If possible you could provide some statistics and examples pointing out differences/ similarities from one country to the other?

34 years in the sector of guarantee President and CEO of a Spanish SGR (1981-1996) President of CESGAR (1991-96) and Founding President AECM (1992-96) Technical Secretary REGAR - 19 consecutive annual forums Lecturer and researcher, Award UNICAJA of economic research from 2007.

Panelist and speaker lectures about 33 countries. PhD in Economics and Business Sciences. Associate Professor at University

of Cordoba (Spain). International guarantee systems (CGSs) consultant since 1996 with projects

developed in Latin America for national and multilateral institutions and international cooperation (AECID; GTZ; COSUDE, FUNDES, PNUD, IDB, AFD, WB, UE, etc.)

XIX Iberoamerican Forum guarantee systems, 17-19 of September 2014, Valladolid – Madrid (Spain)

8 moderators, 40 panelists, 500 participants from 22 countries, of which 135 international together with national 365, representatives of public and private guarantee systems, and other authorities of Latin America. This year, in addition to four panels, we have developed four working groups that has involved the intervention of 4 moderators and a few 25 panelists in different geographical areas.

● WORLD BANK In 2015 created the Task Force on "Desing, implementation and evaluation of credit guarantee schemes CGSs for small and medium enterprises" and document "Principles for credit guarantee schemes CGS s for SMEs“ http://www.slideshare.net/AecmEurope/principles-consultative-document-june-2015

● OECD An OECD report in 2012 highlights that nearly every country should launch loan guarantee programs. http://www.aecm.be/es/oecd-publishes-scoreboard-of-sme-finance-smes-harder-hit-by-credit-crunch-than-larger-companies.html?IDC=119&IDD=1211&NEWSLETTERID=1214

● IMF An IMF report in 2010 highlights the importance of guarantees to improve the access to finance for SMEs http://www.imf.org/external/pubs/ft/weo/2010/update/01/index.htm

● An study in 2010 about the macroeconomic benefits of the activity of the German Guarantee Banks, VDB The activity of the German Guarantee Banks has lead to an improvement of GDP growth and of the State's financing, in addition to the improvement of the access to finance for SMEs http://www.aecm.be/es/inmit-study-on-the-macroeconomic-benefits-of-the-german-guarantee-banks.html?IDC=31&IDD=183

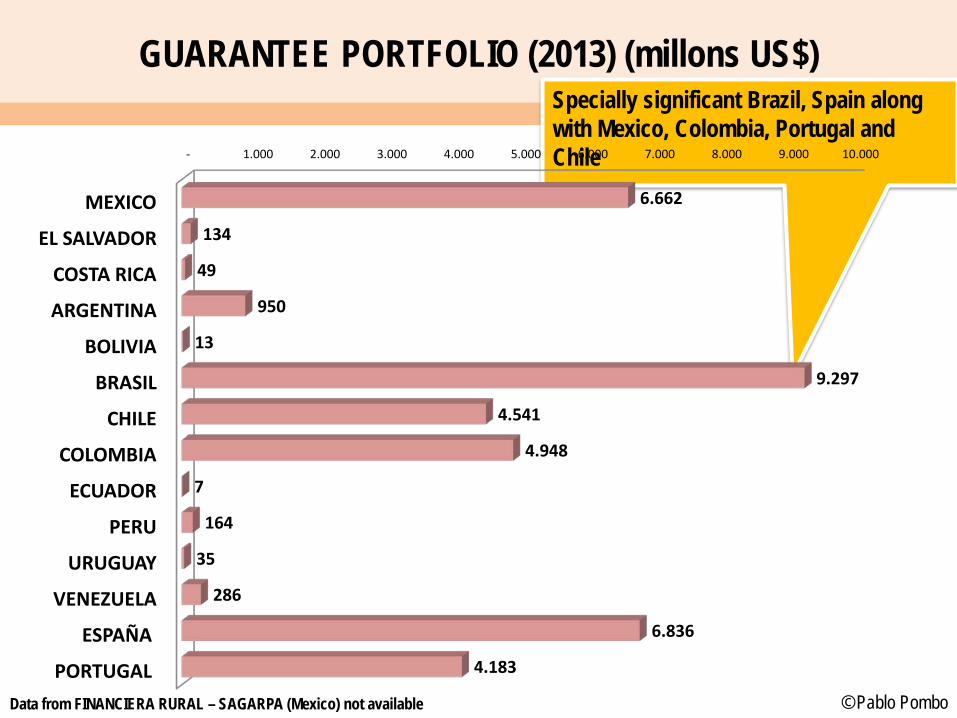

• Classification and characterization • Relations with financial institutions and SME • 2013 statistics: situation, trends, perspectives and challenges

The requirements of equity and provisions (technical reserves) are established according to international rules

The financial system optimizes its management about the quality of its assets coverage

Bank for International Settlements (BIS) Basel I, II y III

The guarantee is a strategic value for financial institutions: their balance, accounts of results and requirements of coverage of the equity and provisions

For guarante coverage of less quality higher requirements of equity and provisions if it is of higher quality

The Classification of risks according to the classification and weighting of guarantee coverage

Source: Own elaboration

DIAGNOSIS OF THE PROBLEM: International rules may represent bigger difficulties and unwanted effects

State Policy: promoting access to finance for employer (the GS can not be questioned, so that it can develop and remain strong and stable – it is not a fad- to be fully integrated into the financial system)

"Strategic Alliance" and full consensus among the actors involved (public authorities, financial institutions and micro and SMEs and their organizations) in the legislative and operational development of the GS that satisfies the legitimate interests of all parties.

SOLUTION: Guarantee systems (CGSs)

Transfer of credit risk from the bank to guarantee systems (CGSs)

Strategies and general principles of implementation of a CGS

GUARANTEE SYSTEMS (CGSs) AS A SOLUTION: strategies and general principles of implementation of a guarantee scheme CGS

The fully integration of the guarantee system (CGS) in the financial system means a major approach shift: it is about taking the employer to the credit, under the best conditions from the guarantee coverage by the guarantee system (CGS).

By the mortgage Law citizens generally can access, with that coverage, to the financing of a home or other real state .. Through the guarantee system (CGS) the employer can access

THE GUARANTEE OPERATOR SUPPORTS THE GUARANTEE COVERAGE ON ITS EQUITY /

BALANCE

THE GUARANTEE OPERATOR DOES NOT SUPPORTS THE

GUARANTEE COVERAGE ON ITS EQUITY / BALANCE

SCHEMESON MERCANTILE

COMPANIES

SCHEMES ON PUBLIC INSTITUTIONS

ADMINISTRATORS OFGUARANTEE FUND

ADMINISTRATORS OFGUARANTEE TRUSTS

Source: Own elaboration

75%

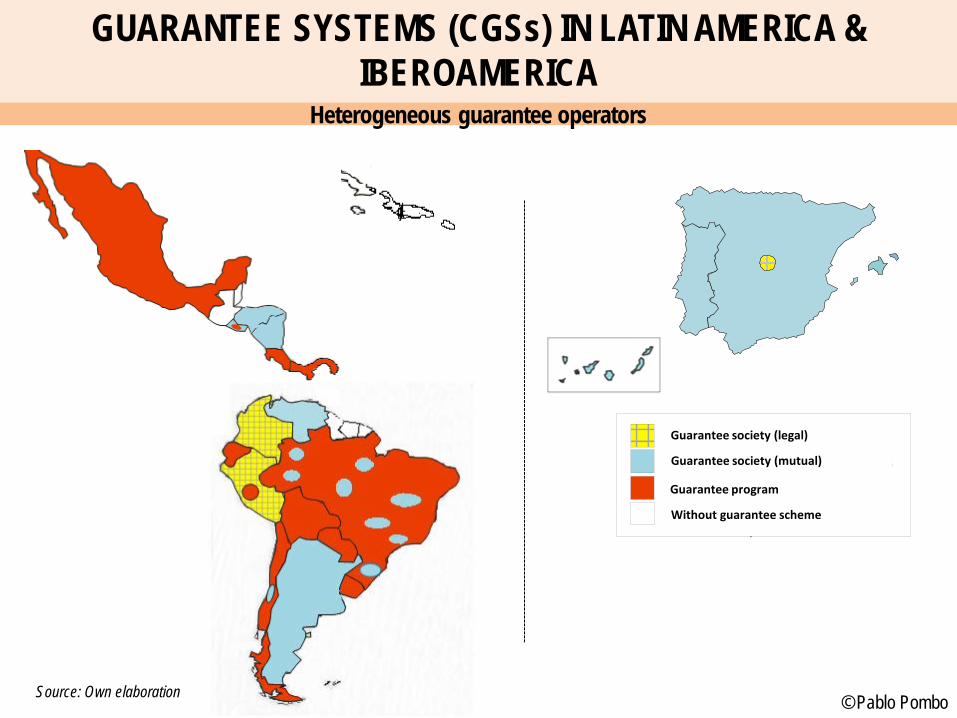

Empirical classification of the guarantee systems / schemes in Latin-American - 2013 IDB NT - 503 study

Heterogeneous operators guarantee

Operator of the guarantee is the entity that develops and executes the activity for the granting and formalization ofguarantee coverage, real and effective, according to rules of operation.

• To decide or choose on that model of guarantee system (CGS) to apply, we need to know that types or models of guarantee system (CGS) exist.

• Than usual in the studies and analyses carried out is to address operational issues but not the strategic passing, before anything, knowing that there are models to confront and solve the problem of access to funding for SMEs through guarantee schemes (CGSs).

• Therefore the focus of work passes through delimit two issues that should be clear to be well located

1. One corresponds to the conceptual classification and characterization of (what has been done on European and Latin American samples) guarantee systems (CGSs), and other

2. On the implementation of the guarantee systems (CGS) <implemented in Latin America, in several countries in three phases>

CLASSIFICATION AND CHARACTERIZATION OF THE GUARANTEE SYSTEMS (CGSs)

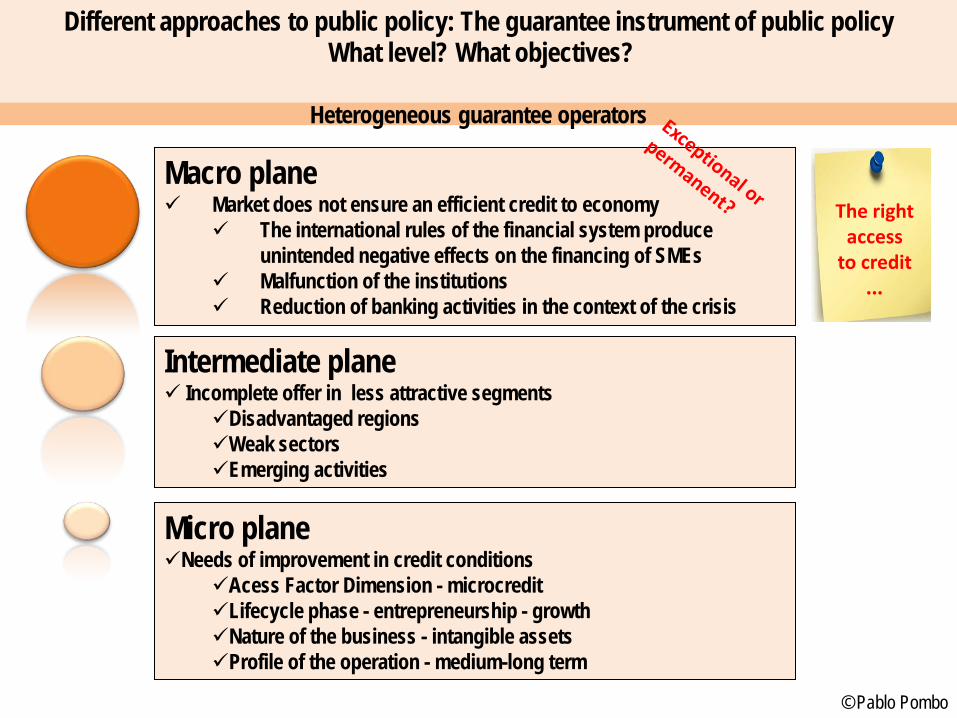

Micro plane Needs of improvement in credit conditions

Acess Factor Dimension - microcredit Lifecycle phase - entrepreneurship - growth Nature of the business - intangible assets Profile of the operation - medium-long term

Macro plane Market does not ensure an efficient credit to economy

The international rules of the financial system produce unintended negative effects on the financing of SMEs

Malfunction of the institutions Reduction of banking activities in the context of the crisis

Intermediate plane Incomplete offer in less attractive segments

Disadvantaged regions Weak sectors Emerging activities

Different approaches to public policy: The guarantee instrument of public policy What level? What objectives?

How to do it? Programa de garantía – Agencias Públicas – Aval del Estado – Fondo/Fideicomiso de garantía Socieada de Garantia – Sociedad de Garantía Recíproca/Mútua – Sociedad/Fondo de Reafianzamiento

Guarantee operator is the entity that develops and executes the activity for the granting and formalization of guarantee coverage, real and effective, according to rules of operation.

Guarantee Programs (managed by public institutions specialized in financing / promotion or development of SMEs)

Guarantee Programs (managed by public agencies or institutions delegated by it)

Companies with business participation

Source: Own elaboration

Guarantee societies are societies, which can have different legal personalities, that have own resources of its shareholders, public or private, and operate under the corporate commercial or banking rules/law,, and / or legislation of the activity itself ... Even though were called "Guarantee Fund"

Empirical classification of the guarantee systems / schemes (CGSs) in Europe (UNICAJA economic research award 2007)

THE GUARANTEE OPERATOR SUPPORTS THE GUARANTEE COVERAGE ON ITS EQUITY /

BALANCE

THE GUARANTEE OPERATOR DOES NOT SUPPORTS THE

GUARANTEE COVERAGE ON ITS EQUITY / BALANCE

SCHEMES

ON MERCANTILE COMPANIES

SCHEMES ON

PUBLIC INSTITUTIONS

ADMINISTRATORS OF

GUARANTEE FUND

ADMINISTRATORS OF GUARANTEE TRUSTS

Source: Own elaboration

75%

Empirical classification of the guarantee systems / schemes in Latin-American - 2013 IDB NT - 503 study

Operator of the guarantee is the entity that develops and executes the activity for the granting and formalization of guarantee coverage, real and effective, according to rules of operation.

The resource is usually in a Autonomous public liquid resource (Fund or Trust of Guarantee)

Autonomous public liquid assets (Fund of Guarantee)

A institution manages the resource: Public Bank, Development Agency, public body, trust, etc..

Financing / Credit

Grants Guarantee

COMPANY - SME

Public Budget

Request of credit

Request of Guarantee

Source: Own elaboration

BASIC OUTLINE OF THE PERFORMANCE OF A GUARANTEE PROGRAM

BANK

The guarantee is operated by an "institutional" that manages a public autonomous liquid resource and does not supports the guarantee coverage in his patrimony / balance

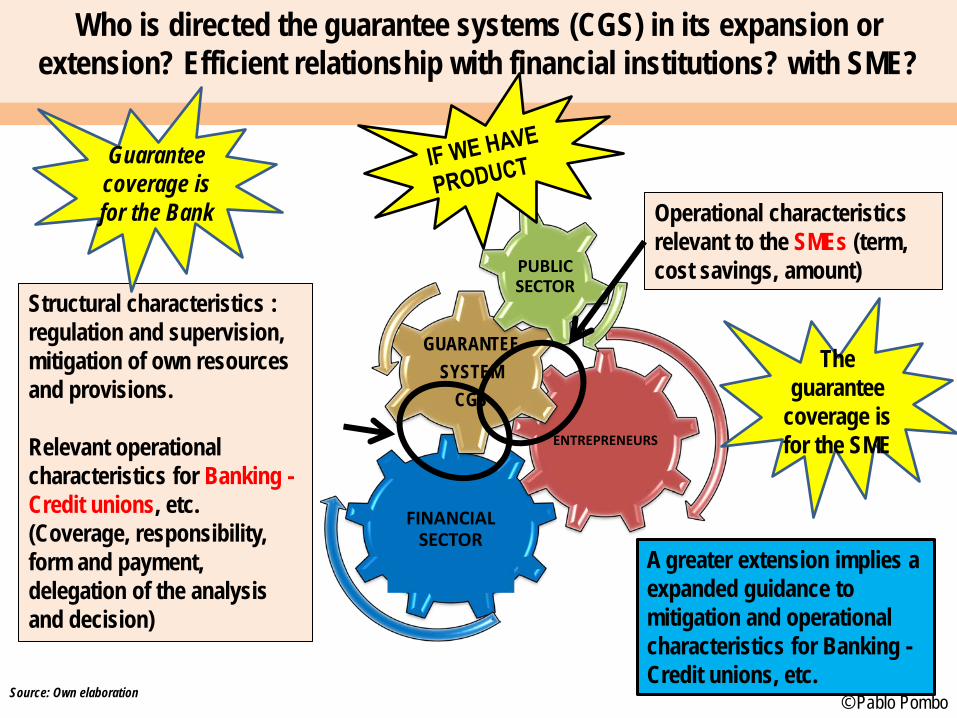

Operational characteristics relevant to the SMEs (term, cost savings, amount)

Who is directed the guarantee systems (CGS) in its expansion or extension? Efficient relationship with financial institutions? with SME?

Structural characteristics : regulation and supervision, mitigation of own resources and provisions. Relevant operational characteristics for Banking - Credit unions, etc. (Coverage, responsibility, form and payment, delegation of the analysis and decision)

A greater extension implies a expanded guidance to mitigation and operational characteristics for Banking - Credit unions, etc.

A REGULATORY FRAMEWORK... GOOD PROFILING... WELL DIRECTED... TO GET PRODUCT … Change of approach: for the Bank... IF... coop. CTO. …

1. Structural characteristics for the IF: legal certainty, regulation and supervision, mitigation equity and provisions.

2. Relevant operational characteristics for the IF (coverage, liability, payment, delegation analysis and decision) - Coverage: 100% ? - Operational guarantee:

•Solidary or subsidiary? •Automatic or semi-automatic? •Analysis - decision would delegate? •Do pay failed or non-payment? •Do I pay first requirement or conditioned?

? Do we have product?

The guarantee coverage is for the bank … IF … coop. cto. …

Recognition of financial activity: financial activity (subsystem of the financial

system) Regulation and financial supervision as integration in the financial system:

regulation and supervision by the Superintendence of the financial system (SBEF) Regime of authorizations to operate, manage, etc.: Resources: capitalization (in SGR society of variable capital and FPT) to develop

and comply with the restrictions on growth and creation FDSGR Government structure: organs, representing and votes Other legal and/or corporate issues Structuring of a counter-guarantee (reavaladora) system: key factor in mixed

systems of the guarante systems

A REGULATORY FRAMEWORK... GOOD PROFILING ... WELL DIRECTED ... TO GET PRODUCT … PROFILE OF THE REGULATORY FRAMEWORK OF THE GUARANTEE SYSTEM (CGS) …

- Guarantee: product regulated vs unregulated product - Product accepted by the stakeholder: banking (IF) and SMEs

Future important growths and developments. - Major expansion and high % of growth - Impact assessment

.

Continuity of the important role of the State in the implementation and development, coexisting with private participation that is increasingly expanding and relevant.

Guarantee program with an important boost to MGS’s. It involves methods of capitalization and specific operational profiles.

Implementation of regulatory frameworks and quality and efficient supervision.

Integration of the financial system. Scoring and weighting of guarantees and national counter-guarantees in the mitigation of own resources and provisions for IFI’S and MGS’s.

Consolidation of initiatives by multilateral organizations of supranational counter-guarantee

• Extension of experiences such as FLAG CAF, CII, FG MERCOSUR. • And national: FOGAPE , GF Brasil, FOGAPYME, FONPYME, etc.

framework in the SG, as well as recognition of the coverage of the SG

• Establish regulatory frameworks of quality (legal certainty and permanence) and efficient supervision (control)

• Achieve frameworks of stable long-term partnerships with the public, financial and corporate sectors.

• International Financial Crisis

Internal • Practice transparency to transmit a certain

knowledge of the legal and operational realities of the SG

• Encourage internal decisions towards the integration into the financial system of the SG

• Strengthen the role of MSMEs and others of the private sector in the SG

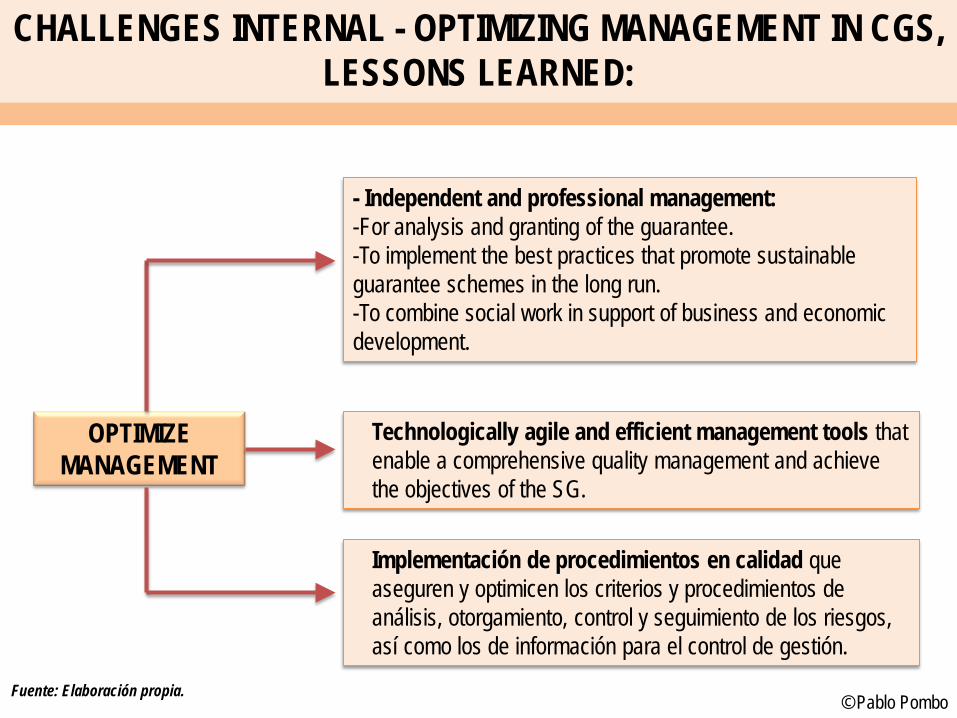

• Optimize management: learned lessons (independent and professional management; tools technologically agile and efficient , implementation of quality procedures)

- Independent and professional management: -For analysis and granting of the guarantee. -To implement the best practices that promote sustainable guarantee schemes in the long run. -To combine social work in support of business and economic development.

OPTIMIZE MANAGEMENT

Technologically agile and efficient management tools that enable a comprehensive quality management and achieve the objectives of the SG.

Implementación de procedimientos en calidad que aseguren y optimicen los criterios y procedimientos de análisis, otorgamiento, control y seguimiento de los riesgos, así como los de información para el control de gestión.

Fuente: Elaboración propia.

CHALLENGES INTERNAL - OPTIMIZING MANAGEMENT IN CGS, LESSONS LEARNED:

REGAR Red Iberoamericana de Garantías www.redegarantias.com

AECM Asociación Europea de Caución Mutua www.aecm.be

ACSIC Asian Credit Supplementation Institution Confederation www.acsic.org/acsic/index.jsp

ALIGA Asociación Latinoamericana de Instituciones de Garantía www.aligalat.org/index.html

"Guarantee systems for micro and SMEs in a globalized economy" www.redegarantias.com

"Guarantee systems in Latin America: experiences and recent developments" www.redegarantias.com y www.alide.org.pe

"Conceptual contributions and characteristics for classifying guarantee systems / schemes“ http://www.redegarantias.com/archivos/web/ficheros/2010/edicion_ii_premio_unicaja_investigacion_economica_english_version).pdf “A guarantee systems classification: the Latin American experience” http://www.iadb.org/es/publicaciones/publicaciones,4126.html?doctype=Technical%20Notes&docTypeID=TechnicalNotes&searchLang=&keyword=pombo&selectList=All&topicDetail=0&tagDetail=0&jelcodeDetail=0