1.Explain how overconfidence prevents corporate boards from putting compensation systems in place that align the interests of managers and shareholders

2.Explain the role of prospect theory casino effects in aligning the interests of shareholders and managers

3

3.Describe how aversion to a sure loss can interfere with the alignment of the interests of investors and the interests of auditors engaged to monitor managers

4.Analyze how, because of aversion to a sure loss and overconfidence, stock option-based compensation can exacerbate agency conflicts

4

Traditional Approach

Agency theory is used to study the structure of compensation contracts that principals offer to agents engaged to act on their behalf.

In the corporate governance setting, shareholders are the principals, the board of directors is charged with representing the interests of shareholders, and the firm’s managers are the agents.

5

6

Plot

Bialystock raises a large amount of money from investors by selling more than 100% of a new show—25,000% actually.

He enlists a meek accountant named Leo Bloom to produce a flop that will enable him to hide his actions.

In Bialystock’s plan, the show fails, enabling him to apologize to investors for having lost their money, which he then proceeds to keep.

7

The Point

The plot of The Producers has 3 key features. 1. Principal-agent relationship involved, where

principals (the investors) entrust their money to an agent (the producer).

2. Inherent conflict of interest between the principals and the agent.

3. Third, the agent is better informed than the principals.

Only a successful show would reveal the producer’s true action.

8

Traditional Approach

Rational principals offer contracts to rational agents that combine positive rewards and penalties, so called carrots and sticks, with three goals in mind.

1. Participation: offer the agent a contract that is attractive enough.

2. Incentive compatibility: Set the carrot-stick differential to induce the agent to represent the interests of the principal.

3. Don't overpay the agent.

9

Risk and Agency Conflicts

In the traditional approach, incentive compatibility typically prevents managers from diversifying away all the unique risk of their firms, especially career risk. Managers who bear such risk might react by

behaving in too risk averse a fashion, to the detriment of investors.

In theory, managerial risk aversion can be countered by using stock options. Options reward managers for favorable outcomes,

but do not penalize them for unfavorable outcomes.

10

Paying for Performance in Practice

Most influential academic studies on executive compensation conclude that CEO pay varies far too little to be consistent with traditional theory.

These studies, published in 1990, indicate that most corporate boards do not structure salaries, bonuses, and stock options so as to provide either large rewards for superior performance or large penalties for poor performance.

11

Executive pay has featured too narrow a carrot-stick differential, resulting in low variability in respect to corporate performance.

The frequency with which CEOs are dismissed for poor results is low.

Corporate stock options do not appear to play a major role in aligning the interests of executives and investors.

Some evidence points to the relative strength of shareholder rights as being key.

12

Low Variability

For the median CEO in the 250 largest companies, a $1,000 change in corporate value corresponded to a change of just 6.7 cents in salary and bonus over two years.

A $1,000 change in corporate value corresponded to a change in CEO compensation of just $2.59. Accounting for all monetary sources of CEO

incentives—salary and bonus, stock options, shares owned, and the changing likelihood of dismissal

13

Changing Attitudes and Perceptions About Risk

In this regard, the value of shares owned by the median CEO changed by 66 cents for every $1,000 increase in corporate value.

At the median, stock options added another 58 cents worth of incentives.

14

Stock Options

There is some evidence that firms offering stock options to their employees perform better.

Options lead to increased firm value, principally because they aid in employee retention, and serve as a substitute for cash compensation in cash-strapped firms.

Less clear is whether stock options serve to align the incentives of executives and employees with those of shareholders.

15

Controversy

Warren Buffet has been a longtime critic of the manner in which firms use stock options.

He suggests that although options can be appropriate in theory, in practice their use has been capricious, inefficient as motivators, and very expensive for shareholders.

The manner in which options are recorded in financial statements has been a long running subject of debate, whether as footnotes or expensed.

16

Shareholder Rights

Provisions that move away from one share one vote and put anti-takeover provisions in place contribute to weak shareholder rights.

The evidence indicates that firms with stronger shareholder rights are associated with

higher firm value higher profits higher sales growth lower capital expenditures, and fewer corporate acquisitions

17

Overconfidence Among Directors and Executives

Overconfident directors underestimate the extent of both traditional agency conflicts, and behavioral biases on the part of executives.

Overconfident directors are inclined to think that they do a better job of addressing agency conflicts than they actually do.

Overconfident directors are prone to approve compensation that feature insufficient pay for performance, and overpayment.

18

Quotes from Fortune

Compensation committee members are not malevolent.

I've seen situations that are f---d up, and yet the directors think they’re doing a hell of a job.

They delude themselves. They think things are being done right and

fairly--they don’t think they’re being had--when actually the excesses they’re approving are just mind-boggling…

19

It’s really “amateurs vs. pros.” I’m classing the directors, in most cases,

as amateurs, and management, together with the compensation consultants they hire, as pros.

You can have a very sophisticated board--and it’ll still be amateurs vs. pros…

20

Insufficient Pay for Performance

So my view of incentive comp of any kind is that it’s fine if it isn’t just a giveaway program.

The pendulum has to swing both ways--and usually it doesn’t.

A comp committee also hears a lot about external factors, things that couldn’t have been anticipated when the budget was being made.

People say, “We worked our butts off”--da-da-da-da. And you have to answer, “Look, that was the deal.

21

You agreed to work here for a year under that deal, and if the shareholders get dung, then you get dung.”

CEOs will claim it’s all deserved, saying, “Look at the way I made my stock go up.”

That’s bunk in a lot of cases, egregiously so at companies that don’t pay dividends.

22

Let me refer you to a Treasury zero bond:

If you buy one today and hold on for ten years, it will rise by 74%.

And you won’t even have had to give President Bush an option on the bond.

23

Better Than Average Effect

How in the world do you stop that when every self-respecting compensation committee--I just read this once again today in a proxy--says,

“We want our CEO’s compensation to be between the 50th and 75th percentile in our peer group.”

If everybody does that, it’s Lake Wobegon, where every kid is above average.

24

Stock Options

There are two important behavioral phenomena associated with stock options being used to compensate employees, especially executives.

1. Excessively optimistic, overconfident employees overvalue the stock options they are granted.

2. “Casino effect.”

25

Casino Effect

They say, “You can fiddle with my bonus, but don’t cut out my options”--because they know there’s the big casino waiting out there.

26

Concept Preview Question 8.1

Indicate which of the following two risky alternatives you would prefer to choose, A or B. (You can also indicate indifference, if you wish).

A: winning $2,000 with a 90% probability winning $0 with a 10% probability.

B: winning $4,000 with a 45% probability winning $0 with a 55% probability.

27

Next, imagine that you are registering to participate in a lottery, where the probability of winning is 0.002 (actually 2/900).

If you win the lottery, your prize is a choice to play yet another lottery, where you will face either alternative A or alternative B above.

You need to commit, in advance, whether you would prefer to play alternative A or alternative B, should you win the opportunity to do so.

28

Concept Preview Question 8.2

Of the two alternatives below, please indicate which one you find preferable, alternative C, alternative D or indifference between C and D.

C: winning $2,000 with probability .002 winning $0 with probability .998

D: winning $4,000 with probability .001 winning $0 with probability .999

29

Reframing

Concept preview question 8.2 is a reframing of the second part of the concept preview question 8.1.

To see why, just multiply the probability of winning the lottery (2/900) by the probability of winning $2,000 in A (0.9), to obtain 0.002 = 2/900 x 0.9.

30

The Point

The point is that when people focus directly on the low probabilities, they act as if they overweight lower probabilities relative to higher probabilities.

In choosing alternative D over alternative C, they act as if they are risk seeking rather than risk averse.

However, in concept preview question 8.1, where they focus on probabilities that are much higher, they act as if they are risk averse.

31

AuditingAgency Conflicts

Managers, as agents, release financial statements in order to report the financial results of their firms to the owners.

How do the principals monitor managers?

The conventional way is to hire the services of a professional auditor.

32

Traditional Perspective

Auditors are vulnerable to being “bribed” by unscrupulous firms in order to issue clean opinions.

Notably, auditing firms are partnerships, not corporations.

The traditional view holds that auditing firms have reputations to protect, reputations for integrity.

33

Signaling

A firm that seeks to communicate that its financial statements are clean might engage the services of an auditor with a high reputation who also charges high fees.

Signaling theory stipulates that firms who face accounting problems would not use such an auditor.

Therefore the choice of auditor in and of itself sends a strong signal to investors.

34

Images from Arthur Andersen

After Enron’s difficulties became public, Andersen employees tampered with documents.

On June 14, 2002, the firm was found guilty of obstructing justice, and was subsequently dissolved.

35

What Happened?

Consulting division had become much more profitable than the auditing division.

In 1989, the consultants managed to alter the profit-sharing rule, in their favor.

The change in sharing rule left the auditors lagging behind those of attorneys, investment bankers, and especially consultants.

36

2X

In 1997, the partners at Andersen Consulting voted to split off completely from Arthur Andersen to become Accenture.

In the wake of their departure Arthur Andersen instituted a policy known as “2X.”

Under 2X, for every dollar of auditing work, partners were required to bring in twice the revenue in non-auditing work.

37

Scandals

One of Andersen’s initiatives was to encourage clients to engage Andersen for both internal and external auditing services.

Among the list of Arthur Andersen’s audit clients were: Boston Chicken, Sunbeam, Waste Management Inc., WorldCom, and Enron.

At each of these firms, a major scandal ensued.

38

Reference Point Issues?

Did 2X shift Andersen’s auditors from perceiving themselves to be in the domain of gains to perceiving themselves to be in the domain of losses?

Does attitude towards risk depend upon whether a person perceives him- or herself to be in the domain of losses as opposed to the domain of gains?

39

Conflicts of Interest

Arthur Andersen decided to take on the roles of both internal and external auditor.

Arthur Levitt chaired the Securities and Exchange Commission (SEC) raised concerns that practices of this sort would jeopardize the quality of audits.

potential conflict of interest

40

Sarbanes-Oxley

Since 2000, a succession of corporate scandals with varying degrees of fraud made clear that compensation in the form of stock and stock options could not be counted upon to align the interests of investors and managers.

Among the firms involved in fraudulent activities were Coca-Cola, IBM, Sunbeam, Cendant, Xerox, Lernout & Hauspie, Parmalat, Enron, WorldCom and Healthsouth.

41

Certification

In the wake of these financial scandals, Congress passed the Sarbanes-Oxley Act of 2002.

SEC requires that the CEO and CFO of every publicly traded firm certify, under oath, the veracity of their firm’s financial statements.

42

SOX and the Board

Sarbanes-Oxley increased the number of independent directors on corporate boards.

Independent directors neither work for nor do business with a corporation or its executives.

Board audit committees are required to include at least one financial expert.

Every quarter, after the CEO and CFO have certified the firm’s financial statements, the full panel must review those statements.

43

Section 404 of SOX

Each annual report must contain 1. Statement of management's responsibility for

establishing and maintaining adequate internal control structure and procedures for financial reporting

2. management's assessment of the effectiveness of the company's internal control structure and procedures for financial reporting

3. company's auditor to attest to management's assessment in accordance with Public Company Accounting Oversight Board

44

Fraud and Options

Excessive optimism and overconfidence already counteract managers’ undue caution.

Granting of stock options might serve to induce managers to accept risky projects that feature negative net present value.

45

Amplification

Moreover, excessively optimistic, overconfident managers who are unethical will be prone to underestimate the chances that fraudulent behavior on their parts will be discovered.

Indeed, stock and stock option compensation can actually amplify agency conflicts when managers find they can manipulate the market value of their firms.

46

Images from HealthSouth

47

HealthSouth

HealthSouth was founded in 1984. At year-end 2001, HealthSouth was the

largest U.S. provider of outpatient surgery, diagnostic imaging and rehabilitation services.

In 2002 HealthSouth was investigated for an accounting fraud that prosecutors suspect began as early as 1986.

48

Overstated Income and Insider Trading

Between 1999 and the second quarter of 2002, HealthSouth overstated its income by $1.4 billion.

The SEC accused HealthSouth executives of having engaged in insider trading by selling substantial amounts of HealthSouth stock while they knew that the firm’s financial statements grossly misstated its earnings and assets.

As part of their compensation, HealthSouth’s executives received options on 3.6 million shares of HealthSouth stock.

49

Richard Scrushy

HealthSouth’s founder and CEO was Richard Scrushy.

Specifically, the SEC alleged that Scrushy induced HealthSouth executives to manipulate the firm’s stock price until he could sell off large blocks of stock worth $25 million.

The SEC claimed that since 1991 Scrushy sold “at least 13.8 million shares for proceeds in excess of $170 million.”

50

Ernst & Young

HealthSouth’s auditor was a top tier accounting firm, E&Y.

HealthSouth appears to have engaged in numerous practices that were intended to deceive their auditors.

In 2001 HealthSouth paid Ernst & Young $1.16 million in auditing fees.

It also paid an additional $2.39 million in “audit-related fees” for what HealthSouth called “pristine audits.”

51

Stock Price Driven by Financials

Exhibit 8-1

HealthSouth vs. S&P 500 Cumulative Returns Sept 1986 - Dec 2002

0

5

10

15

20

25

30

Date

S&P 500

HealthSouth

HealthSouth Return on Equity 1986 - 2001

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

1986 1988 1990 1992 1994 1996 1998 2000

Date

52

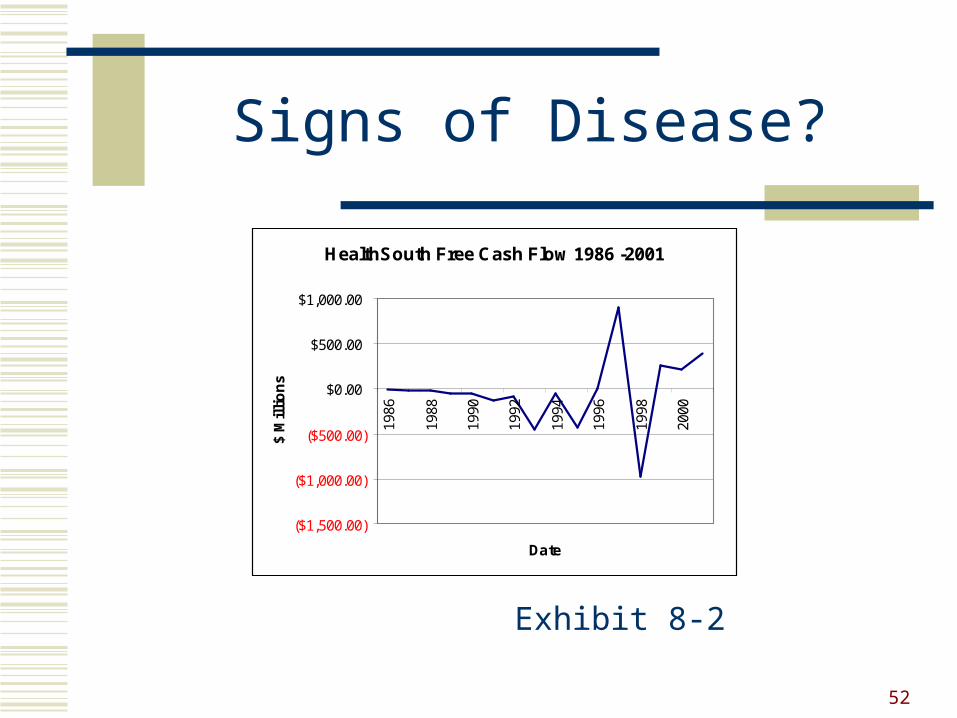

Signs of Disease?

Exhibit 8-2

HealthSouth Free Cash Flow 1986 -2001

($1,500.00)

($1,000.00)

($500.00)

$0.00

$500.00

$1,000.00

1986

1988

1990

1992

1994

1996

1998

2000

Date

$ M

illi

on

s

53

Borrowing

Much of HealthSouth’s negative free cash flow in exhibit 8-2 stems from continued borrowing.

High leverage does not necessarily force fraudulent firms to fail in short order.

Only on April 1, 2003 did the firm announce that it would default on a $350 million bond payment and was dismissing its CEO Richard Scrushy.

54

Scrushy on CFO's Concerns About Phony Financial Statements

When they get you is when you go into bankruptcy. That’s when they come in on you. They don’t come in on a company that’s paying their bank debt down. They don’t come in on a company that’s doing good. They come in on a company that’s screwed up. And we’re, we’re seeing a healthy day right now in stock. We’re seeing that. I just hate to go down there and just give the keys to them.

55

Debiasing for Better Decisions

Errors or biases: Managers behave unethically. Why does it happen? High ambitions coupled with aversion to a sure loss. How does it happen? High reference points. What can be done about it? Reset reference point, or make use of an explicit rule that mandates that losses be recognized beyond a prespecified level. Also, remember that most people do not beat the

odds.

56

Summary

In practice, executive compensation displays too little variability in respect to pay for performance, insufficient dismissal, and excessive payment for executives.

Directors have been overconfident in their ability to structure incentives appropriately without overpaying executives.

Directors' tasks are made more difficult by overconfidence on the part of executives.

57

In traditional theory, employee stock options are used to align the risk attitudes of managers and shareholders.

Managers who behave in accordance with prospect theory might find the risk characteristics of stock options attractive because of its casino effect.

Stock options might also induce risk seeking behavior because of the tendency to overweight low probabilities.

58

The combination of aversion to a sure loss and overconfidence can also induce ambitious, unethical managers to manipulate accounting information in order to exercise their stock options when the stock was overpriced.

In this respect, a combination of behavioral phenomena and agency conflicts affected some accounting firms.

Those events were the catalyst for the passage of the Sarbanes-Oxley Act.