Chapter 1 CAPITAL INVESTMENT APPRAISAL Learning outcomes After studying this chapter candidates must be able to: Demonstrate knowledge of key investment, regarding appraisal methods and the following. The concept of the time value of money Net present value (NPV) Real and normal interest rates Payback Internal rate of return Multiple IRRs Unequal Project appraisal & Audit INTRODUCTION Capital Budgeting involves the assessment of how much should be spent on assets or project and which assets should be acquired. Before deciding which project/assets to invest in, corporations must compare the benefits to be derived from the acquisition/investment against the costs involved in the investment. The investment will not purely depend upon financial aspects but to a large extent, the strategic direction of the business. Remember the financial decisions fall with the long-term corporate strategy formulation process. 1

Transcript

Chapter 1

CAPITAL INVESTMENT APPRAISAL

Learning outcomes

After studying this chapter candidates must be able to: Demonstrate knowledge of key investment, regarding appraisal methods and the following.

The concept of the time value of money Net present value (NPV) Real and normal interest rates Payback Internal rate of return Multiple IRRs Unequal Project appraisal & Audit

INTRODUCTION

Capital Budgeting involves the assessment of how much should be spent on assets or project and which assets should be acquired.

Before deciding which project/assets to invest in, corporations must compare the benefits to be derived from the acquisition/investment against the costs involved in the investment.

The investment will not purely depend upon financial aspects but to a large extent, the strategic direction of the business. Remember the financial decisions fall with the long-term corporate strategy formulation process.

Appraisal Methods

The main methods of investment appraisal, which are normally in use, are:

(a) Payback (b) Internal rate of return (c) Net present value (d) Accounting rate of return.

1

The investment appraisal methods can be divided into traditional and scientific methods. The traditional methods ignore the fine value of money whilst the scientific methods recognise the fine value of money in the evaluation.

Net Present Value (NPV)

The Net Present Value of a project is the difference between the sum of the project discounted cash inflows and outflows attributable to a capital investment or other long-term project.

The Net Present Value approach holds that cash received in the future is less valuable than cash received today.

In the Net Present value computations, all cash flows are expressed in present day values by the cash flows, which are realised in the future.

A comparison is then made, in present day terms of the total costs of the investment (cash outflows) and the total receipts from the investment (cash inflows).

When the present value of the inflows exceeds that of outflows (which includes any relevant taxation liabilities, as well as the more obvious initial investment outlay), the net present value is positive and purely on financial grounds, the investment should be accepted. In contrast, if the present value of the outflows exceeds the present value of inflows, the net present value is negative and the investment should be rejected.

Discount Factors/ Interest Rate

The interest rate, at which investors can borrow or lend money, is key to the Net Present Value model (NPV). The model is based on the assumption that an investor may invest money in the financial market at an interest rate prevailing or invest money in real assets, undertake a combination of the two options, or borrow in order to invest in real asset.

Real assets will only be attractive to a rational investor if they offer a rate of return in excess of the cost of money (the rate at which the money has been borrowed).

By discounting the financial costs and benefits associated with real assets at this rate, the investor can determine whether a return in excess of discount rate ‘r’ is available from the real asset in question.

NPV and The Agency Theory

Senior managers of an organisation normally save the interests of shareholders and they are thereby employed to maximise the wealth of shareholders.

Since Net present Value models decision rule advocates that a project whose financial benefits outweigh its financial cost, henceforth having a positive net present value should

2

be accepted and be pursued and vice versa. The net present value upholds the thenetical sole objective of business of maximisation of shareholder’s wealth through maximisation of returns from the project.

Assumption in Net Present Value

The Net Present Value technique is based on the following assumption.

The Discount rate must be a measure of the opportunity cost of funds for wealth maximisation to result.

Perfect capital market and perfect information exists The model assumes that a single rate which reflects the opportunity cost for all

individuals and companies. All Shareholders have an objective of wealth maximisation

Net Present Value, Risk and Uncertainty

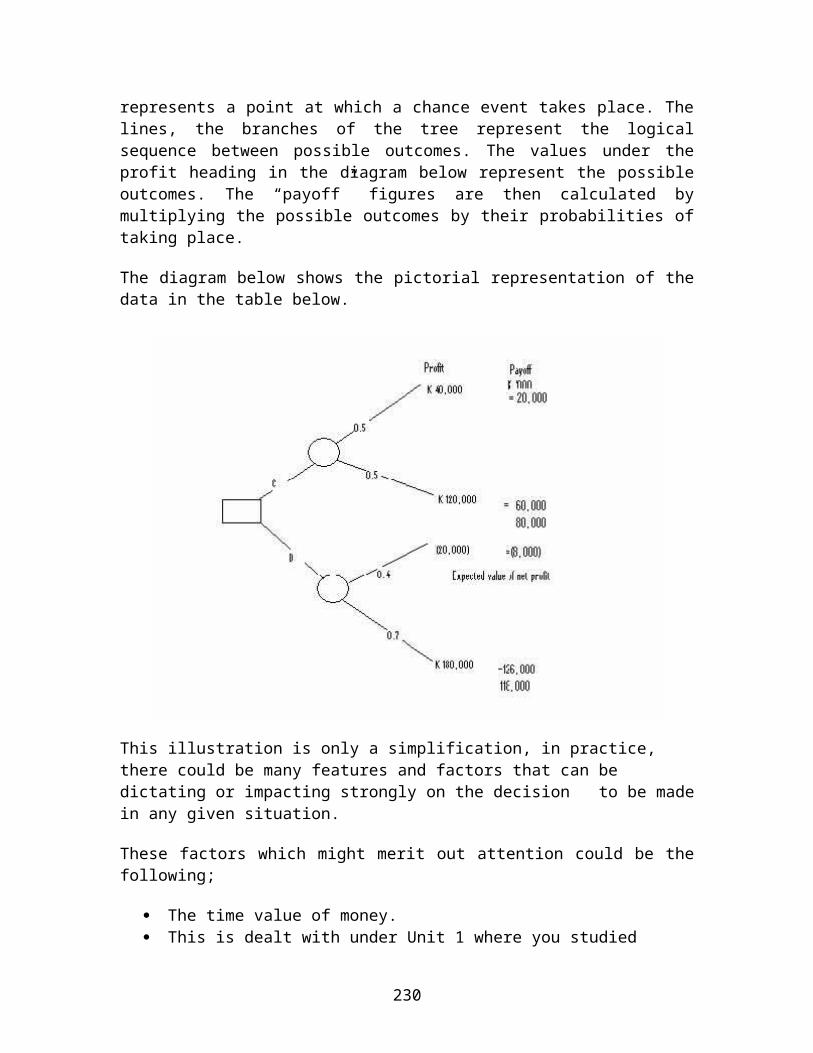

Risk management does not leave out project appraisal and evaluation process. Past experiences can be new, is a guide in assigning specific possible outcomes for the action currently proposed. This can also be used as the basis for assigning probabilities to these outcomes what we can use to calculate the expected cashflows of a project for our NPV computations. In the absence of past experience, we would have no basis upon which we can base our probability on. Advanced risk analysis and management are outside the scope of the text.

Example

Chaswe Engineering Consultants have been engaged in developing four (4) projects on behalf of their client, Ninsh Corporation.

However, the project sponsors, Ninsh Corporation have asked their Management Accountant to evaluate the 4 projects for their viability before it commits its finances to the projects.

The cost of funds for NINSH Corporation is 5%.

3

Required

In your capacity as Management Accountant of NINSH Corporation, evaluate the viability of the four (4) projects given that the cash inflows and cash outflows of the projects are as shown below on the Net Present Value basis.

Project: A B C D

Capital K’000 K’000 K’000 K’000(Outlay) year 0 (40,000) (40,000) (20,000) (20,000)

Project B, C, & D are giving positive present values indicating that purely on financial information, they are viable and hence management of Ninsh Corporation should undertake the projects in order to maximize shareholder wealth.

Project A is yielding a negative net present value and hence, purely on financial grounds, the project should not be undertaken as it is posed to destroy value of Ninsh Corporation.

Internal Rate of Return (IRR) Internal rate of return is achieved by a project at which the sum of the discounted cash inflows over the life of the projects is equal to the sum of the discounted cash flow.

In other terms, the IRR of an investment is that rate which when used to discount the cash flows of the investment will result in a rate present value of zero. The IRR of a project with conventional cashflows can be calculated using a process of trial and error.

The following steps represent a systematic, methodical trial and error approach to the calculation of project IRR.

1. The net present value of the project at zero interest rate needs to be established. This must be a positive figure if an investment with conventional cashflows is to have a positive IRR.

2. A positive discount rate should be selected and the Net Present value of the project at this rate is calculated.

3. The procedure under (2) should be repeated for one or more additional discount rates. The Net Present Value profiles should be sketched and an approximate IRR estimated.

Example

Suppose a company has project Y with the following cashflows to evaluate. Estimate the IRR of project Y using the data given at a cost of capital of 14%.

Project Y Cash flows Year K’000

0 (20,000) 1 200

2 2003 160,0004 160,000

6

Solution:

Years Cashflows Discount Present ValuesFactors (14%)

In case the IRR, the decision rule is to compare opportunity cost of funds and accept the project if the IRR is greater than the company’s cost of money and reject it if it is not i.e. purely on financial grounds.

This decision rule would always lead to the selection of an identical set of projects as the application of NPV rule given the assumptions that have been made so far namely; certainty, conventional cashflows and perfect capital markets and the additional assumption of independent projects.

The Reinvestment Assumptions

The Net Present Value technique assumes that all cash flows from a project will be re-invested at the discount rate used in the calculation of the project’s net present value, which in a real/free world is the prevailing base interest rate.

This assumption is realistic as application of the NPV rule means that all projects offering a return in excess of the discount rate will be accepted and the marginal funds are invested at the prevailing interest rate.

In contrast IRR assumes that all cash flows will be reinvested at the projects own IRR. There are not practical supporting reasons for this assumption though.

This assumption will lead to favour projects with concentrated cash flows in the early years of the project running than those with low cash flows in the early years of running.

This can be illustrated by using an example of 2 projects M & K and calculations of their terminal values. In the early years of the project running than those with low cash flows in the early years of running.

The terminal value of an investment is the total value of the cashflows generated by an investment at the end of its life.

7

In calculating the terminal values, interim cash flows must be projected forward to the end of the investment’s life by the application of a particular reinvestment rate.

The Net terminal value is calculated by subtracting the terminal value of the initial investment from the terminal value of the cashflows.

It’s assumed below that the interim cashflows will be reinvested at 5%.

Projects M K Years cash flows cash flows K’000 K’000

By definition, the IRR is the discount rate of zero and you should not be surprised to see that it is also the discount rate which gives a net terminal value of zero. This is clearly seen in the case of project K; the small positive NTV of M arises because 49% is a slight under estimate of the IRR as perusal of the above analysis.

Example

Seakwe Ltd is considering which of two mutually inclusive projects it should undertake. The finance director thinks that the project with the higher net present value should be chosen where the managing director thinks that one with the higher IRR should be undertaken especially as both projects have the same initial outlay and length of life. The company anticipates a cost of capital of 10% and the cashflows of the projects are as follows:

(2). The recommendation should be to undertake Project X for the following reasons:

Project X has a positive Net Present Value, showing that it exceeds the company’s cost of capital.

In addition, assuming that the company’s object is to maximise the Present Value of future cashflows Project X offers the higher Net Present Value.

Project X indicates a higher NPV, whereas project Y offers a higher internal rate of return where such conflicting indications appear, it is generally appropriate to accept the Net Present Value result, net present value being regarded as technically more sound than internal rate of return.

The two projects have radically different time profiles. Projects X’s cashflows are grouped in the three middle years of the project, while nearly 90% of Y’s inflows come in the first year of the project, leading to a situation where project Y shows a higher internal rate of return.

10

Risk, uncertainty and timing if cashflows may be considered by the Directors in making the final investment decisions.

+100+80+60+40+20

0 10 20 30 40 60-20 Discount rate; %-40

Although in the above illustration we have shown the graphical representation using straight lines, the true relationship between the Net Present Value and discount rate is a cumulative one.

Multiple IRR (Multiple Yields)

At this point in time, we would want to appreciate that in cases where a project does not have conventional cashflows, there is a possibility of having multiple IRR in the project whose cashflows are unconventional.

By a project having conventional cashflows, we mean that there will be a cash outflow followed by a stream of inflows.

A project with non- conventional cashflows may have a cash outflow followed by an inflow or inflows then followed by a further outflow or by further outflows.

As a result of these cashflows coming in and out of the project at different times, the IRR computation might give rise to two or more internal rate of return rates.

Example

Lunga Plc is proposing making a machine it will use in its manufacturing process, the cost of which will be paid in two stages. Revenue can be expected from its demonstration, although it will be expensive to break up and dispose of at the end of its useful life. The cashflows associated with the project are as follows.

11

Years Cash flows K’000

0 (7,820)1 (20,000)2 80,0003 (53,020)

The appropriate discount rate is 15%.

Solution:

This project has two internal rates of return as shown below.

Years Cash flows Discount PV K’000 Factor (6%) K’000

As both IRRs are equally valid, the decision whether or not to accept this investment cannot be made by reference to these rates alone. Therefore, NPV method can be used to get a clearer result.

If NPV shows that the NPV of the same project lower consideration is positive, then the project should be accepted as it shows that the net financial benefits far outweigh the financial costs of the project and hence demonstrating financial viability of the project.

Internal Rate of Return for Projects With Unequal lines

When two projects or more mutually exclusive investments with unequal lives are being evaluated and compared, consideration must be given to the time period over which a comparison of the investments is to be made.

Example

Consider two projects

Years 0 1 2 K’000 K’000 K’000

Project P (60,000) 40,000 40,000

Q (60,000) 75,100 -

Compute the IRRs of the two projects assuming a cost of capital of 10%.

A comparison can be made over an equal time span for both investments; the lives of P and Q can be equalised by assuming that the company can invest in another project like Q at the end of year 1. The cashflows of two consecutive investments in Q would be as follows:

(1) Using unadjusted K’000 IRRCash flows NPVP = 4,711 22%(i.e. P over 2 yrsand Q over 1 yr) NPVQ = 4,090 25%

13

(2) Cashflow adjusted to K’000 IRR Equalise project lives NPVP = 4,711 22% (i.e. P over 2 yrs and

Q over 2years) NPVQ = 7,810 25%

Conclusion and analysis

Ranking project P and Q on an IRR basis makes project Q the superior choice, irrespective of the period over which the comparison is made.

In conclusion, regardless of the project lives, the project with a higher IRR should be chosen as the IRR does not seem to be affected by the length of the project life or repeated reinvestment of the cash flows. TRADITIONAL APPROACHES TO PROJECTS/CAPITAL INVESTMENT APPRAISAL

As you can remember, from the outset of the chapter, the payback period and accounting rate of return are the commonly used traditional methods of appraising capital investments.

Payback Period Method

Computation of payback period of a project is the time required for the cash inflows from a capital investment project to equal the cash outflows.

If we assume that cashflows are received at the end of each year, the payback period for the four projects below will be:

The pay back period for the projects is as follows:

Project Payback period

A 2 years B 4years C 2years D 4years

14

In practice corporations will have a benchmark of the payback period, which is going to be adopted in their company policy as the threshold or cut off point for appraising and assessing the payback periods of projects.

For instance if the company above has a corporate policy of only accepting project with payback period of 3 years only project A and C promise to payback a three year period.

Hence only project A and C would be accepted and be undertaken in this instance.

Decision rule:

Only projects with short payback periods are preferred. Limitations of Payback Period Method

The payback period method has a limitation not taking the time value of money into consideration and it ignores the future cashflows beyond the payback threshold as per company policy no matter how healthy the cashflows might be.

Discounted Payback Period

In order to go round the problem of the lack of recognition of the time value of money some evaluators opt to use discounted pay back where the payback of the project is deferred using discounted cash flows as opposed to simple cashflows.

Exercise

Please compute the present values of the cashflows from the above 4 projects A, B, C and D at a cost of capital of 5% and you will discover that the discounted payback (year) will be as follows:

Project Discounted payback (years) A No Payback B 4 yearsC 2 yearsD 4 years

This is a slightly more comprehensive evaluation that the crude simple method of using simple cash flows.

15

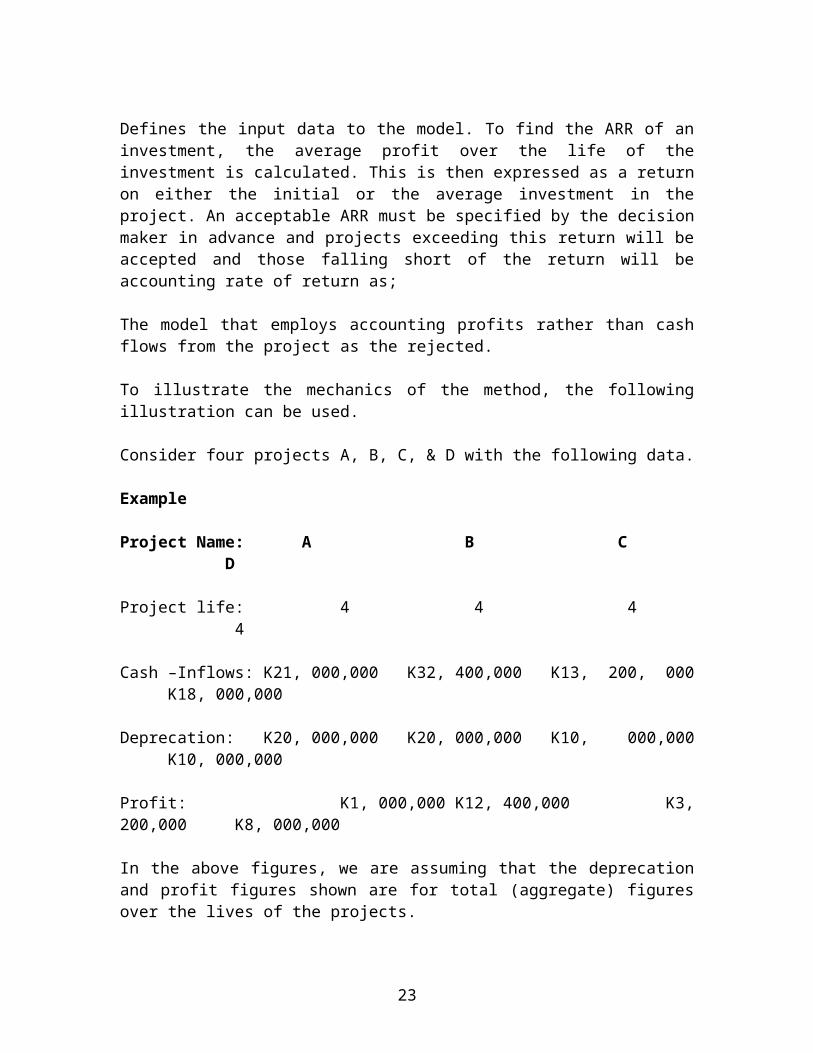

The Accounting Rate of Return (ARR)

Computing Accounting Rate of Return

A mathematical expression of:

Average annual profit from an investment x 100Average Investment

Defines the input data to the model. To find the ARR of an investment, the average profit over the life of the investment is calculated. This is then expressed as a return on either the initial or the average investment in the project. An acceptable ARR must be specified by the decision maker in advance and projects exceeding this return will be accepted and those falling short of the return will be accounting rate of return as;

The model that employs accounting profits rather than cash flows from the project as the rejected.

To illustrate the mechanics of the method, the following illustration can be used.

Consider four projects A, B, C, & D with the following data.

In the above figures, we are assuming that the deprecation and profit figures shown are for total (aggregate) figures over the lives of the projects.

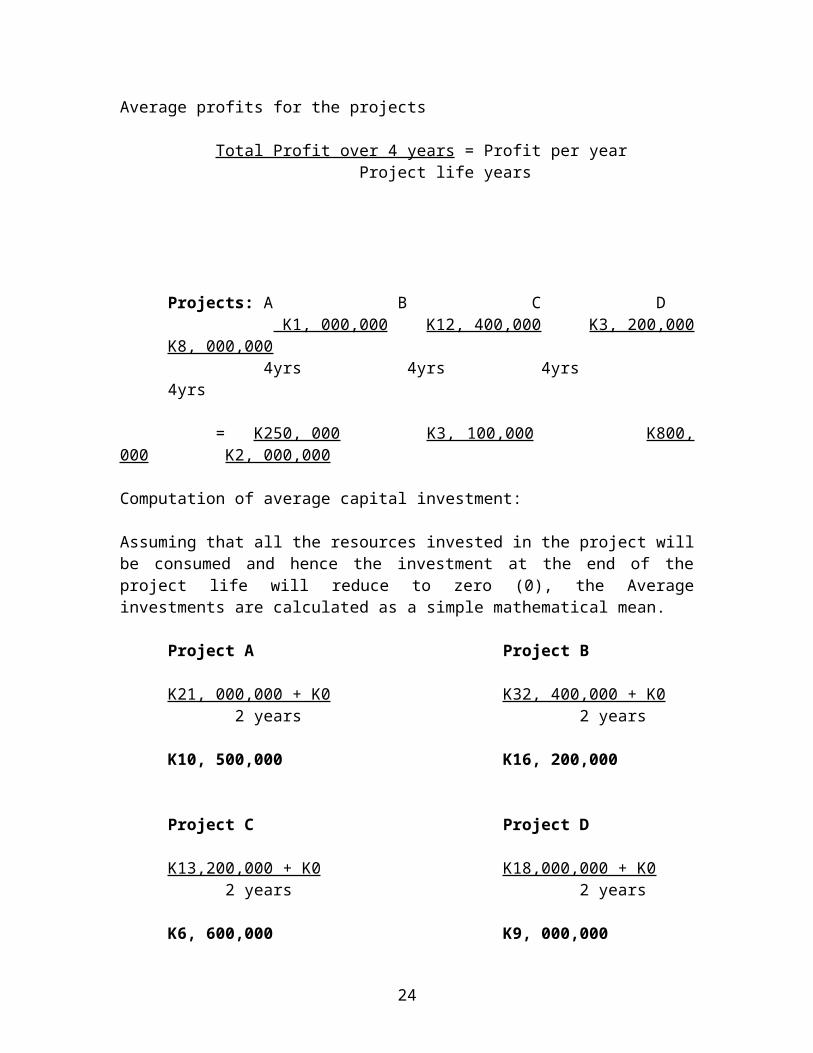

Average profits for the projects

Total Profit over 4 years = Profit per year Project life years

16

Projects: A B C D K1, 000,000 K12, 400,000 K3, 200,000 K8, 000,000

4yrs 4yrs 4yrs 4yrs

= K250, 000 K3, 100,000 K800, 000 K2, 000,000

Computation of average capital investment:

Assuming that all the resources invested in the project will be consumed and hence the investment at the end of the project life will reduce to zero (0), the Average investments are calculated as a simple mathematical mean.

Project A Project B

K21, 000,000 + K0 K32, 400,000 + K0 2 years 2 years

K10, 500,000 K16, 200,000

Project C Project D

K13,200,000 + K0 K18,000,000 + K0 2 years 2 years

K6, 600,000 K9, 000,000

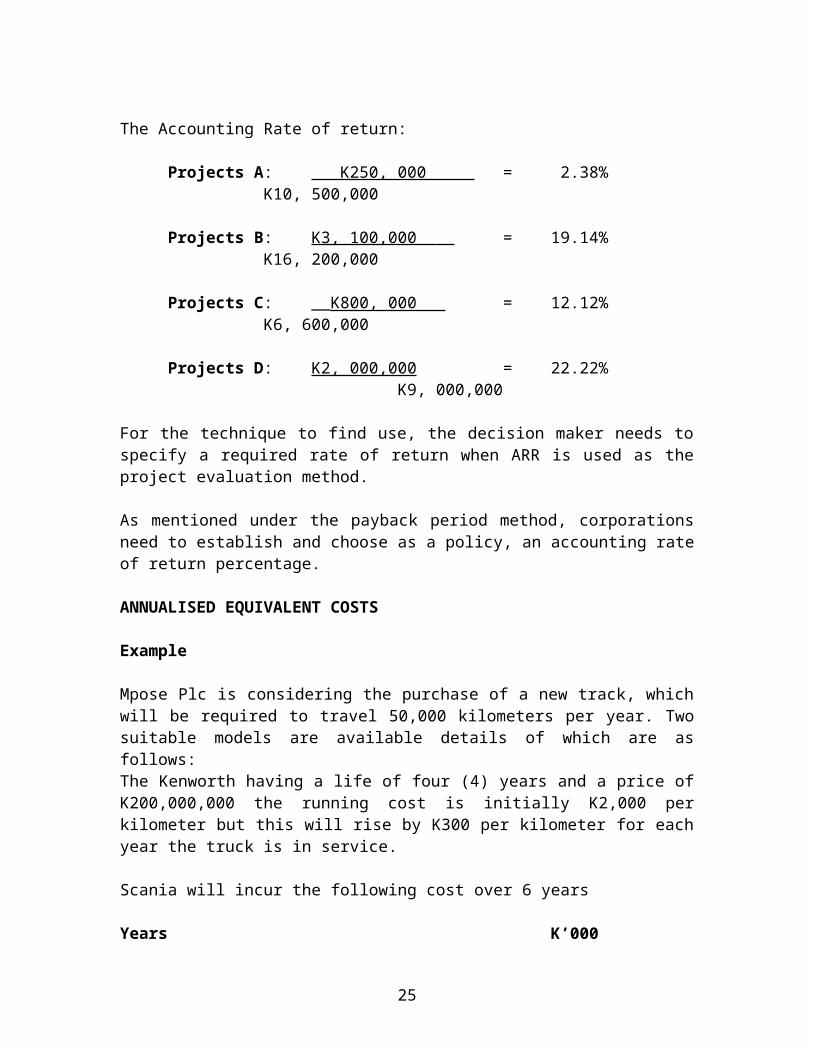

The Accounting Rate of return:

Projects A: K250, 000 = 2.38%K10, 500,000

Projects B: K3, 100,000 = 19.14%K16, 200,000

Projects C: __K800, 000 = 12.12%K6, 600,000

Projects D: K2, 000,000 = 22.22% K9, 000,000

For the technique to find use, the decision maker needs to specify a required rate of return when ARR is used as the project evaluation method.

17

As mentioned under the payback period method, corporations need to establish and choose as a policy, an accounting rate of return percentage.

ANNUALISED EQUIVALENT COSTS

Example

Mpose Plc is considering the purchase of a new track, which will be required to travel 50,000 kilometers per year. Two suitable models are available details of which are as follows:The Kenworth having a life of four (4) years and a price of K200,000,000 the running cost is initially K2,000 per kilometer but this will rise by K300 per kilometer for each year the truck is in service.

Scania will incur the following cost over 6 years

Years K’0000 350,0001 75,0002 90,0003 105,0004 120,0005 135,0006 150,000

The cost of capital for Mpose Plc is 12%

Required:

Explain which truck (between the Kenworth and the Scania) should be purchased.

Solution:

As we can see the comparison of the two projects is complicated by their unequal lines. We are going to use annualized costs to compare the two projects. Therefore the annualized cost of the Kenworth is:

Year Costs K’0000 200,0001 100,0002 115,0003 130,0004 145,000

This is determined by calculating the Net Present Value of acquiring and operating a Kenwork truck over four years and converting it an equal annual equivalent cost by dividing the Net Present Value by 3.037.

Therefore in conclusion, the Kenworth Truck is the best option with a lower annualized cost.

19

PREFERENCE FOR APPRAISAL METHOD

Investment Appraisal method

Advantages and disadvantages of Investment Appraisal Methods

PAYBACK PERIOD METHOD

Advantages

(a) It is easily understood and interpreted, especially to non-financial managers, and its implications for liquidity are clear.

(b) It can be used as preliminary project appraisal screening method, before scientific methods (discounted cash flows are applied for the appraisal process).

Disadvantages

(a) It ignores cash flows beyond the payback period and it does not take into account of the time value of money.

NET PRESENT VALUES

Advantages

(a) It takes account the timing of cash flows.(b) It takes proper account of the size and duration of projects.(c) It takes into account the greater uncertainty of later years’ cash flow by using a

higher discount rate for these years.

Disadvantages

(a) It produces a number which is less familiar to management than a rate of return.(b) It's complex in its mechanics.(c) Not easily understood by non-financial managers.

INTERNAL RATE OF RETURN

Advantages

(a) It takes into account of the timing of the cash flow.(b) It is easily compared to a given return, which project owners are looking for, in

assessing a project’s viability.

20

Disadvantages

(a) It does not take account of the size of the project, so a small project with a high return looks better than a large project with a lower return, even through the latter will contribute more to earnings.

(b) The Internal Rate of Rate (IRR) cannot evaluate properly the duration of projects. This is because IRR takes no account of what happens to the returns after they are achieved.

(c) Another potential difficulty, which may sometimes arise, is the possibility of two or more solutions to the IRR calculation. This usually happens when a project has unconventional cash flows, meaning that cash flows with negative and positive signs may come through during the life of the project.

Capital Replacement

Corporations will most times want a specific type of capital asset for a period of time which exceeds the physical life of any one individual asset, or part of an asset or part of that type. For instance, demand for the output of a particular production process may extend into the indefinite future, whereas the life of the machine required carrying out the process will be limited to a finite period.

Asset replacement may be undertaken in response to the poor physical condition of an asset or more reasonably replacement may be planned. The timetable for a planned replacement will be determined by a consideration of the costs of replacing over one time horizon rather than other.

Consider the example of a company which provides its entire sales people with a company car. The cost to the company of providing the car is made up of the initial capital cost and the annual running costs, less the resale value at the time of disposal. Data on the type of car, which our hypothetical company provides for its sales people, is given below.

K’000Initial purchases price: 50,000Annual running cost (average per year) 20,000Re-sale value if sold after: 2yrs 30,000

3yrs 25,0004yrs 15,0005yrs 5,000

21

Since the company requires the cars to extend into future, a replacement policy must be decided upon. If the company would like to minimise the overall cost of operating its fleet of cars, cars should be replaced at the point in time at which this cost is minimised. For ease of exposition we would assume that the annual operating cost is independent of the age of the car and that the data given above will remain valid indefinitely. As the annual operating cost is constant, irrespective of the replacement cycle it can be ignored for the purposes of setting the replacement policy. Therefore what needs to be considered are the purchase price of the car and the resale value.

Although, the purchase price itself is not variable the total expenditure of the company is variable as it depends on the sale of the cars, which in turns depends on the replacement cycle. The net cost of the investment in each car is given by the initial outlay less the present value of the sale proceeds.

Assuming a cost of capital of 5%, the computation would be as below.

Schedule 1

Year Resale Discount Present Purchase Net PresentValues factor (5%) values price cost K’ 000

The final column of the table shows the net present cost of owning the car over differing time periods, two years in the case of the first row, and three years for the second row etc. This cost does not of itself provide a basis for comparing the relative attractiveness of the alternative replacement cycles. In order to make such a comparison, the cost must be expressed as a net present cost per annum, which is obtained by dividing the net present cost over the relevant time period. This procedure allows the expression as an annual figure of a cost or income occurring on a regular but not annual basis.

For example taking the figures in the first row of the schedule, the K22,790,000 spent today is equivalent to an expenditure of K12,256,642 (22,790,000/1.8594) for each of the next two years at the discount rate is 5%, we would be indifferent as to which spending pattern we incurred.

It can be seen that the minimum annual equivalent cost is K10, 431,000 the cost of replacing the cars on a three-year cycle. Other things being equal the company should adopt a three-year replacement policy.

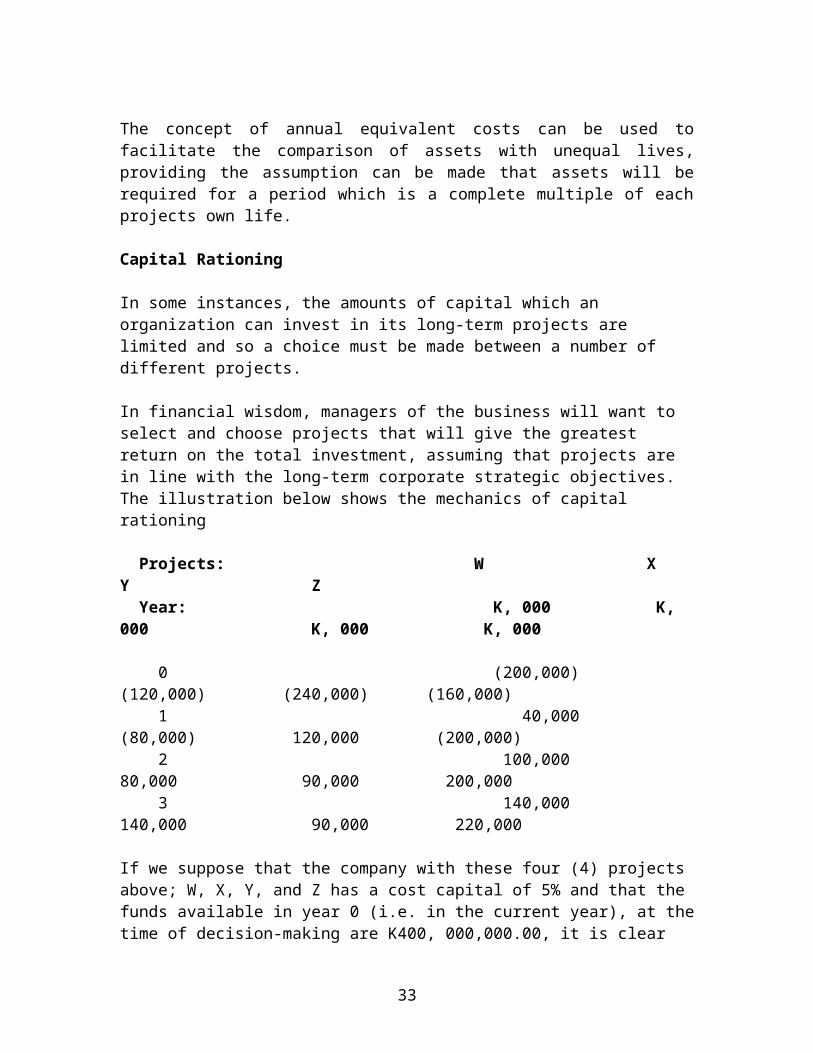

The concept of annual equivalent costs can be used to facilitate the comparison of assets with unequal lives, providing the assumption can be made that assets will be required for a period which is a complete multiple of each projects own life.

Capital Rationing

In some instances, the amounts of capital which an organization can invest in its long-term projects are limited and so a choice must be made between a number of different projects.

In financial wisdom, managers of the business will want to select and choose projects that will give the greatest return on the total investment, assuming that projects are in line with the long-term corporate strategic objectives. The illustration below shows the mechanics of capital rationing

Projects: W X Y Z Year: K, 000 K, 000 K, 000 K, 000 0 (200,000) (120,000) (240,000) (160,000) 1 40,000 (80,000) 120,000 (200,000) 2 100,000 80,000 90,000 200,000 3 140,000 140,000 90,000 220,000

If we suppose that the company with these four (4) projects above; W, X, Y, and Z has a cost capital of 5% and that the funds available in year 0 (i.e. in the current year), at the time of decision-making are K400, 000,000.00, it is clear that even if the net present values are positive the organization cannot invest in all four projects.

23

Using the profitability index technique of ranking project will be employed to rank projects.

The first step is to calculate the net present values of the projects and then express them as a percentage of the project outflow so that comparable returns are obtained.

The computation below shows the return from each project and their rankings.

Discount W X Y Z Rate @ 5% K, 000 K, 000 K, 000 K, 000 Year 0 1.000 (200,000) (120,000) (240,000) (160,000) 1 0.952 40,000 (80,000) 120,000 (120,000) 2 0.907 100,000 80,000 90,000 200,000 3 0.864 140,000 160,000 90,000 220,000 Discounted cash flows

Analysis and comment As it can be seen above, all projects have positive net present values and so they would be accepted if funds allowed.

24

With only K400, 000,000 to invest, project W would be chosen and 5/6 of project Y, assuming that the investments are divisible.

In many circumstances, divisibility of projects might not be possible, so decisions will have to be made based on net present value technique.

Capital rationing is not really a practical approach for the majority of organizations. It usually works very well if the company in question is not an Investment Company but for most of organizations providing a service or manufacturing products, this solution will not be very helpful.

Effects of Taxation on Investment Appraisal

Although in many instances we are assuming that there are no taxes in perfect financial markets, in reality taxes are usually levied on income earned from investment.

The section aims to show the effects of taxation on investment appraisal.

However, the section starts by looking at basics of discounting future cashflows, which is going to be used widely in capital investment appraisal.

Discounting Methods

Time value of money

Cash flows arising at different points in time cannot be compared directly and must be converted to a common point in time i.e. usually discounted to their present values.

Years 0 1 2 3 4

Discounting

Present value Future value

Present value (PV) is the cash equivalent now of money received/payable at some future date.

25

PV FV

Exercise

Choose between Year 0 (now) Year 5 K10,000,000,000 K5,000,000,000The discount rate is 10%Please make your decision by first discounting and then compounding.

Discounting Year 0 (now) Year 5 K10,000,000,000

K9,315,000,000 = 0.621 x K1, 500,000,000

PV = FV x 1/ (1+r) n

Compounding Year 0 (now) Year 5PV (1 + r) n = FV 10,000,000,000 × (1.1)5 = K16,105,100,000

Therefore we would choose the K10,000,000,000 now with both methods, please note that discounting is the preferred method of comparison in SFM.

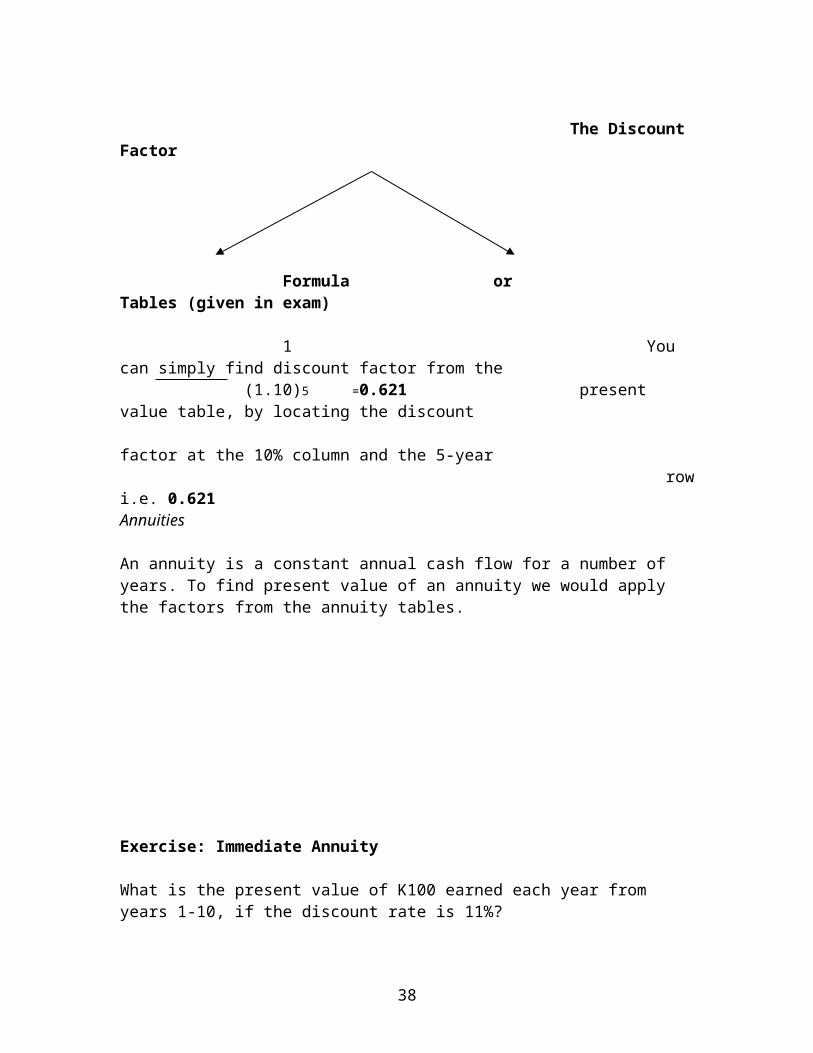

The Discount Factor

Formula or Tables (given in exam)

1 You can simply find discount factor from the (1.10)5 =0.621 present value table, by locating the discount factor at the 10% column and the 5-year row i.e. 0.621Annuities

An annuity is a constant annual cash flow for a number of years. To find present value of an annuity we would apply the factors from the annuity tables.

26

Exercise: Immediate Annuity

What is the present value of K100 earned each year from years 1-10, if the discount rate is 11%?

x

The annuity factor at year ten adds together all the present value factors for the first ten years. In fact the annuity is quite often called the cumulative present value factors. The annuity factors assume that the first cashflow occurs at the end of year one i.e. the first present value factor added in an annuity factor is for year one. Therefore when the first cash flow arises in year one you simply have to apply the annuity factor to find the present value of the annuity. An annuity which commences in year one is called 'an immediate annuity’.

Answer: PV = K100 X 5.889 = K588.9

Exercise: Deferred Annuity

What is the present value of K200 incurred each year from years 3-6 the discount rate is 5%? Answer:

The annuity factor brings all the cash flows to one year before the first cashflow arises. As the first cash flow is in year 3, all the cash flows have been brought to year 2.

To find the present value (year 0) of the annuity, which is currently valued in year two we must multiple it by the present value factor for year two.

27

1 2 3 4 5 6 7 8 9 10

(1 - 4)

0 1 2 3 4 5 6

PV

200 200 200 200

Answer = Apply the structured approached to deferred annuities:

1. Annual cash flow K200 X

2. Annuity factor for two years 1 to 4 3.546 X3. Present value factor for year 2 0.907

Present value of deferred annuity K643

Perpetuities

Perpetuity is an annual cash flow forever. It is the simplest cash flow model known to man. Goddard often implies perpetuity by simply stating, “The cash flows will occur for the foreseeable future”.

The Basic Perpetuity

PV of a perpetuity = Po = annual cash flow r

Discount rate = r = annual cash flow Po Exercise

What is the maximum amount you would pay for perpetuity of K 25,000 per annum, if the discount rate is 10%?

Answers Po = K25, 000 = K250, 000 r = 25,000 = 0.10 10 250,000

Perpetuity with Constant Growth

Perpetuity formulae also assumes that the first payment will be at the end of year one, thus they also bring the cash flows back one year.g = growth expressed as a decimal.

PV of perpetuity – Po = Cash Flow Year 0* (1+ g) r – g

Discount rate in a perpetuity – r = Cash Flow Year 0* (1 + g) Po + g

28

Exercise

What is the PV of perpetuity of K 25,000,000,000 per annum increasing at an annual rate of 5%, if the discount rate is 10% and the first payment is in year 1?

Answer:

Exercise 6: An NPV calculates with both deferred annuity and a deferred perpetuity.

The Financial Director of A plc has prepared the following schedule (excluding inflation) to enable her appraise a new project. The project’s real WACC is 10%. She wants to calculate the NPV using two different assumptions regarding the project duration. The assumptions are as follows:

a) That the real annual cash flow will be K 250,000,000,000 from year to the foreseeable future (deferred perpetuity).

b) That the real annual cash flow will be K250, 000,000,000 from year to year eighteen (deferred annuity).

Receipts – (or cost savings) X X X XPayments:Wages (X) (X) (X) (X) Materials (X) (X) (X) (X)Variable / Fixed overheads (X) (X) (X) (X)Administration / Distribution expense (X) (X) (X) (X)Capital Allowances/Tax allow dep (X) (X) (X) (X)

Taxable Profits = EBIT X X X X

Tax: (X) (X) (X) (X)

Add back: Capital Allowances X X X X

Initial outlay (X)Net Realisable Value X

Working capital (X) X

Net Cash Flows/Free Cash Flows (X) X X X X

Discount rate (X%) X X X X X

Present value (X) X X X X

Net Present Value X(X)A positive NPV is when the expected return on a project more than compensates the investor for the perceived level of (systematic) risk i.e. that the expected is greater than the required return.

Decision Rules:

Single Project:

Positive or zero NPV: Based on the estimates it appears that the project is financially viable.Negative NPV: Based on the estimates it appears that the project is not financially viable.

Mutually exclusive project (A or B): (an absolute decision not a relative decision)

Simply pick the project with the highest positive NPV.

30

The Relevant Cash Flows A key concept => include relevant / incremental cash flows in the NPV calculations.

FUTURE CASH FLOWS THAT ARISE AS A CONSEQUENCE OF THE DECICSION

1. Ignore all sunk costs incurred prior to the decision. Ignore all sunk revenues generated prior to the decision. Sunk costs are costs which have already been incurred prior to the decision. They are therefore irrelevant to the decision making process.

Exercise: R+D of K100, 000 was incurred last year.

2. Ignore all non-cash flows. E.g. depreciation.

Exercise: A company is considering investing in a project, which requires an immediate investment of K6m. This project will last for five years and at the end of the project the plant will have a scrap value of K1m. The company depreciates plant on a straight-line basis over a five-year period. What are the relevant cash flows?

Answer: Simply when you buy and a fixed asset.

3. Ignore all overheads in existence prior to the decision i.e. non-incremental cash flows. The allocation / apportionment of fixed costs already present prior to the decision are ignored.

Exercise: A manufacturing company is considering the production of a new type of widget. Each widget will take two hours to make. Fixed overheads are allocated on the basis of K1 per labour hour. If the new widgets are produced the company will have to employ an additional superior at a salary of K15, 000 per annum. The company will produce 10,000 widgets per annum. What are the relevant cash flows?

Answer: The K15,000 salary only.

Exam Focus: If you are calculating an NPV in relation to the purchase or sale of a company you should include all existing fixed costs because to the purchaser / seller they represent future cash flows will commence / cease sale.

4. Ignore interest payments and their tax effects as implicit in the discount rate. This is because if it were subtracted this would amount to double counting because the opportunity cost of capital already incorporates the cost of these funds. This simple example ignores tax relief on interest.

31

Market values Annual cash Cost of Capital Flows required

General inflation 2% Discount rate – factors Present value N.P.V

32

Two types of inflation

Specific inflation rates General inflation

Applies to all the individual cash flows items Applies to the discount rate

This is because the investors in a Project are interested in their ability to buy a basket of general goods. Not only one particular good.

The two methods

Includes the two types inflation Excludes the inflation

Money or normal Terms Real terms Discount “money” cash flows Discount “real” cash flows at money discount rate at real discount rate

Real term cash flows are Cashflows at current prices

or year zero

33

EXAM FOCUS:

When to use the money or Real method Is there one rate of inflation in the question?

No *Yes

Money / Nominal Method If the cash flows are in:

E.g. Wages 3%, Materials 4% and Real Terms Money Terms General inflation 5%

Real Methods Money Methods

* If there is one rate of inflation in the question both the real and money method will give the same answer. However it is easier to adjust one discount rate, rather than all the cash flows over a number of years. Thus the form of the cash flows defines the method to be used.

Adjusting the Discount Rate

Invariably Goddard will give you the cash flows in one form and the discount rate in the other form. So you will have to adjust the discount rate.

Cash flows in real terms Cash flows in money terms

Discount rate in money terms Discount rate in real terms

Deflate to find the real discount rate Inflate up to find money discount rate

Real discount rate to money discount rate

The fisher Equation

(1 + money rate) = (1 + real rate) x (1 + general inflation rate)

34

Exercise

If the real rate of return is 10% and general inflation is 5%, what is the money rate of return?

If the real rate of return is 8% and general inflation is 4%, what is the money rate of return?

Answer:

Money discount rate to Real discount rate

The money discount rate also sometimes called the market rate of return includes general inflation. Therefore to find the real rate of return you must deflate as follows:

Deflate:

1 + money rate = 1+ real rate 1+ general inflation

Exercise

If the money rate return is 14.4% and general inflation is 4%, what is the real rate of return?

Answer: (1.144/1.04) - 1 = 0.1 say 10%

Exercise

If the money rate of return is 13.42% and general inflation is 3%, what is the real rate of return?

Answer: (1.1342/1.03) – 1 = 0.10 say 10%

CASH FLOWS DEFINE THE METHOD ESPECIALLY WHEN THERE IS AN ANNUITY:

35

Exercise

ABC plc provides the following projected data for the next ten years excluding inflation.

0 1 2 3 – 10Net cash flows (1,700) 100 200 300

The rate of inflation is 3% and the market return is 11.24%

Calculate the present value of the cash flows over the 10-year period.

Real Method: - cash flows are in real terms; simply deflate the money discount rate to get the real rate.

Real discount rate: (1.1124/1.03) - 1 = 0.08 say 8%

Real cash flows:0 1 2 3 – 10

Net cash flows (1,700) 100 200 300Annuity factor 5.747Discount factor 1.000 0.926 0.857 0.857Present value (1,700) 93 171 1,478

NPV 42

Money Method: - calculate the money cash flows for each year and discount by the money discount rate.

“The understanding assumption that the general inflation rate is equal to the specific inflation rates for all the cash flows items is somewhat simplistic. In reality each cash

36

flow item would probably have a different specific rate of inflation, thus requiring the money method approach.”

Example:

Twincle Plc has provided and marketed camping kits for several years. The camping bags are much heavier than some of the modern camping kits being brought into the market. The company is concerned about the effect this will have on its sales. Twinkle Plc is considering investing in new technology that would enable them to provide a much lighter and more compact camping kits. The new machine will cost K500,000,000 and is expected to have a life of four (4) years with a scrap value of K20,000,000 in addition an investment of K70,000,000 in working capital will be required initially.

The following forecast annual trading account has been prepared for the project:

K’000Sales 400,000

Materials (80,000)

Labour (60,000) Variable overheads (20,000)

Depreciation (40,000)Annual profit 200,000

The company’s cost of capital is 10%. Corporation tax is charged at 30% and is payable quarterly, in the 7th and 10th months of the year in which the profit is earned and the 1st

and 4th month of the following year. A writing down allowance of 25% on a reducing balance is available on capital expenditure.

Required

Advise the management of Twinkle Plc on whether they should invest in the new technology

Your recommendation should be supported with relevant calculations. Solution

Writing down allowances

Year AssetValueK’000

30% TaxK’000

Year 1

K’000

Year 2

K’000

Year 3

K’000

Year 4

K’000

Year 5

K’000500,000

37

Yr1 25% WDA (125,000) 37,500 18,750 18,750375,000

Yr2 25% WDA (93,750) 28,125 14,063 14,063281,250

Yr3 25% WDA (70,313) 21,094 10,547 10,547 210,937

Yr4 Scrap value (20,000)Yr 4 Bal adjusted 190,937 57,281

Net Present Value of new technology investment. 141,406

Contribution = Annual Profit + Depreciation

= K200,000,000 + K40,000,000 = K240,000,000

Therefore purely on financial grounds, management of Twincle Plc should invest in the new technology, as the Net Present Value of the new technology is positive.

DIFFERENT NPV FORMATS

Exercise

DEF plc provides the following project financial data for the next 4 years, including inflation.

Year 1 Year 2 Year 3 Year 4K’000s K’000s K’000s K’000s

The rate of inflation is 3% and the real discount rate is 6.80%. Machinery cost K800, 000 life 4 years, tax allowance depreciation is at straight line and the tax rate is 30%.

Calculation of the present value of the cash flows.

Note: Only one inflation rate and cash flows are in money terms therefore use the money method. Therefore need to calculate money discount rate i.e. (1.03) x (1.068) = 1.10. i.e. 10%.

Assume that you have been appointed finance director of Breakall plc. The company is considering investing in the production of an electronic security device, with an expected market life of five years.

The pervious finance director has undertaken an analysis of the proposed project; the main features of analysis are shown below.

Proposed electronic security device project Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 K’000 K’000 K’000 K’000 K’000 K’000

Investment in depreciable Fixed assets 4,500Cumulative investment inWorking capital 300 400 500 600 700 700Sales 3,500 4,900 5,320 5,740 5,320

Treatment of Leasing and Hire Purchase Transactions

Introduction

Leasing is a technique used to finance the use of an asset. It is an alternative to outright purchase, financing by using existing cash reserves or by borrowing.

The motivation for choosing leasing rather than purchasing is often tax efficiency.

A lease contract is an agreement between the owner of an asset (the lessor) and the user (the lessee) under which.

- The lessee may have use of the asset for a specified period.

- The lessee in consideration for use of the asset promises to make a series of payments/ rentals to the lessor.

- The lessor remains the legal owner of the asset during the terms of the lease.

Typically lessors would be banks or subsidiaries of subsidiaries of banks. The lessee chooses the asset and the lessor / bank purchases the asset, thus fulfilling the ownership requirements for tax purchases.

Advantages of Leasing

There are two significant reasons for a company to lease assets rather than buying outright.

1. Tax benefits2. Flexibility / cash flow3. Access to additional sources of liquidity as a result of increased debt capacity.

Tax Benefits to the Lessor

Tax saving was the original drive or motivation behind the development of the leasing market. In many countries legal ownership of a qualifying asset entitles the owner (e.g. a bank) to amortize the capital cost over the life or the lease period of the asset for tax purposes.

This gave valuable cash flows benefits to those with the taxable capacity to sketcher their tax allowances.

42

Large commercial banks usually had such tax shelter, which they could use as lessors passing on to the lessee some of the economic benefits of tax relief cash flows.

Tax Benefits to the Lessee

While the tax charges reduce the benefits of leasing, the ability of lessors to pass on capital allowance tax benefits to lessees still makes leasing attractive for entities which have no tax capacity themselves.

The circumstances in which some entities might not have tax capacity and hence can benefit from leasing would include the following;

1. In a situation where a loss making business is still creditworthy

2. Where we have start-up projects or businesses, which may not move into profits for several years such as most Biotechnology companies and start-up information technology (IT) companies.

3. For institutions which do not pay corporation tax e.g. local authorities universities and colleges.

4. In a situation where a profitable corporation, with large continuing capital expenditure and consequent large capital allowances but with low profits available as tax shelter.

FLEXIBILITY AND ENHANCE CASH FLOWS

Whilst the availability of tax allowances continues to be important the users of the leasing market rely increasingly on the advantages of cash flows and flexibility.

Lease structures can be flexible and innovative and the payment schedules can be tailored to fit the projected cash flows arising from the underlying business. For some types of assets such as aircrafts computers, containers and rail wagons, complex structures have been developed which facilitate the marketing of asset reconciling the news of the buyer and setter on their deliveries. Types of Leases

There are two main types of lease:

1. Finance leases2. Operating leases

Finance Lease

43

A finance lease transfers substantially all the risks and rewards of ownership of an asset to be leased. The rewards and risks which are to a very large extent transferred are as fellows:

The full use of assets owner it’s economic Idle capacity Breakdowns Obsolescence

The conductance below usually acts as criteria for testing a finance lease. In many laitance of a lease is going to be classified as a finance lease.

1. The present value of retails for the leased asset usually exceeds the value of the asset.

2. In a situation where the primary contact parole is somewhat equal or approximately equal to the useful economic life of the asset in question.

3. Where the retorm is margin over the lessor’s cost of funds reflecting the credit rate the contract.

The main motivation of finance lease to the lessor is to make a profit by financing the asset. As we allowed to earlier, usually such lessor we financial institutions such as bank.

Operating Lease

By definition, an operating lease is one other than a finance lease.The motivation underlying an operating lease is the leased product (asset).

The following criteria will be distinguished with operating lease. Usually in operating lease the present value of the rentals is way below the asset value.Usually the lease life (tenure) is less than the assets useful economic life. Operating leases may be a sales aid for the product manufacture/ distributor. However, if the manufacturer does not have the finance or tax capacity to act as lessor it may engage the services of a finance institution to act on its behalf.

Features of Leases

- Lease rentals.Usually equal, but can be translated to sort the lessees cash flow if value contract is large enough to justify the effort.

44

- Usually underlying interest rate Usually fixed interest rates are used smaller items for simplicity and a floating rate for large items if the lessee requires it.

- Insurance and maintenance In finance leases the lessee will be responsible for payment of such costs where as in an operating lease since the lessor is clearly the legal owner and according to the substance over form standard, the lessor will be responsible for maintenance and insurance costs payments.

- Relocation With finance leases the lessee is usually responsible for relocating the asset to the lessors’ instructions at the end of the lease contract so it can be sold.

- Sale proceedsIn most situations the major part of the sales proceeds are typically passed to the original lessee as a refund of the lease rentals.

LEASE RENTAL COMPUTATIONSEXAMPLE – TREATMENT OF LEASING AND HIRE PURCHASE TRANSACTIONS

Singa Ltd owns 20 print and computer shops in Kitwe. At present it hires its 35 photocopying machines from Rent-a-copier Ltd at an annual Rental fee of K11,200,000 each, payable monthly (assume that cashflows occur at the year end).

The rental agreement covers a 24 hour repair service which assists Singa Ltd to maintain high reputation for a quick and reliable service. Singa estimates that each machine generates K15,200,000 of contribution each year. Xero company sells photocopier machines and is trying to break into the Kitwe market and offers to sell to Singa Ltd new machines for K36,000,000 each payable on installation. Singa Ltd is considering this and has found some research that suggests that each machine stands a 0.7 chance of being unreliable. The reliability of the machines will be discovered by the end of the first year. All machines that are reliable at the end of year 1 will still be reliable at the end of year 4. If a machine proves reliable, Singa Ltd will keep it for four (4) years in total and it will generate a contribution of K16,000,000 each year after which time it will be scraped and sold for K1,200,000. If the machine proves unreliable, it will be scrapped after year one (1) and sold for K800,000. An unreliable machine is expected to generate a contribution of K10,000,000 each year.

The company’s annual cost of capital is 8%. The management of Singa Ltd consider that a time horizon of no longer than 6 years should be used when evaluating decisions on photocopiers, as beyond the date photocopier machines are likely to be outdated technology.

Required:

45

a) Prepare computations to show whether a rented or purchased machine is the financially better option.

b) Xero Company has now made an alternative introductory, once only, offer. It will buy back 30% of the machines at the end of either the first or second year if, required.

The buy – back price will be 60% of the original purchase price at the end of year 1 and 50% at the end of year 2. Singa Ltd must nominate in advance which replacement option it prefers. If Singa Ltd agrees to either of Xero company’s proposals, it would remain with the company during the life of the purchased and replaced photocopiers. Because most shops have two photocopiers available, the management of Singa Ltd has now agreed that further replaced photocopiers available, the management of Singa Ltd has now agreed that further replacements after either year 1 or year 2 would be unnecessary.

Required

Advice Singa Ltd whether or not it should accept the revised offer.

- Having prepared the calculations in (a) and (b) you now realize that the effect of taxation should have been considered. The corporation tax rate is 30%. It is payable in four quarterly installments in the seventh and tenth months of the year in which the profit is earned and in the first and fourth months of the following year. The equipment will qualify for a 25% annual reducing balance writing down allowance. Assume that the 8% cost of capital is the after tax rate for part (c).

Required:

Explain and illustrate with calculations the impact of taxation on the financial appraisal of: a rented machine a purchased reliatie machine (that is one that is kept for 4 years).

Solution:

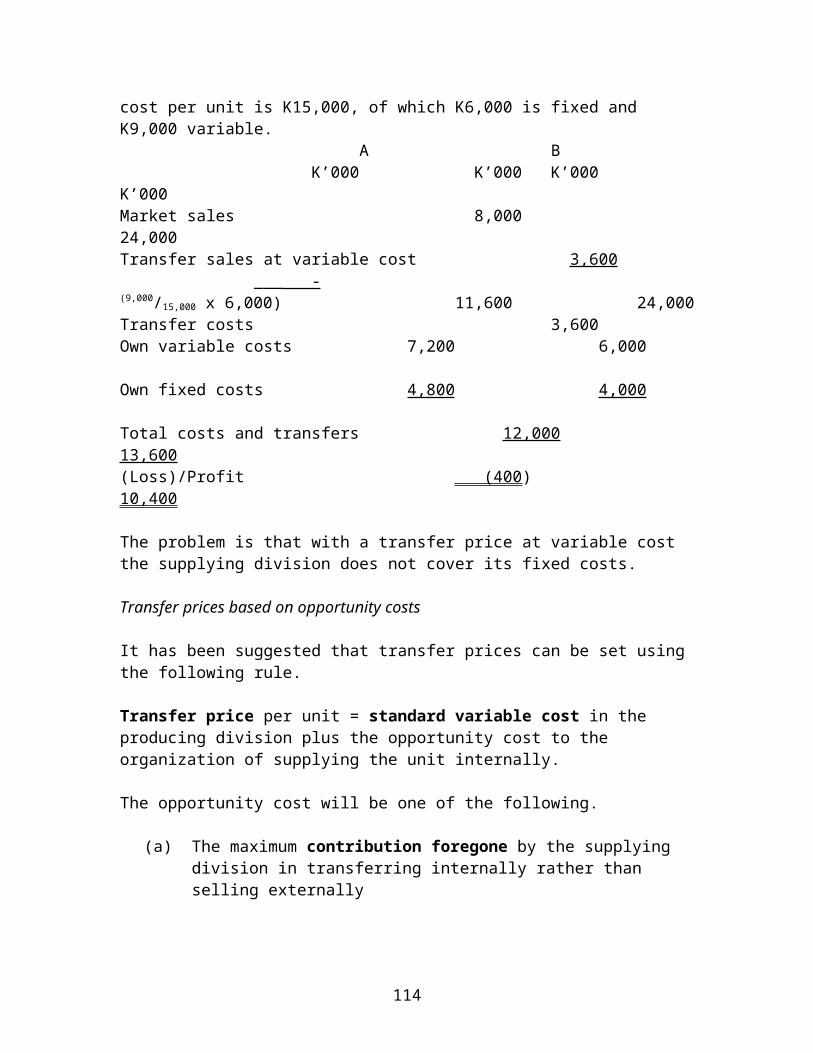

(a) Buying a single machine: K’000 K’000

Year 0 cost 36,000 (36,000)

Reliable:

Year 1-4 (K16, 000,000 x 3.312) 52,992

Year 4 (K1, 200,000 x 0.735) 882

46

33,874 x 0.7 37,712 1,712

Unreliable

Year 1 (K10, 000,000 x 0.926) 9,260

K800, 000 x 0.926 74110,001 x 0.3 3,000

4,712Renting machine over corporate time period:

0.7 Probability of machine kept for 4 years.

= (K15, 200,000 - K11,200,000) = K4,000,000

K 4,000,000 x 0.7 x 3.312 = K9,273,600

0.3 Probability of a machine kept for 1 year:

4,000,000 x 0.3 x 0.926 = K1,111,200 Corporate figure for renting 10,384,800

Therefore the rented machine is definitely the better option:

K10,384,800 – K4,712,000= K5,672,800

1. Assume a faulty photocopier.

Year 1 replacement over year 2:

Year Cashflow Discount rate Present value (K’000) (K’000)

1 21,600 (36,000) 0.926 (13,334) (cash received a

new purchase price)

2 4,200 *1 0.857 3,600 (net benefit of new machine over 2 yrs option)

(18,000) 36,000 0.857 15,426 (saving by net replacing in

year 2)

5 1,080 * 2 0.681 735 (sale of machine)

6 (1,080) (sale income forgone)

47

(14,200) (Loss of additional years income)

2,000 0.630 (7,106)(income from renting included for companion)

* 1 0.7 x K16,000,000 = K11,200,0000.3 x K10,000,000 = K 3,000,000

K14,200,000 – K10,000,000 = K4,200,000

*2 0.7 x K1,200,000 = K840,0000.3 x K800,000 = K240,000

K1,080,000

Therefore replacement at the end of year 2 is better.

Renting over a 6 (six) year cycle:

Yr 1-6 : 35 machines x K4,000,000 x 4.623 = K647,220,000

Replacing in year 2 – assuming a full 6 year cycle for comparison

(in years 5 & 6, some machines will have to be rented, that is 35 machines x 0.7 = 24.5)

Therefore, renting still remains the better option by a small margin.

2. The amount of taxation paid will be affected by the profit earned, business expenses and the purchase of assets.

3. Machine rented

Taxation will be levied on the profit earned but the expense of renting a machine can be set against this, so the taxation calculation for renting a machine becomes (K15,200,000 – K11,200,000) x 30% = K1,200,000 per year. Half of the tax will be paid in the year in which the profit is earned and half the following year. (This will reduce the net present value over 4 years by K1,200,000 x 3.312 = K3,974,400 approximately, ignoring the time factor (lag).

4. Machine purchased

If the machine is purchased tax will still be paid on the profit earned but there will be no rented expense to set against this (increase in tax K11,200,000 x 0.3 = K3,360,000 each year for a reliable machine).

However, instead of depreciation being charged each year a capital allowance may be set against profit. The government sets the capital allowance rates. The capital allowance rate in the scenario is 25% on a reducing balance basis and the table below shows how this would be applied to a reliable machine and the final net present value of the capital allowances.

Lease rental calculations are very similar to a discounted cash flow exercise as you could have seen it early in this chapter. Rental calculation assumptions for an example, which we will work, though are summarized below. In the illustration below the tax effect the extreme case of 100% in the first year allowance and 50% tax rate is used.

Cost-Benefit Analysis

In many situations where senior managers of a business make decisions, the decisions made can either be structured or unstructured.

Structured and Unstructured Decisions

In structured decisions managers use standard procedures in an outlined manner to deal with situations in a prescribed way.

In unstructured decision-making, managers use the least pool of experience and intellect to make sound judgments, which are in the best interest of the company or organizations.

Goal Congruence and Decision Making

All decisions which are made should be consistent with the corporate objectives. We should realize at this point that business managers are leading corporations which have been established with a view to making profits.

Therefore, all decisions which the business managers make should be seen to be adding more value to the business ultimately in excess of the costs involved, than the costs involved in carrying them out.

Therefore, in whatever context we look at business decision making, business managers are going to consider the benefits against the cost of pursuing a given strategy before they embark on implementing that particular decision.

Nature of Cost- Benefit Analysis

As we have mentioned above, before a corporate strategy is implemented in a business, the managers will have need to carry out a rigorous cost benefit analysis.

Therefore, a cost-benefit analysis will involve a comprehensive comparison of the net benefits expected to accrue to an organization by pursuing a chosen strategy against the costs which are to be incurred in pursuit of the strategy.

Please note that the benefits and costs can be either quantitative and / or qualitative at the same time.

50

However, as we mentioned earlier where, the qualitative costs and benefits might be more difficult to establish due to the grey nature of the qualitative consequences of our actions. Cost- Benefit Analysis Techniques

There are a lot of techniques used to undertake cost benefit analyses.Some of the methods include the following:

Profitability/ Net Cash-Flow

Typically and usually when carrying out a cost benefit analysis, most business list the financial and quantitative revenues which the business is likely to earn against the total costs likely to be incurred in the pursuing the strategy. Scoring and Ranking

Another commonly used technique for carrying out a cost-benefits analysis is by the use of scoring and ranking of several capital investments available to the business.

Ranking and scoring is used both in situations where we are evaluating a single strategy or where we are evaluating multiple strategies so that we can eventually choose the best option out of them all.

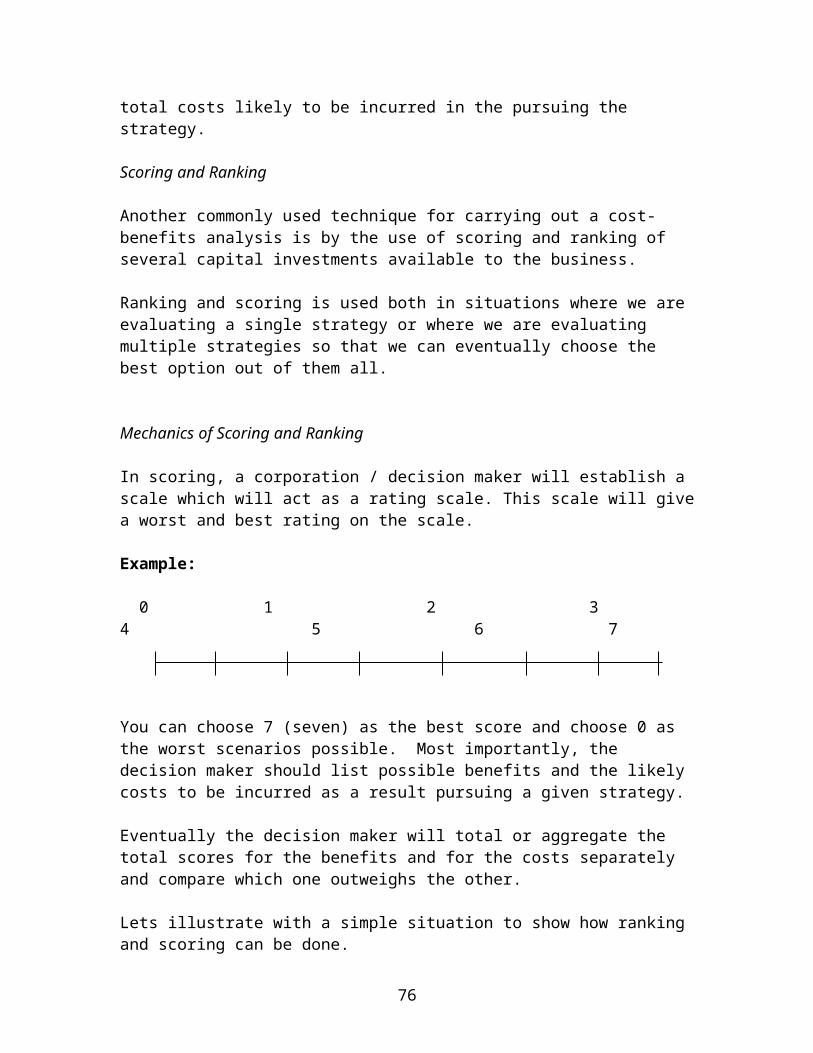

Mechanics of Scoring and Ranking

In scoring, a corporation / decision maker will establish a scale which will act as a rating scale. This scale will give a worst and best rating on the scale.

Example:

0 1 2 3 4 5 6 7

You can choose 7 (seven) as the best score and choose 0 as the worst scenarios possible. Most importantly, the decision maker should list possible benefits and the likely costs to be incurred as a result pursuing a given strategy.

Eventually the decision maker will total or aggregate the total scores for the benefits and for the costs separately and compare which one outweighs the other.

Lets illustrate with a simple situation to show how ranking and scoring can be done.

51

Assume that Chinsa Ltd has been experiencing low sales of its product, the Manex. As a result the entire management is concerned deeply and they have the following views: The Marketing Director has suggested that the company should invest heavily in the marketing activities. However, the Finance Director is a bit sceptical concerning the likely benefits of this hefty expenditure on the marketing campaign.

As a result, the CEO has requested you in your capacity as management accountant to carry out a comprehensive cost-benefit analysis. Suggested illustration

STEP 1

Set and establish a rating scale or the purpose of this illustration assuming that 1 represents the worst situation and 5 represents the best scenario.

RATING SCALE

1 2 3 4 Worst Best

STEP 2

List the likely benefits and costs of staging (mounting) up a massive marketing campaign. The likely benefits and costs would be the following: These are not exhaustive

Benefits Costs

- Good corporate image - Huge financial outlay

- Bigger client base - Expected continued advertising

- Increase profits

STEP 3

Assign weightings or ratings from the scale to each benefit and each cost

Benefits Rating

1. Good corporate image 3

2. Bigger client base 4

3. Increase profits 2

52

Total scores for benefits costs: 9

(i) Huge financial outlay 4

(ii) Expected continued advertising 4

Total scores for the costs: 8

STEP 4

Compare the total scores for benefits and the one for costs.

Benefits 9

Costs 8

Difference 1

As can be seen above, the analysis and comparison show that the benefits of staging a massive campaign will gives Chinsa Ltd more of benefits than costs.

So purely following the scoring and ranking we expect Chinsa Ltd to benefit greatly from the marketing campaign, and so the decision to invest in it should be upheld.

This is only a simplistic approach. However, in practice so many factors are likely to be taken into consideration and the management accountant will need to carryout the analysis with a great amount of help from marketing professionals and other business personal who may make work as researchers and general R&D employees with Chinsa Ltd.

It should be noted that in the above exercise, the scores represent both the qualitative and quantitative benefits, which are associated to the various benefits and costs identified by the management accountant and his team.

Post Project Completion Audit

From the onset of the chapter we have only been looking at evaluation of projects, which is only a part of the investment process.

To conclude the chapter, lets look at an equally important aspect of project evaluation and management. This is the aspect of Post-completion Audit.

The post completion audit of projects provide the mechanism whereby experience of past projects can be fed into the firm’s decision-making process as an aid to the improvement of further projects.

53

Benefits of Post –Completion Auditing

There are a number of benefits that stand out so clearly from a project post – completion audit.

The benefits can be classified in two main categories.

Type 1

Those benefits that relate to the performance to the current project i.e. the project under review.

Mechanics of Post – Completion Audit

A post – audit small team, typically professionals such as an engineer who had some involvement in the project, usually carries out completion audit.

The post – completion audit reviews all aspects of a completed project, to assess whether it lived up to initial expectations in term of revenues and costs and analyse the causes of deviations from planned results.

Its main purpose is to enable the experiences, good or bad gained during the life of one project to be made available for the benefit of future projects. The audit is thus essentially a forward-looking one as it seeks to establish lessons from the past for the future benefit of the corporation.

Type 2

The second and final category of benefits relates to the additional information concerning the choice and performance of future projects and the main benefits are given below.

It improves the quality of decision making by providing a mechanism whereby past experience can be made readily available to decision makers.

It encourages greater realism in project appraisal by providing a mechanism where past inaccuracies in forecasts are made public.

It highlights reasons for successful projects, which may be important in achieving greater benefits from future projects.

54

Chapter 2

PRICING THEORY

Learning Outcomes:

At the end of this chapter candidate Should identify and discuss market situations which influence the pricing

policy adopted by an organization Should explain and discuss the variations that influence demand of a

product or service Should be able to calculate prices using full cost and marginal cost as the

pricing base Should be able to compare the use of full costing pricing and marginal

cost pricing as planning and decision making aids Should be able to appreciate the concept of transfer pricing and its

mechanics.

55

Definition of price

Organizations operating as businesses always produce or provide tangible products or intangible services for sales to customers in order for them to pursue their primary corporate objective of enhancing shareholders wealth.

The products and services are sold at a price.

Therefore price refers to the monetary amount which corporations sale their chosen units of products/services.

Influences on Price

There are so many variations that dictate the price at which given commodities or services can be sold at.

The following are the main factors that influence price of services or products.

(a) Quality

This is an aspect of price perception. In the absence of other information, customers tend to judge quality by price. Thus a price rise may indicate improvements in quality, a price reduction may signal reduced quality.(b) Existence of intermediaries

If an organization distributes products or services to the market through independent intermediaries, such intermediaries are likely to deal with a range of suppliers and their aims concern their own profits rather than those of suppliers.

(c) Competitor Activities

In the same industries, pricing moves in unison. In others, price changes by one supplier may initiate a price war. Competition is discussed in more detail below.

(d) Inflation

In periods of inflation the organization may need to change prices to reflect increases in the prices of supplies, labour, rent and so on.

Traditional Pricing Bases

The two main traditional methods of pricing one

(i) full-cost pricing

56

(ii) marginal cost pricing

Cost plus Pricing

With full cost pricing, the sales price is determined by calculating the full cost of the product and then adding a percentage mark-up for profit, so this ensures that all costs are covered.

The full cost pricing is useful if prices have to be justified to customers.

On the other side, the full cost pricing method takes no account of the market or demand conditions.

It may also require arbitrary decisions about absorption of costs.The cost accountants may also have problems in determining the accurate profit mark-ups.

Marginal Pricing

With marginal cost pricing, a profit margin is added on to either the marginal cost of production or the marginal cost of sales.

This is sometimes called ‘mark-up’ pricing.

It draws management attention to contribution, and the effects of higher or lower sales volumes on profit.

In this way, it helps to create a better awareness of the concepts and implications of marginal costing and cost-volume profit analysis.

The marginal cost pricing is convenient if there is a readily identifiable variable cost e.g. in retail businesses.

However, again it takes no account of market or demand conditions.

In practice as you already know, pricing decisions cannot ignore fixed costs in the long term.

Example

Muti Ltd has begun to produce a new product, product X, for which the following cost estimates have been.

KDirect materials 27,000

Direct labour: 4 hours at K5,000 per hour 20,000

57

Variable production overheadsMachining, ½ hour at K6,000 per hour 3,000

50,000

Production fixed overheads are budgeted at K300,000 per month and because of the shortage of available machining capacity, the company will be restricted to 10,000 hours of machine time per month. The absorption rate will be a direct labour rate, however, and budgeted direct labour hours are 25,000 per month. It is estimated that the company could obtain a minimum contribution of K10,000 per machine hour on producing items other than product X.

The Direct Cost estimates are not certain as to material usage rates and direct labour productivity, and it is recognized that the estimates of direct materials and direct labour costs may be subject to an error of + 15%.

Machine time estimates are similarly subject to an error of + 10%.

The company wishes to make a profit of 20% of full production cost from product X. What should the full cost based price be?

The following solutions have been developed based on four (4) assumptions.

(a) Exclude machine time opportunity costs:

Ignore possible costing errors K

Direct materials 27,000

Direct labour (4 hours) 20,000

Variable production overheads 3,000

Fixed productionOverhead (K300,000,000 = K12,000 per

25,000 48,000direct labour hour

Full production cost 98,000

Profit mark-up (20%) 19,600

Selling price per unit of product X 117,600

(b) Include machine time opportunity costs:

58

Ignore possible costing errors. K

Full production cost is in (a) 98,000

Opportunity cost of machine time(Contribution forgone (½hr x K10,000) 5,000

Adjusted full cost 103,000

Profit mark-up (20%) 20,600

123,600

(c) Exclude machine time opportunity costs but make full allowance for possible under-estimates of costs.

K KDirect materials 27,000Direct labour 20,000

47,000

Possible error (15%) 7,050 54,050

Variable production Overheads 3,000

3,000Fixed productionOverheads (4 hrs x K12,000) 48,000

Possible error (labour time) (15%) 72,000 55,200

Potential full production cost 112,550

Profit mark-up (20%) 22,510

135,060

(d) Include machine time opportunity costs and make a full allowance for possible under-estimates of cost.

KPotential full production cost as in (c) 112,550

59

Opportunity cost of machine time(Potential contribution forgone)(½hr x K10,000 x 110%) 5,500

Profit mark-up (20%) 23,610

Selling price per unit of product X 141,660

Full Cost Versus Marginal Cost Pricing

The most important and common criticism of full cost pricing is that it fails to recognize that since sale demand may be determined by sales price, there will be a profit – maximization combination of price and demand.

A full cost based approach to pricing will be most unlikely, except by coincidence or luck to arrive at the profit-maximising price. In contrast a marginal costing approach to looking at costs and prices would be more likely to help with identifying a profit–maximising price.

Example

Luangwa Ltd has budgeted to make 50,000 units of its product, the Luan.

The variable cost of a Luan is K5,000 and annual fixed costs are expected to be K150,000,000.

The Finance Director of Luangwa Ltd suggested that a profit margin of 25% on full cost should be charged for every product sold.

The Marketing Director has challenged the wisdom of this suggestion, and has produced the following estimates of sales demand for the Luan.

Price per unit Demand K Units 9,000 42,00010,000 38,00011,000 35,00012,000 32,00013,000 27,000

Required

(a) Calculate the profit for the year if a full cost price is charged.

(b) Calculate the profit-maximising price.

60

Assume in both (a) and (b) that 50,000 units of the Luan are produced regardless of sales volume.

Solution

(a) (i) The full cost per unit is K5,000 variable cost plus K150,000,000 = K3,000\unit 50,000 units

hence i.e. K8,000 (K5,000 + K3,000) in total.

A 25% mark-up on this cost gives a selling price of K10,000 per unit so that sales demand would be 38,000 units. (production is given as 50,000 units).

(ii) Profit (absorption costing)

K 000 K000

Sales 380,000

Costs of production (50,000 units)

Variable (50,000 x K5,000) 250,000

Fixed (50,000 x K3,000) 150,000

400,000

Less increase in stocks(12,000 units x 8) (96,000)

Cost of sales 304,000

Profit 76,000

(i) Profit using marginal costing instead of absorption costing so that fixed overhead costs are written off in the period they occur, it would be as follows (the 38,000 unit demand level is chosen for comparison purposes).

KContribution (38,000 x K(10,000 – 5,000) 190,000 Fixed costs 150,000

Profit 40,000

61

Since the company go on indefinitely producing an output volume in excess of sales volume, this profit figure is more indicate of the profitability of the Luan in the longer term.

(b) A profit-maximising price is one which gives the greatest net (relevant) cash flow, which in this case is the contribution-maximising price.

Price Unit Contribution Demand Amount K K units K 9,000 4,000 42,000 168,00010,000 5,000 38,000 190,00011,000 6,000 35,000 210,00012,000 7,000 32,000 224,00013,000 8,000 27,000 216,000

The profit maximizing price is K12,000 with annual sales demand of 32,000 units.

This example shows that a cost based price is unlikely to be the profit – maximizing price, and that a marginal costing approach, calculating the total contribution at a variety of different selling prices, will be more helpful for establishing what the profit – maximizing price ought to be.

Activity Based Pricing (ABP)

Activity based costing provides an opportunity for organizations that use cost-based pricing to gain a greater understanding of their costs and so correct pricing anomalies that derive from the distorted view given by conventional volume-related costing.

Under the ABC approach, overheads are allocated to products on the basis of the activities that caused them to be incurred, rather than according to some arbitrary base like labour hours. The implication for pricing is that the full cost on which prices are based may be radically different if ABC is used.

Example

ABP Ltd makes two products, X and Y with the following cost patterns.

Product Product X Y K K

Direct materials 27,000 24,000

Direct labour at K5,000/hr 20,000 25,000

62

Variable productionOverheads at K6,000 Per hour 3,000 6,000

50,000 55,000

Production fixed overheads total K300,000,000 per month and these are absorbed on the basis of direct labour hours. Budgeted direct labour hours are 25,000 hours per month. However, the company has carried out an analysis of its production support activities and found that its fixed costs actually vary in accordance with non volume-related factors.

Product Product Total CostActivity Cost driver X Y K 000Set-ups Production runs 30 20 40,000

Material Production runs 30 20 150,000

Inspection Inspections 880 3,520 110,000300,000

Budgeted production is 1,250 units of product X and 4000 units of product Y.

Required:

Given that the company wished to make a profit of 20% on full production cost, calculate the prices that should be charged for products X and Y using the following.

(a) Full cost pricing(b) Activity based cost pricing

Solution

(a) The full cost and mark-up will be calculated as follows:

Product Product X Y

K K

Variable costs 50,000 55,000

Fixed productionOverheads

63

*K300,000,000\25,000 = 12,000\hr) 48,000 60,000

98,000 115,000

Profit mark-up (20%) 19,600 23,000

Selling price 117,600 138,000

(b) Using activity based costing, overheads will be allocated on the basis of cost drivers.

The results in (b) are radically different from those in (a). On this basis it appears that the company has previously been making a huge loss on every unit of product X sold for K117,600. If the market will not accept a price increase, it may be worth considering leasing production of product X entirely. It also appears that there is scope for a

64

reduction in the price of product Y and this would certainly be worthwhile if demand for the product is elastic.

Target Pricing