25

Aggregate Supply Module 18

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | sophie-holt |

| View: | 219 times |

| Download: | 0 times |

Aggregate Supply

Module 18

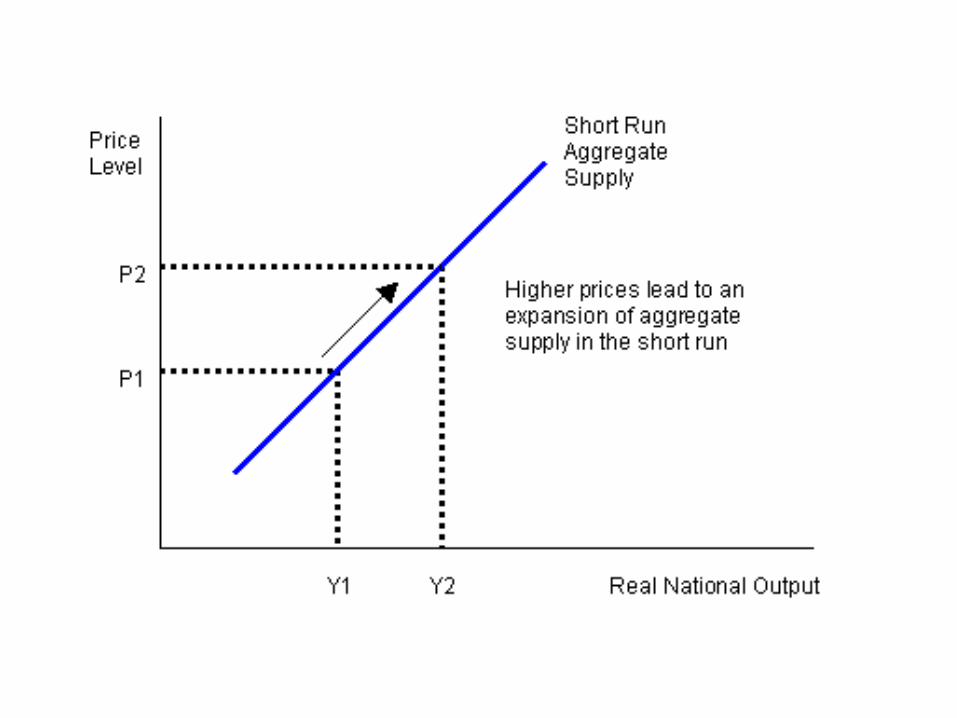

Short-Run Aggregate Supply(SRAS)

• Upward sloping, just as in market case– But again for different reasons

• Profits = Price of Outputs – Price of Inputs– Revenue generated by price increases outpaces

increases in input costs (wages are “sticky”)– So, in the short-run curve slopes upwards

• Reverse is also true

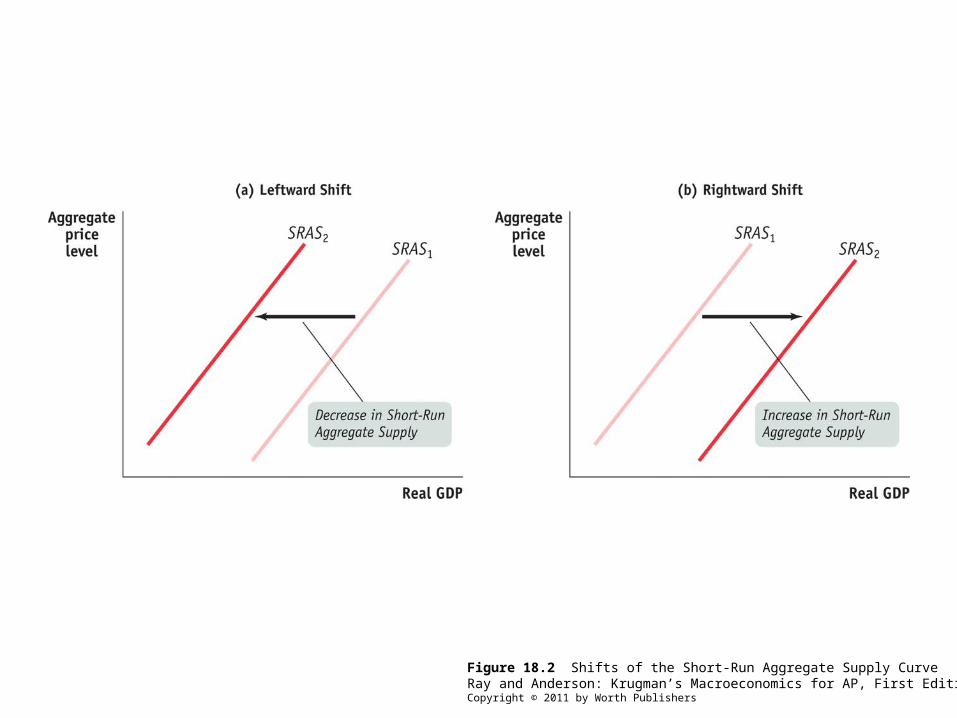

Changes in SRAS1. Changes in commodity prices

– Oil; steel– Decrease in commodity prices = increase in SRAS

2. Changes in nominal wages– Increase in nominal wages = decrease in SRAS

3. Change in productivity– Increases in productivity = increase in SRAS

Figure 18.2 Shifts of the Short-Run Aggregate Supply CurveRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

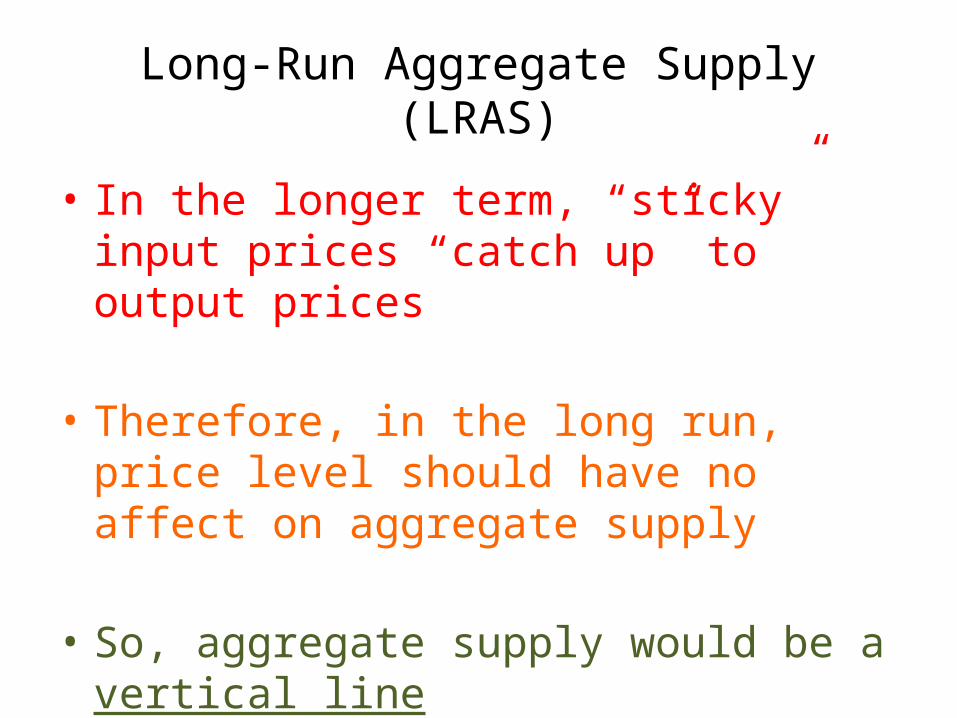

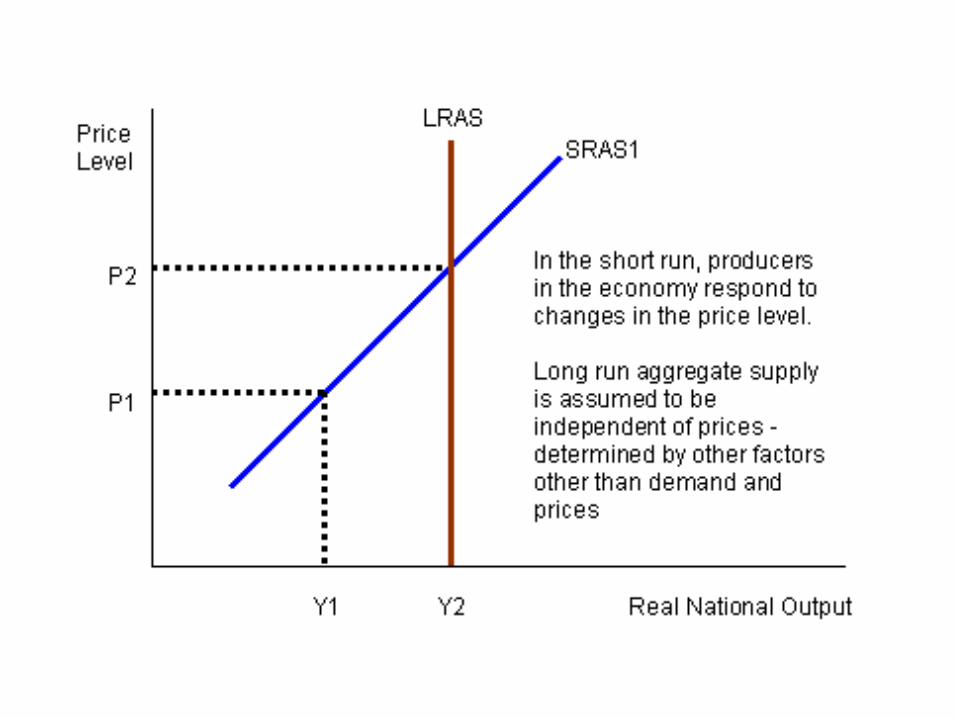

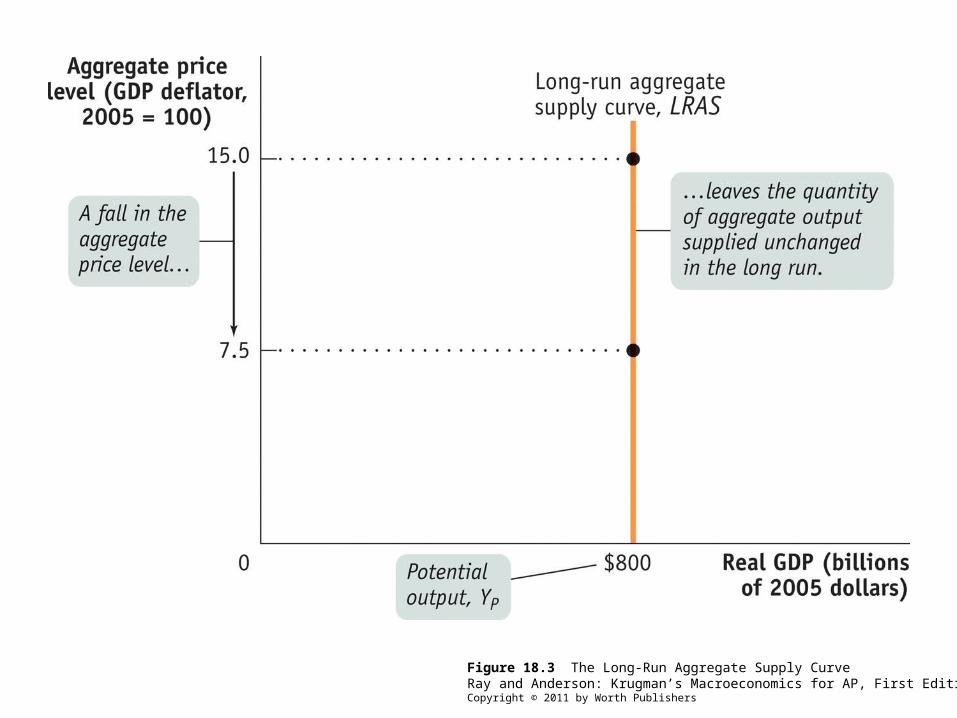

Long-Run Aggregate Supply(LRAS)

• In the longer term, “sticky” input prices “catch up” to output prices

• Therefore, in the long run, price level should have no affect on aggregate supply

• So, aggregate supply would be a vertical line

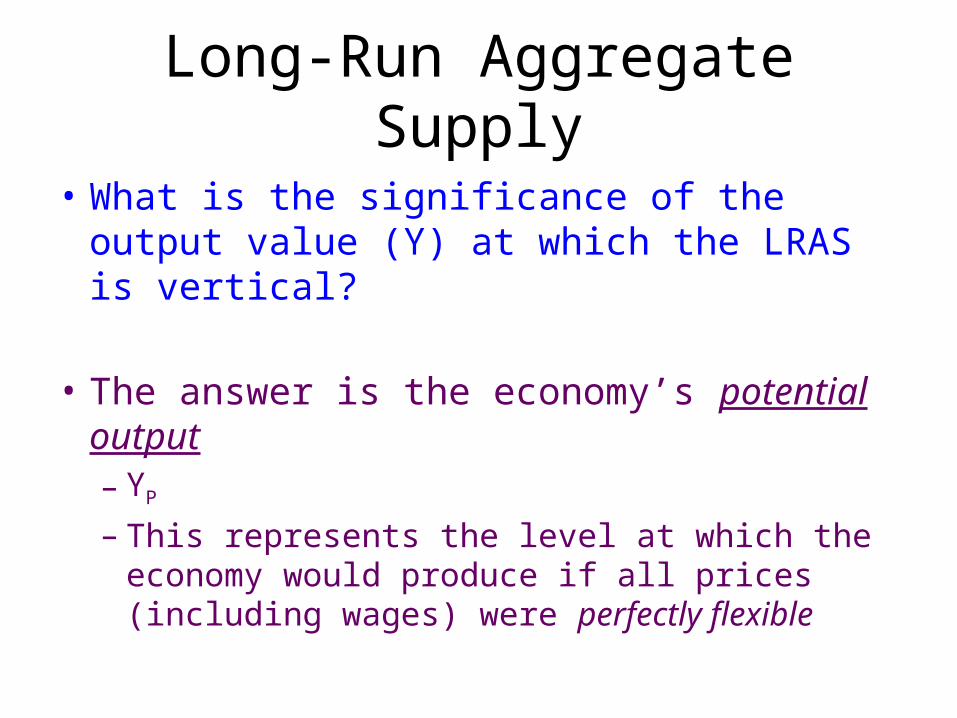

Long-Run Aggregate Supply

• What is the significance of the output value (Y) at which the LRAS is vertical?

• The answer is the economy’s potential output– YP

– This represents the level at which the economy would produce if all prices (including wages) were perfectly flexible

Figure 18.3 The Long-Run Aggregate Supply CurveRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

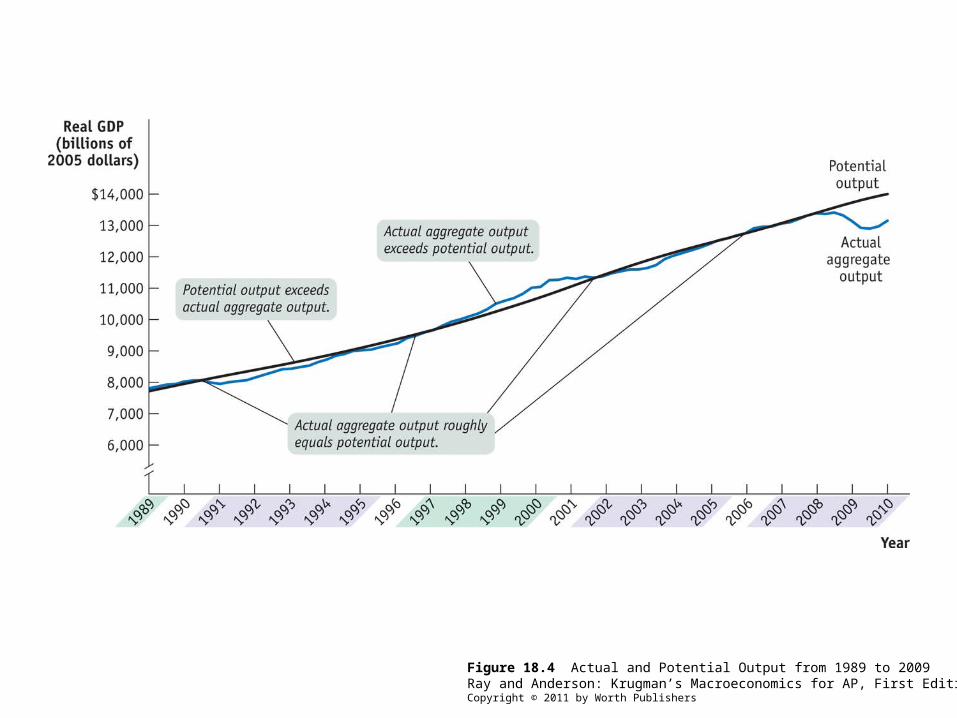

Figure 18.4 Actual and Potential Output from 1989 to 2009Ray and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

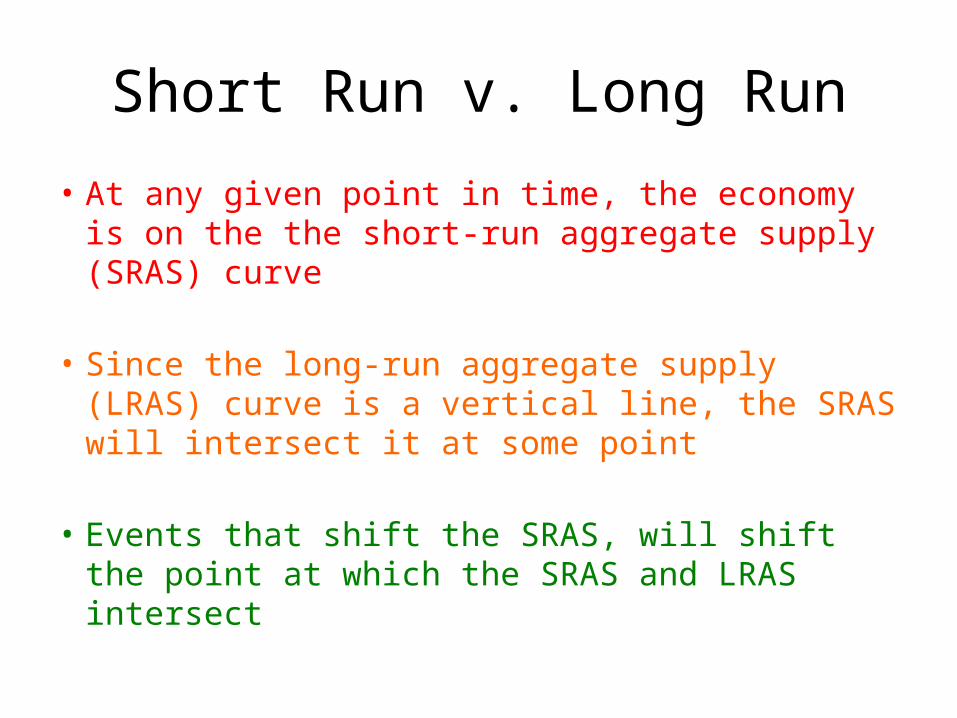

Short Run v. Long Run

• At any given point in time, the economy is on the the short-run aggregate supply (SRAS) curve

• Since the long-run aggregate supply (LRAS) curve is a vertical line, the SRAS will intersect it at some point

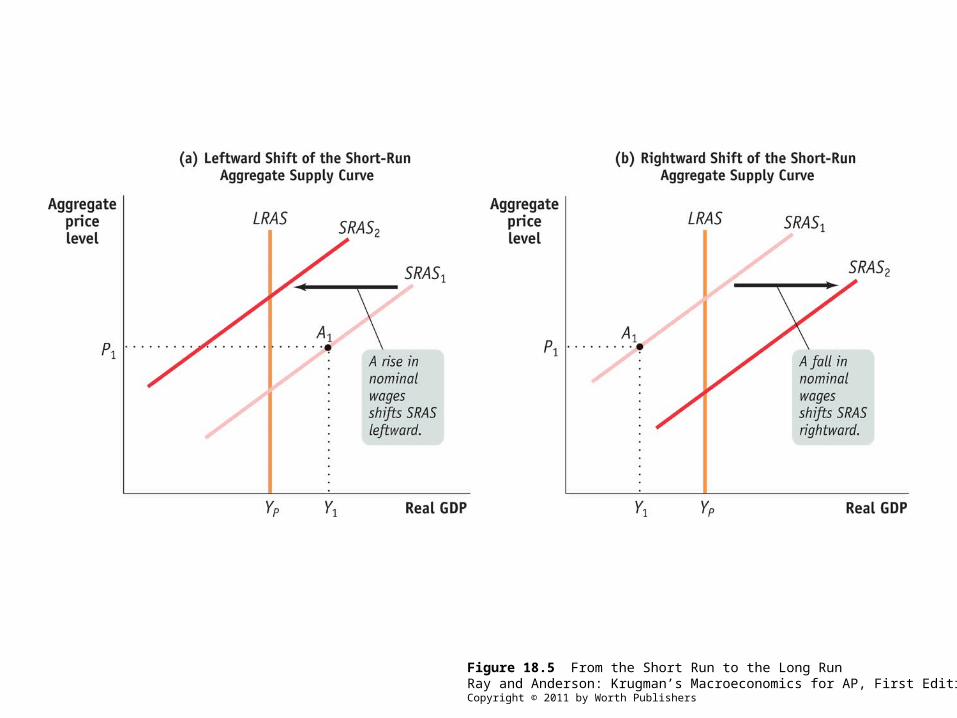

• Events that shift the SRAS, will shift the point at which the SRAS and LRAS intersect

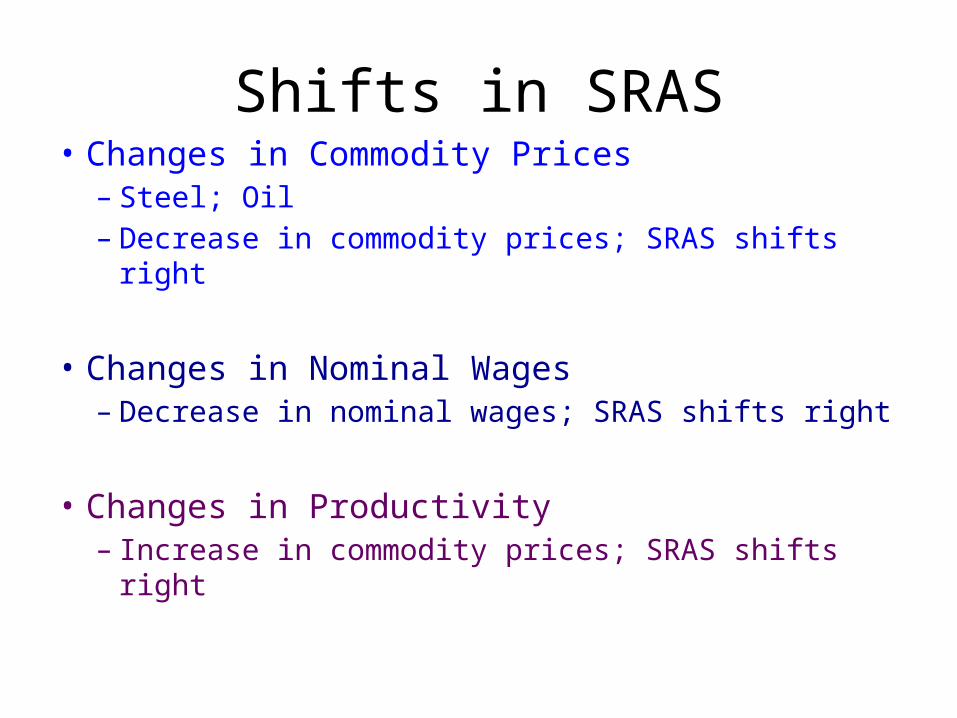

Shifts in SRAS• Changes in Commodity Prices

– Steel; Oil– Decrease in commodity prices; SRAS shifts right

• Changes in Nominal Wages– Decrease in nominal wages; SRAS shifts right

• Changes in Productivity– Increase in commodity prices; SRAS shifts right

Figure 18.5 From the Short Run to the Long RunRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

Macroeconomic EquilibriumThe AD-AS Model

Module 18

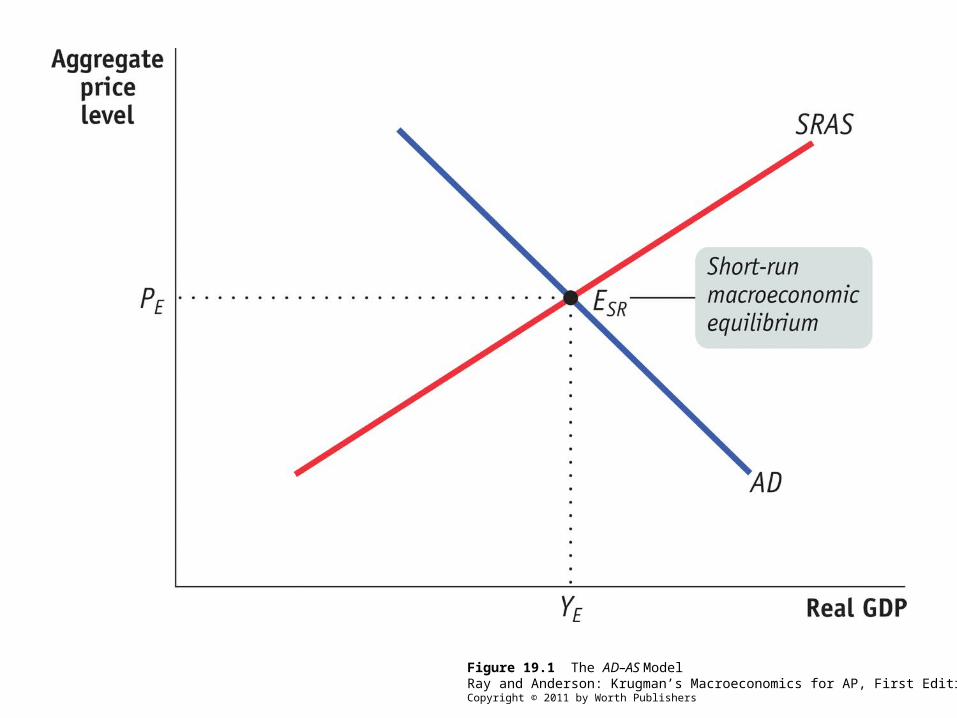

Figure 19.1 The AD–AS ModelRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

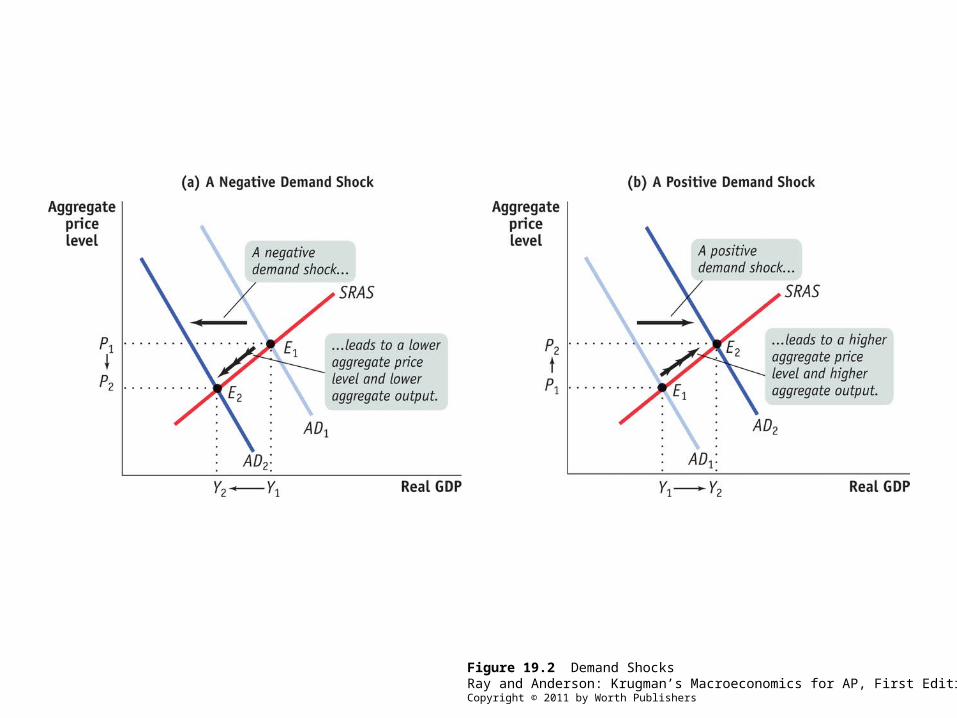

Demand Shocks

• Expectations

• Wealth

• Stock of productive capital

Figure 19.2 Demand ShocksRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

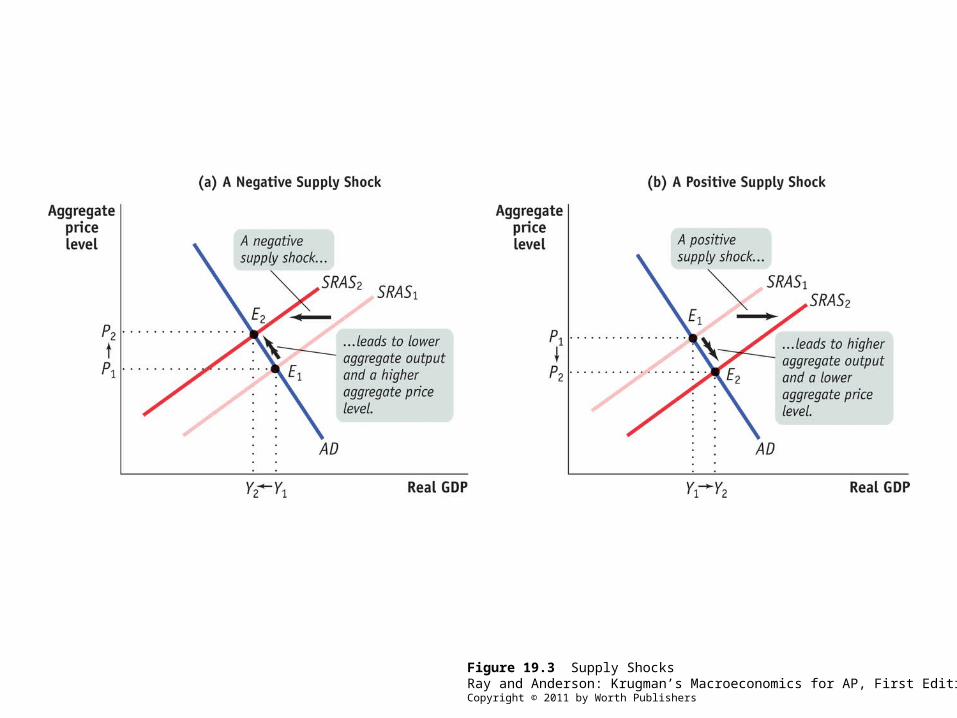

Supply Shocks

• Commodity prices

• Nominal wages

• Productivity

Figure 19.3 Supply ShocksRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

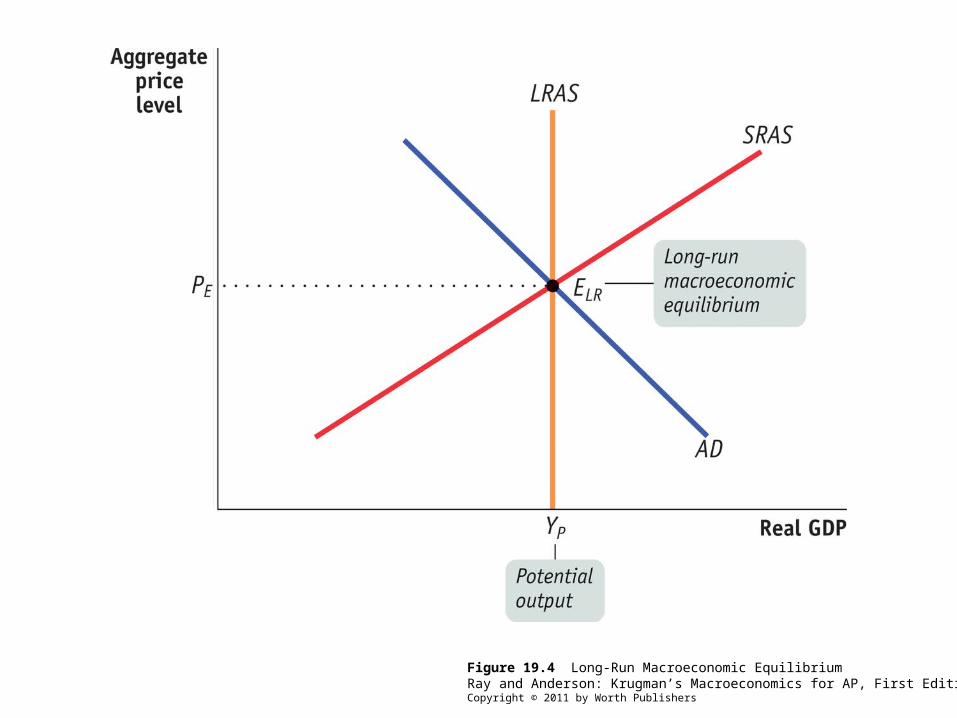

Figure 19.4 Long-Run Macroeconomic EquilibriumRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

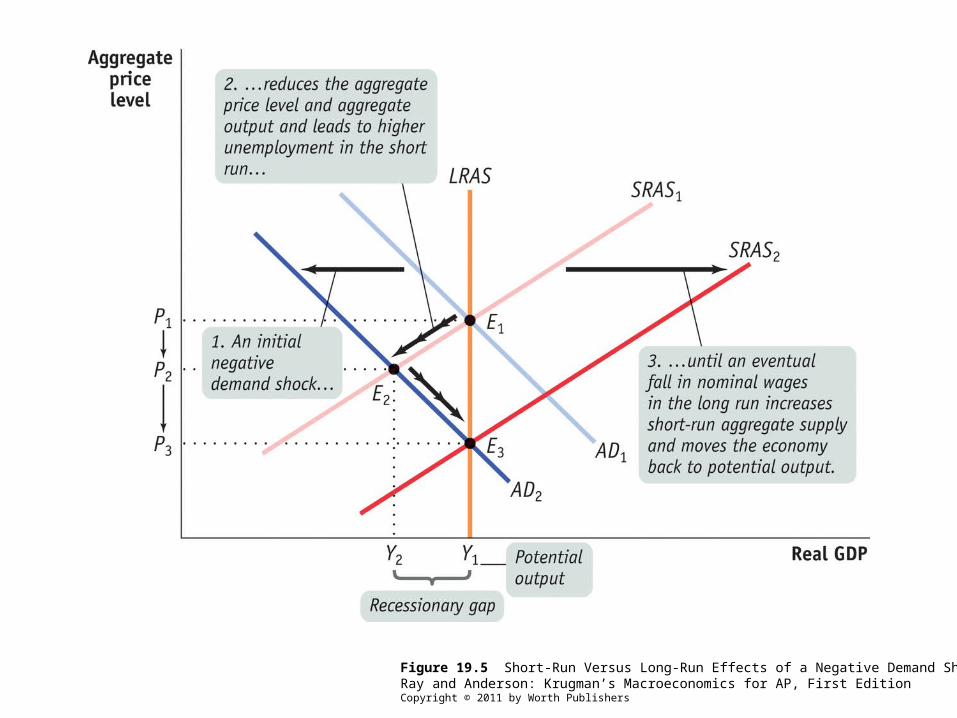

Figure 19.5 Short-Run Versus Long-Run Effects of a Negative Demand ShockRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

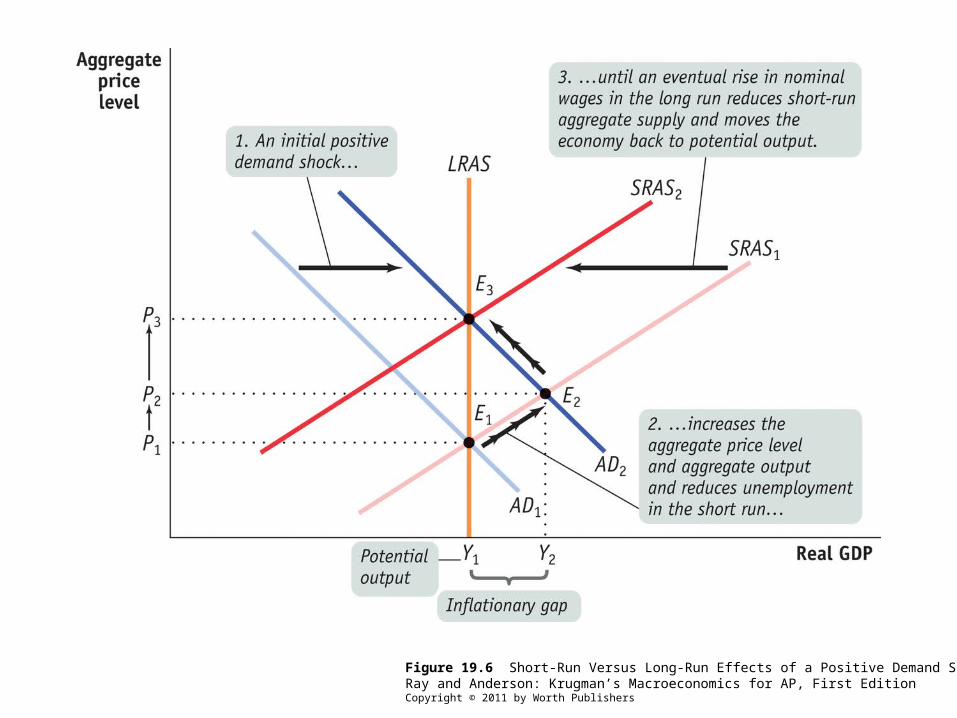

Figure 19.6 Short-Run Versus Long-Run Effects of a Positive Demand ShockRay and Anderson: Krugman’s Macroeconomics for AP, First EditionCopyright © 2011 by Worth Publishers

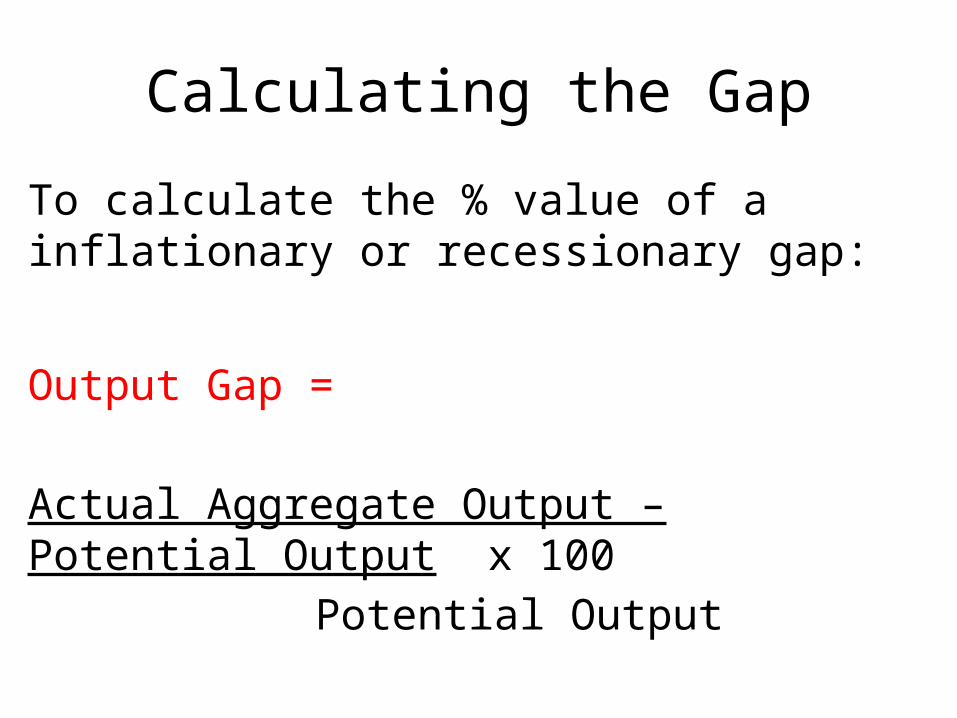

Calculating the Gap

To calculate the % value of a inflationary or recessionary gap:

Output Gap =

Actual Aggregate Output – Potential Output x 100Potential Output

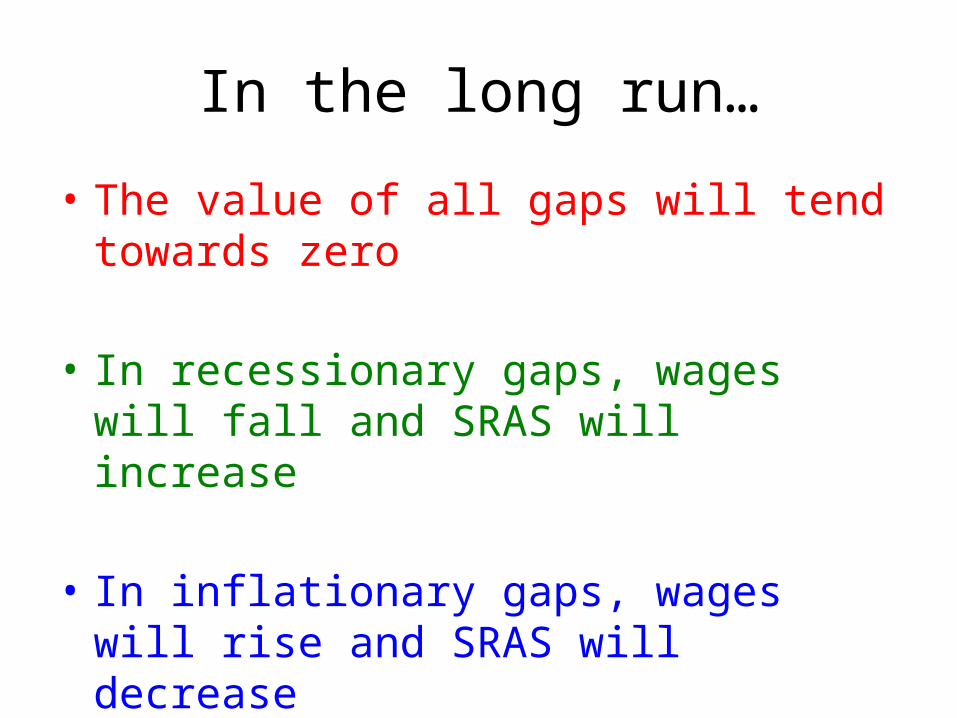

In the long run…

• The value of all gaps will tend towards zero

• In recessionary gaps, wages will fall and SRAS will increase

• In inflationary gaps, wages will rise and SRAS will decrease

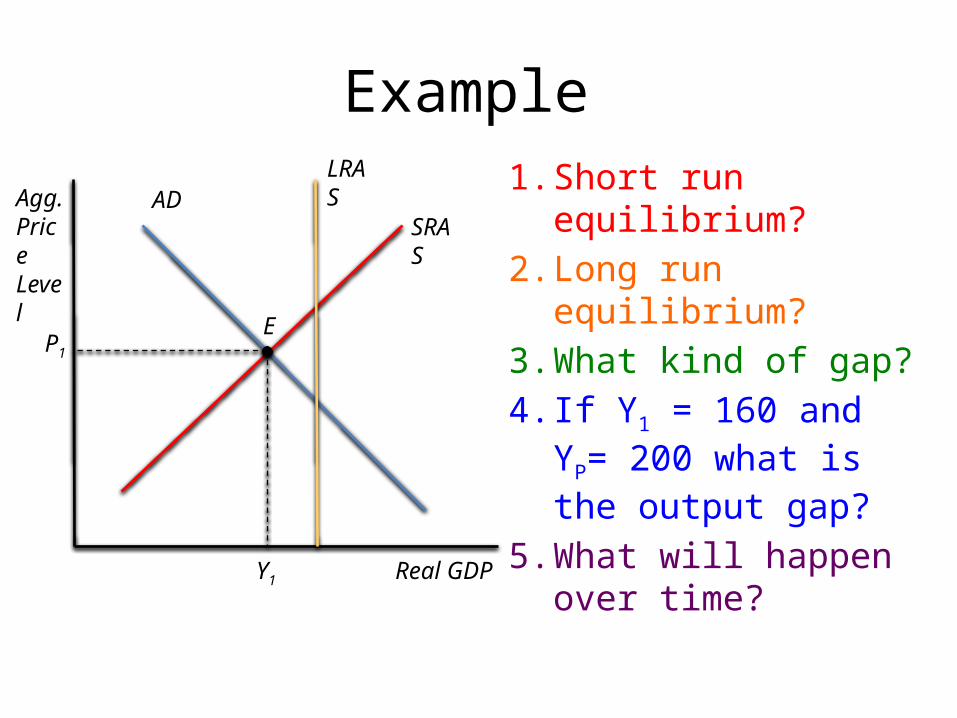

Example1. Short run equilibrium?2. Long run equilibrium?3. What kind of gap?4. If Y1 = 160 and YP= 200

what is the output gap?

5. What will happen over time?

LRAS

SRASAD

Real GDP

Agg.PriceLevel

EP1

Y1