Page 1

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 1/69

SUMMER TRAINING REPORT

ON

A STUDY OF LOANS AND ADVANCES

OFFERED AT CANARA BANK

Submitted in partial fulfillment for the award of the degree of

Master in Business Administration (2008- 2010)

Submitted To: Submitted By:

Punjab Business School Aditya Balak Mehta

Chunni kalan MBA3rdSemester

PREFACE

Page 2

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 2/69

Management training has gained rapid and tremendous importance over the past five years.

Management was previously considered as an inborn art or talent Management training has

gained rapid and tremendous importance over the past five years. Management was previously

considered as an, but in today’s fast developing world, these have been modified.

I undertook six weeks (starting from 13th July 2009 to 26th August 2009) summer training in

CANARA Bank As an essential and obligatory part of master program in business

administration, curriculum of Punjab Technical, University.

The report embodies the result of the project an extensive market research program was

accomplished. We deem it as a matter of great fortune to get summer training at CANARA Bank

khanna.

The summer training was quite interesting, inspiring, satisfying, learning and academicallyawarding.

STUDENTS DECLARATION

Page 3

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 3/69

I ADITYA BALAK MEHTA submitted my project report on

“STUDY OF LOANS & ADVANCES OFFERED AT CANARABANK”. I have

my training at canara bank. It is the original work done and the information

provided in the study is authentic to the best of my knowledge.

Date: Aditya Balak Mehta

Place : Chunni kalan

ACKNOWLEDGEMENT

Page 4

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 4/69

I would like to express my heart felt gratitude to all the persons involved in the process of

preparing this report.

Firstly I would like to thank Mr. Jagjit Singh Chief Manager for allowing me to do my six

weeks summer training from Canara Bank. Secondly I would like to express my sincere thanks

to my project guide Mr. Sucha Singh, Loan Manager, Mr. VIJAY RATAN, Officer, for his

valuable support and guidance throughout the project and preparing this report. His constant

appreciation of the work and support helped me immensely in the successful completion of my

training period.

It would be unfair on my part if don’t express my thanks to the following persons who provided

me with all possible records and helped me in every possible manner in carrying out the various

studies I required in completing my training report.

Mr. Paramjeet Kullar, Manager who guide me during my training.

I am especially thankful to the staff of bank and payroll section for their patience to bear with me

while interviewing the absentees for collection of primary data.

Executive Summary

Page 5

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 5/69

A loan is a type of debt. Like all debt instruments, a loan entails the redistribution of financial

assets over time, between the lender and the borrower.

In a loan, the borrower initially receives or borrows an amount of money, called the principal,

from the lender, and is obligated to pay back or repay an equal amount of money to the lender at

a later time. Typically, the money is paid back in regular installments, or partial repayments; in

an annuity, each installment is the same amount.

The loan is generally provided at a cost, referred to as interest on the debt, which provides an

incentive for the lender to engage in the loan. In a legal loan, each of these obligations and

restrictions is enforced by contract, which can also place the borrower under additional

restrictions known as loan covenants. Although this article focuses on monetary loans, in

practice any material object might be lent.

Acting as a provider of loans is one of the principal tasks for financial institutions. For other

institutions, issuing of debt contracts such as bonds is a typical source of funding.

So Canara Bank is also involved in issuing loans.

Page 6

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 6/69

Table of Contents

Section 1: Introduction to Project

1. Introduction of loans Offered at Canara Bank

2. Types of loans

Section 2: Industry Profile

1. Introduction to Banking Sector

2. Scope of Banking Indus

3. Banking Opportunity

Section 3: Company Profile

1 History of Canara Bank

2 Canara Bank in India

3 Products Information

4 Mission &Vision of Canara Bank

5 Profile of Canara Bank

Section 4: Objectives

Section 5: Research and Methodology

Section 6: Analysis and Interpretations

Section 7: Swot Analysis

Section 8: Limitations

Section 9: Recommendations

Page 7

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 7/69

Section 10: Suggestions

Section 11: Annexure

• Bibliography

• Questionnaire

• Balance Sheet of Canara Bank

• Profit & Loss Account of Canara Bank

• Cash Flow Statement of Canara Bank

Page 8

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 8/69

INTRODUCTION

INTRODUCTION

Canara Bank has been serving its customers since July 1906 and has undergone various stages of

growth over hundred years of excellence. Founded by Shri Ammembal Subba Rao, the bank has

attained nationalization in the year 1969. The banking operations are customer friendly and the

bank has emerged as the largest nationalized bank in India.

Page 9

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 9/69

Canara Bank Loans are offered to the customers to fulfill their monetary requirements.

Canara Bank provides all conventional banking facilities and various contemporary banking

products. The various types of Canara Bank Loans, which are offered to the customers include:

• Personal Loan

• Home Loan

• Consumer Loan

• Vehicle Loan

• Educational Loan

• CEMAT Facilities

• Agricultural Loan

Canara Bank Car Loans:

The car loans by the Canara Bank are offered for buying new or used four wheelers. The loans

are given to the salaried people with regular income and those who have the capacity to repay

the loan amount. Corporate firms and business people are eligible for car loans. For new car

loans, there is no ceiling on the loan amount. For the used cars, the bank offers finance for the

cars that are older than 5 years.

Canara Bank Home Loans:

Canara Bank Home Loans are provided for the purchase or construction of houses and flats.

The bank also offers loans for the renovation and furnishing of the existing house or flat. Loanamount subject to the maximum of Rs. 1,00,00,000 is provided to the customers. For site loans,

the amount should be repaid within a period of 5 to 10 years. For other loans, the loan amount

can be repaid within 5 to 20 years. Canara Bank Home Loans are also offered for the purchase

or construction of companies or corporations.

Canara Bank Education Loans:

The educational loans by Canara Bank are provided to the meritorious students and the needy

students. The funds are offered to the Indian students only. The loans are granted for pursuing

graduate courses, professional courses and technical courses. Finance is provided by the Canara

Bank for advanced studies abroad as well.

The education loans are offered for the payment of fees, purchase of educational equipment and

books. For study in India, the maximum loan amount that is provided is Rs. 7.50 lacs and for

studies abroad, the ceiling is Rs.15 lacs. The loan amount needs to be repaid within 5 to 7

years.

Page 10

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 10/69

Canara Bank Personal Loans:

Personal loans are offered by Canara Bank to fulfill various personal needs of the customers.

The personal loans are provided to all who have the ability to repay the loan amount.

Canara Bank Loans are also provided to the Non-Resident Indians.

CANARA BANK LOANS

Canara Bank provides provides loans to almost every section of the society.

Some of the loans are mentioned as under:

• Agriculture & Rural Credit

• Kisan Credit

• Loans for Agri- Clinic

• Minor Irrigation Loans

• Farm Machinery Loans

• Farm Development Loans

• Vehicle Loan for Agriculturists

• Loan for Plantation Crops

•Loan for Marine Fisheries

• Loan for Inland Fisheries

• Loan for Sericulture

• Loan for Purchasing Agricultural Land

• Loan for Poultry

• Export Credit for Agro Products

•

Other Agricultural Loans

• Loans to SSIs

• Charter for SSIs

FOR WOMENS

The Centre for Entrepreneurship Development for Women was established by Canara Bank in

India at the Bank's Corporate Office, Bangalore during the year 1988 with an objective of

assisting the potential women entrepreneurs to select income generating activities and starting

ventures of their own. Subsequently 9 such CED’s were opened and are functioning at Circle

Page 11

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 11/69

Offices situated at various State Capitals. The CED at corporate office brings out a newsletter

VIKAS everybody-monthly.

Mahila Banking branch:

An exclusive branch for women and Mahila banking division - an exclusive division for women

within a branch opened, which is the 1st of kind in the banking industry.

Details are enlisted below:

• Mahila Banking Branch, Jayanagar , Bangalore, Karnataka

• Mahila Banking Division, Mandipet Branch, Davangere, Karnataka

• Mahila Banking Division, M G Road Branch, Agra, UP

•

Mahila Banking Division, N V Street Branch, Madurai, Tamil Nadu

• Mahila Banking Division, West Palace Road, Thrissur, Kerala

• Mahila Banking Division, West Hill, Kozhikode, Kerala

• Mahila Banking Division, Shimoga Main Branch, Karnataka

These specialized branch and divisions offer all banking services to women.

Loans & Advances:

A loan is a type of debt. Like all debt instruments, a loan entails the redistribution of financial

assets over time, between the lender and the borrower.

In a loan, the borrower initially receives or borrows an amount of money, called the principal,

from the lender, and is obligated to pay back or repay an equal amount of money to the lender at

a later time. Typically, the money is paid back in regular installments, or partial repayments; in

an annuity, each installment is the same amount. The loan is generally provided at a cost,

referred to as interest on the debt, which provides an incentive for the lender to engage in the

loan. In a legal loan, each of these obligations and restrictions is enforced by contract, which can

also place the borrower under additional restrictions known as loan covenants. Although this

article focuses on monetary loans, in practice any material object might be lent.

Page 12

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 12/69

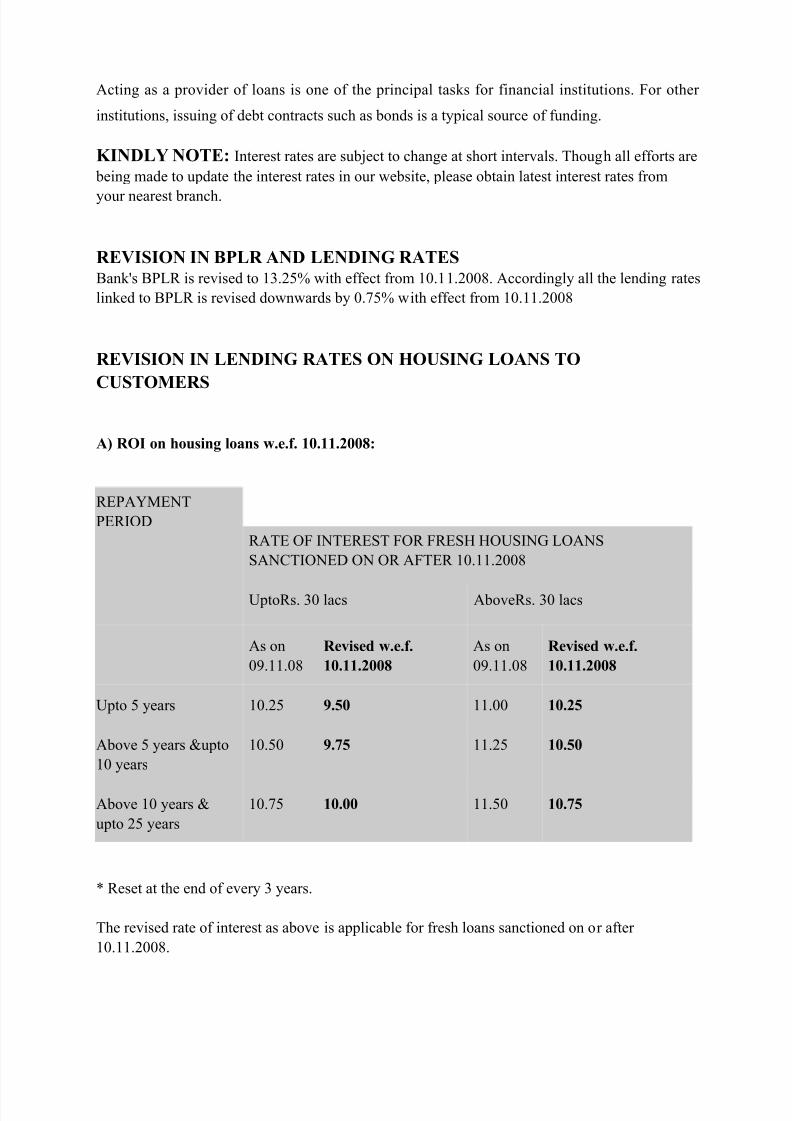

Acting as a provider of loans is one of the principal tasks for financial institutions. For other

institutions, issuing of debt contracts such as bonds is a typical source of funding.

KINDLY NOTE: Interest rates are subject to change at short intervals. Though all efforts are

being made to update the interest rates in our website, please obtain latest interest rates from

your nearest branch.

REVISION IN BPLR AND LENDING RATESBank's BPLR is revised to 13.25% with effect from 10.11.2008. Accordingly all the lending rates

linked to BPLR is revised downwards by 0.75% with effect from 10.11.2008

REVISION IN LENDING RATES ON HOUSING LOANS TO

CUSTOMERS

A) ROI on housing loans w.e.f. 10.11.2008:

REPAYMENT

PERIOD

RATE OF INTEREST FOR FRESH HOUSING LOANS

SANCTIONED ON OR AFTER 10.11.2008

UptoRs. 30 lacs AboveRs. 30 lacs

As on

09.11.08

Revised w.e.f.

10.11.2008

As on

09.11.08

Revised w.e.f.

10.11.2008

Upto 5 years 10.25 9.50 11.00 10.25

Above 5 years &upto

10 years

10.50 9.75 11.25 10.50

Above 10 years &

upto 25 years

10.75 10.00 11.50 10.75

* Reset at the end of every 3 years.

The revised rate of interest as above is applicable for fresh loans sanctioned on or after

10.11.2008.

Page 13

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 13/69

ROI on all slabs linked to BPLR.

Additional interest @ 0.25 % above the card rates for acquisition of second house/flat.

B) Margin for housing loans:

Margin

Loans uptoRs.20 lacs

(Cir.No.152/2007)

Loans above Rs.20 lacs

New house/flat 20% 20 %

Old house/flat 25 % 25 %

C) Loans for acquiring second house/flat:

• Additional interest @ 0.25 % p.a. over and above the applicable rates.

• Margin @ 25 %.

Home Improvement Loan

Rate of Interest:w.e.f 10.11.2008

IF HOME IMPROVEMENT LOAN (HIL) IS AVAILED ALONG WITH THE HOUSING

LOAN OR AN EXISTING HOUSING LOAN IS OUTSTANDING IN OUR BANK THE

RATE OF INTEREST (ROI) AS APPLICABLE TO HOUSING LOANS.

IF THE HOME IMPROVEMENT LOAN IS AVAILED INDEPENDENTLY THE

APPLICABLE ROI IS PREVAILING BPLR, Presently, 13.25% p.a.

Canara Site

w.e.f 04.10.2008

Loans repayable in 5 years 15.00%

Loans repayable in above 5 years term (Max of 10 years) 15.00%

Page 14

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 14/69

Canara jewel

w.e.f 04.10.2008

SCHEME DISCONTINUED – For existing Customer 15.00%

Canara tech

w.e.f 04.10.2008

SCHEME DISCONTINUED – For existing customer 15.00%

Canara travel

w.e.f 04.10.2008

SCHEME DISCONTINUED - for existing customer 15.00%

Canara value

w.e.f 04.10.2008

SCHEME DISCONTINUED – For existing customer 15.00%

Canara Cashw.e.f 04.10.2008

15.00% p.a.

On daily reducing balance,

(Subject to change from time to time)

Can Mobile (Car Loan / Two-Wheeler Loan)

w.e.f 10.11.2008

a. a. Car loan – 12.50% p.a (fixed) - For fresh loans only

Canara Budget (Simple Personal Loan)

w.e.f 04.10.2008

Floating Rate - 15.00% p.a.

Page 15

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 15/69

Canara Pension

w.e.f 07.08.2008

Floating Rate – 12.50% p.a.

A concessional rate for our Senior Citizens!

Teachers Loan scheme

w.e.f 04.10.2008

Floating Rate -15.00% p.a.

Revised Fixed rate

w.e.f 07.11.2008

Revised Floating rate

w.e.f 10.11.2008

(xxii). CANARA RENTCanararent where the lessees are - Navaratna

PSUs, AAACos, Fortune 500 Cos, MNCs, Banks,

Insurance Cos

Other than above

15.25*

15.75*

13.25

13.75

(xxiii). CANARA MORTGAGE 16.25* 15.00

Fixed rate loans to be reset every 3 years

Gold Loan/Swarna Loan Scheme

w.e.f 04.10.2008

13.25%

Loans for Traders & Businessmen: w.e.f. 04.10.2008

Upto Rs.2 lakhs 14.50% p.a.

Above Rs.2 lacs including loans under priority sector 15.00% p.a.(No Change).

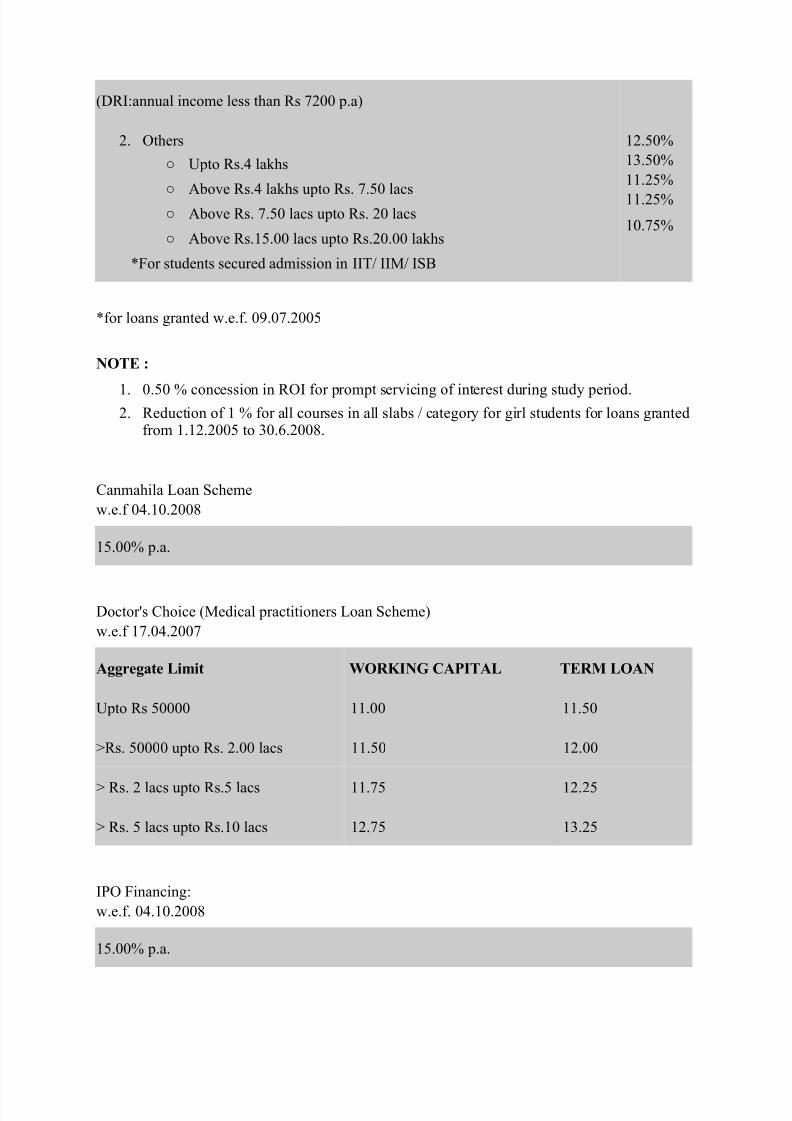

Vidyasagar Loan for Students:

Rate of Interest : (Subject to changes as advised by Bank / RBI from time to time):

1. Student satisfying DRI norms

(irrespective of quantum of loan)

4.00%

Page 16

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 16/69

(DRI:annual income less than Rs 7200 p.a)

2. Others

○ Upto Rs.4 lakhs

○

Above Rs.4 lakhs upto Rs. 7.50 lacs○ Above Rs. 7.50 lacs upto Rs. 20 lacs

○ Above Rs.15.00 lacs upto Rs.20.00 lakhs

*For students secured admission in IIT/ IIM/ ISB

12.50%

13.50%

11.25%

11.25%

10.75%

*for loans granted w.e.f. 09.07.2005

NOTE :

1. 0.50 % concession in ROI for prompt servicing of interest during study period.2. Reduction of 1 % for all courses in all slabs / category for girl students for loans granted

from 1.12.2005 to 30.6.2008.

Canmahila Loan Scheme

w.e.f 04.10.2008

15.00% p.a.

Doctor's Choice (Medical practitioners Loan Scheme)

w.e.f 17.04.2007

Aggregate Limit WORKING CAPITAL TERM LOAN

Upto Rs 50000 11.00 11.50

>Rs. 50000 upto Rs. 2.00 lacs 11.50 12.00

> Rs. 2 lacs upto Rs.5 lacs 11.75 12.25

> Rs. 5 lacs upto Rs.10 lacs 12.75 13.25

IPO Financing:

w.e.f. 04.10.2008

15.00% p.a.

Page 17

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 17/69

Loans under ESOP Scheme :

w.e.f. 04.10.2008

15.00% p.a.

Loans to assist employees to subscribe to shares of their own companies under reserve quota

w.e.f. 04.10.2008

15.00% p.a.

Loans to individuals (Clean OD/DPN other than Teachers’ loan):

15.50% p.a.

BULC:(wef 04.10.2008)

Upto 90 days 14.00% p.a.

Above 90 days Upto 180 days 15.00% p.a.

Loans to individuals against other approved securities:

w.e.f. 07.08.2008

15.00% p.a.

Loans against Debt oriented MFs: w.e.f. 04.10.2008

15.00% p.a.

Corporate Loan scheme : w.e.f. 07.08.2008

14.00% p.a.

STLR : w.e.f. 07.08.2008

14.00% p.a.

Page 18

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 18/69

Canara Guide :

w.e.f. 07.08.2008

12.75% p.a.

Canara Jeevan :

w.e.f 07.08.2008

Fixed – 10.50% - Reset at end of 3 years

Canara Trade :

w.e.f . 04.10.2008

14.00%

Types of Loans

1. Secured

2. Unsecured

Secured:

A secured loan is a loan in which the borrower pledges some asset (e.g. a car or property) as

collateral for the loan.

A mortgage loan is a very common type of debt instrument, used by many individuals to

purchase housing. In this arrangement, the money is used to purchase the property. The financial

institution, however, is given security — a lien on the title to the house — until the mortgage is

paid off in full. If the borrower defaults on the loan, the bank would have the legal right to

repossess the house and sell it, to recover sums owing to it.

Page 19

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 19/69

In some instances, a loan taken out to purchase a new or used car may be secured by the car in

much the same way as a mortgage is secured by housing. The duration of the loan period is

considerably shorter — often corresponding to the useful life of the car. There are two types of

auto loans, direct and indirect. A direct auto loan is where a bank gives the loan directly to a

consumer. An indirect auto loan is where a car dealership acts as an intermediary between the bank or financial institution and the consumer.

A type of loan especially used in limited partnership agreements is the recourse note.

A stock hedge loan is a special type of securities lending whereby the stock of a borrower is

hedged by the lender against loss, using options or other hedging strategies to reduce lender risk

A pre-settlement loan is a non-recourse debt, this is when a monetary loan is given based on the

merit and awardable amount in a lawsuit case. Only certain types of lawsuit cases are eligible for

a pre-settlement loan. This is considered a secured non-recourse debt due to the fact if the case

reaches a verdict in favor of the defendant the loan is forgiven.

Unsecured:

Unsecured loans are monetary loans that are not secured against the borrower's assets. These

may be available from financial institutions under many different guises or marketing packages:

• credit card debt

• personal loans

• bank overdrafts

• credit facilities or lines of credit

• corporate bonds

The interest rates applicable to these different forms may vary depending on the lender and the

borrower. These may or may not be regulated by law. In the United Kingdom, when applied to

individuals, these may come under the Consumer Credit Act 1974.

TERM LOANS

- Term Loan is normally extended for acquisition of Land, Building and machinery,

purchase of vehicles etc. and also along with working capital finance as composite loans.

- Term Loan is given both for industrial and non-industrial borrowers i.e. both for

projects / activities involved in manufacture/processing/repairing and business / trading

Page 20

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 20/69

activities etc. The project needs to establish technical feasibility and economic viability.

- Term loan is extended in different forms such as all rupee loans, foreign currency

loans and Deferred Payment Guarantees (DPG) / acceptance facilities (other than foreign

currency loans obtained from the foreign banks or branches of Indian Banks abroad

without the back-up of DPGs issued by Banks in India).

- Repayment schedule for term loans would be stipulated based upon Debt Service

Coverage Ratio, cash generation and repayment capacity. Repayment would be by way of

periodic instalments with appropriate repayment holiday during implementation of the

project.

- Rate of interest on term loans depend upon various factors like nature of the project,

quantum of loan, risk rating, repayment period and structure of the debt.

- Securities for term loans per se would be as per general lending norms of the banks.

LOAN DELIVERY & EVALUATION:

1. Time norms for disposal of loan applications :

The banks’ credit policy defines time norms for timely disposal of credit proposals. In

this regard, following time norms shall be shall be adhered to in disposing a credit

proposal and accordingly , token of services is issued to the applicant.

1. Loans up to Rs.25000/- - Within 15 days

2. Kisan credit card- Branch powers - Max. 15 days

3. Other Priority Sector advances

(1) loans/ advances upto Rs. 25000/-

(2) loans/ advances over Rs. 25000/-

-

-

2 weeks

8-9 weeks

4. Export credit under gold card scheme

(1) Sanction of fresh/ enhanced credit limits

(2) Renewal of existing credit limits

(3) Sanction of adhoc credit facilities

-

-

-

25 days

15 days

7 days

5. Export credit –other than gold card scheme

(1) Sanction of fresh/ enhanced credit limits

(2) Renewal of existing credit limits

(3) Sanction of adhoc credit facilities

-

-

-

45 days

30 days

15 days

Page 21

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 21/69

6. Advances under Sole Banking, Multiple Banking

Arrangement, Consortium & other than credit

proposal:

1.Sanction of fresh/ enhanced credit limits

2.Renewal of existing credit limits

3. Sanction of adhoc credit facilities

-

-

-

60 days

45 days

30 days

CREDIT RISK MEASUREMENT:

The credit risk assessments help the bank to measure whether the potential borrowers will

be able to meet their loan obligation in accordance with contractual agreements. All

borrower’s with the limit of Rs 200000/- and above are to be rated individually and under

the appropriate risk rating models developed for the purpose.

Rating Models:

a. Risk Assessment Model (RAM):

This model is applicable for the borrowal accounts with sanctioned limit of over

Rs 2 crore.

b. Manual Model:

This model is applicable for the borrowal accounts with sanctioned limit of over

Rs 20 lacs and not more than Rs.2 crore.

c. Small value Model:

This model is applicable for the borrowal accounts with sanctioned limit of Rs 2

lacs and not more than Rs.20 lakh.

d. Portfolio Model:

The borrowal accounts of aggregate limits below Rs. 2 lacs and borrowal

accounts where financial statement are not available are risk rated under portfolio

model, duly grouping the accounts are near homogenous the accounts are near

homogenous pool based on category of borrowers and loan schemes/segment. The

model covers rating of borrowal accounts classified under priority and non

Page 22

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 22/69

priority segments. The priority sector loans include both Direct and Indirect

Agricultural loans, and non priority sector loans include those under schematic

lending under retails schemes.

A. Domestic Credit rating agencies:

• Credit analysis and research limited (CARE)

• CRISIL Limited

• FITCH INDIA Limited

• ICRA Limited

B. International Credit Rating Agencies:

• FITCH

• MOODYS

• STANDAD AND POORS

INDUSTRY PROFILE

Page 23

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 23/69

Page 24

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 24/69

There are various financial products that a bank offers to its customers such as- different types of

accounts viz. Savings Account, Fixed Deposit Account and other facilities like Loans,

Investments, Insurance etc. Since this sector is facing lot of competition, banks have to design

their policies and strategies to attract more and more customers. It is a race to catch the position

of market leader with maximum market share.

MARKETING OF BANK SERVICES:

It means designing good services as well as good delivery of these services. It covers following

functions:

• Identification of customer needs, financial/service related

• Developing appropriate services/products to suit the needs and determining their prices.

• Setting up channels for their delivery and making the present and potential customers

aware about their availability.

• Developing proper attitude, orientation and culture among the employees for delivering

the services to the satisfaction of the customers.

SCOPE OF BANKING INDUSTRY:

Banks have voluntarily taken on the entire task of mobilization of savings of the household

sector, over the past several decades, and helped achieve impressive household savings rates of

20% of the

Country’s GDP. We are already witnessing the ATMs progressing, Tele banking, and Home

Banking, and the trends towards aggregation and cross selling of various financial products,

such as Banking, Mutual Funds, and Insurance, to name just a few, are very evident. The

ATMs may even be smart ATMs- using biometrics, to recognize customers by their voice face or

fingerprints. In essence, the new generation ATMs will be retailing ports and will change the

very face of banking as well as retailing. As we achieve higher economic growth, the demand for

banking products and services will increase exponentially – particularly, in areas outside thehandful of major cities and towns. The entire banking industry is set to undergo dramatic and

sweeping changes.

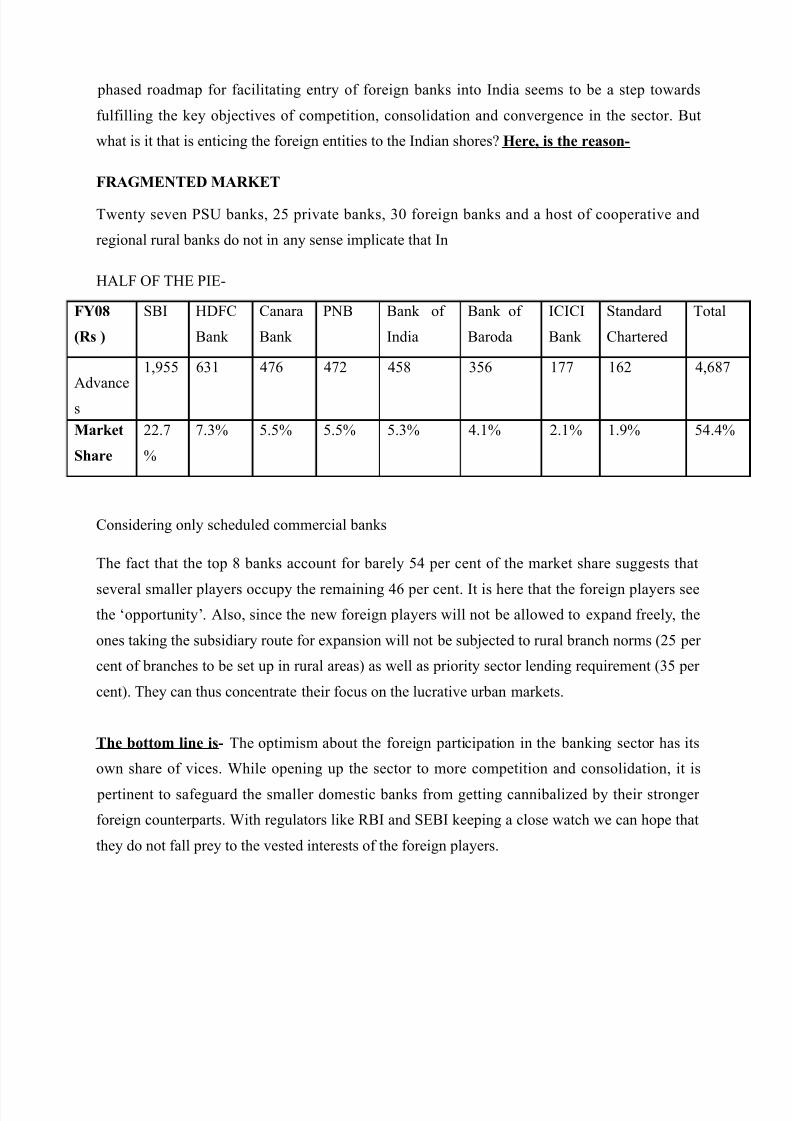

BANKING OPPORTUNITY: INDIA CALLING

It is not just the reports saying that foreign financial entities (GE Money, Goldman Sachs and

Merrill Lynch to name a few) are showing interest in Indian banking sector, but the concerned

authorities in the country also seem to be encouraging the same. Reserve Bank of India’s twin-

Page 25

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 25/69

phased roadmap for facilitating entry of foreign banks into India seems to be a step towards

fulfilling the key objectives of competition, consolidation and convergence in the sector. But

what is it that is enticing the foreign entities to the Indian shores? Here, is the reason-

FRAGMENTED MARKET

Twenty seven PSU banks, 25 private banks, 30 foreign banks and a host of cooperative and

regional rural banks do not in any sense implicate that In

HALF OF THE PIE-

FY08

(Rs )

SBI HDFC

Bank

Canara

Bank

PNB Bank of

India

Bank of

Baroda

ICICI

Bank

Standard

Chartered

Total

Advance

s

1,955 631 476 472 458 356 177 162 4,687

Market

Share

22.7

%

7.3% 5.5% 5.5% 5.3% 4.1% 2.1% 1.9% 54.4%

Considering only scheduled commercial banks

The fact that the top 8 banks account for barely 54 per cent of the market share suggests that

several smaller players occupy the remaining 46 per cent. It is here that the foreign players see

the ‘opportunity’. Also, since the new foreign players will not be allowed to expand freely, the

ones taking the subsidiary route for expansion will not be subjected to rural branch norms (25 per

cent of branches to be set up in rural areas) as well as priority sector lending requirement (35 per

cent). They can thus concentrate their focus on the lucrative urban markets.

The bottom line is- The optimism about the foreign participation in the banking sector has its

own share of vices. While opening up the sector to more competition and consolidation, it is

pertinent to safeguard the smaller domestic banks from getting cannibalized by their stronger

foreign counterparts. With regulators like RBI and SEBI keeping a close watch we can hope that

they do not fall prey to the vested interests of the foreign players.

Page 26

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 26/69

COMPANY PROFILE

COMPANY PROFILE

BANK HISTORY

Founded as ‘CANARA BANK Hindu Permanent Fund’ in 1906, by late Sri Ammembal Subba

Rao Pai, a philanthropist, this small seed blossomed into a limited company as ‘CANARA

BANK Ltd.’In 1910 and become Canara Bank in 1969 after nationalization.

Page 27

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 27/69

"A good bank is not only the financial heart of the community, but also one with an

obligation of helping in every possible manner to improve the economic conditions of the

common people" - A. Subba Rao Pai.

Founding Principles:-

1. To spread education among all to sub-serve the first principle.

2. To inculcate the habit of thrift and savings.

3. To transform the financial institution not only as the financial heart of the community but

the social heart as well.

4. To assist the needy.

5. To work with sense of service and dedication.

6. To develop a concern for fellow human being and sensitivity to the surroundings with a

view to make changes/remove hardships and sufferings.

7. To develop the internet-banking service between their customers.

8. To assistance the educated or professional persons for their self employment.

9. To invest the savings of their investors in proper projects or in institutions.

10. Sound founding principles, enlightened leadership, unique work culture and remarkable

adaptability to changing banking environment have enabled Canara Bank to be a

frontline banking institution of global standards.

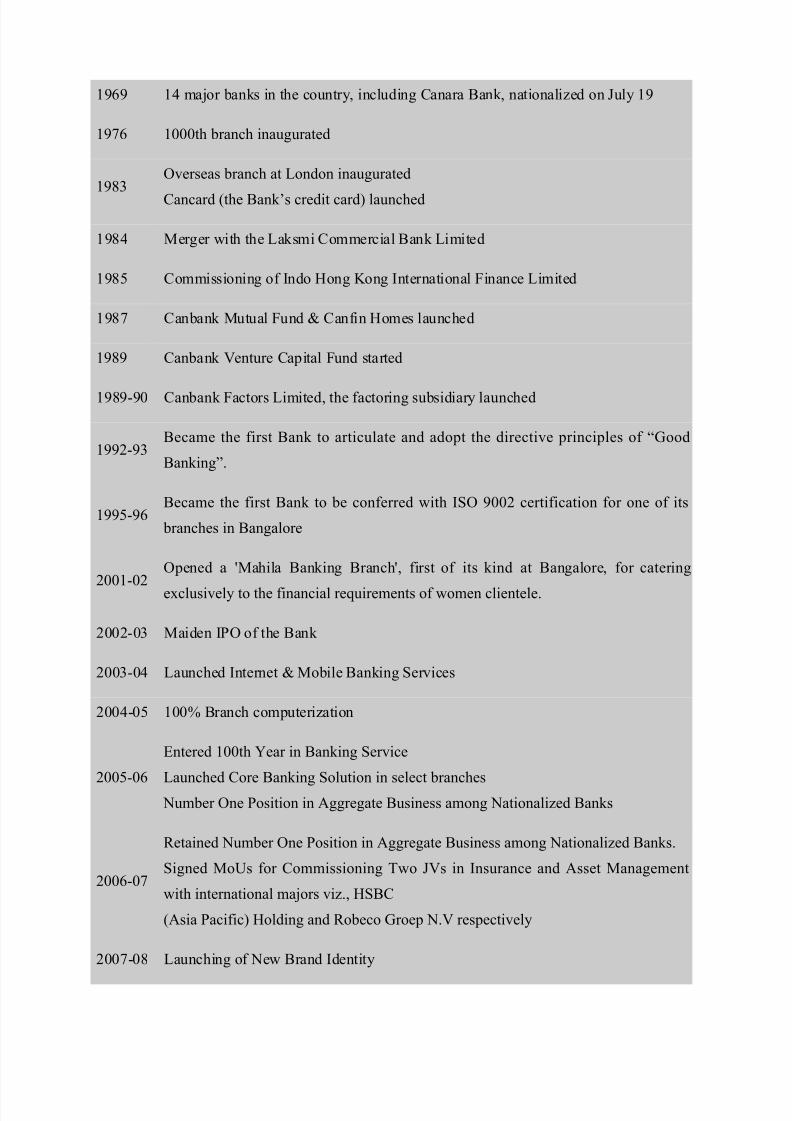

Significant milestones

Year

1st July

1906

Canara Hindu Permanent Fund Ltd. formally registered with a capital of 2000 shares

of Rs.50/- each, with 4 employees.

1910 Canara Hindu Permanent Fund renamed as Canara Bank Limited

Page 28

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 28/69

1969 14 major banks in the country, including Canara Bank, nationalized on July 19

1976 1000th branch inaugurated

1983Overseas branch at London inaugurated

Cancard (the Bank’s credit card) launched

1984 Merger with the Laksmi Commercial Bank Limited

1985 Commissioning of Indo Hong Kong International Finance Limited

1987 Canbank Mutual Fund & Canfin Homes launched

1989 Canbank Venture Capital Fund started

1989-90 Canbank Factors Limited, the factoring subsidiary launched

1992-93Became the first Bank to articulate and adopt the directive principles of “Good

Banking”.

1995-96Became the first Bank to be conferred with ISO 9002 certification for one of its

branches in Bangalore

2001-02Opened a 'Mahila Banking Branch', first of its kind at Bangalore, for catering

exclusively to the financial requirements of women clientele.

2002-03 Maiden IPO of the Bank

2003-04 Launched Internet & Mobile Banking Services

2004-05 100% Branch computerization

2005-06

Entered 100th Year in Banking Service

Launched Core Banking Solution in select branches

Number One Position in Aggregate Business among Nationalized Banks

2006-07

Retained Number One Position in Aggregate Business among Nationalized Banks.

Signed MoUs for Commissioning Two JVs in Insurance and Asset Management

with international majors viz., HSBC

(Asia Pacific) Holding and Robeco Groep N.V respectively

2007-08 Launching of New Brand Identity

Page 29

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 29/69

PROFILE OF CANARA BANK:

A Brief Profile of the Bank Widely known for customer centricity, Canara Bank was

founded by Shri Ammembal Subba Rao Pai, a great visionary and philanthropist, in July 1906, at

Mangalore, then a small port in Karnataka. The Bank has gone through the various phases of its

growth trajectory over hundred years of its existence. Growth of Canara Bank was phenomenal,

especially after nationalization in the year 1969, attaining the status of a national level player in

terms of geographical reach and clientele segments. Eighties was characterized by business

diversification for the Bank. In June 2006, the Bank completed a century of operation in the

Indian banking industry. The eventful journey of the Bank has been characterized by several

memorable milestones. Today, Canara Bank occupies a premier position in the comity of Indian

banks. With an unbroken record of profits since its inception, Canara Bank has several firsts to

its credit. These include:

• Launching of Inter-City ATM Network

• Obtaining ISO Certification for a Branch

• Articulation of ‘Good Banking’ – Bank’s Citizen Charter

• Commissioning of Exclusive Mahila Banking Branch

• Launching of Exclusive Subsidiary for IT Consultancy

• Issuing credit card for farmers

• Providing Agricultural Consultancy Services

•

Page 30

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 30/69

Vision:

To emerge as a ‘Best Practices Bank’ by pursuing global benchmarks in

profitability, operational efficiency, asset quality, risk management and expanding theglobal reach.

Mission:

To provide quality banking services with enhanced customer orientation, higher

value creation for stakeholders and to continue as a responsive corporate social citizen

by effectively blending commercial pursuits with social banking.

Canara Bank in India

Canara Bank in India has a history of nine decades and is the largest public sector banks in India.

Canara Bank India has a deposit advance base of Rs.640 bn and Rs 332 bn (figure in the year

2002).

Canara Bank of India has a total of 47,843 employees and is spread with 2409 branches

throughout the country. Canara Bank India has an exposure to petroleum, engineering,

infrastructure, factoring, investment management, venture capital, home finance and securities.

Canara Bank entered Forex arena in 1953 with the opening of its first Foreign Exchange

Department in Mumbai. The Bank has 5 forex dealing rooms located in Mumbai, New Delhi,

Calcutta, Chennai and Bangalore in India and one in London branch. Can bank provides a wide

range of services and products like sale and purchase of 7 world currencies, swap currency and

forward bookings.

SHARES OF CANARA BANK :-

Canara Bank Shares are listed at Bangalore, Mumbai and National Stock exchanges.

The Bank has appointed the under mentioned as its share transfer agent to whom

communications regarding change of address, change in Bank Mandate, transfer of shares ,

Mandate for ECS etc. should be addressed.

Karvy Consultants Ltd46,Avenue,

4StreetNo.1BanjaraHills

Hyderabad-500034

Page 31

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 31/69

Interms of SEBI guidelines, the Registrar and Transfer agent of the Bank is extending the facility

of simultaneous transfer -cum dematerialization of shares to the investors. On transfer of shares

in the name of the transferee, they are being apprised to submit letters to their depository

participants for dematerialization of shares. On receipt of Demat request forms, the shares aredematerialized and confirmation through electronic mode is sent. If the demat request number is

not received within a period of 30 days, the duly transferred share certificate is dispatched to the

transferee.

Canara Bank Share holding pattern are as below:

Government of India Rs.300.00 Crs 73.17%

Mutual Funds/Other Institutions Rs. 23.56 Crs 5.75%

Awards/Accolades:

Received during 2007-08

• First National Award, instituted by the Ministry of Micro, Small & Medium

Enterprises, Govt. of India for 'Excellence in Micro & Small Enterprises (MSE) Lending' for

2006-07.

• 'Golden Peacock Award for Corporate Social Responsibility' for the year

2007. Canara Bank is the first PSB to receive the award since its institution in the year 1991.

• ‘Golden Peacock National Training Award-2007’, instituted by the Institute of

Directors, New Delhi, a pioneer in Quality Revolution.

• Conferred the Business Superbrands Status for 2008.

• 'The Organization of the Year Award- for PR Excellence', instituted by Public

Relations Council of India.

• Excellence in the field of Khadi & Village Industries in South Zone for the year

2006-07, instituted by Khadi & Village Industries Commission, Ministry of Micro, Small &

Medium Enterprises, Government of India.

Received during 2008-09

• Conferred 'First Rank' in India's Best Banks awards under the category

'Strength and Soundness' for 2006-07 by a survey conducted by Ernst & Young.

Page 32

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 32/69

• Best Performing Bank under Rural Employment Generation Programme,

(REGP) of Khadi and Village Industries Commission (KVIC), in South Zone for the year 2007-

08, instituted by the Ministry of MSME, Government of India.

• Golden Peacock National Training Award 2008 for excellence in training.

• Global HR excellence in Training, an award conferred by the Asia Pacific HR

Congress, the largest rendezvous of HR Professionals, at its Employer Branding Talent

Management Congress held on 22nd and 23rd August 2008, Delhi.

• Best Corporate Social Responsibility Practice Award, instituted by BSE,

NASSCOM and Times Foundation & The Bank won two Silver Corporate Collateral Awards for

Best Corporate Ad in the Print Media and Best Corporate Film on Corporate Social

Responsibility at the Public Relations Council of India Awards 2009.

Product Information

Page 33

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 33/69

Product Information

Deposits: - CANARA Bank offers wide variety of deposit products to suit customer’s

requirements. Coupled with convenience of networked branches, over 1800 ATMs and facility of

E-channels like Internet and Mobile Banking, CANARA Bank brings banking at their doorstep.

Customers have to select any of their deposit products and provide details online and bank’s

representative will contact them for account opening.

1. Savings Account: CANARA Bank offers its customers

power packed Savings Account with a host of convenient features and banking channels

Page 34

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 34/69

transact through.

✔ Debit-cum-ATM card

✔ Value Added Saving Account

✔ Internet Banking

✔ Credit Cards.

✔ Phone Banking

✔ Anywhere Banking

✔ Standing instructions

✔ Nomination facility

✔ Doorstep service

2. Fixed Deposit: It ensures safety, flexibility, liquidity

and returns!!!! CANARA Bank offers its customers a combination of unbeatable features of

the Fixed Deposit.

✔ Wide range of tenures

✔ Choice of investment plans

✔ Partial withdrawal permitted

✔ Safe custody of fixed deposit receipts

✔ Auto renewal possible

✔ Loan facility available

✔ Easy Deposit:

✔ Free Debit

Page 35

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 35/69

✔ ATM card

✔ No need to open a Savings account.

✔ Options of Easy Withdrawal and Easy Loan

✔ Wide range of tenures

✔ Auto renewal possible

✔ Loan facility available

3. Recurring Deposit: When expenses are high, people

may not have adequate funds to make big investments. But simply going ahead without

saving for the future is not an option for them. Through CANARA Bank Recurring Deposit

they can invest small amounts of money every month that ends up with a large saving on

maturity. So they enjoy twin advantages- affordability and higher earnings.

✔ Encourages savings

✔ Loans against deposits available

✔ High rates of interest

✔ Non-applicability of Tax Deduction At Source

✔ The minimum balance of deposit is Rs.1,000p.m. and thereafter, in multiples of

Rs.100

✔ The minimum period is 6 months and thereafter, in multiples of 3 months.

4.

Page 36

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 36/69

Salary Account: CANARA Bank Salary Account is a benefit-rich payroll account for

Employers and Employees.

✔ Easy disbursements of salaries

✔ Free 24 hour Phone Banking

✔ Free Internet Banking

✔ Reduces paperwork

✔ Saves remittance costs

✔ Employees receive instant credit of salaries

✔ Defense Banking Services

✔ All benefits of being an CANARA Bank account holder

✔5. Senior Citizen Services: As a person reaches the age toretire, he does have certain concerns … whether his hard earned money is safe and secure

…

✔ Whether his investments give him the kind of returns that he needs. That's why

CANARA has an ideal banking service for those who are 60 years and above. The Senior

Citizen Services from CANARA Bank has several advantages that are tailored to bring

more convenience and enjoyment in their life.

✔ Higher Interest Rates

✔ Special Demand Loans against deposit

✔ Free collection of outstation cheques drawn on our locations

✔ Debit-cum-ATM card

✔ Internet Banking

✔ Phone Banking

✔ Anywhere Banking

Page 37

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 37/69

✔ Nomination facility

6. Kids Account: It's really important to help children

learn the value of finances and money management at an early age. Banking is a

✔ Serious business, but the bank makes banking a pleasure and at the same time children

learn how to manage their personal finances.

✔ Secure child’s future

✔ Teaches the child to be financially responsible and independent

✔ For children aged 1-18 years

✔ Choice of saving bank account, fixed deposit account or recurring deposit account

✔ Minimum balance at Rs.500 per quarter from savings bank

✔ Free personalized cheque book

✔ Free Domestic Debit Card for children above 10 years

✔ Facility to invest in GOI Relief Bonds and Mutual Funds

✔ Free Internet Banking

✔ Facility of shopping at Young Stars very own shopping page

7. Loans:

A loan is a type of debt. Like all debt instruments, a loan entails the redistribution of financial

assets over time, between the lender and the borrower.

Page 38

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 38/69

OBJECTIVES

OBJECTIVES

• To know various kind of loans offered by canara bank.

• To know the terms & conditions relating to loans.

• To know the economic mode of granting loans.

Page 39

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 39/69

• To conduct EDPs and Skill development programmes (EDPs) for different target groups.

• To assist potential Women Entrepreneurs to start/establish/run an Enterprise

professionally.

• To guide existing entrepreneurs to improve the working and modernization of an existing

unit.• To co-ordinate with Government/Voluntary organizations engaged in promoting

entrepreneurship among women.

• To offer counseling services to the Entrepreneurs existing as well as new.

• To assist in the formation of self-help groups.

• To assist the customers for different financial products in the market.

• To offer the new loan facilities to their customers and guide properly time to time.

• To help their customers time to time relating to new policies and guidelines of the

Reserve Bank of India which is opted in the bank.

• To develop the proper co-ordination between all the customers of the bank and the sent

the appropriate information.

NEED FOR THE STUDY:

• Banks are operating in the oligopolistic market condition with the sellers selling more or

less same products but with some differentiation. Since, the prices are determined by the

market forces, the only way banks can make profit is by providing differentiated products

and services. The need for doing this project was to analyze the strategies employed by

banks to provide d To find out the effectiveness of advertising campaign of banks.

• To identify the competition in the banking industry.

Page 40

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 40/69

• To analyze the satisfaction level among the bank’s customers with regard to the products

and services offered to them.

• To find out awareness level in customers regarding the services of banks.

• To find out the effectiveness of advertising campaign of banks.

• To identify the competition in the banking industry.

• To analyze the satisfaction level among the bank’s customers with regard to the products

and services offered to them.

• To analyze the paying capacity of the customers of the bank.

SCOPE:

The research zone selected by me was Khanna (Punjab).

FEATURES OF KHANNA:

– Population: - rich crowded city.

– Geographical Location: - Khanna near to Mandi gobindgarh is an industrial area in

Punjab. It is surrounded by many industries around it.

Rationale:

The rationale of doing this project was to get the clear understanding of the marketing strategy

for selling various financial products by banks and develop analytical skills to analyze the

performance and productivity of public sector and private sector banks through ratio analysis.

The scope of research was limited to only Khanna. Khanna is a small city. Thus, the analysis can

be biased and inaccurate.

• Because of scope being limited to Khanna the conclusions drawn may not hold true for

other areas.

• The reluctance of the respondents to fill up the questionnaires was also a limitation.

Page 41

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 41/69

• Non-availability of the financial data of other private sector and public sector banks for

the whole year on Internet posed a limitation in calculating and comparing ratios.

• The scope of learning in banking sector is very vast. But, because of time constraint the

focus of knowledge was limited.

RESEARCH

AND

METHODOLOGY

Page 42

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 42/69

RESEARCH AND METHODOLOGY

RESEARCH For doing the research on this project, I did the analysis of marketing of various

financial products like savings account, fixed deposit account; demat account, loans, insurance

etc. in CANARA Bank .

A similar analysis was also done in other private sector banks like ICICI and public sector banks

like State Bank of India.

After that a comparative analysis by the means of pie chart and bar diagram was done between

CANARA Bank v/s other Pvt. Sector Banks.

I have also studied financial statement of CANARA Bank and compared it with other private

sector banks and public sector banks, which gave an idea of the productivity and performance of

these banks.

SAMPLE SELECTION CRITERIA:

The sampling technique used for my research was Probability Sampling Technique i.e. number

of items were selected at random.

DATA COLLECTION METHOD:

Primary data: Primary data was collected by the means of questionnaires which contained all

closed ended questions except one open ended question for critical comments, if any. Besides

this, personal interviews from the staff & customers of CANARA Bank.

Secondary data: For the purpose of doing study of financial statement and other information,

secondary data was collected from Internet, old records of the bank.

Sample size:

Page 43

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 43/69

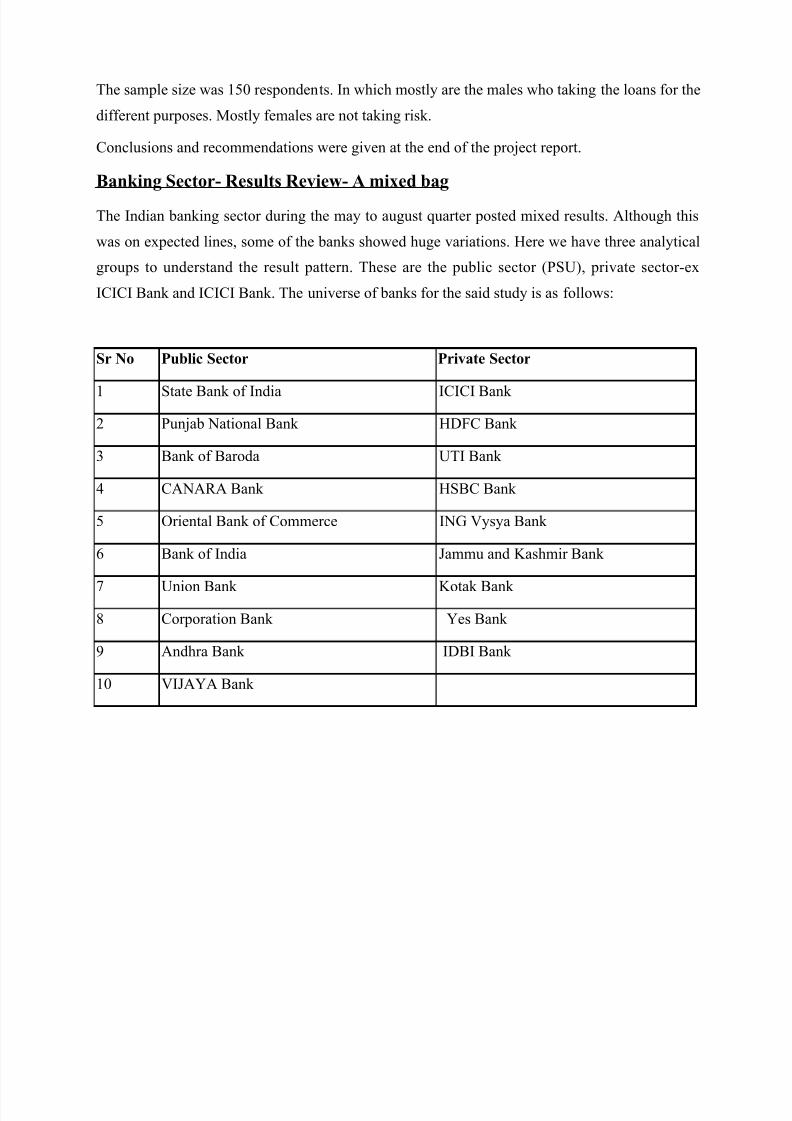

The sample size was 150 respondents. In which mostly are the males who taking the loans for the

different purposes. Mostly females are not taking risk.

Conclusions and recommendations were given at the end of the project report.

Banking Sector- Results Review- A mixed bag

The Indian banking sector during the may to august quarter posted mixed results. Although this

was on expected lines, some of the banks showed huge variations. Here we have three analytical

groups to understand the result pattern. These are the public sector (PSU), private sector-ex

ICICI Bank and ICICI Bank. The universe of banks for the said study is as follows:

Sr No Public Sector Private Sector

1 State Bank of India ICICI Bank

2 Punjab National Bank HDFC Bank

3 Bank of Baroda UTI Bank

4 CANARA Bank HSBC Bank

5 Oriental Bank of Commerce ING Vysya Bank

6 Bank of India Jammu and Kashmir Bank

7 Union Bank Kotak Bank

8 Corporation Bank Yes Bank

9 Andhra Bank IDBI Bank

10 VIJAYA Bank

Page 44

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 44/69

DATA ANALYSIS

&

INTERPRETATION

DATA ANALYSIS & INTERPRETATION

Q1. Are you interested in taking loan?

Response No. of response Percentage %

Yes 70 67

No 30 33

Page 45

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 45/69

Total 100 100

Interpretation:

Under this, 100 peoples who are agreed to take loan for the different jobs, mostly all are the

males who taking the risk and pay the install of loan in time. But 50 peoples can not take loan

due to heavy interest rates and paying capacity, risk factor, mostly these are all females.

Q2. What kind of loan you want to avail?

Response No. of response Percentage %

House loan 15 15

Educational loan 35 35

Personal loan 21 21

Vehicle loan 29 29

Total 100 100

Interpretation:

15% respondents want to avail house loan, 35% educational loan, 21%personal loan & 29%

vehicle loan.

Q3. For how many years you want to avail loan?

Page 46

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 46/69

Response No. of response Percentage %

Less than 1 Year 15 15

1 to 3 Year 35 35

3 to 5 Year 21 21

More than 5 Year 29 29

Total 100 100

Interpretation:

15% respondents want to avail loan less than 1 year, 35% avail loan for 1 to 3years,

21%respondent avail loan for 3 to 5 years & 29% avail loan for more than 5 years.

Q4. Which Bank is preferred by you for making transactions relating to loans and advances?

Banks Public Sector Bank Private Sector Banks Co-operative Sector Banks

No. of

respondents

60 25 15

INTERPRETATION:

The figures show that most of the respondents are transacting with the nationalized banks. The

sum total is not 100(sample size being 100) because of 3 respondents having banking

relationship with more than one bank. Other private banks include ICICI Bank, Co-operative

Banks etc. While nationalized banks include State Bank Of India, Bank Of Baroda, Vijaya Bank,

Punjab National Bank, Canara Bank, Corporation Bank etc.

Q5. Which class avail the maximum bank services?

Occupation Business Service Self-employed Others

Page 47

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 47/69

No. of respondents 35 38 11 16

INTERPRETATION:

The no. of respondents under service and business class was almost same. Others group includes

students and housewives etc. who do not fall under any other category. The no. of respondents in

self-employed group was the least. This is due to the randomly selected data.

Q6. What kinds of accounts are used by customers according to their income?

INTERPRETATION:

Majority of the respondents fall under the middle-income group category. Most of these

respondents were either businessmen or service class people. The respondents under the category

of nil income were students and housewives. They usually operate their account on the basis of

their savings and other sources.

Monthly Income (Rs.) 5,000-10,000 10,000-20,000 20,000 & above Nil

No. of respondents 27 46 15 12

Page 48

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 48/69

Q7. How you prefer to pay your installments ?

Response No. of response Percentage %

MONTHLY 25 25

QUARTERLY 40 40

ANNUALLY 35 35

Total 100 100

INTERPRETATION:

The no. of respondent given in the question, out of which 25% respondent pay the installment

monthly, 40% prefers quarterly and 35% respondent pay the installment yearly. According to

requirement every respondent have different categories.

Comparison between CANARABank v/s other private sector banks v/s public

sector banks:

The PSU sector showed strong core income growth due to robust business. Although interest

income did not show a great picture, interest on advances figure gave a better indication. Despite

no incremental growth in interest on investments, interest income still managed to post decent

growth number on back of good growth in interest on advances. Employee expenses continued to

grow at steady rate of around 17%. This figure is inclusive of the VRS expenses. The next fiscal

figure is expected to show a lower growth, as most of the PSU banks are in their last year of

VRS expenditure amortization. Provisioning for the PSU banking group registered a huge rise as

Page 49

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 49/69

most of the top PSU banks refrained from transferring securities to the held to maturity (HTM)

basket in the September quarter.

The private sector banks stood out among the sector during the December quarter results. While

most of the PSU peers posted negative growth in profits, the private sector peers managed to post

a decent profit growth of 13%. The private sector banks posted a strong net interest income

growth through higher level of growth in interest income. Drop in interest cost for CANARA

Bank has kept the private bank groups’ interest cost with a marginal growth. Operating expenses

for the private sector banks continue to grow at a much faster rate, at around 30%. The private

sector banks have market linked pay structure for the employees apart from the strong thrust on

retail lending which increases operating cost.

Contrary to PSU peers, the private sector banking groups recorded fairly normal provisioning

expenditure. Few banks in the PUBLIC ex CANARA Bank registered a drop in tax provisions.Most of these banks are those with negative profit growth, trying to shore up profits.

The net interest income of CANARA Bank increased by 51.2%, which is more than other private

and public sector banks. Though interest income of Private Banks excluding CANARA Bank

was more than PSU Banks and HDFC Bank, the net interest income declined due to increase in

interest expenses. Because of increase in net interest income of CANARA Bank, it recorded

more growth in total income than that of other banks. PUBLIC Banks excluding CANARA Bank

showed very little growth in operating profit because of high growth in operating expenses that is

mainly due to employee’s pay structure and thrust on retail lending. The growth was almost

equal in CANARA Bank and Other Banks.

PAT decreased in PSU Banks because of considerable increase in provision and contingencies. It

increased slightly in Pvt. Banks. It increased by 17.6% in CANARA Bank due to decrease in

provision and contingencies

Interest on advances is a major source of income in banks. It increased almost equally in

CANARA Bank and Other Banks. But, it increased more in Public sec. Banks ex-CANARA

Bank. Overall, it can be concluded that the performance of CANARA Bank is better than

Private Banks.

Ratio analysis:

PSU Banks

Pvt Banks ex-ICICI

Bank

CANARA Bank

Page 50

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 50/69

Period to 12/04 12/03

Growt

h 12/04 12/03 Growth

12/04 12/03 Growth

(Figures in %) (3) (3) (%) (3) (3) (%) (3) (3) (%)

Other Income/ Total

Income 32.6 33.3 (0.7) 32.6 36.2 (3.6)

54.9 62.6 (7.7)

Interest Expense/

Interest Income 55.1 59.8 (4.8) 53.7 55.6 (1.9)

69.2 77.9 (8.7)

Cost / Income 46.0 46.0 (0.1) 48.0 42.5 5.5 52.5 49.7 2.8

Employee Cost/ Total

Cost 67.3 68.4 (1.0) 32.6 34.3 (1.7)

21.6 22.4 (0.8)

Ratio analysis shows the same trend for private banks as their PSU counterparts, the striking

difference has been the cost to income ratio. Private Banks due to a rise in their operating

expense reported a rise in cost to income ratio. Most of the rise has come through non-employee

costs, which are a result of a greater thrust on retail products, which require a higher publicity

budget and increased investment in infrastructure. The decline in interest expense to total income

in CANARA Bank was more which shows that it has reduced its expenses in total income.

Though other banks also reported the same, but it was less than CANARA Bank.

SWOT ANALYSIS

Page 51

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 51/69

SWOT ANALYSIS

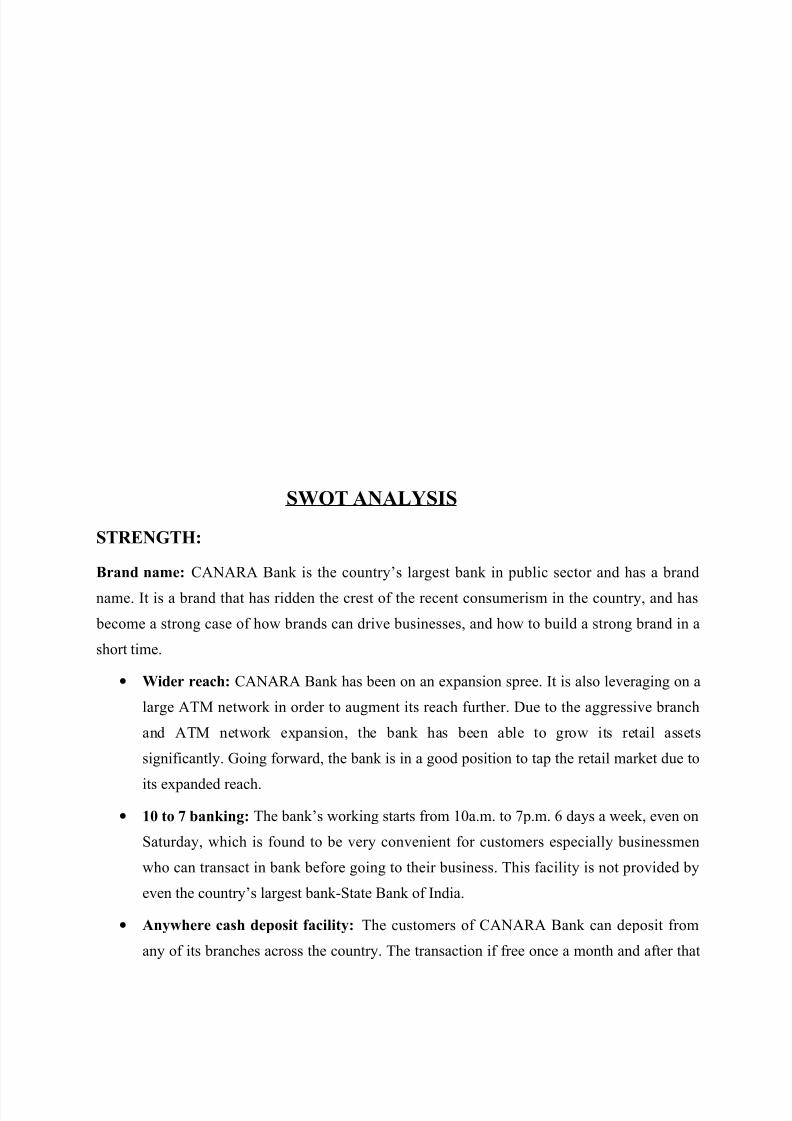

STRENGTH:

Brand name: CANARA Bank is the country’s largest bank in public sector and has a brand

name. It is a brand that has ridden the crest of the recent consumerism in the country, and has

become a strong case of how brands can drive businesses, and how to build a strong brand in a

short time.

• Wider reach: CANARA Bank has been on an expansion spree. It is also leveraging on a

large ATM network in order to augment its reach further. Due to the aggressive branch

and ATM network expansion, the bank has been able to grow its retail assets

significantly. Going forward, the bank is in a good position to tap the retail market due to

its expanded reach.

• 10 to 7 banking: The bank’s working starts from 10a.m. to 7p.m. 6 days a week, even on

Saturday, which is found to be very convenient for customers especially businessmen

who can transact in bank before going to their business. This facility is not provided by

even the country’s largest bank-State Bank of India.

• Anywhere cash deposit facility: The customers of CANARA Bank can deposit from

any of its branches across the country. The transaction if free once a month and after that

Page 52

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 52/69

nominal charge is to be paid, which is debited automatically from the amount being

deposited. The charges are negligible.

• Efficient services: The bank deserves award for its efficient services from opening a

simple saving account to providing other services like portfolio management and demat

services. Customers are provided with hand-to-hand free kit of cheque book and ATM

cum debit card. The bank also provides the facility of same day DD clearance to its

customers.

• Cash Management Service (CMS): The current account holders are provided CMS

facility in which all the cheques and DD are cleared the same day even if the cheques are

out station. This facility is not meant for other account holders.

• Courteous services: The bank not only provides efficient but courteous services too.

They are treated with due courtesy in every branch of CANARA Bank which gives its

customers a feeling of comfort and satisfaction with all the queries being handled within

the branch itself.

• Focus on customer convenience: The bank provides host of services under one roof.

Mutual funds, trading in shares etc. to name a few.

WEAKNESS:

• Strict guidelines: Some of the guidelines are considered strict and not suitable for every

person as per the opinion of customers. For example: for opening savings account in

CANARA Bank, the person has to deposit a minimum amount of Rs.3000 and quarterly

average balance has to be Rs.2700. This is not considered justified by some customers

who have less income and savings and cannot maintain such balance. This is also one of

the reasons of closing of the account by the customers.

• Focus on class banking: The bank is mainly focused on class banking and not mass

banking. But, the bank is witnessing mass banking in some locations. Thus, it is

concentrating on eliminating the customers who are not giving any profit to the bank byimposing charges, the target being class people with high margins and savings.

• Less sales force: The bank is having less force than it needs to create more awareness

among general public. Increase in the number of sales team can help the bank in

expanding its network and customer base.

OPPORTUNITIES:

Page 53

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 53/69

• Growing niche market: There is the opportunity to explore the growing niche market in

rural and semi-urban areas.

• Increase in income: The rising income of people with the economy being growing is

also an opportunity to exploit. With increase in income, savings also increase and thus

leading to increase in investment also. So, this opportunity can be exploited fully to

increase the spread.

• Growing customer awareness: These days, customers are getting more and more aware

about the products of banks. They are now in a better position to decide which bank to

choose to deal with. They want not just variety of services, but efficiency in delivering

those services, which can give them satisfaction. CANARA bank being widely known for

its efficiency in services can play on its strength and exploit this opportunity to the

fullest.

• Advancing technology: This sector is related with the technology. With the

advancement in technology like future ATMs by using biometrics recognizing the

customers by their face, voice or fingerprints can prove to be an opportunity. By imbibing

such kinds of technological changes at the earliest, the bank can become NO.1 in

changing technology with change in time.

• Shift in preference of customers: The customers of many private banks are now

changing their preference towards Nationalised banks because of some loopholes in

• Nationalized banks and filling of unsatisfied needs of customers by private sector banks.

CANARA Bank with its brand name and wider reach can be the beneficiary because of

this shift.

• Changes in government’s policies: The recent change in the government’s policies also

provides opportunities.

THREAT:

• Competition: Competition in banking sector is growing at a rapid pace with the

economy becoming liberalized and opening up of this sector to FDI. Foreign entrants are

giving a challenge to domestic banks to provide something different to its customers.

This poses a threat to banks and if not considered seriously by any bank, can become the

reason for decline in the customer base.

Page 54

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 54/69

LIMITATIONS

Page 55

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 55/69

LIMITATIONS

Due to inflexibility in account opening it is difficult to convince customers.

No authentic evidence of customers is found.

No special facilities of loans to businessman are given in semi rural or rural area.

The facility of commercial loans and working capital finance also not provided.

The bank is not tapping untapped areas.

Lack of communication & delivery channels.

Lack of social banking.

Very less loan schemes for educated unemployed, women and for the education of poor

children.

Page 56

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 56/69

Loans are not provided without security.

Loans are not provided at ease lot of paper work & documentation is involved.

The time bound period is the major limitation in research projects.

RECOMMENDATIONS

RECOMMENDATIONS

Page 57

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 57/69

Recommendations: After conducting the survey, following recommendations can be

suggested to the bank. Hope they will help the bank in achieving excellence.

More customer convenience: Flexibility in account opening procedure should be

introduced on presenting authentic evidences by the customers. For example- accounts should be

opened with cash also and the limit of quarterly average balance should be decreased.

Services for businessmen: The bank should provide special facilities to businessmen in

rural and semi-urban areas also. For example- the facility of commercial loans and working

capital finance should be provided.

Rural Banking: The vast scope of rural banking in nearby places of khanna should be

explored through provision of crop loans, loans for agricultural equipments etc. The bank can

also tap the untapped potential for bank’s presence by establishing more communication and

delivery channels

Social Banking: The bank can promote social banking through provision of loan schemes to

educated unemployed, women and for the education of poor children. Such loans can be

provided without any security and at lower rates of interest.

Page 58

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 58/69

SUGESSTIONS

SUGESSTIONS

The cutthroat competition of 21st century demands not just a satisfied but delighted customer as a

key to success in a service industry. As per the survey conducted, customers’ attitude is changing

with the change in preference from nationalized to private sector banks because of wide

difference in the efficiency of services provided. Long waiting lines, discourteous employees’

attitude, favoritism, lack of attention towards the convenience and comfort of customers are the

loopholes that came in light during the data collection process. Many Indian public sector banks

have even ignored the technological change, and have acceded market share to foreign banks and

Page 59

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 59/69

new private banks. While on the other hand, CANARA Bank’s easy access in terms of wider

reach, healthy organizational culture, courteous behavior of employees, customer focus and

embracement of technology have been repeatedly appreciated. Also, improved advertising

efforts, embracement of latest technology, more and more awareness about internet banking thus

facilitating customers while providing solutions at their convenience and easy reach and anapproach to target the lower income group constituting about 30% of the city population can

serve to be the milestones in CANARA’s success story..

BIBLIOGRAPHY:

Page 60

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 60/69

BIBLIOGRAPHY :

1.BOOKS AUTHORS

Kotler, Philip, Marketing Management, 12th edition, Prentice Hall of Private Ltd, 2007

Keller, Kevinlane, Marketing Management, 12th edition, Prentice Hall of Private Ltd, 2007

Kothari, C.R., Research Methodology, 2nd edition, New Age International(P) Ltd, 2004

2. NEWS PAPERS

Times of India, Date:- 23-06-09, Page no.15.

Financial Express, Date:- 29-06-09, Page no.17

Economic Times, Date:-15-07-09, Page no.16

Page 61

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 61/69

Hindustan Times, Date:- 21-07-09, Page no.17

3. WEBSITES

www.canarabank.com

www.financialexpress.com

www.financialservices.com

www.financialtimes.com

www.financialterms.com

QUESTIONNAIRE

Page 62

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 62/69

QUESTIONNAIRE

Dear Sir/Madam

I am a student of Punjab business school, Chunni kalan, Disst. Fathegarh shahib

And presently doing a project on “A Study of Loans & Advances offered at Canara

Bank.” request you to kindly fill the questionnaire below and assure you that the data generated

shall be kept confidential. ”. Please co-operate to fill this questionnaire.

Q1. Are you interested in taking loan?

(a) If YES ------------- ( refer to Q3)(b) If NO -------------

Q2. Which Bank you prefer while taking loan?

(a) Public sector bank ----------(b) Private sector bank ----------

Q3. What kind of loan you want to avail from the bank?

(a) House loan ------------(b) Educational loan ---------(c) Personal loan ------------(d) Vehicle loan ------------

Page 63

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 63/69

Q4. How much amount you required as loan?

(a) Rs 100000 to 500000 --------------(b) Rs 500000 to 1000000 -------------

(c) More than above ------------

Q5. For how many years you want to avail loan?

(a) 1 to 3 years -------------(b) 3 to5 years -------------(c) 5 to 10 years -----------

Q6. What kind of documents you should give as security to banks?

(a) Salary slips -----------(b) Registries ------------

Q7. How you prefer to pay your Installments?

(a) Monthly installments ------------(b) Quarterly installments ----------(c) Annually installments -----------

Q8. IN what ways you show your residential proof to bank while taking loan?

(a) I Card -------------(b) Voter id ----------(c) Electricity bill ---------(d) PAN NO -------------

Page 64

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 64/69

Q9. Who is giving guarantee on your behalf to bank?

(a) Person within same bank ------------(b) Any other person --------------------

(c) Any branch related to bank------------

Q10. Are you satisfied with the terms & condition relating to loans provided by the bank to you?

(a) Fully satisfied -------------(b) Partially satisfied --------------(c) Unsatisfied -------------

Q11. Any Suggestions & Recommendations ---------------------------

BACKGROUND DATA

1. Name _________________________________________

2. Sex: (a) Male (b) Female

Page 65

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 65/69

3. Age: (a) Below 18 (b) 18-35

(c) 35-50 (d) Above 50

4. Education: (a) Under Graduate (b) Graduate

(C) Post Graduate

5. Occupation: (a) Service (b) Profession

(c) Business (d) Others

6. Income: (a) Less than Rs. 50,000

(b) Rs. 50,000 to 1,50.000

(c) Rs. 1,50,000 to 3,00,000

(d) Rs. 3,00,000 & above

7. Address __________________________________________

__________________________________________

__________________________________________

8.Phone no. __________________________________________

Page 66

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 66/69

*Thanks for your valuable time and co-operation*

Financial Statements

Page 67

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 67/69

BALANCE SHEET OF CANARA BANK

Balance Sheet of Canara Bank (In Crores)

Mar ' 09 Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05

Sources of funds

Owner's fundEquity share capital 410.00 410.00 410.00 410.00 410.00

Share application money - - - - -

Preference share capital - - - - -

Reserves & surplus 9,629.61 7,885.63 7,701.11 6,608.86 5,582.04

Loan funds

Secured loans - - - - -

Unsecured loans 1,86,892.51 1,54,072.42 1,42,381.45 1,16,803.23 96,908.42

Total 1,96,932.12 1,62,368.06 1,50,492.57 1,23,822.09 1,02,900.46

Uses of fundsFixed assets

Gross block 4,440.07 4,254.33 4,056.39 1,718.60 1,577.53

Less : revaluation reserve 2,168.16 2,204.86 2,242.87 113.38 116.92

Less : accumulated depreciation 1,510.61 1,337.46 1,195.04 1,030.13 904.72

Net block 761.30 712.01 618.48 575.09 555.90

Capital work-in-progress - - - - -

Investments 57,776.90 49,811.57 45,225.54 36,974.18 38,053.88

Net current assets

Current assets, loans & advances 4,060.26 2,684.17 2,994.53 2,909.95 2,488.34Less : current liabilities & provisions

13,488.91 13,438.55 11,651.25 8,860.57 7,173.63

Total net current assets -9,428.66 -10,754.38 -8,656.72 -5,950.62 -4,685.29

Miscellaneous expenses notwritten

- - - - -

Total 49,109.55 39,769.21 37,187.30 31,598.66 33,924.48

Page 68

8/6/2019 Aditya Project Final Ok

http://slidepdf.com/reader/full/aditya-project-final-ok 68/69

Profit & Loss account of Canara Bank

Profit loss account (Rs Crores)

Mar ' 09 Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05

Income