36

Adoption of Carbon Credit Programs among SFI Participants in Maine: A Study by Keeping Maine’s Forests February, 2017

Adoption of Carbon Credit Programs among SFI Participants in Maine:

A Study by Keeping Maine’s Forests

February, 2017

i

Acknowledgements This study was conducted under a grant to Keeping Maine’s Forests (KMF) from the Sustainable Forestry

Initiative, Inc.’s Conservation Grants program, with additional funding from the Horizon Foundation. Alison

Truesdale, KMF Coordinator, was the principle author and conducted the survey of Maine SFI participants.

However, the study’s Advisory Panel was instrumental in insuring the accuracy and balance of the paper; KMF is

grateful for their expertise, time and contributions.

Advisors Mark Berry, M.S.; President and CEO, Schoodic Institute.

Mark leads Schoodic Institute at Acadia National Park, a nonprofit dedicated to advancing ecosystem science

and learning for all ages. From its Acadia National Park campus, the Institute engages scientists, educators,

students, and the public in research and learning. Schoodic Institute’s programs build understanding and

appreciation for science and the natural world and contribute to addressing complex challenges in a changing

environment. Mark holds a Master’s of Science degree in Ecology and Evolutionary Biology from the University

of Colorado and a bachelor’s degree in Environmental and Evolutionary Biology from Dartmouth College. He

formerly served as Executive Director of Downeast Lakes Land Trust, where he led landscape scale forest

conservation projects, managed a 34,000‐acre Community Forest, and implemented one of the nation’s first

carbon offset projects.

Ivan Fernandez, Professor in the School of Forest Resources, Climate Change Institute, and

School of Food and Agriculture at the University of Maine

Ivan J. Fernandez is Professor in the School of Forest Resources, Climate Change Institute, and School of Food

and Agriculture at the University of Maine. He was made a Distinguished Maine Professor in 2007,

CASE/Carnegie in Washington DC named him Professor of the Year for Maine in 2008, and was named a fellow

in the Soil Science Society of America in 2010 among other awards. He has served on U.S. Environmental

Protection Agency Science Advisory Board committees in Washington DC since 2000, he currently chairs a panel

of the EPA Clean Air Scientific Advisory Committee (CASAC) that is evaluating the secondary National Ambient

Air Quality Standards in the Clean Air Act for sulfur and nitrogen oxides, he represents the University of Maine in

the USDA Northeast Climate Hub, and has been involved in leading the Maine’s Climate Future assessments in

2009 and 2015. He is a soil scientist by training, with a research program that focuses on the biogeochemistry of

ecosystems in a changing physical and chemical climate.

Sherry Huber, Maine TREE Foundation and KMF Steering Committee member

Sherry is a founder of Keeping Maine’s Forests and serves on the Steering Committee. She is the former

Executive Director of the Maine Waste Management Agency, served in the Maine House of Representatives for

six years, and is a Corporator of Maine Health. Sherry chaired the board of Mainewatch Institute and is a former

trustee of the College of the Atlantic. She is a former director of The Nature Conservancy, the Land Trust

Alliance and NatureServe and currently serves on the Council of Advisors of the last two. She is a former

President and current member of the Forest Society of Maine and a member of the University of Maine School

of Law Board of Visitors, the Leadership Council of the Yale School of Forestry and Environmental Studies and

Maine Conservation Voters. She is an Advisory Trustee of the Maine Audubon Society and an Honorary Director

of the Friends of Casco Bay.

George Jacobsen, Ph.D.; Climate Change Institute, Maine State Climatologist and Professor

Emeritus at the University of Maine

ii

George L. Jacobson is Professor Emeritus of Biology, Ecology, and Climate Change at the University of Maine.

Since his arrival in Maine in 1979, Dr. Jacobson has been a member of the Climate Change Institute, and was

Director of the Institute for nearly a decade. His scientific research has focused on long‐term climate variability

and specifically on forest responses to climate changes during the past 60,000 years. Prof. Jacobson’s projects

have included sites in North America, South America, and Europe. Among other things, he has served as an

outside advisor on climate to the European Science Foundation, and to the Finnish Academy of Sciences. From

2008 to 2014, he had the honorary designation of Maine State Climatologist.

Professor Jacobson joined the faculty of the University of Maine in 1979 after three years working in the United

States Senate in Washington, D.C., first as a AAAS Congressional Science Fellow and then as a staff scientist for

the U.S. Senate Committee on Environment and Public Works. He was born and raised in Rapid City, South

Dakota, and earned a B.A. in 1968 from Carleton College, and a Ph.D. in 1975 from the University of Minnesota.

From 1968‐1970 he served as a medical specialist in the United States Army.

Dylan Jenkins, M.S.; Vice President of Portfolio Development, Finite Carbon

For over 20 years, Dylan has worked with America’s private forest landowners to make sustainable forestry a

more feasible proposition. Dylan is currently vice‐president of portfolio development for Finite Carbon and

leads their sales, marketing, and client relations activity. Before focusing on forest carbon markets, Dylan

directed The Nature Conservancy’s Forest Conservation Program in Pennsylvania where he developed TNC’s

Working Woodlands program, and earlier directed the Virginia Forest Landowner Education Program at Virginia

Tech. He was the 2006 SAF National Young Forester of the Year, served as the Virginia SAF chair, was a member

of the SAF National Committee on Forest Policy, and co‐chaired the SAF Certification Review Board. Dylan has

been published in Science, the Journal of Forestry, the Journal of Forest Economics, Forest Landowner, and the

ACF Consultant. He is a member of the Association of Consulting Foresters, is an SAF Certified Forester and has

a B.S. in Forest Management from Clemson and an M.S. in Forest Economics from Virginia Tech.

Kenneth M. Laustsen, M.F.; Biometrician, Maine Forest Service

Ken has been the Biometrician for the Forest Health and Monitoring Division of the Bureau of Forestry since

1999. Previously, he was Woodlands Analyst, Operations Forester, and staff forester for Great Northern Paper

Company in Millinocket (1979‐1999).

He has been a member of the Society of American Foresters since 1974, was named an SAF Fellow in 2008,

served as an SAF Forest Technology School Accreditation Committee member from 2013 to 2016, and as an SAF

Certification Review Board Committee member from 2007 to 2012.

Ken won the United States Forest Service Director’s Award for Excellence in 2001. He has been a Member of the

USDA Forest Service, Forest Inventory & Analysis, Techniques Research Band since 2008, and a was a member of

the Statistics Band from 2002 to 2007. Ken earned a B.S. in Forest Management in 1974 and an M.F. in

Forest Management in 2010, both from the University of Maine.

John McNulty, President and CEO, Seven Islands Land Company

John McNulty is President and CEO of Seven Islands Land Company and its subsidiaries based in Bangor, Maine.

Seven Islands manages 815,000 acres of forestland for the Pingree family and an additional 350,000 of investor

owned timberland through Seven Islands’ subsidiary Orion Timberlands. All the lands under management are

certified by SFI and the Pingree ownership is dual certified by SFI and FSC. Seven Islands’ owns and operates a

hardwood sawmill, a chipping facility and a hardwood flooring company all located in northern Maine.

iii

John started his career with Seven Islands in 1978 and was named President in 2008. He has been active in the

certification arena, both Forest Stewardship Council (FSC) and Sustainable Forestry Initiative (SFI) since 1994

when John was project leader for the Pingree family lands certification, which were the first certified large

landholdings under the FSC standard. John has served on the Northeast Standards Committee, several national

FSC working groups and has been a vocal advocate of certification since its inception.

John has been active in forestry circles in Maine and nationally, having served on Maine’s licensing board and

the Society of American Foresters, holding many elected offices in New England as well as representing New

England and NY as District Representative on SAF’s National Council. He earned his B.S. in forest management

from the University of Maine in 1978 and is a licensed forester in Maine.

David Publicover, D.F., Senior Staff Scientist/Assistant Director of Research, Appalachian

Mountain Club

Dr. David Publicover is a Senior Staff Scientist and Assistant Director of Research at the Appalachian Mountain

Club, where he has worked since 1992. His primary responsibility is to provide scientific information and

analyses in support of AMC's mission in forest ecology and management. He oversees AMC's conservation GIS

program which conducts regional landscape assessments to evaluate conservation opportunities and priorities,

as well as the impacts of specific development proposals. He has served on numerous public policy committees

and working groups in the areas of sustainable forestry, ecological reserve design and management and energy

facility siting. He oversees forest management planning and FSC certification on AMC's 75,000 acres of forest

land in Maine and led the development of a Climate Action Reserve forest carbon offset project on a portion of

these lands. Dave holds a BS (Forestry) from the University of New Hampshire, an MS (Botany) from the

University of Vermont and a DF (Forest Ecology) from the Yale School of Forestry and Environmental Studies.

Tom Rumpf, M.F.; former Conservation Strategy Advisor of The Nature Conservancy in Maine

and KMF Steering Committee chair

Tom Rumpf is the former Conservation Strategy Advisor for The Nature Conservancy in Maine, where he worked

in several capacities over the last 21 years, including as Stewardship Director, Director of Land Protection and

Associate State Director. Tom has been project lead for TNC in all the major north woods land conservation

projects over the last 18 years, starting with the St. John River acquisition, and most recently with the East

Branch, Penobscot River Project. He has had a hand in the conservation of nearly one million acres of lands in

Maine. Tom has worked with other TNC staff to explore the feasibility of enrolling TNC lands in Maine in a

carbon offsets program. He started his career in Maine, spending nine years with the Maine Forest Service in

the policy and program management arena. Tom graduated from the University of Massachusetts with a BS in

Forest Management, and holds a Master of Forestry degree from Yale University.

Patrick Sirois, Director of the Maine Sustainable Forestry Initiative

Pat has served as Maine’s SFI director since 1997. He represents the third generation of his family’s sawmill and

logging business in the midcoast area and was a logging contractor for eighteen years.

Executive Summary

1

Executive Summary Maine’s Implementation Committee of the Sustainable Forestry Initiative (SFI) has collaborated with Keeping

Maine’s Forests (KMF) to study Maine’s SFI‐certified landowners’ participation in carbon credit programs.

Forestlands must be certified as sustainably managed to be eligible for the California carbon credit market, and

millions of acres of Maine’s commercial forest lands are enrolled in the SFI program, yet none have enrolled in

potentially lucrative carbon credit programs. The KMF study enlists the expertise of a panel of advisors from the

University of Maine’s Climate Change Institute, Maine land managers and forestry experts, and a professional

carbon project developer to find out why.

California has the dominant cap‐and‐trade carbon credit market in North America, paying the highest prices for

forestry projects that offset carbon emissions from the state’s industries. Quebec has linked their program with

California’s so that Canadian landowners can obtain credits in the California market, and Ontario is in the

process of doing the same. While the Regional Greenhouse Gas Initiative (RGGI, covering the New England

states, Delaware, Maryland and New York) has the regulations in place to accept forestry offsets projects and

has adopted California’s forest offset protocols, so far, no one has sought carbon credits for forestry projects in

the RGGI market and so no price for forestry offset credits has been established.

To date, the California Air Resources Board (ARB) has issued approximately 57 million offset credits, with 65% of

these issued for so‐called “improved forest management (IFM) projects”. From 2013‐2020, as many as 200

million total offset credits have been or may be demanded by California industries to meet their greenhouse gas

emission caps. Assuming forestry continues to account for the same percentage of issued offset credits, almost

93 million credits may be in demand from forestry projects between now and 2020. Current offset prices are

around $10 per credit, with projections in the low to mid‐teens by 2020. Even if the price stays at today’s $10

per ton, all registered forestry offset projects between now and 2020 are potentially worth nearly one billion

dollars.

KMF surveyed Maine’s nine SFI participants to find out whether land managers had looked into obtaining carbon

credits, and if so, what factors had weighed in their decision to move forward or not. Of the seven survey

respondents, all of them had carefully considered getting carbon credits through the California market, but had

decided against it, at least for now. While the up‐front payout from carbon credits can be substantial and a good

way to diversify income from forest land, the land managers found that costs, risks, and the 100‐year

commitment required by carbon projects not worthwhile at current credit prices.

IFM project carbon stocks are measured against a baseline — the average carbon stocking in the ecological

region in which the project lies. Credits are issued for carbon stocking above this baseline and, if the landowner

wishes, for future tree growth. Projects are required to maintain a stable or increasing level of carbon. To

document, verify and track this carbon, the ARB has rigorous standards for measurement, modeling, inventories,

and verification audits. While SFI participants have the advantage of having the staff, software, record keeping

and systems in place for designing and maintaining a carbon project over 100 years, the auditing processes for

SFI certification and carbon project verification are not similar, so these processes represent additional costs for

landowners. Landowners are at risk of having to pay back credits, sometimes with an additional penalty, if the

land’s carbon stocks decline due to harvests.

Sixteen to nineteen percent of a project’s credits are automatically transferred into an insurance pool, which

fully covers carbon losses due to unintentional declines in carbon stocks from weather events, wildfire, and

insect, disease, and pathogen outbreaks. It is not clear, however, whether pre‐salvage harvests related to

Executive Summary

2

spruce budworm infestation would be covered. Indeed, presalvage harvests may require landowners to

surrender credits and possibly incur penalties. Given that landowners in Maine can expect two to three spruce

budworm outbreaks over the course of a 100‐year project, this lack of regulatory clarity represents a substantial

risk to current and potential program participants.

The ARB regulations are in effect until 2020 and allow regulated entities to obtain offset credits through

November 1, 2021. While the California legislature has committed to a further reduction of statewide

greenhouse gas emissions to 2030, the cap‐and‐trade and offset programs have not yet been renewed and the

program’s continuation is still being debated. There may be opportunities to influence Quebec and Ontario’s

GHG reduction programs to facilitate SFI certificate holder participation. Other Canadian Provinces such as New

Brunswick and Nova Scotia are also now considering the adoption of market‐based greenhouse gas emission

reduction regulations and programs. In the meantime, carbon credits are a viable option for landowners whose

forestland portfolios have areas with high carbon stocking that can be maintained over the long term. Higher

credit prices or poor wood markets could also tip the balance of considerations in favor of improved forestry

management projects.

Introduction

3

Introduction Maine has 17.6 million acres of forests, 17.1 million acres (97%) of which is considered timberland. Maine forest

landowners are growing more wood than they harvest, and the carbon in the state’s forests has increased in

volume by almost 5% from 2004 to 2012.1 Over eight million acres in Maine is managed according to the

sustainability standards of the Sustainable Forestry Initiative, Inc. (SFI), and/or the Forest Stewardship Council

(FSC), or the American Tree Farm System (ATFS) — a key eligibility criterion for carbon credit programs. Yet,

none of the 6.3 million acres of SFI‐certified lands in Maine are enrolled in a carbon credit program — not for

lack of interest, because all of Maine’s SFI participants have considered carbon credits. Maine landowners who

participate in other certification programs or adhere to a sustainable long‐term management plan approved by a

state or federal agency have enrolled tens of thousands of acres in carbon agreements worth millions of dollars.

This paper examines the degree to which forests managed to the Sustainable Forestry Initiative’s (SFI) standards

in Maine are enrolled in carbon credit programs; analyzes the opportunities and constraints these programs

represent for landowners; and examines the strengths and weaknesses of different landowner types when

considering enrolling land in a carbon credit program. The study examines the value that sustainability

certification adds to the process of obtaining carbon credits, and how changes to the protocol for obtaining

carbon credits might enhance the incentives to enroll land.

This study does not address questions about the efficacy of the carbon programs in achieving greenhouse gas

reductions or in permanently sequestering carbon in Maine forests. Rather, it examines how carbon credit

programs, in fact, function in Maine, regardless of the programs’ goals or intentions. The study’s survey of SFI

participants in Maine, as well as an examination of the carbon projects in Maine that have earned credits for

landowners, reveals that a variety of constraints prevent some landowners from entering the carbon market.

Some constraints are imposed by the program regulations, others by the forest landowner’s institutional

organization and culture. Consequently, the findings of this paper are specific to Maine. Their applicability to

similar forest types or forest landowner types elsewhere should be examined carefully, and on a case‐by‐case

basis.

The carbon credit market is a relatively new economic model; one that has been refined since its inception in

2006 by California’s Assembly Bill 32, and is undergoing revision as this paper is written. The California Air

Resources Board’s cap‐and‐trade program was the first carbon credit program, and due to the state’s status as

the world’s eighth largest economy, remains the dominant one. Other programs are aligning with California’s

even as they create their own market.

In 2016, the California legislature passed a bill to extend the state’s targeted greenhouse gas (GHG) emission

reduction goal to 2030. While the existing program rules were designed to reduce California’s emissions to 1990

levels by 2020, the new rules will aim to reduce emissions to 40% below 1990 levels. It is not known now

whether the new rules will affect the incentives for Maine landowners to enroll their land in carbon credit

programs, but AB 32’s codified process for revision allows for this possibility, and it is hoped that this paper

might inform that process. In the meantime, it is the goal of this paper to apprise Maine land owners and

managers about the opportunities and risks inherent in enrolling land in a carbon credit project.

1 The Economic Importance of Maine’s Forest‐Based Economy, North East State Foresters Association; 2013; pp. 3 and 7.

Part I: Carbon Markets

4

Part I: Carbon Markets Carbon credit markets have been developed as a means of rewarding those who either reduce their own

greenhouse gas (GHG) emissions below regulatory levels, or capture carbon at a rate beyond a “business as

usual” scenario, thereby offsetting others’ GHG emissions. Carbon markets can be either regulatory or

voluntary.

The voluntary markets have been set up as a way for businesses to demonstrate corporate social responsibility

or a higher standard of operation than their industry peers in a non‐regulated environment. Voluntary carbon

credits are purchased to satisfy personal objectives or corporate standards, and to differentiate a business in the

market place as being more sustainable. Voluntary markets were in operation for a decade before the

regulatory compliance markets, and served as a testing ground for carbon accounting, verification and pricing.

The regulatory markets have been developed to respond to the carbon emissions goals set by the UN

Framework Convention on Climate Change including the Kyoto Protocol.2 While there are several regulatory

markets (the Regional Greenhouse Gas Initiative (RGGI)3, the Ontario and Quebec carbon markets4, and the

California market developed and administered by the California Air Resources Board (ARB)), the California

market is the largest that allows the use of forestry and forest carbon offset credits, and also commands the

highest prices for carbon credits. Maine’s SFI‐certified forestland managers who are considering carbon credit

programs will be most interested in getting the highest price for credits, therefore the discussion below will

focus on the ARB standards and processes.

California’s Carbon Credit Market California’s Assembly Bill 32 (2006) was designed to reduce the state’s overall GHG emissions to 1990 levels by

2020, or 15% lower than the emissions would have been without the regulations. The regulations went into

effect in 2013, setting the emissions cap at 2% below 2012 levels. The cap was set another 2% lower for 2014,

and then is reduced by 3% each year from 2015 to 2020. Approximately 450 entities that emit 25,000 metric

tons of carbon dioxide equivalent (mtCO2e) or more annually are covered, representing 85% of California’s total

emissions. These GHGs include not only carbon dioxide, but methane, hydrofluorocarbons, and four other

gases.

The California program requires direct reductions in emissions through energy efficiency improvements, or by

generating power from renewable sources rather than from fossil fuels. The annual statewide emissions cap is

translated into tradable emission allowances (each allowance typically equivalent to one metric ton of carbon

dioxide or carbon dioxide equivalent), which are auctioned or allocated to regulated emitters on a regular basis.

At the end of each compliance period, each regulated emitter must surrender enough allowances to cover its

actual emissions during the compliance period.

Regulated emitters may also purchase credits for indirect emission reductions. Up to 8% of their emissions can

be offset from projects outside capped sectors that are voluntarily engaged in carbon reductions and/or

2 Even though the US has not ratified the Protocol. 3 The RGGI has adopted California’s forest offset protocol, but has not set a price on offset projects. 4 As of 2014, Quebec and California linked their GHG emissions reporting programs. However, because Quebec currently lacks a forest offset protocol, forest offset projects may not be developed in Quebec for use in the Quebec and California’s program. However, forest offset projects developed under the California’s forestry protocol are being used by Quebec entities for compliance purposes in the California market. As of the end of 2016, Ontario was still in the process of developing offset protocols.

Part I: Carbon Markets

5

sequestration.5 For example, a power plant in California that has not reduced its emissions to the regulatory

target level may purchase carbon offset credits from a forest landowner in Maine that has an offset project

registered with the ARB, counting the additional carbon sequestered in the forest project area against the power

plant’s emissions in order to meet its compliance obligation cap.

As of January 2017, a regulated emitter in California will pay $50‐$120/ton for pollution control equipment,

$13.57/ton for a California Carbon Allowance (CCA); or $10+/ton for a California Carbon Offset (CCO). With

these price differentials, emitters will maximize the amount of offset credits they can buy each year, ensuring a

steady demand for offset credits at least through the end of the 2020.

Carbon Offset Projects ARB‐approved carbon offset projects can be for ozone depleting substances; agricultural methane; urban

forestry; mine methane capture; rice cultivation; and US forests. US forest projects, in turn, include

reforestation (the reestablishment of forest cover either naturally or artificially); avoided conversion

(“preventing the conversion of forestland to a non‐forest land use by dedicating the land to continuous forest

cover through a qualified conservation easement or transfer to public ownership, excluding transfer to federal

ownership”); and improved forest management projects.

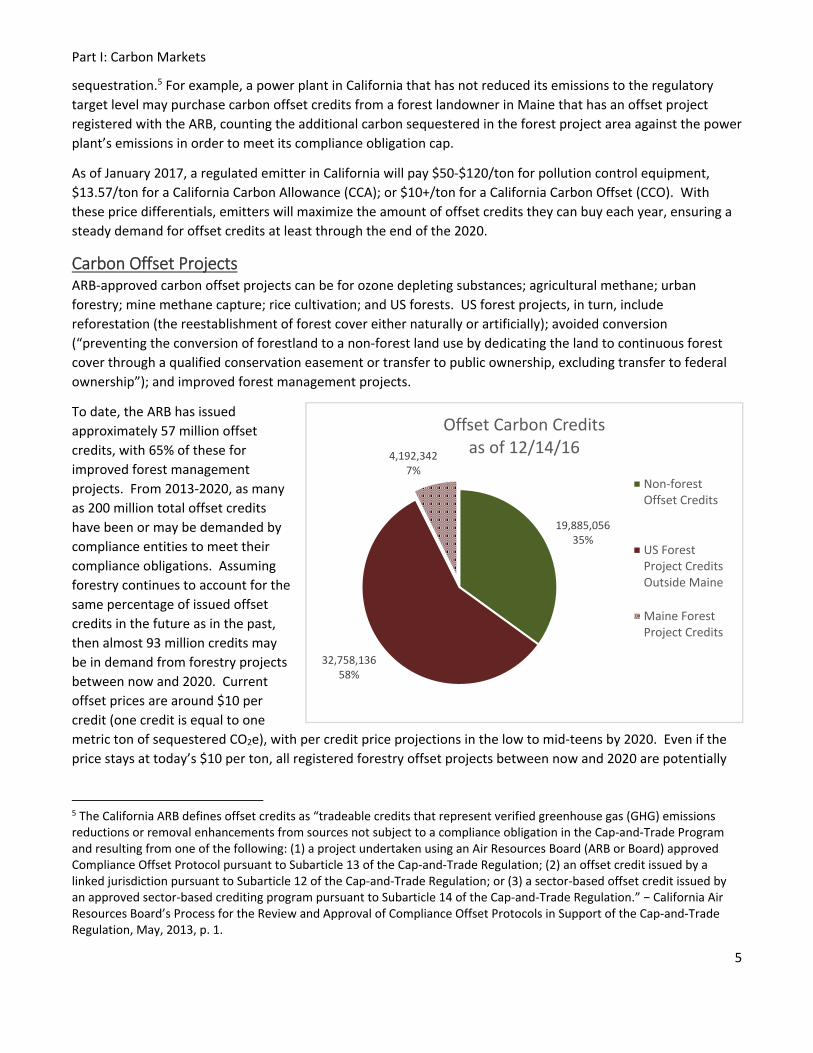

To date, the ARB has issued

approximately 57 million offset

credits, with 65% of these for

improved forest management

projects. From 2013‐2020, as many

as 200 million total offset credits

have been or may be demanded by

compliance entities to meet their

compliance obligations. Assuming

forestry continues to account for the

same percentage of issued offset

credits in the future as in the past,

then almost 93 million credits may

be in demand from forestry projects

between now and 2020. Current

offset prices are around $10 per

credit (one credit is equal to one

metric ton of sequestered CO2e), with per credit price projections in the low to mid‐teens by 2020. Even if the

price stays at today’s $10 per ton, all registered forestry offset projects between now and 2020 are potentially

5 The California ARB defines offset credits as “tradeable credits that represent verified greenhouse gas (GHG) emissions reductions or removal enhancements from sources not subject to a compliance obligation in the Cap‐and‐Trade Program and resulting from one of the following: (1) a project undertaken using an Air Resources Board (ARB or Board) approved Compliance Offset Protocol pursuant to Subarticle 13 of the Cap‐and‐Trade Regulation; (2) an offset credit issued by a linked jurisdiction pursuant to Subarticle 12 of the Cap‐and‐Trade Regulation; or (3) a sector‐based offset credit issued by an approved sector‐based crediting program pursuant to Subarticle 14 of the Cap‐and‐Trade Regulation.” − California Air Resources Board’s Process for the Review and Approval of Compliance Offset Protocols in Support of the Cap‐and‐Trade Regulation, May, 2013, p. 1.

19,885,05635%

32,758,13658%

4,192,3427%

Offset Carbon Creditsas of 12/14/16

Non‐forestOffset Credits

US ForestProject CreditsOutside Maine

Maine ForestProject Credits

Part I: Carbon Markets

6

worth nearly one billion dollars.

Offset Project Requirements To meet the rigorous standards of the ARB market and qualify for credits, all offset projects must demonstrate

that the carbon emissions they are reducing are:

1. Additional

The climate benefits from the project must be above and beyond the “business as usual” baseline of reductions

as defined by the offset protocol. Specifically, the project must sequester carbon stocks that are higher than

would be otherwise required by law or regulation, and in the case of forestry projects, higher than the average

that occurs on land in the project’s surrounding region, with similar growing conditions and under prevalent

management practices.

2. Real, measurable, standardized

The project must use the best science to rigorously measure carbon and calculate its climate benefits.

3. Verifiable

The calculations of the sequestered carbon must be confirmed by an independent third party.

4. Permanent

The project reductions must be enduring and functionally equivalent (in the atmosphere) to the emissions the

project is offsetting. For forestry projects, “permanent” is defined as 100 years from the date that credits are

issued.

The California Air Resources Board has identified three types of forestry projects, each with its own

methodology, for meeting the requirements outlined above. The types of forestry projects include:

Reforestation projects which increase removals of CO2 from the atmosphere through “the restoration of tree

cover on land that currently has no, or minimal, tree cover.”

Avoided Conversion projects which avert CO2 emissions by preventing land from being converted from forest to

other land uses. Principally, forest land that is demonstrably threatened by development and placed under a

qualified permanent conservation easement, or that is transferred to non‐federal public ownership within a year

of the project commencement date, qualifies as an avoided conversion project.

Improved Forest Management (IFM) projects which involve management activities that maintain or increase

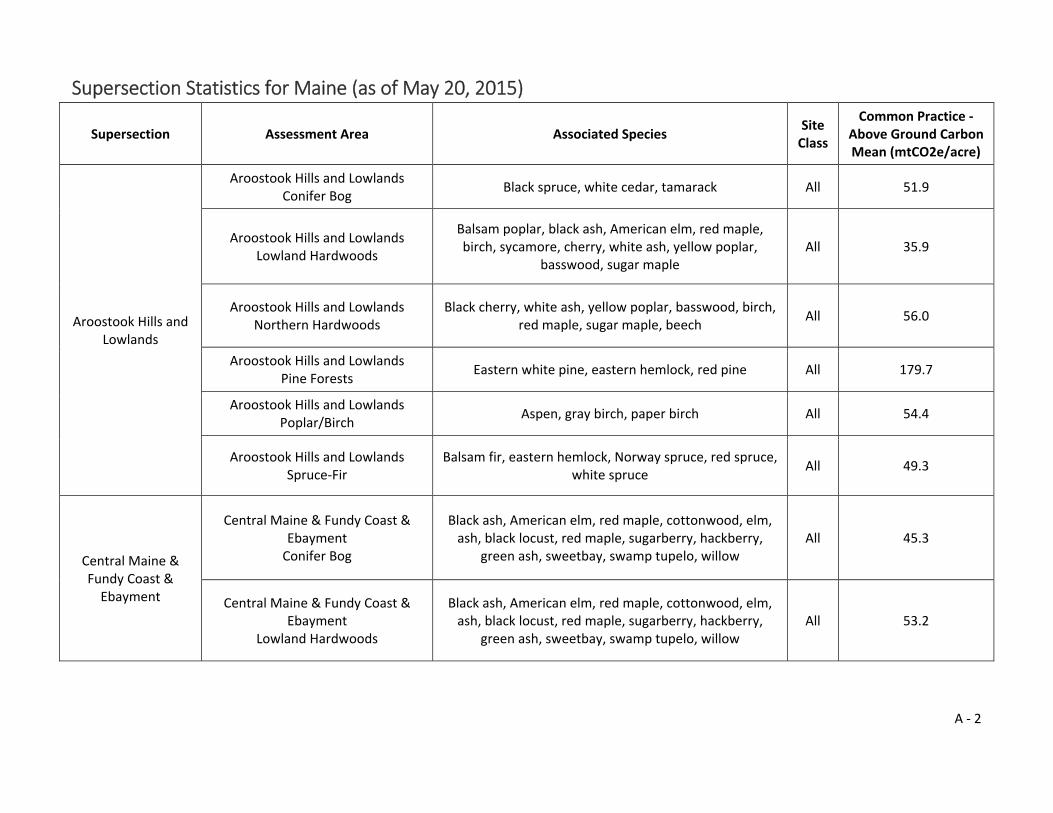

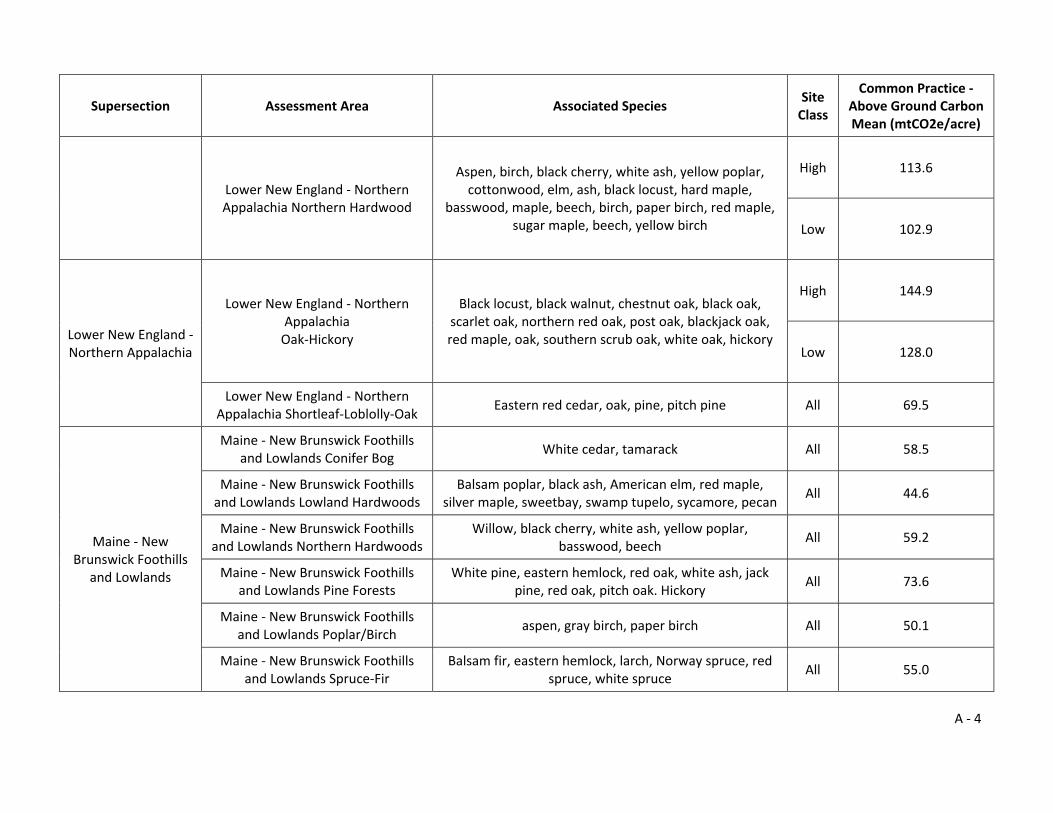

carbon stocks on forested land relative to baseline levels of carbon stocks, or “common practice”. Common

practice statistics for metric tons of carbon equivalent per acre (mtCO2e/acre) are established by major forest

types within supersections (large regions) that have relatively uniform climate, dominant natural vegetation,

geology, and soils. The common practice is the average above‐ground carbon volume in a project’s assessment

area (distinct forest community), and is derived from USDA Forest Service’s Forest Inventory and Analysis (FIA)

datasets. To determine how much additional carbon is being sequestered by a project, a property’s on‐site

carbon stocks are compared against the common practice statistics for the appropriate assessment area.

Maine is 89% forested, and does not have significant opportunities for reforestation (note that natural

regeneration of exiting forests after a harvest is distinct from reforestation). On the other hand, Maine has over

8 million acres of forest certified as sustainably managed. Some of these lands have carbon stocks above ARB’s

“common practice” benchmark and are eligible for carbon credits as improved forest management projects.

Lands that are newly placed under easement could also be eligible as avoided conversion projects. However,

Part I: Carbon Markets

7

because of the substantial eligibility requirements of avoided conversion projects and the high carrying costs of

reforestation projects, improved forest management projects are the most significant opportunity for forest

landowners, both in Maine and throughout the US.

Process for Obtaining Credits There is a multi‐step process for obtaining credits for improved forest management projects.

Listing The preliminary step for a project owner (called an Offset Project Operator, or OPO) to receive credits is listing

the project on one of three ARB‐approved registries: the Carbon Action Reserve, Verified Carbon Standard, or

American Carbon Registry. Listing a project demonstrates that the registry has verified that the project has met

the basic eligibility criteria for offset projects and provides basic information about the project to the public such

as who the project operator is, the project’s location and size, and the estimated amount of carbon sequestered

above and beyond the “common practice” or project baseline.

Listing requires that the OPO establish accounts with both a registry and the ARB, and can be thought of as an

application for developing the carbon offset project. It occurs prior to project development (when the project’s

carbon stocks are inventoried and verified) and all ARB‐compliant projects are publicly listed on the registry’s

website. Listing, by itself, does not guarantee that a project will be developed, or that it will be successfully

completed with credits issued. It does, however, establish a project commencement date from which various

reporting periods and deadlines are measured; the estimated baseline carbon stocks against which the project,

if developed, will be measured; and establishes the applicable protocol under which the project will be

developed and monitored.

Project Development Before issuing carbon credits, the ARB must confirm that the OPO has conducted the initial carbon inventory,

growth modeling, monitoring, reporting and verification in accordance with the applicable ARB cap and trade

regulation6 and current forest protocol7. The regulation describes the process for obtaining and trading credits

and describes the requirements for measuring, verifying and reporting carbon stocks. The forest protocol

prescribes the formulae for calculating carbon stocks and the requirements for managing forests so that a

project area’s carbon stocks are maintained over time.

6 This paper’s description of the cap and trade regulations are taken from the unofficial electronic version of the Regulation for the California Cap on Greenhouse Gas Emissions and Market‐Based Compliance Mechanisms accessed on March 2, 2016 at: https://www.arb.ca.gov/cc/capandtrade/capandtrade/unofficial_ct_030116.pdf. The official regulation can be accessed at: https://govt.westlaw.com/calregs/Browse/Home/California/CaliforniaCodeofRegulations?guid=I47A831C02EBC11E194EACEFFB46E37D1&originationContext=documenttoc&transitionType=Default&contextData=(sc.Default). 7 The 2015 protocol can be accessed at: https://www.arb.ca.gov/cc/capandtrade/protocols/usforest/forestprotocol2015.pdf.

Part I: Carbon Markets

8

The Carbon Inventory

After project listing, the OPO conducts a carbon inventory for the project area which includes not only

merchantable wood, but also the carbon in non‐merchantable trees and tree parts. One of the key benefits of

carbon credit programs for forest landowners is to be able to monetize portions of trees that are underutilized

in conventional forest products. In addition to the carbon in tree and tree components used for conventional

wood products, OPOs may be issued credits for the carbon volume in:

unsound trees,

stumps, coarse roots, and branches,

standing dead trees,

trees without a single straight bole, and

trees that are 1.0‐4.9” in diameter.

Sample plots within the project area are defined and

mapped so that they can be remeasured with

accuracy over the 100‐year life of the project. All

woody biomass (4.5” DBH and larger) within the

sample plots must be measured, plots are generally

monumented, and each tree is marked with an

individual identifier. Accuracy is essential, as the ARB

requires a confidence level on the sample of 90%, plus

or minus 10%. Designing the sampling process is

critical to the success of a project and requires a

registered forester with special expertise.

The carbon inventoried in a forest offset project includes a portion of the harvested timber. Generally speaking,

kiln‐dried wood is 50% carbon, so, depending on the ultimate use of the wood, harvests do not cause all the

trees’ carbon to be lost to the atmosphere. In addition to the carbon in the standing timber, forestry offset

projects can be credited for the long‐term storage of carbon in long‐lasting wood products. On the other hand,

the ARB forestry protocol recognizes that harvesting, processing, and transporting wood and wood products

necessitates the use of machinery that burns fossil fuels. Projects can also necessitate soil disturbances during

site work and cause decomposition of forest materials, both of which result in greenhouse gas emissions. 8 The

protocol includes formulae for calculating these secondary effects of a harvest and requires the reduction of the

carbon stocks accordingly.

Modeling

Once the initial carbon stocks are inventoried and verified, the OPO conducts an annual “desktop” audit. This

involves estimating the current amount of biomass and growth within the project area and then accounting for

planned harvests and the end use of the harvested wood. The annual modelling is done using mill receipts,

harvest tallies, ARB‐approved biometric equations, and growth and yield software.

The initial inventory and modeling data are submitted to the ARB as an Offset Project Data Report (OPDR).

Assuming the project is approved by the ARB, the OPO will submit OPDRs annually for the life of the project.

These reports serve as a mechanism for monitoring the credited carbon over the life of the project and

document the growth (or decline) of carbon stocks as new trees take root and existing trees grow and die

8 Although soil carbon is not a creditable pool under the ARB forest offset protocol.

Steps in Calculating Carbon Credits

1. Estimate baseline onsite carbon stocks;

2. Estimate baseline carbon in harvested wood

products;

3. Determine actual onsite carbon stocks;

4. Determine actual carbon in harvested wood

products;

5. Calculate the forest project’s secondary

effects; and

6. Determine applicable confidence deductions

and discount factors.

Part I: Carbon Markets

9

and/or are removed through scheduled harvests and silvicultural operations. The OPO can request credits for

additional growth over and above the initial carbon stocks, with the provision that the timeline for the project is

reset for 100 years from the date of the issuance of the new credits.

Reporting

The OPO must submit the first Offset Project Data Report (OPDR), including inventory and modelled projections,

within 24 months of listing the project. Thereafter, the OPO submits annual reports based on the remodeled

carbon accounting and new inventory, when applicable. Failure to submit a data report is interpreted by the

ARB as a voluntary termination of the project.

After the first reporting period, verification must be conducted at least once every six years and may cover up to

six reporting periods for which Offset Project Data Reports were submitted. All verification reports must be

submitted within 11 months of the reporting period being verified.

Verification

The ARB requires third‐party verification on a sample of the inventoried plots. The verification body must be

ARB approved, and the offset verification statement (OVS) itself must be reviewed internally by someone not

directly involved in the verification process. As a third check for reliability, the ARB reviews the verification

statements. Finally, no verification body can issue verification statements for the same project for more than six

consecutive reporting periods. After the sixth verification statement, the OPO must rotate to another

verification service.

The verification of the initial data report requires a site visit after the report is submitted and must:

a. Confirm that the offset project is eligible under the ARB protocol and that the project meets the

requirements for additionality;

b. Confirm that the offset project boundary is appropriately defined;

c. Review the project baseline calculations and modeling;

d. Assess the project’s operations, functionality, and data control systems, and review the techniques for

measuring and monitoring GHG; and

e. Confirm that all eligibility criteria applicable to project design, measurement, chain of custody, and

monitoring conform to the Offset Protocol.

Assuming the offset project is approved, the OPO’s data reports will then be verified every six years, and

inventories every twelve years. If a verification statement is not received within 11 months of the reporting

period which the statement has reviewed, the project will not receive any carbon credits for the carbon

sequestration documented by the OPDR.

The project development process demands a deep understanding of the forest protocol, how to design a precise

sequential sampling regime, and how to strategically optimize forest management plans. While most OPOs will

hire professionals to develop an IFM project, not all do. The ongoing inventory, modeling and reporting

requirements demand a high level of expertise, staff time and the necessary hard‐ and software. In this regard,

SFI participants are particularly well‐suited to developing and maintaining IFM projects.

Registration and Sales

Once a project receives a successful third‐party OVS, the registry will then review the project and, if it is in

compliance with the protocol, issue temporary registry offset credits (ROCs) to the project. The project is then

handed off from the registry to the ARB for a final review of compliance with the offset regulation and protocol.

Part I: Carbon Markets

10

If the ARB approves the project, the ROCs are cancelled and the ARB issues Air Resource Board Offset credits

(ARBOCs) which may be sold by the OPO and used by regulated entities for compliance purposes within the

ARB’s GHG emissions trading program.

Credits do not have to be sold: they can be “banked” (essentially left on the books in the OPO’s account at the

ARB), traded for credits in other compatible markets, or sold gradually over time. When credits are sold, the

price is negotiated privately between the buyer and seller.

Invalidation Risk, Reversals, and Project Termination The number and value of the carbon credits issued to a project take into consideration the risk that a project’s

stated climate benefits are later found to be invalid; that the carbon stocks may be diminished, either

inadvertently or purposefully; and that the project may be terminated. These risks are calculated at the

beginning of the project.

Invalidation If a project, after registration, is found to be fraudulent or its carbon stocks cannot be verified, it is considered

invalid. The ARB regulations allow an 8‐year window for credits to be found invalid. Credit buyers can demand a

price discount to hedge against this risk or require a 3‐year invalidation window instead, obtained by getting a

second successful independent third‐party verification.9

Unintentional Reversals The regulation requires the landowner to replace all “reversed” offsets. Weather events, insect damage and

other uncontrollable circumstances can effectively release carbon to the atmosphere. If credits have been

issued to a forest offset project for this carbon, it is considered an unintentional reversal. Unintentional

reversals are compensated for from a mandatory reversal risk “buffer pool” of credits managed by the ARB. The

buffer pool serves as an insurance mechanism for unintentional reversals of any magnitude and on average,

approximately 16‐20% of a project’s initial credits are placed into this buffer account which insures all forestry

offset projects. Offset credits deposited into the risk buffer pool have no market value per se, and may not be

traded between market participants. The amount contributed to the buffer account may be reduced through

the use of a qualified conservation easement that gives the ARB third‐part enforcement rights.

As an example, a wildfire that burns part of a project area is an unintentional reversal, releasing a significant

portion of the above‐ground carbon fixed in the wood to the atmosphere. Other examples of unintentional

reversals include those from insect damage or wind storms. Project operators are required to report a reversal

within 30 days of its discovery, remeasure the project’s carbon stocks within one year of the reversal, and have

the new carbon inventory verified by a third party. The later inventory is compared with the previous annual

estimate on record for issued credits. The ARB then retires a number of credits from the buffer account equal to

the number of tons reversed.

Intentional Reversals The ARB defines an intentional reversal as “any reversal . . . which is caused by a forest owner's negligence, gross

negligence, or willful intent, including harvesting, development, and harm to the area within the offset project

boundary.”10 The reporting requirements for intentional reversals are the same as for unintentional reversals,

9 Both the voluntary and compliance markets also sell premium or “golden” credits for projects with no invalidation risk.

10 “A reversal caused by an intentional back burn set by, or at the request of, a local, state, or federal fire protection agency for the purpose of protecting forestlands from an advancing wildfire that began on another property through no

Part I: Carbon Markets

11

but compensation for the lost carbon must be paid for, within 6

months, in credits from the OPO’s account (rather than the buffer

account).

Legitimate intentional reversals may occur as a planned part of

silvicultural operations (for example to balance age classes or reduce

wildfire risk). These are recognized by the ARB, but do not change

the requirement to compensate for such reversals. Project owners

should retain sufficient unsold credits in their account to compensate

for these anticipated reversals.

Project Termination Whether intentional or unintentional, a major reversal can potentially eliminate all, or even more, of the

sequestered carbon for which credits have been issued. When a project’s carbon inventory goes below the

baseline carbon stocks at the project’s initiation, the ARB will terminate the project.11 If the reversal was

unintentional, the project’s buffer account will cover the reversal, and the OPO must re‐inventory the project

area to document the project termination.

When an intentional reversal causes the project to terminate, the OPO must pay back the offset credits out of

their own account, plus a penalty. The amount of the penalty depends on the duration of the project. It can be

between 1 and 1.4 times the number of credits reversed, with newly commenced projects incurring penalties at

higher rates (see the table at right).

Forest Management For improved forest management projects, the additionality criterion means the forest protocol represents an

extra layer of proscriptions, over and above what is required by state regulations and sustainability certification

standards, and beyond the “common practice.” This paper will focus on the forest management requirements in

the 2015 Compliance Offset Protocol: U.S. Forest Projects, although it should be noted that early forestry offset

projects were registered using the previous (2014) protocol.

Eligibility requirements for forest offset projects are as follows:

1. projects must be located within the contiguous 48 states, or specific parts of Alaska;

2. the Offset Project Operator must demonstrate that the forest is sustainably managed; and

3. projects must be managed under a “natural forest management” regime.

The latter two requirements are designed to ensure that projects will be managed so that carbon stocks will be

maintained over the course of the project. Forests are considered sustainably managed if they are third party

certified under the Sustainable Forestry Initiative, the Forest Stewardship Council, or the American Tree Farm

System. Alternatively, lands can be managed under a federal‐ or state‐sanctioned sustainable management

plan, or with uneven‐aged silvicultural practices with canopy retention averaging at least 40% across all the

negligence, gross negligence, or willful misconduct of the forest owner is not considered an intentional reversal but, rather, an unintentional reversal.” Title 17. Division 3. Chapter 1. Subchapter 10. Article 5. Subarticle 2, § 95802. (190). 11 Projects can also be terminated when the project land or timber rights are sold and the new owner does not wish to be responsible for the project commitments; or the OPO can terminate the project themselves. In these instances, credits must be repaid.

Penalty Rate for Early Termination Due to Intentional Reversal

# years between offset project commencement

and termination

Compensation Rate

0‐5 1.40

>5‐10 1.20

>10‐20 1.15

>20‐25 1.10

>25‐50 1.05

>50 1.00

Part I: Carbon Markets

12

forestland owned by the Offset Project Operator (whether part of the project area or not).

Natural Forest Management The “natural forest management” requirement includes the following provisions:

A project’s standing live tree carbon stocks must consist of at least 95% native species.

If even‐aged management is practiced on a watershed scale up to 10,000 acres (or the project area,

whichever is smaller), projects must maintain no more than 40% of their forested acres in ages less

than 20 years, and certain harvest size and buffer area requirements must be met.

Generally, projects must maintain one metric ton of carbon per acre or 1% of standing live tree carbon

stocks, whichever is higher, in standing dead tree carbon stocks to diversify the forest structure and

provide wildlife habitat.

Projects must maintain the standing live tree carbon stocks within the project area over any 10

consecutive year period during the project life, except as follows:

o Any decrease is demonstrably necessary to substantially improve the project area’s resistance to

wildfire, insect, and/or disease risks;

o The decrease is associated with a planned balancing of age classes;

o The decrease is due to an unintentional reversal; or

o The decrease in standing live tree carbon stocks occurs after the final crediting period (during the

required 100‐year monitoring period) and the residual live carbon stocks are maintained at a level

that assures all credited standing live tree carbon stocks are permanently maintained.

Forest offset projects must not:

experience a decrease in standing live tree carbon stocks that results in the standing live tree carbon

stocks falling below the forest project’s baseline standing live tree carbon stocks (derived from the

mtCO2e/acre for the project’s assessment area) or 20 percent less than the forest project’s standing live

tree carbon stocks at the project’s initiation, whichever is higher; nor

employ broadcast fertilization.

Part II: Results from Survey of Maine Land SFI Participants

13

Part II: Results from Survey of Maine Land SFI Participants Large landowners (with over 10,000 acres) in Maine

include families, forest products companies, logging

contractors, nonprofit conservation organizations, tribes,

real estate investment trusts (REITs), timber investment

management organizations (TIMOs), and the public (state

and federal government). In general, it should be noted

that many of Maine’s large landowners do not manage

their own land, but hire forest management companies for

this purpose. Consequently, the decision‐making body

that sets overall financial and management goals differs

from the one that makes and executes day‐to‐day forest

management decisions.

There are 8.3 million acres in Maine certified as

sustainably managed. Seventy‐five percent (6.3 million

acres) are SFI‐certified. In the summer of 2016, Keeping Maine’s Forests emailed the nine companies that

manage these lands a survey regarding their past and future assessments of carbon credit programs. The

questions were open‐ended so that the survey didn’t predispose the respondents toward specific answers. The

questions were as follows:

Seven of the nine surveys were returned. All the respondents had considered a carbon credit project on their

lands; some had been looking into the feasibility of a project as long ago as 2008. Most companies had been

approached by, or worked with, one or more firms that develop carbon projects. Several land management

companies said that they had considered carbon projects several times, or on an ongoing basis. Uniformly, land

managers said they considered carbon projects for the potential revenue. Two also responded that they wanted

to understand their options with regard to the carbon credit programs.

Land managers are clearly diligent in investigating carbon credit programs. They reported having done analyses

of the fiscal impacts of entering into a carbon credit program, they looked at more than one potential carbon

Acres in Maine Certified as Sustainably Managed by Third Parties as of August 18, 2016

Certification Program Acres

SFI and FSC dual certification 3,378,242

SFI only 2,874,277

FSC only 1,680,701

American Tree Farm System 375,000

Total 8,308,220

Source: Ken Laustsen, Maine Forest Service, personal communication; November 7, 2016

Survey of SFI Participants

1. Have you ever considered entering into any carbon credit program?

a. Why, or why not? What were your reasons for investigating carbon credit programs (or not)?

2. Have you pursued entering into any carbon credit program?

a. If yes, what activities did you engage in to explore carbon credit programs (e.g., looked into hiring an

expert to evaluate the viability of credits for my land; conducted an analysis of the costs and benefits;

reviewed the forestry protocol, etc.)?

b. If no, why not?

3. Are you currently engaged in a carbon credit project?

a. If so, when was/will your project be listed? On which registry?

b. For those who looked into carbon credit programs but decided against pursuing a project, what made

you decide not to pursue carbon credits for your land? Please be as specific as you can be.

Part II: Results from Survey of Maine Land SFI Participants

14

project area, and they consulted with various experts. Some also said that they periodically review the carbon

credit program rules and forestry protocol.

Respondents’ Reasons for Not Enrolling Land None of the seven survey respondents had enrolled SFI‐certified land into a carbon credit program. Their

responses as to why varied in content and detail. Following is a synopsis of all the reasons cited; many of these

reasons are closely associated with one another.

Length of Commitment The time commitment of maintaining and operating a forest offset project for 100 years (or longer, if credits

were obtained for growth after the initiation of the project) was a universal concern. Often the length of the

commitment was mentioned in conjunction with other concerns − cost, risk, or impact on forest management –

as an exacerbating factor.

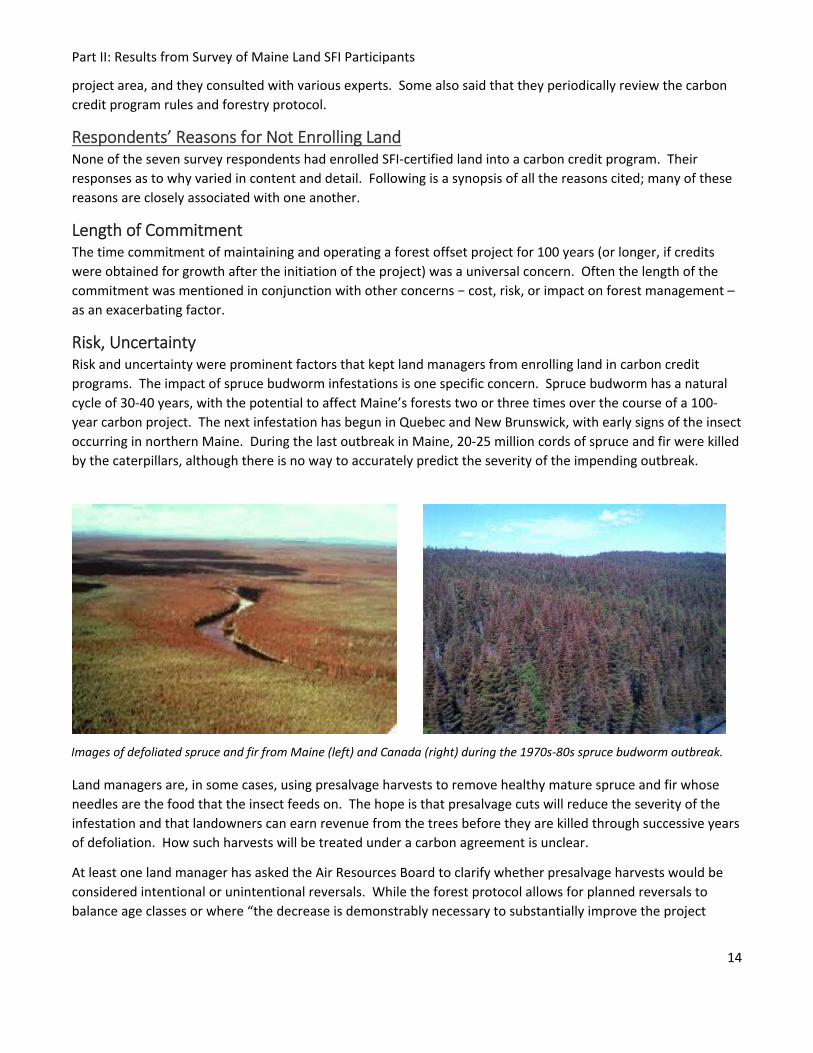

Risk, Uncertainty Risk and uncertainty were prominent factors that kept land managers from enrolling land in carbon credit

programs. The impact of spruce budworm infestations is one specific concern. Spruce budworm has a natural

cycle of 30‐40 years, with the potential to affect Maine’s forests two or three times over the course of a 100‐

year carbon project. The next infestation has begun in Quebec and New Brunswick, with early signs of the insect

occurring in northern Maine. During the last outbreak in Maine, 20‐25 million cords of spruce and fir were killed

by the caterpillars, although there is no way to accurately predict the severity of the impending outbreak.

Land managers are, in some cases, using presalvage harvests to remove healthy mature spruce and fir whose

needles are the food that the insect feeds on. The hope is that presalvage cuts will reduce the severity of the

infestation and that landowners can earn revenue from the trees before they are killed through successive years

of defoliation. How such harvests will be treated under a carbon agreement is unclear.

At least one land manager has asked the Air Resources Board to clarify whether presalvage harvests would be

considered intentional or unintentional reversals. While the forest protocol allows for planned reversals to

balance age classes or where “the decrease is demonstrably necessary to substantially improve the project

Images of defoliated spruce and fir from Maine (left) and Canada (right) during the 1970s‐80s spruce budworm outbreak.

Part II: Results from Survey of Maine Land SFI Participants

15

area’s resistance to wildfire, insect, and/or disease risks”,12 there has not been a clear answer from the ARB as to

how they would view presalvage harvests. As IFM projects in general are still a relatively new type of offset

credit, this may be because the ARB does not, yet, have an agreed‐upon mechanism for determining when a

presalvage harvest has been demonstrated to be necessary. In any case, with the prospect of having to either

pay back credits for a reversal due to presalvage harvests or allow a substantial volume of spruce and fir to die

on the stump and then having to harvest other species to meet wood supply agreements (which would also risk

credit repayments for intentional reversals), the decision was not to enter into a carbon credit program at all.

Other perceived risks mentioned by survey respondents included: uncertainty about the accuracy of the

required modeling (especially when accounting for Maine tree species’ shorter life cycle and the mortality

caused by spruce budworm); the adequacy of the buffer pool to cover losses due to windthrow and spruce

budworm; and how the long‐term encumbrances might be perceived and valued by timberland lenders and

buyers. Land managers are also unsure of what the cap‐and‐trade program will look like in the future,

specifically the value of carbon credits and potential revisions to the forest protocol. Two survey respondents

were concerned that future FIA updates would reduce the additionality on the lands they manage. One cited

easements on others’ lands that disallow harvesting as a factor that they had no control over, but which would

diminish additionality on the lands they manage over time.

Forest Protocol Restrictions Some provisions of the ARB forest protocol are a concern for Maine’s SFI participants − primarily, the regulation

of even‐age management that restricts clearcutting and shelterwood harvests. In Maine, where the life spans of

some common tree species are significantly shorter than in California and spruce budworm infestations must be

managed, even‐age management is an important management tool for stimulating tree growth. Even‐age

management also provides early successional wildlife habitat which can help landowners meet sustainability

certification standards.

Value of Credits Versus Costs of the Program Over 100 Years The survey respondents were concerned with the costs of entering into a carbon agreement and maintaining a

carbon project. Project development costs (inventory, modeling and project documentation, verification, and

offset transactions) vary widely, but are approximately $150,000 for the smallest offset projects. In addition,

landowners must set aside at least $200,000 to cover long term project maintenance and operations costs over

100 years or more for ongoing modeling, inventories and verifications. If a consultant is needed to conduct a

feasibility study, that is a significant, additional cost.

Two other reasons were given by one forest land manager as to why they did not enter into carbon credit

programs. First, a substantial portion of the lands they manage are covered by a working forest conservation

easement that was purchased using Land for Maine’s Future (LMF) bond funds. The easement includes

language that has been interpreted as prohibiting lands protected through the LMF program from participating

in carbon credit programs. In fact, the current template for working forest easements purchased with LMF bond

funds expressly extinguishes the right to use land to mitigate for development elsewhere, “as might otherwise

occur in cluster zoning laws, transfer of development rights schemes, and carbon sequestration and carbon

12 See 3.1(b)(1)(A), pages 21‐22 of Compliance Offset Protocol: U.S. Forest Projects; California Environmental Protection Agency Air Resources Board; Adopted June 25, 2015.

Part II: Results from Survey of Maine Land SFI Participants

16

dioxide credit programs.”13 Second, the manager noted that subdivision of land under a carbon agreement is

difficult and complicated.

Land managers summed it up by saying that carbon credits were simply not valued highly enough to make

carbon programs worthwhile. As one person put it, “where there are good markets for wood, it pays more to

grow and harvest that wood.” While higher credit prices will not address all the concerns raised by the survey

respondents, they would address cost and, to some extent, risk concerns. One land manager thought that a

price of $20 per carbon credit (roughly double the current price) would be enough to have them enroll land in a

program.

Current Carbon Credit Projects in Maine Despite these barriers to participation in carbon markets, as of December 2016, there have been six projects

that have obtained carbon credits in Maine. Clearly, some landowners are finding benefits to entering into

carbon agreements.

Carbon Credit Projects in Maine as of December 2016, by Acreage

Project Name Ownership Type (OPO) #

Acres # Offset Credits

Carbon Market Initial Credits/ Acre

Passamaquoddy Tribe Tribe

(Passamaquoddy Tribe) 98,532 3,218,469 CA ARB 33

Lyme Grand Lake Stream TIMO

(GLS Woodlands, LLC) 19,552 599,217 CA ARB 31

Farm Cove Community Forest Project

NGO(Downeast Lakes Land Trust)

19,118 284,043* CA ARB 13

Katahdin Iron Works Ecological Reserve

NGO(Appalachian Mountain Club)

9,037 123,344 voluntary market 14

Alder Stream Preserve NGO

(Northeast Wilderness Trust) 1,530 36,596** CA ARB 20

Howland Research Forest NGO

(Northeast Wilderness Trust) 552 54,017*** CA ARB 79

Source: California Air Resources Board: https://www.arb.ca.gov/cc/capandtrade/offsets/issuance/arb_offset_credit issuance_table.pdf and embedded links to project documentation; and the Climate Action Reserve: https://thereserve2.apx.com/myModule/rpt/myrpt.asp#top, accessed January 11, 2017. * Includes 242,131 credits for carbon stocks at project initiation and 41,912 credits for growth. ** Includes 31,290 credits for carbon stocks at project initiation and 5,306 credits for growth. *** Includes 43,687 credits for carbon stocks at project initiation and 5,165 credits for growth.

Most of Maine’s carbon projects have been initiated by NGOs.14 Since 75‐90% of the income from carbon credit

programs comes from the up‐front payment for existing carbon stocks, the landowners who will benefit most

13 Maine Department of Agriculture, Conservation and Forestry; Drafting Guidelines for Working Forest Easements Funded by the Land for Maine’s Future Program, adopted by the Land for Maine’s Future Board June 25, 2002; page 6‐10. The exact language of LMF‐funded working forest easements has changed over time; earlier language did not mention carbon credit programs specifically.

14 To date, the lands in Maine that have been enrolled in carbon credit projects have been FSC‐certified rather than SFI‐certified; this is based on only a few projects and appears to be largely a result of a tendency for Maine NGOs to have

Part II: Results from Survey of Maine Land SFI Participants

17

are those with older growth and less need for timber revenues going forward. The Katahdin Iron Works

Ecological Reserve, Alder Stream and Howland Research Forest projects are all operated by entities that prohibit

all harvesting on these lands. The other projects are operated by entities that do allow harvesting, but

presumably are confident they will not risk significant reversals due to harvesting or natural events.

The Lyme Grand Lake Stream project is the only one initiated by a TIMO. With this project, Lyme Timber

Company entered into a carbon agreement with the understanding that part of the proceeds would go toward

lowering the price of the land for their buyer, Downeast Lakes Land Trust. The trust was able to obtain the

forest land at a reduced price, and assumed the operation and maintenance costs of the project. These costs

may be somewhat reduced since their Farm Cove Community Forest project is adjacent to the Grand Lake

Stream project, and the trust can, perhaps, take advantage of some efficiencies.

There is a wide range of credits earned per acre. Northeastern projects typically earn 10‐25 credits per acre at

initial issuance. The Passamaquoddy and Howland projects demonstrate that the value of carbon projects

increases the longer the forest has been conservatively managed. The Howland Research Forest is dominated

by spruce and hemlock stands that average 140 years old, but that’s a rare occurrence in Maine where the

forests have been managed for 250 years.

Landownership Type and Culture The predominance of NGOs in the group of carbon project operators in Maine points to another factor which

influences whether and when landowners enter into the carbon market: the legal structure of the landowner

and their organizational mission. Each institution has its own legal structure, history and culture that influence

its values and tolerance for risk and regulatory oversight. There are some institutional landowners that have

made a commitment to offsetting climate change consistent with their organizational mission (e.g., the

Appalachian Mountain Club); others have a fiduciary responsibility to provide an income stream to shareholders

(e.g., family landowners). These are all important decision‐making characteristics that come into play when

making a 100‐year commitment.

The length of time a landowner plans to hold the land is a factor. TIMOs, REITs and Industrial landowners who

are not structurally committed to long‐term ownership must factor into their decision‐making process that a

carbon project may affect the sale price of a piece of land. On the other hand, it can also enable the seller to

benefit from the initial credit sale, while leaving the long‐term project costs to the new landowner (as with the

Lyme Grand Lake Stream project).

Different owner types have different needs in terms of revenue streams. Some owners, such as NGOs, may not

require much or any revenue from timber. Others may depend on a steady income from timber revenues and

may see the California forestry protocol as potentially conflicting with their needs.

Likewise, family ownerships rely on a steady stream of timber revenues over the long term. Carbon credits may

pay off up front, but the long‐term costs may mean that the carbon revenues need to be held in escrow for

project operation and maintenance costs rather than used for shareholder income, making the project less

attractive as a source of revenue.

Incentives for Landowners to enter Carbon Credit Programs

preferred FSC certification. There is no limitation of the SFI certification program with regard to the potential for enrollment of SFI certified lands in carbon offset projects.

Part II: Results from Survey of Maine Land SFI Participants

18

In sum, there is a robust, if short‐term, market for carbon credits through 2020 that Maine forest landowners

can take advantage of. There are important considerations for each landowner entering into the carbon credit

market, and there is no one‐size‐fits‐all approach to deciding whether the costs and risks are worth the tangible

and intangible benefits. Despite the deterrents discussed above, there are important incentives for all

landowners which include:

• Payments for conservative harvests, or no harvesting.

• Revenue from otherwise unmerchantable wood; and

• The opportunity to diversify revenue streams – from harvesting and from carbon.

In addition, some landowners may be able to:

• Capitalize on the expertise, staff and software needed for sustainability certification in order to manage

a carbon project over the long‐term; and

• Monetize carbon value that exists as a consequence of conservation or preservation practices that are

part of the organization’s mission or practice, but that would otherwise be unrealized.

Part III: Strengths, Limitations, Opportunities and Constraints of Carbon Credit Programs for SFI Participants

19

Part III: Strengths, Limitations, Opportunities and Constraints of Carbon Credit

Programs for SFI Participants The California ARB cap and trade regulations and Improved Forest Management protocol represent both

potential opportunities and constraints for forest landowners in Maine who are managing their lands in

accordance with forest sustainability certification criteria. There are also strengths and weaknesses in the forest

landowners’ decision‐making processes, along with a culture and history that make them more or less likely to

consider entering into carbon credit programs.

Landowner Strengths Since participation in one of the three sustainability certification programs (through the Sustainable Forestry

Initiative, Forest Stewardship Council, or the American Tree Farm programs) is the primary means of satisfying

the forest sustainability criterion for eligibility to participate in carbon credit programs, being an SFI participant

is an asset for those seeking credits. All the carbon credit programs recognize that sustainable harvests are a

prerequisite for maintaining carbon levels in managed forests.

Participation in SFI and other sustainability certification programs have other benefits, however, that are not as obvious. Certification programs have their own programmatic and practical requirements that confer advantages to participants seeking carbon credits. Sustainability certification requires the same centralized organizational, decision‐making, record‐keeping, and program monitoring structures that are necessary to develop and maintain a carbon credit program. In addition, both certification and carbon offset programs require:

• Sufficient ownership and tree cover to make forest and/or carbon management fiscally feasible; • Compliance with applicable laws and regulations; • Natural forest management practices; • Sustainable harvesting levels; • Forest monitoring activities; • Forest inventory data collection; • Growth and yield projections; and • Independent third party verification.

These requirements, in turn, necessitate having highly qualified staff who can utilize sophisticated software and sampling and inventory methodologies (or the capacity to manage relationships with consultants that provide these capabilities). The costs and rigor of carbon credit projects mean that landowners who are participants in sustainability programs have a substantial advantage in developing and/or maintaining a carbon project over non‐certified landowners. Relative to their certified peers, non‐certified landowners that participate in carbon offset projects will likely be more reliant on hiring new staff, training their own staff, and/or contracting with consultants over the 100 years of the carbon project, incurring additional project operations and maintenance costs.

Certification also necessitates that the landowner be willing to accept and manage long‐term agreements.

Forestry in general, but managing for sustainability and for carbon credits particularly, require long‐term

planning in accordance with performance standards. The forestry expertise, record keeping, staffing and

practices that certified landowners have in‐house enable them to conduct and implement these long‐term

plans, but also enable them to take on the operations and management of a carbon credit project with less

additional effort, time, and expense.

Part III: Strengths, Limitations, Opportunities and Constraints of Carbon Credit Programs for SFI Participants

20

Landowner Limitations There are some characteristics of forest landowner organizations that may make them less likely to participate

in carbon credit programs. Landowners who manage their lands extensively and intensively, whose annual

harvest levels equal or exceed net annual growth, or who maintain their forests with stocking levels that are

comparable to the regional average, are less likely to have sufficiently large areas with stocking levels that

exceed common practice to be good candidates for a carbon credit project. The forestland is less likely to earn

enough credits to cover the costs of project development, operations and maintenance, and reversal risk.

Ownerships with many shareholders (particularly family holdings) may resist carbon credit programs due to their

relatively complex decision making structure, and because they may prefer to distribute income immediately

rather than set aside a portion of the proceeds from carbon credits to cover long‐term project operations and

maintenance costs. Owners who are institutionally or culturally averse to risk, regulation, or long‐term

agreements are also likely to find carbon credit programs unpalatable.

Programmatic Constraints Maine’s SFI participants who responded to the survey for this paper mentioned several aspects of the ARB

program that had prevented them from applying for carbon credits. The biggest challenges for them were the

costs and risks of a carbon project over 100 years, weighed against the current markets for wood and relative

ease of subdividing and selling land.

Maine landowners and managers are particularly concerned about the lack of clarity regarding how reversals

from presalvage harvests will be handled by the ARB. Spruce budworm infestations can be expected to occur

two or three times over the minimum 100‐year life of a carbon project, and if credits must be repaid for

reversals from presalvage harvests, depending on the magnitude and intensity of the outbreak, it could pose a

considerable risk to the viability of a project.

The limitations on clearcutting and shelterwood harvests are a lesser deterrence for landowners, but a

deterrence nonetheless. In general, the “natural forest management” proscriptions on even‐age management

in the Forest Protocol are misaligned with management practices of most large commercial ownerships in

Maine. Even‐age management is a common tool in the state, and Maine forestry regulations already restrict

clearcutting. At the same time, millions of acres in Maine are managed to sustainability standards. It is not clear

that the Forestry Protocol adds anything of value to the offset carbon credit market beyond the state

regulations and sustainability certification rules, and for landowners, it only represents another layer of

regulation, requiring additional training, monitoring and reporting.

For certified landowners whose lands are encumbered by working forest conservation easements funded by

Land for Maine’s Future bonds, obtaining carbon credits for use in a compliance program such as the California

ARB cap‐and‐trade program is likely prohibited. The precise easement language has changed over time and it is

not clear whether every iteration applies to carbon credit programs, but language in the current easement

template specifically prohibits the landowners from obtaining carbon credits to offset “development”