117

AFM TAX TRAINING DAY Hosted by Deloitte 16 June 2015

AFM TAX TRAINING DAY Hosted by Deloitte

16 June 2015

!

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Association of Financial Mutuals Tax training day Operational taxes – ‘corporate’

Alistair Nichol

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Agenda

► Devolved taxes ► Financial transaction taxes ► Withholding taxes and double taxation agreements

AFM tax training day Page 3 16 June 2015

Devolved taxes

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Devolved taxes

► Devolution or evolution? ► Now: Scotland only

► Revenue Scotland ► Land and Buildings Transaction Tax

► Replacement for UK (E,W&NI!) SDLT ► Transactions from 1 April 2015 ► LBTT ‘progressive’ for both commercial and residential

► Landfill tax

AFM tax training day Page 5

http://www.gov.scot/Topics/Government/Finance/scottishapproach/devolvedtaxes * SDLT is a “slab” tax, ie SDLT on a 300,000 transaction would be charged at 3% on 300,000

Commercial property SDLT* LBTT

0 to 150,000 NRB NRB 150,001 to 250,000 1.00% 3.00% 250,001 to 350,000 3.00% 3.00% 350,001 to 500,000 3.00% 4.50% Over 500,000 4.00% 4.50%

16 June 2015

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Devolved taxes (cont.)

► Now: Scotland only (cont.) ► Scottish rate of income tax

► NOT strictly a devolved tax ► Applies from 1 April 2016 to income ► Allows Scotland to set final 10% (+/-) of each band ► Only one “Scottish rate” ► Define “Scottish” ► Collected by HMRC (not Revenue Scotland) ► Employees ► Annuitants

► Scotland Bill 2015 / 2016

16 June 2015 AFM tax training day Page 6

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/434834/Scottish_taxpayer_guidance_TechNote.pdf

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Devolved taxes (cont.)

► Future? ► Corporation Tax (Northern Ireland) Act 2015 – now law

► Commencement date to be set by regulations ► 12.5%?

► Wales ► Consultation issued (closed Dec 2014) ► Responses far from unanimous in support of devolution

16 June 2015 AFM tax training day Page 7

http://www.legislation.gov.uk/ukpga/2015/21/section/5/enacted http://gov.wales/docs/caecd/consultation/150210-devolved-responses-en.pdf

Financial transaction tax(es)

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Financial transaction tax

Page 9 AFM tax training day

► Supposed to be EU wide ► Then 11 countries ► Then DIY ► Spectre still haunting halls of EU power ► It might look like

► Phased intro: equities, derivatives, fixed interest ► Wide base, low rate ► Apply to each party to a transaction (ie compounds) ► Apply to entities established, or assets registered, in one of the 11 countries ► From 1 January 2016 (honest!)

► For now, take extra care to check for local transfer taxes (don’t rely on precedent)

http://ec.europa.eu/taxation_customs/taxation/other_taxes/financial_sector/index_en.htm http://www.steuer-gegen-armut.org/fileadmin/Dateien/Kampagnen-Seite/Unterstuetzung_Ausland/EU/2015/150127_Statement_FTT.pdf

Germany France Italy

Spain Austria Portugal

Belgium Estonia Greece

Slovakia Slovenia

‘The 11’

16 June 2015

Withholding taxes & double taxation agreements

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Withholding taxes

Page 11 AFM tax training day

► In theory applies to ► Dividends ► Interest ► Royalties

► (In)consistent with EU fundamental freedoms? ► Fokus / Denkavit ► Interaction with DTR (GLO)

► Often a genuine cost to businesses ► Administration

► Custodians ► WHT reclaims

16 June 2015

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Double Taxation Agreements

► UK has one of the widest DTA networks (>100) ► DTAs cover

► Taxation rights ► ‘Treaty rates’

► Portfolio dividends ► Interest ► Royalties ► Management / technical fees ► ‘Treaty rates’ range from 0% to 25%

► Fit for purpose?

AFM tax training day Page 12

https://www.gov.uk/government/collections/tax-treaties-signed-and-in-force http://www.hmrc.gov.uk/cnr/withholding-tax.pdf

16 June 2015

Summary & questions

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Summary

► Local and international influence ► Devolution versus harmonisation ► Constantly (d)evolving ► This time next year?

AFM tax training day Page 14 16 June 2015

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Questions

► ?

AFM tax training day Page 15 16 June 2015

About color themes Choose the appropriate design theme for your presentation. The first two options on the design tab are correct EY themes, these two are the only ones that should be used. (1) dark backgrounds for onscreen; (2) light backgrounds for handouts.

1

!

2

Thank you

EY | Assurance | Tax | Transactions | Advisory

Ernst & Young LLP

© Ernst & Young LLP. Published in the UK. All Rights Reserved.

The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

ey.com

16th June 2015

Operational taxes The Customer

19 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

LAPR

Chargeable events

Qualifying policies

LAPR

21 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Life Assurance Premium Relief

LAPR

12.5% relief

Pre - March 1984

Practical issues

Simplify the

system

Reduce admin

Few policies affected

Taxation of life policy investors

23 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Life policy Basics of taxation

Taxed at company and policyholder level

Taxed in life co @ 20% (through I-E system)

Premiums (no tax relief)

Tax on exit (it depends)

24 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

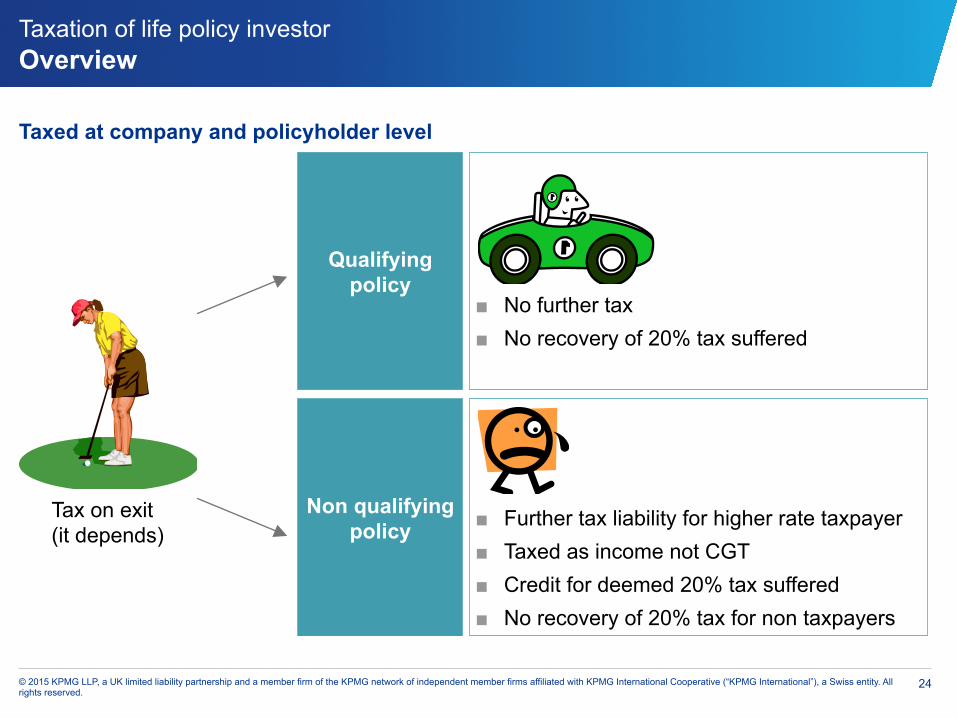

Taxation of life policy investor Overview

Taxed at company and policyholder level

Tax on exit (it depends)

Qualifying policy

Non qualifying policy

■ No further tax ■ No recovery of 20% tax suffered

■ Further tax liability for higher rate taxpayer ■ Taxed as income not CGT ■ Credit for deemed 20% tax suffered ■ No recovery of 20% tax for non taxpayers

25 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

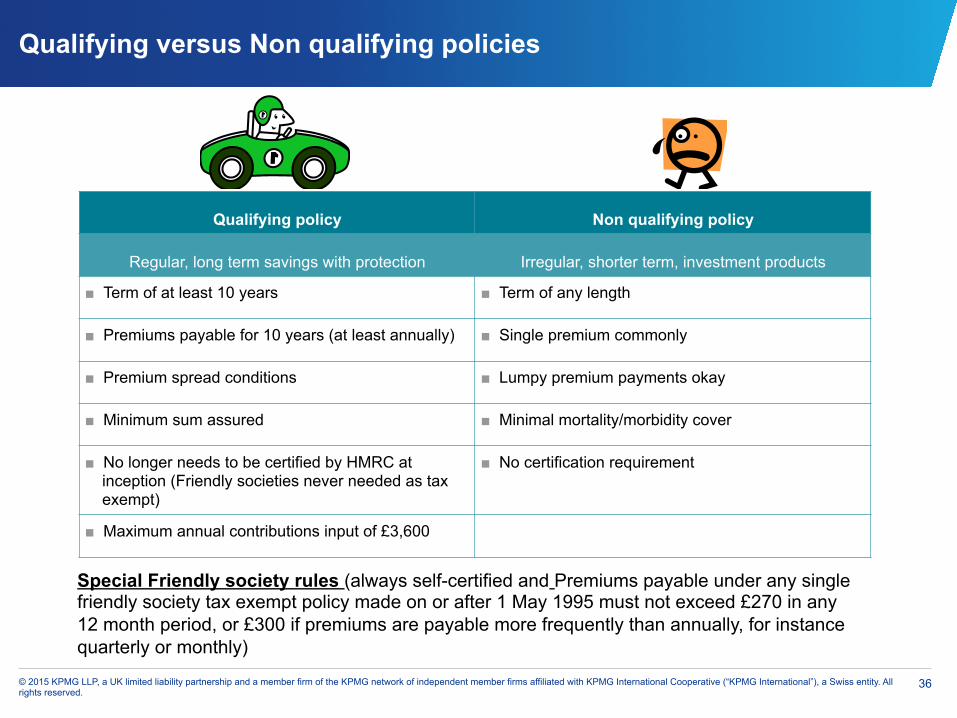

Qualifying versus Non qualifying policies

Qualifying policy Non qualifying policy

Regular, long term savings with protection Irregular, shorter term, investment products

■ Term of at least 10 years ■ Term of any length

■ Premiums payable for 10 years (at least annually) ■ Single premium commonly

■ Premium spread conditions ■ Lumpy premium payments okay

■ Minimum sum assured ■ Minimal mortality/morbidity cover

■ No longer needs to be certified by HMRC at inception (Friendly societies never needed as tax exempt)

■ No certification requirement

■ Maximum annual contributions input of £3,600

Special Friendly society rules (always self-certified and Premiums payable under any single friendly society tax exempt policy made on or after 1 May 1995 must not exceed £270 in any 12 month period, or £300 if premiums are payable more frequently than annually, for instance quarterly or monthly)

Chargeable events

27 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What is a chargeable event?

Chargeable Events

Terminal Events

Death

Maturity

Full surrender

Full assignment (for money or

money’s worth)

Calculation Events

Part surrenders

Excess events

Part assignments

28 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

When do chargeable events arise?

Qualifying policy Non qualifying policy

Maturity ■ Only if the policy has been made paid up within 10 years (or ¾ of term if less)

■ Yes

Death (of life assured)

■ Only if the policy has been made paid up within 10 years (or ¾ of term if less)

■ Yes

Surrender (full or part)

■ Only if

– occurs within first 10 years (or ¾ of term if less)

– or policy has been made paid up within 10 years (or ¾ of term if less)

■ Yes

Assignment (full or part) – for consideration

■ Only if

– occurs within first 10 years (or ¾ of term if less

– or policy has been made paid up within 10 years (or ¾ term if less)

■ And is for consideration

■ Only if for consideration

29 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

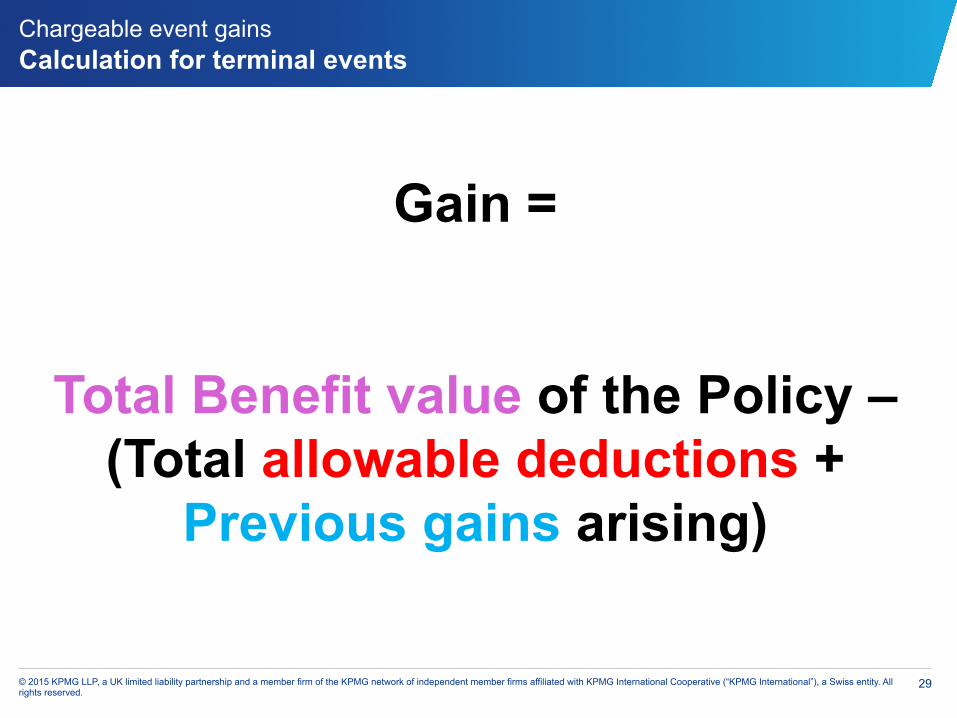

Chargeable event gains Calculation for terminal events

Gain =

Total Benefit value of the Policy – (Total allowable deductions +

Previous gains arising)

30 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

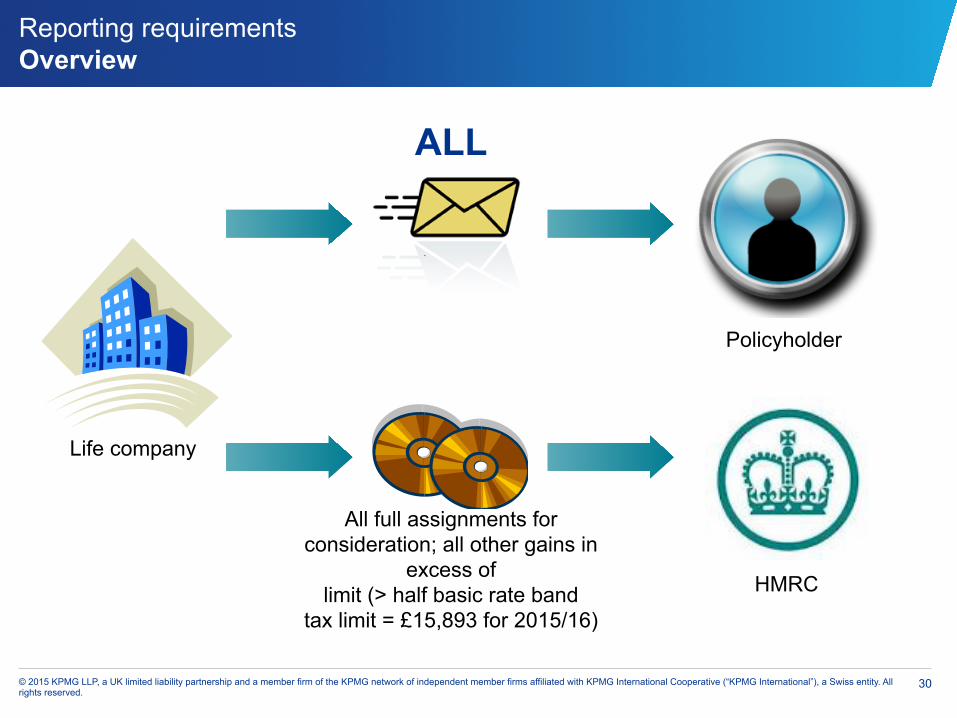

Reporting requirements Overview

Life company

HMRC

Policyholder

ALL

All full assignments for consideration; all other gains in

excess of limit (> half basic rate band

tax limit = £15,893 for 2015/16)

31 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Reporting requirements Reporting to policyholder

No prescribed format 7

Policy number 1

Nature of chargeable event 2

Date of occurrence (sometimes more than one date required) 3

Number of relevant years 4

Chargeable event gain 5

Whether basic rate tax to be treated as paid, including amount (unless event is a full assignment)

6

Different requirements for full assignment - Time frame for reporting: later of 3 months from event / receipt of written notification - Report only 'substantial' gains and all full assignments for consideration

32 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

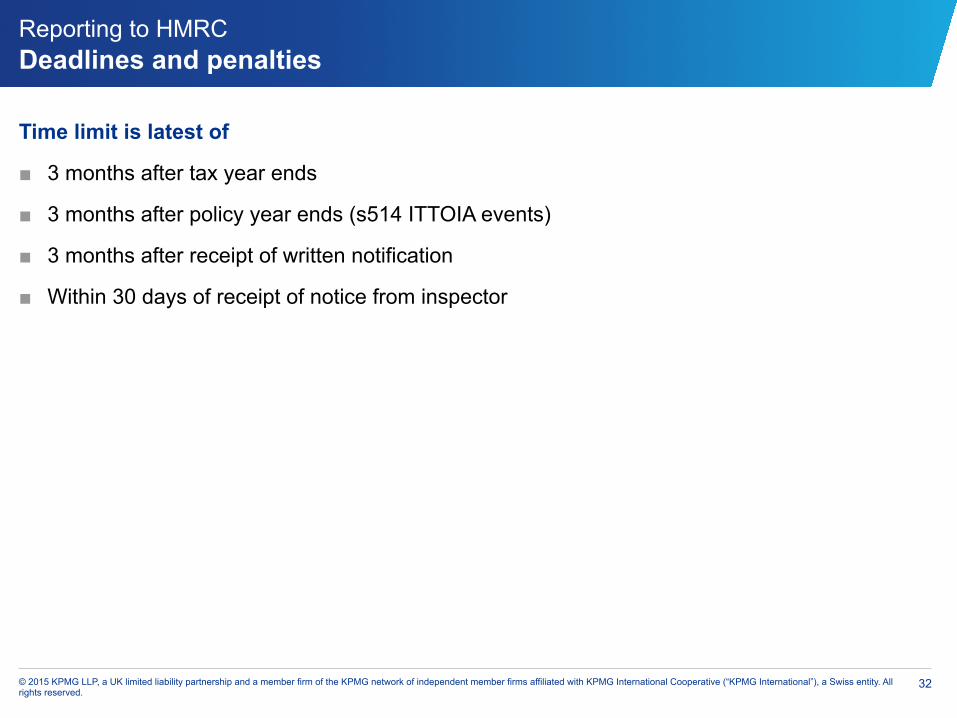

Reporting to HMRC Deadlines and penalties

Time limit is latest of

■ 3 months after tax year ends

■ 3 months after policy year ends (s514 ITTOIA events)

■ 3 months after receipt of written notification

■ Within 30 days of receipt of notice from inspector

33 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Chargeable events Common problems

Common issues

Systems issues- full automation

complex

Legacy problems

Late issue of CECs on death

Failure to recognise an

event has occurred

Gains incorrect

34 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

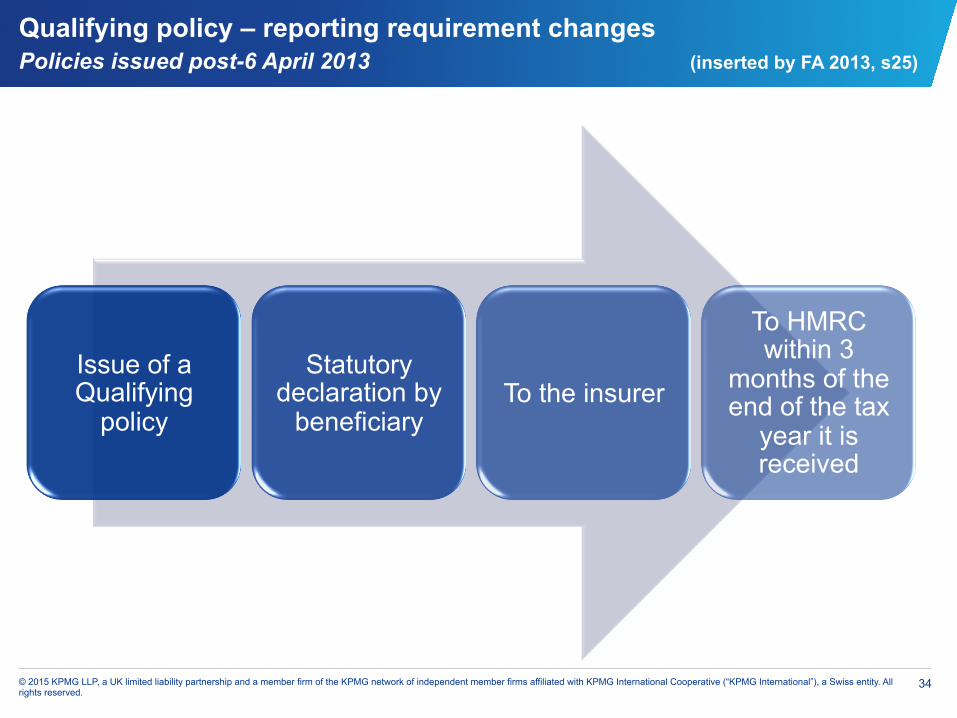

Qualifying policy – reporting requirement changes Policies issued post-6 April 2013 (inserted by FA 2013, s25)

Issue of a Qualifying

policy

Statutory declaration by

beneficiary To the insurer

To HMRC within 3

months of the end of the tax

year it is received

Qualifying v Non-qualifying

36 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Qualifying versus Non qualifying policies

Qualifying policy Non qualifying policy

Regular, long term savings with protection Irregular, shorter term, investment products

■ Term of at least 10 years ■ Term of any length

■ Premiums payable for 10 years (at least annually) ■ Single premium commonly

■ Premium spread conditions ■ Lumpy premium payments okay

■ Minimum sum assured ■ Minimal mortality/morbidity cover

■ No longer needs to be certified by HMRC at inception (Friendly societies never needed as tax exempt)

■ No certification requirement

■ Maximum annual contributions input of £3,600

Special Friendly society rules (always self-certified and Premiums payable under any single friendly society tax exempt policy made on or after 1 May 1995 must not exceed £270 in any 12 month period, or £300 if premiums are payable more frequently than annually, for instance quarterly or monthly)

37 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

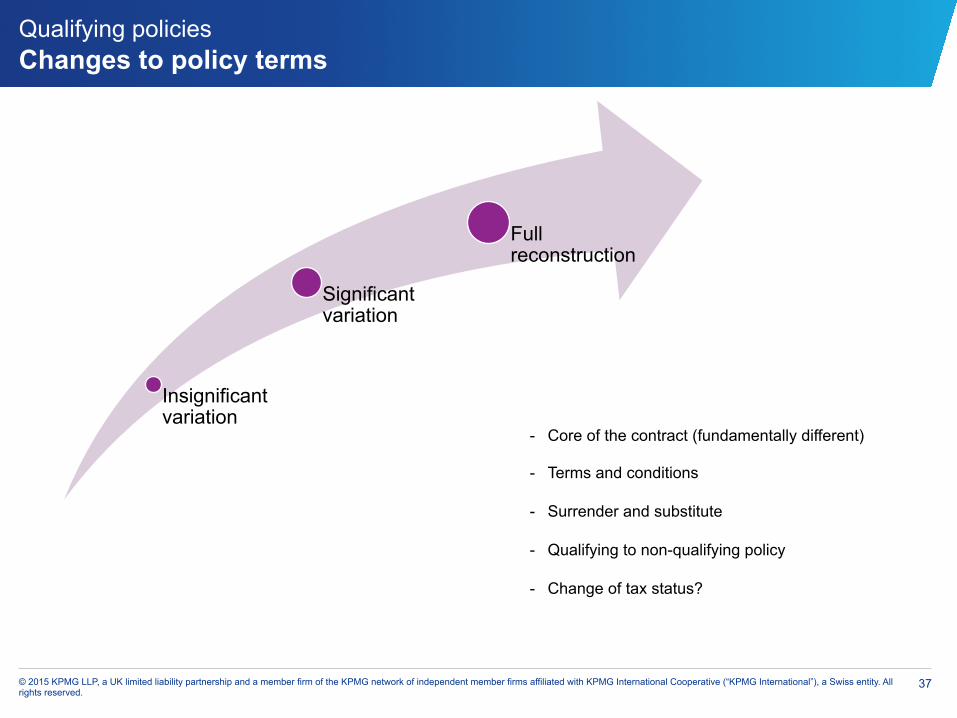

Qualifying policies Changes to policy terms

Insignificant variation

Significant variation

Full reconstruction

- Core of the contract (fundamentally different)

- Terms and conditions

- Surrender and substitute

- Qualifying to non-qualifying policy

- Change of tax status?

38 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Cancellation and substitution Examples

Addition or removal of an option which if exercised would end the policy

Changes to lives assured (possible exception for QP)

Conversion between whole of life, endowment or term assurance

Change from first death to last survivor or vice versa

Anything which is fundamental

Addition or removal of a disability and / or critical illness benefit payment of which would have terminated the contract

Reducing premium to a nominal amount (“peppercorn”)

39 © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

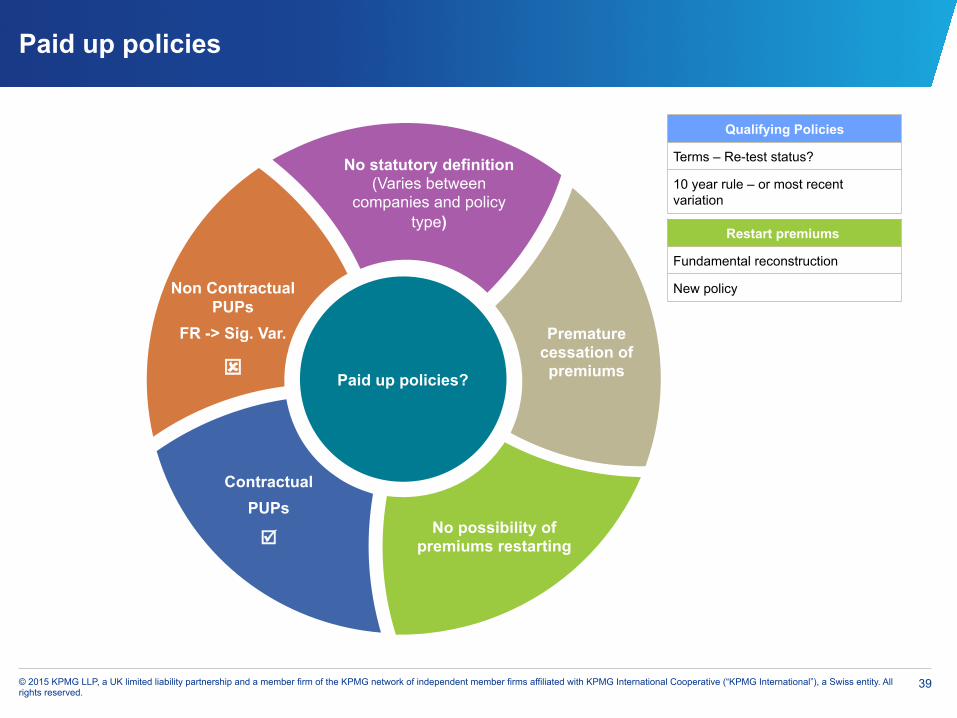

Paid up policies

No statutory definition (Varies between

companies and policy type)

Premature cessation of premiums

No possibility of premiums restarting

Contractual PUPs

þ

Non Contractual

PUPs FR -> Sig. Var.

ý Paid up policies?

Restart premiums

Fundamental reconstruction

New policy

Qualifying Policies

Terms – Re-test status?

10 year rule – or most recent variation

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Life Insurance -Chargeable Event Gains The Audit Process

Jim Adam & Dave Pendreigh

LB Scotland & Northern Ireland

Life Insurance -Chargeable Event Gains The Audit Process

Background

• Our role in the audit process

• Your role in the audit process

• No insurer or friendly society is exempt from an audit

| 44

Life Insurance -Chargeable Event Gains The Audit Process

Method of Selection

Risk based selection based on: 1. Previous audit results, if any

2. Changes in systems within the company

3. Changes in third party administrators etc.

4. Information received

Life Insurance -Chargeable Event Gains The Audit Process

Initial Contact

• Initial contact will be by e-mail or phone and may follow on from discussion at a risk review meeting between the Head of Tax and the CRM.

• Potential dates will be discussed.

• We are happy to accommodate timing preferences.

Life Insurance -Chargeable Event Gains The Audit Process

Audit Notice

• The audit notice is a formal document detailing specific requirements relating to products, systems and processes

Life Insurance -Chargeable Event Gains The Audit Process

Prior to the Audit

• Pre audit meeting • Managers responsible for CE processes • IT support

• Above includes any 3rd party providers

• Internal Audit

Life Insurance -Chargeable Event Gains The Audit Process

Exception reports

• Exception reports should be produced in excel format with a separate tab for

each event type

• Exception reports should contain details of every event during the specified audit period

• The audit period will generally be from the end of the last audit period to 5 April in the last completed tax year

Life Insurance -Chargeable Event Gains The Audit Process

Selection of Samples

• On receipt of the exception reports we will make an appropriate selection of

samples

• The samples will then be returned to the company to enable them to prepare for the audit visit.

• Sample sizes vary but we cannot carry out statistical sampling.

Life Insurance -Chargeable Event Gains The Audit Process

Audit visit

• With good planning and co-operation from the business we have found that we can usually complete an audit visit for even the larger insurers within one week, often involving only three days on site.

• For a small friendly society this should be much quicker

Life Insurance – Chargeable Event Gains The Audit Process

Qualifying Policies & Tax Exempt Savings Plans

• Paid up policies

• Policies which have been varied

• Policies which have lost QP status

Life Insurance – Chargeable Event Gains The Audit Process

Qualifying Policies & Tax Exempt Savings Plans

• Discuss systems in place to identify any changes or breaches of the premium limits.

• Look at Internal guidance to ensure that processing staff are aware of what is required when variations occur.

• Look at processes in place to ensure that statements are being sent and received.

• Check to ensure that the insurer has complied with the reporting requirements.

• Offer advice where required

Life Insurance -Chargeable Event Gains The Audit Process

Voluntary Disclosures

• There are a number of companies who are very proactive in submitting voluntary disclosures outwith the audit process.

• We would like to encourage this.

Life Insurance -Chargeable Event Gains The Audit Process

Penalties • The penalty for a late certificate is a maximum of £300 per error. • The penalty for an incorrect certificate is a maximum of £3,000 per error • Penalties will be considered in all cases where there has been a failure to issue

certificates correctly and on time. • Abatement of penalties is considered based on Disclosure, Co-operation and

Seriousness • This applies equally to errors found during an audit and voluntary disclosures

made by companies to HMRC • Each disclosure will be looked at separately

Thank you Jim Adam

Contact: 03000 541796 [email protected]

John McCrossan

Contact 03000 541795 [email protected]

Dave Pendreigh

Contact: 03000 541799 [email protected]

AFM UPDATE Martin Shaw, June 2015

!

Stewardship Financial inclusion

VALUES OF MUTUALITY

Customer-owned

Supporting communities

Caring

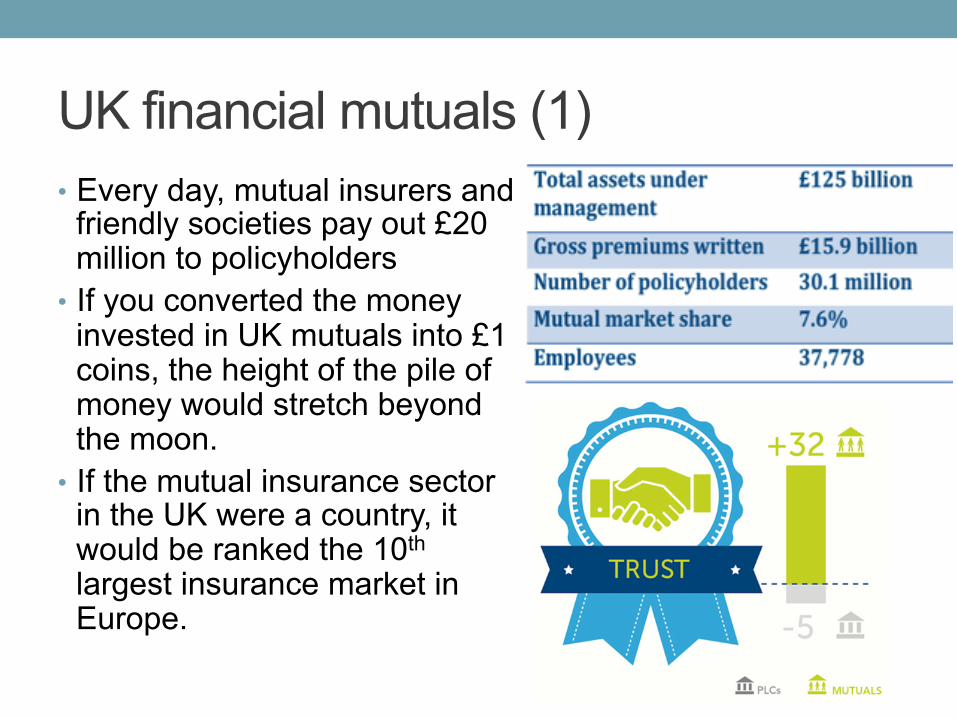

UK financial mutuals (1) • Every day, mutual insurers and

friendly societies pay out £20 million to policyholders

• If you converted the money invested in UK mutuals into £1 coins, the height of the pile of money would stretch beyond the moon.

• If the mutual insurance sector in the UK were a country, it would be ranked the 10th largest insurance market in Europe.

UK financial mutuals (2) • 7% of the insurance sector; 20% mortgage market • Around half the population are a member of one or more

mutuals • Demutualisations mean almost 90% of mutual insurance

market lost in last 20 years • 85% of sector within five largest mutual insurers: due to

mergers and relative growth

The Times, 3 June 2015

Mutual capital: an abiding issue • Accumulating capital

• Constraints on growth• Who owns the capital

• “All, or almost all the capital in a with-profits fund belongs to the with-profits policyholders”

• Solvency 2 • Higher capital levels, and restrictions on its use

• We’ve been working on solutions • Regulatory option to define mutual capital• Political inquiry in 2014• And…

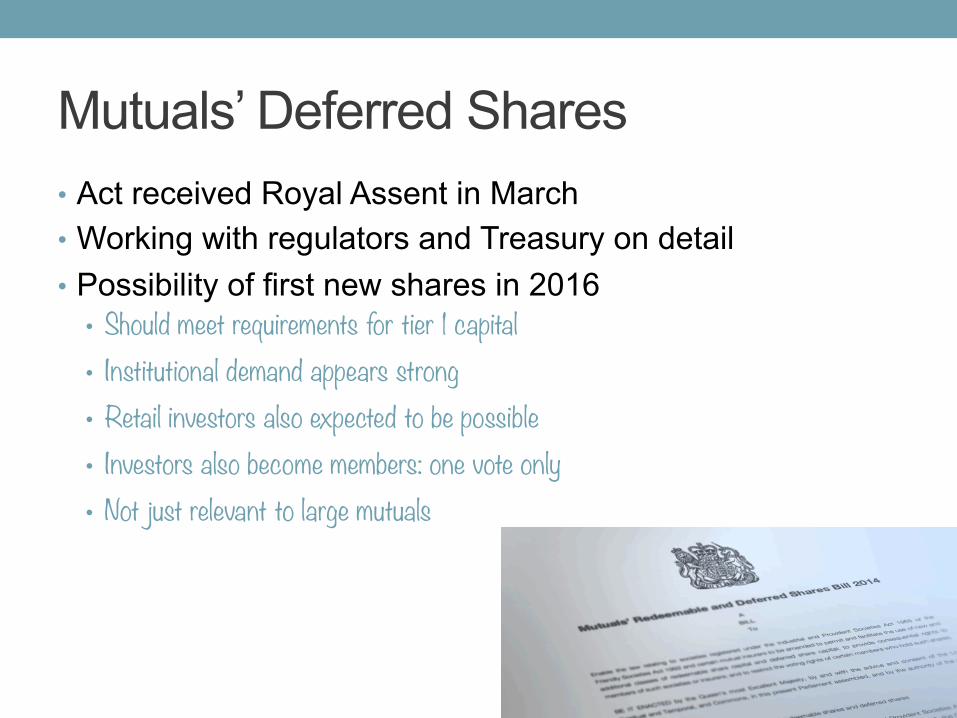

Mutuals’ Deferred Shares • Act received Royal Assent in March • Working with regulators and Treasury on detail • Possibility of first new shares in 2016

• Should meet requirements for tier 1 capital• Institutional demand appears strong• Retail investors also expected to be possible• Investors also become members: one vote only• Not just relevant to large mutuals

members Board

Committees

Working groups

networks conference

AGM

Working with

partners

Member visits

• Newsletters • Blogs • Updates • Websites • E-learning

AFM: connecting with members

AFM UPDATE Martin Shaw, June 2015

!

AFM TAX TRAINING DAY Hosted by Deloitte 16 June 2015

!

AFM Automatic exchange of information and the Common Reporting Standard (CRS) Presented by Peter Frost and Graham Miller 16 June 2015

Agenda

► Introduction - the journey so far

► CRS overview

► CRS key differences from FATCA.

► A word on reporting to HMRC

► HMRC Developments and Guidance update

► Royal London – The practicalities of CRS implementation

► Questions

Page 66

Introduction – The journey so far

Introduction – The journey so far

Page 68

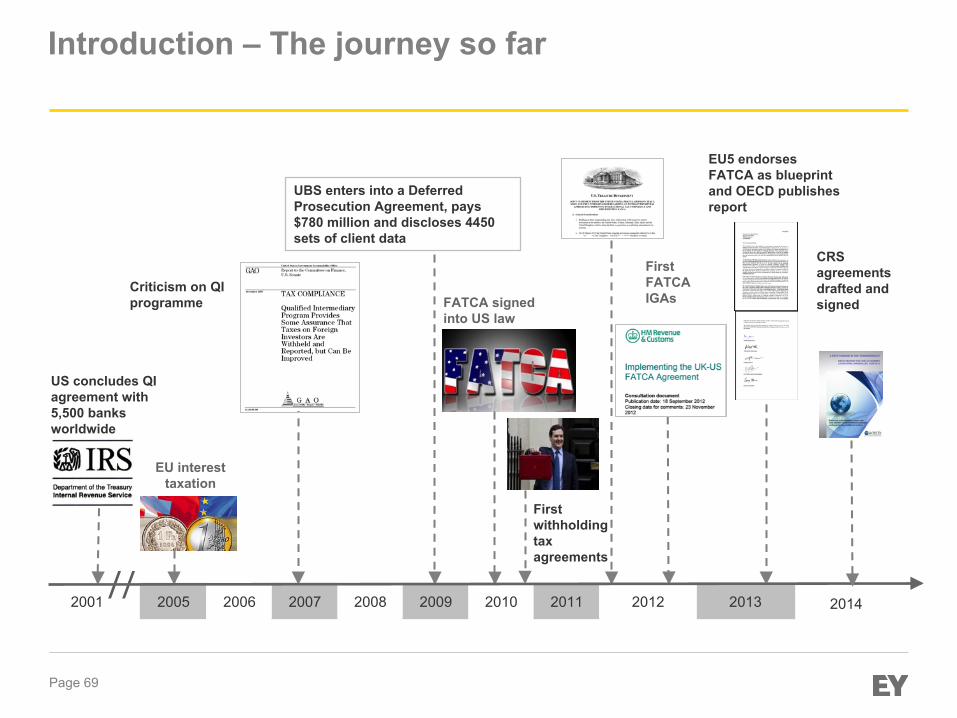

Ø Increasing globalisation has made it easier for taxpayers to hold and manage investments through financial institutions outside of their country of residence. Large amounts of money are kept offshore and can go untaxed should the “tax shy” fail to comply with the tax requirements of their home jurisdiction.

Ø A few recent examples of countries tackling the “tax shy” includes Ø Spain going after footballers and a princess. Ø UK prosecuting celebrities using tax avoidance schemes. Ø UBS at the centre of an investigation into offshore accounts by the French authorities . Ø The Swiss investigating FIFA. Ø The Italians launching a search of Credit Suisse’s Milan offices in their hunt for tax evasion

involving insurance policies.

Ø Co‑operation between tax administrations is seen as key in the fight against tax evasion and in protecting the integrity of tax systems. A key aspect of that co‑operation is exchange of information. That is the model underpinning FATCA and that is the model on which the Common Standard is based.

Introduction – The journey so far

2001 2005 2007 2006 2009 2008 2011 2010 2012 2013

EU interest taxation

Criticism on QI programme

First withholding tax agreements

US concludes QI agreement with 5,500 banks worldwide

UBS enters into a Deferred Prosecution Agreement, pays $780 million and discloses 4450 sets of client data

First FATCA IGAs

EU5 endorses FATCA as blueprint and OECD publishes report

CRS agreements drafted and signed FATCA signed

into US law

Page 69

2014

CRS overview

The Common Reporting Standard

Page 71

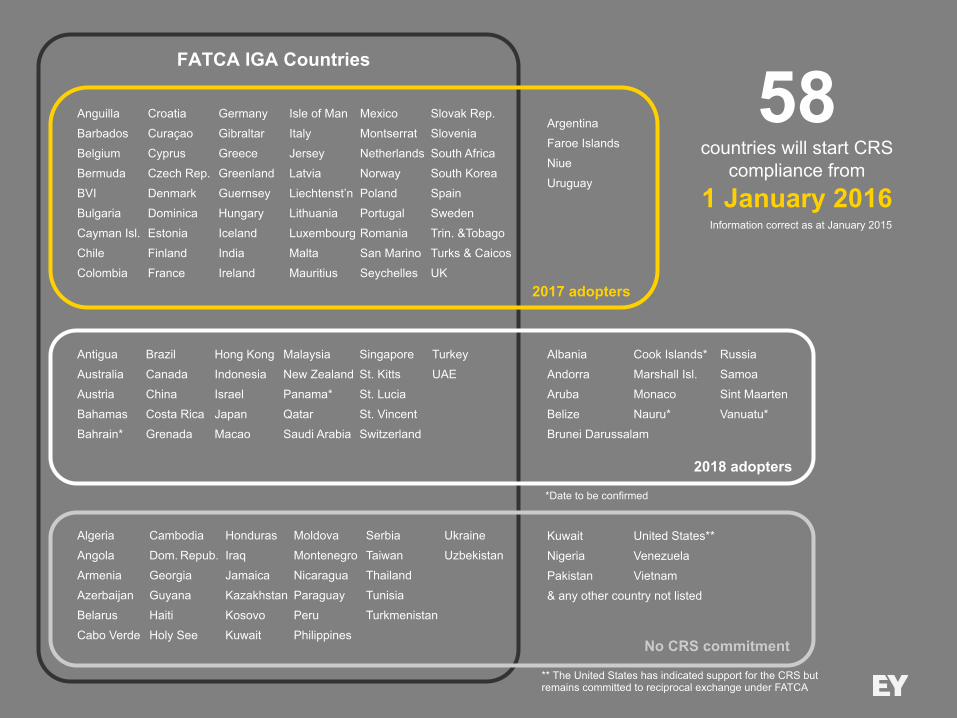

► Blueprint for the automatic exchange of information issued by the OECD on 15 July 2014 covering 307 pages.

► Mandatory early adoption by EU member states is a requirement of the EU Directive on Administrative Cooperation (DAC) published on 14 October 2014.

► The CRS model covers: i. Definitions; ii. Types of information to exchange; iii. The time and manner of exchange; iv. Collaboration and enforcement; v. Confidentiality of data and safeguards that must be respected; and vi. Commentary

► It also states that “Given that implementation will be based on domestic law, it is important to ensure consistency in application across jurisdictions to avoid creating unnecessary costs and complexity for financial institutions in particular those with operations in more than one jurisdiction”

Anguilla Croatia Germany Isle of Man Mexico Slovak Rep.

Barbados Curaçao Gibraltar Italy Montserrat Slovenia

Belgium Cyprus Greece Jersey Netherlands South Africa

Bermuda Czech Rep. Greenland Latvia Norway South Korea

BVI Denmark Guernsey Liechtenst’n Poland Spain

Bulgaria Dominica Hungary Lithuania Portugal Sweden

Cayman Isl. Estonia Iceland Luxembourg Romania Trin. &Tobago

Chile Finland India Malta San Marino Turks & Caicos

Colombia France Ireland Mauritius Seychelles UK

Algeria Cambodia Honduras Moldova Serbia Ukraine

Angola Dom. Repub. Iraq Montenegro Taiwan Uzbekistan

Armenia Georgia Jamaica Nicaragua Thailand

Azerbaijan Guyana Kazakhstan Paraguay Tunisia

Belarus Haiti Kosovo Peru Turkmenistan

Cabo Verde Holy See Kuwait Philippines

Argentina

Faroe Islands

Niue

Uruguay

Albania Cook Islands* Russia

Andorra Marshall Isl. Samoa

Aruba Monaco Sint Maarten

Belize Nauru* Vanuatu*

Brunei Darussalam

Antigua Brazil Hong Kong Malaysia Singapore Turkey

Australia Canada Indonesia New Zealand St. Kitts UAE

Austria China Israel Panama* St. Lucia

Bahamas Costa Rica Japan Qatar St. Vincent

Bahrain* Grenada Macao Saudi Arabia Switzerland

FATCA IGA Countries

2017 adopters

2018 adopters

Kuwait United States**

Nigeria Venezuela

Pakistan Vietnam

& any other country not listed

No CRS commitment

58 countries will start CRS

compliance from 1 January 2016

Information correct as at January 2015

** The United States has indicated support for the CRS but remains committed to reciprocal exchange under FATCA

*Date to be confirmed

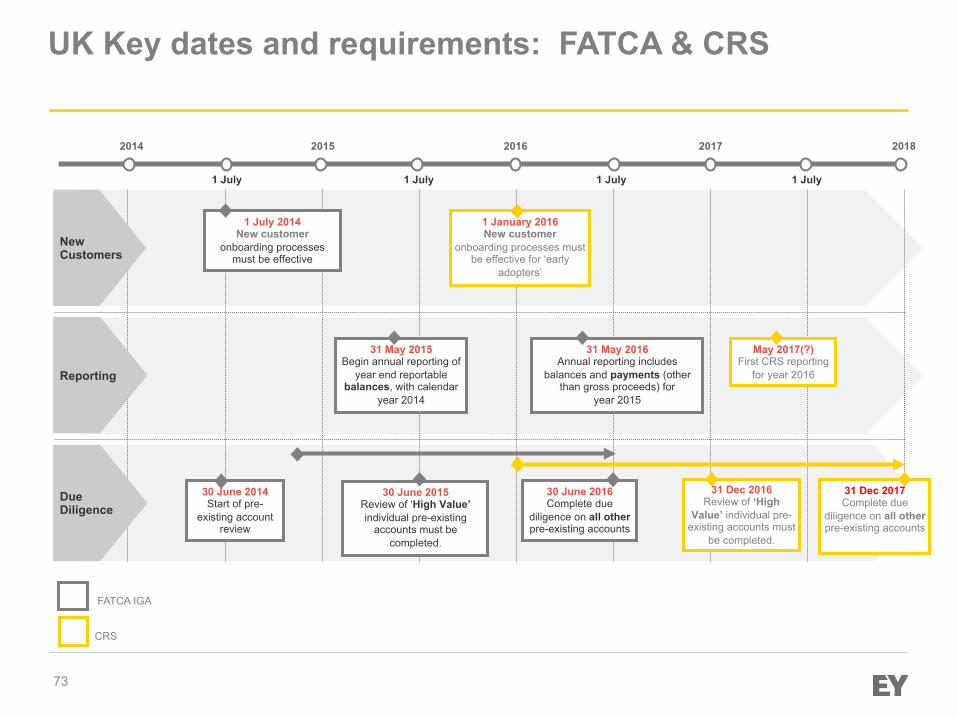

UK Key dates and requirements: FATCA & CRS

Due Diligence

Reporting

New Customers

1 July 2014 New customer

onboarding processes must be effective

1 January 2016 New customer

onboarding processes must be effective for ‘early

adopters’

31 May 2016 Annual reporting includes

balances and payments (other than gross proceeds) for

year 2015

31 Dec 2016 Review of ‘High

Value’ individual pre-existing accounts must

be completed.

31 Dec 2017 Complete due

diligence on all other pre-existing accounts

30 June 2015 Review of ‘High Value’ individual pre-existing

accounts must be completed.

30 June 2016 Complete due

diligence on all other pre-existing accounts

30 June 2014 Start of pre-

existing account review

May 2017(?) First CRS reporting

for year 2016

1 July

2014 2015 2016 2017 2018

1 July 1 July 1 July

31 May 2015 Begin annual reporting of

year end reportable balances, with calendar

year 2014

FATCA IGA

CRS

73

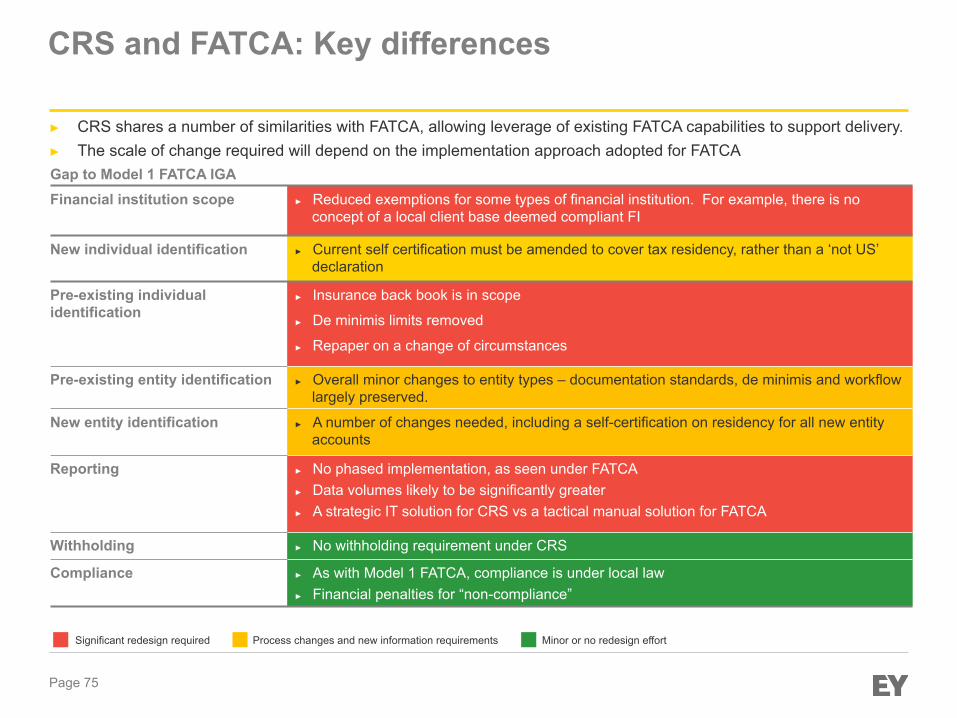

CRS and FATCA: Key differences

CRS and FATCA: Key differences ► CRS shares a number of similarities with FATCA, allowing leverage of existing FATCA capabilities to support delivery. ► The scale of change required will depend on the implementation approach adopted for FATCA Gap to Model 1 FATCA IGA Financial institution scope ► Reduced exemptions for some types of financial institution. For example, there is no

concept of a local client base deemed compliant FI

New individual identification ► Current self certification must be amended to cover tax residency, rather than a ‘not US’ declaration

Pre-existing individual identification

► Insurance back book is in scope

► De minimis limits removed

► Repaper on a change of circumstances

Pre-existing entity identification ► Overall minor changes to entity types – documentation standards, de minimis and workflow largely preserved.

New entity identification ► A number of changes needed, including a self-certification on residency for all new entity accounts

Reporting ► No phased implementation, as seen under FATCA ► Data volumes likely to be significantly greater ► A strategic IT solution for CRS vs a tactical manual solution for FATCA

Withholding ► No withholding requirement under CRS

Compliance ► As with Model 1 FATCA, compliance is under local law ► Financial penalties for “non-compliance”

Significant redesign required Process changes and new information requirements Minor or no redesign effort

Page 75

CRS and UK penalties for non-compliance

Penalties for failure to comply with CRS Regulations ► Failure to comply with the Regulations incurs a fixed penalty of £300

Daily default penalties

► After notification of a failure to comply, a further penalty of up to £60 a day may be levied for each subsequent day of non-compliance

Penalty for inaccurate information ► A penalty of up to £3,000 may be due if

► A) there is a failure to identify reportable accounts, or a deliberate act, or ► B) The inaccuracy is known, but not disclosed to HMRC, or ► C) The inaccuracy is later discovered, and reasonable steps are not taken to notify

HMRC

Reporting considerations

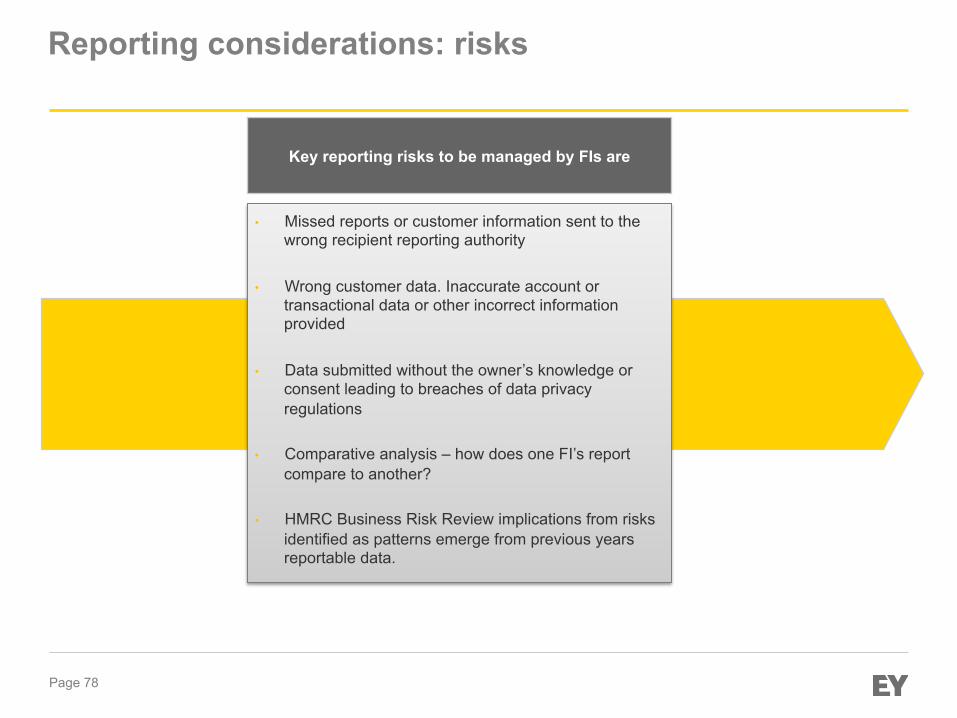

Reporting considerations: risks

Key reporting risks to be managed by FIs are

• Missed reports or customer information sent to the wrong recipient reporting authority

• Wrong customer data. Inaccurate account or transactional data or other incorrect information provided

• Data submitted without the owner’s knowledge or consent leading to breaches of data privacy regulations

• Comparative analysis – how does one FI’s report

compare to another?

• HMRC Business Risk Review implications from risks identified as patterns emerge from previous years reportable data.

Page 78

Reporting considerations: solutions

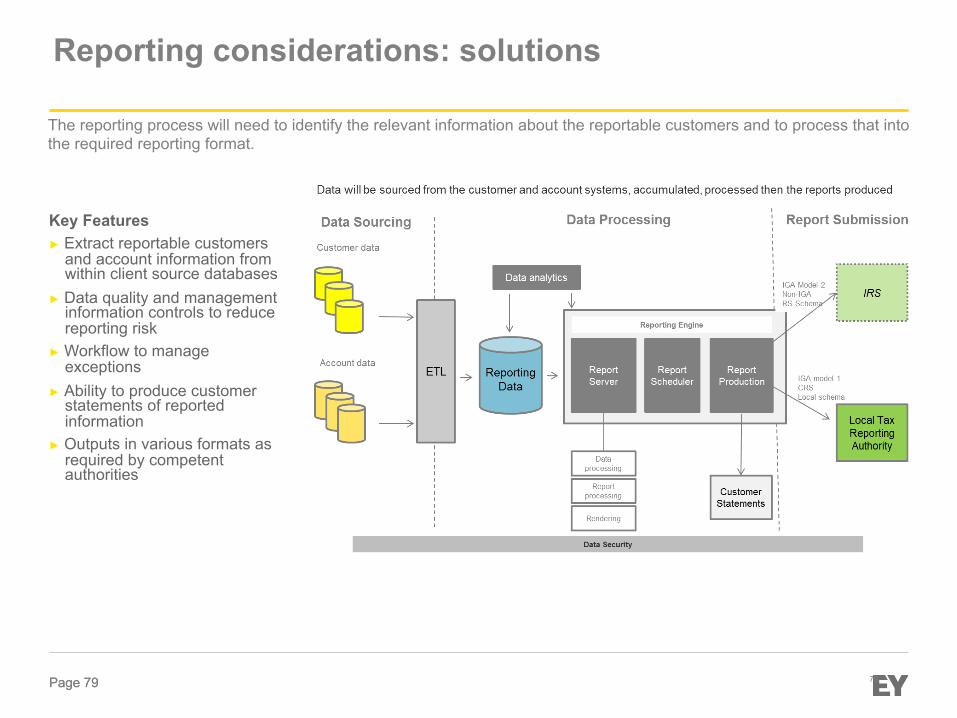

The reporting process will need to identify the relevant information about the reportable customers and to process that into the required reporting format.

Key Features ► Extract reportable customers

and account information from within client source databases

► Data quality and management information controls to reduce reporting risk

► Workflow to manage exceptions

► Ability to produce customer statements of reported information

► Outputs in various formats as required by competent authorities

79 Page 79 Page 79

HMRC developments & guidance update

HMRC developments & guidance update

Page 81

Ø Guidance is due in the “summer”.

Ø HMRC have asked for a list by today of priority areas for them to focus on at a meeting on Friday. Ø Key issues for consideration include

Ø Due diligence guidance for accounts held by trusts. Ø Due diligence guidance for the insurance back book. Ø Assistance with procedures in cases involving policy assignments. Ø Guidance to include practical examples involving the use of platforms to distribute products. Ø Clarity over the circumstances where a self certification must be obtained before an account is

opened. Ø A description of compliance activity and examples of instances where penalties may apply. Ø Reporting and guidance over when a nil report is required. Ø Guidance over what amounts to sufficient notification for an individual reportable person.

THE PRACTICALITIES OF CRS IMPLEMENTATION

16 June 2015 Graham Miller

THE PRACTICALITIES OF CRS IMPLEMENTATION

• Royal London - Background

• FATCA experiences – Self certificates

• Initial CRS impact assessment

• Back book review

• On-boarding

• IT based solutions – manual based approach?

• Other considerations

• Summary

• Questions

83

INTRODUCTION

THE PRACTICALITIES OF CRS IMPLEMENTATION

• We have approx. 5.3 million customers with 9 million policies.

• We are mainly based in the UK but have establishments in Guernsey and Ireland.

• We have expanded over the last 15 years through a succession of acquisitions of other life assurance companies.

• Aside from life assurance we offer a wide range of collective investment products and operate a fund platform.

• Focusing on the life assurance business we mostly write pensions and protection but have a small amount of With Profits business too.

• Significant amount of legacy with profits business.

84

ROYAL LONDON - BACKGROUND

THE PRACTICALITIES OF CRS IMPLEMENTATION

• Exemption for individual policies for US FATCA.

• De-minimis limits have also helped to reduce cases to review.

• Generally FATCA has had a relatively light impact

• Still some administration issues……self certificates……..!!

85

ROYAL LONDON - BACKGROUND

THE PRACTICALITIES OF CRS IMPLEMENTATION

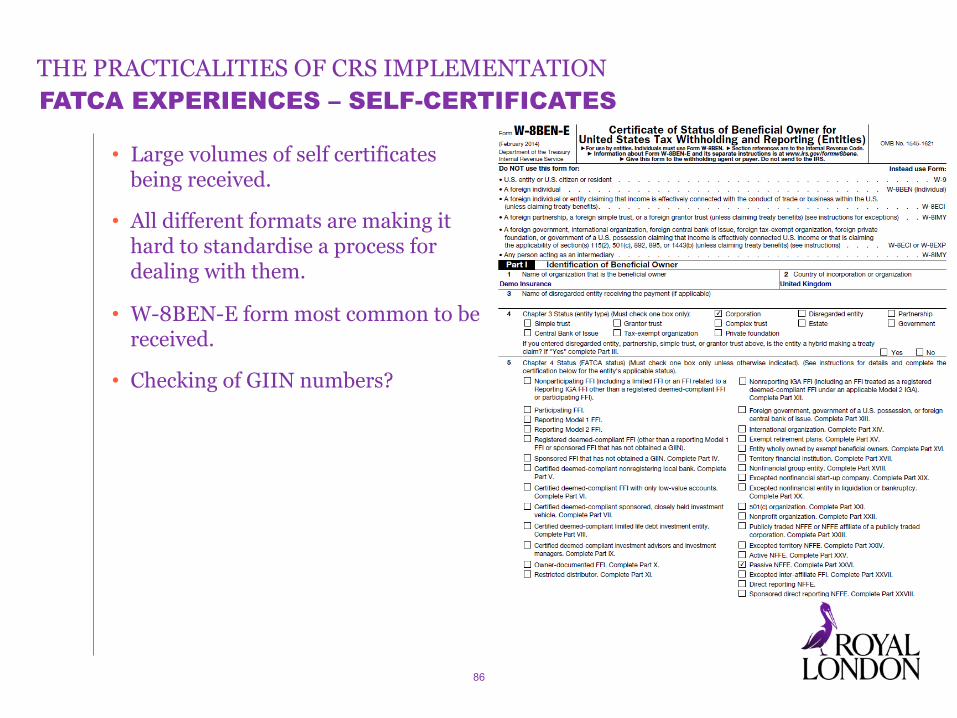

• Large volumes of self certificates being received.

• All different formats are making it hard to standardise a process for dealing with them.

• W-8BEN-E form most common to be received.

• Checking of GIIN numbers?

86

FATCA EXPERIENCES – SELF-CERTIFICATES

THE PRACTICALITIES OF CRS IMPLEMENTATION

• We have adopted the Investment Association template as our standard document, however,

• Clients find it difficult to understand the technicalities so make up their own categories.

• Some add in new check boxes, e.g. “Non-Profit organisation”

87

FATCA EXPERIENCES – SELF CERTIFICATES

THE PRACTICALITIES OF CRS IMPLEMENTATION

• Generally there is a poor response rate for requests for self certificates, about 20% non-returns.

• Current totals suggest we will be reporting around 2,500 un-documented cases,

• Platform business accounts for majority of cases – poor IFA FATCA awareness

• Additional administration involved with chase-up process.

• On the positive side using the $50,000 de-minimis limit for new individual policies has helped to reduce the need to issue self-certificates.

88

FATCA EXPERIENCES – SELF CERTIFICATES

THE PRACTICALITIES OF CRS IMPLEMENTATION

• FATCA – used the exemptions and de-minimis limits to reduce administration work, but…for CRS….

• Removal of exemption for policies issued to individuals.

• Coupled with the removal of the $250,000 de-minimis limit for lower value individual policies.

• Plus 58 countries to report on from 1 January 2016 onwards.

• On top of that further entrants in 2017.

• Result…….a lot more administration work to do!!!

• Significantly more cases to (potentially) report • Under FATCA, due to the exemptions, we have small volumes of insurance

cases to report – in the region of low 100’s • Under CRS we anticipate having thousands of insurance cases to report

89

INITIAL CRS ASSESSMENT – INSURANCE BACK BOOK REVIEW

THE PRACTICALITIES OF CRS IMPLEMENTATION

• For CRS our on-boarding process will mostly apply to assignments of policies in our legacy book of insurance business.

• For FATCA we have used the $50,000 exemption limit on individual policies to drastically slim down the amount of self certificates issued but….

• For CRS there is no exemption limit so a self certificate must be issued for every assignment.

• Our experience under FATCA has told us that policies are assigned first and then we are told after the event.

• It is also impossible to enforce self-certification procedure as there are no conditions in the policy contract to deal with this.

• Therefore we have to accept the assignment first and deal with the self certificate process afterwards. No opportunity to enforce completion of self-certificate before assignment.

• So, under CRS we expect there to be a much greater level of administration work that has to be undertaken!!

90

INITIAL CRS ASSESSMENT - ON-BOARDING (NEW BUSINESS)

THE PRACTICALITIES OF CRS IMPLEMENTATION

• We have a lot of old legacy based life systems that are used to service our closed book businesses .

• At best they are difficult and costly to change, at worst they cannot be changed.

• For FATCA, due to the limited number of cases, we have applied an offline spreadsheet based data storage approach. Cheap and effective.

91

IT BASED SOLUTIONS / MANUAL BASED APPROACH?

THE PRACTICALITIES OF CRS IMPLEMENTATION

• Under CRS, with the significant increase in the number of cases to review and report this option is not likely to be viable.

• Also we need to capture additional data in respect of: • Place of birth (possibly?) • Tax Identification Number (TIN)

• Therefore we have no option but to consider implementing an IT based solution.

• This is likely to be costly to implement but would appear to be the only solution.

92

IT BASED SOLUTIONS / MANUAL BASED APPROACH

THE PRACTICALITIES OF CRS IMPLEMENTATION

• The implementation date of 1 Jan 2016 is set.

• This avoids the repetition of moving deadlines suffered with FATCA.

• However, it only gives us 6 months to complete our project.

• There may be opportunities to harmonise procedures between FATCA and CRS and this may be necessary to limit the compliance complications, especially around the use of de-minimis limits.

• We have to factor in the need for the additional review of the back book business when new territories sign up to CRS in later years.

• And look for opportunities to future proof your systems/processes especially for the back book review and new entrants.

93

OTHER CONSIDERATIONS

THE PRACTICALITIES OF CRS IMPLEMENTATION

• No individual exemption and lack of de-minimus limits means much more administrative work to undertake.

• IT solutions are likely to need to be developed if not already in place – costs will be involved.

• The fixed deadline means we need to start acting now in order to meet the 1 January 2016 deadline date.

94

SUMMARY

95

Questions?

THANK YOU

Intermission

Hot Topics Philip Lewis, PwC

www.pwc.com

Graham Wilson

Hot Topics From the “Coal face”

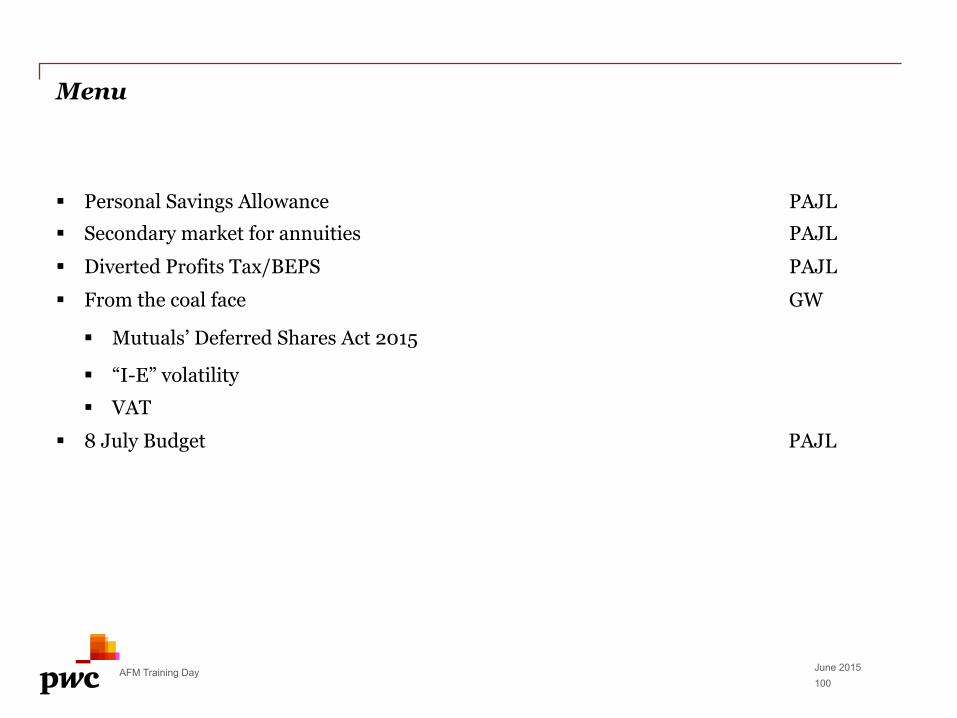

Menu

§ Personal Savings Allowance PAJL § Secondary market for annuities PAJL § Diverted Profits Tax/BEPS PAJL § From the coal face GW

§ Mutuals’ Deferred Shares Act 2015

§ “I-E” volatility § VAT

§ 8 July Budget PAJL

June 2015 AFM Training Day 100

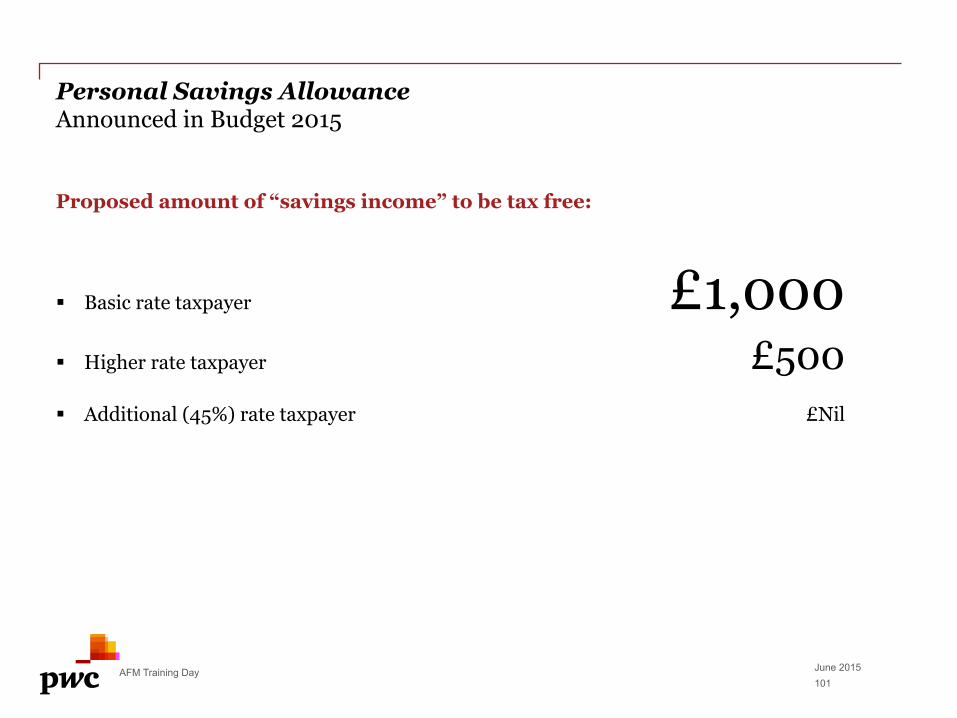

Personal Savings Allowance Announced in Budget 2015

Proposed amount of “savings income” to be tax free:

§ Basic rate taxpayer £1,000 § Higher rate taxpayer £500 § Additional (45%) rate taxpayer £Nil

June 2015 AFM Training Day 101

Personal Savings Allowance Should be effective 6 April 2016

Key questions (o/s) § What is savings income – existing definition includes chargeable events gains (but not

pension income) § Factsheet only refers to “interest” § Interaction with other provisions e.g. starting rate for savings (0%) § Banks no longer need deduct tax – what about insurers? Issues for insurers § Competition – chargeable event gains already effectively tax free for basic rate taxpayers § Competition – undermines benefits of e.g. TESPs § AFM will be speaking to HMRC on implications for the mutual life sector

June 2015 AFM Training Day 102

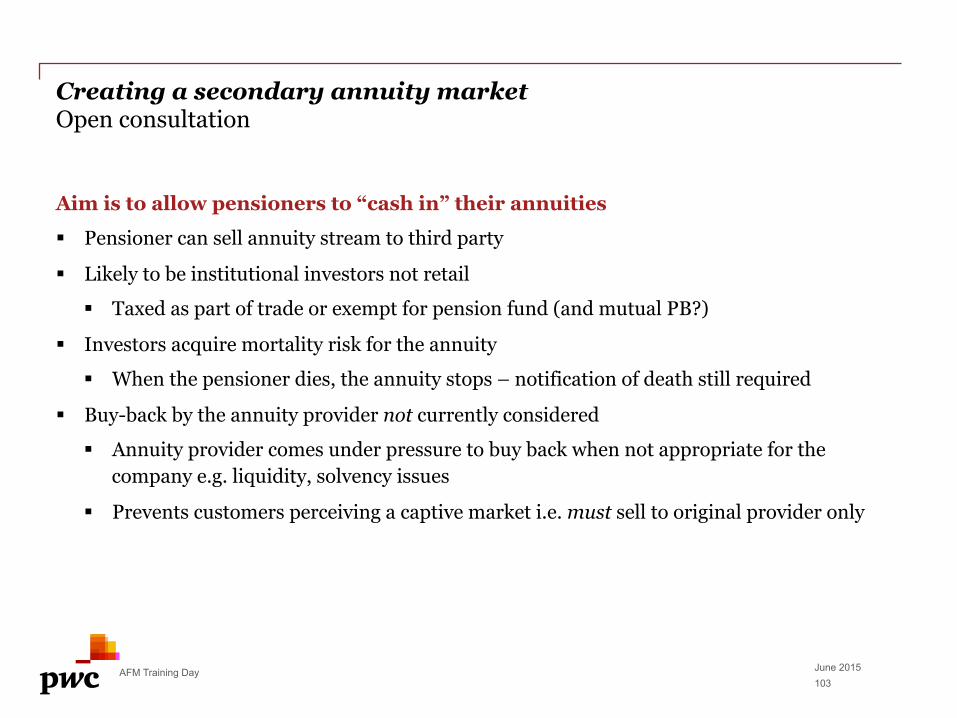

Creating a secondary annuity market Open consultation

Aim is to allow pensioners to “cash in” their annuities

§ Pensioner can sell annuity stream to third party

§ Likely to be institutional investors not retail

§ Taxed as part of trade or exempt for pension fund (and mutual PB?)

§ Investors acquire mortality risk for the annuity

§ When the pensioner dies, the annuity stops – notification of death still required

§ Buy-back by the annuity provider not currently considered

§ Annuity provider comes under pressure to buy back when not appropriate for the company e.g. liquidity, solvency issues

§ Prevents customers perceiving a captive market i.e. must sell to original provider only

103 June 2015 AFM Training Day

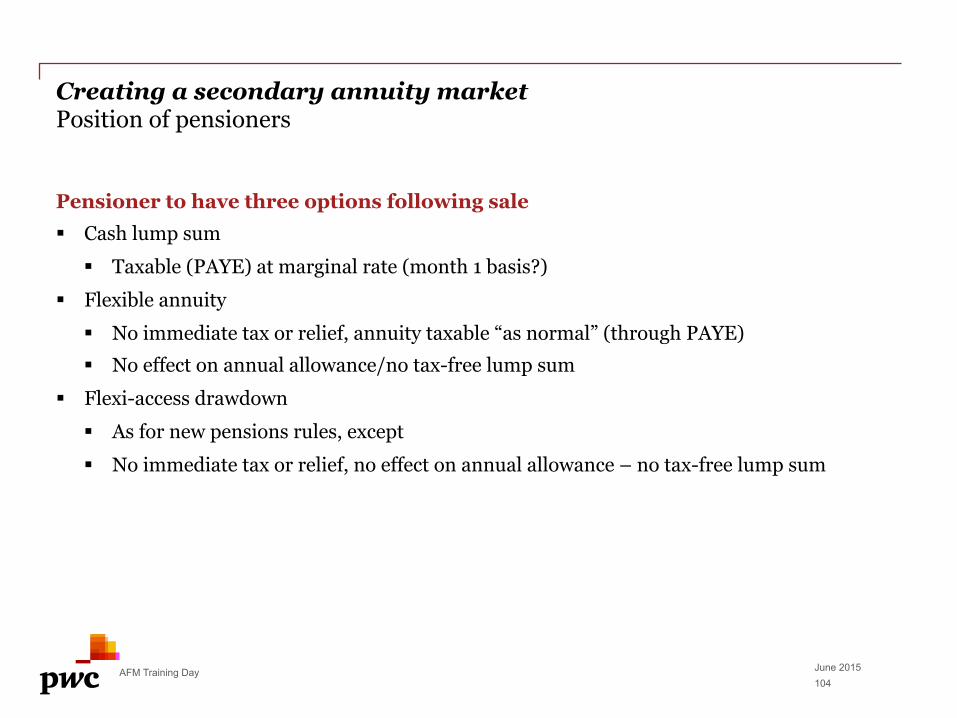

Creating a secondary annuity market Position of pensioners

Pensioner to have three options following sale § Cash lump sum

§ Taxable (PAYE) at marginal rate (month 1 basis?) § Flexible annuity

§ No immediate tax or relief, annuity taxable “as normal” (through PAYE) § No effect on annual allowance/no tax-free lump sum

§ Flexi-access drawdown § As for new pensions rules, except § No immediate tax or relief, no effect on annual allowance – no tax-free lump sum

104 June 2015 AFM Training Day

Creating a secondary annuity market Consultation still open - just

Consultation closes 18 June 2015 - Thursday Document is 28 pages long – not counting the covers § 18 questions

§ 7 on “how might the market work” § 2 on legislative changes proposed § 9 on consumer protection

§ Website states consultation closes at 23:45 (so you can go home 15 mins early!) Document can be found at: https://www.gov.uk/government/consultations/creating-a-secondary-annuity-market-call-for-evidence

June 2015 AFM Training Day 105

Diverted profits tax Tax avoidance

Diverted profits tax announced last year and came in 1 April this year Aimed to prevent companies avoiding (UK) corporation tax by “shifting” profits offshore § Two main scenarios:

§ “Avoiding a UK taxable presence”

§ “Entities or transactions lacking economic substance” § Diverted profits are taxed at 25% – therefore provides HMRC with a big stick § Notification requirements § Suggestion that application may be limited but need to consider facts

June 2015 AFM Training Day 106

Diverted profits tax Avoiding a UK taxable presence

Non-UK company “avoids” having a UK PE Does the non-UK company (carrying on an activity in the UK): § have an “effective tax mismatch”, OR § have a tax avoidance purpose? Possible application to insurers is offshore bond companies § helpful comments in guidance, but § very dependent on facts

June 2015 AFM Training Day 107

Diverted profits tax Transactions lacking economic substance

Do the transactions § have an “effective tax mismatch”,

§ profits of counterparty taxed at less than 80% of UK rate; AND § have insufficient economic substance

§ financial and other benefits < tax savings? One application to insurers is offshore reinsurance, but § may not need an offshore company § may be wider applications

June 2015 AFM Training Day 108

BEPS (Base Erosion and Profit Shifting) OECD initiatives similarly looking at diversion of profits

Ongoing OECD exercise on 15 “actions” relating to profit shifting etc Selected key areas (principally reporting later this year): § treatment of interest deductions § avoidance of permanent establishments § CFC (controlled foreign company) rules § transfer pricing – implications of risk and capital Need to keep in view – e.g. offshore bond providers may protect their position against DPT but then find the action on PEs comes into play.

June 2015 AFM Training Day 109

Graham Wilson

Hot Topics From the “Coal face”

Hot Topics Points to cover

§ Mutuals’ Deferred Shares

§ “I-E” Volatility

§ VAT

Hot Topics Mutual Deferred Shares

§ The Mutuals’ Deferred Shares Act 2015 was granted Royal Assent on 26 March 2015 and grants the Treasury power to create regulations to permit the issue of deferred shares by a friendly society or mutual insurer.

§ A number of issues need to resolved before the regulations can be implemented including Tax. The Tax Questions to be addressed include. - Will the deferred shares be treated similarly to shares or will they be treated similarly to debt - If shares, then will the dividends constitute distributions for tax purposes and will they attract a tax credit. - If debt, will distributions be deductible for corporation tax purposes and will they fall generally within the

loan relationship regime. Any withholding tax implications ? - Will the deferred shares constitute “ordinary share capital” for the purposes of corporate grouping rules - Will the issue/transfer of deferred shares attract a charge to stamp duty or stamp duty reserve tax.

§ AFM Tax Committee hope to work with HM Treasury/HMRC to progress the consideration of these issues.

Hot Topics “I-E“ Volatility

§ When New Life Tax regime introduced in 2013, expectation was that corporate tax yields from life companies to the Exchequer would fall (reduced BLAGAB business etc)

§ Actual experience in 2014 very different with large favourable movements in BLAGAB leading to the erosion or total removal of XSE a number of companies.

§ 2015 seems to be carrying on the trend of volatility. - January – large Loan relationship favourable movement - February – largely reversal of above - March – another month of favourable loan relationship movements - April – largely reversal of March - May – benign month for Loan Relationship, large favourable movements in CGT

• Volatile tax charge for companies, with the continuing need to ensure that CT & DT charge are appropriately reflected in amounts charged to the asset shares of the policyholders.

Hot Topics VAT

§ In the past much of attention to VAT efficiency in companies has concentrated on maximising their VAT Partial Exemption method.

§ However, particularly where investment management is outsourced to a third party, attention

moving to examining where VAT is incurred. § In order to mitigate the impact of VAT on such fees, besides the implications of the ATP case, the

use of structures such as Tax Transparent Funds and Authorised Contractual Schemes are being investigated.

8 July Budget Post-election jollity for the Chancellor

Not expecting huge changes to insurers – but who can say

§ AFM will send update if major implications announced

June 2015 AFM Training Day 115

Any questions ... (or any other favourite radio programme that springs to mind)

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. © 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

Contacts (because we’re here for you) Philip Lewis, PwC 020 7213 1584 [email protected] Graham Wilson, LV= 01202 542176 [email protected]

AFM TAX TRAINING DAY Hosted by Deloitte 16 June 2015

!