AUTOMATIC ENROLMENT WHAT ARE THE RULES? WHAT DOES IT MEAN FOR EMPLOYERS? ROBERT COCHRAN 13 TH MAY 2014 The slides are authorised for use by accredited Scottish Widows staff in corporate pensions presentations to employers, trustees and UK financial advisers and should not be distributed to or relied upon by any other person.

Transcript

AUTOMATIC ENROLMENT

WHAT ARE THE RULES?

WHAT DOES IT MEAN FOR EMPLOYERS?

ROBERT COCHRAN

13TH MAY 2014

The slides are authorised for use by accredited Scottish Widows staff in corporate pensions presentations to employers, trustees and UK financial advisers and should not be distributed to or relied upon by any other person.

AGENDA

• HOW BIG A CHANGE IS AUTOMATIC ENROLMENT?

• WHAT ARE THE RULES?

• IMPACT ON EMPLOYERS

• Q&A

2

RULES

HOW BIG A CHANGE

3

A tidal wave of schemes and

new members is set to hit the UK

pensions providers.

Corporate Adviser, September 2013

CAPACITY PRESSURE FOR ALL

4

• 1.35 million employers

• 21,000 advisers

• How many schemes per adviser?

• 64

• How many schemes have been written in the last 20 years?

EMAIL EXTRACT (RECIEVED AUGUST 2013) – STRUGGLING WITH DATA ISSUES

• I’ve opted for Plan B. We’re asking all employees to come to the NEC in Birmingham tomorrow.

• We’ll then do a hands up as to whose in a pension plan, they can then go. Who’s 21 or under, or over state

pension age, they’re on the bus out immediately.

• Next out are those earning less than £787.

• With the remainder, we’ll ask them who they are, where they live, what their NINO is, email address, and so on.

They’ll then be auto enrolled and will be free to leave.

• This will be called the Thomson Pettigrew auto enrolment method, similar in its eventual complexity to the

Duckworth Lewis method for determining who’s won in a game of cricket shortened by rain.

• Seriously though, I’m sat with an envelope and pen, and would appreciate a little help. Can you call me when

you’re free, please?

CONTRIBUTIONS – PHASING IN

8

BASED ON QUALIFYING BAND EARNINGS

SIMPLIFIED CERTIFICATIONS OPTIONS

9

EMPLOYER MINIMUM MINIMUM TOTAL

Full basic salary (pensionable pay) 4% 9%

Full basic salary, and at least 85% of total pay is pensionable

3% 8%

Total earnings (P60) 3% 7%

QUALIFYING EARNINGS DEFINITION (2014/15) – P60 INCOME FROM £5,772 TO £41,685

OPTING OUT

10

Every 3 years

OPTING OUTEngage your

workforce

REVIEWEngage your

workforce

1 monthwindow

Opt outnotice

Fill innotice

Refundworker

Inform

provider

Refund

employer

1 monthwindow

Opt outnotice Fill in

notice

Refundworker

Inform

provider

Refund

employer

Default ‘re-enrolment date’ is 3rd anniversary of employer staging date.

ADDITIONAL REQUIREMENTS

11

ALL EMPLOYERS WILL HAVE ADDITIONAL REGULATORY REQUIREMENTS

• Employers prohibited from incentivising opt outs.

• Register with TPR to show they are meeting their duties.

• Payments will be monitored by administrators orscheme trustees who need to report failures.

• Must keep records for six years.

• Must retain opt in and opt out notices for four years

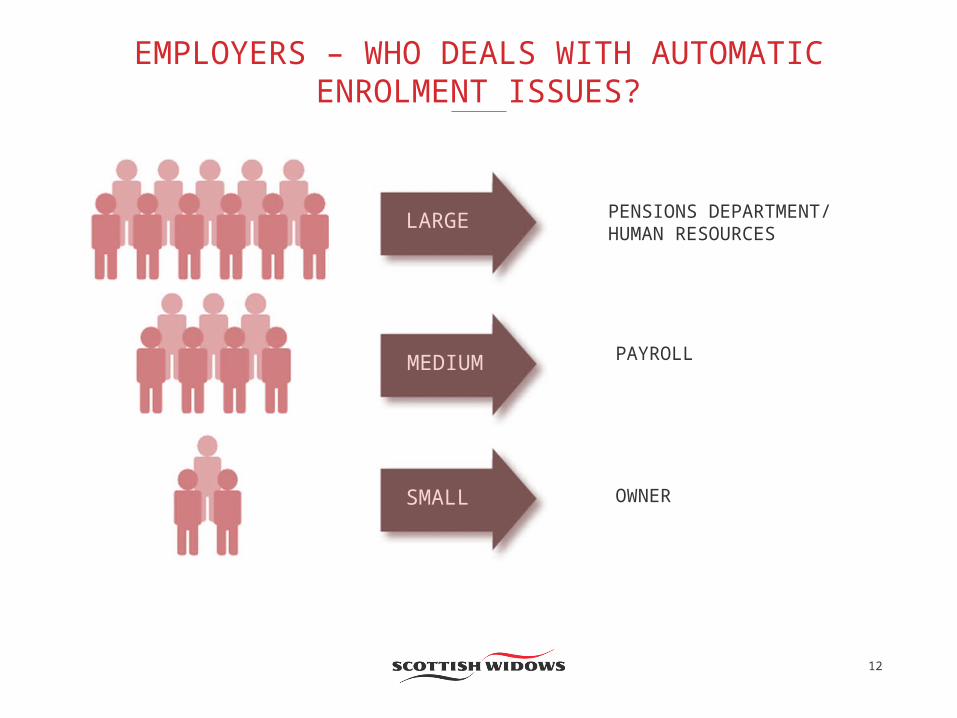

CHECKLIST

EMPLOYERS – WHO DEALS WITH AUTOMATIC ENROLMENT ISSUES?

12

LARGE

MEDIUM

SMALL

PENSIONS DEPARTMENT/HUMAN RESOURCES

PAYROLL

OWNER

EMPLOYERS NEED TO BE THINKING ACROSS THREE AREAS

13

HR, Payroll & Finance

Change to Systems/Processes

Hard cost of contributions

Compliance and registering

Administration• Set up & Day 1 costs• Ongoing costs

• Eligible employee• Non eligible employees

• Avoiding risk and failure • Governance Framework

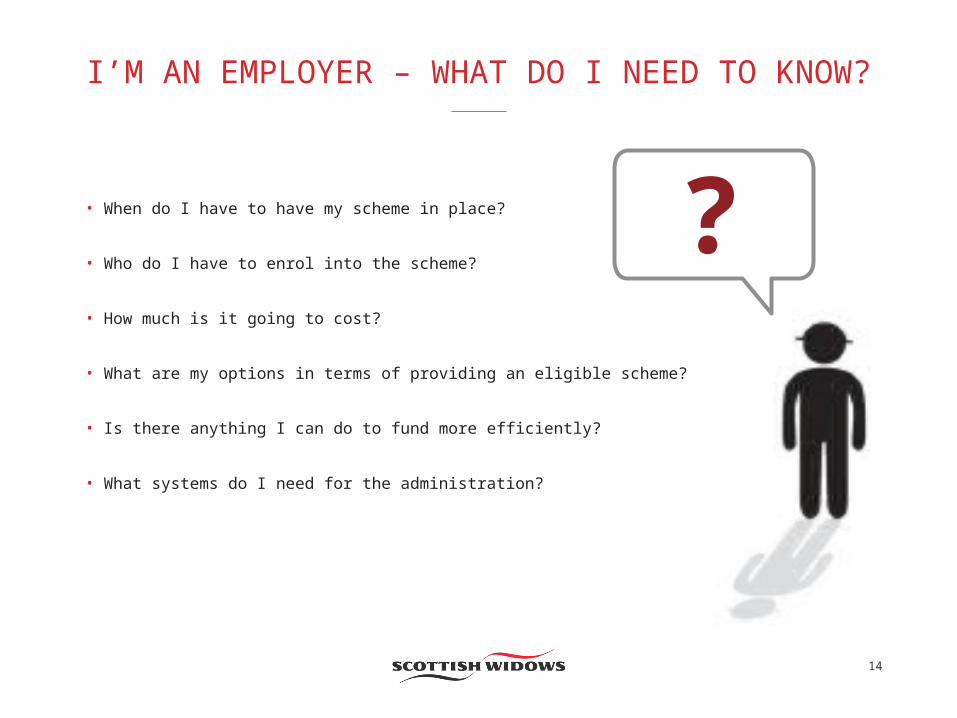

I’M AN EMPLOYER – WHAT DO I NEED TO KNOW?

14

• When do I have to have my scheme in place?

• Who do I have to enrol into the scheme?

• How much is it going to cost?

• What are my options in terms of providing an eligible scheme?

• Is there anything I can do to fund more efficiently?

• What systems do I need for the administration?

?

WHEN DO I HAVE TO HAVE MY SCHEME IN PLACE?

15

EMPLOYER SIZE AUTOMATIC ENROLMENT STAGING DATE

120,000 1 October 2012

50,000-119,999 1 November 2012

30,000-49,999 1 January 2013

20,000-29,999 1 February 2013

10,000-19,999 1 March 2013

6,000-9,999 1 April 2013

4,100-5,999 1 May 2013

4,000-4,099 1 June 2013

3,000-3,999 1 July 2013

2,000-2,999 1 August 2013

1,250-1,999 1 September 2013

800-1,249 1 October 2013

500-799 1 November 2013

350-499 1 January 2014

250-349 1 February 2014

50-249 1 April 2014 to 1 April 2015

Test tranche <30 employees 1 April 2015 to 30 June 2015*

30-49 employees 1 August 2015 to October 2015

Less than 30 employees 1 January 2016 to 1 April 2017

New employers 1 May 2017 to February 2018

The rules for staging within each size grouping have still to be confirmed

EMPLOYER STAGING DATES

* Please note that there are nine staging dates within this period, depending on the employer’s size. For further information, please visit The Pension Regulator website.

WHO DO I HAVE TO ENROL AND HOW MUCH WILL IT COST?

16

EMPLOYER REPORT

17

• Staging date calculation.

• Employer timeline.

• Check certification of existing scheme.

• Workforce assessment.

• Employer cashflow modeling.

WHAT ARE MY OPTIONS FOR PROVIDING AN ELIGIBLE SCHEME?

18

• Defined Benefit occupational trust based.

• Defined Contribution occupational trust based.

• Group Personal Pension.

• Group Stakeholder.

• Multi Employer Trust.

• People’s Pension.

• Now: Pensions.

• Nest.

Samecontributiontest.

IS THERE ANYTHING I CAN DO TO FUND THIS MORE EFFICIENTLY?

19

Source: Corporate Adviser, September 2010.

WHY SALARY EXCHANGE?

20

POTENTIAL INCREASED

CONTRIBUTION OVER NORMAL

NET PAY METHOD

POTENTIAL INCREASED

CONTRIBUTION OVER NORMAL

NET PAY METHOD

EARNINGS £30,000 EARNINGS £50,000

33.9% 17.7%

*Assumes net take home pay remains the same, employer 100% NI reinvested.

ONLINE AUTOMATIC ENROLMENT SOLUTION – AN INTEGRATED APPROACH

22

Employerpayroll file

*Best Group Pension Provider Award, Corporate Adviser 2013.

PAYROLL PROVIDERS OR THIRD PARTY SOLUTIONS - WHAT CAN THEY DO?

23

EverythingEverything

PartialPartial

Assessment & ContributionsCommunications

Opt-outs

Assessment Contribution Calculations

Collect Contributions

No AssistMeBack office linkNo AssistMe

Back office link

NothingNothing

1 Pass AssistMe1 Pass AssistMe

2 Pass AssistMe2 Pass AssistMe

ADEQUACY

24

MEDIAN INCOME EARNER…..SAVING FOR 40 YEARS.

30% 45%

60-66%1

Automatic Enrolment Additional Savings

state pension state pension & auto enrolment

target income replacement rate

Source: Making Automatic Enrolment work – Oct 2010

1A New Pension Settlement for the 21st century, second report, Pensions Commission, Nov 2005, Govt target by 2053

IMPACT

25

PENSIONS REPLACEMENT AMOUNT THROUGH AUTO ENROLMENT – 30 YEAR OLD SAVER

ALL 68%

ALL 44%

ALL 28%

£15,000 Salary

£30,000 Salary

£90,000 Salary

Source: Scottish Widows Replacement Calculator

RETIREMENT EXPECTATIONS

26

Source: Scottish Widows UK Pensions Report, June 2013Ninth Annual Pensions Report, Retirement savings across the nation.

WHAT CAN YOU EXPECT FROM YOUR PENSION PROVIDER?

27

What providers can do to help you make automatic enrolment a success.

• Benefit of experience.

• Technology to meet your needs.

• Robust communications.

• Education and employee engagement.

DISCLAIMER

28

This presentation represents Scottish Widows’ interpretation of current and proposed legislation and HM

Revenue & Customs practice as at the date of publication – these may change in future.

This material is for use by UK Financial Advisers only. It is not intended for onward transmission to private

customers and should not be relied upon by any other person.

Scottish Widows plc. Registered in Scotland No. 199549. Registered Office in the United Kingdom at 69 Morrison Street, Edinburgh EH3 8YF. Telephone: 0131 655 6000.Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register number 191517.