators with respect to proportionate actuarial services in inclusive insurance markets

Some key recommendations from “Issues Paper: Addressing the Gap in Actuarial Services in Inclusive Insurance Markets” IAA Task Force on Microinsurance, February 2014

3

Objective

The IAIS, in cooperation with the IAA, will identify

and develop approaches to establish and apply

actuarial expertise in inclusive insurance markets

based on an understanding of a proportionate

application of prudential requirements in inclusive

insurance markets.

4

Deliverables

► IAA Paper: “Approaches to Actuarial Services in Inclusive Insurance Markets” Focus on actuarial matters

► IAIS Application Paper: “Proportionate Prudential Requirements in Inclusive Insurance Markets” Focus on supervisory matters

► Both scheduled for the Consultation later in 2017 and finalisation by the end for 2017

5

Context

► Three key players Actuarial profession

Product providers

Supervisors

► Progress limited by the least capacity Need to progress together and co-operatively

► A key outcome will be to provide a common ‘language’ to facilitate discussion and improve understanding between and within these key players

6

Criteria for success

► Short term Actuarial contributions in the financially inclusive

context are accepted as being valid and are adopted by all the key players

► Longer term Actuarial contributions seen to contribute to better

outcomes of financial inclusion services by all the key players

► Challenges: Address ‘proportionality’ in meaningful way

Flexibility to cater for changing environments

Recognise key differences between inclusive and traditional insurance

7

Actuarial guiding principles

► Barriers: Not intentionally create them for Financially

Inclusive Insurance, and permit innovation

► Simplicity: Of use of outcomes for end users (not the

same as of underlying process

► Differences: Manage key differences (risks and needs)

between FII and Conventional insurance

► Assessments: Objective and quantifiable to give language

to start conversations (recognising need for professional

judgement

► Interactions: Parallel development of the three key players

► Sustainability: Long term in local environment

► Consumers: Solution support their needs and protect their

interests

8

Actuarial skill levels needed► Need to recognise realities

Very few qualified actuaries in many countries

Development of insurance products is taking place regardless of this

► Some preliminary thoughts for discussion:

9

Low Qualified actuarial technician

Low-Med Qualified actuarial technician

+ Initial Review by Fully Qualified Actuary

Medium Qualified actuarial technician

+ Periodic Review by Fully Qualified Actuary

High Qualified Actuary

Expert Qualified Actuary

+ Topic Experienced

Approach

► Develop a ‘scorecard’ approach, which takes into account criteria to assess: Riskiness of proposed product designs

Capacity of a provider to deliver the product

Readiness of the (financial inclusive) insurance market

Supervisory capacity

► This will provided a process and ‘language’ to support discussions starting and then outcomes emerging using professional judgement

10

Business risk assessment (indicative)

11

Colours:

► Focus of IAA paper

► The outcome is input to Supervisory risk assessment

► Need for actuarial skills increases as outcome assessments move from Low to

High risk

Residual risks of product

Low xx Medium xx High

Insurer

capacity

Low

xx

Medium

xx

High

Low outcome (residual) risk High outcome (residual) risk

Some key challenges

► What are, and who may provide, ‘Actuarial

services’

And who ensures criteria are met

► How to:

Enhance the value, role and reputation of actuarial

services amongst users

Develop and retain actuarial skills and expertise to

deliver (various) actuarial services

Support supervisors carry out their actuarial (and risk

management) responsibilities effectively

12

Moving forward

► These are challenging issues

► In theory and in practice ‘on the ground’

► New concepts to apply in evolving and non-

traditional environments

► The glass is half full!

13

Thank you …

Actuarial Services in Microinsurance:

Joint IAA-IAIS Project

Nigel Bowman

Jules Gribble

14