43

Actuaries and banking: Where can actuarial skills be applied? Simple model of banks Exploring core banking risks

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | gabriel-blankenship |

| View: | 219 times |

| Download: | 0 times |

Actuaries and banking:

Where can actuarial skills be applied?

Simple model of banks

Exploring core banking risks

• Qualified at Scottish Life:

• Pricing roles across offshore bonds, pensions and investments

• Have family exposure to Lloyds Reinsurance market

• Range of roles at bank

• Group Strategy under another actuary

• Developed NPV Pricing models for retail finance

• Roped into technical help for regulatory investigations

• Built new customer value models

• Developed new pricing team – recently delivered pricing promises

My experience

There is no open door for actuaries to get involved:

• Banks already have developed specialist risk departments:

• Credit risk

• Fraud risk

• Bank capital management

• Liquidity risks

• Market risk

• There are no reserved roles

• Finance and accountants manage many trade offs

• They already have core statutory roles

Banks already have experts in place

Actuarial training is unique as it crosses siloes:

• Credit risk is analgous to underwriting

• Provisioning is analgous to reserving

• Bank capital management is like solvency

• Liquidity risks can be understood through:

• behavioural assumptions,

• yield curve and duration matching / reinvestment risks

• Market risk is a given from asset models

• Understand Accounting

• Understand Economists

But breadth of actuarial skills still unique

Automatically want to trade off risk and reward:

• Able to develop NPV pricing models

• Able to build Customer Value models cross siloes

• “Seen as a “neutral adviser” on pricing

• Can pick up random problems

Automatically look through time

• 5 year plus horizon rather than 1 year margin

Consider risk or ruin

• Philosophy like older bankers – first job is to protect savers, then think of maximising profits

As are actuaries’ ways of thinking

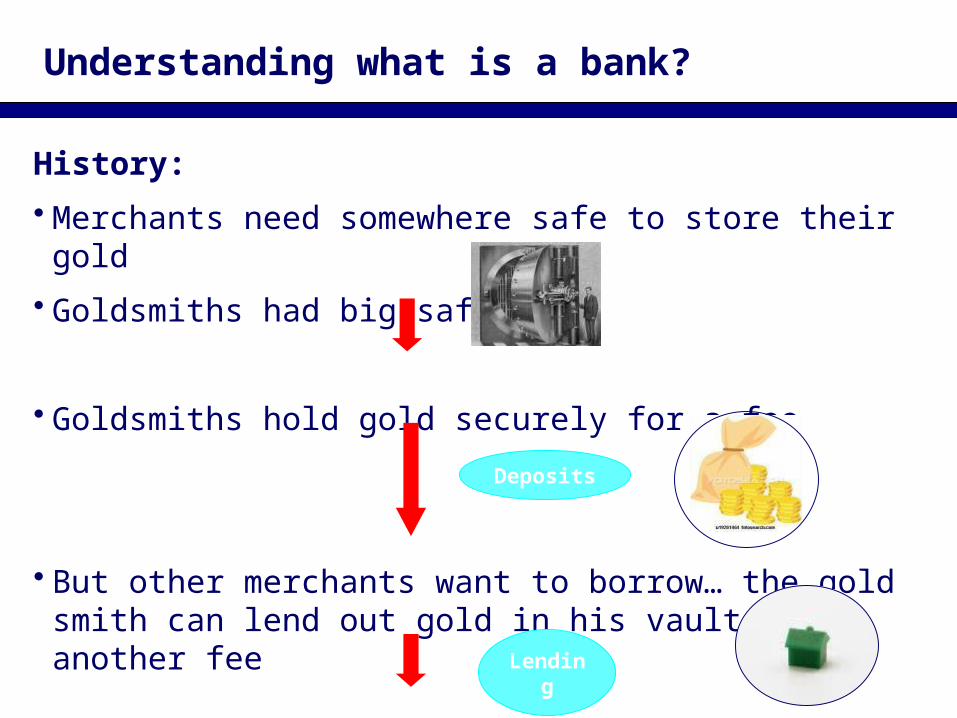

History:

• Merchants need somewhere safe to store their gold

• Goldsmiths had big safes

• Goldsmiths hold gold securely for a fee

• But other merchants want to borrow… the gold smith can lend out gold in his vault for another fee

Understanding what is a bank?

Deposits

Lending

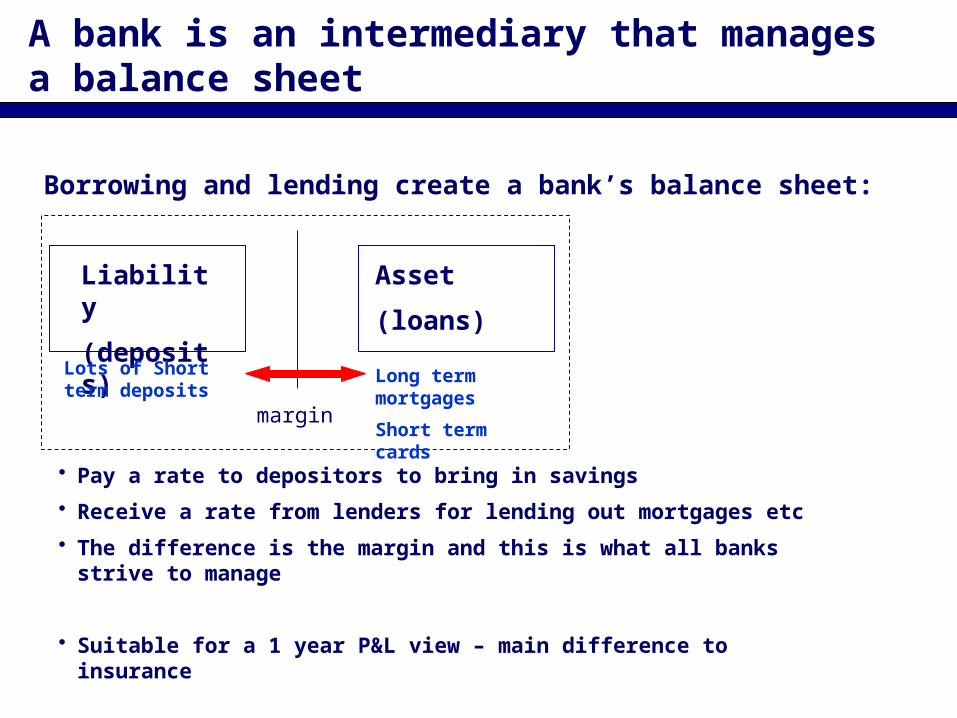

A bank is an intermediary that manages a balance sheet

Liability

(deposits)

margin

Asset

(loans)

• Pay a rate to depositors to bring in savings

• Receive a rate from lenders for lending out mortgages etc

• The difference is the margin and this is what all banks strive to manage

• Suitable for a 1 year P&L view – main difference to insurance

Borrowing and lending create a bank’s balance sheet:

Lots of Short term deposits

Long term mortgages

Short term cards

History shows risks:

• Credit risk: – loan not repaid

• Liquidity risk: – depositors all want their money back at the same time ... But its been lent out

This creates two key risks a bank must manage

“I’d like to make a withdrawal”

Credit risk:Expected and unexpected losses

• We allow for expected losses when setting lending rates and fees … but losses will vary over time

• Peak losses don’t occur every year, but when they do, they can be large

Figure 1

Time

Lo

ss r

ate

Expected loss (EL)

Unexpected loss (UL) Need a buffer in case of unexpected losses

Day to day business - price and make decisions on expected losses

Credit score cards are developed to manage expected losses

•Score cards bring in a lot of customer data •Score cards built by looking at the correlation of this data against historic loss•Score cards use this past behaviour to rank customers in order of risk•Very similar to underwriting•Track with similar techniques – rainbow curves versus chain ladder

Risk score

Pro

bab

ility

of

def

ault

•Like insurance banks make money by taking risk •The more accurately risk and expected loss can be predicted the easier it is to

manage

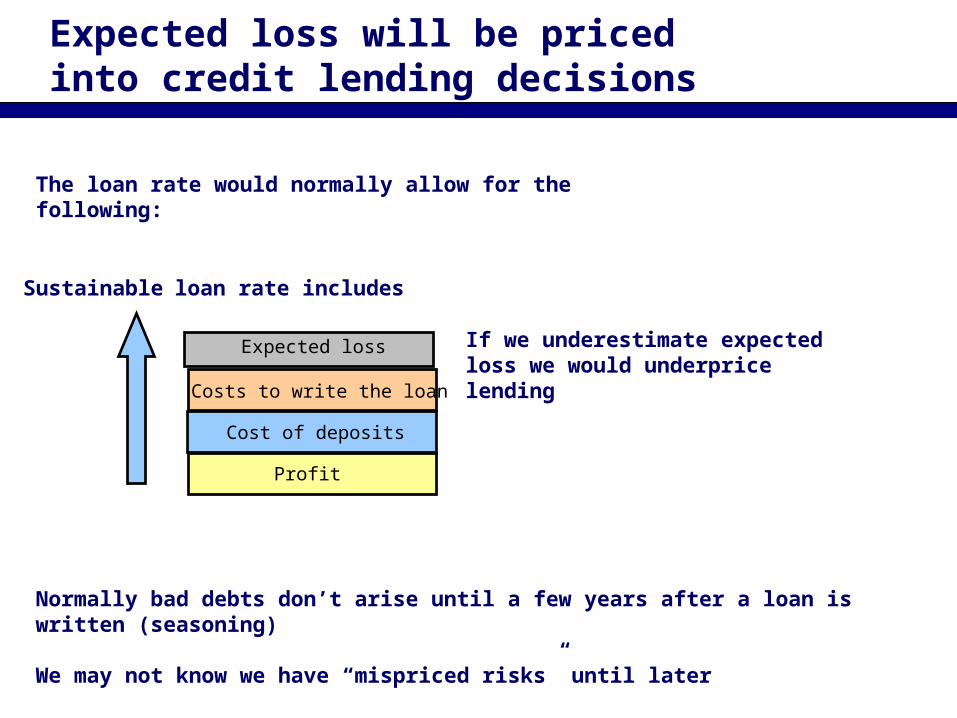

Expected loss will be priced into credit lending decisions

The loan rate would normally allow for the following:

Expected loss

Costs to write the loan

Cost of deposits

Profit

Sustainable loan rate includes

If we underestimate expected loss we would underprice lending

Normally bad debts don’t arise until a few years after a loan is written (seasoning)

We may not know we have “mispriced risks” until later

Credit risk: Capital protects banks from unexpected losses

Bank:

Bank capital

Savers

Corporate

Borrowers:

• Loans

• Mortgages

• Cards

• Overdrafts

Bank lends funds borrowed from savers and wholesale – & its own capital

Banks hold capital to protect savers from unexpected losses

~ 10%

~ 90%

Holding capital creates a trade off:

• Holding less capital lets balance sheet grow larger by leverage

• It also lets bank grow faster in future years

• This generates more profit in the good years

• But this creates more risk – less of a buffer, potential for asset bubbles

Bankers used to plan for worst

• But last two decades, cheap funding ,growing economy , Greenspan put and low bad debts – all factors that encouraged higher risk taking

• Actuaries can consider trade offs more easily than most – can challenge

There is tension with capital

History shows risks:

• Credit risk: – loan not repaid

• Liquidity risk: – depositors all want their money back at the same time ... But its been lent out

This creates two key risks a bank must manage

“I’d like to make a withdrawal”

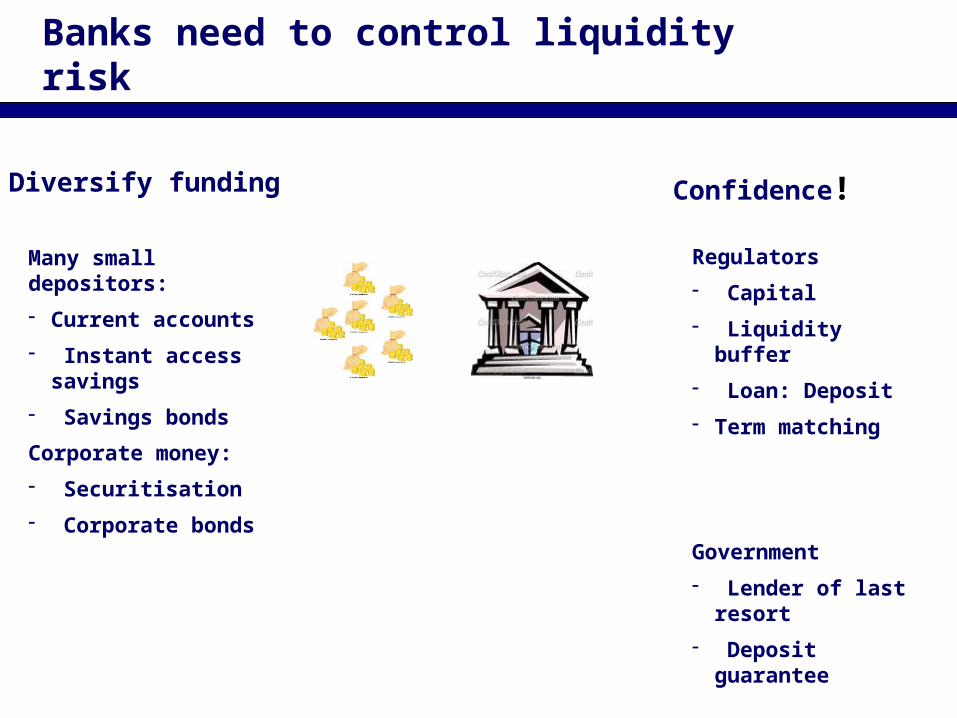

Banks need to control liquidity risk

Diversify funding

Many small depositors:

- Current accounts

- Instant access savings

- Savings bonds

Corporate money:

- Securitisation

- Corporate bonds

Confidence!

Regulators

- Capital

- Liquidity buffer

- Loan: Deposit

- Term matching

Government

- Lender of last resort

- Deposit guarantee

Lots of small deposits can be more stable:

• An individual account sees lots of cashflows in and out:

• If each account acts independently then flows in and out tend to balance

• Total balance is more stable and can be lent out long term

• Key is investigating behaviours

• Risk arises If independence breaks down

• Liquidity crisis and panic

• Bankers worst nightmare

Diversify funding across many customers

Different behavioural characteristics:

• People need to keep money in current accounts – more stable

• Bonds can lock money away – but cost more

• 30 or 60 day notice accounts delay a bank run

• Different balance sizes behave differently (especially Vs FSCS)

• Internet / branch etc behave differently:

• Corporate borrowing gives certainty such as 5 year bond

• But cant be rolled over if markets closed at maturity (HBOS had £164 bn to roll over with less than 12m)

Actuaries can help treasury functions

Diversify funding across account types

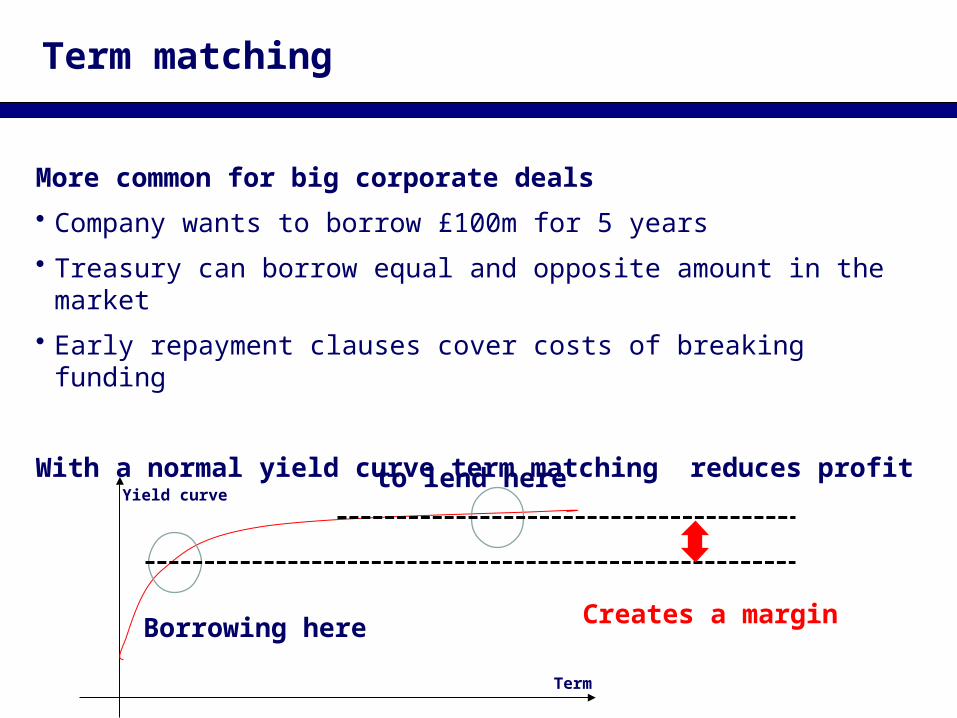

Term matching

More common for big corporate deals

• Company wants to borrow £100m for 5 years

• Treasury can borrow equal and opposite amount in the market

• Early repayment clauses cover costs of breaking funding

With a normal yield curve term matching reduces profit

Term

Yield curve

Borrowing here

to lend here

Creates a margin

Controlling liquidity risk:Liquidity buffer

Liquidity buffers

Easy to confuse with capital – but not the same thing

Bank:

Deposits

Corporate

Own capital

Lending:

• Loans

• Mortgages

• Cards

• Overdrafts

Liquid assetsBanks hold a portfolio of liquid assets such as Government debt – Gilts

In a time of stressed cash outgoing banks can sell these liquid assets to raise liquidity

Regulators look to hold enough to cover > 30 days of stressed outgoings.

This has a cost

Gilts yield ~ 2%

Bank marginal cost of raising cash is ~ 3%

Cost ~ -1% pa

Liability Asset

Controlling liquidity risk:Government - confidence

Lender of last resort

• Bank of England acts a lender of last resort

• Government stepped in to save banks

Guarantees deposits

• FSCS with £85K individual limit

Regulators set rules

• Actuaries need to demonstrate skills to these bodies to make headway

Capital and liquidity can influence lending in society

Great in the good times• Seems like a “magical way” to create money

• Fuels economic growth and expansion

• Historically helped Britain defeat France in 1700’s – 1800s

• But problem is when this goes into reverse

£100 £90

Deposit Loan

£90 £90

Deposit

£81

Loan

Each time money is deposited assume ~ 90% is lent out

This creates a pattern of deposits …. £100, £90, £81, £73 ….

This is a geometric series that adds up to £1,000

Our original £100 deposit can be lent out, spent and deposited to make £1,000!

Purchase

Banks need to manage spread as economy changes:

• As interest rates or inflation change rates paid to savers and rates charges to borrowers need to change

• Easier on new business

• Requires product design on back book

• Why mortgages revert to SVR – pricing break point

• Why Savings rates can be varied and bonus offers are attractive

Not just income

• Impact on affordability and bad debts

• Impact on asset prices and bad debts

Third banking risk is managing margins

Actuaries understand the yield curve

Bank cost of funding reflects the Gild curve

• Start with Gilt yields

• Add on extra yields for credit risk.

• Add on extra for “liquidity risk” if bank bonds are less liquid

Term

Yield

Base Rate

credit risk and liquidity risk

UK Government Gilt yield

Bank cost of borrowing

Government has programs to reduce borrowing costs at all terms

Term

Gilt yield

Base Rate

Set at 0.5%

Quantitative Easing

Buys gilts to keep yield low

Funding for Lending

Offers low cost borrowing to banks to lend

Short Medium Long

The government is trying to keep this low – to stimulate the economy

Banks carry more systemic risk:

• Leverage inherent in model creates risks:

• Capital

• Funding

• Interconnected so risk if one fails next can fail

• Play key roles in economy

• Money transmission

• Investment in new businesses key to capitalism (Creative destruction)

• Lending key to multiplier effect in economics

Other differences between banks and insurance

Banking risks easy to understand:

• A simple goldsmiths model captures core banking risks

• Actuaries can help banks by:

• crossing siloes to see trade offs (risk reward and through time)

• taking position of older bankers – first job is protecting savers

• There are opportunities … but no open doors

Fundamentally interesting industry

• Lot of challenges

• Change creates opportunities

• Has a vital social role to fulfil – if they get it right

Conclusion

Appendices:

What banks do for society

Risk based pricing

How much capital is needed

Services people need – payment transactions

• Provide money transmission services:

Services people need - cash flow management

• Overdrafts, revolving credit, trade finance

• Loans, mortgages (Variable rate / fixed rate)

Safe deposit – somewhere to keep savings

• Current account, savings accounts, bonds

Long term savings and protection

• Pensions, investments, life insurance

What do banks give to customers?

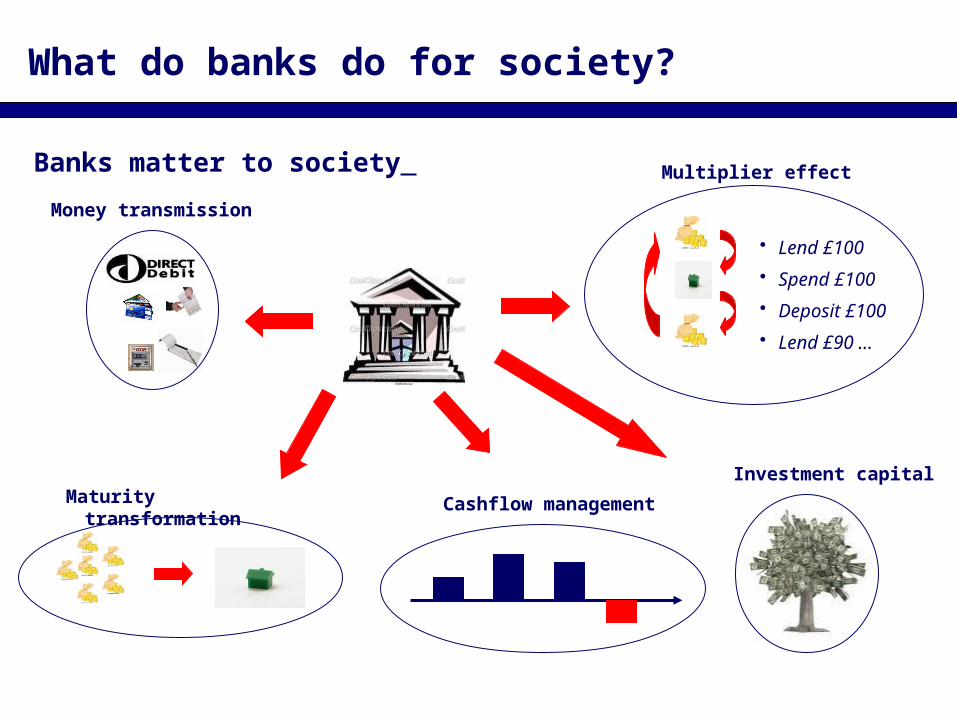

Banks matter to society

• Lend £100

• Spend £100

• Deposit £100

• Lend £90 …

Cashflow management

Money transmission

Investment capital

Multiplier effect

Maturity transformation

What do banks do for society?

Each of our current accounts can’t do much on their own• Balance is very volatile – can change daily

• Balance is quite small

• Individuals can’t usefully lend this to anybody as we don’t know when we will spend it

• This is “useless money for society”

Banks add them together• A few million current accounts add up to a lot of balances

• Added up these are much more stable

• As these are stable they can be lent out

• Used for mortgages, investment in new business etc

• Suddenly otherwise useless balances are being used by society

What do banks do for society:Maturity transformation

What do banks do for society:Cashflow management

Lets go back to Dickens’s Britain• Banks less developed

• Debtors prisons quite common

• Mr Micawbers quote to David Copperfield

“Annual income £20, annual expenditure 19 pounds 19 shillings & sixpence – result happiness”

“Annual income £20, annual expenditure 20 pounds & sixpence – result misery”

Today’s loans and overdrafts:• Short term: Let us smooth cashflows – borrow when we need to

• Long term: Lets us buy houses out of future income

What do banks do for society:Investment capital

Great ideas don’t always coincide with money to exploit them• Entrepreneurs have a good idea

• If developed this can create jobs, tax revenue, exports …

• However often people with good ideas don’t have the money

• People with money don’t have time to find those who need to borrow

• People with money may be more risk adverse

Banks acts as an intermediary:• Takes deposits

• Lends to those with good ideas

• Has experience to make these sort of lending decisions

What do banks do for society:Multiplier effect – in reverse

Real issue for banking policy makers• When people are worried about the future they start to save more

• They borrow less

• They spend less

This means that the multiplier effect we saw above can actually start to go into reverse

This can cause money supply to reduce and can trigger a recession / depression

Policy makers have been trying to avoid this:

• Encourage lending (base rate low at 0.5% and asset purchase scheme)

• Funding for lending scheme

Risk based pricing – lending to more customers

•If banks charge a higher rate then customers who were unprofitable become profitable

•Banks can therefore lend to more customers at a highrr rate.

PD

value

Extra customers who can get credit with risk based

pricing

6% Break even score

6% rate

15% rate 15% Break even score

How much capital for two banks?

Banks have same size of balance sheet of £10bn

Assets Bank A Bank B

Cash £1bn £1bn

Secured Residential Mortgages --- £9bn

Personal lending (Credit card, loan etc) £9bn ---

But quite different RWAs

Assets Bank A Bank B

Cash 0 0

Secured Residential Mortgages 0 3.15bn

Personal lending (Credit card, loan etc) 9bn 0

How much capital for two banks Basle I rules

Banks have same size of balance sheet of £10bn

Assets Bank A Bank B

Cash £1bn £1bn

Secured Residential Mortgages --- £9bn

Personal lending (Credit card, loan etc) £9bn ---

But quite different RWAs

Assets Bank A Bank B

Cash 0 0

Secured Residential Mortgages 0 4.5bn

Personal lending (Credit card, loan etc) 9bn 0

How much capital also recognises different types of capital

Tier 1 capital.

The banks own money.

• Initial share issues

• Rights issues (additional shares issued)

• Retained profits

Very loss absorbing

Tier 2 capital.

Like a normal corporate bond (IOU that pays interest and capital)

Not be repaid until depositors get their money back.

This is less loss absorbing and hence less secure

The RWAs then set out how much capital we need to hold

Regulatory MINIMUM capital calculated from RWAs

• 4% Tier 1

• 4% Tier 2

This is a minimum level of protection for depositors

Regulators require more than this minimum

Actual minimum agreed with regulators

Banks now hold ~ 10% Tier 1 capital

Regulators want to increase further (eg Basel III)

(but … recall from multiplier effect that this will constrain banks lending while they build up this capital or reduce lending)

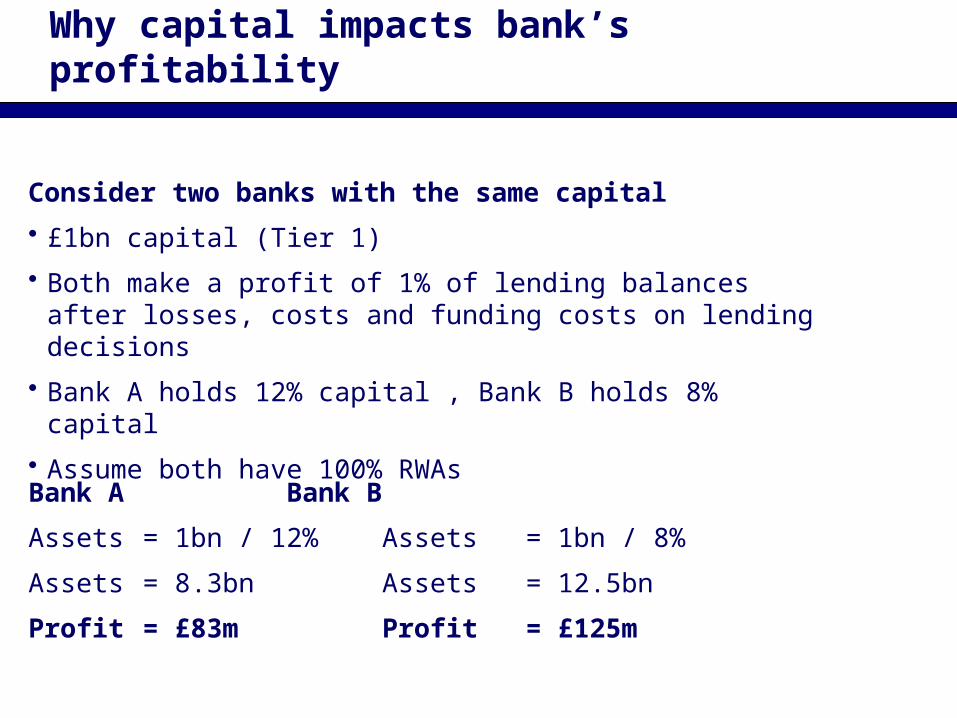

Why capital impacts bank’s profitability

Consider two banks with the same capital

• £1bn capital (Tier 1)

• Both make a profit of 1% of lending balances after losses, costs and funding costs on lending decisions

• Bank A holds 12% capital , Bank B holds 8% capital

• Assume both have 100% RWAs

Bank A Bank B

Assets = 1bn / 12% Assets = 1bn / 8%

Assets = 8.3bn Assets = 12.5bn

Profit = £83m Profit = £125m

Why capital impacts on bank’s growth

Consider same two banks – next year

• 50% of profit paid out (dividends / bonuses)

• 50% invested to support new lending growth

• Same capital ratios maintained

Bank A Bank B

Assets = 8.3bn Assets = 12.5bn

Profit = £83m Profit = £125m

Retained = £42m Retained = £62.5m

New Assets supported:

£42m / 0.12 = £347m £62.5 / 0.08 = £781m

(4%) (6%)

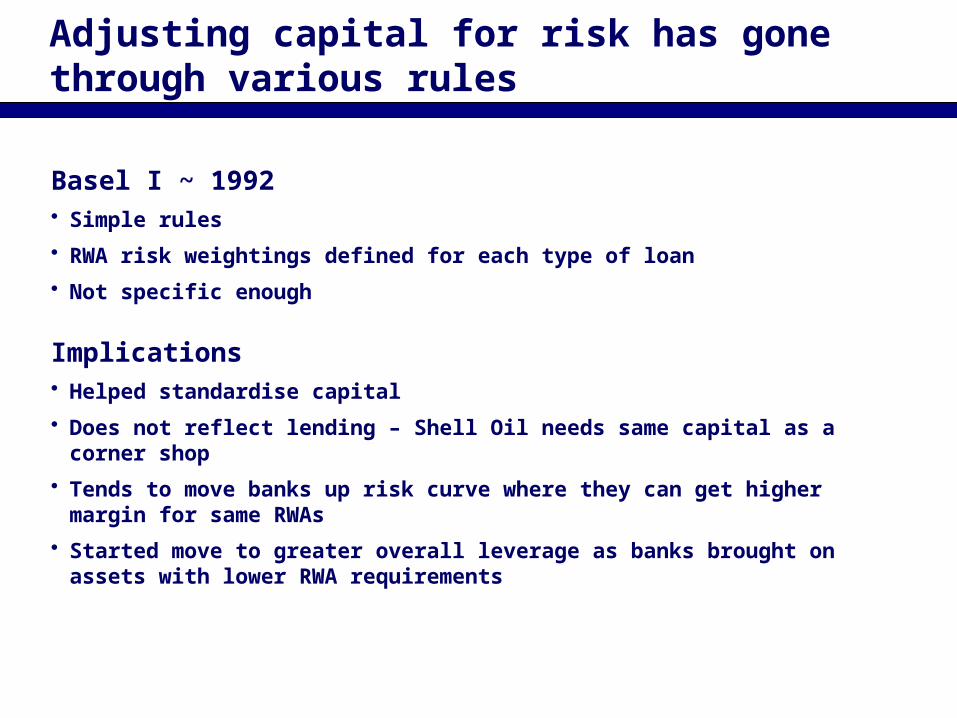

Adjusting capital for risk has gone through various rules

Basel I ~ 1992 • Simple rules

• RWA risk weightings defined for each type of loan

• Not specific enough

Implications• Helped standardise capital

• Does not reflect lending – Shell Oil needs same capital as a corner shop

• Tends to move banks up risk curve where they can get higher margin for same RWAs

• Started move to greater overall leverage as banks brought on assets with lower RWA requirements

Adjusting for risk has gone through various rules

Basel II ~ 2004 to 2008• Pillar I - RWA calculation specific to banks lending experience

• Based on key risk metrics – Probability of Default, Exposure at Default, Loss given default

• Increased disclosure in “pillars II and III”

Implications• Focused on credit risk rather than liquidity risk

• In a benign environment PDs and LGDs low (especially secured lending as house prices and land values rise)

• In benign environment capital required at its lowest point – just before it is needed

• When things go wrong capital requirements increase (PD, LGD rise) just when profits fall and cannot rebuild capital

Adjusting for risk has gone through various rules

Basel III ~ 2013 to 2018 ?• Under discussion

• Includes liquidity requirements

• Procylical capital buffer to be built up in good times

• More focus on quality of capital (loss absorbing)

Implications• Higher capital requirements

• Higher costs for liquidity buffer ( discussed later)